Dynamical generalized Hurst exponent as a tool to monitor unstable periods in financial time series

Abstract

We investigate the use of the Hurst exponent, dynamically computed over a moving time-window, to evaluate the level of stability/instability of financial firms. Financial firms bailed-out as a consequence of the 2007-2010 credit crisis show a neat increase with time of the generalized Hurst exponent in the period preceding the unfolding of the crisis. Conversely, firms belonging to other market sectors, which suffered the least throughout the crisis, show opposite behaviors. These findings suggest the possibility of using the scaling behavior as a tool to track the level of stability of a firm. In this paper, we introduce a method to compute the generalized Hurst exponent which assigns larger weights to more recent events with respect to older ones. In this way large fluctuations in the remote past are less likely to influence the recent past. We also investigate the scaling associated with the tails of the log-returns distributions and compare this scaling with the scaling associated with the Hurst exponent, observing that the processes underlying the price dynamics of these firms are truly multi-scaling.

keywords:

Generalized Hurst exponent , multi-scaling analysis , Econophysics1 Introduction

The search for scaling behaviors in financial markets is nowadays a very rich discipline

[1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11]

where the growing amount of empirical data is continuously advancing the understanding of markets behaviors.

Two types of scaling [12, 13] are observed and studied in the finance literature: the first one is associated with any volatility measure and its scaling in time (e.g. moments of the returns distribution), while the second one reflects the behavior of the tails of the distribution of returns.

In this paper we look at both of them and at the relationship between the two by using the generalized Hurst exponent (GHE) approach.

Previous works [14, 15] have highlighted that the value of the GHE allows to characterize the stage of development of a market, with values of the GHE greater than indicating a low stage of development, typical of the emerging markets, while values of the GHE lower than corresponding to an advanced stage of development.

Here we study whether the same paradigm can be applied to characterize the level of stability of a firm.

To this purpose we introduce a weighted average to compute the dynamical generalized Hurst exponent obtaining a finer differentiation in the historical time series by smoothing the propagation of large fluctuations from the remote past to the near present.

Although multi-scaling analysis based on the GHE has been already extensively pursued in the literature [9, 10, 11, 14, 15, 16, 17, 18, 19, 20], the dynamics of the GHE has been scarcely investigated [21].

In this work we have used a moving time-window and studied the behavior in time of the GHE of different financial time series with the aim of both uncovering the statistical properties of the empirical data and pointing out further potentials for the applications of this tool.

In particular, our analyses have been focused in determining whether the GHE may be used to track the stability of firms from several market sectors.

The data are from 395 stock prices of companies listed in the New York Stock Exchange (NYSE) and have been provided by Reuters. We have analyzed several companies belonging to different market sectors but we have focused our attention on the companies most severely involved in the unfolding of the 2007-2010 “credit crunch” crisis.

The scaling analysis based on the estimation of the GHE is also compared to the one associated with the behavior of the tails of the distribution.

This paper is structured as follows: section 2 recalls the definition of the GHE; section 3 describes the weighted-average algorithm; in section 4 the empirical analysis is performed and a proper choice of the parameters of the system is discussed; section 5 introduces the scaling of the distributions of the returns whose relations to the GHE is reported in section 6; conclusions are drawn in section 7.

2 Generalized Hurst Exponent

The generalized Hurst exponent is a tool to study directly the scaling properties of the data via the qth-order moments of the distribution of the increments and it is associated with the long-term statistical dependence of a certain time series , with , defined over a time-window with unitary time-steps.111Here, to simplify notation, we use unitary time-steps; generalization to arbitrary time-steps is straightforward. Being a measure of correlation persistence, it is necessarily related to fundamental statistical quantities which turn out to be the qth-order moments of the distribution of the increments, defined as [14, 22]

| (1) |

where can vary between 1 and and denotes the sample average over the time-window. Note that for , is proportional to the autocorrelation function: . The generalized Hurst exponent is then defined from the scaling behavior of when the following relation holds:

