Shifeng Xiong1, Bin Dai2 and Peter Z. G.

Qian333Corresponding author: Peter Z. G. Qian. Email: peterq@stat.wisc.edu

1 Academy of Mathematics and Systems Science

Chinese Academy of Sciences, Beijing 100190

2 Tower Research Capital, 377 Broadway, New York, NY 10013

3 Department of Statistics

University of Wisconsin-Madison, Madison, WI 53706

Abstract We propose an algorithm, called OEM (a.k.a. orthogonalizing EM), intended for various least squares problems. The first step, named active orthogonization, orthogonalizes an arbitrary regression matrix by elaborately adding more rows. The second step imputes the responses of the new rows. The third step solves the least squares problem of interest for the complete orthogonal design. The second and third steps have simple closed forms, and iterate until convergence. The algorithm works for ordinary least squares and regularized least squares with the lasso, SCAD, MCP and other penalties. It has several attractive theoretical properties. For the ordinary least squares with a singular regression matrix, an OEM sequence converges to the Moore-Penrose generalized inverse-based least squares estimator. For the SCAD and MCP, an OEM sequence can achieve the oracle property after sufficient iterations for a fixed or diverging number of variables. For ordinary and regularized least squares with various penalties, an OEM sequence converges to a point having grouping coherence for fully aliased regression matrices. Convergence and convergence rate of the algorithm are examined. These convergence rate results show that for the same data set, OEM converges faster for regularized least squares than ordinary least squares. This provides a new theoretical comparison between these methods. Numerical examples are provided to illustrate the proposed algorithm.

KEY WORDS: Design of experiments; MCP; Missing data; Optimization; Oracle property; Orthogonal design; SCAD; The Lasso.

1 INTRODUCTION

Consider a regression model

(1)

where is the regression matrix,

is the response vector, is the vector of regression coefficients, and is the vector of random errors with

zero mean. The ordinary least squares (OLS) estimator of is the solution to

(2)

where denotes the Euclidean norm. If is a part of a known orthogonal

matrix

(3)

where is an

matrix, (2) can be efficiently computed by the Healy-Westmacott procedure (Healy and Westmacott 1956). Let

(4)

be the vector of complete responses with missing data of points.

In each iteration, the procedure imputes the value of , and updates the OLS estimator for the complete data . This update involves no matrix inversion since is (column) orthogonal. Dempster, Laird, and Rubin (1977)

showed that this procedure is an EM algorithm.

The major limitation of the procedure is the assumption that must be embedded in a pre-specified orthogonal matrix . We propose a new algorithm, called orthogonalizing EM (OEM) algorithm, to remove this restriction and extend to other directions. The first step, called active

orthogonization, orthogonalizes an arbitrary regression matrix by elaborately adding more rows. The second step imputes the responses of the new rows. The third step solves the OLS problem in (2) for the complete orthogonal design. The second and third steps have simple closed forms, and iterate until convergence.

For the OLS problem in (2), OEM works with an arbitrary regression matrix . For with no full column rank, the OLS estimator is not unique, and we prove that the OEM

algorithm converges to the Moore-Penrose generalized inverse-based least squares estimator. OEM outperforms

existing methods for such an inverse.

OEM also works for regularized least squares problems by adding penalties or constraints to in (2). These penalties include the ridge regression

(Hoerl and Kennard 1970), the nonnegative garrote (Breiman 1995), the lasso (Tibshirani 1996), the SCAD (Fan and Li 2001), and the MCP (Zhang 2010), among others. Here, the first step of OEM uses the same active orthogonalization as that for OLS. The second and third steps of OEM imputes the missing data and solves the regularized problem

for the complete data . Both the second and third steps have a simple closed form. We prove that OEM converges to a local minimum or stable point of the regularized least squares problem under mild conditions. Convergence rate of OEM is also established. These convergence rate results show that for the same data, OEM converges faster for regularized least squares than ordinary least squares. This difference provides a new theoretical comparison between these methods. Compared with existing algorithms, OEM possesses two unique theoretical features. 1. Achieving the oracle property for nonconvex penalties: An estimator of in (1) having the oracle property can not only select the correct submodel asymptotically, but also estimate the nonzero coefficients as efficiently as if the correct submodel were known in advance. Fan and Li (2001) proved that there exists a local solution of SCAD with this property. From the optimization viewpoint, the SCAD problem can have

many local minima (Huo and Chen 2010) and it is not clear which one has this property. Zou and Li (2008) proposed the local linear approximation

(LLA) algorithm to solve the SCAD problem and showed that the one-step LLA estimator has the oracle property with a good initial estimator for a fixed . The LLA estimator is not guaranteed to be a local minimum of SCAD. To the best of our knowledge, no theoretical results so far show that any existing algorithm can provide such a local minimum. We prove that the OEM solution for SCAD can achieve a local solution with this property. 2. Having

grouping coherence: An estimator of is said to have grouping coherence if it has the same coefficient for full aliased columns in . For the lasso, SCAD, and MCP, an OEM sequence converges to a point having grouping coherence, which implies that the full aliased variables will be in or out of the selected model together. This property cannot be achieved by existing algorithms including the coordinate descent algorithm. In terms of numerical performance, OEM can be very fast for ordinary least squares problems and SCAD for big tall data with . For big wide data with , OEM can be slow. This drawback can be mitigated by adopting a two-stage procedure like that in Fan and Lv (2008), where the first stage uses a screening approach to reduce the dimensionality to a moderate size, and the second stage uses OEM.

The remainder of the article will unfold as follows. Section 2 discusses the active orthogonalization procedure. Section 3 presents OEM for OLS. Section 4 extends OEM to regularized least squares. Section 5 provides convergence properties of OEM.

Section 6 shows that for a regression matrix with full aliased columns, an OEM sequence for the lasso, SCAD, or MCP converges to a solution with grouping coherency. Section 7 establishes the oracle property of the OEM solution for SCAD and MCP. Section 8 presents numerical examples to compare OEM with other algorithms for regularized least squares. Section 9 concludes with some discussion.

2 ACTIVE ORTHOGONALIZATION

For an arbitrary matrix in (1), we propose active orthogolization to actively orthogolize an arbitrary matrix by elaborately adding more rows. Let be a diagonal matrix with non-zero diagonal elements . Define

(5)

Consider the eigenvalue decomposition of (Wilkinson 1965), where is an orthogonal matrix and is a diagonal

matrix whose diagonal elements, , are the nonnegative eigenvalues of . For , let

(6)

denote the number of the equal . For example, if and for , then . If ,

then .

Define

(7)

and

(8)

where

is the submatrix of consisting of the last rows. Put and row by row together to form a complete matrix .

It then follows that , which completes the proof.

∎

Here is the underlying geometry of active orthogolization. For a vector , let denote its projection onto a subspace of

. Lemma 1 implies that for the column vectors of in (1), there exists a

set of mutually orthogonal vectors of in (3) satisfying

, for . Proposition 1 makes this precise.

