Measuring Association between Random Vectors

Abstract

This paper suggests five measures of association between two random vectors and . They are copula based and therefore invariant with respect to the marginal distributions of the components and . The measures capture positive as well as negative association of X and Y. In case they reduce to Spearman’s rho. Various properties of these new measures are investigated. Nonparametric estimators, based on ranks, for the measures are derived and their small sample behavior is investigated by simulation. The measures are applied to characterise strength and direction of association of bond and stock indices of five countries over time.

keywords:

Copula , Pearson Correlation , Rank Correlation , Simulation , Bootstrap , Jackknife1 Introduction

Association of two random variables and has been thoroughly investigated in the statistical literature but much less work concerns association of two random vectors and . In the classical statistical framework of multivariate normality and linear correlation the theory of canonical correlation (see Hotelling (1936)) and the socalled RV coefficient (see Escoufier (1973) and Robert and Escoufier (1976)) are well known and often applied, in particular in the natural sciences.

The focus of our application, however, is financial data which is notoriously non-normal. It has further been pointed out (see Embrechts et al. (2002)) that linear correlation might be inappropriate to measure the strength of association of financial data. Finally the above mentioned measures are not capable of distinguishing between positive and negative association which is a must in dealing with financial data.

The recently introduced distance correlation (see Székely et al. (2007) and Székely and Rizzo (2009)) suffers from similar weaknesses. Further it depends on the marginal distributions of and and requires moment restrictions. This should be considered as a disadvantage in application to financial data (see again Embrechts et al. (2002) and Rémillard (2009)).

The increasing use of copulas in the analysis and modeling of financial data suggests the development of copula based measures of association. Concerning association within one vector there exist various such measures (see Schmid et al. (2009) for a recent survey). In this paper, we propose copula based measures of association between two vectors and They are invariant with respect to marginal distributions as association is solely determined by the joint copula of and . Therefore distributional assumptions (beside continuity) as well as moment restrictions are not necessary. The measures are further capable of measuring negative association.

The measures are defined in such a way that they reduce to Spearman’s rank correlation coefficient for Instead of Spearman’s coefficient, other measures, such as Kendall’s coefficient, could have been used. The details of this approach are very similar and are omitted.

Note that it is not the aim of this paper to derive tests for independence of and (see Beran et al. (2007), Kojadinovic and Holmes (2009) and Quessy (2010) for recent contributions). On the contrary the focus is measurement of type and strength of association in the case where and are dependent.

The structure of the paper is as follows: In section 2, we describe the notation and terminology used within the paper. In section 3, we state population versions of the five copula based measures of association and derive some of their properties. For convenience, some calculations are collected in the appendix. Estimators for the measures are introduced in section 4. Their finite sample properties are analysed in a simulation study. Matlab code for the estimators is available on request. Section 5 contains an empirical example with financial data, illustrating the usefulness of the new measures. Section 6 concludes.

2 Notation and definitions

Let and be random vectors of dimensions and , respectively, defined on the same probability space. Throughout the paper we assume that the marginal distribution functions for and for are continuous functions. Therefore, according to the theorem of Sklar (1959) there exists a unique copula with

for and . Extensive portrayals of copulas are given in Nelsen (2006), Joe (1997) and Cherubini et al. (2004). Let

and

The copula is the joint distribution function of . The marginal copulas of and are given by and for and . Here, and denote vectors of ones of length and , respectively. By construction, and are the marginal distribution functions of and , respectively.

3 Population versions of measures of association

This section introduces population versions of five copula based measures of association between random vectors and .

3.1 Mean of pairwise association

The simplest measure of association between and is the mean of all bivariate associations of and for and , i.e.,

where is Spearman’s rho of and . Note that is copula based because of

and is the marginal copula of and (see Nelsen (2006)).

The properties of are easy to derive and follow directly from its definition.

-

1.

We have and the measure is invariant with respect to permutations within and .

