Research supported by the Australian Research Council Grants DP0881011 and

DP0988483

1. Introduction

In scientific computations, expectations with respect to probabilities, induced by

continuous time processes, are often replaced by Monte Carlo averages over independent trajectories.

For diffusions, generated by stochastic differential equations (SDEs), the trajectories are usually approximated numerically

(see e.g. [16]).

The accuracy assessment of such numerical procedures is a well studied topic and

the available theory establishes and quantifies the convergence of the approximations to the actual solution in a variety of

modes, depending on the properties of the SDE coefficients. This in turn typically suffices to claim convergence of expectations

for path functionals, continuous in an appropriate topology, but unfortunately, may not apply to

discontinuous functionals, some of which arise naturally in applications.

One important example of such a functional is the hitting time of a domain boundary.

Let be

the diffusion process on , generated by the Itô SDE

|

|

|

(1.1) |

where is the Brownian motion and the coefficients and are functions,

assumed to satisfy the regularity conditions, guaranteeing existence of the unique strong solution

(see e.g. [23, 24]). The hitting time of the level is

|

|

|

where . Thus is an extended random variable with

values in the Polish space , endowed with the

metric , .

Consider a family of continuous processes , generated by

a numerical scheme with the time step parameter

(such as e.g. the Euler-Maruyama recursion (2.2) and (2.3) below)

and suppose that approximates the diffusion in the sense of weak convergence.

More precisely, let be the space of real valued continuous functions on ,

endowed with the metric

|

|

|

(1.2) |

Then converges weakly to , if for any bounded and continuous functional

|

|

|

(1.3) |

Such convergence can often be established using the techniques, developed in e.g. [5], [11], [18].

In particular, if is a functional, almost surely continuous with respect to the

measure induced by , then (1.3)

implies

|

|

|

(1.4) |

for any continuous and bounded function . In other words, the weak convergence

of the processes implies the weak convergence of the random variables or, equivalently,

the convergence of the probability distribution functions

for any , at which the distribution function is continuous.

Let us now take a closer look at the hitting time

|

|

|

viewed as a functional on . Clearly is discontinuous

at some paths: for example, if and , then

as , but and for all .

On the other hand, is continuous at any , which either upcrosses :

|

|

|

or downcrosses :

|

|

|

If this type of paths is typical for the diffusion (1.1), i.e.

if the set of all such paths is of full measure, induced by the process , then is essentially continuous

and the weak convergence still implies the weak convergence .

However, if is an accessible absorbing boundary of , the paths which hit cannot leave it at any further time.

For such diffusions is discontinuous on a set of positive probability and the weak convergence

cannot be directly deduced from .

Hitting times play an important role in applied sciences, such as physics or finance, and since their exact probability distribution

cannot be found in a closed form beyond special cases, practical approximations are of considerable

interest. There are two principle approaches to compute such approximations. One is based on the fact

that the expectation of a given function of the hitting time solves the Dirichlet boundary problem for an appropriate PDE, and

thus the approximations can be computed using the generic tools from the PDE numerics.

Sometimes, the particular structure of the emerging PDE can be exploited to calculate expectations of special functions of hitting times, such as moments (as e.g. in the linear programming approach of [10]).

The probabilistic

alternative is to use the Monte Carlo simulations, in which the diffusion paths are approximated by numerical solvers.

Typically the diffusions are simulated on a discrete grid of points and the evaluation of the hitting times requires

construction of the continuous paths through an interpolation. The naive approach is to use the general purpose interpolation techniques,

such as the one used in our paper (see (2.3) below). Better results are obtained if the possibility of having a hit

between the grid points is taken into account as in e.g. [17], [6], [7], [12].

The convergence analysis of the approximations of the hitting times, based on the various numerical schemes,

appeared in [19], [21, 20], [9], [8]. The results obtained in these

works, assume ellipticity or hypoellipticity of the diffusion processes under consideration, which corresponds to

the case of non-absorbing boundary in the preceding discussion. The analysis beyond these non-degeneracy conditions appears to be

a much harder problem.

In this paper we consider a particular diffusion on , with an absorbing boundary at .

