Instituto Superior de Ciências Sociais e Políticas (ISCSP), Technical University of Lisbon

Quantum Financial Economics - Risk and Returns

Abstract

Financial volatility risk and its relation to a business cycle-related intrinsic time is addressed through a multiple round evolutionary quantum game equilibrium leading to turbulence and multifractal signatures in the financial returns and in the risk dynamics. The model is simulated and the results are compared with actual financial volatility data.

keywords:

Quantum Financial Economics, Business Cycle Dynamics, Intrinsic Time, Quantum Chaotic VolatilityE-mail: cgoncalves@iscsp.utl.pt

1 Introduction

Ever since Mandelbrot identified the presence of multifractal turbulence in the markets [15, 16, 17], this empirical fact has become a major research problem within financial economics.

Mandelbrot [15, 16] hypothesized that financial systems’ dynamics has to be addressed in terms of an intrinsic temporal notion, linked to the economic rhythms and (chaotic) business cycles. Such intrinsic time would not be measured in clock time, but in terms of economic rhythms that would rescale volatility with the usual square root rule that holds for clock-based temporal intervals.

In the present work, we return to such a proposal, providing for a quantum game theoretical approach to market turbulence with chaotic intrinsic time leading to multifractal signatures in volatility dynamics. The approach followed is that of path-dependent quantum adaptive computation within the framework of quantum game theory, such that a game is divided in rounds and, for each round, an equilibrium condition is formalized in terms of a payoff quantum optimization problem, subject to: (1) a time-independent Schrödinger equation for the round; (2) an update rule for the Hamiltonian, depending on some evolutionary parameter(s)111The time-independent Schrödinger equation can be addressed either as attaching an eigenstate to the whole round, for the game’s result, or as assigning it to the round’s end, and the change in the parameters leads to a change in the time-independent equation for the round, given the previous round. In [9], such approach with discrete game rounds was also considered, with unitary evolution between each two rounds. In the present case, instead of a unitary evolution operator, we have a quantum optimization problem per round, leading to a quantum strategy formulation. For the game proposed in [9] the two approaches are, actually, equivalent, since they form part of the underlying approach to the path-dependent quantum computation approach to quantum games..

The Hamiltonian for the time-independent Schrödinger equation constitutes a quantum evolutionary expansion of the classical harmonic oscillator approaches to the business cycle dynamics in economics [11, 8, 24, 19, 7], thus, leading to a quantum business cycle approach to business financial valuation by a financial market, such that a clock time independent quantum state is associated with each round, where business-cycle related financial intrinsic time results from the quantum game itself, without any stochastic temporal subordination over clock time [15, 16].

The model, therefore, incorporates the business cycle by adapting the standard economic tradition, in business cycle dynamics modelling, in particular, extending to the quantum setting a standard harmonic oscillator model of the business cycle, within the context of an adaptive quantum business optimization problem with nonlinear evolutionary conditions.

The present model’s main objective is to translate into a quantum repeated game setting what consitutes Mandelbrot’s hypothesis of economic complexity with financial market efficiency, such that turbulence and multifractal signatures do not come from anomalous trading behavior or speculative trading systems, but from the business cycle nonlinear dynamics, that is, from underlying economic evolutionary dynamics affecting a company’s fundamental value in a value efficient financial market, such that trading accurately reflects that underlying economic business cycle dynamics in the markets’ turbulent volatility dynamics.

Our present goal is, therefore, to contribute to the discussion within financial economics, regarding the issue of business cycle-related trading time, raised by Mandelbrot as a criticism to the empirical validity of the geometric Brownian motion and geometric random walk models of price dynamics, used in financial economics as mathematical tools for solving pricing problems.

In section 2., we provide for a brief review of financial economics and quantum financial economics, laying down the background to the present work in its connection with other works and with the general field of financial economics. In section 3., we introduce the model and address the main findings from the model’s simulation. In section 4., we address the implications of the model for financial economics.

2 Financial Economics

Financial economics is a branch of economic theory which deals with a combination of mathematical finance tools with economic theories, applying these to the context of financial problems dealing with time, uncertainty and resource management (in particular allocation and deployment of economic resources), as stressed by Merton [18].

