Efficient algorithm to select tuning parameters in sparse regression modeling with regularization

Kei Hirose1, Shohei Tateishi2 and Sadanori Konishi3

1 Division of Mathematical Science, Graduate School of Engineering Science, Osaka University,

1-3, Machikaneyama-cho, Toyonaka, Osaka, 560-8531, Japan

2 Toyama Chemical Co., Ltd., 3-2-5, Nishi-Shinjuku, Shinjuku-ku, Tokyo, 160-0023, Japan.

3 Faculty of Science and Engineering, Chuo University,

1-13-27 Kasuga, Bunkyo-ku, Tokyo, 112-8551, Japan.

E-mail: mail@keihirose.com, shohei.tateishi@gmail.com,

konishi@math.chuo-u.ac.jp.

Abstract

In sparse regression modeling via regularization such as the lasso, it is important to select appropriate values of tuning parameters including regularization parameters. The choice of tuning parameters can be viewed as a model selection and evaluation problem. Mallows’ type criteria may be used as a tuning parameter selection tool in lasso-type regularization methods, for which the concept of degrees of freedom plays a key role. In the present paper, we propose an efficient algorithm that computes the degrees of freedom by extending the generalized path seeking algorithm. Our procedure allows us to construct model selection criteria for evaluating models estimated by regularization with a wide variety of convex and non-convex penalties. Monte Carlo simulations demonstrate that our methodology performs well in various situations. A real data example is also given to illustrate our procedure.

Key Words: , Degrees of freedom, Generalized path seeking, Model selection, Regularization, Sparse regression, Variable selection

1 Introduction

Variable selection is fundamentally important in high-dimensional linear regression modeling. Traditional variable selection procedures follow the best subset selection along with model selection criteria such as Akaike’s information criterion (Akaike, 1973) and the Bayesian information criterion (Schwarz, 1978). However, the best subset selection is often unstable because of its inherent discreteness (Breiman, 1996), and then the resulting model has poor prediction accuracy. To overcome this drawback of the subset selection, Tibshirani (1996) proposed the lasso, which shrinks some coefficients toward exactly zero by imposing an penalty on regression coefficients, resulting in simultaneous model selection and estimation procedure.

Over the past 15 years, there has been a considerable amount of lasso-type penalization methods in literature: bridge regression (Frank and Friedman, 1993; Fu, 1998), smoothly clipped absolute deviation (Fan and Li, 2001), elastic net (Zou and Hastie, 2005), group lasso (Yuan and Lin, 2006), adaptive lasso (Zou, 2006), composite absolute penalties family (Zhao et al., 2009), minimax concave penalty (Zhang, 2010) and generalized elastic net (Friedman, 2008) along with many other regularization techniques. It is well known that the solutions are not usually expressed in a closed form, since the penalty term includes non-differentiable function. A number of researchers have presented efficient algorithms to obtain the entire solutions (e.g., least angle regression, Efron et al., 2004; coordinate descent algorithm, Friedman et al., 2007, 2010, Mazumder et al., 2011; generalized path seeking, Friedman, 2008).

A crucial issue in the sparse regression modeling via regularization is the selection of adjusted tuning parameters including regularization parameters, because the regularization parameters identify a set of non-zero coefficients and then assign a set of variables to be included in a model. Choosing the tuning parameters can be viewed as a model selection and evaluation problem. Mallows’ type criteria (Mallows, 1973) estimate the prediction error of the fitted model, and give better accuracy than cross validation in some situations (Efron, 2004). The concept of degrees of freedom (e.g., Ye, 1998; Efron, 1986, 2004) plays a key role in the theory of type criteria.

In a practical situation, however, it is difficult to directly derive an analytical expression of (unbiased estimator of) degrees of freedom for sparse regression modeling. A few researchers have derived the analytical results by using the Stein’s unbiased risk estimator (Stein, 1981) for only specific penalties. Zou et al. (2007) showed that the number of non-zero coefficients is an unbiased estimate of the degrees of freedom of the lasso. Kato (2009) derived an unbiased estimate of the degrees freedom of the lasso, group lasso and fused lasso based on a differential geometric approach. Mazumder et al. (2011) proposed a re-parametrization of minimax concave penalty, which enables us to calibrate the degrees of freedom of minimax concave family. However, these selection procedures do not cover more general regularization methods via convex and non-convex penalties. In such a situation, the cross validation and the bootstrap (e.g., Ye, 1998; Efron, 2004; Shen and Ye, 2002; Shen et al., 2004) may be useful to estimate the degrees of freedom. These approaches, however, can be computationally expensive, and often yield unstable estimates.