Proposition 1.

Let be an -dimensional subspace of with . If , then for any vectors ,

there exist vectors such that for and

for .

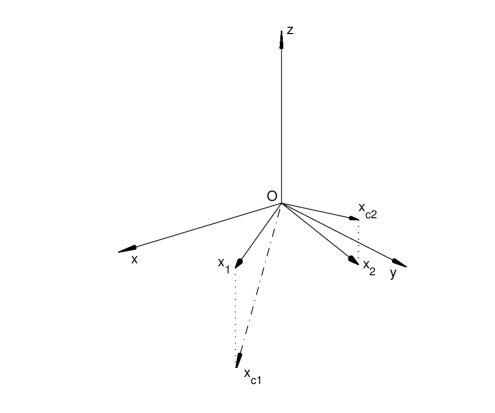

For illustration, Figure 1 expands two vectors and in to two orthogonal vectors and in

.

[0.8]

Figure 1: Expand two two-dimensional vectors and to two three-dimensional vectors and with

.

Remark 1.

In (8) has rows, which does not rely on the number of rows in , and only rows need to be added to make

it orthogonal.

Remark 2.

The form of in (5) can be chosen flexibly. One possibility is with

(9)

with , and

is standardized as the Euclidean norm of each column is .

The regression matrix including all main effects and two-way interactions is

where the last three columns for the interactions are fully aliased with the first three columns for the main effects. For and , (8)

gives

The structure of is flexible in that the interaction columns do not need to be a product of other two columns.

Example 4.

Consider a random matrix with entries independently drawn from

the uniform distribution on . Using in (10), (8) gives

Only nine rows need to be added to make this large matrix orthogonal.

3 OEM FOR ORDINARY LEAST SQUARES

We now study OEM for the OLS problem in (2) when the regression matrix has an arbitrary form.

The first step of OEM is active orthogonalization to obtain in (8). For an initial estimator , the second step imputes

in (4) by . Let . The third step solves

(11)

Then, the second and third

steps iterate for obtaining

until convergence. Define

(12)

For in (3), let denote the diagonal elements of .

For let

which is separable in the dimensions of . Thus, (14) has a simple form

(15)

which involves no matrix inversion.

In (13), for active orthogonalization, instead of computing in (8), one can compute and the diagonal entries

of . If in (8), , where is a number no less than

the largest eigenvalue of . A possible choice is . Another choice is to obtain the fastest

convergence; see Remark 5. We compute by the power method (Wilkinson 1965) described below. Given a nonzero initial vector

, let . For , compute

and

until convergence. If is not an eigenvector of any unequal to , then converges to .

For in (6), the convergence rate of the power method is linear (Watkins 2002) specified by

When ,

replace the matrix with the matrix in the power method to reduce computational cost as the two matrices have the same non-zero eigenvalues.

When has full column rank, the convergence results in Wu (1983) indicates that the OEM sequence given by (15) converges to the OLS

estimator for any initial point . Next, we discuss the convergence property of OEM when is singular, which covers the case

of . Let denote the rank of . For , the singular value decomposition (Wilkinson 1965) of is

where is an orthogonal matrix, is a orthogonal matrix, and is a diagonal matrix with diagonal elements which are the positive eigenvalues of

. Define

(16)

where + denotes the Moore-Penrose generalized inverse

(Ben-Israel and Greville 2003).

Theorem 1.

Suppose that . If lies in the linear space spanned by the first columns

of , then as , for the OEM sequence of the ordinary least squares,

.

Proof.

Define

. Note that . By induction,

As ,

and

, which implies that

This completes the proof.∎

In active orthogonalization, the condition holds if and in (8). Using

satisfies the condition in Theorem 1.

The Moore-Penrose generalized inverse is widely used in statistics for a degenerated system. Theorem 1 indicates that OEM converges to in

(16) in this case. When , the limiting vector given by an OEM sequence has the following properties. First, it has the minimal Euclidean norm

among the least squares estimators (Ben-Israel and Greville 2003). Second, its model error has a simple form,

. Third, implies for any vector . The third property

indicates that inherits the multicollinearity between the columns in . This property is stronger than grouping coherence for regularized least squares in

Section 6.

A widely used method for computing is to obtain by the eigenvalue decomposition (Golub and Van Loan 1996) and then compute the

product of and . This method is implemented in the MATLAB function

pinv with core code in Fortran and in the R function ginv with core code in C++. The R function is slower than the MATLAB function. When some eigenvalues are close to zero, the eigenvalue decomposition method is unstable, and OEM is more stable due to its iterative nature. The following example illustrates this difference.

Example 5.

Construct a matrix , where is generated from a uniform

distribution on . The eigenvalues of are , and . Generate all entries of independently from the uniform

distribution on . We compare OEM and the eigenvalue decomposition method for computing using the MATLAB function pinv. For OEM, the stopping criterion is

when relative changes in all coefficients are less than . The two methods are replicated 100 times in MATLAB. Over the 100 replicates, the largest and

smallest values of by the eigenvalue decomposition method are and , indicating unstability. The two values computed by OEM are and ,

which are much more stable.

Next, we discuss the computational efficiency of OEM for computing in (16) when is degenerated. Recall that and

have the same nonzero eigenvalues. The computation of in the OEM iterations by the power method has complexity

. Since the complexity of the OEM iterations is , the whole computational complexity of OEM for computing is

. The eigenvalue decomposition method computes first by eigenvalue decomposition to obtain , and has computational complexity . The

OEM algorithm is superior to this method in terms of complexity.

OEM

eigenvalue

decomposition

Table 1: Average runtime (second) comparison between OEM and the prevailing method for

OEM

eigenvalue

decomposition

Table 2: Average runtime (second) comparison between OEM and the eigenvalue decomposition method for

We conduct a simulation study to compare the speeds of OEM and the eigenvalue decomposition method for computing in (16). Generate all entries of and independently from the standard normal distribution. A new predictor calculated as the mean of all the covariates is added to degenerate the design matrix. Tables 1 and

2 compare our R package oem with main code in C++ and the eigenvalue decomposition method in computing .

The two methods give the same results. Tables 1 and 2 indicate that OEM is faster than the eigenvalue decomposition method for any combination

of and , validating the above complexity analysis.

4 OEM FOR REGULARIZED LEAST SQUARES

It is easy to extend OEM to regularized least squares problems. Consider a penalized version of (1):

(20)

where ,

is a subset of , is a penalty function, and is the vector of tuning parameters. To apply the penalty equally to all the

variables, the regression matrix is standardized so that

(21)

Popular choices for include the

ridge regression (Hoerl and Kennard 1970), the nonnegative garrote (Breiman 1995), the lasso (Tibshirani 1996), the SCAD (Fan and Li 2001), and the MCP (Zhang 2010).

