Multigrid methods for two-player zero-sum stochastic games

Abstract

We present a fast numerical algorithm for large scale zero-sum stochastic games with perfect information, which combines policy iteration and algebraic multigrid methods. This algorithm can be applied either to a true finite state space zero-sum two player game or to the discretization of an Isaacs equation. We present numerical tests on discretizations of Isaacs equations or variational inequalities. We also present a full multi-level policy iteration, similar to FMG, which allows to improve substantially the computation time for solving some variational inequalities.

1 Introduction

In the present paper, we are interested in solving non-linear finite dimensional equations of the form :

| (1) |

with unknown the function , where . Here , are finite sets; the functions and are given such that ; and is a given constant. These equations appear when solving the following particular dynamic games.

An infinitely repeated game, or discrete time dynamic game, or infinite horizon multi-stage game, consists in an infinite sequence of state transitions, where at each step, the transition depends on the actions of the players, and each player receives a reward which depends on the state of the game and the actions of all players at this step. The aim of each player is to maximize his own objective function, for instance his payoff which is the sum of the rewards he received at all steps. The game is stochastic when the state sequence is a random process with a Markov property, then the objective function is the expected payoff. It is a two player zero-sum game when there are two players with opposite rewards, hence player aims to minimize player objective function. When the game does not stop in finite time (almost surely), one often consider a discounted payoff where the reward at each step is discounted by some multiplicative factor , with .

Consider in particular a two player zero-sum discounted stochastic game with finite state space and action spaces and for player and player respectively. Denote by the reward of player when (at the current step) the state is and the actions of player and are , respectively. Denote by the transition probability from state to state when the actions of player and are , respectively. Assume that player plays before player , and that at each step, player is choosing his action as a function of the current state , and player is choosing his action as a function of the current state and action of player . Assume each player is maximizing his own objective function. Under the previous finiteness conditions on (, , ), there exists a function which associates to each the expected payoff of player when the initial state of the game is . This function is called the value or the value function of the game. It is the unique solution of Equation (1) [54], called itself the dynamic programming equation or Shapley equation of the game. Solving Equation (1) is important since it also gives the optimal stationary strategies of the game, see section 2 for precise definitions of strategies and details. Discrete time zero-sums stochastic games arise in several domains of applications, such as military operations [43], network flow control [4], pursuit-evasion problems (although often studied in the deterministic case), see [46] for other applications references.

Equations of the form (1) can also be obtained as special discretizations of partial differential equations associated to differential stochastic games, where the state space is now a subset of (see section 3 for details). For instance the following non-linear elliptic partial differential equation called Isaacs equation :

| (2) |

allows one to solve a differential game in the same way as (1) solves a discrete time dynamic game. Here , are either finite sets or subsets of some spaces, is a scalar, and , the set of positive definite symmetric matrices, , and are given functions. Such equations may be applied in particular to pursuit-evasion games (see for instance [6]), but they also appear in solving optimal control problems (see for instance [9]), or risk-sensitive optimal control problems [32], in particular for finance applications [25]. The discretization of Equation (2) with a monotone scheme in the sense of [8] yields an equation of the form (1) which can then be interpreted as the dynamic programming equation of a stochastic game with discrete time and finite state space. Suitable possible discretizations schemes are for instance : Markov chain discretizations [39, 40], monotone discretizations [8], full discretizations of semi-Lagrangian type [6], and max-plus finite element method [3] for deterministic games or control problems. Hence, we are interested in solving discretizations of Equation (2) which have the form of Equation (1), in order to find an approximation of the value of the corresponding differential stochastic game.

In the presence of a discount factor , the nonlinear equation (1) can be solved by applying the fixed point iterations which are called, in the optimal control and game literature, value iterations or the value iteration algorithm [10]. The iterations of this method are cheap but their convergence slows considerably as the discount factor approaches one. Moreover, when we discretize Equation (2) with a finite difference or finite element method with a discretization step , we obtain an equation of the form (1) with a discount factor , then when is small is close to one and the value iteration method is as slow as the Jacobi or Gauss-Seidel iterations for a discretized linear elliptic equation. Another approach consists in the so called policy iteration algorithm, initially introduced by Howard [38] for one player stochastic games (i.e. stochastic control problems). Later adaptations of this algorithm were proposed for the two player games : by Hoffman and Karp [35] for a special mean-payoff case, by Dernado [23] for approximations of value functions in discounted stochastic games, in Puri thesis [49] for discounted stochastic games, and by Cochet-Terrasson and Gaubert [19] for the general mean-payoff case. In all cases, policy algorithm converges faster than the value iteration algorithm and in practice it ends in few steps (see for instance [24] for numerical examples in the case of deterministic games).

A (feedback) policy (or pure Markovian stationary strategy, see Section 2 below) for the first player is a function which maps any to an action . Then, starting with an initial policy for player , the policy iteration algorithm for the two player zero-sum stochastic game consists in applying successively a policy evaluation step followed by a policy improvement step. The policy evaluation step amounts to compute the value of the game for the current policy , that is the solution of (1) where instead of taking the maximum of the expression inside the “max”, one evaluates it with . The policy improvement step consists in finding the optimal policy for the current value function , that is the policy optimizing the expression inside the “max” in (1) when the value function is . Computing the above value functions (in the policy evaluation steps) is performed using the policy iteration algorithm for a one-player game. The policy iteration algorithm is explained in more general settings in Section 4. It stops after a finite number of steps when the sets of actions are finite, see [41, 14, 50] for one player games and [49, 19] for two player games. In addition, under regularity assumptions on the maps and , the policy iteration algorithm for a one player game with infinite action spaces is equivalent to Newton’s method, thus can have a super-linear convergence in the neighborhood of the solution, see [51, 15] for superlinear convergence under general regularity assumptions, and [51, 2, 5] for order superlinear convergence under additional regularity and strong convexity assumptions.

Each policy iteration for a one player game (or each iteration in the inner loop of the two player algorithm) requires the solution of a linear system. Indeed, when we fix feedback policies and for player and respectively, the system of equations (1) yields a linear system of the form : where are respectively the value function of the game and the vector of rewards for the fixed policies and , is the discount factor and is a Markov matrix whose elements are the transition probabilities for (and each rowsum of equals one). When the dynamic programming equation (1) is coming from the discretization of an Isaacs partial differential equation (2), this linear system corresponds to the discretization of a linear elliptic partial differential equation, hence it may be solved in the best case in a time in the number of discretization points by using multigrid methods, that is the cardinality of the discretized state space , or the size of the matrix . For general stochastic games on a finite state space , since is a Markov matrix, the matrix of the linear system is an invertible M-matrix [13], and one may expect the same complexity when solving them by using an algebraic multigrid method.

In the present paper, we consider the combination of policy iterations with the algebraic multigrid method (AMG) introduced by Brandt, McCormick and Ruge [17, 18], see also Ruge and Stüben [53]. We shall call AMG the resulting algorithm. This algorithm can be applied either to a true finite state space zero-sum two player game or to the discretization of an Isaacs equation, although in the present paper we restrict ourselves to numerical tests for the discretization of stochastic differential games, since the AMG algorithm needs some improvements to be applied to arbitrary non symmetric linear systems arising in game problems. Such an association of multigrid methods with policy iteration has already been used and studied in the case of one player games, that is discounted stochastic control problems (see Hoppe [36, 37] and Akian [1, 2] for Hamilton-Jacobi-Bellman equations or variational inequalities, Ziv and Shimkin [48] for AMG with learning methods). However, it is new in the case of two player games. We have implemented this algorithm (in C) and shall present numerical tests on discretizations of Isaacs or Hamilton-Jacobi-Bellman equations or variational inequalities, while comparing AMG with the combination of policy iterations with direct solvers.