In the present paper, we propose a new algorithm that can iteratively calculate the degrees of freedom by extending the generalized path seeking algorithm (Friedman, 2008). The proposed procedure can be applied to a wide variety of convex and non-convex penalties including the generalized elastic net family (Friedman, 2008). Furthermore, our algorithm is computationally-efficient, because there is no need to perform numerical optimization to obtain the solutions and degrees of freedom at each step. The proposed methodology is investigated through the analysis of real data and Monte Carlo simulations. Numerical results show that criterion based on our algorithm performs well in various situations.

The remainder of this paper is organized as follows: Section 2 briefly describes the degrees of freedom in linear regression models. In Section 3, we introduce a new algorithm that iteratively computes the degrees of freedom by extending the generalized path seeking. Section 4 presents numerical results for both artificial and real datasets. Some concluding remarks are given in Section 5.

2 Degrees of freedom in linear regression models

In linear regression models, the degrees of freedom can be used as a model complexity measure in Mallows’ type criteria. Suppose that () are predictors and is a response vector. Without loss of generality, it is assumed that the response is centered and the predictors are standardized by changing a location and employing scale transformations

Consider the linear regression model

where is an predictor matrix, is a coefficient vector and is an error vector with and . Here is an identity matrix.

The linear regression model is estimated by the penalized least square method

| (1) |

where is a squared error loss function

| (2) |

is a penalty term which yields sparse solutions (e.g., the lasso penalty is ), and is a tuning parameter. An equivalent formulation of (1) is

where is a regularization parameter, which corresponds to in (1).

We consider the problem of selecting an appropriate value of tuning parameter (or ) by using type criteria, for which the concept of degrees of freedom plays a key role (Ye, 1998). Assume that the expectation and the variance-covariance matrix of the response vector are

| (3) |

where is a true mean vector and is a true variance. Given a modeling procedure , the estimate can be produced from the data vector . Then, the degrees of freedom of the fitting procedure is defined as (Ye, 1998; Efron, 1986, 2004)

| (4) |

where is the th element of . For example, when the estimator is expressed as a linear combination of response vector, i.e. with being independent of , the degrees of freedom is . The trace of matrix is referred to as an effective number of parameters (Hastie and Tibshirani, 1990), which is widely used to select the tuning parameter in ridge-type regression. In sparse regression modeling such as the lasso, however, it is difficult to derive the degrees of freedom, since the penalty term is not differentiable at () so that the solutions are not usually expressed in a closed form.

Mallows’ criterion, which is an unbiased estimator of the true prediction error, can be constructed with the degrees of freedom defined in (4). Assume that the response vector is generated according to (3), and the true expectation is estimated by linear regression model. As a criterion to measure the effectiveness of the model, we consider the expected error (e.g., Hastie et al., 2008) defined by

| (5) |

where the expectation is taken over independent of .

Lemma 2.1.

The expected error in (5) can be expressed as

| (6) |

Proof.

The proof is in Appendix. ∎

Lemma 2.1 suggests criterion (e.g., Efron, 2004)

which is an unbiased estimator of the expected error in (5). The optimal model is selected by minimizing . As an estimator of the true variance of , the unbiased estimator of error variance of the most complex model is usually used.

The degrees of freedom can lead to several model selection criteria, which are summarized in Table 1. Zou et al. (2007) introduced Akaike’s information criterion (AIC; Akaike, 1973) and Bayesian information criterion (BIC; Schwarz, 1978). Wang et al. (2007, 2009) showed that the Bayesian information criterion holds the consistency in model selection. We also introduce bias corrected Akaike’s information criterion (AICC; Sugiura, 1978; Hurvich et al., 1998) and generalized cross validation (GCV; Craven and Wahba, 1979). These two criteria do not need the true variance .

| Criterion | Formula |

|---|---|

| AIC | |

| AICC | |

| BIC | |

| GCV |

3 Efficient algorithm for computing the degrees of freedom

In this section, first, the generalized path seeking algorithm is briefly described. Then, a new algorithm that iteratively computes the degrees of freedom is introduced. Furthermore, we modify the algorithm to ease the computational burden for large sample sizes.

3.1 Generalized path seeking algorithm

Friedman (2008) proposed the generalized path seeking, which is a fast algorithm to solve the problem (1). The generalized path seeking can produce the entire solutions that closely approximate those for a wide variety of convex and non-convex constraints. Suppose that the penalty term satisfies following condition:

| (7) |

This condition defines a class of penalties where each member in the class is a monotone increasing function of absolute value of each of its arguments. For example, the lasso penalty is included in this class, because . Similarly, elastic net (Zou and Hastie, 2005), group lasso (Yuan and Lin, 2006), adaptive lasso (Zou, 2006), composite absolute penalties family (Zhao et al., 2009), minimax concave penalty (Zhang, 2010) and generalized elastic net (Friedman, 2008) with many other convex and non-convex penalties are included in this class.

