Multiplicative Asset Exchange with Arbitrary Return Distributions

Abstract

The conservative wealth-exchange process derived from trade interactions is modeled as a multiplicative stochastic transference of value, where each interaction multiplies the wealth of the poorest of the two intervening agents by a random gain , with a random return. Analyzing the kinetic equation for the wealth distribution , general properties are derived for arbitrary return distributions . If the geometrical average of the gain is larger than one, i.e. if , in the long time limit a nontrivial equilibrium wealth distribution is attained. Whenever , on the other hand, Wealth Condensation occurs, meaning that a single agent gets the whole wealth in the long run. This concentration phenomenon happens even if the average return of the poor agent is positive. In the stable phase, behaves as for , and we find exactly. This exponent is nonzero in the stable phase but goes to zero on approach to the condensation interface. The exact wealth distribution can be obtained analytically for the particular case of Kelly betting, and it turns out to be an exponential . We show, however, that our model is never reversible, no matter what is. In the condensing phase, the wealth of an agent with relative rank is found to be for finite times . The wealth distribution is consequently for finite times, while all wealth ends up in the hands of the richest agent for large times. Numerical simulations are carried out, and found to satisfactorily compare with the above mentioned analytic results.

1 Multiplicative Trade model

The pervasive existence of inequalities in the distribution of wealth

in human societies has puzzled observers since long, but only recently

became a focus of research by physicists [1]. The

observation of a power-law distribution for wealth and income in

capitalist societies, originally made by Pareto [2], has

been confirmed and perfected analyzing extensive sets of data that are

nowadays available. These show that the upper five to ten percent of

richest individuals follow a power-law, while the middle to low income

sector of a population follow a Gibbs or lognormal

law [3, 1, 4]. The range of typical wealth

variation may be orders of magnitude larger than the natural

variability in individual abilities and capacities, in case one would

attempt to resort to these in order to explain the former. Clearly, it

is of interest to understand what mechanisms may drive the appearance

of such startling differences. Apart from the fact that wealthier

individuals or entities have, on average, more political power to

influence their social environment to their advantage, thus producing

a self-reinforcing inequality cascade, it is also valid to ask oneself

whether the microscopic mechanisms of wealth production and

redistribution carry within themselves the property of spontaneously

producing inequality.

In a pioneering work [5], Angle proposed the use of

conservative wealth exchange models in order to explain wealth

inequalities. He envisaged the wealth exchange process as a stochastic

transfer of “surplus”, in which the looser transfers a random

fraction of its wealth to the winner. This is nowadays called

the “looser scheme” since it is a fraction of the looser’s wealth

what is at stake [6]. If both interacting agents are

assumed to win with the same probability, then such a process avoids

wealth concentration by favoring the poorest agent, because he risks

to loose less than he can win. Aiming to understand the observed

wealth concentration, Angle then argues that the richer agent, because

of the competitive advantage allowed by his larger wealth, usually has

a larger probability of winning in each encounter. Therefore, in the

context of Angle’s initial proposal, wealth concentration is a

consequence of an explicit advantage, or edge favoring

the richer agent 222An agent is said to have an edge when the

expectation value of a single trade favors him..

Although being richer does provide an advantage in the context of

certain wealth appropriation processes, it is now

recognized [7, 8] that, from a statistical point of

view, an explicit advantage favoring the rich is not a

necessary ingredient for wealth concentration to happen. This is a

remarkable result that only recently has been stressed in the

Econophysics literature. For certain realistic wealth exchange rules

to be discussed in this work, in the long run all wealth may end up in

the hands of just one agent, even if the poor agent has an edge over

the rich one. The key ingredient for this rather counterintuitive

phenomenon is the fact that the amount at stake in each transaction is

a fraction of the poorest agent’s

wealth [6, 7, 9, 10, 8], not of the

looser’s wealth. This apparently minor difference in the rules of

these so-called “poorest scheme” models profoundly alters the

outcome, as now the poor agent has to be given an explicit advantage

in order to avoid a catastrophic concentration of wealth called Wealth

Condensation. In other words, multiplicative stochastic transfer whose

scale is dictated by the wealth of the poorest intervening agent

implies a “hidden” bias in favor of the rich. This is one of the

statistical factors driving wealth concentration.