The complexity of two player zero-sum stochastic games is still unsettled, one only knows that it belongs to the complexity class of NPcoNP [49]. Indeed, the number of policy iterations is bounded by the number of possible policies, which is exponential in the cardinality of . Friedmann has shown [34] that a strategy improvement algorithm requires an exponential number of iterations for a “worst”-case family of games called parity games, this result can be extended to other types of zero-sum stochastic games, in particular to mean-payoff and discounted zero-sum stochastic games, and to undiscounted stochastic control problems (one-player games) as shown by Fearnley [27, 28]. However, as for Newton’s algorithm, convergence can be improved by starting the policy iteration with a good initial guess, close to the solution. With this in mind, we present a full multi-level policy iteration, similar to FMG. It consists in solving the problem at each grid level by performing policy iterations until a convergence criterion is verified, then to interpolate the strategies and value to the next level, in order to initialize the policy iterations of the next level, until the finest level is attained. When at each level policy iterations are combined with the algebraic multigrid method, we shall call FAMG the resulting full multi-level policy iteration algorithm. For one-player discounted games with infinite number of actions and under regularity assumptions, one can show [2, 1] that this kind of full multi-level policy iteration has a computing time in the order of the cardinality of the discretized state space at the finest level. In Section 6, we give numerical examples on variational inequalities for two player games, the computation time of which is improved substantially using FAMG instead of AMG.

The paper is organized as follow. The three following sections are some recalls about basic definitions on the subject. In Section 2, we introduce the definition of a two player zero-sum stochastic game with finite state space and the corresponding dynamic programming equation. Section 3 is about two player zero-sum stochastic differential games, we recall here the definition of the Isaacs equation, the variational inequalities and the discretization scheme that we use. Section 4 is devoted to the numerical background needed to solve the dynamic programming equation, including the policy iteration algorithm and the algebraic multigrid method. Section 5 describes our algorithms AMG and FAMG. We present in Section 6 some numerical tests on discretizations of Isaacs equations and variational inequalities. Last section gives ending remarks.

2 Two player zero-sum stochastic games: the discrete case

The class of two player zero-sum stochastic game was first introduced by Shapley in the early fifties [54]. We recall in this section the definition of these games in the case of finite state space and discrete time (for more details see [54, 29, 55]).

We consider a finite state space . A stochastic process on gives the state of the game at each point time , called stage. At each of these stages, both players have the possibility to influence the course of the game.

The stochastic game starting from is played in stages as follows. The initial state is equal to and known by the players. The player who plays first, say max, chooses an action in a set of possible actions . Then the second player, called min chooses an action in a set of possible actions . The actions of both players and the current state determine the payment made by min to max and the probability distribution of the new state . Then the game continues in the same way with state and so on.

At a stage , each player chooses an action knowing the history defined by for max and for min. We call a strategy or policy for a player, a rule which tells him the action to choose at any stage and in any situation. There are several classes of strategies. Assume and for some sets and . A behavior or randomized strategy for max (resp. min) is a sequence (resp. ) where (resp. ) is a map which to a history with , , for (resp. ) at stage associates a probability distribution on a probability space over (resp. ) which support is included in the possible actions space (resp. )). A Markovian (or feedback) strategy is a strategy which only depends on the information of the current stage : (resp. ) depends only on (resp. )), then (resp. ) will be denoted (resp. ). It is said stationary if it is independent of , then is also denoted by and by . A strategy of any type is said pure if for any stage , the values of (resp. ) are Dirac probability measures at certain actions in (resp. )) then we denote also by (resp. ) the map which to the history assigns the only possible action in (resp. )).

In particular, if is a pure Markovian stationary strategy, then with for all and is a map such that for all . In this case, we also speak about pure Markovian stationary strategy for and we denote by the set of such maps. We adopt a similar convention for player min : .

A strategy (resp. ) together with an initial state determines stochastic processes for the actions of max, for the actions of min and for the states of the game such that

| (3a) | ||||

| (3b) | ||||

| (3c) | ||||

where is the history process, is a history vector at time : and (resp. ) are measurable sets in () resp.). For instance, for each pair of pure Markovian stationary strategies (, ) of the two players, that is such that for : with and with , the state process is a Markov chain on with transition probability

and and .

The payoff of the game starting from is the expected sum of the rewards at all steps of the game that max wants to maximize and min to minimize. In this paper we consider discounted games with discount factor : the reward at time is the payment made by min to max times . When the strategies for max and for min are fixed, the payoff of the game starting from is then

where denotes the expectation for the probability law determined by (3). A discounted game can be seen equivalently as a game which has, in each stage, a stopping probability equal to , independent of the actions taken by both players. The value of the game starting from , , is then given by

| (4) |

where the supremum is taken over all strategies for max and the infimum is taken over all strategies for min. Note that a non terminating game without any discount factor (or ) is called ergodic.

We are concerned in finding optimal strategies for both players and the value of the discounted game in each point. These are given by the dynamic programming equation [54] defined below.

Theorem 2.1 (Dynamic programming equations [54]).

Assume and are finite sets for all , . Then, the value of the stochastic game , defined in (4), is the unique solution of the following dynamic programming equation:

| (5) |

We denote by the dynamic programming operator from to itself which maps to the function

| (7) |

where is defined in (5). This operator is monotone and contracting with constant in the sup-norm, i.e. for all . Hence, fixed point iterations on Equation (5), called value iterations in the optimal control and game literature, are contracting for the sup-norm with constant .

3 Two player zero-sum stochastic differential games: the continuous case

Another class of games which we consider is the class of two player differential stochastic games in continuous time. In these games, the state space is a regular open subset of and the dynamics of the game is governed by a stochastic differential equation which is jointly controlled by two players (see [31, 56] and below). In this case, the value of the game (defined below) is solution of a non linear elliptic partial differential equation of type (2), called Isaacs equation (see also [31, 56]). The discretization of this equation with a monotone scheme in the sense of [8] yields the dynamic programming equation (5) of a stochastic game with discrete state space which was described in the previous section.

In the first following subsection, we give the definitions of differential stochastic games with a bounded state space and a discounted payoff. Then, in the next subsection, we present a subclass of these differential games called optimal stopping time games. Finally, in the last subsection, we introduce the finite difference discretization scheme that we use to discretize the Isaacs equation (12) and (13) respectively. Numerical examples of such kind of games will be presented in section 6.

3.1 Differential games with regular controls.

Assume now that the state space is a regular open subset of . Suppose a probability space is given, as well as a filtration over it (that is a non decreasing sequence of -algebras over ). We consider games which dynamics is governed by the following stochastic differential equation :

| (8) |

with initial state . Here is a -dimensional Wiener process on ; and are stochastic processes taking values in closed subsets and of and respectively; and are given functions. The dimension of the Wiener process may be different from and is given by the modeling of the problem. Assuming that and are adapted to the filtration (that is for all , and are -measurable), allows one to define the stochastic process satisfying Equation (8) and it is a necessary condition to the assumption that the actions of the two players depend only on the past states and actions. We also consider strategies (resp. ) of player max (resp. min) determining the process (resp. ). In particular, for pure Markovian stationary strategies, one has and .

When , the discounted payoff of the game with discount rate is given by :

| (9) |

where is the (instantaneous, or running) reward function. Now, we consider that is a regular open subset of . In this case, we denote by the first exit time of the process from , i.e. . Then, the discounted payoff of the game stopped at the boundary is :

| (10) |

where the function is called the terminal reward. The value function of the differential stochastic game starting from is defined as in section 2 by

| (11) |

where the supremum is taken over all strategies for max and the infimum is taken over all strategies for min.

As previously, we are interested in finding the value function of the game and the corresponding optimal strategies. We denote by the following second order partial differential operator :

with . When and is onto for all , the matrix is of full rank and the operator is elliptic. The value of the game is solution, under some regularity assumptions on and on the functions , , and (for instance boundedness and uniform Lipschitz continuity), of the dynamic programming equation, called Isaacs partial differential equation :

| (12) |

This has been shown in the viscosity sense in [31]. See also [20] and references therein for uniqueness of the solution of (12). If the value of the game is a classical solution of (12), and are strategies such that for all in and in , and are the unique actions that realize the maximum and the minimum in Equation (12) for max and min respectively, then and are pure Markovian stationary strategies, that are optimal for (11) (with satisfying (8), (10), with and ).