Suppose that and in (20) are decomposable as and . For the

problem in (20), the first step of OEM is active orthogonalization, which computes in (8). For an initial estimator , the second

step imputes in (4) by . Let . The third step

solves

The second and third steps iterate to compute for until convergence. Similar to (14), we have an iterative formula

(22)

with in (13). This shortcut applies to the following penalties:

with , , and . Here, is the indicator function. If in (1)

is standardized as in (21) with

for all , (22) becomes

(28)

6. The MCP (Zhang 2010), where , , and

(29)

with and . If in (1) is standardized as in (21) with for

all , (22) becomes

(30)

7. The “Berhu” penalty (Owen 2006), where , for some , and (22) becomes

OEM for (20) is an EM algorithm. Let the observed data follow the model in (1). Assume that the complete data in (4) follows a regression model

, where is from . Let be a solution to (20) given by

, and the regularized likelihood function is

Given , the second step of OEM for (20) is the E-step,

for some constant . Define

(31)

The third step of OEM is the M-step,

(32)

which is equivalent to (22) when and in (20) are decomposable.

Example 6.

For the model in (1), let the complete matrix be an orthogonal design from Xu (2009) with 4096 runs in 30 factors. Let in (1)

be the submatrix of consisting of the first 3000 rows and let be generated from (1) with and

(33)

Here, let , , and the response values for the last 1096 rows of be missing. OEM is used to solve the SCAD problem with an initial

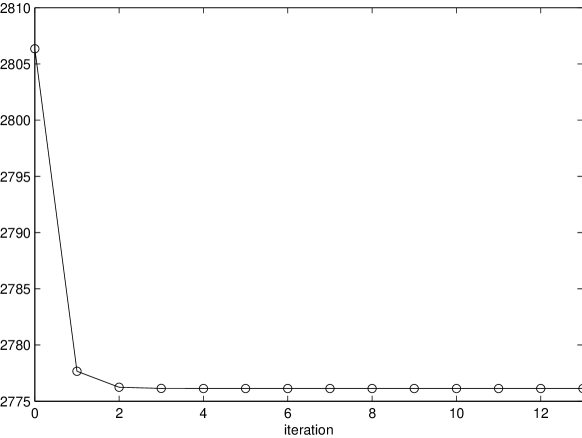

value and a stopping criterion when relative changes in all coefficients are less than . For and in (27), Figure

2 plots values of the objective function in (20) with the SCAD penalty of the OEM sequence against iteration numbers, where the convergence occurs

at iteration 13, and the objective function significantly reduces after two iterations.

[0.5]

Figure 2: Values of the objective function of an OEM sequence for the SCAD against iterations for Example 6.

5 CONVERGENCE OF THE OEM ALGORITHM

We now derive convergence properties of OEM with the general penalty in (20). We also give results to compare the convergence rates of

OEM for OLS, the elastic-net, and the lasso. These convergence rate results show that for the same data set, OEM converges faster for regularized least squares than ordinary least squares. This provides a new theoretical comparison between these methods. The objective functions of existing EM convergence results like those in Wu (1983), Green (1990) and McLachlan and Krishnan

(2008) are typically continuously differentiable. This condition does not hold for the objective function in (20) with the lasso and other penalties, and these existing results do not directly apply here.

The parameter space is a closed convex subset of .

Assumption 2.

For a fixed , the penalty as .

Assumption 3.

For a fixed , the penalty is continuous with respect to .

All penalties discussed in Section 4 satisfy these assumptions. The assumptions cover the case in which the iterative sequence

defined in (32) may fall on the boundary of (Nettleton 1999), like the nonnegative garrote (Breiman 1995) and the nonnegative lasso (Efron et al. 2004).

The bridge penalty (Frank and Friedman 1993) in (36) also satisfies the above assumptions.

For the model in (1), denote the objective function in (20) by

(34)

For penalties like the bridge, it is infeasible to perform the M-step in (32) directly. For this situation, following the generalized EM algorithm in

Dempster, Laird, and Rubin (1977), we define the following generalized OEM algorithm

(35)

where is a

point-to-set map such that

Here, is given in (31). The OEM sequence

defined by (32) is a special case of (35). For example, the generalized OEM algorithm can be used for the bridge penalty, where and

(36)

for some in (20). Since the solution to (22) with the bridge penalty has no closed form, one may use one-dimensional search to compute

that satisfies (35). By Assumption 1, is compact for any . By Assumption

3, is a closed point-to-set map (Zangwill 1969; Wu 1983).

The objective functions in (20) with the lasso and other penalties are not continuously differentiable. A more general definition of stationary points is needed. We call a stationary point of if

Let denote the set of stationary points of

. Analogous to Theorem 1 in Wu (1983) on the global convergence of the EM algorithm, we have the following result.

Theorem 2.

Let be a generalized OEM sequence generated by (35). Suppose that

(37)

Then all limit points of are elements of and converges monotonically to for some .

Theorem 3.

If is a local minimum of , then .

This theorem follows from the fact that is differentiable and

Remark 3.

By Theorem 3, if , then cannot be a local minimum of . Thus, there exists at least one point

such that and therefore satisfies the condition in (37). As a

special case, an OEM sequence generated by (32) satisfies (37) in Theorem 2.

Next, we derive convergence results of a generalized OEM sequence in (35), which, by Theorem 3, hold automatically for an

OEM sequence. If the penalty function is convex and has a unique minimum, Theorem 4 shows that converges

to the global minimum.

Theorem 4.

For defined in Theorem 2, suppose that in (34) is a convex function on with a unique

minimum and that (37) holds for . Then as .

Proof.

It suffices to show that . For with and ,

This implies .

∎

Theorem 5 discusses the convergence of an OEM sequence for more general penalties. For , define . From Theorem 2, all limit points of an OEM sequence are in , where is the limit of in Theorem 2.

Theorem 5 states that the limit point is unique under certain conditions.

Theorem 5.

Let be a generalized OEM sequence generated by (35) with . If (37) holds, then all

limit points of are in a connected and compact subset of . In particular, if the set is discrete in that its only connected components

are singletons, then converges to some in as .

Proof.

Note that . By Theorem 2,

as . Thus,

. This theorem now follows immediately from Theorem 5 of Wu (1983).∎

Since the bridge, SCAD and MCP penalties all satisfy the condition that is discrete, an OEM sequence for any of them converges to the stationary points of .

Theorem 5 is obtained under the condition is not singular.

It is easy to show that Theorem 5 holds with probability one if the error in (1) has a continuous distribution.

We now derive the convergence rate of the OEM sequence in (32). Following Dempster, Laird, and Rubin (1977), write

where the map is defined by (32). We capture the convergence rate of the OEM sequence through .

Assume that (9) holds for , where

is the largest eigenvalue of . For active orthogolization in Section 2, this assumption holds by taking ; see Remark 2.