Denote is the solution at tuning parameter . The generalized path seeking algorithm starts at with . The solution can be iteratively computed: for given , the solution can be produced, where is a small positive value. Suppose the path is a continuous function of and all coefficient paths are monotone function of , that is, For each step, one element of coefficient vector , say , is incriminated in a correct direction with all other coefficients remaining unchanged, i.e.

| (8) | |||||

| (9) |

where and are defined as

| (10) |

Here and are

The derivation of the generalized path seeking algorithm is in Appendix.

Remark 3.1.

We assumed that is continuous and each element is monotone function of . Although these conditions can be satisfied in most cases, sometimes is discontinuous or non-monotone function. Friedman (2008) proposed an approach for non-monotone case, which is as follows: first, we define a set . When is not empty, the index is selected by . Otherwise, . The detailed description of discontinuous case is also given in Friedman (2008).

When (i.e. the lasso penalty), (8) yields

| (11) |

Note that the updated coefficient in (8) and (11) moves in the same direction even if the lasso penalty is not applied, because the condition in (7) yields . This means that the update equations (8) and (11) produce the same solution path when unless or diverges. Therefore, we can use the update equation in (11) instead of (8). If the update equation in (11) is applied, an iterative algorithm that computes the degrees of freedom in (4) can be derived.

From (9) and (11), the predicted value at is

| (12) |

Because the loss function is squared loss as (2), we have . Thus, is

| (13) |

Example 3.1.

Let be orthogonal, i.e. . By substituting (13) into , the update equation of is

Because of the orthogonality, we have

where is the number of times that th coefficient is updated until time step . It is shown that the absolute value of is monotone non-increasing function and when . When , the least squared estimates can be obtained because for all .

3.2 Derivation of update equation of degrees of freedom

Equation (13) suggests the update equation of the covariance matrix in (4) as follows:

| (14) |

The degrees of freedom is iteratively calculated by taking the trace of (14). The initial value of is set to zero-matrix because of the following equation:

Let and be the index of updated element of coefficient vector at time step . The update equation of the degrees of freedom in (14) can be expressed as

| (15) |

where . Then, the covariance matrix can be updated by

| (16) |

Example 3.2.

The degrees of freedom can be easily derived when is orthogonal. Because of the orthogonality, the covariance matrix in (16) can be calculated as

where is defined in Example 3.1. Then, the degrees of freedom is

When is very small, the degrees of freedom is close to since is sufficiently small. As gets larger, the degrees of freedom increases since . When for all , the degrees of freedom becomes the number of parameters, which coincides with the degrees of freedom of least squared estimates.

3.3 Modification of the update equation

The update equation in (12) causes little change in predicted values from to near the least squared estimates, because is very close to zero. In order to overcome this difficulty, we update the th element of coefficient vector times. Here is an integer which becomes large near least squared estimates. Since as shown in the Example 3.1, the is

| (17) |

The update equation in (17) can be applied even when is a positive real value.

The following update equation can be used so that the coefficient is appropriately updated near the least squared estimates:

| (18) | |||||

Equations (17) and (18) give us

| (19) |

It should be assumed that for any step so that exists.

When is given by (19), the update equation of the degrees of freedom in (15) can be replaced with

| (20) |

where . The algorithm that computes the solutions and the degrees of freedom is given in Algorithm 1.

3.4 More efficient algorithm

The update equation (20) suggests each step costs operations to update the covariance matrix . Because the number of iterations denoted by is usually very large such as , the proposed algorithm seems to be inefficient when is large. However, a simple modification of the algorithm eases the computational burden. With the modified process, each step costs only operations, where is the number of selected variables through the generalized path seeking algorithm: variables are not selected at all steps for generalized path seeking algorithm. When is very large, is smaller than and early stopping is used. For example, suppose that ; if we do not want more than 200 variables in the final model, we set and stop the algorithm when 200 variables are selected.

The modified algorithm is as follows: first, the generalized path seeking algorithm is implemented to obtain the entire solutions. The degrees of freedom is not computed, whereas the value of should be stored in the memory. Then, the QR decomposition of matrix is implemented, where are variables selected by the generalized path seeking algorithm. Note that . The matrix can be written as , where is an orthogonal matrix and is a upper triangular matrix. Note that can be written as , where is the -vector which consists of th column of . The update equation of the degrees of freedom based on (20) is

| (21) | |||||

| (22) |

Therefore, the computational cost of (LABEL:modified_update_equation) is only .

We provide a package msgps (Model Selection criteria via extension of Generalized Path Seeking), which computes Mallows’ criterion, Akaike’s information criterion, Bayesian information criterion and generalized cross validation via the degrees of freedom given in Table 1. The package is implemented in the R programming system (R Development Core Team, 2010), and available from Comprehensive R Archive Network (CRAN) at http://cran.r-project.org/web/packages/msgps/index.html.

4 Numerical Examples

4.1 Monte Carlo simulations

Monte Carlo simulations were conducted to investigate the effectiveness of our algorithm. The predictor vectors were generated from Gaussian distribution with mean vector zero. The outcome values were generated by

The following four Examples are presented here.