On the other hand, it can be generally argued that stochastic

multiplicative “poorest scheme” transfer rules constitute an

appropriate simple model of the wealth exchange process occurring

during commercial interaction, or trade [7, 10].

Wealth transfer occurs in a trade operation not because money changes

hands, which is not necessarily always the case, but as a consequence

of the difference in values between the items swapped. This confers

the interaction a clear stochastic character, as none of the agents is

perfectly aware of the true values of the items being interchanged.

Furthermore, it can be argued that the amount at stake must be

proportional to the wealth of the poorest agent, since an interaction

in which the richest agent has the possibility to loose orders of

magnitude more than he can win cannot be considered realistic if one

wishes to reproduce a consensual trade process [7, 10].

In this work, an analytic and numerical study is presented of wealth

exchange models in which the transference is stochastic,

multiplicative and proportional to the poorest agent’s wealth. In each

interaction, the poor agent risks a fraction of its wealth,

where is a random variable called the return. Scafetta,

Picozzi and West [10] have numerically studied a model of

this type in which the return distribution depends on the wealths of

both intervening agents. In order to simplify the derivation of

analytic results, we restrict ourselves to the case in which the

distribution or returns is the same for all pairs of

agents.

2 Trading with an arbitrary distribution of returns

2.1 The model

Trade interactions are modeled as a process in which wealth is stochastically transferred between a pair of agents, according to the following rules. In each transaction a pair of agents is chosen at random and the poorest one, initially with wealth , receives a gain , where is a random return with distribution . The richest agent’s wealth changes by . The transaction is thus conservative, and given by

| (1) |

The condition ensures that both agents have positive

wealth after the trade.

Yard-Sale [7, 11, 9, 8] is a particular case

of this process that can be described as a “bet” for a fraction

of the wealth of the poorest agent, and where the poorest agent has a

probability to win. Therefore with probability and

with probability , so .

2.2 Wealth Condensation

Depending on , long term evolution under rules (1) may give rise either to a stable wealth distribution or to wealth condensation [8]. The surface consisting of distributions separating these two cases is called condensation interface. We now derive the location of this interface as follows: Consider an agent who has become so poor that, in most subsequent trades he will be the poorest. His own wealth will thus almost always evolve according to

| (2) |

i.e. it will undergo a Random Multiplicative Process [12] with multiplier at each timestep. After a large number of timesteps, the appropriate central tendency estimator for its wealth is therefore not the arithmetic average

| (3) |

but the geometric average

| (4) |

Clearly the wealth of a poor agent will diminish steadily if , in which case there is a sustained transference of wealth from poorer to richer agents, the system is in a condensing phase, and the whole wealth ends up in the hands of one agent in the long run [8]. This catastrophic collapse of the wealth distribution is called wealth condensation. By the heuristic arguments above, the condensation interface is therefore defined by

| (5) |

This result will be rederived later in Section 3.3 by means of a rigorous analysis of the kinetic equation for this process.

3 Kinetic Equation Analysis

3.1 Kinetic Equation in the Stationary Limit

In A we show that the equilibrium wealth distribution satisfies

| (6) |

where is the fraction of agents with wealth above , and indicates expectation value with respect to the return distribution . The first and second terms on the right hand side of (6) represent the contributions of exchanges with agents that have a wealth respectively larger and smaller than . This equation can be solved exactly only for special cases that we discuss later in Section 3.4. In the general case, however, useful exact results can still be extracted from it, as described next.

3.2 Small-wealth limit for

The small-wealth behavior of the wealth distribution in the stable phase can be derived as follows. Assume for . Plug this expression into the stationary kinetic equation (6), approximate for small , and notice that the last integral only contributes higher order terms, to find

| (7) |

This result can be rationalized by referring to Kesten

processes [13, 14, 15], as discussed in

Section 5. Numerical results to be presented later in

Section 4 support the validity of Eq. (7) in the

limit of small wealth.