Let be the limit of the OEM sequence . As in Meng (1994), we call

(38)

the global rate of convergence for the OEM

sequence. If there is no penalty in (20), i.e., computing the OLS estimator, the global rate of convergence in (38) becomes the largest eigenvalue of

, denoted by , where is the Jacobian matrix for having th entry . If

(9) holds, then with . Thus,

(39)

For (20), the penalty function typically is not sufficiently smooth and in (38) has no analytic form. Theorem 6 gives an

upper bound of , the value of for the elastic-net penalty in (25) with .

Let denote the th column of matrix in (1) and denote the th column of ,

respectively.

For an OEM sequence for the elastic-net, by (26),

where

For , observe that

Thus,

This completes the proof.∎

Remark 4.

Theorem 6 indicates that, for the same and in (1), the OEM solution for the elastic-net numerically converges faster than its

counterpart for the OLS. Since the lasso is a special case of the elastic-net with in (25), this theorem holds for the lasso as well.

Remark 5.

From (39) and Theorem 6, the convergence rate of the OEM algorithm depends on the ratio of

and equal to or larger than . This rate is the fastest when , i.e., if is orthogonal and standardized. This result suggests

that OEM converges faster if has controlled correlation like from a supersaturated design or a nearly orthogonal Latin hypercube design (Owen 1994).

[0.6]

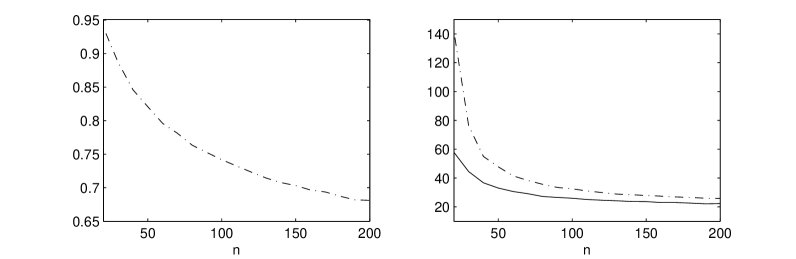

Figure 3: (Left) the average values of in (39) against increasing for Example 7; (right) the average iteration numbers against increasing

for Example 7, where the dashed and solid lines denote the OLS estimator and the lasso, respectively.

Example 7.

We generate from dimensional Gaussian distribution with independent observations, where the th entry of is 1 for

and for . Values of and are generated by (1) and (33). The same setup was used in Friedman, Hastie, and Tibshirani (2009).

For and increasing , the left panel of Figure 3 depicts the average values of in (39) against increasing

and the right panel of the figure depicts the average iteration numbers against increasing , with the dashed and solid lines corresponding to the OLS estimator

and the lasso, respectively. This figure indicates that OEM requires fewer iterations as becomes larger, which makes OEM particulary attractive for situations

with big tall data. The OEM sequence for the lasso requires fewer iteration than its counterpart for the OLS, thus validating Theorem 6.

6 POSSESSING GROUPING COHERENCE

Data with fully aliasing structures commonly appear in observational studies and designed experiments. Here we consider the convergence of the OEM algorithm

when the regression matrix in (1) is singular due to fully aliased columns. Let be standardized as in (21) with columns

. If and are fully aliased, i.e., , then the objective function in (20) for the lasso is not

strictly convex and has many minima (Zou and Hastie 2005).

If some columns of are identical, it is desirable to have grouping coherence with the same regression coefficient. This is suggested by Zou and Hastie (2005) and

others. Definition 1 makes this precise.

Definition 1.

An estimator of in (1) has grouping coherence if implies

and implies .

Some penalties other than the lasso can produce estimators with grouping coherence (Zou and Hastie 2005; Bondell and Reich 2008; Tutz and Ulbricht 2009; Petry and

Tutz 2012), but they require more than one tuning parameters, which leads to more computational burden. Instead of changing the penalty, OEM can

give a lasso solution with this property. This also holds for SCAD and MCP. Recall that in (16), which can be obtained by OEM, has a stronger

property than grouping coherence.

Let denote the zero vector in . Let be the vector obtained by replacing the th and th entries of with . Let

be the vector obtained by replacing the th and th entries of with and , respectively. Let denote the set of all

and . By Definition 1, an estimator has grouping coherence if and only if for any with

, .

Lemma 2.

Suppose that (9) holds. For the OEM sequence of the lasso, SCAD or MCP, if and for ,

then .

Proof.

For in (13), for any with and .

Then by (24), (28) and (30), an OEM sequence of the lasso, SCAD or MCP satisfies the condition that if , then

for . This completes the proof.∎

Remark 6.

Lemma 2 implies that, for , has grouping coherence if has grouping coherence. Thus, if

converges, then its limit has grouping coherence. By Theorem 5, if in (9), then an OEM sequence for the SCAD or MCP

converges to a point with grouping coherence.

When in (1) has fully aliased columns, the objective function in (20) for the lasso has many minima and hence the condition in Theorem

4 does not hold. Theorem 7 shows that, even with full aliasing, an OEM sequence (24) for the lasso converges to a point with grouping

coherence.

Theorem 7.

Suppose that (9) holds. If has grouping coherence, then as ,

the OEM sequence of the lasso converges to a limit that has grouping coherence.

Proof.

Partition columns of in (1) as , where no two columns of are fully aliased and any

column of is fully aliased with at least one column of . Let denote the number of columns in . Partition as

and as , corresponding to and , respectively. For , let

By Lemma 2, for , if and

otherwise, where . It follows that is an OEM sequence for solving

(40)

where , and the columns of are . Because the objective function in

(40) is strictly convex, by Theorem 4, converges to a limit with grouping coherence. This completes the proof.∎

7 ACHIEVING THE ORACLE PROPERTY WITH NONCONVEX PENALTIES

Fan and Li (2001) introduced an important concept called the oracle property and showed that there exists one local minimum of the SCAD problem with this property when

is fixed. The corresponding results with a diverging were presented in Fan and Peng (2004) and Fan and Lv (2011). Because the optimization problem in (20)

with the SCAD penalty has an exponential number of local optima (Huo and Ni 2007; Huo and Chen 2010), no theoretical results in the current literature, as far as we are aware, show that an

existing algorithm can provide such a local minimum. Zou and Li (2008) proposed the local linear approximation (LLA) algorithm to solve the SCAD problem and showed that

the one-step LLA estimator has the oracle property with a good initial estimator for a fixed . The LLA estimator is not guaranteed to be a local minimum of SCAD. In contrast, we prove that the OEM solution to the

SCAD or MCP can achieve this property. Like Fan and Peng (2004) and Fan and Lv (2011), we allow to depend on , which covers the fixed case as a special case.