| (2) |

Processes exhibiting this scaling behavior can be divided into two classes: (i) Processes with , i.e. independent of . These processes are uniscaling (or unifractal) and their scaling behavior is uniquely determined by the constant (Hurst exponent or self-affine index [14]); (ii) Processes with not constant. These processes are called multiscaling (or multifractal) and each moment scales with a different exponent. Previous works have pointed out how financial time series exhibit scaling behaviors which are not simply fractal, rather multi-fractal, or multiscaling [14, 15]. The GHE is computed from an average over a set of values corresponding to different values of in Eq.1 [15, 16, 23]. The analysis based on the generalized Hurst exponent is very simple as all the information about the scaling properties of a signal is enclosed in the scaling exponent .

3 Weighted exponential smoothing

To take into account the fact that the recent past is more important than the remote past we can assume that the informational relevance of observations decays exponentially. This ‘exponential smoothing’ is attained by defining weights as

| (3) |

where is the weights’ characteristic time and its inverse is the exponential decay factor . The parameter is given by [24]

| (4) |

The weighted average over the time-window for a general quantity is thus

| (5) |

and the weighted GHE (wGHE) is therefore obtained by substituting the normal averages in Eq.1 with weighted averages:

| (6) |

From the scaling law in Eq.2 this leads to the linear relation

| (7) |

from which the wGHE can be computed. In the next section we apply this tool to the empirical time series.

4 Empirical Analysis

The empirical time series here analyzed include daily stock prices from 1 January 1996 to 30 April 2009. From these prices we define a new time series of the daily log-returns

| (8) |

where is the daily price.

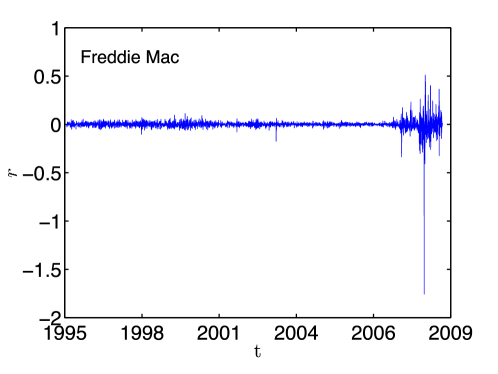

In Fig.1 an example of log-returns for the Freddie Mac stock prices is shown.

Not surprisingly, these returns exhibit large fluctuations in the crisis period.

From the log-returns we have then computed the wGHE by using Eq.7.

In analogy with [16, 15, 23] we have estimated the as an average of several linear fits of Eq.7 with and varying between 5 and 19.

As proxy of the statistical uncertainty of the scaling law we have computed the standard deviation of the over this range of .

To track the evolution of the stage of development of a certain company, we have studied the dynamics in time of the wGHE on overlapping time-windows with a constant 50 days shift between any two successive windows.

First of all, to fully capture the advantages of the weighted average method, a choice of the parameters and , namely the characteristic time and the width of the time-window, has to be made.

In particular the time-window must be large enough to provide good statistical significance but it should not be too large in order to retain sensitivity to changes in the scaling properties occurring over time.

In order to satisfy both these requirements we take a rather long time-window combined with a relatively short characteristic time .

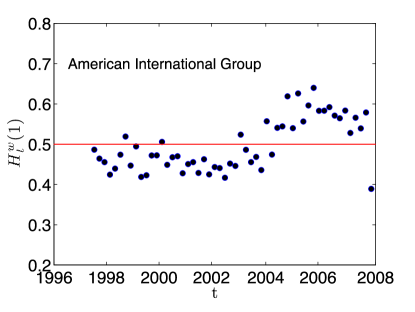

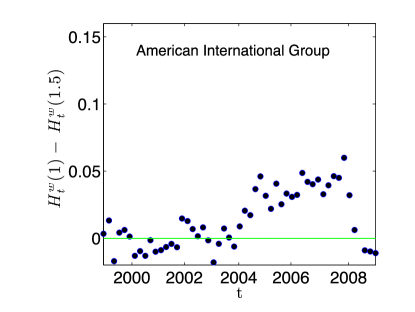

For instance, in Fig.3 we show how the manipulation of the parameters and affects the dynamics of the Hurst exponent of the company American International Group (AIG).