Numerical simulation (Section 4) shows that, using

the value of resulting from (7), the entire wealth

distribution can be approximated by a gamma-function

| (8) |

where the normalization conditions on the zeroth and first moments of fix , and . Notice, however, that the wealth distribution (see Figs. 1 and 2) is not exactly given by (8), except in special cases.

3.3 Condensation interface

Equation (7) allows us to determine the location of the condensation interface by the following rigorous argument. Given that for , the fraction of agents whose wealth is below an arbitrarily small but finite level is finite for all , but diverges as . The divergence of indicates that most agents impoverish absolutely, equivalently that all wealth concentrates in the hands of a few ones. Therefore, the condensation interface is defined by the condition . Now rewrite (7) as and expand it in powers of to obtain

| (9) |

After eliminating the trivial solution , we are left with

| (10) |

Therefore, to lowest order,

| (11) |

We thus find that the condensation condition amounts to

, which is the same as Eq. (5),

derived previously by analyzing the typical behavior of a poor agent’s

wealth.

For the case of Yard-Sale, where with probabilities

and , the condensation interface (5) is

given by , a result that has

been verified numerically [8]. Notice that ,

i.e. the poor has to be given a significant explicit advantage, or

edge, in order for condensation not to occur.

For a flat distribution of returns between two limits , on the other hand, the critical condition for condensation reads

| (12) |

Here again, notice that it is possible to have condensation even when the average return of the poor agent, which is , is positive.

3.4 Exponential Solution and Kelly Betting

We now show that, for certain return distributions , the equilibrium wealth distribution is exponential. For this we replace into (6), and get

| (13) |

which is a sufficient condition for the stable wealth distribution to be exponential. Particularized to , this condition reduces to , which is just Eq. (7) in the case , as appropriate for an exponential distribution. However, notice that (13) is much more restrictive than just (7) with , because it has to be satisfied for all . Trivially, if two return distributions and satisfy (13), so does any normalized linear combination of them. Therefore, a meaningful approach to solving (13) consists in first finding simple return distributions which satisfy it, and then building more general ones by linear combination. Proposing a binary distribution , one finds that Eq. (13) is only satisfied if and, additionally, , that is

| (14) |

This return distribution corresponds to Yard-Sale [8] but particularized to the case of Kelly betting [16, 17], which fixes . Possible implications of this result are explored in Section 5.

3.5 More general return distributions with exponential solutions

3.6 Wealths by rank in the condensing phase

Let be the wealths of the agents ordered by rank , so that . When an agent with rank interacts with another agent with rank , we have

| (17) |

Notice that (17) is not valid in general, since it disregards rank changes resulting from interactions. Its validity is restricted to the case in which agents keep fairly constant ranks, i.e. there is no “social mobility”. This holds in the condensed phase, but not in the stable phase. In the condensed phase, furthermore, one has so that the interaction with poorer agents can be neglected altogether, to write

| (18) |

Averaging over , over all possible choices of , and defining the relative rank so that corresponds the richest agent,

| (19) |

The typical value of therefore satisfies

| (20) |

where we have defined . Normalization for a system of agents with a total wealth then results in

| (21) |

Now since we have that . From (20) we thus obtain

| (22) |

The validity of (20) and (22) is verified for uniformly distributed returns in Section 4.

4 Numerical Results

4.1 Stable phase

a)  b)

b)

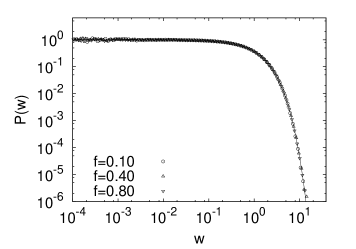

We first consider the case of Yard-Sale exchange [8], i.e. . Eq. (7) amounts in this case to

| (23) |

Some particular cases of interest are

| (24) | |||||

| (25) | |||||

| (26) |

Eq. (24) defines the condensation interface. Its accuracy has been

numerically verified in previous work [8].