Note that for a game with one player, i.e. for a stochastic control problem, Equation (12) is the so-called Hamilton-Jacobi-Bellman equation. Also when is bounded, and is strongly uniformely elliptic (if for some , for all ), then the case can also be considered.

3.2 Differential games with optimal stopping control

When the action of the players are not continuous or not bounded, the dynamic programming equation of the game is no more of the form of Equation (12), but may be a variational inequality or a quasi-variational inequality, see for instance [33, 11] for the case of optimal stopping games with one or two players and [30, 12] for impulse or singular control.

We consider here an optimal stopping game, that is a game in which one of the players have the choice of stopping the game at any moment (see [33] for a more general case). We assume here that max has this ability. Then at each time , he chooses to stop or not the game, that is he is choosing an element of the action space where means that the game is continuing, that the game stops, with and for when (i.e. , in (8)). The second player min plays as previously and we consider the same model as in previous subsection. The value of a strategy for max determines a process adapted to the filtration of (that is ), then a stopping time adapted to the process and vice versa.

So if , the discounted payoff (10) can be written as a function of the stopping time instead of :

Indeed, if , then , , so , and . The value function (11) of the game starting from is then given by :

where the supremum is taken over all stopping times and the infimum is taken over all strategies for min.

Since the variable “” appears only when equal to , one can ommit it in equations, hence Equation (12) becomes :

| (13) |

since , one can divide the term \raisebox{-0.9pt}{\hspace*{0.7pt}${2}$}⃝ by , and get the variational inequality in the usual form used in viscosity solutions literature. In another usual way, Equation (13) can be written as :

| (14) |

with for . Both Equation (13) and Equation (14) are called variational inequalities. Note however, that Equation (13), or the resulting equation obtained by simplifying by in \raisebox{-0.9pt}{\hspace*{0.7pt}${2}$}⃝, reveals more the control nature and can be used to define viscosity solutions (where one need to write equations in the form on ), whereas Equation (14) is more adapted to a variational approach.

As for (12), if is a classical solution of (13) or (14), if for all in : is equal to or if resp. \raisebox{-0.9pt}{\hspace*{0.7pt}${1}$}⃝ or \raisebox{-0.9pt}{\hspace*{0.7pt}${2}$}⃝ is maximum in (13) and if for all in : is the action which realize the minimum in \raisebox{-0.9pt}{\hspace*{0.7pt}${1}$}⃝, then an optimal pure Markovian stationary strategy is obtained by taking and equal to the first time when . So this equation behaves as Equation (12) but where the first player has a discrete action space equal to , meaning continue to play and meaning stop the game. This variational inequality can be treated with the same methods as (12).

3.3 Discretization

Several discretization methods may transform equations (12) or (13) into a dynamic programming equation of the form (5). This is the case when using Markov discrezation of the diffusion’s (12) as in [39, 40] and in general when using discrezation schemes that are monotone in the sense of [8]. One can obtain such discretizations by using the simple finite difference scheme below when there are no mixed derivative (that is is a diagonal matrix). Under less restrictive assumptions on the coefficients, finite difference schemes with larger stencil also lead to monotone schemes [16, 45]. In the deterministic case (when ), one can also use semi-Lagrangian scheme [6, 7] or max-plus finite element method [3], both of them having the property of leading to a discrete equation of the form (5).

We suppose that is the -dimensional open unit cube. Let () denote the finite difference step in each coordinate direction, the unit vector in the -coordinate direction, and a point of the uniform grid . Equation (12) is discretized by replacing the first and second order derivatives of by the following approximation, for :

| (15) |

or

| (16) |

| (17) |

Approximation (15) may be used when is uniformly elliptic and is small, whereas (16) has to be used when is degenerate (see [39, 40]). For equations (12) and (13), these differences are computed in the entire grid , by prolonging on the “boundary”, using Dirichlet boundary condition:

We obtain a system of non linear equations of unknowns, the values of the function :

| (18) |

where and is a function which to , , , associates the approximation of .

When there are no mixed derivatives ( if , ), the discretization is monotone in the sense of [8], then if (12) has a unique viscosity solution, the solution of (18) converges uniformly to the solution of (12) [8]. Moreover, multiplying Equation (18) by with small enough, it can be rewritten in the form (5), with a discount factor . A similar result holds for the discretization of (13) (by multiplying only the diffusion part by ).

4 Background for numerical solution of discrete dynamic programming equations

In this section, we present the policy iteration algorithm to solve the dynamic programming equation (5) of a two player zero-sum discounted stochastic game with finite state space. We first present the policy iteration algorithm for a one player game which is then used in the following subsection to define the policy iteration algorithm for the two player case. The last part of this section is devoted to a recall of multigrid methods which we will use in the policy iterations for solving the linear systems.

4.1 Policy iteration algorithm for one player games

First, we consider a one player stochastic game with a min player and finite state space . In this case, the dynamic programming operator , mapping to itself, is given for each by :

| (19) |

This game is more commonly called a Markov Decision Process (MDP) with finite state space , we refer to [38, 22, 50] for a deeper description on this topic. Then, the discounted value of the game starting in is given by :

where the processes and strategies are defined such as in the section 2. The value of the game is solution of the dynamic programming equation : for in . Then the policy iteration algorithm for Markov Decision Processes, that was first introduce by Howard [38], is given in Algorithm 1 and give us the discounted value of the game and the optimal policy for min.

Given an initial policy , the policy iterations consist in applying successively the two following steps:

-

1.

Compute the value of the game with fixed feedback policy , that is the solution of

(20) -

2.

Improve the policy: Find the optimal feedback policy for the value , i.e. for each in , chose such that :

until we cannot improve the policy anymore.

Each policy iteration of Algorithm 1 strictly improves the current policy and produces a non increasing sequence of values . It implies that the algorithm never visits twice the same policy. Hence if the action sets are finite in each point of , the policy iterations stop after a finite time (see for instance [51, 41, 14]). Moreover, under regularity assumptions, the policy iteration algorithm for a one player game with infinite action spaces is equivalent to Newton’s method [2, 5, 15, 51]. Indeed, define , then the problem is to find the solution of where all entries of are concave functions. The policy improvement step can be seen as the computation of an element of the sup-differential of in the current approximation and the value improvement step computes the zero of the previous sup-differential. When is regular, the sequence of value functions is exactly the sequence of the Newton’s algorithm.

4.2 Policy iteration algorithm for two player games

Now, we give the policy iteration algorithm for solving a two player zero-sum stochastic games with finite state space , as defined in Puri thesis [49]. Recall the definitions of section 2, we need to solve the dynamic programming Equation (5) which give us the value of the game (Equation (4)) and the optimal strategies for both players. For a fixed pure feedback policy for max , the value of the game is solution of the equation where is an operator mapping to itself whose -coordinate is given by :

for each and . Note that is the dynamic programming operator of a one player game with only the min player. Then the policy iteration algorithm is given in Algorithm 2.

Given an initial policy for max, the policy iterations consist in applying successively the two following steps:

until we cannot improve the policy anymore.

Step 1 of Algorithm 2 is performed by using the policy iteration algorithm for a one player game. That is, given an initial feedback policy for min , we iterate on min policies and value functions . Then at each step of the interior policy iteration (Algorithm 1 step 1), one computes , the value of the game with fixed strategies for max and for min. This is done by solving the linear system :

| (21) |

where for all : is a stochastic matrix whose elements are defined by for all and is the vector whose elements are defined by for .

As for the one player case, each iteration of the policy iteration algorithm strictly improve the current policy, hence it can never visit twice the same policy. Moreover, the algorithm produces a non decreasing (resp. non increasing) sequence of values (resp. ) of the external loop (resp. internal loop), see [49, 19]. It follows that if the action sets for both players are finite in each point of , the policy iterations stop after a finite time [49].