-

1.

In Example 1, 200 data sets were generated with observations and eight predictors. The true parameter was and . The pairwise correlation between and was .

-

2.

Example 2 was the dense case. The model was same as Example 1, but with , and .

-

3.

The third example was same as Example 1, but with and . In this model, the true is sparse.

-

4.

In Example 4, a relatively large problem was considered. 200 data sets were generated with observations and 40 predictors. We set

and . The pairwise correlation between and was ().

In this simulation study, there are 3 purposes as follows:

-

•

Degrees of freedom: we investigated whether the proposed procedure can select adjusted tuning parameters compared with the degrees of freedom of the lasso given by Zou et al. (2007).

- •

-

•

Speed: the computational time based on (20) was compared with that based on (LABEL:modified_update_equation).

A detailed description of each is presented.

Degrees of freedom

We compared the degrees of freedom computed by our procedure (, where means generalized path seeking) with the degrees of freedom of the lasso proposed by Zou et al. (2007) (). The degrees of freedom of the lasso is the number of non-zero coefficients. Our method and Zou’s et al. (2007) procedure do not yield identical result, since the is an unbiased estimate of the degrees of freedom while is the exact value of the degrees of freedom. In this simulation study, the true value of was used to compute the model selection criteria.

Table 2 shows the result of mean squared error (MSE) and the standard deviation (SD), which are the mean and standard deviation of the following squared error (SE):

where is the estimate of predicted values for th dataset. The proportion of cases where zero (non-zero) coefficients correctly set to zero (non-zero), say, ZZ (NN), was also computed. We can see that

-

•

Our procedure slightly outperformed Zou’s et al. (2007) one in terms of minimizing the mean squared error for all examples.

-

•

Zou’s et al. (2007) procedure selected zero coefficients correctly than the proposed procedure, while our method correctly detected non-zero coefficients compared with the Zou’s et al. (2007) approach. This means our procedure tends to incorporate many more variables than the Zou’s et al. (2007) one.

| Ex. 1 | Ex. 2 | Ex. 3 | Ex. 4 | ||||||

|---|---|---|---|---|---|---|---|---|---|

| MSE | 2.498 | 2.732 | 2.761 | 3.202 | 0.759 | 0.790 | 41.35 | 42.37 | |

| SD | 1.468 | 1.726 | 1.353 | 1.727 | 0.577 | 0.647 | 10.67 | 12.36 | |

| ZZ | 0.592 | 0.667 | — | — | 0.607 | 0.767 | 0.586 | 0.636 | |

| NN | 0.925 | 0.892 | 0.706 | 0.649 | 1.000 | 1.000 | 0.689 | 0.653 | |

Model selection criteria for several penalties

We compared the performance of model selection criteria based on the degrees of freedom: criterion (), bias corrected Akaike’s information criterion (AICC), Bayesian information criterion (BIC) and generalized cross validation (GCV). Because criterion and Akaike’s information criterion (AIC) yield the same results when true error variance is given, the result of Akaike’s information criterion is not presented in this paper. For criterion and Bayesian information criterion, we need to estimate the true error variance . The value of was estimated by the ordinary least squares of most complex model. The cross validation, which is one of the most popular methods to select the tuning parameter in sparse regression via regularization, was also applied. Since the leave-one-out cross validation is computationally expensive, the 10-fold cross validation was used.

In this simulation study, we also compared the feature and performance of several penalties including the lasso, elastic net and generalized elastic net. The elastic net and generalized elastic net are given as follows:

-

1.

Elastic net:

Here is a tuning parameter. Note that yields the lasso, and produces the ridge penalty.

-

2.

Generalized elastic net:

where is the tuning parameter. Friedman (2008) showed the generalized elastic net approximates the power family penalties , whereas the difference occurs at very small absolute coefficients. The detailed description of the generalized elastic net is in Friedman (2008). A similar idea of generalized elastic net is in Candès et al. (2008).

Note that the degrees of freedom of the lasso (Zou’s et al., 2007) cannot be directly applied to the generalized elastic net family.

We computed mean squared error (MSE), standard deviation (SD), the proportion of cases where zero (non-zero) coefficients correctly set to zero (non-zero), say, ZZ (NN). Tables 3, 4 and 5 show the comparison of model selection criteria for the lasso, elastic net () and generalized elastic net (). The detailed discussion of each example is as follows:

-

•

The generalized elastic net yielded the sparsest solution, while the elastic net produced the densest one. In Example 2, i.e. the dense case, the elastic net performed very well. On the other hand, in sparse case (Example 3), the generalized elastic net most often selected zero coefficients correctly.

-

•

In most cases, bias corrected Akaike’s information criterion (AICC) resulted in good performance in terms of mean squared error. The Bayesian information criterion (BIC) performed very well in some cases (e.g., Examples 3 and 4 on the lasso). In dense cases (Example 2), however, the performance of Bayesian information criterion (BIC) was poor.