-

2.

if and only if for every combination of and , i.e., and are countermonotonic for all and . This implies that

for a random variable and strictly increasing functions and strictly decreasing functions , and it follows that

-

3.

if and only if for every combination and . Here, and are comonotonic for all and . This implies that

for strictly increasing functions and for a random variable . The copula is then

For given and fixed marginal copulas and it is in general not possible to find a copula with and which entails or The latter cases are only possible in the special cases and

-

4.

If and are independent for all combinations and then . The converse is not true as there may be some different from zero, but :

Example 1.

Consider two 2-dimensional random vectors and with the following matrix of Spearman’s rank correlations:

Choosing, for example, and , the matrix is positive semi-definite and thus a correlation matrix. In this case, the random vectors X and Y are clearly dependent, whereas the mean of the pairwise associations is equal to

-

5.

Association as measured by can be decomposed into two parts that describe the association within and between the two random vectors. Let and let denote total association within defined by

where denotes Spearman’s rho of and . Then

Note that

This property might be useful since decomposition of into a between and within part can be interesting in analysing financial data.

3.2 Pearson correlation based measures of association

The vectors and are independent if and only if

for and . Equivalently, and are independent if and only if

for and . Therefore, we may measure the distance of to the independence case of X and Y by

This expression is equal to

where

for and (see Appendix I for a proof).

The covariance is bounded by the product of the respective standard deviations. Thus, a measure of association between and which is bounded by and is

The variances may be expressed by

analogously for (see Appendix I for a derivation). By we denote the component wise minimum of and .

The measure is based on the covariance of and transformed by the functions and An alternative approach is to transform and by their respective distribution functions and (see Nelsen et al. (2003)) and consider the measure of association defined by

It is shown in Appendix I that

and

with an analogous expression for By := we denote component wise maximum of and .

The properties of and are as follows:

-

1.

We have and and the measures are invariant with respect to permutations within and .

-

2.

If the vectors and are independent, and Again, the converse is not true.

-

3.

Measures and are in general not capable to achieve or for given and fixed arbitrary copulas and of and To calculate the maximal and minimal values of, for example, for given copulas and we have to maximise and minimise over all random vectors where the copula of is and the one of is . For fixed and , the only term in the definition of that can vary is

The joint survival function of and will be maximal (minimal) if they are comonotone (countermonotone):

Example 2.

Consider two 2-dimensional random vectors and with copulas and , where is the independence copula and the countermonotone copula. In this case

and

The upper bound is given by

Thus, the maximal association between X and Y in terms of is

Note that similar examples can be given for

3.3 Rank correlation based measures of association

Instead of applying Pearson correlation to and as in or to and as in one may apply rank correlation, leading to the measures and . Let

and

and let and , and . From it follows that

is the joint distribution function and copula of and . Implicitly, since the copula

is the distribution function and copula of Based on these copulas, we define the measures

i.e., Spearman’s rho of and and

i.e., Spearman’s rho of and .

Note that - contrary to the case in section 3.2 - normalisation is not necessary as it is impicitly ensured.

Properties of and

-

1.

We have and and the measures are invariant with respect to permutations within and .

-

2.

If and are independent then and thus . Again, the converse is not true.

-

3.

is equivalent to

and

is equivalent to

and

-

4.

is equivalent to and

is equivalent to

and

-

5.

Contrary to and , the rank correlation based measures and can achieve every value between and for any given and fixed marginal copulas and . To show this for and let be a comonotone pair of random variables such that S has the same distribution as and has the same distribution as . Second, conditionally on let and be independent random vectors whose conditional distributions are given by the one of given and the one of given respectively. Now, the copulas of and are and by construction and due to the comonotonicity of Analogous arguments hold for and

4 Statistical estimation of the measures

In this section we propose nonparametric estimators of the discussed measures. It is assumed that the marginal distribution functions and are unknown for and

Let be i.i.d. samples from Let and denote the empirical distribution function of and for and Then, for

and

are called the pseudo observations of

and

The empirical distribution function of for , i.e.,

is the empirical copula of (see, e.g., Deheuvels (1979)). The marginal empirical copulas of and are estimated by

In the following, estimation is based on the pseudo observations

Estimation of . The estimator for is given by

Estimation of . The estimator for is the Pearson coefficient of correlation of

Estimation of . We first estimate and by

and obtain pseudo observations on and by

is the Pearson coefficient of correlation of these pseudo observations.