4.3 AMG

The linear systems defined in (21) have all the form where a Markov matrix. We solve them using algebraic multigrid methods which we recall in this section.

Standard multigrid was originally created in the seventies to solve efficiently linear elliptic partial differential equations (see for instance [42]). It works as follows. Multigrid methods require discretizations of the given continuous equation on a sequence of grids. Each of them, starting from a coarse grid, being a refinement of the previous until a given accuracy is attained. The size of the coarsest grid is chosen such that the cost of solving the problem on it is cheap. Assume also that transfer operators between these grids are given: interpolation and restriction. Then, a multigrid cycle on the finest grid consists in : first, the application of a smoother on the finest grid; then a restriction of the residual on the next coarse grid; then solving the residual problem on this coarse grid using the same multigrid scheme; then, interpolate this solution (which is an approximation of the error) and correct the error on the fine grid; finally, the application of a smoother on the finest grid. If the multigrid components are properly chosen, this process is efficient to find the solution on the finest grid. Indeed, in general the relaxation process is smoothing the error which then can be well approximated by elements in the range of the interpolation. It implies, in good cases, that the contraction factor of the multigrid method is independent of the discretization step and also the complexity is in the order of the number of discretization points. We shall refer to this standard method as geometric multigrid.

Algebraic multigrid method, called AMG, has been initially developed in the early eighties (see for example [18, 17, 53]) for solving large sparse linear systems arising from the discretization of partial differential equations with unstructured grids or PDE’s not suitable for the application of the geometric multigrid solver or large discrete problems not derived from any continuous problem.

The AMG method consists of two phases, called “setup phase” and “solving phase”. In contrast to geometric multigrids, the mode of constructing the coarse levels (coarse “grids”) which constitute the setup phase, is based only on the algebraic equations. The points of the fine grids are represented by the variables and coarse grids by subset of these variables. The selection of those coarse variables and the construction of the transfer operators between levels are done in such a way that the range of the interpolation approximates the errors not reduced by a given relaxation scheme. Then the “solving phase” is performed in the same way as a geometric multigrid method and consists of the application of a smoother and a correction of the error by a coarse grid solution. The whole process is briefly recall below.

Consider a system of linear equations given in the matrix form:

| (22) |

where the matrix and the vector are given, and we are looking for the vector . We call fine grid the set of all variables of the system, i.e. .

First, recall that a relaxation method consist of the following approximations:

where is called the smoothing operator and is the identity operator in . The error propagates as

The method is said to converge if where is the spectral radius of with his eigenvalues. For example, the smoother operator of the weighted Jacobi method is and that of the Gauss-Seidel is where and are the diagonal and lower triangular part of the matrix resp.

Assume the grid on level where level correspond to the finest grid . The construction of the coarse grid from the fine grid , consists in the splitting of the variables from the grid into two distinct subsets, namely which contains the variables belonging to both grids, and , and the variables belonging to the grid only. We have then . The coarse grid contains variables. This splitting is based on the “connections” between the variables on level [18, 53] and such as the range of the associate interpolation or prolongation operator accurately approximates the errors not efficiently reduced by the relaxation phase (these errors are “smooth” in the algebraic multigrid terminology). The restriction operator maps residuals from grid to the grid . In [18, 53], the operator is fixed to be . The coarse grid operator is defined by where is the approximation of on and . Similarly, for any vector we denote its restriction on . This construction can be repeated recursively from the finest level to the coarsest level .

The solution phase consists in applying the multigrid cycle described in Algorithm 3, it is called V(,)-cycle if and W(,)-cycle if .

Convergence theorem for the V-cycle is given in[53] for symmetric and positive definite. See also [18, 17, 26], for two-level convergence for linear systems where the matrix of the system is a M-matrix, symmetric and positive definite. Also we can find in the literature, two-grid convergence analysis for non-symmetric linear system in [47] and [44].

5 A multigrid algorithm for discrete dynamic programming equations

5.1 Policy iteration combined with algebraic multigrid method (AMG)

Recall that in the policy iteration algorithm for games at each step of the interior policy iteration, we have to solve a linear system (21) which is of the form with a Markov matrix and the discount factor. Since are non singular -matrices, we use AMG to solve those systems. For shortness in the sequel, we shall call the resulting algorithm AMG that is the combination of policy iterations and AMG. The name AMG refers also to the numerical implementation of this algorithm. Note that in practice, in Algorithm 1 (equivalently in Algorithm 2), the policy iterations are stopped when after Step 1, the norm of the residual, , is smaller than a given value denoted by . We used this stopping criterion in AMG. The iterations of AMG are summarized in the scheme represented in Figure 1

where is a sequence of value functions generated by the multigrid solver. The algebraic multigrid methods allows us to solve linear systems arising from either the discretization of Isaacs or Hamilton-Jacobi-Bellman equations or a true finite state space zero-sum two player game. However in the present paper, we restrict ourselves to numerical tests for the discretization of stochastic differential games, since the AMG algorithm needs some improvements to be applied to arbitrary non symmetric linear systems arising in game problems.

5.2 Full multi-level policy iteration (FAMG)

Recall that the number of policy iterations can be exponential in the cardinality of the state space . However, as for Newton’s algorithm, convergence can be improved by starting the policy iterations with a good initial guess, close to the solution. With this in mind, we present a full multi-level scheme, that we shall call FAMG. As in standard FMG, starting from the coarsest level, it consists in solving the problem at each grid level by performing policy iterations AMG until a convergence criterion is verified, then to interpolate the strategies and value function to the next level, in order to initialize the policy iterations of that level. This scheme is repeated until the finest level is attained.

The algorithm FAMG only applies to Isaacs partial differential equations (12). It works as follows. The state space is first discretized on sequence of grids : such that on grid , , the discretization step is , where is the discretization step chosen on the finest grid . Then, the Isaacs PDE is discretized on all levels, , using the finite differences scheme (16)- (17). For level , we denote by the dynamic programming operator, the value of game, and the strategies of max and min respectively. We denote by the linear interpolation operator which maps any vector from to :

where for , and we denote by the operator which interpolates a strategy from grid to grid , for instance for a strategy of max :

where is chosen arbitrary in for . We denote by AMG the algorithm AMG with initial strategy for player max iterations, initial policy for the first iteration of player min, value as initial approximation for the first call of AMG and the stopping criterion for the policy iterations. Then FAMG algorithm is given in Algorithm 4 where is a given constant.

Figure 2 illustrates the FAMG algorithm when V-cycles are use in AMG. The dashed lines represent the interpolation of the solution and strategies from a coarse grid to the next fine grid . The continuous V-lines are the V-cycles of AMG which are not fixed in number since at each level, AMG cycles are performed until a given criterion is attained.

Note that our FAMG program only applies to stochastic differential games since for them coarse representation, including equations and strategies, can be easily constructed by tacking different sizes of discretization step.

6 Numerical results

In this section, we apply our programs AMG and FAMG, which were implemented in C, to examples of two player zero-sum stochastic differential games. Let first give some details about the implementation of the algorithms that we use and some notations for the numerical results.

The AMG linear solver of AMG implements the construction phase, including the coarsing scheme and the interpolation operator, described in [53] and the general recursive multigrid cycle for the solution phase (see Algorithm 3). In the tests, W(,)-cycles were used and the chosen smoother is a CF relaxation method, that is a Gauss Seidel relaxation scheme that relaxes first on C-points and then on F-points. The AMG program is the implementation of the method explained in section 5 with the above AMG linear solver. The FAMG program is the implementation of Algorithm 4.

The following notations are used in the tables: denotes the iteration over max policies and is the corresponding number of iterations for min policies, that is the number of linear systems solved at iteration . The residual error of the game is denoted by and the exact error, when known, by where is the discretized exact solution of the game. The infinite norm and discrete norm are given for each of them.