Earlier models in quantum financial economics have worked with quantum Hamiltonian proposals, including harmonic oscillator potentials and applications of quantum theory to option pricing, most notably one may quote: Segal and Segal [30], which constitutes one of the earliest works in quantum option pricing theory, as well as Baaquie’s quantum path-integral approach to option pricing with stochastic volatility [1, 2, 3, 4], who largely divulged the quantum formalism to the financial economics community, by applying it to problems that are specific of that research area, this is explored in depth in the work [3], with the presentation and explanation of path-integral examples taken from quantum mechanics, including the quantum harmonic oscillator, and with the application to several examples from financial economics. Simultaneously to Baaquie, still within the specific area of quantum applications to financial economics, one may also quote the work of Schaden [27, 28, 29], to name but a few of the early works in the field of quantum financial economics.

Along with quantum financial economics one may also refer the parallel and related research field of quantum financial game theory, specifically the work of Piotrowski and Sladkowski [20, 21, 22] who applied quantum game theory to financial theory, and Gonçalves and Gonçalves [9], who proposed and tested empirically a model of a quantum artificial financial market.

Regarding the quantum harmonic oscillator approach, as a specific formulation within quantum financial game theory, one may refer both Ilinsky [12], who addressed a financial interpretation of the quantum harmonic oscillator, as well as the above quoted work of Piotrowski and Sladkowski [20, 21, 22]. Regarding Piotrowski and Sladkowski’s work, the main difference, in regards to the current approach is that the quantum harmonic oscillator proposed in [20, 21, 22] resulted from a financial operator related to speculators’ buying and selling strategies and risk profiles, while, in our case, it is a quantum extension based upon a tradition of non-quantum economics business cycle modelling, such that the quantum Hamiltonian, in our case, is a company’s strategic operator related to that company’s business value dynamics and the quantum optimization problem is linked to the company’s economic risk management process, which is consistent with the fact that we are dealing with business economic risk linked to the business cycle that is reflected in the stock market price by value investors, thus, leading to a value efficient financial market, as per Mandelbrot’s hypothesis of a financial system which is efficient in intrinsic time [15, 16, 17].

Therefore, while the quantum Hamiltonian operator proposed in [20, 21, 22] constitutes a risk inclination operator and the (financial) mass term corresponds to a financial risk asymmetry in buying and selling strategies, in the model addressed here, the mass term corresponds to a round-specific measure of business economic evolutionary pressure divided by business cycle frequency, therefore, it has an economic business-related interpretation, similarly the harmonic oscillator oscillation frequency corresponds to the business cycle oscillation frequency.

All the variables in the optimization problem, that are worked with in the present model, stem from an expansion of basic business cycle evolutionary economic dynamics to the quantum setting. Therefore, the roots of the present model lie in the classical mechanics-based business cycle economics, addressed from an evolutionary perspective with contra-cyclical adaptive dynamics, resulting from Püu’s review and from proposals regarding chaotic dynamical models for the business cycle [24, 10, 13].

Having circumscribed the approach within the appropriate literature, we are now ready to introduce the model.

3 A Quantum Financial Game and Quantum Financial Economics

Let be the financial market price of a company’s shares, transactioned synchronously by traders, in discrete rounds, at the end of each round, and let be a rate of return, such that:

| (1) |

with:

| (2) |

where is a fixed average return, is the duration of a game’s round, is a fixed volatility component.

The subscript labels the round in accordance with its final transaction time, , as is the usual framework in game theory for a repeated game, where each round corresponds to an iteration of the game with the same game conditions (fixed repeated game) or with evolving conditions (evolutionary repeated game).

Considering a financial market composed by value investors, it is assumed that market participants accurately evaluate the company’s fundamental value such that is a fair return on the company’s shares. In this way, the variable represents a volatility adjusted component representing, in a market dominated by value investors, a company’s value fitness, which is related to the company’s business growth prospects.

If we were dealing with classical economic business cycle dynamics, one might consider the dynamics for to be driven by the harmonic oscillator potential , where the parameter is the business evolutionary pressure, which includes the ability of the company to quickly adapt to adverse economic conditions, as well as increased business growth restrictions, such that: the higher the value of is, the more competitive is the business environment. Unlike in physics, within the economic setting, the parameter is considered dimensionless.

In the economic potential we have that: signals negative factors and possibly a downward period in the business cycle dynamics, while signals positive factors and possibly business grown, thus, in the harmonic oscillator potential, it is assumed that negative is dampened by actions on the part of the company towards the recovery, while positive may be dampened by business growth restrictions, which includes competition with other companies.

