Linear Variance Bounds for Particle Approximations of Time-Homogeneous Feynman-Kac Formulae

Abstract

This article establishes sufficient conditions for a linear-in-time

bound on the non-asymptotic variance for particle approximations of

time-homogeneous Feynman-Kac formulae. These formulae appear in a

wide variety of applications including option pricing in finance

and risk sensitive control in engineering. In direct Monte Carlo

approximation of these formulae, the non-asymptotic variance typically

increases at an exponential rate in the time parameter. It is shown

that a linear bound holds when a non-negative kernel, defined by

the logarithmic potential function and Markov kernel which specify

the Feynman-Kac model, satisfies a type of multiplicative drift condition

and other regularity assumptions. Examples illustrate that these conditions

are general and flexible enough to accommodate two rather extreme

cases, which can occur in the context of a non-compact

state space: 1) when the potential function is bounded above, not

bounded below and the Markov kernel is not ergodic; and 2) when the

potential function is not bounded above, but the Markov kernel itself

satisfies a multiplicative drift condition.

Keywords: Feynman-Kac Formulae; Non-Asymptotic Variance; Multiplicative

Drift Condition.

1 Introduction

On a state space endowed with a -algebra let be a Markov kernel and let be a logarithmic potential function. Then for , consider the sequence of measures defined by

| (1.1) |

for a suitable test function and where denotes expectation with respect to the law of a Markov chain with transition kernel , initialised from .

Feynman-Kac formulae as in (1.1) arise in a variety of application domains. In the case that is non-positive, the quantity can be interpreted as the probability of survival up to time step of a Markovian particle exploring an absorbing medium (Del Moral and Miclo, 2003; Del Moral and Doucet, 2004); the particle evolves according to and at time step it is killed with probability . Another application is the calculation of expectations at a terminal time with respect to jump-diffusion processes which may or may not be partially observed (e.g. Jasra and Doucet (2009)). In particular, for option pricing in finance, there are a variety of options, (e.g. asian, barrier) which can be written in the form (1.1) where the potential function arises from the pay-off function/change of measure and the Markov kernel specifies finite dimensional marginals of some partially observed Lévy process (e.g. Jasra and Del Moral (2011)). It is remarked that in this latter example, the finite dimensional marginals can induce a time-homogeneous Markov chain that is not necessarily ergodic. Furthermore, functionals as in (1.1) arise in certain stochastic control problems, where one considers the bivariate process with being a controlled Markov chain and a control input process. In some cases the transition kernel can be expressed as with corresponding to the control law or policy and to the controlled process dynamics. In a risk-sensitive optimal control framework arises as a cost function one aims to minimise with respect to an appropriate class of policies; see (Whittle, 1990; Di Masi and Stettner, 1999) for details. In such problems it is common to choose to be unbounded from above, e.g. is usually chosen to be a quadratic for linear and Gaussian state space models (Whittle, 1990). More generally (1.1) arises as a special case of a time-inhomogeneous Feynman-Kac formulae studied by Del Moral (2004).

The non-negative kernel , defines a linear operator on functions and (1.1) can be rewritten as , where denotes the -fold iterate of . In the applications described above, the Feynman-Kac formulae (1.1) typically cannot be evaluated analytically. However, they may be approximated using a system of interacting particles (Del Moral, 2004). These particle systems, also known as sequential Monte Carlo methods in the computational statistics literature (e.g. Doucet et al. (2001)), have themselves become an object of intensive study, see amongst others (Crisan and Bain, 2008; Del Moral et al., 2009; van Handel, 2009; Chopin et al., 2011; Del Moral et al., 2011) and references therein for recent developments in a variety of settings.

The present work is concerned with second moment properties of errors associated with the particle approximations of . In order to obtain bounds on the relative variance, we control certain tensor-product functionals of these particle approximations, recently addressed by Cérou et al. (2011), using stability properties of the operators . These stability properties are themselves derived from the multiplicative ergodic and spectral theories of linear operators on weighted -norm spaces due to Kontoyiannis and Meyn (2003, 2005); this is one of the main novelties of the paper. By doing so we obtain a linear-in- relative variance bound under assumptions on which are weaker than those relied upon in the literature to date and which readily hold on non-compact spaces. Furthermore, to the knowledge of the authors, these are the first results which establish

-

•

that a linear-in- bound holds under conditions which can accommodate defined in terms of a non-ergodic Markov kernel ,

-

•

that any form of non-asymptotic stability result for particle approximations of Feynman Kac formulae holds under conditions which can accommodate not bounded above.

1.1 Interacting Particle Systems

Let be a population size parameter. For , let be the -th generation of the particle system, where each particle, , is a random variable valued in . Denote . The generations of the particle system form a -valued Markov chain: for , the law of this chain is denoted by and has transitions given in integral form by:

| (1.2) |

where , is the unit function and for some test function , (here the dependence of on is suppressed from the notation). These transition probabilities correspond to a simple selection-mutation operation: at each time step particles are selected with replacement from the population, on the basis of “fitness” defined in terms of , followed by each particle mutating in a conditionally-independent manner according to .

The empirical measures , defined by

and are taken as approximations of . It is well known (Del Moral, 2004, Chapter 9) that

where denotes expectation with respect to the law of the -particle system.