As it can be appreciated in the figure, which shows plots for AIG with time-windows of respectively 200 days (left panel) and 400 days (right panel) while keeping days, the shape of the outline shrinks and gets neater as the time-window is increased.

The left panel of Fig.3 shows more noisy dynamics when is smaller.

Conversely, in the right panel we can appreciate that a slimmer outline is achieved by increasing the statistics, but duly weighting it.

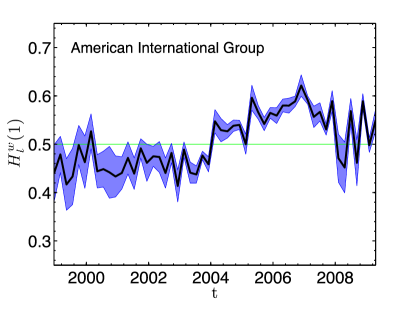

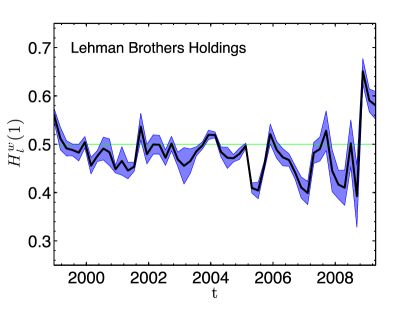

This can be further improved by increasing the value of up to three years of trading time while keeping down to one year. The result of this is shown in Fig.4 for Lehman Brothers Holdings (LBH) and American International Group where the thick lines are the average and the bands are given by the standard deviations over between 5 and 19 days [16, 15, 23]. This choice of the parameters is probably the best as it allows to have a sufficiently large, though not too much, statistics, but at the same time the events are weighted such that not to all the information present in the time series is given the same importance.

Once the choice of the parameters is made, one can notice that the behavior of for AIG is slightly different from the one of LBH. The first one shows indeed a well-defined increasing trend, with a transition from values to values , while LBH keeps steady around , except for a decrease towards the end of the period followed by a sudden leap upwards.