The existence of such contra-cyclical dynamics, affecting both positive and negative business cycle processes is formalized by the harmonic oscillator potential. Such potentials have been widely used within the economic modelling of business cycles, appearing in the dynamics of the multiplier and accelerator as well as in the Frischian tradition to the business cycle modelling [11, 8, 24, 19, 7]. In the present case, the evolutionary interpretation comes from a combination of Püu’s work [24] on the business cycle dynamics with related chaotic evolutionary coupled map lattice proposals [10].

Within a quantum game setting, we consider a repeated business game. The general form of a quantum repeated game, addressed here, is such that the game is divided in rounds, with a fixed Hilbert space, and at each round an optimization problem is assigned with eigenvalue restrictions holding for the round. Thus, given an appropriate payoff operator, the game is completely defined by a sequence of optimization problems leading to a round-specific sequence of game equilibrium wave functions which solve the sequence of optimization problems.

In the present case, we introduce the fitness operator , satisfying the eigenvalue equation:

| (3) |

Since ranges in , it follows that the spectrum is continuous and the kets and the bras are not in a Hilbert space, rather, it becomes necessary to work with a rigged Hilbert space222Well known to the complexity approach to economics’ community, in particular those linked to applications of the Brussels-Austin Schools and Prigogine’s works on complex systems [23, 6] given by the Gelfand triplet , where [14]: (the space of test functions) is a dense subspace of the game’s Hilbert space , arises from the requirement that the wave functions , which correspond to the quantum strategic configurations, be square normalizable and (the space of distributions) is the space of antilinear functionals over , such that . Similarly, to address the bras, we have to work with the triplet , where is the space of the linear functionals over , such that [14]: .

In a repeated quantum game, there is a quantum strategy for each round of the game, therefore, it becomes natural to index the wave function by the corresponding round index in order to identify to which round it belongs, thus, is the quantum strategic configuration for the -th round.

Each round’s strategic configuration results from a quantum optimization problem defining a quantum business game evolutionary equilibrium. The optimization is defined in terms of the squared operator , such that the higher is the round’s expected value for , denoted by , the higher is the company’s economic risk, this means that higher absolute values for returns correspond to higher financial volatility risk linked, in this case, to economic volatility risk, while lower returns in absolute value correspond to smaller volatility risk.

To assume that the company adapts to business economic volatility risk means that the quantum game equilibrium is defined in terms of the minimization of risk, that is, the fitness dispersion is kept as low as possible as well as the returns, making risk smaller, this is achieved by minimizing , or, alternatively, maximizing its negative , since . In order to be more straightforward, in regards to an economic interpretation, we define the optimization game in terms of the company’s risk minimization objective , rather than in terms of the equivalent maximization of a negative payoff, this leads to the following round-specific economic business-cycle volatility minimization problem for the company:

| (6) |

The quantum business cycle Hamiltonian operator translates to the financial economic setting, with a few adaptation in units. Indeed, energy is, in this case, expressed in units of returns and the shares’ Planck-like constant plays a similar role to that of quantum mechanics’ Planck constant, indeed, the quanta of energy for the quantum harmonic oscillator game’s restrictions at round are:

| (7) |

where represents the angular frequency of oscillation of the business cycle for the round , expressed as radians over clock time333It should be stressed that is associated with the round itself, as a part of the game’s restrictions and the subscript identifies the angular frequency as such, and not as a continuous clock time dependency. One may assume, alternatively, that is assigned to the round’s end where the decision takes place with a wave function that results from the optimization problem presented in the text., and is expressed as , where is expressed in units of returns over the business cycle oscillation frequency for the round , such oscillation frequency is, in turn, obtained from , thus, being expressed in terms of the number of business-related oscillation cycles per clock time.

We also consider a business cycle-related mass-like term which can be obtained from the relation:

| (8) |

leading to:

| (9) |

thus, since is dimensionless, the business cycle mass-like term is expressed in units of inverse squared angular frequency.

Solving, first, for the quantum Hamiltonian restrictions, the feasible set of quantum strategies is obtained, for the round, as the eigenfunctions of the quantum harmonic oscillator:

| (10) |

| (11) |

The round specific expected risk for each alternative strategy is, then, given by:

| (12) |

Minimization of expected risk by the company leads to:

| (13) |

Therefore, the quantum game’s evolutionary equilibrium strategy is the eigenfunction for the zero-point energy solution of the quantum harmonic oscillator:

| (14) |

where is a business cycle-related volatility parameter defined as:

| (15) |

which makes explicit the connection between the quantum game equilibrium strategy for the round and the risk optimization problem.