Suppose that the number of nonzero coefficients of in (1) is (with ) and partition as

(41)

where and no component of is zero. Divide columns of the regression matrix in (1) to with

corresponding to . A regularized least squares estimator of in (1) has the oracle property if it can not only select the correct submodel

asymptotically, but also estimate the nonzero coefficients in (41) as efficiently as if the correct submodel were known in advance. Specifically, an

estimator has this property if and follows a normal distribution asymptotically.

We now consider the oracle property of OEM sequences for SCAD. First we prove that, under certain conditions, a fixed point of the OEM iterations for SCAD can possess the oracle property. Here in after, depends on but and are

fixed for simplicity. A definition and several assumptions are needed.

Definition 2.

For a series of numbers and a positive constant , an estimator of is

said to be -concentratively consistent of order to if as , (i) ; (ii)

for any , where is a constant.

Assumption 4.

The random error follows a normal distribution .

Assumption 5.

The matrix is standardized such that each entry on the diagonal

of is 1, and with , where is the largest eigenvalue of .

In active orthogonalization, in Assumption 5 can take any number equal to or larger than .

Assumption 6.

As ,

where is a positive definite matrix.

Assumption 7.

The tuning parameter in (27), in Assumption 5, and satisfy the condition that,

as , and

for any .

For a fixed , the OLS estimator is concentratively consistent with and in Definition 2 under Assumption 4.

Generally, in the above assumptions satisfies . For example, in the consistency analysis for the lasso (Bühlmann and

van de Geer 2011). Let . To satisfy Assumption 7, must be smaller than . Note that . Therefore

if we set for some , must be smaller than . In other words, our results in this section can handle dimensionality of order for

. For such a , we can take the tuning parameter to satisfy Assumption 7, where .

Theorem 8.

Let be a fixed point of the OEM iterations for SCAD with a fixed in (27). Suppose that

is -concentratively consistent of order to with and . Under Assumptions 4-7, as

,

(i) ;

(ii) in distribution.

The proof of Theorem 8 is deferred to the Appendix. This theorem indicates that a fixed point of OEM consistent to the true parameter is an oracle

estimator asymptotically even when grows faster than . If we do not know whether a fixed point is consistent, with an initial point concentratively consistent to , an OEM sequence can converge to that fixed point and possess the oracle property.

Let be the OEM sequence from (28) for the SCAD with a fixed in (27). Let be the largest eigenvalue of

. Clearly, . We need an assumption on .

Assumption 8.

As , , ,

and for any .

As , implies . In fact, can grow much faster than . For example, suppose that

and , where . Take , where . With for any , one choice for to

satisfy Assumption 8 is

Under the above assumptions, Theorem 9 shows that can achieve the oracle property.

Theorem 9.

If is -concentratively consistent of order to with and . Under Assumptions 4-8, as ,

(i)

;

(ii) in distribution.

The proof of Theorem 9 is deferred to the Appendix.

Remark 7.

From (63) in the proof of Theorem 9, for any , is consistent in variable selection. That is,

and as .

Remark 8.

The proof of Theorem 9 uses the convergence rates of and . If an OEM sequence satisfies the condition that when

and when for some positive constant , then and

. Since an OEM sequence for MCP satisfies the above condition, an argument similar to the proof in the Appendix shows that the

convergence rates of and for MCP are the same as those with the SCAD. Thus, under Assumption 4-8, Theorem 9 holds for

MCP with a fixed in (29).

Remark 9.

With minor modifications, Theorem 8 and 9 can allow to tend to infinity at a relatively low rate. They also hold if the normality

condition is replaced by weaken conditions such as the sub-Gaussian condition (see e.g. Zhang 2010).

Theorem 8 and 9 can handle dimensionality of order for . For exceeding this order, penalized regression methods

can perform poorly. A practical approach is a two-stage procedure like that in Fan and Lv (2008). The first stage uses an efficient

screening method to reduce the dimensionality. OEM can be used in the second stage to obtain a SCAD estimator with the oracle property.

The initial point in OEM for nonconvex penalties can be chosen as the OLS estimator if . Otherwise, the lasso estimator, which is consistent under certain

conditions (Meinshausen and Yu 2009; Bühlmann and van de Geer 2011), can be used as the initial point.

Huo and Chen (2010) showed that, for the SCAD penalty, solving the global minimum of the SCAD problem leads to an NP-hard problem. Theorem 9 indicates that as

far as the oracle property is concerned, the local solution given by OEM will suffice.

8 NUMERICAL ILLUSTRATIONS FOR SOLVING PENALIZED LEAST SQUARES

Existing algorithms for solving the regularized least squares problem in (20) include those in Fu (1998), Grandvalet (1998), Osborne, Presnell, and Turlach (2000), the LARS algorithm in Efron, Hastie, Johnstone, and

Tibshirani (2004) and the coordinate descent (CD) algorithm (Tseng 2001; Friedman, Hastie, Hofling and Tibshirani 2007; Wu and Lange 2008; Tseng and Yun 2009). The corresponding R packages include lars (Hastie and Efron 2011), glmnet (Friedman, Hastie, and Tibshirani 2011), and scout (Witten and

Tibshirani 2011). For nonconvex penalties like SCAD and MCP, existing algorithms include local quadratic approximation (Fan and

Li 2001; Hunter and Li 2005), local linear approximation (Zou and Li 2008), the CD algorithm (Breheny and Huang 2011; Mazumder, Friedman, and Hastie

2011) and the minimization by iterative soft thresholding algorithm (Schifano, Strawderman, and Wells 2010), among others. Different from these algorithms, OEM

handles each dimension of the iterated vector separably and equally as in (14), and has appealing features such as

grouping coherence in Section 6 and the oracle property in Section 7. Putting these properties aside, one may be interested in numerical comparisons of OEM and other algorithms. Here we compare OEM with the CD and LARS algorithms for regularized least squares.

8.1 COMPARISONS WITH OTHER ALGORITHMS

8.1.1 GROUPING COHERENCE

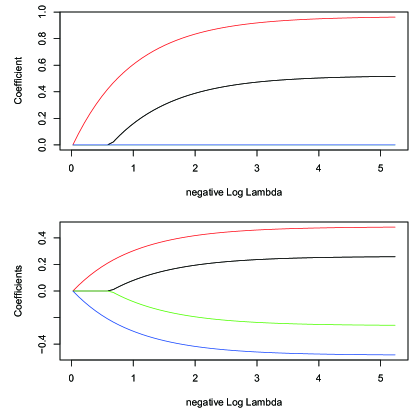

We illustrate grouping coherence of OEM in Section 6 with a simulated data set of four predictors, where the variables and

are generated from independent standard normal distributions. The degenerated design matrix is formulated by and , where the predictors

consist of two pairs of perfectly negative correlated random variables. The true relationship between the response and predictors is

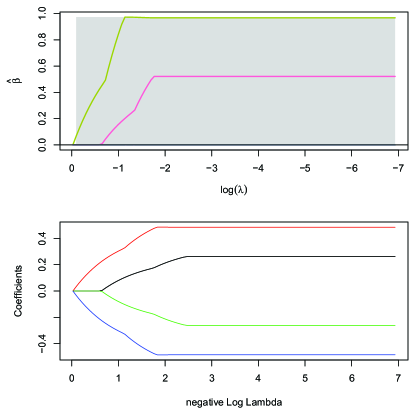

Figure 4: Solution paths of the lasso fitted by CD (the upper panel) and OEM (the lower panel) in Section 8.1.1.