Estimation of . In order to estimate we first have to estimate by

for and similarly . Let

and

for . Then with

an estimator for is

Estimation of . The estimator for is derived in a similar way as Let

and

Then

and

for . For

it follows

and thus

We have derived asymptotic normality of and using the asymptotic theory of the copula process introduced by Rüschendorf (1976) (see, e.g., Fermanian et al. (2004) and Segers (accepted) for recent references) and the functional delta method (see, e.g., Van der Vaart and Wellner (1996)). Details can be obtained from the authors. The asymptotic normality of for has not yet been derived.

In the following, the finite sample properties of and , i.e. their bias and standard deviation are investigated by a Monte Carlo simulation. In order to estimate the standard deviation of the estimators, we use the bootstrap and the jackknife.

For a given sample of i.i.d. observations, the bootstrap draws observations of the sample with replacement. Ties are solved by mid-ranks. For bootstrap samples, the standard deviation is estimated by

where is the estimator of the association of the -th bootstrap sample and their mean.

For the jackknife estimator of the standard deviation of let denote the estimator, where the -th observation of is deleted. The jackknife estimate of the standard deviation is then given by

For the simulation study, we consider observations from the Gaussian copula (see Joe (1997)) and the Clayton copula (see Clayton (1978)) with different dimensions and different sample sizes. The Gaussian copula is defined by

where is the distribution function of the multivariate normal distribution with zero mean, unit variances and positive definite correlation matrix . Further, denotes the quantile function of the univariate standard normal distribution.

To reduce the number of parameters in our model, we only consider the case of equi-correlation for the Gaussian copula, although simulations with more complex correlation matrices show similar results. The results are based on 10,000 Monte Carlo simulations and bootstrap iterations, respectively.

Tables 1 to 3 show simulation results with the Gaussian copula for , and for two random vectors of dimensions and and sample sizes and as well as different correlation parameters . Results for the remaining measures and for the Clayton copula are omitted, but can be obtained from the authors. They are, however, very similar to the results presented.

The first two columns in the tables contain the value of the dependence parameters and the sample sizes. The third column of the tables shows an approximation to the true value of the measures of association, which has been derived from samples of size 1,000,000. Comparing the true values to the mean of the estimated associations in column 4, we observe a small finite sample bias, which decreases with increasing sample size. The standard deviation of the estimator and the means of the bootstrap estimation and the jackknife estimation are shown in colums and . It can be seen that both procedures for the estimation of the standard deviation perform well for the Gaussian copula. Furthermore, the standard deviation of the estimator decreases with increasing sample size in a reasonable way. Finally, columns and show that the standard error of the bootstrap standard deviation estimates is slightly smaller than the obtained jackknife estimates.