Introducing the volatility component , such that:

| (16) |

that is, is equal to the expected value of the quantum harmonic oscillator’s kinetic energy for the round, divided by the evolutionary pressure constant, thus, is called kinetic volatility component. Replacing in , we obtain:

| (17) |

The final result of this quantum game, for the financial returns, is the returns’ wave function for the game round:

| (18) |

In the Gaussian random walk model of financial returns, within neoclassical financial theory, the following density is assumed [16]:

| (19) |

where is a discrete time step.

Mandelbrot’s proposal is that the business cycle-related intrinsic time lapse should be used instead of the clock time interval of , the business cycle rhythmic time444Volume, absolute returns or any other relevant such measure have been used as surrogates for such intrinsic market time, any such notion that can define a sequence of steps on a devil’s staircase can represent a form of intrinsic time, which does not coincide with clock time units. Intrinsic time is, thus, assumed to be financial business cycle-related time which is usually measured in financially relevant units [16]. marks a round duration that does not numerically coincide with a clock time interval, but rather with an intrinsic business cycle time interval, for the round , denoted by which affects the volatility as follows:

| (20) |

thus, the intrinsic time frame is expressed not in clock time but in units of returns related to the financial energy, as explained earlier. The intrinsic temporal sequence is, thus, given by , this sequence naturally defines a nondecreasing sequence. When has a turbulent stochastic behavior, the sequence leads to a devil’s staircase, corresponding to a turbulent intrinsic time related to the business cycle rhythmic time.

The corresponding Gaussian probability density is, in this case, given by:

| (21) |

the two temporal notions, that of clock time and that of intrinsic time, appear in the density. The clock time appears multiplying by the average returns, since the evidence is favorable that the intrinsic time is directly related to market volatility rather than to the average returns555That is, the market seems to evaluate the average returns with a clock temporal scale, while the volatility scales in intrinsic time, which is related to the fact that the volatility is linked to transaction rhythms and to the business cycle risk processing by the markets [15, 16]..

Turbulence, power-law scaling and multifractal signatures arise, in the model, from the dynamics of , through the following power-law map:

| (22) |

with parameters and . The above map is conjugate to the coupled shift map:

| (23) |

through the power law relation defined over the kinetic volatility component666The power law dependency is to be expected, following Mandelbrot’s empirical work, which shows that economic processes seem to lead to scale invariance in risk dynamics[15, 16, 17].:

| (24) |

From conjugacy with the shift map it follows that, when , the following normalized invariant density holds for :

| (25) |

with normalization achieved from division by . Therefore, is a scaling power-law parameter related to the volatility statistical distribution, such that if we write , and , we obtain the power-law density:

| (26) |

which is consistent with evidence from power-law volatility scaling in the financial markets [15, 16, 17].

The Bernoulli shift map for the dynamics of formalizes a dynamics of business cycle-related expansion and contraction in volatility conditions with a uniform invariant density777Conceptually, the variable can be interpreted as synthesizing risk factors associated with fundamental value, that is, to fundamental value risk drivers.. The Bernoulli map is coupled to the previous round’s financial returns, formalizing a feedback from the market itself upon the economic behavior of the volatility fundamentals . For a coupling of , the quantum feedback affects the chaotic map, leading to a situation in which the previous round’s volatility, measured by the absolute returns, affects the current round’s chaotic dynamics.

Taking all of the elements into account, the final quantum game’s structure is given by:

| (27) |

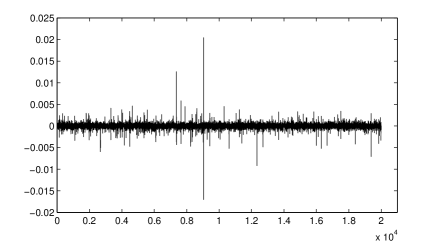

In figure 1, is shown the result of a simulation of the quantum financial game with this structure. The presence of market turbulence can be seen in the financial returns series, resulting from the Gaussian density shown in Eq.(21).