-

•

The performance of cross validation (CV) for generalized elastic net family was excellent on Example 3. On Examples 1, 2 and 4, however, the mean squared error was large compared with other model selection criteria based on the degrees of freedom. The cross validation estimates expected error by separating the training data from the test data. Unfortunately, the regularization method with non-convex penalty such as generalized elastic net does not produce unique solution: small change in the training data can result in different solution. Thus, the cross validation may be unstable for non-convex penalty in many cases.

| AICC | GCV | BIC | CV | |||

|---|---|---|---|---|---|---|

| Ex. 1 | MSE | 2.604 | 2.497 | 2.614 | 2.567 | 2.905 |

| SD | 1.562 | 1.463 | 1.583 | 1.500 | 1.722 | |

| ZZ | 0.519 | 0.562 | 0.498 | 0.622 | 0.605 | |

| NN | 0.925 | 0.923 | 0.935 | 0.918 | 0.903 | |

| Ex. 2 | MSE | 2.807 | 2.772 | 2.781 | 2.891 | 3.195 |

| SD | 1.435 | 1.399 | 1.420 | 1.462 | 1.712 | |

| ZZ | — | — | — | — | — | |

| NN | 0.733 | 0.729 | 0.750 | 0.678 | 0.686 | |

| Ex. 3 | MSE | 0.855 | 0.790 | 0.879 | 0.744 | 0.986 |

| SD | 0.666 | 0.601 | 0.673 | 0.594 | 0.692 | |

| ZZ | 0.543 | 0.573 | 0.524 | 0.639 | 0.716 | |

| NN | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | |

| Ex. 4 | MSE | 41.66 | 42.91 | 43.82 | 39.22 | 43.59 |

| SD | 10.72 | 11.19 | 11.74 | 9.512 | 11.83 | |

| ZZ | 0.577 | 0.545 | 0.530 | 0.671 | 0.643 | |

| NN | 0.692 | 0.704 | 0.713 | 0.653 | 0.655 |

| AICC | GCV | BIC | CV | |||

|---|---|---|---|---|---|---|

| Ex. 1 | MSE | 2.860 | 2.814 | 2.826 | 2.933 | 3.017 |

| SD | 1.520 | 1.487 | 1.533 | 1.552 | 1.556 | |

| ZZ | 0.066 | 0.088 | 0.061 | 0.101 | 0.074 | |

| NN | 0.995 | 0.993 | 0.995 | 0.993 | 0.997 | |

| Ex. 2 | MSE | 2.199 | 2.061 | 2.169 | 2.218 | 2.301 |

| SD | 1.434 | 1.303 | 1.352 | 1.489 | 1.432 | |

| ZZ | — | — | — | — | — | |

| NN | 0.973 | 0.967 | 0.976 | 0.958 | 0.964 | |

| Ex. 3 | MSE | 1.566 | 1.675 | 1.577 | 1.714 | 1.720 |

| SD | 0.754 | 0.834 | 0.755 | 0.878 | 0.960 | |

| ZZ | 0.014 | 0.031 | 0.016 | 0.036 | 0.028 | |

| NN | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | |

| Ex. 4 | MSE | 25.15 | 23.31 | 25.55 | 24.73 | 24.73 |

| SD | 10.51 | 8.656 | 11.27 | 9.031 | 9.431 | |

| ZZ | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | |

| NN | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| AICC | GCV | BIC | CV | |||

|---|---|---|---|---|---|---|

| Ex. 1 | MSE | 3.060 | 2.996 | 3.051 | 3.112 | 3.785 |

| SD | 1.825 | 1.810 | 1.835 | 1.821 | 2.015 | |

| ZZ | 0.709 | 0.776 | 0.695 | 0.811 | 0.792 | |

| NN | 0.798 | 0.778 | 0.813 | 0.752 | 0.707 | |

| Ex. 2 | MSE | 3.757 | 3.747 | 3.658 | 4.018 | 4.411 |

| SD | 1.638 | 1.587 | 1.619 | 1.671 | 2.108 | |

| ZZ | — | — | — | — | — | |

| NN | 0.502 | 0.462 | 0.517 | 0.416 | 0.457 | |

| Ex. 3 | MSE | 0.889 | 0.803 | 0.949 | 0.683 | 0.485 |

| SD | 0.773 | 0.722 | 0.780 | 0.690 | 0.641 | |

| ZZ | 0.714 | 0.749 | 0.679 | 0.805 | 0.859 | |

| NN | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | |

| Ex. 4 | MSE | 74.68 | 74.12 | 75.15 | 78.75 | 80.56 |

| SD | 18.22 | 17.97 | 18.90 | 16.19 | 22.41 | |

| ZZ | 0.796 | 0.796 | 0.766 | 0.912 | 0.815 | |

| NN | 0.379 | 0.382 | 0.408 | 0.262 | 0.352 |

Speed

The computational time based on update equation (20) (naïve update) was compared with that based on (LABEL:modified_update_equation) (modified update). In order to compare the timings for various number of samples, we changed the number of samples for all Examples: , and . Table 6 shows the result of timings averaged over 200 runs for lasso penalty. All timings were carried out on an Intel Core 2 Duo 2.0 GH processor on Mac OS X. Note that the “timing” means the computational time of producing the solutions and computing the model selection criteria. The speed based on naïve update was very slow when , because we need operations to compute the degree of freedom for each step. However, the modified algorithm was fast even when the number of samples was large.