1.2 Standard Regularity Assumptions for Stability

Recent work on analysis of tensor product functionals associated with , (Del Moral et al., 2009), has lead to important results regarding higher moments of the error associated with these particle approximations; in a possibly time-inhomogeneous context Cérou et al. (2011) have proved a remarkable linear-in- bound on the relative variance of . In the context of time-homogeneous Feynman-Kac models, the assumptions of Cérou et al. (2011) are that

| (1.3) |

and that for some , there exists a finite constant such that

| (1.4) |

The result of Cérou et al. (2011) is then of the form:

| (1.5) |

where is as in (1.4). The efficiency of the particle approximation is therefore quite remarkable: a natural alternative scheme for estimation of is to simulate independent copies of the Markov chain with transition and approximate the expectation in (1.1) by simple averaging, but the relative variance in that case typically explodes exponentially in . The restriction is that (1.4) rarely holds on non-compact spaces. The present work is concerned with proving a result of the same form as (1.5) under assumptions which are more readily verifiable when is non-compact. The main result is summarized after the following discussion of (1.3)-(1.4) and how they relate to the assumptions we consider.

The condition of (1.4) and its variants are very common in the literature on exponential stability of nonlinear filters and their particle approximations, see for example (Del Moral and Guionnet, 2001; Le Gland and Oudjane, 2004) and references therein. It can be interpreted as implying a uniform bound on the relative oscillations of the total mass of , i.e.,

| (1.6) |

and this is very useful when controlling various functionals which arise when analysing the relative variance as in (1.5), (see Cérou et al. 2011, Proof of Theorem 5.1). However one may take the interpretation of (1.4) in another direction: it implies immediately that there exist finite measures, say and , and such that

| (1.7) |

In the case that (i.e is a probabilistic kernel) and is -irreducible and aperiodic, this type of minorization over the entire state space implies uniform ergodicity of , which is in turn equivalent to satisfying a Foster-Lyapunov drift condition with a bounded drift function (Meyn and Tweedie, 2009, Theorem 16.2.2). In the scenario of present interest, where in general , one may take to be defined by , for all , and then when (1.3) holds, it is trivially true that there exists and such that satisfies the multiplicative drift condition,

| (1.8) |

where is the indicator function on . may then also be viewed as a bounded linear operator on the space of real-valued and bounded functions on endowed with the -norm, which is norm-equivalent (in the sense of Meyn and Tweedie, 2009, p.393) to , with any bounded weighting function.

1.3 Setting and Main Result

Del Moral (2004, (e.g. Chapter 4 and Section 12.4)) and Del Moral and Doucet (2004) address the setting in which is considered as a semigroup of bounded linear operators on the Banach space of real-valued and bounded functions on , endowed with the -norm, and Del Moral and Miclo (2003) address the setting, connecting stability properties of the measures and their normalized counterparts to the spectral theory of bounded linear operators on Banach spaces.

Kontoyiannis and Meyn (2003, 2005) have developed multiplicative ergodic and spectral theories of operators of the form in the setting of weighted -norm spaces; a function space setting which has already proved to be very fruitful for the study of general state-space Markov chains (Meyn and Tweedie, 2009, Chapter 16) without reversibility assumptions. The reader is referred to (Kontoyiannis and Meyn, 2003, 2005) for extensive historical perspective on this spectral theory and related topics, including (of particular relevance in the present context) the theory of non-negative operators due to Nummelin (2004, Chapter 5). The work of (Kontoyiannis and Meyn, 2003, 2005; Meyn, 2006) is geared towards large deviation theory for sample path ergodic averages under the transition and in that context it is natural to state assumptions on and separately. By contrast, when studying the particle systems described above, we are not directly concerned with such sample paths, but rather the relationship between the properties of the particle approximations and their exact counterparts . Some of the results of Kontoyiannis and Meyn (2003, 2005) will be applied to this effect, but starting from assumptions expressed directly in terms of which reflect the scenario of interest.

The core assumptions in the present work (see Section 2.2 for precise statements) are that for some constants , and all large enough,

| (1.9) | |||||

| (1.10) |

with unbounded and a sublevel set. It is noted that one recovers the minorization and drift of (1.7)-(1.8) in the case that is bounded and . We will also invoke a density assumption which is weaker than the upper bound in (1.7). It will be illustrated through examples in Section 4 that (1.9)-(1.10) can be satisfied in circumstances which allow to be non-ergodic. Furthermore, it will also be demonstrated that, in contrast to (1.3), conditions (1.9)-(1.10) can be satisfied with not bounded above, subject to strong enough assumptions on and a restriction on the growth rate of the positive part of .

The main result obtained in the present work (Theorem 3.2 in Section 3) is a bound of the form:

with

where , , , , are constants which are independent of , and and for a real number we denote as the smallest integer such that . In this display is the eigenfunction associated with the principal eigenvalue of and the constant is directly related to the size of the spectral gap of . Verification of the existence of along with various other spectral quantities plays a central role in the proofs.