6.1 Isaacs equations

The first example concern a diffusion problem where the value of the game is solution of the following Isaacs PDE :

| (23) |

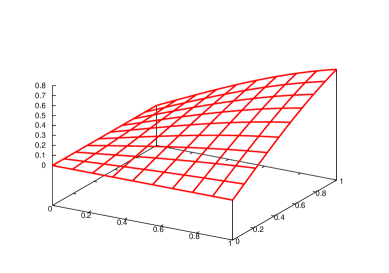

where is the unit square, , , for , and with for . Note that the exact solution is on and is represented in Figure 3. Indeed, by convex duality (or computation of Fenchel-Legendre transformations [52]), we have that

for all , and are optimal solutions in these equations.

To solve Equation (23), we first discretize the domain on a grid with points in each direction, i.e. with a discretization step and we obtain a discrete space with boundary . We denote by with such that and . Then, using the discretization scheme (16)- (17), Equation (23) becomes for :

multiply by , where , and adding on both sides, we obtain :

| (24) |

where is replaced by for . This equation has the form of Equation (5) with a discount factor equal to , transition probabilities from to are given by :

| (25) | |||||

and the running cost is, for :

Note that when the sum of the transition probabilities from to the points of equals , when or is in this sum is strictly less than . Hence, the matrix in (21) is substochastic, and since it is irreducible, it has a spectral radius strictly less than one. So even when or equivalently , the system (21) has an unique solution and the dynamic programing equations has also an unique solution. Hence, we shall take in the numerical tests. Note also that for this example, the matrices in (21) are not symmetric but close to be symmetric when is small, since the non-symmetric part correspond to the order one term in equation (24) and are dominated by order two terms when is optimal in (24).

| Policy iteration with LU | ||||||

| cpu time (s) | ||||||

| AMG | ||||||

|---|---|---|---|---|---|---|

| cpu time (s) | ||||||

In tables 1, we present numerical results when equations (23) is discretized on a grid with points in each direction, i.e. with a discretization step of . The stopping criterion for the policy iterations is . The first table of 1 shows the results of the policy iteration algorithm with a direct solver LU (we used the package UMFPACK [21]) and the second table of 1 the results of AMG. We observe that AMG solves the problem faster than the policy iterations with a direct solver. In both tables, we see that only three steps on max policies are needed (first column) and a total of six steps on min policies (second column) which involves the resolution of six linear systems. The small number of iterations is due to the fact that the solution is regular. In table 2, we show that the computation time is improved when applying FAMG with to the same example. In this case, the problem is solved in approximately .

| cpu time (s) | ||||||

| points in each direction : , h | ||||||

| points in each direction : , h | ||||||

| points in each direction : , h | ||||||

| points in each direction : , h | ||||||

| points in each direction : , h | ||||||

| points in each direction : , h | ||||||

| points in each direction : , h | ||||||

| points in each direction : , h | ||||||

| points in each direction : , h | ||||||

| points in each direction : , h | ||||||

In figure 4, we compare the policy iteration algorithm with a direct solver LU (UMFPACK [21]) and AMG for solving equation (24), when increasing by one the number of discretization points in each direction from to . The stopping criterion for the policy iterations is . In figure 5, we represent the corresponding number of iterations on min policies, i.e the number of linear systems solved for each size of problem, this number is the same for both methods. We can see that the most part of the computation time for the resolution of the non-linear equation (24) is used to solved the linear systems involved in the policy iteration. We also remark that the computation time for AMG seems to grow linearly with the size of the problem.

| AMG | cpu time (s) | ||||||

| AMG | cpu time (s) | ||||||

| AMG | cpu time (s) | ||||||

| AMG | cpu time (s) | ||||||

| AMG | cpu time (s) | ||||||

| AMG | cpu time (s) | ||||||

Each table 8 to 8 contains numerical results for Equation (23) discretized on grids with discretization step , , , , and respectively. For these tests, the stopping criterion for the policy iterations is where is the discretization step. The stopping criterion for the linear solver AMG is where is the residual for the linear system. For each line of the tables, the third column, named AMG, contains the number of iterations needed by AMG for solving each linear system ( systems per line). We can see that the number of iterations of AMG is independent of the size of the problem. Note that the norm of the error decrease slowly when the grid becomes finer, this is because the exact solution (Figure 3) is smooth and a small number of points is sufficient to get a good approximation, also the non-linearity of the problem gives a worse approximation than one might expect in the linear case. But a smooth solution is generally more difficult for linear iterative solvers.

6.2 Optimal stopping game

Next tests concern an optimal stopping time game where the value of the game is solution of the variational inequality :

| (26) |

where is the unit square, the sets , , for , for :

and for : where

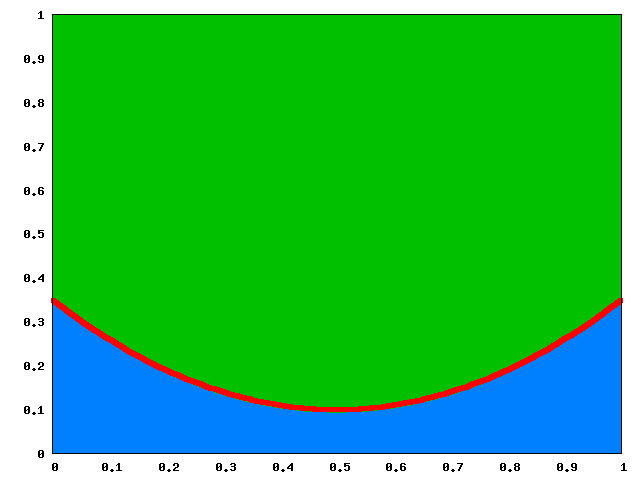

The definitions of the functions , and are chosen such that the function , represented in Figure 6, is solution of (26) almost everywhere and such that the terms \raisebox{-0.9pt}{\hspace*{0.7pt}${1}$}⃝ and \raisebox{-0.9pt}{\hspace*{0.7pt}${2}$}⃝ in Equation (26) are non positive for all (this condition must hold for the variational inequality to be well-defined). This example leads to a free boundary problem for the actions of max. Indeed, the points of the state space can be divided in two parts, the points where max chooses action (means continue to play) and the points where max chooses action (means that he stops the game). For , the optimal strategy for max is if and else, for all .

As for the previous example, the domain is discretized on a grid with points in each direction, i.e. with a discretization step and we obtain a discrete space with boundary . Then, Equation (26) is discretized by using the discretization scheme (16)- (17). After, the equations \raisebox{-0.9pt}{\hspace*{0.7pt}${1}$}⃝ and \raisebox{-0.9pt}{\hspace*{0.7pt}${2}$}⃝ are simplified separately by keeping equations (14) true. In this case, only equation \raisebox{-0.9pt}{\hspace*{0.7pt}${1}$}⃝ is multiply by with an appropriate constant. After discretization, we obtain the following dynamic programming equation for a game with state space :

with and for . The same comments about non-symmetry and the discount factor in equation (24) hold here. That is or equivalently .