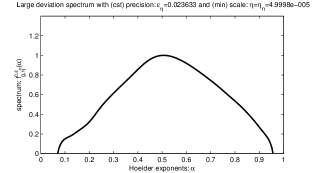

In figure 2, a multifractal large deviation spectrum (estimated with Fraclab) is presented for the financial returns, showing a peak around 0.5, which is in accordance with Mandelbrot, Fisher and Calvet’s hypothesis of multifractal financial efficiency [15, 16, 17].

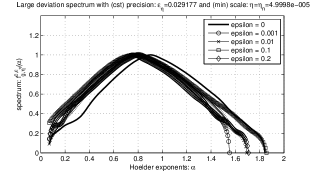

In figure 3, the multifractal spectra for the dynamics of is shown, assuming three different values for the coupling parameter. The presence of multifractality for shows that the chaotic dynamics is responsible for the emergence of the turbulence and multifractal scaling, thus, we are dealing with multifractal chaos with origin in the nonlinear dynamics of business cycle volatility risk888The presence of chaos in business cycles is a known empirical fact [7], the current model addresses that chaos in connection to volatility..

For , the quantum fluctuations that affect the dynamics for seem to lead to a lower value of the peak of the multifractal spectrum, indicating a higher irregularity in the motion. On the other hand, when , there emerges a multifractal spectrum with a peak that is closer to 1, showing evidence of higher persistence and more regular dynamics. For all of the couplings, however, there is evidence of persistence in the dynamics of , which is in accordance with previous findings for the financial markets and business cycles’ empirical data [15, 16, 17, 12].

One can also identify, in the volatility spectra of the simulations, Hölder exponents larger than 1, which is characteristic of turbulent processes where there are clusters of irregularity representing short run high bursts of activity which tend to be smoothed out by laminar periods in the longer run. This signature is not dominant in the game’s simulations but may take place, which is favorable evidence since such spectra signatures take place in actual market volatility measures expressing adaptive expectations regarding volatility fundamentals, as it is shown in figure 4, for the volatility index “VIX” which is the volatility index on the S&P 500.

Even though the is not a volatility index, the conceptual proximity regarding the incorporated expectations allow for some comparison. The large deviation spectrum of the VIX also shows a lower persistence which is more consistent with the cases for , a result to be expected since the financial returns’ volatility seem to be affected by the magnitude of previous returns.

4 Conclusions

The present work has combined chaos theory and quantum game theory to provide for a game theoretic equilibrium foundation to Mandelbrot’s argument of intrinsic time linked to the business cycle as a source of turbulent dynamics and multifractal signatures in the financial markets.

If we were to let , then, we would trivially obtain the traditional log-normal random walk model, by letting we were able to implement Mandelbrot’s proposal of a business cycle-related intrinsic time, and, thus, to provide for a quantum version of an evolutionary business cycle approach to financial turbulence.

A significant econometric point of the model regards the volatility scaling, indeed the multifractal signatures, in this case, result from the nonlinear dependencies rather than from a prescribed fixed multifractal measure: we are dealing with power-law conditional heteroscedasticity responsible for the emergence of multifractal signatures. This allows one to establish a bridge between Mandelbrot’s proposal and conditional heteroscedasticity models.

From the economic analysis perspective, the game’s simulations show that the interplay between economic chaos and volatility dynamics may account for the emergence of turbulence and multifractal signatures. The quantum approach has advantages over the classical stochastic processes since it provides for theoretical foundations underlying the probability measures, linking the probability densities to the underlying game structures and economic dynamics, while sharing the same advantage of being ammenable to econometric analysis and estimation, which can prove useful in portfolio management, derivative pricing and risk management, all areas of application of financial economics.

References

- [1] B. E. Baaquie, L.C. Kwek and M. Srikant, Simulation of Stochastic Volatility using Path Integration: Smiles and Frowns, arXiv:cond-mat/0008327v1, 2000.

- [2] B. E. Baaquie and Srikant Marakani, Empirical investigation of a quantum field theory of forward rates, arXiv:cond-mat/0106317v2 [cond-mat.stat-mech], 2001.

- [3] B.E. Baaquie, Quantum Finance: Path Integrals and Hamiltonians for Options and Interest Rates, Cambridge University Press, USA, 2004.

- [4] B. E. Baaquie and T. Pan, Simulation of coupon bond European and barrier options in quantum finance. Physica A, 390, 2011, 263-289.