| n | ||||||||

|---|---|---|---|---|---|---|---|---|

| Two 3-dimensional vectors | ||||||||

| -0.1 | 50 | -0.096 | -0.094 | 0.040 | 0.039 | 0.040 | 0.007 | 0.007 |

| 100 | -0.096 | -0.095 | 0.027 | 0.028 | 0.028 | 0.003 | 0.003 | |

| 500 | -0.096 | -0.096 | 0.012 | 0.012 | 0.012 | 0.001 | 0.001 | |

| 0.2 | 50 | 0.191 | 0.188 | 0.063 | 0.063 | 0.064 | 0.008 | 0.008 |

| 100 | 0.191 | 0.189 | 0.045 | 0.044 | 0.045 | 0.004 | 0.004 | |

| 500 | 0.191 | 0.191 | 0.020 | 0.020 | 0.020 | 0.001 | 0.001 | |

| 0.5 | 50 | 0.483 | 0.474 | 0.069 | 0.070 | 0.071 | 0.007 | 0.008 |

| 100 | 0.483 | 0.479 | 0.049 | 0.049 | 0.049 | 0.004 | 0.004 | |

| 500 | 0.483 | 0.482 | 0.022 | 0.022 | 0.022 | 0.001 | 0.001 | |

| Two 4-dimensional vectors | ||||||||

| -0.1 | 50 | -0.096 | -0.094 | 0.028 | 0.027 | 0.028 | 0.005 | 0.005 |

| 100 | -0.096 | -0.095 | 0.019 | 0.019 | 0.020 | 0.003 | 0.003 | |

| 500 | -0.096 | -0.095 | 0.009 | 0.009 | 0.009 | 0.001 | 0.001 | |

| 0.2 | 50 | 0.191 | 0.188 | 0.054 | 0.054 | 0.055 | 0.007 | 0.007 |

| 100 | 0.191 | 0.189 | 0.038 | 0.038 | 0.039 | 0.004 | 0.004 | |

| 500 | 0.191 | 0.191 | 0.017 | 0.017 | 0.017 | 0.001 | 0.001 | |

| 0.5 | 50 | 0.483 | 0.474 | 0.064 | 0.064 | 0.065 | 0.006 | 0.007 |

| 100 | 0.483 | 0.478 | 0.045 | 0.045 | 0.046 | 0.003 | 0.003 | |

| 500 | 0.483 | 0.481 | 0.020 | 0.020 | 0.020 | 0.001 | 0.001 | |

| n | ||||||||

|---|---|---|---|---|---|---|---|---|

| Two 3-dimensional vectors | ||||||||

| -0.1 | 50 | -0.225 | -0.218 | 0.104 | 0.113 | 0.110 | 0.029 | 0.038 |

| 100 | -0.225 | -0.220 | 0.071 | 0.072 | 0.073 | 0.018 | 0.021 | |

| 500 | -0.225 | -0.225 | 0.031 | 0.031 | 0.031 | 0.005 | 0.005 | |

| 0.2 | 50 | 0.349 | 0.335 | 0.146 | 0.143 | 0.155 | 0.021 | 0.030 |

| 100 | 0.349 | 0.343 | 0.103 | 0.102 | 0.106 | 0.012 | 0.015 | |

| 500 | 0.349 | 0.347 | 0.046 | 0.046 | 0.046 | 0.003 | 0.003 | |

| 0.5 | 50 | 0.682 | 0.664 | 0.095 | 0.098 | 0.100 | 0.021 | 0.025 |

| 100 | 0.682 | 0.673 | 0.066 | 0.066 | 0.067 | 0.012 | 0.012 | |