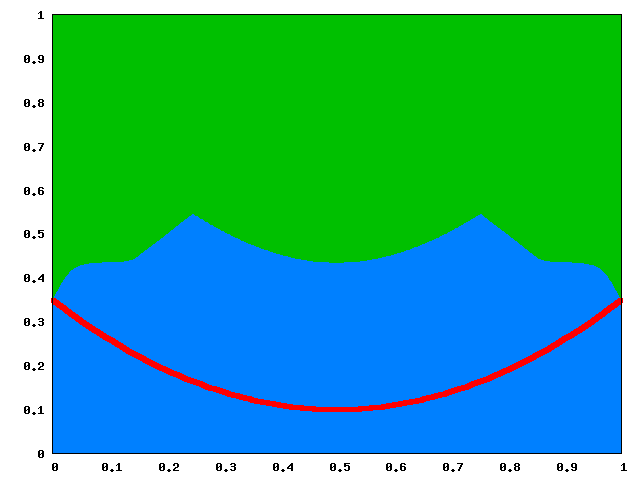

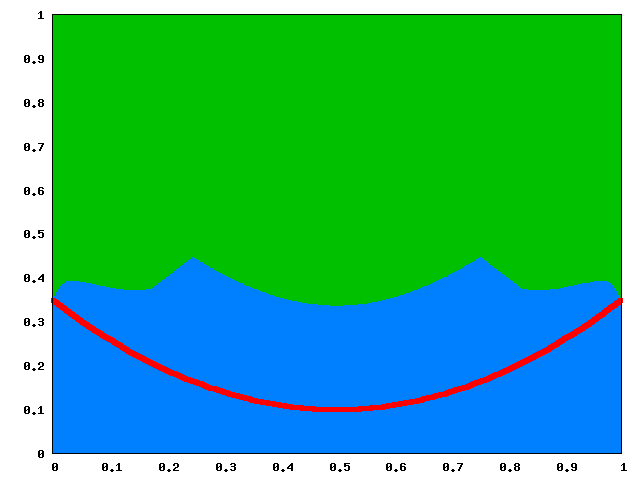

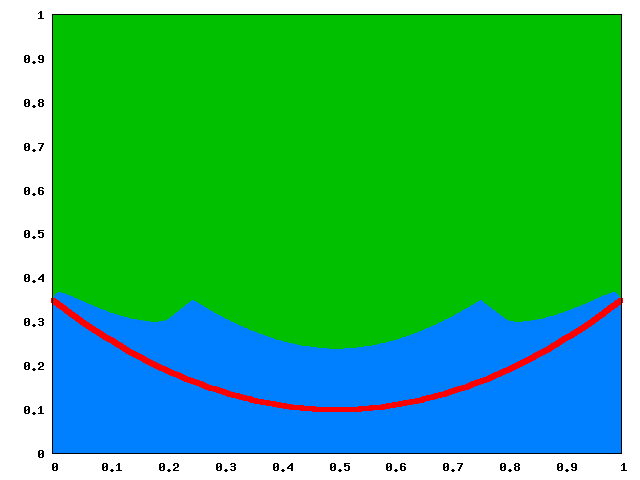

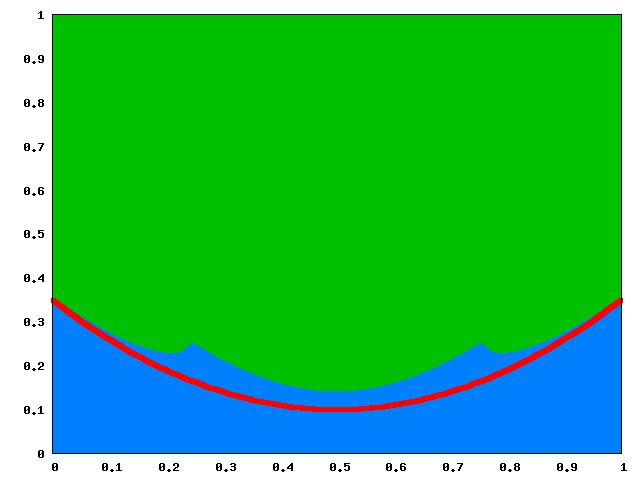

(a) (a) |

(b) (b) |

|---|---|

(c) (c) |

(d) (d) |

(e) (e) |

(f) (f) |

(g) (g) |

| cpu time (s) | ||||||

| cpu time (s) | ||||||

| points in each direction : , step size : | ||||||

| points in each direction : , step size : | ||||||

| points in each direction : , step size : | ||||||

| points in each direction : , step size : | ||||||

| points in each direction : , step size : | ||||||

| points in each direction : , step size : | ||||||

| points in each direction : , step size : | ||||||

| points in each direction : , step size : | ||||||

| points in each direction : , step size : | ||||||

| points in each direction : , step size : | ||||||

(a)

(b)

(b)

(c)

(d)

(d)

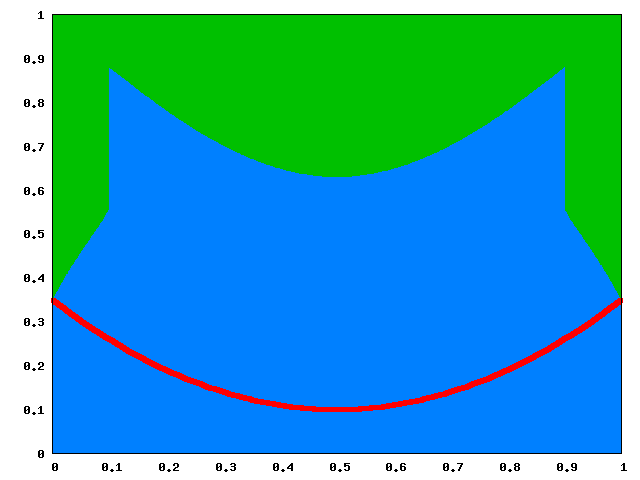

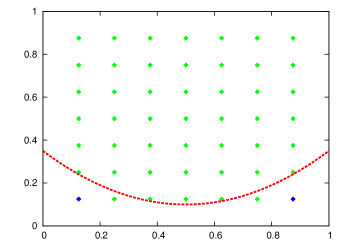

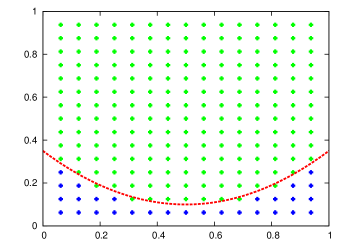

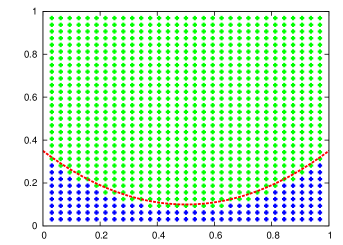

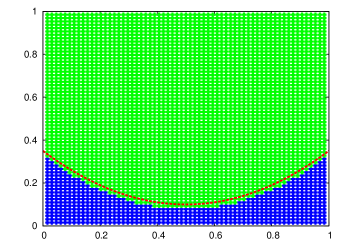

The numerical results are performed for Equation (26) when discretized on a grid with points in each direction. In the domain , for a fixed strategy of max, we represent a points with a green color when , that is where max decides to continue playing, and with a blue color when , that is when max decides to stop the game. The optimal strategy for max is to have only green points above the red curve, , and only blue points under. We start the tests with for all , that is with blue points in the whole domain.

Numerical results with AMG are shown geometrically in Figure 7 where the strategies of max obtained after , , , , , and iterations are represented. We observe in Table 9 that AMG finds an approximation of the solution after iterations and in about two hours and 15 minutes. The stopping criterion for policy iterations of AMG in this test is . This criterion was chosen to ensure the convergence of the policy iterations, indeed with a smaller it did not converge because the intern policy iterations did not gave a precise enough approximation.

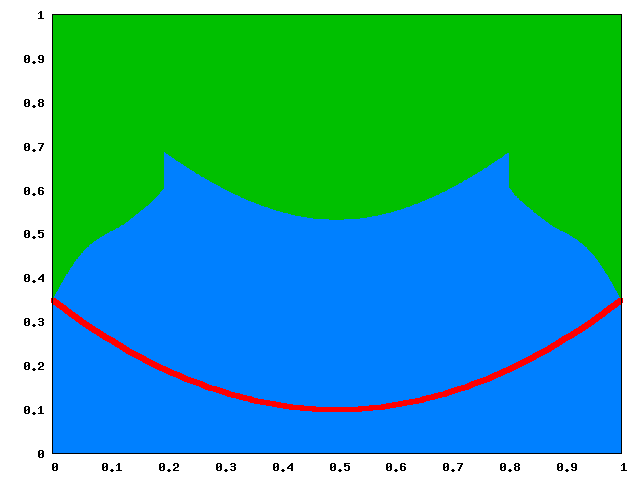

In table 10, we present numerical results for the application of FAMG with and to problem (26) for a points grid. We observe that our algorithm solves the problem in about seconds. Geometrical representation of the strategies of max obtained by AMG on four successive levels in the FAMG algorithm, are shown in Figure 8. We can see that on coarse grids, the algorithm can find a good approximation of the solution in a few iterations. The interpolation of this solution and the corresponding strategies, are used to start AMG on the next fine level and we observe that only a few numbers of policy iterations are needed on each level.