As explained above, the absorption time in this case is a genuinely discontinuous functional of the

diffusion paths, which makes the convergence analysis of the approximations a delicate

matter. We propose a simple approximation procedure, based on the Euler-Maruyama scheme, and prove its weak consistency.

In the next section we formulate the precise setting of the problem and state the main result, whose prove is

given in Section 3. The results of numerical simulations are gathered in Section 4

and some supplementary calculations are moved to the appendices.

2. The setting and the main result

Consider the diffusion process , generated by the Itô SDE

|

|

|

(2.1) |

where , and are constants and

is the Brownian motion, defined on a filtered probability space , satisfying the

usual conditions. This SDE has the unique strong solution (Proposition 1 in [1]) and

is known in mathematical finance as the Constant Elasticity of Variance (CEV) model (see e.g. [3]).

For , it is also Feller’s branching diffusion, being the weak limit of the Galton - Watson

branching processes under appropriate scaling.

The process is a regular diffusion on and a standard calculation reveals

that is an absorbing (or Feller’s exit) boundary (see §6, Ch. 15 in [13]).

We will denote by the corresponding family of Markov probabilities with , induced by

on the measurable space with the metric (1.2).

Consider the continuous time process , , which satisfies

the Euler-Maruyama recursion at the grid points

|

|

|

(2.2) |

and is piecewise linear otherwise:

|

|

|

(2.3) |

where , is a small time step parameter and is a sequence of i.i.d.

random variables.

Since the diffusion coefficient of (2.1) degenerates and is not Lipschitz on the boundary , this SDE does not quite

fit the standard numerical frameworks such as [15] or [22]. Nevertheless the scheme (2.2) does approximate the solution of (2.1)

in the sense of the weak convergence of measures, as was recently shown in

[1] (see also [27], [26], [2]). Consequently, for any -a.s. continuous

functional

|

|

|

(2.4) |

where stands for the the weak convergence, defined in (1.4).

Since a typical trajectory of oscillates around the level after crossing it, the functional is -a.s. continuous for (see Lemma 3.3 below) and hence as .

This argument, however,

does not apply to , since it is essentially discontinuous, as discussed in the Introduction.

Leaving the question of convergence open, we shall prove the following result

Theorem 2.1.

For any ,

|

|

|

(2.5) |

Note that is a continuous functional for any fixed

and hence can be seen as a mollified version of the discontinuous . The parameter

controls the mollification, relatively to the step-size parameter of the Euler-Maruyama algorithm.

In practical terms, the convergence (2.5) provides theoretical justification for the procedure, in which the approximate trajectory ,

generated by (2.2) and (2.3), is stopped not at , but at , which only approaches zero as .

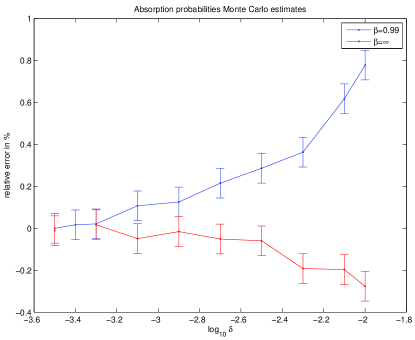

Our method does not quantify the convergence in terms of e.g. rates, but the numerical experiments in Section

4 indicate that this stopping rule produces practically adequate results.

Remark 2.2.

As will become clear from the proof, our approach exploits the local behavior of the SDE coefficients

near the boundary and can be applied to the more general one-dimensional diffusions of the form (1.1),

for which a weakly convergent numerical scheme is available. For example, all the arguments in the proof of

Theorem 2.1 directly apply to the diffusion, whose

coefficients and have a similar local asymptotic at as the CEV model.

The SDE (2.1) is a study case, which seems to capture the essential difficulties of the problem, related to

the degeneracy of the SDE coefficients on the absorbing boundary.

It is a convenient choice, since the weak convergence (2.4), being the starting point of our approach,

has been already established for the CEV model in [1], and the explicit formulas for the probability

density of are available, allowing to carry out the numerical experiments.