| 500 | 0.682 | 0.681 | 0.029 | 0.029 | 0.029 | 0.003 | 0.002 | |

| Two 4-dimensional vectors | ||||||||

| -0.1 | 50 | -0.235 | -0.226 | 0.073 | 0.123 | 0.087 | 0.025 | 0.033 |

| 100 | -0.235 | -0.231 | 0.048 | 0.058 | 0.054 | 0.013 | 0.015 | |

| 500 | -0.235 | -0.234 | 0.021 | 0.021 | 0.021 | 0.003 | 0.003 | |

| 0.2 | 50 | 0.388 | 0.370 | 0.157 | 0.151 | 0.168 | 0.025 | 0.045 |

| 100 | 0.388 | 0.378 | 0.110 | 0.108 | 0.115 | 0.016 | 0.023 | |

| 500 | 0.388 | 0.387 | 0.050 | 0.049 | 0.050 | 0.004 | 0.004 | |

| 0.5 | 50 | 0.723 | 0.666 | 0.094 | 0.097 | 0.099 | 0.021 | 0.026 |

| 100 | 0.723 | 0.674 | 0.065 | 0.066 | 0.067 | 0.011 | 0.012 | |

| 500 | 0.723 | 0.721 | 0.028 | 0.028 | 0.028 | 0.003 | 0.003 | |

| n | ||||||||

|---|---|---|---|---|---|---|---|---|

| Two 3-dimensional vectors | ||||||||

| -0.1 | 50 | -0.310 | -0.250 | 0.126 | 0.133 | 0.147 | 0.010 | 0.017 |

| 100 | -0.310 | -0.277 | 0.091 | 0.089 | 0.100 | 0.006 | 0.008 | |

| 500 | -0.310 | -0.302 | 0.041 | 0.039 | 0.042 | 0.002 | 0.001 | |

| 0.2 | 50 | 0.375 | 0.330 | 0.123 | 0.118 | 0.135 | 0.012 | 0.016 |

| 100 | 0.375 | 0.353 | 0.086 | 0.083 | 0.092 | 0.007 | 0.008 | |

| 500 | 0.375 | 0.369 | 0.039 | 0.038 | 0.040 | 0.002 | 0.002 | |

| 0.5 | 50 | 0.694 | 0.635 | 0.081 | 0.084 | 0.090 | 0.015 | 0.019 |

| 100 | 0.694 | 0.665 | 0.057 | 0.057 | 0.060 | 0.008 | 0.010 | |

| 500 | 0.694 | 0.688 | 0.025 | 0.025 | 0.025 | 0.002 | 0.002 | |

| Two 4-dimensional vectors | ||||||||

| -0.1 | 50 | -0.462 | -0.265 | 0.110 | 0.150 | 0.144 | 0.011 | 0.021 |

| 100 | -0.462 | -0.337 | 0.085 | 0.101 | 0.102 | 0.007 | 0.010 | |

| 500 | -0.462 | -0.428 | 0.038 | 0.036 | 0.040 | 0.002 | 0.002 | |

| 0.2 | 50 | 0.433 | 0.356 | 0.118 | 0.116 | 0.137 | 0.012 | 0.017 |

| 100 | 0.433 | 0.394 | 0.085 | 0.080 | 0.092 | 0.007 | 0.009 | |

| 500 | 0.433 | 0.426 | 0.037 | 0.036 | 0.038 | 0.002 | 0.002 | |

| 0.5 | 50 | 0.740 | 0.667 | 0.077 | 0.080 | 0.086 | 0.015 | 0.020 |

| 100 | 0.740 | 0.704 | 0.052 | 0.052 | 0.055 | 0.008 | 0.010 | |