With this example we show the advantage of using FAMG. Indeed, the computation time of the FAMG algorithm seems to be in the order of the number of discretization points whereas that of a AMG algorithm is about times greater. This is due to the large number of iterations needed by AMG for solving this kind of games. Indeed, this number should be compared to the diameter of the graph (that is the largest number of edges which must be cover to travel from one point to another) associated to the corresponding game problem, for instance the union of all graphs of the Markov chains associated to all couple of fixed policies and . Hence due to the finite differences discretization, the arcs of the graphs are supported by edges of the grids in , so the diameter is with .

6.3 Stopping game with two optimal stopping

In this example, we consider a stopping game where both players have the possibility to stop the game, see [33] for a complete theory about this subject. In this case, the value of the game starting in is given by :

where and we assume (, then is solution of equation :

| (27) |

or equivalently,

that is

For the numerical tests, we consider the stochastic differential game whose value is solution of :

| (28) |

where , for all : , with and . For all , the sets of actions are for max and for min, where action means that the player chooses to stop the game and receive when max stops or when min stops, action means that the game is continuing. Here, the exact solution of Equation (28) in the viscosity sense is

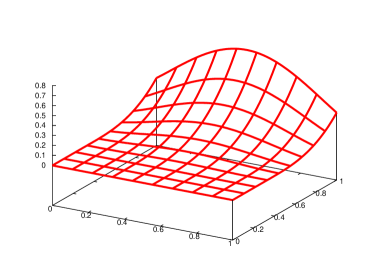

where the constant and is represented in Figure 9. For all , the optimal strategy for max is if and else. For all , the optimal strategy for min is if and else.

We present numerical results for the discretization of Equation (28) on a grid with points in Table 11 when using AMG with and in Table 12 when using FAMG with and . As in the previous example, we see the advantage of using FAMG for this kind of games. Indeed, FAMG solves the problem in about one second while AMG needs about minutes. As for the previous example, the computation time of the FAMG seems to be in the order of the number of discretization points. For this example, due to the finite differences discretization, the diameter of the graph is with . We see in Table 11 that both numbers of intern and external policy iterations for AMG are of the order of the diameter of the graph.

| cpu time (s) | ||||||

| cpu time (s) | ||||||

| points in each direction : , step size : | ||||||

| points in each direction : , step size : | ||||||

| points in each direction : , step size : | ||||||

| points in each direction : , step size : | ||||||

| points in each direction : , step size : | ||||||

| points in each direction : , step size : | ||||||

| points in each direction : , step size : | ||||||

| points in each direction : , step size : | ||||||

| points in each direction : , step size : | ||||||

| points in each direction : , step size : | ||||||

| points in each direction : , step size : | ||||||

7 Conclusion and perspective

In this paper, we have presented our algorithm AMG for solving two player zero-sum stochastic games. This program combines the policy iteration algorithm with algebraic multigrid methods. Our experiences on a Isaacs equation show better results for AMG in comparison with policy iteration combined to a direct linear solver. We observed that the most part of the computation time for the resolution of a non-linear equation (5) is used to solved the linear systems involved in the policy iteration algorithm. Hence, we noticed that the computation time of AMG increase linearly with the size of the problem.

Furthermore, we also presented a full multi-level algorithm, called FAMG, for solving two player zero-sum stochastic differential games. The numerical results on some stopping differential stochastic games presented here show that FAMG improves substantially the computation time of the policy iteration algorithm for this kind of games. Indeed the computation time of FAMG seems to be in the order of the number of discretization points whereas that of AMG algorithm is about to times greater. This is due to the large number of iterations needed by AMG for solving this kind of games. Indeed, this number should be compared to the diameter of the graph associated to the corresponding game problem, for instance the union of all graphs of the Markov chains associated to fixed policies and .

The FAMG algorithm uses coarse grids discretizations of the partial differential equation and so cannot be applied directly to the dynamic programming equation of a two player zero-sum stochastic game with finite state space. One may ask if adapting the FAMG algorithm to this kind of games is possible. Indeed, the complexity of two player zero-sum stochastic games is still unsettled, one only knows that it belongs to the complexity class of NPcoNP [49], and any new approach maybe useful to understand this complexity.

References

- [1] Marianne Akian. Analyse de l’algorithme multigrille FMGH de résolution d’équations d’Hamilton-Jacobi-Bellman. In Analysis and optimization of systems (Antibes, 1990), volume 144 of Lecture Notes in Control and Inform. Sci., pages 113–122. Springer, Berlin, 1990.

- [2] Marianne Akian. Méthodes multigrilles en contrôle stochastique. Institut National de Recherche en Informatique et en Automatique (INRIA), Rocquencourt, 1990. Thèse, Université de Paris IX (Paris-Dauphine), Paris, 1990.

- [3] Marianne Akian, Stéphane Gaubert, and Asma Lakhoua. The max-plus finite element method for solving deterministic optimal control problems: basic properties and convergence analysis. SIAM J. Control Optim., 47(2):817–848, 2008.

- [4] E. Altman. Flow control using the theory of zero sum Markov games. IEEE Trans. Automat. Control, 39(4):814–818, 1994.

- [5] Randolph E. Bank and Donald J. Rose. Analysis of a multilevel iterative method for nonlinear finite element equations. Math. Comp., 39(160):453–465, 1982.

- [6] M. Bardi, M. Falcone, and P. Soravia. Fully discrete schemes for the value function of pursuit-evasion games. In Advances in dynamic games and applications (Geneva, 1992), volume 1 of Ann. Internat. Soc. Dynam. Games, pages 89–105. Birkhäuser Boston, Boston, MA, 1994.

- [7] Martino Bardi, Maurizio Falcone, and Pierpaolo Soravia. Numerical methods for pursuit-evasion games via viscosity solutions. In Stochastic and differential games, volume 4 of Ann. Internat. Soc. Dynam. Games, pages 105–175. Birkhäuser Boston, Boston, MA, 1999.

- [8] G. Barles and P. E. Souganidis. Convergence of approximation schemes for fully nonlinear second order equations. Asymptotic Anal., 4(3):271–283, 1991.

- [9] T. Başar and P. Bernhard. -optimal control and related minimax design problems. Systems & Control: Foundations & Applications. Birkhäuser Boston Inc., Boston, MA, second edition, 1995. A dynamic game approach.

- [10] Richard Bellman. Dynamic programming. Princeton University Press, Princeton, N. J., 1957.

- [11] A. Bensoussan and J.-L. Lions. Applications des inéquations variationnelles en contrôle stochastique. Dunod, Paris, 1978. Méthodes Mathématiques de l’Informatique, No. 6.

- [12] A. Bensoussan and J.-L. Lions. Contrôle impulsionnel et inéquations quasi variationnelles, volume 11 of Méthodes Mathématiques de l’Informatique [Mathematical Methods of Information Science]. Gauthier-Villars, Paris, 1982.

- [13] Abraham Berman and Robert J. Plemmons. Nonnegative matrices in the mathematical sciences, volume 9 of Classics in Applied Mathematics. Society for Industrial and Applied Mathematics (SIAM), Philadelphia, PA, 1994. Revised reprint of the 1979 original.

- [14] D. P. Bertsekas. Dynamic programming. Prentice Hall Inc., Englewood Cliffs, NJ, 1987. Deterministic and stochastic models.