| Ex. 1 | Ex. 2 | Ex. 3 | Ex. 4 | |||||

|---|---|---|---|---|---|---|---|---|

| naïve | modified | naïve | modified | naïve | modified | naïve | modified | |

| 1.399 | 0.145 | 1.434 | 0.164 | 1.398 | 0.143 | 1.521 | 0.343 | |

| 4.827 | 0.190 | 4.834 | 0.246 | 4.820 | 0.188 | 5.012 | 0.375 | |

| 69.92 | 0.313 | 69.96 | 0.351 | 69.89 | 0.310 | 70.38 | 0.459 | |

4.2 Application to diabetes data

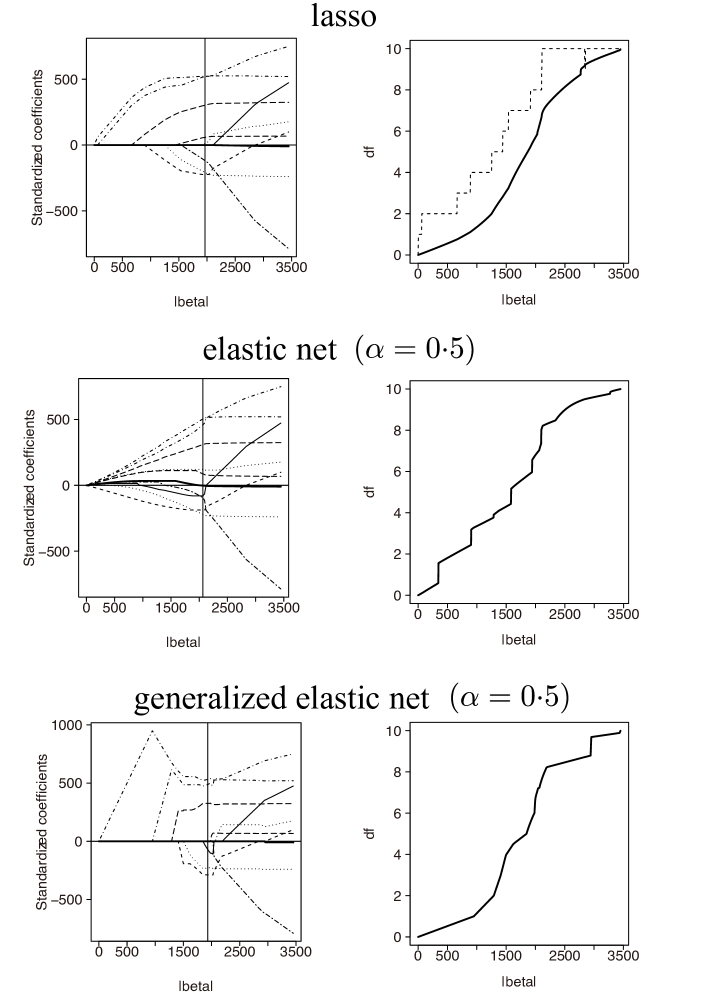

The proposed algorithm was applied to diabetes data (Efron et al., 2004), which has and . Ten baseline predictors include age, sex, body mass index (bmi), average blood pressure (bp), and six blood serum measurements (tc, ldl, hdl, tch, ltg, glu). The response is a quantitative measure of disease progression one year after baseline. We considered the following three penalties: the lasso, elastic net (), and generalized elastic net (). The entire solution path along with the solution selected by criterion, and the degrees of freedom are presented in Figure 1. On the lasso penalty, the degrees of freedom of the lasso (Zou et al., 2007) is also depicted. The degrees of freedom of our procedure was smaller than that of the lasso (Zou et al., 2007) except for , where the degrees of freedom of the lasso decreased because the non-zero coefficient of th variable became zero at .