We note that Del Moral and Doucet (2004); Cérou et al. (2011) also consider the case in which may touch zero and the former are also directly concerned with approximation of the eigenvalue corresponding to via the empirical probability measures . These issues are beyond the scope of the present article but the study of these and related issues in a more general time-inhomogeneous setting is underway. It is also remarked that Cérou et al. (2011) consider a more general type of particle system, which involves an accept/reject evolution mechanism. The approach taken here is also applicable in that context, but for simplicity of presentation we only consider the selection-mutation transition in (1.2).

The remainder of the paper is structured as follows. Section 2 is largely expository: it introduces various spectral definitions and the main assumptions of the present work and goes on to show how these assumptions validate the application of multiplicative ergodicity results of Kontoyiannis and Meyn (2005). It is stressed that much of the content of this section is included in order to make clear the similarities and differences between the setting of interest and the main stated assumptions and results of Kontoyiannis and Meyn (2005). Section 3 deals with the variance bounds for the particle approximations. Numerical examples are given in Section 4. Many of the proofs of the results in Section 2 are in Appendix A. Some proofs and lemmas for the results in Section 3 can be found in Appendix B.

2 Multiplicative Ergodicity

2.1 Notations and Conventions

Let be a state space and be an associated countably generated -algebra. We are typically interested in the case , , but our results are readily applicable in the context of more general non-compact state-spaces. For a weighting function , and a measurable real-valued function on , define the norm and let be the corresponding Banach space. Throughout, when dealing with weighting functions we employ an lower/upper-case convention for exponentiation and write interchangeably .

For a kernel on , a function and a measure denote , and . Let be the collection of probability measures on , and for a given weighting function let denote the subset of such measures such that . For the -fold iterate of is denoted:

The induced operator norm of a linear operator acting is

The spectrum of as an operator on , denoted by , is the set of complex such that does not exist as a bounded linear operator on . The corresponding spectral radius of , denoted by , is given by

where the limit always exists by subadditive arguments, but may be infinite. The following definitions are from Kontoyiannis and Meyn (2005).

-

•

A pole is of finite multiplicity if

-

–

for some we have ,

-

–

and the associated projection operator

can be expressed as a finite linear combination of some and ,

where

-

–

-

•

admits a spectral gap in if there exists such that is finite and contains only poles of finite multiplicity.

-

•

is -uniform if it admits a spectral gap and there exists a unique pole of multiplicity 1, satisfying .

-

•

has a discrete spectrum if for any compact set , is finite and contains only poles of finite multiplicity.

-

•

is -separable if for any there exists a finite rank operator such that

2.2 Multiplicative Ergodic Theorem

In this section we present the main assumptions and state some results from Kontoyiannis and Meyn (2005) (see also Kontoyiannis and Meyn (2003)).

2.2.1 Assumptions

-

(H1)

The semigroup is -irreducible and aperiodic (see Meyn (2006, Section 2.1)).

-

(H2)

There exists an unbounded , constants , and with the following properties:

For each and ,

there exists and such that is -small for , i.e.,

(2.1) with . Furthermore for all .

there exists such that the following multiplicative drift condition holds,

(2.2)

-

(H3)

is such that

-

(H4)

There exists and for each there exists a measure , such that and

where denotes the law of the Markov chain with transition and .

Remark 2.1.

We take care to emphasize the following differences and similarities between the above assumptions and the setting of Kontoyiannis and Meyn (2005).

-

•

Assumption (H(H2)) equation (2.2) applies directly to the kernel, whereas Kontoyiannis and Meyn (2005) impose a multiplicative drift condition on . The key issue is that the multiplicative drift condition for is the essential and implicit ingredient of Lemma B.4 of Kontoyiannis and Meyn (2005), and as we shall see in Section 4, under the conditions that is bounded above but not bounded below, assumption (H(H2)) can hold without geometric drift assumptions on . A related phenomenon is considered by Meyn (2006) in order to obtain “one-sided” large deviation principles for ergodic sample-path averages for the chain with transition .

-

•

Assumption (H(H2)) requires the sublevel sets of to be small for and this is exploited in Lemma A.1. The explicit -step minorisation condition makes it easy to bound below the spectral radius of , see Lemma 2.1. In the setting of Kontoyiannis and Meyn (2003) the spectral radius of is bounded below by as is assumed centered with respect to the invariant probability distribution for . In the present context, this centering assumption is unnatural, especially as we want to consider some situations where such an invariant probability does not exist.

-

•

Assumption (H(H3)) is weaker than the corresponding assumption in the statement of (Kontoyiannis and Meyn, 2005, Theorem 3.1). However, (H(H3)) coincides with the first part of (Kontoyiannis and Meyn, 2005, Equation 73), which combined with (H(H1)), (H(H2)) and (H(H4)) in Lemma 2.2 below, is enough to prove that has a discrete spectrum in .

- •

2.2.2 Results

We now give a collection of results which are used to prove the MET, Theorem 2.2. The proofs are given in Appendix A. It is remarked that the steps in the proof of Theorem 2.2 are effectively the same as part of the proof of Theorem 3.1 of Kontoyiannis and Meyn (2005), however, our starting assumptions are stated differently.

The following preparatory lemma establishes that the Feynman-Kac formula (1.1) is well defined and presents bounds on the spectral radius of .