- [15] Olivier Bokanowski, Stefania Maroso, and Hasnaa Zidani. Some convergence results for Howard’s algorithm. SIAM J. Numer. Anal., 47(4):3001–3026, 2009.

- [16] J. Frédéric Bonnans and Housnaa Zidani. Consistency of generalized finite difference schemes for the stochastic HJB equation. SIAM J. Numer. Anal., 41(3):1008–1021 (electronic), 2003.

- [17] A. Brandt, S. McCormick, and J. Ruge. Algebraic multigrid (AMG) for sparse matrix equations. In Sparsity and its applications (Loughborough, 1983), pages 257–284. Cambridge Univ. Press, Cambridge, 1985.

- [18] Achi Brandt. Algebraic multigrid theory: the symmetric case. Appl. Math. Comput., 19(1-4):23–56, 1986. Second Copper Mountain conference on multigrid methods (Copper Mountain, Colo., 1985).

- [19] Jean Cochet-Terrasson and Stéphane Gaubert. A policy iteration algorithm for zero-sum stochastic games with mean payoff. C. R. Math. Acad. Sci. Paris, 343(5):377–382, 2006.

- [20] Michael G. Crandall, Hitoshi Ishii, and Pierre-Louis Lions. User’s guide to viscosity solutions of second order partial differential equations. Bull. Amer. Math. Soc. (N.S.), 27(1):1–67, 1992.

- [21] Timothy A. Davis. Algorithm 832: Umfpack v4.3—an unsymmetric-pattern multifrontal method. ACM Trans. Math. Softw., 30:196–199, June 2004.

- [22] E. V. Denardo and B. L. Fox. Multichain Markov renewal programs. SIAM J. Appl. Math., 16:468–487, 1968.

- [23] Eric V. Denardo. Contraction mappings in the theory underlying dynamic programming. SIAM Rev., 9:165–177, 1967.

- [24] Vishesh Dhingra and Stéphane Gaubert. How to solve large scale deterministic games with mean payoff by policy iteration. In valuetools ’06: Proceedings of the 1st international conference on Performance evaluation methodolgies and tools, page 12, New York, NY, USA, 2006. ACM.

- [25] R. J. Elliott and T.K̃. Siu. A stochastic differential game for optimal investment of an insurer with regime switching. Quant. Finance, 11(3):365–380, 2011.

- [26] Robert D. Falgout, Panayot S. Vassilevski, and Ludmil T. Zikatanov. On two-grid convergence estimates. Numer. Linear Algebra Appl., 12(5-6):471–494, 2005.

- [27] John Fearnley. Exponential lower bounds for policy iteration. In Automata, Languages and Programming, pages 551–562, 2010.

- [28] John Fearnley. Exponential lower bounds for policy iteration, 2010. arXiv:1003.3418v1.

- [29] Jerzy Filar and Koos Vrieze. Competitive Markov decision processes. Springer-Verlag, New York, 1997.

- [30] W. H. Fleming and H. M. Soner. Controlled Markov processes and viscosity solutions, volume 25 of Stochastic Modelling and Applied Probability. Springer, New York, second edition, 2006.

- [31] W. H. Fleming and P. E. Souganidis. On the existence of value functions of two-player, zero-sum stochastic differential games. Indiana Univ. Math. J., 38(2):293–314, 1989.

- [32] Wendell H. Fleming. Risk sensitive stochastic control and differential games. Commun. Inf. Syst., 6(3):161–177, 2006.

- [33] Avner Friedman. Stochastic games and variational inequalities. Arch. Rational Mech. Anal., 51:321–346, 1973.

- [34] Oliver Friedmann. An exponential lower bound for the parity game strategy improvement algorithm as we know it. In LICS, pages 145–156. IEEE Computer Society, 2009.

- [35] A. J. Hoffman and R. M. Karp. On nonterminating stochastic games. Management Sci., 12:359–370, 1966.

- [36] Ronald H. W. Hoppe. Multigrid methods for Hamilton-Jacobi-Bellman equations. Numer. Math., 49(2-3):239–254, 1986.

- [37] Ronald H. W. Hoppe. Multigrid algorithms for variational inequalities. SIAM J. Numer. Anal., 24(5):1046–1065, 1987.

- [38] Ronald A. Howard. Dynamic programming and Markov processes. The Technology Press of M.I.T., Cambridge, Mass., 1960.

- [39] Harold J. Kushner. Probability methods for approximations in stochastic control and for elliptic equations. Academic Press [Harcourt Brace Jovanovich Publishers], New York, 1977. Mathematics in Science and Engineering, Vol. 129.

- [40] Harold J. Kushner and Paul G. Dupuis. Numerical methods for stochastic control problems in continuous time, volume 24 of Applications of Mathematics (New York). Springer-Verlag, New York, 1992.

- [41] P.-L. Lions and B. Mercier. Approximation numérique des équations de Hamilton-Jacobi-Bellman. RAIRO Anal. Numér., 14(4):369–393, 1980.

- [42] Stephen F. McCormick, editor. Multigrid methods, volume 3 of Frontiers in Applied Mathematics. Society for Industrial and Applied Mathematics (SIAM), Philadelphia, PA, 1987.

- [43] W.M. McEneaney, B.G. Fitzpatrick, and I.G. Lauko. Stochastic game approach to air operations. IEEE Trans. Aero. Elec. Systems, 40:1191–1216, 2004.

- [44] C. Mense and R. Nabben. On algebraic multi-level methods for non-symmetric systems—comparison results. Linear Algebra Appl., 429(10):2567–2588, 2008.

- [45] Rémi Munos and Hasnaa Zidani. Consistency of a simple multidimensional scheme for Hamilton-Jacobi-Bellman equations. C. R. Math. Acad. Sci. Paris, 340(7):499–502, 2005.

- [46] A. Neyman and S. Sorin. Stochastic games and applications, volume 570. Springer Netherlands, 2003.

- [47] Yvan Notay. Algebraic analysis of two-grid methods: The nonsymmetric case. Numer. Linear Algebra Appl., 17(1):73–96, 2010.

- [48] N. Shimkin O. Ziv. Multigrid methods for policy evaluation and reinforcement learning. In Proc. IEEE International Symposium on Intelligent Control (ISIC05). IEEE, 2005.

- [49] Anuj Puri. Theory of hybrid systems and discrete event systems. PhD thesis, Berkeley, CA, USA, 1995.

- [50] M. L. Puterman. Markov decision processes: discrete stochastic dynamic programming. Wiley Series in Probability and Mathematical Statistics: Applied Probability and Statistics. John Wiley & Sons Inc., New York, 1994.

- [51] Martin L. Puterman and Shelby L. Brumelle. On the convergence of policy iteration in stationary dynamic programming. Math. Oper. Res., 4(1):60–69, 1979.

- [52] R. T. Rockafellar. Convex analysis. Princeton University Press, 1970.

- [53] J. W. Ruge and K. Stüben. Algebraic multigrid. In Stephen F. McCormick, editor, Multigrid methods, volume 3 of Frontiers Appl. Math., pages 73–130. SIAM, Philadelphia, PA, 1987.

- [54] L. S. Shapley. Stochastic games. In Stochastic games and applications (Stony Brook, NY, 1999), volume 570 of NATO Sci. Ser. C Math. Phys. Sci., pages 1–7. Kluwer Acad. Publ., Dordrecht, 2003. Reprint of Proc. Nat. Acad. Sci. U.S.A. 39 (1953), 1095–1100 [0061807].

- [55] Sylvain Sorin. Classification and basic tools. In Stochastic games and applications (Stony Brook, NY, 1999), volume 570 of NATO Sci. Ser. C Math. Phys. Sci., pages 27–36. Kluwer Acad. Publ., Dordrecht, 2003.

- [56] Andrzej Świpolhkech. Another approach to the existence of value functions of stochastic differential games. J. Math. Anal. Appl., 204(3):884–897, 1996.