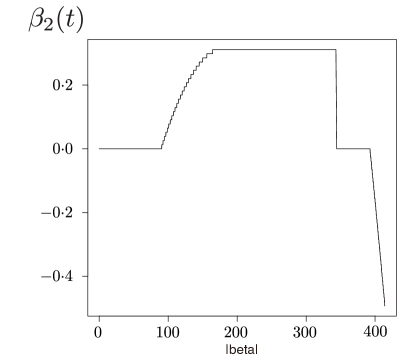

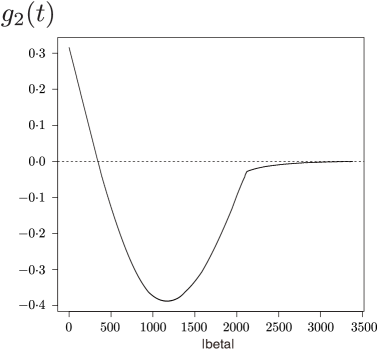

On the elastic net penalty with , the degrees of freedom increased rapidly at some points. For example, when , the degrees of freedom increased by about 0.864. Figure 2 shows the solution path of 2nd variable and , which is helpful for understanding why the degrees of freedom rapidly increased. When attained , the sign of changed. At this point, . Thus, at , which means was updated because the set in line 4 in Algorithm 1 became ={2}. When was sufficiently small, in (19) became very large, which made a substantial change in the degrees of freedom.

The estimated standardized coefficients for the diabetes data based on the lasso, elastic net () and generalized elastic net () are reported in Table 7. The tuning parameter was selected by criterion, where the degrees of freedom was computed via the proposed procedure. The generalized elastic net yielded the sparsest solution. On the other hand, the elastic net did not produce sparse solution.

| (Intercept) | age | sex | bmi | map | tc | ldl | hdl | tch | ltg | glu | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| lasso | 152 | 0 | 209 | 522 | 303 | 120 | 0 | 224 | 12 | 518 | 58 |

| enet | 152 | 2 | 220 | 504 | 309 | 93 | 81 | 188 | 122 | 460 | 87 |

| genet | 152 | 0 | 228 | 532 | 326 | 0 | 70 | 288 | 0 | 489 | 0 |

5 Concluding Remarks

We have proposed a new procedure for selecting tuning parameters in sparse regression modeling via regularization, for which the degrees of freedom was calculated by a computationally-efficient algorithm. Our procedure can be applied to construct model selection criteria for evaluating models estimated by the regularization methods with a wide variety of convex and non-convex penalties. Monte Carlo simulations were conducted to investigate the effectiveness of the proposed procedure. Although the cross validation has been widely used to select tuning parameters, the model selection criteria based on the degrees of freedom often yielded better results, especially for non-convex penalties such as generalized elastic net.

In the present paper, we considered a computationally-efficient algorithm to select the tuning parameter in the sparse regression model. For more general models including generalized linear models, multivariate analysis such as factor analysis and graphical models, it is also important to select appropriate values of tuning parameters. As a future research topic, it is interesting to introduce a new selection algorithm that handles large models by unifying the mathematical approach and computational algorithms.

Appendix

Proof of Lemma 2.1

Derivation of generalized path seeking algorithm

We derive the generalized path seeking algorithm. First, the following lemma is provided.

Lemma 5.1.

Let us consider the following problem.

| (A6) |

The solution is .

Proof.

When is sufficiently small, the problem (A6) can be approximately written as

| (A7) | |||

| (A8) |

Since all coefficient paths are monotone functions of , we have . Therefore, the problem in (A8) can be expressed as

| (A9) |

The problem in (A9) can be viewed as a linear programming. Then, the updates in (8) and (9) can be derived.

References

- Akaike (1973) Akaike, H. (1973), “Information theory and an extension of the maximum likelihood principle,” in 2nd Int. Symp. on Information Theory, Ed. B. N. Petrov and F. Csaki, pp. 267–81. Budapest: Akademiai Kiado.

- Breiman (1996) Breiman, L. (1996), “Heuristics of instability and stabilization in model selection,” Ann. Statist., 24, 2350–2383.

- Candès et al. (2008) Candès, E., Wakin, M., and Boyd, S. (2008), “Enhancing Sparsity by Reweighted Minimization,” J. Fourier. Anal. Appl., 14, 877–905.

- Craven and Wahba (1979) Craven, P. and Wahba, G. (1979), “Smoothing noisy data with spline functions: Estimating the correct degree of smoothing by the method of generalized cross-validation,” Numer. Math., 31, 377–403.

- Efron (1986) Efron, B. (1986), “How biased is the apparent error rate of a prediction rule?” J. Am. Statist. Assoc., 81, 461–470.

- Efron (2004) — (2004), “The estimation of prediction error: covariance penalties and cross-validation,” J. Am. Statist. Assoc., 99, 619–642.

- Efron et al. (2004) Efron, B., Hastie, T., Johnstone, I., and Tibshirani, R. (2004), “Least angle regression (with discussion),” Ann. Statist., 32, 407–499.

- Fan and Li (2001) Fan, J. and Li, R. (2001), “Variable selection via nonconcave penalized likelihood and its oracle properties,” J. Am. Statist. Assoc., 96, 1348–1360.