To clarify how assumptions (H(H1))-(H(H4)) connect with the results of Kontoyiannis and Meyn (2005) we next present a lemma regarding the -separability of which is a stepping stone to the MET. Observe that the multiplicative drift condition (H(H2)) implies that can be approximated in norm to arbitrary precision by truncation to the sublevel sets of , in the sense that for any ,

| (2.5) |

and then with , it follows immediately that . In the following lemma, which combines (Kontoyiannis and Meyn, 2005, Lemmata B.3-B.5) and is included here for completeness, the density assumption (H(H4)) plays a key role in establishing that iterates of this truncation of can be approximated by a finite rank kernel.

The following theorem makes a key connection between -separability and a discrete spectrum.

Theorem 2.1.

(Kontoyiannis and Meyn, 2005, Theorem 3.5) If the linear operator is bounded and is -separable for some , then has a discrete spectrum in .

Under (H(H2)) is indeed bounded, so has a discrete spectrum in and then by definition it also admits a spectral gap in . For any we may consider the resolvent operator defined by

| (2.6) |

We can now state and prove the MET:

Theorem 2.2.

Assume (H(H1))-(H(H4)). Then is a maximal and isolated eigenvalue for . For any and , the operator defined by

| (2.7) |

is bounded as an operator on , with .

The function and measure defined by

| (2.8) |

are independent of and satisfy

Furthermore, there exist constants and such that for any , any and any ,

| (2.9) |

Proof.

We give only a sketch proof, as it is essentially that of Theorem 3.1 of Kontoyiannis and Meyn (2005). As established in Lemma 2.1, under our assumptions . Furthermore the semigroup associated with is -irreducible, and as observed above is bounded on , has a discrete spectrum and therefore admits a spectral gap in . Proposition 2.8 of Kontoyiannis and Meyn (2005) therefore applies. Thus is -uniform and is a maximal and isolated eigenvalue.

By the minorization condition of (H(H2)) one can obtain a minorization condition for of (2.6):

which holds for any . Therefore by the argument in Kontoyiannis and Meyn (2005)[Proof of Proposition 2.8], for any and , the spectral radiue of is strictly less than . Thus is bounded as an operator on and the sum in (2.7) converges in the operator norm.

Then also by (Kontoyiannis and Meyn, 2005)[Proposition 2.8], is an eigenfunction for with eigenvalue . By similar arguments to Kontoyiannis and Meyn (2003)[proof of Proposition 4.5] it is easily verfied that is an eigenmeasure. The normalization to and is justified by the finiteness, under our assumptions, of the associated quantities. By (Kontoyiannis and Meyn, 2003)[Theorem 3.3 part (iii), see also comments on p.332] and constructed using any are respectivaly the -essentially unique eigenfunction and unique eigenmeasure satisfying , , hence the lack of dependence on .

To obtain (2.9) one may define the twisted kernel:

| (2.10) |

which can be seen to be well defined as a Markov kernel, as is strictly positive and finite and (H(H2)) implies is everywhere finite and strictly positive. Furthermore one observes immediately that admits , defined by , as an invariant probability distribution. By Lemma A.1 in Appendix A one can apply Theorem 3.4 of Kontoyiannis and Meyn (2005) to the Markov chain associated to the twisted kernel, (in the notation of of Theorem 3.4 of Kontoyiannis and Meyn (2005), take , ). This results in the bound (2.9), which completes the proof. ∎

Remark 2.2.

3 Non-Asymptotic Variance

3.1 Tensor Product Functionals

The various tensor product functionals considered in the remainder of this paper require some additional notation. For a measurable function on and a weighting function , we define the norm and denote the corresponding function space. For two functions , we denote by the tensor product function defined by . Let be a kernel on . The two-fold tensor product operator corresponding to is defined, for any , by

The iterated operator notation of the previous section is carried over so that

Corresponding to the particle empirical measures of section 1.1, for , we introduce the tensor product empirical measures (or 2-fold statistic):

Following the definition of Cérou et al. (2011), the coalescent integral operator , acting on functions on , is defined by

For any , we denote by the set of coalescent time configurations over a horizon of length and for and , the nonegative measure on , and its normalised counterpart , are defined by

| (3.1) |

for , and for , and . We refer the reader to Cérou et al. (2011, Section 3) for a helpful visual representation of the integrals in the transport equation (3.1). We have already checked in Lemma 2.1 that the Feynman-Kac formula (1.1) is well defined under our assumptions in the setting, which validates the denominator of (3.1).

3.2 Non-Asymptotic Variance

In this section we give our main result. The proof is detailed in section 3.3. The following additional assumption imposes some further restrictions on the function class considered, but this is not overly demanding, considering that we will be dealing with coalesced tensor product quantities.

-

(H5)

Let and be as in assumption (H(H2)). There exists and for all , there exists such that

The following theorem is due to Cérou et al. (2011).

Theorem 3.1.

(Cérou et al., 2011, Proposition 3.4) For any , and the following expansion holds:

| (3.2) |

where denotes expectation w.r.t. the law of the -particle system.

A full proof is not provided here. However, we note that we may write

| (3.3) |

where the equality is due to the lack of bias property and the definition of . In summary, the proof of Theorem 3.1 involves recursive calculation of the expectation on the right of (3.3), followed by organisation of the resulting terms into the form (3.2). The reader is directed to (Cérou et al., 2011) for the details.