Fig. 1a shows wealth distributions for three values of

, where is given by (25), and therefore correspond

to , i.e. should be constant for . Notice that all

values of in this figure satisfy . This is consistent

with the results derived in Section 3.4, namely

that the wealth distribution is exponential whenever is

satisfied. So in this case, for any pair satisfying

(25) the wealth distribution is the same. For , the

wealth distribution should approach the origin as . This

is verified by considering the data shown in Fig. 1b,

obtained with given by (26). However, in this case,

notice that the wealth distribution does depend on , i.e. the

asymptotic exponent does not determine the whole distribution. A

similar observation holds for the rest of the plane: the

equilibrium distribution depends on on all lines of constant ,

except on the line , where and .

a)  b)

b)

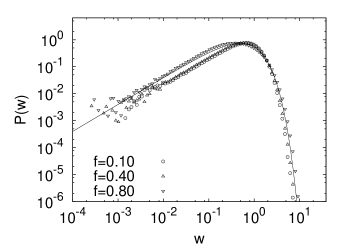

Let us now consider a flat return distribution for , where . This last condition ensures that the gain lies between zero and two, and therefore that both agents can always pay. Eq. (7) can be worked out exactly also in this case, and the result is

| (27) |

We consider the following particular cases

| (28) | |||||

| (29) | |||||

| (30) |

The condensation interface has been obtained numerically (not shown)

and found to be in accordance with (28). In the case of

, Eq. (29) can be shown to be equivalent to writing and , where is a free

parameter restricted to . We have

simulated flat return distributions with and given by the

expressions above with several values of (Fig. 2a),

and found wealth distributions consistent with in all cases,

i.e. reaching as a constant. Notice that only in the limit , in which case , the distribution approaches an

exponential. When , Eq. (30) amounts to letting ,

within the limits given by . Examples are shown in

Fig. 2b, where again good accordance with analytic

predictions for the small-wealth exponent is found.

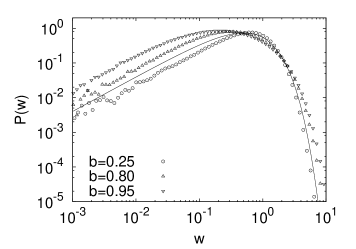

4.2 Condensed phase

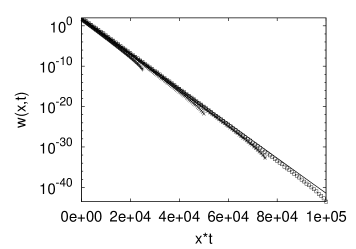

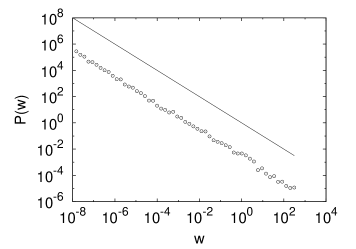

We now verify the approximate expression (20), derived in Section 3.6, for the wealth of an agent with relative rank in the condensing state. Fig. 3a shows for returns distributed uniformly between and . Therefore , and the system is in the condensing state. The analytic prediction given by (20) is seen in this case to be acceptable, except perhaps for the very poorest agents. Accordingly, the wealth distribution obtained in this condensing state is, as shown in Fig. 3b, consistent with as derived in Section 3.6.

a)  b)

b)

5 Discussion

Multiplicative “poorest-scheme” asset-exchange models with an

arbitrary return distribution were studied, analyzing

the kinetic equation (6). It was shown that the the whole

system’s wealth “condenses” onto one agent whenever

. Given that , it is possible to have

, and therefore wealth condensation, even in

cases in which the average return is positive. But

having a positive average return means, according to (3),

that the expectation value of a poor agent’s wealth grows

exponentially in time. The apparent paradox suggested by the fact

that poor agents loose wealth steadily despite their average return

being positive is solved by recognizing that the expectation value is

not an appropriate central-tendency estimator when considering

multiplicative processes [12]. In other words, while the

exponential growth indicated by (3) would only be realized

after averaging over an enormously large number of repetitions of the

multiplicative process, the typical outcome of one realization follows

the geometric average (4), which, in the condensing phase,

decreases exponentially fast in time.