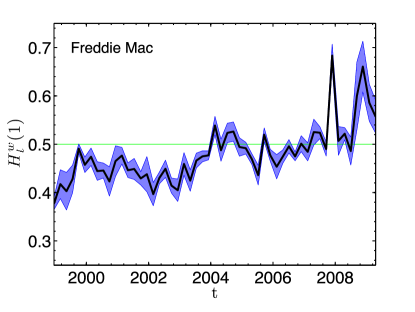

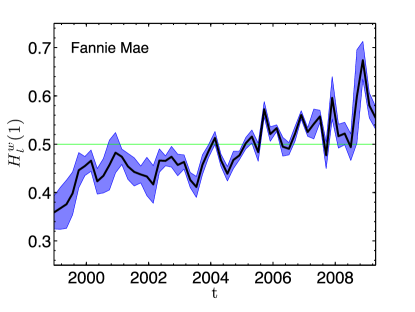

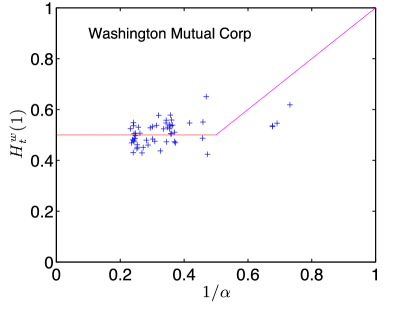

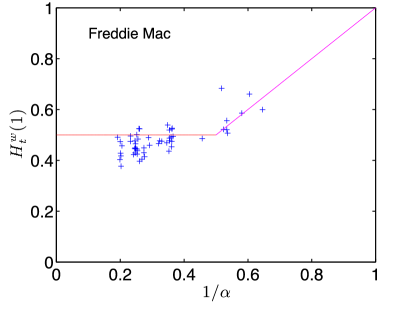

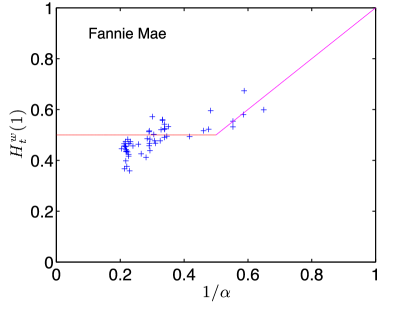

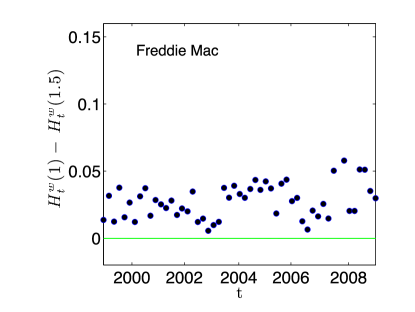

In Fig.5 the dynamics in time of for the companies Freddie Mac and Fannie Mac is reported. These are public government sponsored enterprises which in September 2008 had to be put into conservatorship by the U.S. Treasury; namely the huge debts of these companies were purchased by the U.S. government. After playing a central role in the market during the mortgages’s boost both firms defaulted. Their fate is pretty well pictured by the dynamical wGHE.

Indeed, there is a clearly visible trend in these plots showing how the value of for these companies has been increasing since 1996 until 2009.

This is particularly interesting if we compare the two panels. According to [14, 15] these trends might suggest a transition from a stable stage of the companies to an unstable one.

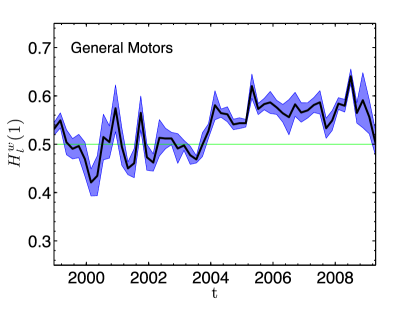

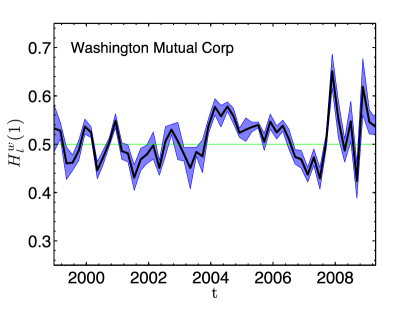

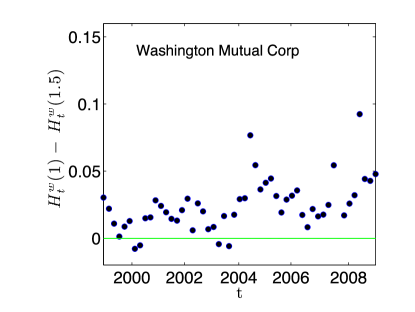

Other bailed-out companies which show the same trend are shown in Fig.6. Again the trend is increasing and crossing over the value of towards the end of the time-period when the crisis fully unfolded.

We have compared these results with those obtained by looking at other companies either from the financial sector or belonging to other market sectors to test the significance of these results.

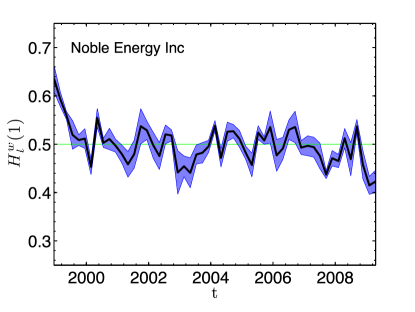

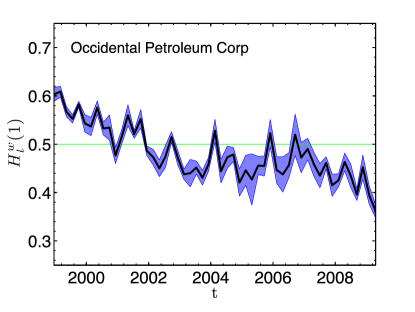

For example, in the Basic Materials sector, we find many companies whose dynamical wGHE decreases in time, thus exhibiting an opposite behavior to that shown by the bailed-out companies in the financial sector.