It is remarked that there is a different error decomposition in (Chan and Lai, 2011), which can hold to any order under appropriate regularity conditions; one would conjecture that this decomposition can also be treated, but this is not considered here. The main result of this section is the following theorem, whose proof is postponed.

3.3 Construction of the Proof

In the following Section, we detail the argument to prove Theorem 3.2. To that end, we present the essence of the argument with Proposition 3.1 and Lemma 3.1 below; the proofs of which are in Appendix B along with some supporting results.

The proof of Theorem 3.2 is constructed in the following manner. By Theorem 3.1 we have the decomposition (3.2) in terms of the operators . The proof in Cérou et al. (2011) focuses upon controlling these expressions via the regularity conditions mentioned in section 1.2; our proof will do the same, except under (H(H1))-(H(H5)).

Throughout the remainder of this paper, let is defined by

| (3.4) |

where is as in (H(H5)). We proceed with the following key proposition.

Proposition 3.1.

Assume (H(H1))-(H(H5)). Then there exists depending only on the quantities in (H(H1))-(H(H5)) such that for all , , and ,

| (3.5) |

with the conventions that the product in the numerator is unity when , and in the case of . In the above display, is as in (H(H2)), is the eigenfunction as in Theorem 2.2 and is as in (3.4).

This result of Proposition 3.1 connects the operators with expectations of the Lyapunov functions and and the eigenfunction, w.r.t. the twisted chain. Given this result, one needs to control the numerator and denominator. The latter can be achieved by the MET of Theorem 2.2 and the former via the following:

Lemma 3.1.

We now proceed with the proof of Theorem 3.2.

Proof.

[Proof of Theorem 3.2] By Proposition 3.1 and Lemma 3.1 we have that there exists a finite constant depending only on the quantities in (H(H1))-(H(H5)) such that

| (3.7) |

Using the fact that we appeal to (2.9) of the MET of Theorem 2.2 as follows. Without loss of generality, it can be assumed that . Then for all

| (3.8) |

Throughout the remainder of the proof the left-most inequality in (3.8) is assumed to hold. Then combining (3.8) with (3.7) and recalling the definition of we have that there exists such that

Proceeding by the essentially the same argument as in (Cérou et al., 2011, Proof of Theorem 5.1), we use the identity:

which holds for any and , to establish via Theorem 3.1 that

Then exactly as in (Cérou et al., 2011, Proof of Corollary 5.2),

This completes the proof. ∎

4 Examples

This section gives some discussion and examples of circumstances in which the assumptions can be satisfied. In particular we focus on the drift assumption of (H(H2)). It seems natural to consider two general cases: those in which it is not assumed, or it is assumed, that the Markov kernel itself satisfies a multiplicative drift condition.

4.1 Cases without a multiplicative drift assumption on

In this situation, the decay of the potential function plays a key role in establishing the multiplicative drift condition, illustrated as follows.

Lemma 4.1.

Assume that there exists unbounded such that and for all , is -small for , with and for all . If for all , , and there exists such that and for some , , assumption (H(H2)) is satisfied.

Proof.

We have

As is unbounded, for any there exists large enough such that for all and ,

which is enough to verify the drift part of (A2). The minorization condition with and the part are direct as is bounded below on . ∎

In the extensive literature on Lyapunov drift for Markov kernels there are several conditions which immediately guarantee the existence of such that . For example, any satisfying the polynomial drift condition of Jarner and Roberts (2002) automatically satisfies for the same up to a factor of . However, ergodicity of is not necessary, as illustrated in the following simple example.

4.1.1 Gaussian Random Walk

Let and and be defined by

where denotes Lebesgue measure. Taking as Lebesgue measure, the -irreducibility and aperiodicity of is immediate. For the drift and minorization conditions of (H(H2)), elementary manipulations show that equation (2.2) holds with for suitable and solutions of the minorization condition (2.1) are also easily obtained. Condition (H(H3)) is trivially satisfied because is non-positive. The density assumption (H(H4)) is satisfied with proportional to the restriction of Lebesgue measure to . Assumption (H(H5)) holds for small enough and .

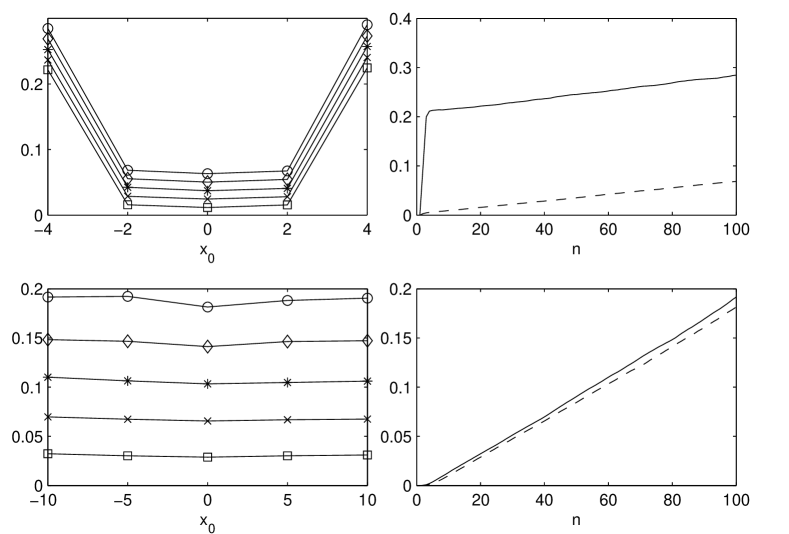

It is generally not easy to obtain or estimate values for the constants in Theorem 3.2. In all the numerical examples which follow, we consider a fixed value of and consider the relative variance as a function of the and the initial condition .