Figure 4 displays the solution paths for the data using the lasso fitted by R packages glmnet and oem on the same set of tuning

parameters . The package lars gives the same solution path as glmnet. This figure reveals that OEM estimates the perfectly negative correlated

pairs to have exactly the opposite signs but CD only has and in the model and fixes and to be zero for any . This difference is due to

the fact that in every iteration, both CD and LARS will find the predictor with the largest improvement on the target function and if more than one coordinates can give

better results, only the one with the smallest index will enter the model. In contrast, OEM considers all the predictors in every iteration equally, so the ones with

same contribution to the target will receive equal steps.

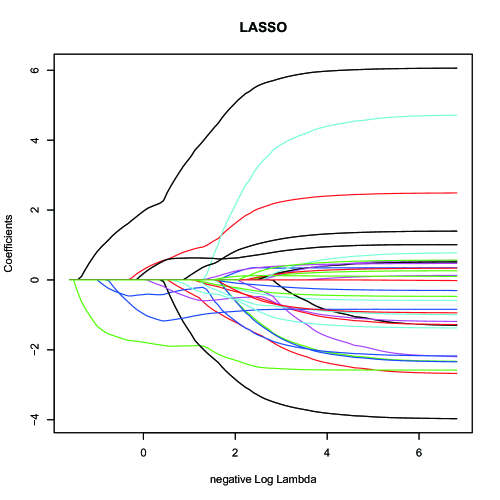

Figure 5: Solution paths of SCAD fitted by CD (from package ncvreg) in the upper panel and OEM for the lower panel in Section 8.1.1..

Grouping coherence of OEM also holds for non-convex penalties such as SCAD, with the solution paths shown in Figure 5, where the same data used above for the lasso is used.

8.1.2 SPEED

We now compare the computational efficiency of OEM for regularized least squares problems with the coordinate descent (CD) algorithm, which is considered the fastest

among the current choices. OEM is implemented in R package oem with main code in C++. For fitting the lasso, we compare OEM and the R

package glmnet, which has the main code in Fortran and uses several tricks to speed up. We found that glmnet is faster than oem in most scenarios, but oem has grouping

coherence; see Section 8.1.1. Next, we focus on comparisons of OEM and the package ncvreg developed in C for SCAD and MCP

penalties.

We first consider the situation when the sample size is larger than the number of variables . Three different covariance matrix structures for the

predictor variables are compared. The first is the case where all the variables are independently generated from standard normal distribution, the second and third

cases involve design matrices with a correlation structure

(42)

where . The response is generated independent of the design matrix and the true model is , where follows the normal

distribution .

OEM

CD

Table 3: Average runtime (second) comparison between OEM and CD for SCAD when is larger than

To compare the performance of the OEM and CD algorithms for SCAD penalty, data are generated 10 times and the average runtime are given in Table 3.

The table indicates that OEM has advantages when the sample size is significantly larger than the number of variables especially for the independent design. Both

algorithms require more fitting time when the correlations among the covariates increase.

Table 4 compares the algorithms with large small . It turns out that the CD algorithm is faster and the

computational gap gets wider when the ratio of increases. Since regularized least squares methods are usually more efficient after the dimensionality is reduced from very large to moderate by a

screening procedure (Fan and Lv 2008), a remedy for this drawback is to use OEM after screening the important variables.

OEM

CD

Table 4: Average runtime (second) comparison between OEM and CD for SCAD for large

8.2 PERFORMANCE COMPARISONS WITH ONE-STEP ESTIMATOR

We compare the SCAD solution computed by OEM with Zou and Li (2008)’s one-step LLA estimator. The model used here is

The sample size is fixed as 60. We first use the OEM algorithm to compute the

SCAD solution with the initial point being the OLS estimator. The tuning parameter in (27) is selected by BIC (Wang, Li, and Tsai 2007). With the same

, we compute the one-step estimator, and compare the variable selection errors (VSEs) and the model errors (MEs) of the two estimators. The VSE and ME of an estimator are respectively defined as

and

where denotes

cardinality and .

OEM

one-step

VSE

1.487 (1.67)

1.111 (1.36)

1.420 (0.67)

1.730 (1.92)

1.441 (1.73)

3.550 (1.14)

3.448 (1.12)

3.060 (1.09)

3.614 (1.26)

3.408 (1.18)

3.294 (1.17)

4.474 (0.96)

ME

0.091 (0.06)

0.084 (0.05)

0.076 (0.07)

0.136 (0.09)

0.123 (0.09)

0.138 (0.14)

1.043 (0.56)

1.048 (0.61)

1.168 (0.63)

1.070 (0.56)

1.090 (0.60)

1.207 (0.64)

Table 5: Average VSEs and MEs of OEM and the one-step estimator (standard deviations in parentheses)

The average VSE and ME values of the two estimators over 1000 times are given in Table 5. The SCAD estimator computed by OEM outperforms the one-step

estimator in most cases, especially when is large.

8.3 REAL DATA EXMAPLE

Consider a dataset from US Census Bureau County and City Data Book 2007. The response is population change in percentage. The covariates include

1.

Economic variables like income per capita, household income, poverty.

2.

Population distribution like percentages of different races, education levels.

3.

Crime rates like violent crimes and property thefts.

4.

Miscellaneous variables like Republic, Democratic, death and birth rates.

These variables are in percentage of population of the individual counties.