Analyzing the kinetic equation, the small-wealth exponent of

, was found to be given by Eq. (7). This result can be

understood in the context of Kesten

processes [13, 14, 15], as follows. In the stable

phase, where , the inverse wealth

of a poor agent undergoes a contractive multiplicative process

due to its interaction with richer

agents, with a small additive noise term given by its almost

negligible interaction with poorer agents, as . Because in the stable phase , it follows that

. The theory of Kesten processes then ensures

that has a power-law right tail of the form with

satisfying . By a simple change of variables, our

result (7) then follows for .

In Section 3.4 it was shown that the wealth

distribution is exactly exponential when corresponds to

Kelly betting [16, 17]. Kelly betting is a gambling

strategy devised to maximize the long-time rate of growth of a

bettor’s capital when faced with a set of risky choices. In its

simplest inception, one considers a gambler who is given a choice

between a single risky asset (a bet) and a riskless asset

(e.g. deciding not to bet). Assuming a bet that pays double or

nothing, the gambler doubles its stake or looses it altogether,

respectively with probabilities and . The bettor can decide

the (fixed) fraction of his wealth that will be risked at each

time step, while the rest is kept in the riskless asset

(e.g. cash). His total wealth thus evolves as if the bet is won, and as if the bet is

lost. In other words, the gambler’s gain is with

probability , and with probability . This is

exactly the way in which the wealth of the poorest agent evolves in

Yard-Sale. The only difference is the fact that, in the betting

optimization problem, and are not independent parameters,

since the gambler wishes to find the most profitable for a given

.

The average gain is , which is

larger than one whenever , i.e whenever the edge

is positive. If the bettor were to maximize ,

the recommended strategy would then be choosing as large as

possible 333 In this context, may be acceptable and would

mean that the gambler lends money from the riskless asset for

gambling. . However, this approach is doomed to fail in the long

run, since sooner or later a loosing bet would produce his absolute

ruin. Kelly then proposes that the most profitable strategy in

the long run consists in using the value of maximizing the

average growth rate of the gambler’s wealth, defined by . The average growth rate is then given by the average

logarithmic gain , since a random multiplicative

process typically follows its geometric average. Maximization of

with respect to

then results in , which is the recommendation of Kelly

theory for this problem. Equivalently, and ,

from which we can recognize that (14) describes Yard-Sale

exchange in the case of Kelly betting.

From the discussion above, is the fraction at stake that

produces the fastest growth in the wealth of a poor agent, for a given

. However, notice that this is not the value of that produces

the least density of poor agents in Yard-Sale for a given . The

density of poor agents in Yard-Sale in equilibrium is minimum in the

limit , for any fixed . This conclusion may be reached by

noticing that the fraction of poor agents is smaller the larger is

and analyzing (7) particularized to Yard-Sale, in the limit

.

The link between Kelly betting and an exponential wealth distribution

in these exchange models is intriguing. The Kelly strategy can be

restated in the language of information theory as a way to maximize

the rate of transfer of information over a noisy

channel [16]. On the other hand, the exponential distribution

maximizes the entropy

subject to the constraints of constant total wealth

and number of players . Of course, there is in

principle no logical relation between extremization of an entropy

transfer rate, and maximizing the total entropy in equilibrium,

however the connection seems worth analyzing.

Because the dynamics is conservative, if the microscopic exchange

rules are reversible it can be shown [18] that the

equilibrium wealth distribution has to be exponential. However, the

converse is of course not true, i.e. the existence of a stable

exponential solution does not imply reversibility. In fact,

multiplicative exchange rules of the type discussed here usually

violate reversibility, since the role of both agents is clearly

different. Nevertheless, it could in principle be the case that, for

some specific return distributions, the general exchange rules

considered here were reversible. This in turn would provide a clearcut

explanation for the appearance of an exponential solution. However,

in B it is shown that this is not the case,

i.e. reversibility is not satisfied for exchange rules of the general

type (1), no matter what the return distribution

is. Therefore, the wealth distribution in equilibrium

is exponential for return distributions of the form (14), not

because of reversibility, but because of accidental cancellation of

asymmetries in the transition rules.

Appendix A Kinetic Equation

Consider an interaction between two agents and with initial wealths and , assuming without loss of generality . The interaction processes contributing to are those in which is the wealth of one of the two interacting agents, either before or after the interaction. Adopting the shorthand notation , , and , one has:

-

1.