The numerical results of Figure 4.1 show estimates of with fixed , for various and , with in each case the expectation approximated by averaging over independent simulations of the particle system. For this model can be computed analytically, and this exact value was used in the estimates. The linear growth of the relative variance and its dependence on the initial point is apparent from the figure.

4.2 Cases with a multiplicative drift assumption on

The following Lemma shows that condition (H(H2)) holds for suitable when itself satisfies a multiplicative drift condition.

Lemma 4.2.

Assume that there exists unbounded, , and for each there exists such that

| (4.1) |

and the set is -small for , with and for all . Then if , and for all finite , , assumption (H(H2)) holds.

Proof.

4.2.1 Ergodic Autoregression

Let and and be defined by

for fixed . Elementary manipulations then show that, for and large enough, satisfies (4.1) with . As per the random walk example, readily admits minorization on the sublevel sets .

The potential function clearly satisfies (H(H3)). Lemma 4.2 shows that (H(H2)) is satisfied. The density assumption (H(H4)) is satisfied for proportional to Lebesgue measure restricted to . Again it is straightforward to check that (H(H5)) is satisfied for small enough and .

Figure 4.1 also shows estimates of the relative variance obtained by simulation for this model with and using particles, averaged over independent realizations. Again the linear growth of the variance is apparent, but there appears to be less variation with respect to the initial condition than in the random walk example.

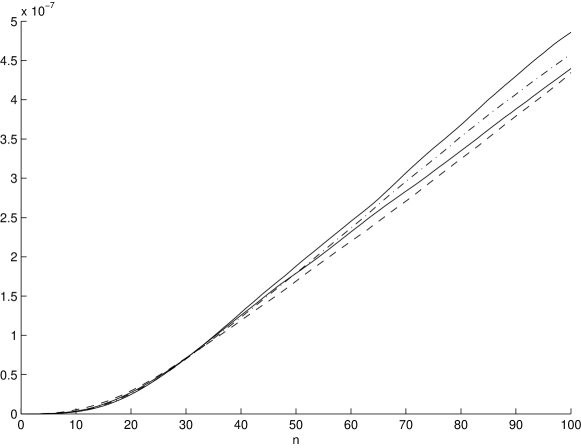

4.2.2 Cox-Ingersoll-Ross Process

The Cox-Ingersoll-Ross (CIR) process, (Cox et al., 1985), is a diffusion process that is typically used in financial applications to capture mean-reverting behaviour and state-dependent volatility, which is thought to occur in many real scenarios. The process is defined via the stochastic differential equation:

where is standard Brownian motion, is the mean-reversion rate, is the level of mean-reversion and is the volatility. We assume that so that the process is stationary and never touches zero.

Throughout the remainder of section 4.2.2, for we denote by the transition probability from any time to of the CIR process with parameters . The following lemma identifies a drift function for , exhibiting a trade-off between growth rate of the drift function specified by a parameter , the parameters of the CIR process and the time step size .

Lemma 4.3.

For and , consider the candidate drift function , defined by

| (4.2) |

Then subject to the conditions:

| (4.3) |

the following multiplicative drift condition is satisfied:

with as in (4.2) and .

Proof.

For define

and the scaled process . Conditional on , has a non-central chi-square distribution with degree of freedom and non-centrality parameter taking the value (Cox et al., 1985). We then have for any ,

where the equalities hold due to the existence of the moment generating function , for , which is satisfied under the conditions of (4.3). Under these conditions we also then have for and ,

and for ,

∎

We will consider as an example the case where the Markov chain is the skeleton of the CIR process over a discrete time grid of spacing and for some fixed . Lemmata 4.2 and 4.3 establish that (H(H2))-(H(H3)) are satisfied and one can check (H(H4))-(H(H5)) are satisfied similarly to the previous example.

Figure 4.2 displays estimates of the relative variance for this model, computed via simulation, when , (i.e. ), , , , and . This was obtained using particles, averaged over independent realizations. Again the linear growth of the relative variance is present for different initial conditions. Note one may interpret as the geometric mean , which can be used for prediction in a variety of financial applications.

5 Summary

In this paper we have established a linear-in- bound on the non-asymptotic variance associated with particle approximations of time-homogeneous Feynman-Kac formulae, under assumptions that can be verified on non-compact state-spaces.

There are several possible extensions to this work. Firstly, to consider non-homogeneous Feynman-Kac formulae, which occur routinely in applications such as filtering and Bayesian statistics. Secondly, an important developing area in the analysis of sequential Monte Carlo methods is the case when the dimension of the state-space can be very large (Beskos et al., 2011). Such analysis has relied on classical geometric drift conditions and it would be interesting to consider the role of multiplicative drift conditions in this context.