An example is reported in Fig.7 where the dynamical wGHE’s for two companies belonging to the sector of Basic Materials are shown.

We notice a very definite overall decreasing trend, as if the companies securities gained persistence in going through the period of crisis.

This is in agreement with what has been considered as the boost of the commodities market during the crisis, where investors were turning away from the financial sector.

There are other sectors that have revealed instead no particular trend in the dynamical wGHE. We stress that even in the Financial sector itself, the increasing trend found for the bailed-out companies is not common to others; for instance, many companies, like American Express Co and Morgan Stanley show stable behaviors, with wGHE values steadily fluctuating about 0.5.

We will see in the next paragraph that the sectors exhibiting a defining trend in the dynamical wGHE are also those showing extreme values in the tail exponents of their distributions of returns.

Although the increase or decrease of the wGHE is not simply related with the return statistics only, both behaviors are associated with the fluctuations of the log-returns distributions.

5 Fat-tails and extreme events

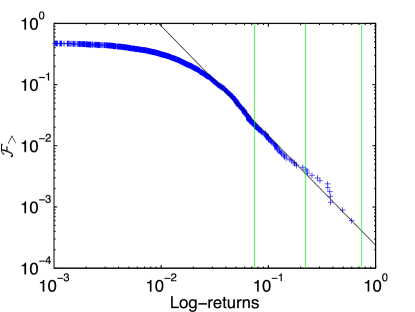

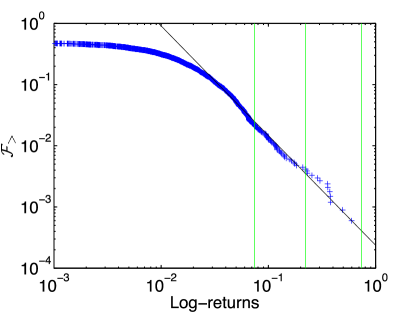

The unfolding of the 2008-2009 ”credit crunch” financial crisis has made all of us again aware that in markets very large fluctuations can happen with finite probability. Indeed large fluctuations are very unlikely, say impossible, in a normal statistics frame but are instead rather common in complex systems and they are properly accounted by non-normal statistics. In order to quantitatively catch these large fluctuations we have investigated the scaling of the tails of the distributions of the log-returns. In Fig.8 we report the complementary cumulative distributions for the stock prices of the same companies studied in the previous section. Let us recall that, given a probability density function , its complementary cumulative distribution 222The plot of in Fig.8 is a so-called rank-frequency plot. This is a very convenient and simple method to analyze the tail region of the distribution without any loss of information which would instead derive from gathering together data points with an artificial binning. In order to make this plot from a given set of observations , one first sorts the T observed values in ascending order and then plots them against the vector . Indeed, we have that is defined by