- [5] P. Bak and M. Paczuski, Complexity, contingency, and criticality, Proceedings of the National Academy of Sciences of the USA, 1995, 92: 6689-6696.

- [6] R.C. Bishop. Brussels-Austin Nonequilibrium Statistical Mechanics: Large Poincaré Systems and Rigged Hilbert Space. http://philsci-archive.pitt.edu/id/eprint/1156. 2003.

- [7] P. Chen, Equilibrium Illusion, Economic Complexity and Evolutionary Foundation in Economic Analysis, Evol. Inst. Econ. Rev., 2008, 5(1): 81–127.

- [8] R. Frisch, Propagation Problems and Impulse Problems in Dynamic Economics, in Economic Essays in Honour of Gustav Cassel. George Allen & Unwin, London, 1933.

- [9] C. P. Gonçalves, and C. Gonçalves, An Evolutionary Quantum Game Model of Financial Market Dynamics - Theory and Evidence, Capital Markets: Asset Pricing & Valuation, 2008, Vol. 11, Issue 31.

- [10] C. P. Gonçalves, Multifractal Financial Chaos in an Artificial Economy, Game Theory & Bargaining Theory eJournal, 2010, Vol. 2, Issue 37.

- [11] R.M. Goodwin. A Growth Cycle. In C.H. Feinstein (ed.): Socialism, Capitalism and Economic Growth. Cambridge University Press, Cambridge, 1967.

- [12] K. Ilinsky, Physics of Finance, Gauge Modelling in Non-equilibrium Pricing. John Wiley & Sons, 2001.

- [13] M. O. Madeira and C.P. Gonçalves, Ontologies: On the Concepts of: Possibility, Possible, ’Acaso’, Aleatorial and Chaos, Metaphysics eJournal, 2010, Vol. 3, Issue 1.

- [14] R. de la Madrid, The role of the rigged Hilbert space in Quantum Mechanics. Eur. J. Phys., 2005, 26, 287.

- [15] B. B. Mandelbrot, A. Fisher and L. Calvet, A Multifractal Model of Asset Returns, Cowles Foundation Discussion Papers: 1164, 1997.

- [16] B. B. Mandelbrot, Fractals and Scaling in Finance, Springer, USA, 1997.

- [17] B. B. Mandelbrot and R. L. Hudson, The (Mis)behaviour of Markets: A Fractal View of Risk, Ruin and Reward, Basic Books, USA, 2004.

- [18] R.C. Merton, Applications of Options Pricing Theory: Twenty-Five Years Later. Nobel Lecture, 1997.

- [19] H.-W. Lorenz, Nonlinear Dynamical Economics and Chaotic Motion, Springer-Verlag, Germany, 1997.

- [20] E.W. Piotrowski and J. Sladkowski, Quantum-like approach to financial risk: quantum anthropic principle, Acta Phys.Polon., 2001, B32, 3873

- [21] E.W. Piotrowski and J. Sladkowski, Quantum Market Games, Physica A, 2002, Vol.312, 208-216.

- [22] E.W. Piotrowski and J. Sladkowski, Quantum auctions: Facts and myths, Physica A, 2008, Vol. 387, 15, 3949-3953.

- [23] I. Prigogine. The End of Certainty. Time, Chaos and the New Laws of Nature. The Free Press, France, 1997.

- [24] T. Püu. Nonlinear Economic Dynamics, Springer-Verlag, Germany, 1997.

- [25] V. Saptsin and V. Soloviev, Relativistic quantum econophysics - new paradigms in complex systems modelling, arXiv:0907.1142v1 [physics.soc-ph], 2009.

- [26] V. Saptsin and V. Soloviev, Heisenberg uncertainty principle and economic analogues of basic physical quantities, arXiv:1111.5289v1 [physics.gen-ph], 2011.

- [27] M. Schaden, Quantum Finance. Physica A, 316, 2002, 511-538.

- [28] M. Schaden, Pricing European Options in Realistic Markets. arXiv:physics/0210025v1 [physics.soc-ph], 2002.

- [29] M. Schaden, A Quantum Approach to Stock Price Fluctuations. arXiv:physics/0205053v2 [physics.soc-ph], 2003.

- [30] W. Segal and I.E. Segal, The Black–Scholes pricing formula in the quantum context. PNAS March 31, 1998, vol. 95 no. 7, 4072-4075.