Acknowledgements

We would like to thank the associate editor and the referee for some very useful comments that have lead to considerable improvements in the paper. The first and third authors acknowledge the assistance of the London Mathematical Society for their funding, via a research in pairs grant. The second author was supported by the EPSRC programme grant on Control For Energy and Sustainability EP/G066477/1.

Appendix A Proofs and Auxiliary Results for Section 2

Proof.

[Proof of Lemma 2.1] Fix any . The upper bound of (2.3) is an immediate consequence of the inequality , implied by (2.2).

For the upper bound of (2.4), use the standard inequality and then also due to the drift condition in (2.2), . Now consider the lower bound. It is claimed that for any and ,

| (A.1) |

where is as in (H(H2)). For each , the claim is verified by induction in ; fix arbitrarily. For ,

which initializes the induction. Now assume that (A.1) holds at rank . Then at rank , applying the induction hypothesis

where (2.1) has been applied, thus the claim is verified.

Proof.

[Proof of Lemma 2.2] Set arbitrarily and let . For , denote by the -fold iterate of .

Then under (H(H3)),

and therefore under (H(H4)),

| (A.2) |

Lemma B3 of (Kontoyiannis and Meyn, 2005) then implies that is -separable.

In order to establish that is -separable, we will prove that can be made arbitrarily small through suitable choice of . By decomposing the difference in a telescoping fashion and applying the sub-additive and sub-multiplicative properties of the operator norm we obtain:

| (A.3) |

Now for any , , where the final inequality follows from equation (2.3) of Lemma 2.1, and by (2.5) we have as . Therefore it follows from (A.3) that as , so we conclude that is -separable. This completes the proof. ∎

The following lemma considers the twisted kernel defined in (2.10).

Lemma A.1.

Proof.

Under the assumptions of the lemma, we have already seen via (Kontoyiannis and Meyn, 2005, Proposition 2.8) that the twisted kernel is well defined. First consider, (A.4); under (H(H2)), setting , for any ,

As is unbounded, there exists such that for all , equation (A.4) holds with .

Appendix B Proofs and Auxiliary Results for Section 3

In this appendix we detail the proofs and auxiliary results that are used in Section 3. The proofs and results are provided in a logical order; that is, each result at most depends on the preceding one(s). In particular, the proof of Lemma 3.1 follows the proof of Lemma B.1.

Lemma B.1.

Proof.

Under the assumptions of the lemma, Theorem 2.2 holds, the eigenfunction , and the twisted kernel is well defined. Then under (H(H5)), we have for any ,

As is unbounded, there exists such that for all , equation (B.1) holds with . The proof of (B.2) then follows exactly as in the proof of Lemma A.1. ∎

Proof.

[Proof of Lemma 3.1] We first consider some bounds on iterates of the twisted kernel. Standard iteration of the geometric drift condition in equation (B.2) shows that there exists a finite constant such that

| (B.3) |

and then due to the multiplicative drift condition in equation (B.1),

| (B.4) |

where .

In order to prove (3.6) first fix arbitrarily , and . The proof is via a backward inductive argument through the coalescent time indices. Assume that at rank ,

| (B.5) |

Assuming (B.5) is true, then at rank ,

where the final inequality is due to equation (B.4). Furthermore

where the inequality is again due to (B.4) and therefore at rank ,

The above arguments prove that (B.5) holds at rank and the proof of the Lemma is then also complete as , and were arbitrary. ∎

Lemma B.2.

Proof.

By standard iteration of the geometric drift condition in equation (A.6) of Lemma A.1, there is a finite constant such that

| (B.7) |

Then due to the definition of the twisted kernel and (see Lemma A.1), there exists a constant such that for any , and ,

| (B.8) | |||||

where the final inequality is due to (B.7). ∎

Lemma B.3.

Proof.

Throughout the proof is a finite constant whose value may change on each appearance.

When ,

where the first inequality is due to Lemma B.2 and the second inequality is due to the definition of .

Proof.

[Proof of Proposition 3.1] The starting point of the proof is to write, using the definition of the twisted kernel,

Thus in order prove (3.5), we need to prove

| (B.9) |

for each , and each possible configuration of the coalescent time indices . We will consider first the case and then . Throughout the remainder of the proof, denotes a finite and positive constant, whose value may change on each appearance but depends only on the constants in (H(H1))-(H(H5)).

Consider the case . It is claimed that there exists a finite constant such that for any , , , and any ,

| (B.10) |

with the convention that the product is equal to unity when . For a given , the claim is proved by backward induction through the coalescent time indices. The inductive hypothesis is that at rank ,

| (B.11) |

with the convention that the product equals unity when .

To initialise the induction, we have at rank that the left hand side of (B.11) is

and Lemma B.3 then shows immediately that (B.11) does indeed hold at rank . We point out that the constraint in the statement of the proposition is imposed because in the case we immediately encounter , and we can control integrals involving using the drift conditions, as in Lemma B.3. If we were to give a separate treatment of for coalescent time configurations in which , the constraint on could be relaxed to a larger function class.

Proceeding with the induction, when the hypothesis (B.11) holds at rank , we have at rank :

where the inequality follows from applying the induction hypothesis, then multiplying by and then applying Lemma B.2 with the -dependent part of the right hand side of (B.11). This concludes the inductive proof of (B.10).