| 500 | 0.740 | 0.733 | 0.022 | 0.022 | 0.023 | 0.002 | 0.002 | |

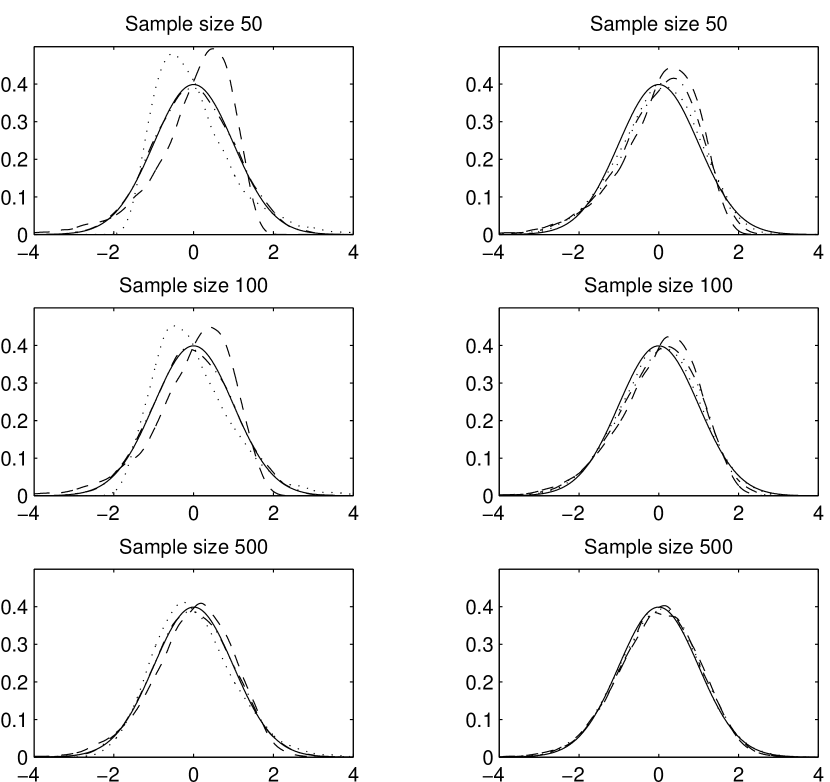

We further investigate how well the finite sample distribution of the introduced empirical measures of association can be approximated by the normal distribution. To this end, we compute and for 10,000 Monte Carlo simulations from two -dimensional random vectors from the Gaussian copula and the Clayton copula. For each copula, we use different dependence parameters and various sample sizes. We standardise the 10,000 measures obtained from the Monte Carlo simulation by their sample mean and standard deviation, respectively, and use a kernel estimator to approximate their density.

The left panel of figure 1 shows the results for in case of the Gaussian copula, where the correlation matrix has the form

with and . Whereas the density of the estimator is highly skewed for and for a sample size of , this asymmetry vanishes with increasing sample size and the density of the for all of the considered values of is barely distinguishable from the normal density for a sample size of 500. It has to be noted that and are the upper and lower bound of such that is a correlation matrix. For values closer to , the asymmetries are smaller.

The right panel of figure 1 shows the results for a Clayton Copula with parameters and . Again, we used to measure the association. The other measures, however, show similar results, which are available upon request by the authors. For a sample size of , the density of the estimator is slightly skewed for all parameters, nevertheless the highest skewness occurs for . As for the Gaussian copula, the skewness decreases with increasing sample size and is barely observable for a sample size of 500.

Having performed similar Monte Carlo simulations for other dimensions and dependence parameters, we conclude that for a sample size of the finite sample distribution of the association measure can very well be approximated by the normal distribution.