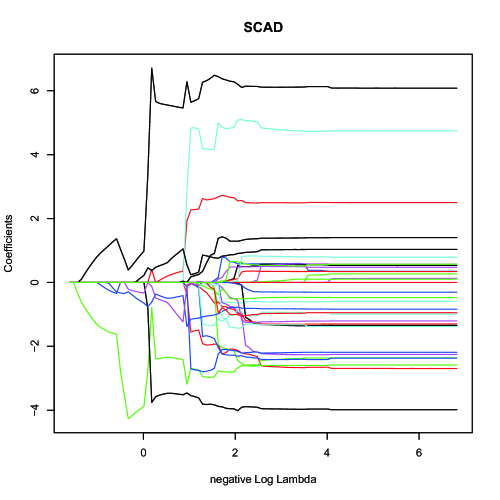

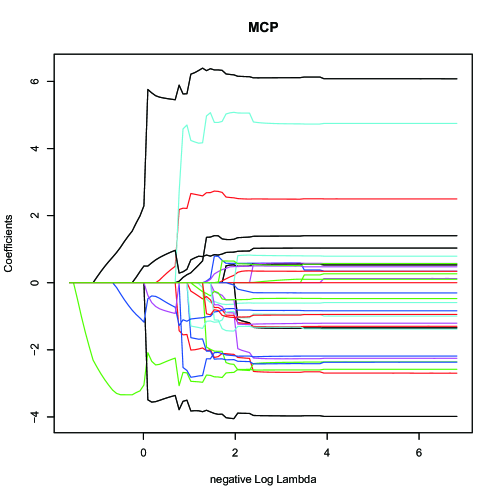

There are (counties) observations without missing observations. The linear regression model in (1) is used to fit the data. The solution paths for the

lasso, SCAD and MCP fitted to the data set are given in Figure 6. The number of non-zero coefficients, cross validation residual sum of squares, AIC and

BIC are presented in Table 6, where the tuning parameter is chose by BIC. The selected significant variables include

•

Percentage of Household income above dollars, which has large positive effect on the percentage of population change.

•

Social security program beneficiaries. The larger the number of beneficiaries in the program, the higher the population change.

•

Both the percentages of retired people and under 18 years old have negative effects since they are major sources of migrants leaving the county.

•

Birth and death rate with positive and negative effects, respectively.

The significant variables reveal that the population change is highly related to the living standards of the counties. Table 6 compares the fitted models from different regularized least squares

problems. Note that MCP has the most sparse model with little sacrifice of CV error, AIC and BIC scores. LASSO has the model with smallest CV error but including nearly

all the candidate predictors. In the example, the regularized models favor complex models with many nonzero coefficients and this reveals the fact that there are

many factors that have profound influence on population change of counties in the US. In addition, the last two columns of Table 6 also give the runtime of

fitting the 10-fold cross-validation to the data, where OEM is implemented in the R package oem, LASSO with CD from glmnet, and SCAD and MCP from

ncvreg.

[0.4]

[0.4]

[0.4]

Figure 6: Solution paths for LASSO, SCAD and MCP for US census bureau data.

Penalty

Final Model

Runtime (s)

Size

CV error

AIC

BIC

OEM

CD

LASSO

SCAD

MCP

Table 6: Lasso, SCAD and MCP results for the U.S. Census Bureau data

9 DISCUSSION

We have proposed a new algorithm called OEM for solving ordinary and regularized least squares problems with general data structures. OEM has unique theoretical properties, including convergence to the

Moore-Penrose generalized inverse-based least squares estimator for singular regression matrices and convergence to a point having grouping coherence for the lasso, SCAD or MCP. Different from existing algorithms, OEM can provide a local solution with the oracle property for the SCAD and MCP penalties. This suggests a new interface between optimization and statistics for regularized methods.

OEM is very fast for big tall data with , such as the data deluge in astronomy, the Internet and marketing (the Economist 2010), large-scale industrial experiments (Xu 2009) and modern simulations in engineering (NAE 2008). For applications for big wide data with like micro-array, OEM is generally slow. We can use a two-stage procedure like that in Fan and Lv (2008) to mitigate this drawback. The first stage uses an efficient screening method to reduce the dimensionality. OEM can be used in the second stage to obtain a SCAD estimator with the oracle property.

An R package for the OEM algorithm has been released. The algorithm can be speeded up by using various methods from the EM literature (McLachlan and Krishnan

2008). For example, following the idea in Varadhan and Roland (2008), one can replace the OEM iteration in (32) by

where

, and . This scheme is found to lead to significant

reduction of the running time in several examples. For problems with very large , one may consider a hybrid algorithm to combine the OEM and coordinate descent ideas.

It partitions in (1) into groups and in each iteration, it minimizes the objective function in (34) by using the OEM algorithm with respect

to one group while holding the other groups fixed. Here are some details. Group as . For ,

solve

(45)

by OEM until convergence. Note that (45) has a much lower dimension than the iteration in (32). For , the hybrid

algorithm reduces to the OEM algorithm and for , it becomes the coordinate descent algorithm. Theoretical properties of this hybrid algorithm will be studied and

reported elsewhere.

Here are additional definitions and notation. Let be the cumulative distribution function of the standard normal random variable. For and in

(27) and in Assumption 6, define

and

The OEM sequence from (28) satisfies the condition that

, where

(46)

For , define two sequences of events and . Without loss of generality, assume

in (1).

Proof of Theorem 8. Since is a fixed point, ,

where . Therefore,

(47)

Thus,

(48)

By (47)

and the fact that is concentratively consistent to , for ,

. By in Assumption 7, . For the other part in (48),

Xiong is partially supported by grant 11271355 of the National Natural Science Foundation of China. Dai is partially support by

Grace Wahba through NIH grant R01 EY009946, ONR grant N00014-09-1-0655 and NSF grant DMS-0906818. Qian is partially supported by NSF grant DMS 1055214. The authors thank Jin Tian for useful discussions, and thank

Xiao-Li Meng, Grace Wahba, the editor, associate editor, and two referees for their comments and suggestions which lead to improvements in the article.

REFERENCES

Ben-Israel, A. and Greville, T. N. E. (2003), Generalized Inverses, Theory and Applications, 2nd ed., New York: Springer.

Bondell, H. D. and Reich, B. J. (2008), “Simultaneous Regression Shrinkage, Variable Selection and Clustering of Predictors With Oscar,” Biometrics 64,

115–123.

Breiman, L. (1995), “Better Subset Regression Using the Nonnegative Garrote,” Technometrics, 37, 373–384.

Breheny, P. and Huang, J. (2011), “Coordinate Descent Algorithms for Nonconvex Penalized Regression, With Applications to Biological Feature Selection,” The

Annals of Applied Statistics, 5, 232–253.

Bühlmann, P. and van de Geer, S. (2011). Statistics for High-Dimensional Data: Methods, Theory and Applications, Berlin: Springer.

Dempster, A. P., Laird, N. M. and Rubin, D. B. (1977),

“Maximum Likelihood from Incomplete Data via the EM Algorithm,” Journal of the Royal Statistical Society, Ser. B, 39, 1–38.

Efron, B., Hastie, T., Johnstone, I. and Tibshirani, R. (2004), “Least Angle Regression,”

The Annals of Statistics, 32, 407–451.

Fan, J. and Li, R. (2001), “Variable Selection via Nonconcave Penalized Likelihood and Its Oracle Properties,”

Journal of the American Statistical Association, 96, 1348–1360.

Fan, J. and Lv, J. (2008)

“Sure Independence Screening for Ultrahigh Dimensional Feature Space (with discussion),”

Journal of the Royal Statistical Society, Ser. B, 70, 849–911.