Consider the case . Multiplying the right hand side of (B.10) by and recalling the definition of and , we immediately obtain (B.9), as desired. In the case , we multiply (B.10) by and apply Lemma B.2 in a similar fashion as before to yield

so again we obtain (B.9) as desired. This completes the treatment of the case .

References

- Beskos et al. (2011) A. Beskos, D. Crisan, and A. Jasra. On the stability of sequential Monte Carlo methods in high-dimensions. 2011.

- Cérou et al. (2011) F. Cérou, P. Del Moral, and A Guyader. A nonasymptotic variance theorem for unnormalized Feynman Kac particle models. Annales de l’Institut Henri Poincaré, 47(3), 2011.

- Chan and Lai (2011) H. P. Chan and T. Lai. A sequential Monte Carlo approach to computing tail probabilities in stochastic models. The Annals of Applied Probability, 14(1):(to appear), 2011.

- Chopin et al. (2011) N. Chopin, P. Del Moral, and S. Rubenthaler. Stability of Feynman Kac formulae with path-dependent potentials. Stochastic Processes and their Applications, 121(1):38–60, 2011.

- Cox et al. (1985) J.C. Cox, J.E. Ingersoll Jr, and S.A. Ross. A theory of the term structure of interest rates. Econometrica, 7(2):385–407, 1985.

- Crisan and Bain (2008) D. Crisan and A. Bain. Fundamentals of Stochastic Filtering. Stochastic Modelling and Applied Probability. Springer, 2008.

- Del Moral (2004) P. Del Moral. Feynman-Kac Formulae. Genealogical and interacting particle systems with applications. Probability and its Applications. Springer Verlag, New York, 2004.

- Del Moral and Doucet (2004) P. Del Moral and A. Doucet. Particle motions in absorbing medium with hard and soft obstacles. Stochastic Analysis and Applications, 22:1175–1207, 2004.

- Del Moral and Guionnet (2001) P. Del Moral and A. Guionnet. On the stability of interacting processes with applications to filtering and genetic algorithms. Annales de l’Institut Henri Poincaré (B) Probability and Statistics, 37(2):155–194, 2001.

- Del Moral and Miclo (2003) P. Del Moral and L. Miclo. Particle approximations of Lyapunov exponents connected to Schrödinger operators and Feynman Kac semigroups. ESAIM: Probability and Statistics, 7:171– 208, March 2003.

- Del Moral et al. (2009) P. Del Moral, F. Patras, and S. Rubenthaler. Tree based functional expansions for Feynman Kac particle models. Annals of Applied Probability, 19(2):778–825, 2009.

- Del Moral et al. (2011) P. Del Moral, A. Doucet, and A. Jasra. On adaptive resampling strategies for sequential Monte Carlo methods. Bernoulli, 2011. To appear.

- Di Masi and Stettner (1999) G. B. Di Masi and L. Stettner. Risk-sensitive control of discrete-time Markov processes with infinite horizon. SIAM J. Control Optim., 38:61–78, November 1999.

- Doucet et al. (2001) A. Doucet, N. De Freitas, and N. Gordon, editors. Sequential Monte Carlo methods in practice. Springer, New York, 2001.

- Jarner and Roberts (2002) S.F. Jarner and G.O. Roberts. Polynomial convergence rates of Markov chains. Annals of Applied Probability, 12(1):224–247, 2002.

- Jasra and Del Moral (2011) A. Jasra and P. Del Moral. Sequential Monte Carlo methods for option pricing. Stochastic Analysis and Applications, 29(2):292–317, 2011.

- Jasra and Doucet (2009) A. Jasra and A. Doucet. Sequential Monte Carlo methods for diffusion processes. Proceedings of the Royal Society A, 465:3709–3727, 2009.

- Kontoyiannis and Meyn (2003) I. Kontoyiannis and S.P. Meyn. Spectral theory and limit theorems for geometrically ergodic Markov processes. The Annals of Applied Probability, 13(1):304–362, 2003.

- Kontoyiannis and Meyn (2005) I. Kontoyiannis and S.P. Meyn. Large deviation asymptotics and the spectral theory of multiplicatively regular Markov processes. Electronic Journal of Probability, 10(3):61–123, 2005.

- Le Gland and Oudjane (2004) F. Le Gland and N. Oudjane. Stability and uniform approximation of nonlinear filters using the Hilbert metric and application to particle filter. The Annals of Applied Probability, 14(1):144–187, 2004.

- Meyn and Tweedie (2009) S. Meyn and R L. Tweedie. Markov Chains and Stochastic Stability. Cambridge University Press, 2nd edition, 2009.

- Meyn (2006) S.P. Meyn. Large deviation asymptotics and control variates for simulating large functions. Annals of Applied Probability, 16(1):310–339, 2006.

- Nummelin (2004) E. Nummelin. General irreducible Markov chains and non-negative operators. Cambridge Tracts in Mathematics. Cambridge University Press, 2004.

- van Handel (2009) R. van Handel. Uniform time average consistency of Monte Carlo particle filters. Stochastic Processes and their Applications, 119(11):3835–3861, 2009.

- Whittle (1990) P. Whittle. Risk-Sensitive Optimal Control. John Wiley and Sons, 1990.