| (9) |

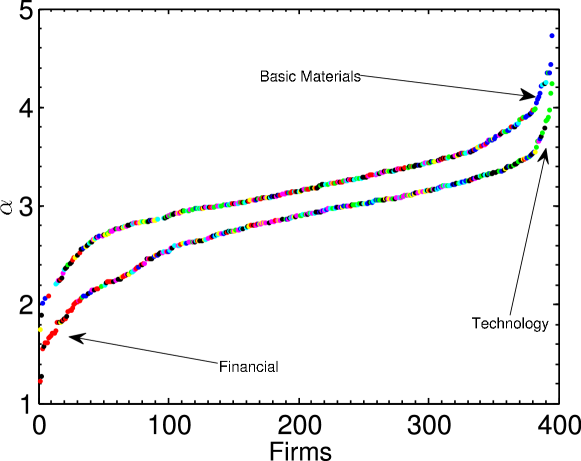

We can see from Fig.8 that fluctuations above have frequencies above and therefore are occurring on average several times a year. We can also observe that the tails decrease linearly in log-log scale. Indeed, we find, in the tail region, good fits with the power law function with . Although the linear decrease of large fluctuations in log-log scale is not necessarily a proof for power-law behavior, in this case the power law hypothesis is enforced by the p-value test ( for AIG and for LBH) [25]. However we stress that by excluding the recent unstable period from the same dataset, i.e. taking off the years 2008-2009, a slightly different picture emerges with the scaling exponents exhibiting larger values and the frequency of very large fluctuations becoming an order of magnitude smaller. Fig.9 shows the exponents for all the firms, computed both over the entire period and over the period excluding the crisis.

One can note from Fig.9 that, excluding the crisis period, the exponent increases across all firms and the occurrence of extreme events is much lower than the one observed when the crisis is included.

In particular Fig.9 shows how the financial sector forms a cluster at the bottom end of the sorted companies, when the crisis period is included.

It’s also interesting to note that the firms belonging to the Technology sector appear to be the most stable.

Values of the scaling exponents between 2 and 4 are commonly observed in these systems [26, 27].

These distributions typically have finite second moment but diverging larger moments and this explains in turn why we find very large values for the excess kurtosis (139 for AIG and 761 for LBH).

The fact that the tail exponents change by including or excluding in the statistics data referring to some extreme events is not a surprise though.

It is not a surprise either, the fact that stock prices do not obey normal statistics.

Nonetheless these large fluctuations over the last time-period when the crisis was unfolding may be somehow the cause for the increase of the wGHE, and this is what we are going to discuss in the next section.

6 Discussion

In order to understand the link between the two types of scaling, let us first investigate the simple ideal case where the underlying process is a random walk with where . In this case, for an arbitrary , the log-returns can be written as a sum of random variables:

| (10) |

If the are iid, the Central Limit Theorem applies to the and there are two cases: (1) the probability distribution function of has finite variance and therefore the distribution of converges to a normal distribution for large ; (2) the variance is not defined and the asymptotic distribution of the converges to a Levy Stable distribution. For distributions well approximated by power-law functions in the tail region, the parameter that distinguishes between these two cases is the tail index . Namely leads to normal distributions, while leads to Levy Stable distributions. Moreover, given that is a sum of random variables and given that both cases (1) and (2) lead to stable distributions333A distribution is stable if and only if, for any , the distribution of is equal to the distribution of , with . This implies (11) where is the aggregate distribution of the sum of the i.i.d. variables and is the distribution of the . , the probability distribution , of the log-returns must scale with as [26, 27]

| (12) |

Accordingly, the q-moments scale as

| (13) |

Here denotes the expectation value. Finally, if we restrict to the class of self-affine processes, i.e. those processes where the probability distribution of is equal to the probability of , for any positive , and we consider stationary increments, the q-moments must scale as

| (14) |

By comparing Eq.13 with Eq.14 we get

| (15) |

Eq.14 holds also for the moments computed using the weighted average, by substituting with and the expectation values with weighted averages. Processes with the property in Eq.14 are deemed uniscaling. For we retrieve and the processes scales as a Brownian motion. Let us here stress that the result in Eq.15 is only valid for a random-walk type iid process with defined noise distribution. On the other hand, it is well known that financial time series cannot be described within this framework. However, Eq.15 is a valuable reference which can be used as a tool to compare the relation between the tail exponent and the Hurst exponent in more complex signals.

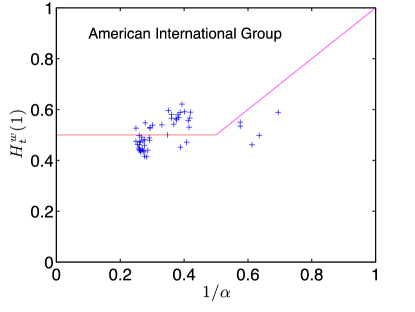

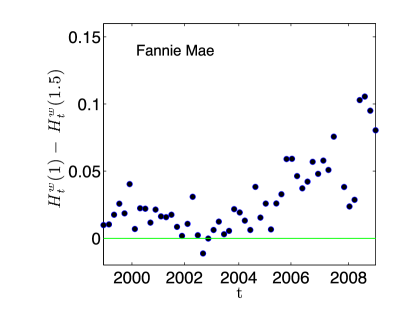

In Fig.10 we report plots of the wGHE, , versus the tail exponents computed at different times (see caption for details).