5 Empirical example

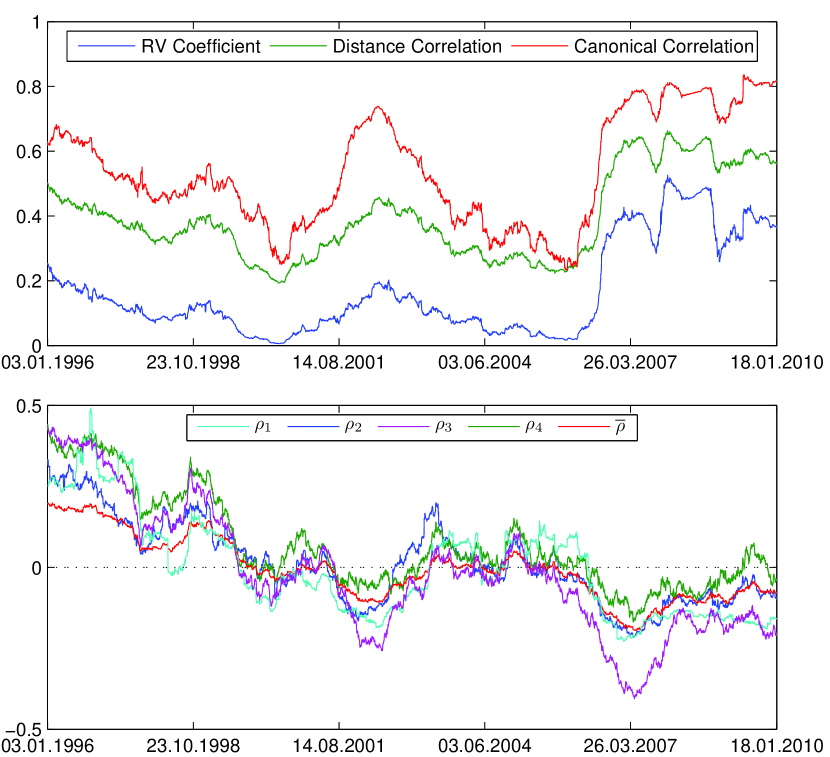

In our empirical example we make an attempt to measure strength and direction of association of the bond and the stock market. We make use of the five copula based measures of association presented in section 3. Moreover, for the sake of comparison, the traditional canonical correlation, the RV coefficient and distance correlation are applied. We consider daily returns of the stock market indices of five major countries111All Ordinaries (Australia), CAC 40 (France), DAX (Germany), Nikkei 225 (Japan) and S&P 500 (USA) as well as government bonds indices from The Bank of America Merrill Lynch 222The BofA Merrill Lynch Australia Government Index (G0T0), The BofA Merrill Lynch French Government Index (G0F0), The BofA Merrill Lynch Japan Government Index (G0Y0), The BofA Merrill Lynch German Government Index (G0D0) and The BofA Merrill Lynch Australia Government Index (G0T0) for the respective countries during the period from January 3rd, 1996 to December 30th, 2010. Figure 2 shows the evolution of the association of bond and stock market, based on a forward-looking moving window with a window size of 250 days. In particular, the first value of each measure is based on the 250 daily returns following January, 2rd, 1996. The last value is estimated from the 250 daily returns from January 18th, 2010 until the end of 2010. The top panel shows that canonical correlation, distance correlation and the RV coefficient exhibit similar patterns of association. Their scaling is quite different, however. Canonical correlation is always highest, RV coefficient always lowest. Distance correlation is somehow between the two, but closer to the canonical correlation in general. The evolution of association over time as indicated by the five measures and is shown in the bottom panel. The differences between their values are in general smaller than these of the aforementioned measures. The evolution of seems to be smoothest which is not surprising, while is most erratic. It can be seen that there is a tendency of decreasing association from 1996 to 2002, association is close to zero between 2002 and 2006 and becomes negative afterwards. A pattern of association like this can only be recorded by using measures of the type which we introduced in section 3. Note that the identified pattern of association is an empirical finding, for which we do not attempt to provide an economic explanation. The graphs in figure 2 are based on the returns themselves. We have, however, made similar graphs for filtered data where autocorrelation and heteroscedasticity have been removed. The results for the filtered data are very close to those of the unfiltered data.

6 Conclusion

Five measures of association between two random vectors and have been introduced. They are copula based and do therefore not depend on the marginal distributions of the components and They measure strength and direction of association, so they are capable of distinguishing positive and negative association. This is a substantial advantage in applications to real life data, in particular financial data. Estimators for the measures have been proposed and it was demonstrated by simulation that they have favorable small sample properties at least for There is space for extension and complementation of the measures. First, it can be seen that the measures have in common that they are based on transformations and , say, where and may, or may not, depend on the marginal copulas and Therefore more general classes of measures can be defined, if further measures of bivariate association are applied to and

Second, measures for association between vectors of dimensions respectively, can be defined if measures of -variate association (see, e.g., Schmid and Schmidt (2007)) are applied to for appropriate functions

7 Acknowledgements

Funding for Johan Segers’ research was provided by IAP research network grant P6/03 of the Belgian government (Belgian Science Policy) and by “Projet d’actions de recherche concertées” number 07/12/002 of the Communauté française de Belgique, granted by the Académie universitaire de Louvain. Funding in support of Julius Schnieders’ work was provided by the Deutsche Forschungsgemeinschaft (DFG). Morever, we are grateful to the Regional Computing Center at the University of Cologne for providing the computational resources required.

References

References

- Beran et al. (2007) Beran, R., Bilodeau, M., Lafaye de Micheaux, P., 2007. Nonparametric tests of independence between random vectors. Journal of Multivariate Analysis 98 (9), 1805–1824.

- Cherubini et al. (2004) Cherubini, U., Luciano, E., Vecchiato, W., 2004. Copula methods in finance. Wiley.

- Clayton (1978) Clayton, D., 1978. A model for association in bivariate life tables and its application in epidemiological studies of familial tendency in chronic disease incidence. Biometrika 65, 141–151.