Fan, J. and Lv, J. (2011). “Properties of Non-concave Penalized Likelihood with NP-dimensionality,” Information Theory, IEEE Transactions, 57, 5467–5484.

Fan, J. and Peng, H. (2004), “Non-concave Penalized Likelihood With Diverging Number of Parameters,” The Annals of Statistics, 32, 928–961.

Frank, L. E. and Friedman, J. (1993), “A Statistical View of Some Chemometrics Regression Tools,” Technometrics, 35, 109–135.

Friedman, J., Hastie, T., Hofling, H. and Tibshirani, R. (2007), “Pathwise Coordinate Optimization,” The Annals of Applied Statistics, 1, 302–332.

Friedman, J., Hastie, T. and Tibshirani, R. (2009), “Regularization Paths for Generalized Linear Models via Coordinate Descent,”

Journal of Statistical Software, 33, 1–22.

Friedman, J., Hastie, T. and Tibshirani, R. (2011), “Glmnet,” R package.

Fu, W. J. (1998), “Penalized Regressions: The Bridge versus the LASSO,” Journal of Computational and Graphical Statistics, 7, 397–416.

Golub, G. H. and Van Loan, C. F. (1996), Matrix computations, 3rd ed., Baltimore: The Johns Hopkins University Press.

Grandvalet, Y. (1998), “Least Absolute Shrinkage is Equivalent to Quadratic Penalization,” In: Niklasson, L., Bodén, M., Ziemske, T. (eds.), ICANN’98. Vol.

1 of Perspectives in Neural Computing, Springer, 201–206.

Green, P. J. (1990), “On Use of the EM Algorithm for Penalized Likelihood Estimation,” Journal of the Royal Statistical Society, Ser. B, 52, 443–452.

Hastie, T. and Efron, B. (2011), “Lars,” R package.

Healy, M. J. R. and Westmacott, M. H. (1956), “Missing Values in Experiments Analysed on Automatic Computers,”

Journal of the Royal Statistical Society, Ser. C, 5, 203–206.

Hoerl, A. E. and Kennard, R. W. (1970), “Ridge Regression: Biased Estimation for Nonorthogonal Problems,” Technometrics, 12, 55–67.

Hunter, D. R. and Li, R. (2005), “Variable Selection Using MM Algorithms,” The Annals of Statistics, 33, 1617–1642.

Huo, X. and Chen, J. (2010), “Complexity of Penalized Likelihood Estimation,” Journal of Statistical Computation and Simulation, 80, 747–759.

Huo, X. and Ni, X. L. (2007), “When Do Stepwise Algorithms Meet Subset Selection Criteria?” The Annals of Statistics, 35, 870–887.

Mazumder, R., Friedman, J. and Hastie, T. (2011), “SparseNet: Coordinate Descent with Non-Convex Penalties,”

Journal of the American Statistical Association, 106, 1125–1138.

Meinshausen, N. and Yu, B. (2009). “Lasso-Type Recovery of Sparse Representations for High-Dimensional Data,” The Annals of Statistics, 37, 246–270.

McLachlan, G. and Krishnan, T. (2008), The EM Algotithm and Extensions, 2nd ed., New York: Wiley.

Meng, X. L. (1994), “On the Rate of Convergence of the ECM Algorithm,” The Annals of Statistics, 22, 326–339.

NAE (2008), “Grand Challenges for Engineering,” Technical report, The National Academy of Engineering.

Nettleton, D. (1999), “Convergence Properties of the EM Algorithm in Constrained Parameter Spaces,” Canadian Journal of Statistics, 27, 639–648.

Osborne, M. R., Presnell, B. and Turlach, B. (2000), “On the LASSO and Its Dual,” Journal of Computational and Graphical Statistics, 9, 319–337.

Owen, A. B. (1994), “Controlling Correlations in Latin Hypercube Samples,” Journal of the American Statistical Association, 89, 1517–1522.

Owen, A. B. (2006), “A Robust Hybrid of Lasso and Ridge Regression,” Technical Report.

Petry, S. and Tutz, G. (2012), “Shrinkage and variable selection by polytopes,” Journal of Statistical Planning and Inference, 9, 48–64.

Schifano, E. D., Strawderman, R. and Wells, M. T. (2010), “Majorization-Minimization Algorithms for Nonsmoothly Penalized Objective Functions,”

Electronic Journal of Statistics, 23, 1258–1299.

The Economist (2010), “Special Report on the Data Deluge, (February 27),” The Economist, 394, 3–18.

Tibshirani, R. (1996), “Regression Shrinkage and Selection via the Lasso,”

Journal of the Royal Statistical Society, Ser. B, 58, 267–288.

Tseng, P. (2001), “Convergence of a Block Coordnate Descent Method for Nondifferentialble Minimization,”

Journal of Optimization Theory and Applications, 109, 475–494.

Tseng, P. and Yun, S. (2009), “A Coordinate Gradient Descent Method for Nonsmooth Separable Minimization,” Mathematical Programming B, 117, 387–423.

Tutz, G. and Ulbricht, J. (2009), “Penalized Regression With Correlation-Based Penalty,” Statistics and Computing, 19, 239–253 .

Varadhan, R. and Roland, C. (2008), “Simple and Globally Convergent Methods for Accelerating the Convergence of Any EM Algorithm,”

Scandinavian Journal of Statistics, 35, 335–353.

Wang, H., Li, R., and Tsai, C-L. (2007), “Tuning Parameter Selectors for the Smoothly Clipped Absolute Deviation Method,” Biometrika, 94, 553–568.

Watkins, D. S. (2002), Fundamentals of Matrix Computations, 2nd ed., New York: Wiley.

Wilkinson, J. H. (1965), The Algebraic Eigenvalue Problem, New York: Oxford University Press.

Witten, D. M. and Tibshirani, R. (2011), “Scout,” R package.

Wu, C. F. J. (1983), “On the Convergence Properties of the EM Algorithm,” The Annals of Statistics, 11, 95–103.

Wu, T. and Lange, K. (2008), “Coordinate Descent Algorithm for Lasso Penalized Regression,” The Annals of Applied Statistics, 2, 224–244.

Xu, H. (2009), “Algorithmic Construction of Efficient Fractional Factorial Designs With Large Run Sizes,” Technometrics, 51, 262–277.

Zangwill, W. I. (1969), Nonlinear Programming: A Unified Approach, Englewood Cliffs, New Jersey: Prentice Hall.

Zhang. C-H. (2010), “Nearly Unbiased Variable Selection under Minimax Concave Penalty,” The Annals of Statistics, 38, 894–942.

Zou, H. and Hastie, T. (2005), “Regularization and Variable Selection via the Elastic Net,”

Journal of the Royal Statistical Society, Ser. B, 67, 301–320.

Zou, H. and Li, R. (2008), “One-step Sparse Estimates in Nonconcave Penalized Likelihood Models,” The Annals of Statistics, 36, 1509–1533.