According to the previous considerations, we must observe a linear trend of vs. for and, instead, a flat behavior for .

In the figure we can indeed observe a departure from a linear trend occurring around .

On the other hand, the poor agreement with the prediction from Eq.15 reveals that the process is not uniscaling and this is a signature of multifractality.

This multifractality can be measured by tracking the difference over the time-windows (see Fig.11).

Intriguingly, this difference remains stable for most of the time for all the companies reported in the figure but, instead, it increases as soon as the unstable period is reached, suggesting that the scaling properties of the time series change with the unfolding of the crisis.

We stress that the behavior observed in the empirical data is not necessarily related to a change of the stochastic process underlying the financial time series.

The increase in the multifractality of these kinds of signals is likely to occur in the presence of large price fluctuations.

In this case indeed, the attitude of the investors, and thus the prices’ movements, in the short period, are very rarely reflecting the price behavior over larger periods.

Let us finally note that for the bailed-out companies it would also be interesting to look at , which, as we said, is associated to the scaling of the auto-correlation function of the time series. However, in spite of the behavior being very similar to that observed for , for (which is the case for these companies) the second moment is not defined and thus it’s difficult to interpret the real meaning of .

7 Conclusions

We have studied the scaling behavior in time of log-returns of the companies more severely affected by the ‘credit-crunch’ crisis. The results obtained for these companies have been compared to those obtained for companies belonging to different market sectors, showing persistent differences. To allow a reasonable differentiation in the time series we have introduced a weighting procedure which renders recent events more significant that remote ones. With this exponential smoothing method we have computed the weighted Generalized Hurst exponent for overlapping time-windows spanning a period of 13 years (1996-2009). The bailed-out companies reveal an increasing trend which crosses 0.5 hinting therefore to a transition between different stages of development. This behavior, not observed for many other companies, including others belonging to the financial sector itself, might suggest that the wGHE is conveying important information about the stability of a company and that by tracking its value in time one could have a further tool to assess risk. A comparison with the scaling of the distributions of the log-returns shows that large fluctuation over a period may be related to the increase of the wGHE. We have also looked at the multifractal behavior in time of these companies revealing a multiscaling behavior with multifractality increasing when the crisis occurred. These empirical facts will be the basis of future work aiming to realistically model the price formation and evolution in financial markets [28, 15, 29, 30].

Acknowledgements

We wish to thank the COST MP0801 project for partially supporting this work.

References

- [1] B. Mandelbrot. The variation of certain speculative prices. The journal of business, 36:394–419, 1963.

- [2] B. Mandelbrot. Fractals and scaling in finance: discontinuity, concentration, risk. Springer Verlag, 1997.

- [3] L. Calvet and A. Fisher. Multifractality in asset returns: theory and evidence. Review of Economics and Statistics, 84:381–406, 2002.

- [4] J.P. Bouchaud, M. Potters, and M. Meyer. Apparent multifractality in financial time series. The European Physical Journal B-Condensed Matter and Complex Systems, 13:595–599, 2000.

- [5] R.N. Mantegna and H.E. Stanley. Scaling behaviour in the dynamics of an economic index. Nature, 376:46–49, 1995.

- [6] B. LeBaron. Stochastic volatility as a simple generator of apparent financial power laws and long memory. Quantitative Finance, 1:621–631, 2001.

- [7] T. Kaizoji. Scaling behavior in land markets. Physica A, 326:256–264, 2003.

- [8] E. Scalas. Scaling in the market of futures. Physica A, 253:394–402, 1998.