- Deheuvels (1979) Deheuvels, P., 1979. La fonction de dépendance empirique et ses propriétés. Acad. Roy. Belg. Bull. Cl. Sci. 65 (5), 274–292.

- Embrechts et al. (2002) Embrechts, P., McNeil, A., Straumann, D., 2002. Risk Management: Value at Risk and Beyond. Cambridge University Press, Ch. Correlation and dependency in risk management: properties and pitfalls, pp. 176–223.

- Escoufier (1973) Escoufier, Y., 1973. Le traitment des variables vectorielles. Biometrics 29 (4), 751–760.

- Fermanian et al. (2004) Fermanian, J.-D., Radulović, D., Wegkamp, M., 2004. Weak convergence of empirical copula processes. Bernoulli 10 (5), 847–860.

- Hotelling (1936) Hotelling, H., 1936. Relations between two sets of variates. Biometrika 28, 321–377.

- Joe (1997) Joe, H., 1997. Multivariate Models and Dependence Concepts. Chapman & Hall, London.

- Kojadinovic and Holmes (2009) Kojadinovic, I., Holmes, M., 2009. Tests of independence among continuous random vectors based on cramér-von mises functionals of the empirical copula process. Journal of Multivariate Analysis 100, 1137–1154.

- Nelsen (2006) Nelsen, R. B., 2006. An Introduction to Copulas, 2nd Edition. Springer Series in Statistics. Springer, New York.

- Nelsen et al. (2003) Nelsen, R. B., Quesada-Molina, J. J., Rodríguez-Lallena, J. A., Úbeda Flores, M., 2003. Kendall distribution functions. Statistics & Probability Letters 65 (3), 263 – 268.

- Quessy (2010) Quessy, J., 2010. Applications and asymptotic power of marginal-free tests of stochastic vectorial independence. Journal of Statistical Planning and Inference 140, 3058–3075.

- Rémillard (2009) Rémillard, B., 2009. Discussion of: Brownian distance covariance. The Annals of Applied Statistics 3 (4), 1295–1298.

- Robert and Escoufier (1976) Robert, P., Escoufier, Y., 1976. A unifying tool for linear multivariate statistical methods: the rv-coefficient. Appl. Statist. 25 (3), 257–265.

- Rüschendorf (1976) Rüschendorf, L., 1976. Asymptotic distributions of multivariate rank order statistics. Annals of Statistics 4 (5), 912–923.

- Schmid et al. (2009) Schmid, F., Schmid, R., Blumentritt, T., Gaisser, S., Ruppert, M., 2009. Copula-based measures of multivariate association. In: Jaworski, P., Durante, F., Härdle, W., Rychlik, T. (Eds.), Copula Theory and its applications. Lecture Notes in Statistics - Proceedings.

- Schmid and Schmidt (2007) Schmid, F., Schmidt, R., 2007. Multivariate extensions of spearman’s rho and related statistics. Statistics Probability Letters 77 (4), 407–416.

- Segers (accepted) Segers, J., accepted. Asymptotics of empirical copula processes under nonrestrictive smoothness assumptions. Bernoulli, ArXiv:1012.2133v2.

- Sklar (1959) Sklar, A., 1959. Fonctions de réparation à n dimensions et leurs marges. Publ. Inst. Statist. Univ. Paris 8, 229–231.

- Székely and Rizzo (2009) Székely, G., Rizzo, M., 2009. Brownian distance covariance. The Annals of Applied Statistics 3 (4), 1236–1265.

- Székely et al. (2007) Székely, G., Rizzo, M., Bakirov, N., 2007. Measuring and testing dependence by correlation of distances. Ann. Statist. 35 (6), 2769–2794.

- Van der Vaart and Wellner (1996) Van der Vaart, A. W., Wellner, J. A., 1996. Weak convergence and empirical processes. Springer Verlag, New York.

8 Appendix I

-

1.

Let and

Then

-

2.

Consider and

We then have

and

Further

and

Therefore

The measure to be defined is therefore based on the weighted difference

where the weights are given by and .

Further