3. The proof of Theorem 2.1

The proof, inspired by the approach of S.Ethier [4], is based on the following

observation (a variation of Billingsley’s lemma, see Proposition 6.1 [4])

Proposition 3.1.

Let , and be Borel probability measures on a metric space such that

as . Let be a separable metric space with metric ,

and suppose that , and are Borel measurable

mappings of into such that

-

(i)

is -a.s. continuous for all

-

(ii)

, -a.s.

-

(iii)

for every ,

|

|

|

for an increasing real sequence .

Then as .

Proof.

Let be a continuous with respect to bounded real valued function on , then

|

|

|

where and denote the expectations with respect to and respectively.

Since is continuous and , -a.s., the last term vanishes as by the dominated convergence.

Moreover, since for any fixed ,

is -a.s. continuous and as ,

|

|

|

Consequently,

|

|

|

where the latter equality holds by (iii).

The claim follows by arbitrariness of .

∎

Let us now outline the plan of the proof.

In our context, the probability measures, induced by the family , play the role of

and by Proposition 3.2 they converge weakly to the law of the diffusion .

Since the diffusion coefficient of (2.1) is positive, away from the boundary point 0,

is a -a.s. continuous functional (Lemma 3.3) and hence (i) of Proposition 3.1

holds.

On the other hand, for any (Lemma 3.4),

which implies (ii) of Proposition 3.1. The more intricate part is the convergence (iii), which is

verified in Lemma 3.5, using the particular structure of the SDE (2.1).

The statement of Theorem 2.1 then follows from Proposition 3.1.

The following result is essentially proved in [1]:

Proposition 3.2.

The processes , defined by (2.2) and (2.3),

converge weakly to the diffusion , defined by (2.1), as .

Proof.

For the process, obtained by piecewise constant

interpolation of the points generated by the recursion (2.2), the claim is established in

Theorem 1.1 in [1]. The extension to the piecewise linear interpolation

(2.3) is straightforward.

∎

Lemma 3.3 (Proposition 4.2. in [4]).

For all , is a -a.s. continuous functional on .

Proof.

We shall prove the claim for completeness and the reader’s convenience.

For and , let

|

|

|

and define

|

|

|

We shall first show that is continuous on , i.e. that

|

|

|

(3.1) |

and then check that

|

|

|

(3.2) |

To this end, note that if and , then for all

(recall for ). Thus

implies and hence . Since is arbitrary, ,

i.e. (3.1) holds.

Now take , such that . If , the claim obviously holds by continuity of . If , fix an such that .

Since

|

|

|

we have

and thus .

On the other hand, as , for any , there is an , such that .

It follows that and hence .

By arbitrariness of , we conclude that and (3.1) holds.

It is left to show that (3.2) holds. The diffusion satisfies the strong Markov property and thus (we write

for ),

|

|

|

and hence the required claim holds, if .

Take now to be a scale function of the diffusion , i.e. a solution to the equation

, where is the generator of :

|

|

|

(3.3) |

It is well known, e.g. [14],

that we can take it to be positive and increasing, specifically, for (3.3),

|

|

|

can be taken.

The process is a nonnegative local martingale and thus a supermartingale (e.g. [14] p. 197).

The random variable

is a bounded stopping time and by the optional stopping theorem we have for any

|

|

|

(3.4) |

By the definition of and path continuity of , it follows that

, and

since is increasing, we have that . Thus it follows from (3.4) that for all and, consequently,

, -a.s. for .

On the other hand, , on the set , -a.s.

The obtained contradiction implies , as claimed.

Lemma 3.4.

for any .

Proof.

If , then and hence and the claim follows,

since is arbitrary. If , then for an , and thus

. For sufficiently small , and the claim follows.

∎

Let be the probability on the space, carrying the sequence (see (2.2))

and denote by the Markov family of probabilities, corresponding to the discrete time process

with . Since the process is piecewise linear off the grid ,

the condition (iii) of Proposition 3.1 follows from

Lemma 3.5.

For any and

|

|

|

(3.5) |

Proof.