- [9] M. Bartolozzi, C. Mellen, T. Di Matteo, T. Aste, Multi-scale correlations in different futures markets, European Physical Journal B 58:207-220, 2007.

- [10] Ruipeng Liu, Thomas Lux, T. Di Matteo, True and Apparent Scaling: The Proximities of the Markov-Switching Multifractal model to Long-Range Dependence, Physica A 383:35-42, 2007.

- [11] Ruipeng Liu, T. Di Matteo, Thomas Lux, Multifractality and Long-Range Dependence of Asset Returns: The Scaling Behaviour of the Markov-Switching Multifractal model with Lognormal Volatility Components Advances in Complex Systems, 11:669-684, 2008.

- [12] J.W. Kantelhardt, S.A. Zschiegner, E. Koscielny-Bunde, S. Havlin, A. Bunde, and H.E. Stanley. Multifractal detrended fluctuation analysis of nonstationary time series. Physica A: Statistical Mechanics and its Applications, 316:87–114, 2002.

- [13] P.A. Groenendijk, A. Lucas, and C.G. de Vries. A hybrid joint moment ratio test for financial time series. Preprint of Erasmus University, 1:1–38, 1998.

- [14] T. Di Matteo. Multi-scaling in finance. Quantitative Finance, 7:21–36, 2007.

- [15] T. Di Matteo, T. Aste, and M.M. Dacorogna. Long-term memories of developed and emerging markets: Using the scaling analysis to characterize their stage of development. Journal of Banking & Finance, 29:827–851, 2005.

- [16] T. Di Matteo, T. Aste, and M.M. Dacorogna. Scaling behaviors in differently developed markets. Physica A: Statistical Mechanics and its Applications, 324:183–188, 2003.

- [17] J. Barunik and L. Kristoufek. On hurst exponent estimation under heavy-tailed distributions. Physica A: Statistical Mechanics and its Applications, 389:3844–3855, 2010.

- [18] B. Mandelbrot, A. Fisher, and L. Calvet. A multifractal model of asset returns. Cowles Foundation Discussion Paper No. 1164, Sauder School of Business Working Paper, 1997.

- [19] T. Lux. The multifractal model of asset returns: Simple moment and gmm estimation. Journal of Business and Economic Statistics, 2006.

- [20] A. Carbone. Algorithm to estimate hurst exponent of high-dimensional fractals. Physical Review E, 76, 2007.

- [21] A. Carbone, G. Castelli, and H.E. Stanley. Time-dependent hurst exponent in financial time series. Physica A: Statistical Mechanics and its Applications, 344:267–271, 2004.

- [22] A.L. Barabasi and T. Vicsek. Multifractality of self-affine fractals. Physical Review A, 44:2730–2733, 1991.

- [23] T. Aste. Generalized hurst exponent of a stochastic variable:. http://www.mathworks.com/matlabcentral/fileexchange/30076.

- [24] F. Pozzi, F. Aste, and T. Di Matteo. Exponential smoothing weighted correlations. To appear, 2011.

- [25] A. Clauset, C.R. Shalizi, and M.E.J. Newman. Power-law distributions in empirical data. Arxiv preprint arXiv:0706.1062, 2007.

- [26] J.P. Bouchaud and M. Potters. Theory of financial risk and derivative pricing: from statistical physics to risk management. Cambridge University Press, 2003.

- [27] R.N. Mantegna and H.E. Stanley. An introduction to econophysics: correlations and complexity in finance. Cambridge University Press, 2000.

- [28] M.M. Dacorogna, U.A. Müller, R.B. Olsen, and O.V. Pictet. An Introduction to High Frequency Finance. San Diego Academic Press, CA, 2001a.

- [29] R. Liu, T. Di Matteo, and T. Lux. Multifractality and long-range dependence of asset returns: the scaling behavior of the markov-switching multfractal model with lognormal volatility components. Advances in Complex Systems, 11(5):669–684, 2008.

- [30] M. Bartolozzi and A.W. Thomas. Stochastic cellular automata model for stock market dynamics. Physical Review E, 69:046112, 2004.