- Frank and Friedman (1993) Frank, I. and Friedman, J. (1993), “A Statistical View of Some Chemometrics Regression Tools,” Technometrics, 35, 109–148.

- Friedman (2008) Friedman, J. (2008), “Fast sparse regression and classification,” Tech. rep., Stanford Research Institute, California.

- Friedman et al. (2007) Friedman, J., Hastie, H., Höfling, H., and Tibshirani, R. (2007), “Pathwise coordinate optimization,” Ann. Appl. Statist., 1, 302–332.

- Friedman et al. (2010) Friedman, J., Hastie, T., and Tibshirani, R. (2010), “Regularization paths for generalized linear models via coordinate descent,” J. Stat. Software, 33.

- Fu (1998) Fu, W. (1998), “Penalized regression: the bridge versus the lasso,” J. Comput. Graph. Statist., 7, 397–416.

- Hastie and Tibshirani (1990) Hastie, T. and Tibshirani, R. (1990), Generalized Additive Models, Chapman and Hall/CRC Monographs on Statistics and Applied Probability.

- Hastie et al. (2008) Hastie, T., Tibshirani, R., and Friedman, J. (2008), The Elements of Statistical Learning, New York: Springer, 2nd ed.

- Hurvich et al. (1998) Hurvich, C. M., Simonoff, J. S., and Tsai, C.-L. (1998), “Smoothing parameter selection in nonparametric regression using an improved Akaike information criterion,” J. R. Statist. Soc. B, 60, 271–293.

- Kato (2009) Kato, K. (2009), “On the degrees of freedom in shrinkage estimation,” J. Multivariate Anal., 100, 1338–1352.

- Mallows (1973) Mallows, C. (1973), “Some comments on ,” Technometrics, 661–675.

- Mazumder et al. (2011) Mazumder, R., Friedman, J., and Hastie, T. (2011), “SparseNet: Coordinate descent with non-convex penalties,” J. Am. Statist. Assoc., 106, 1125–1138.

- R Development Core Team (2010) R Development Core Team (2010), R: A Language and Environment for Statistical Computing, R Foundation for Statistical Computing, Vienna, Austria, ISBN 3-900051-07-0.

- Schwarz (1978) Schwarz, G. (1978), “Estimation of the mean of a multivariate normal distribution,” Ann. Statist., 9, 1135–1151.

- Shen et al. (2004) Shen, X., Huang, H.-C., and Ye, J. (2004), “Adaptive model selection and assessment for exponential family models,” Technometrics, 46, 306–317.

- Shen and Ye (2002) Shen, X. and Ye, J. (2002), “Adaptive model selection,” J. Amer. Statist. Assoc., 97, 210–221.

- Stein (1981) Stein, C. (1981), “Estimation of the mean of a multivariate normal distribution,” Ann. Statist., 9, 1135–1151.

- Sugiura (1978) Sugiura, N. (1978), “Further analysis of the data by Akaike’s information criterion and the finite corrections,” Commun. Statist. A.-Theor. A., 7, 13–26.

- Tibshirani (1996) Tibshirani, R. (1996), “Regression shrinkage and selection via the lasso,” J. R. Statist. Soc. B, 58, 267–288.

- Wang et al. (2009) Wang, H., Li, B., and Leng, C. (2009), “Shrinkage tuning parameter selection with a diverging number of parameters,” J. R. Statist. Soc. B, 71, 671–683.

- Wang et al. (2007) Wang, H., Li, R., and Tsai, C. (2007), “Tuning parameter selectors for the smoothly clipped absolute deviation method,” Biometrika, 94, 553–568.

- Ye (1998) Ye, J. (1998), “On measuring and correcting the effects of data mining and model selection,” J. Amer. Statist. Assoc., 93, 120–131.

- Yuan and Lin (2006) Yuan, M. and Lin, Y. (2006), “Model selection and estimation in regression with grouped variables,” J. R. Statist. Soc. B, 68, 49–67.

- Zhang (2010) Zhang, C. (2010), “Nearly unbiased variable selection under minimax concave penalty,” Ann. Statist., 38, 894–942.

- Zhao et al. (2009) Zhao, P., Rocha, G., and B., Y. (2009), “The composite absolute penalties family for grouped and hierarchical variable selection,” Ann. Statist., 37, 3468–3497.

- Zou (2006) Zou, H. (2006), “The adaptive Lasso and its oracle properties,” J. Amer. Statist. Assoc., 101, 1418–1429.

- Zou and Hastie (2005) Zou, H. and Hastie, T. (2005), “Regularization and variable selection via the elastic net,” J. R. Statist. Soc. B, 67, 301–320.

- Zou et al. (2007) Zou, H., Hastie, T., and Tibshirani, R. (2007), “On the Degrees of Freedom of the Lasso,” Ann. Statist., 35, 2173–2192.