Roughly speaking, (3.5) means that a trajectory of , which approaches the boundary ,

is very likely to hit it. This seemingly plausible statement is not at all obvious, since the coefficients of

our diffusion decrease to zero near this boundary, making it hard to reach. By letting the level

decrease to zero at a particular rate allows to approximate expectations of the

hitting times by those of , which in turn can be estimated

using their relations to the corresponding boundary value problems.

In what follows, , , etc. denote unspecified constants, independent of and , which may be different in each appearance.

Define the crossing times of level

|

|

|

with .

The sequence , is a strong Markov process and

is a stopping time with respect to its natural filtration.

Since is piecewise linear,

|

|

|

and thus by the triangle inequality

|

|

|

Since

for ,

it follows

|

|

|

|

|

|

|

|

|

where (assuming is small enough).

Further,

|

|

|

|

|

|

and thus (3.5) holds, if we show

|

|

|

(3.6) |

and

|

|

|

(3.7) |

Proof of (3.6)

We shall use the regularity properties of the function

|

|

|

near the boundary point 0,

summarized in the Appendix A. In particular, is continuous on the interval

and is smooth on . Note, however, that the derivatives of explode at the boundary point ,

which is related to the possibility of absorption.

We shall extend the domain of to the whole

by continuity, setting for .

Consider the Taylor expansion

|

|

|

|

|

|

|

|

|

|

|

|

where is between and . After rearranging terms, the latter reads

|

|

|

where is the generator defined in (3.3),

the second term is the martingale

|

|

|

and the last term is the residual

|

|

|

Consequently, for an integer and the stopping time ,

|

|

|

(3.8) |

where

|

|

|

is the residual term, which accommodates the possible overshoot at the terminal crossing time .

Recall that for and hence

|

|

|

(3.9) |

By Lemma A.2, and hence the increments of satisfy

|

|

|

and by the optional stopping theorem (Theorem 2 of §2, Ch. VII, [25]) for .

Now we shall bound the residual terms in (3.8). By Lemma A.2,

|

|

|

and hence

|

|

|

(3.10) |

Similarly, and by Corollary B.2 (applied with )

|

|

|

(3.11) |

To bound , note that

by Lemma A.2,

|

|

|

and thus

|

|

|

(3.12) |

where the latter inequality holds, since on the set .

Since is between and

|

|

|

(3.13) |

For , we have and

thus on the set ,

|

|

|

(3.14) |

On the set we have

|

|

|

(3.15) |

Note that for , and , such that ,

|

|

|

Applying this inequality to (3.15) on the set we get

|

|

|

|

|

|

|

|

|

|

|

|

where the inequalities hold for all sufficiently small and

we used the bounds and .

Consequently, on the set

|

|

|

(3.16) |

Plugging the bounds (3.16) and (3.14) into (3.12) and

applying the Corollary B.2, we obtain the

estimate

|

|

|

|

|

|

|

|

|

where .

Using the Gaussian tail estimate

|

|

|

we get

|

|

|

which

along with (3.10) and (3.11) yields the bound

|

|

|

(3.17) |

Finally, by Corollary B.2,

|

|

|

and hence by Lemma A.2,

|

|

|

and consequently

|

|

|

(3.18) |

Plugging the estimates (3.9), (3.17) and (3.18) into (3.8), we obtain the bound

|

|

|

By the monotone convergence, the latter implies

|

|

|

and by continuity of ,

|

|

|

verifying (3.6).

Proof of (3.7)

Consider the function , whose domain we extend to the whole real line by continuity,

setting for and for . The process , satisfies the

decomposition (3.8), with replaced by .

Taking into account that

for and the bounds from the Lemma A.1, a calculation, similar to the one in the preceding subsection, shows that

|

|

|

On the other hand,

|

|

|

|

|

|

and thus, for sufficiently small ,

|

|

|

Since is continuous on and ,

|

|

|

which verifies (3.7).

Remark 3.6.

The condition originates in the estimate (3.14), which is plugged into (3.12).

The principle difficulty is that the term

cannot be effectively controlled for greater values of as . For example,

it is not clear how to bound the right hand side of (3.12) already for and .