The poorest agent has a return , its wealth thus becoming . This contributes with .

-

2.

The richest agent takes part in an exchange where the poorest agent has return . ’s wealth becomes . The contribution of this process is .

-

3.

Either agent has wealth before the interaction, but not after it, resulting in a contribution .

If is the probability per unit time of a trade, the time derivative of is then given by

| (31) | |||||

Letting , we are left with

| (32) |

It can be seen that this equation conserves the zeroth- and first-moments of , i.e. number of agents and total wealth are conserved.

Appendix B Reversibility

We wish to determine whether the exchange rules considered in this work satisfy reversibility for some return distribution . For this purpose we have to write the kinetic equation in the general form

| (33) |

and check whether is satisfied. A lengthy but straightforward calculation shows that

| (34) | |||||

If reversibility holds, the following conditions must then be met:

| (35) |

The first condition is independent of , so it has to hold for all and . By calling and after some manipulation, this condition reads

| (36) |

Similar manipulation of the fourth case gives

| (37) |

These are only compatible with each other if . Therefore the exchange rules discussed in this work are never reversible.

References

- [1] Yarlagadda S. Chatterjee, A. and B. K. Chakrabarti, editors. Econophysics of Wealth Distributions. Springer-Verlag, Milan, Italy, 2005.

- [2] V. Pareto. Cours d’Economie Politique. Droz, Geneve, 1896.

- [3] A. Chatterjee, B. K. Chakrabarti, and S. S. Manna. Money in gas-like markets: Gibbs and pareto laws. Phys. Scr., T106:36–38, 2003.

- [4] V. M. Yakovenko and J. B. Rosser. Colloquium: Statistical mechanics of money, wealth, and income. Rev. Mod. Phys., 81:1703–1725, 2009.

- [5] J. Angle. The surplus theory of social stratification and the size distribution of personal wealth. Social Forces, 2:293–326, 1986.

- [6] S. Ispolatov, P. L. Krapivsky, and S. Redner. Wealth distributions in asset exchange models. Eur. Phys. J. B, 2:267–276, 1998.

- [7] B. Hayes. Follow the money. Am. Scientist, 90:400–405, 2002.

- [8] C. F. Moukarzel, S. Goncalves, J. R. Iglesias, M. Rodriguez-Achach, and R. Huerta-Quintanilla. Wealth condensation in a multiplicative random asset exchange model. Eur. Phys. J.-Spec. Top., 143:75–79, 2007.

- [9] J. R. Iglesias, S. Goncalves, G. Abramson, and J. L. Vega. Correlation between risk aversion and wealth distribution. Physica A, 342:186–192, 2004.

- [10] N. Scafetta, S. Picozzi, and B. J. West. A trade-investment model for distribution of wealth. Physica D, 193:338–352, 2004.

- [11] S. Sinha. Stochastic maps, wealth distribution in random asset exchange models and the marginal utility of relative wealth. Phys. Scr., T106:59–64, 2003.

- [12] S. Redner. Random multiplicative processes - an elementary tutorial. Am. J. Phys., 58(3):267, March 1990.

- [13] M. Levy and S. Solomon. Power laws are logarithmic boltzmann laws. Int. J. Mod. Phys. C-Phys. Comput., 7:595–601, 1996.

- [14] H Takayasu, AH Sato, and M Takayasu. Stable infinite variance fluctuations in randomly amplified langevin systems. Phys. Rev. Lett., 79(6):966, AUG 11 1997.

- [15] Sornette, D. Multiplicative processes and power laws. Phys. Rev. E, 57(4):4811, April 1998.

- [16] J. L. Kelly. A new interpretation of information rate. Bell Syst Tech J, 35:917–926, 1956.

- [17] L. M. Rotando and E. O. Thorp. The kelly criterion and the stock-market. Am. Math. Mon., 99:922–931, 1992.

- [18] A. Dragulescu and V. M. Yakovenko. Statistical mechanics of money. Eur. Phys. J. B, 17:723–729, 2000.