Optimal stopping problems for the maximum process with upper and lower caps

Abstract

This paper concerns optimal stopping problems driven by the running maximum of a spectrally negative Lévy process . More precisely, we are interested in modifications of the Shepp–Shiryaev optimal stopping problem [Avram, Kyprianou and Pistorius Ann. Appl. Probab. 14 (2004) 215–238; Shepp and Shiryaev Ann. Appl. Probab. 3 (1993) 631–640; Shepp and Shiryaev Theory Probab. Appl. 39 (1993) 103–119]. First, we consider a capped version of the Shepp–Shiryaev optimal stopping problem and provide the solution explicitly in terms of scale functions. In particular, the optimal stopping boundary is characterised by an ordinary differential equation involving scale functions and changes according to the path variation of . Secondly, in the spirit of [Shepp, Shiryaev and Sulem Advances in Finance and Stochastics (2002) 271–284 Springer], we consider a modification of the capped version of the Shepp–Shiryaev optimal stopping problem in the sense that the decision to stop has to be made before the process falls below a given level.

doi:

10.1214/12-AAP903keywords:

[class=AMS]keywords:

60G40, 60G51, 60J75, Optimal stopping, optimal stopping boundary, principle of smooth fit, principle of continuous fit, Levy processes, scale functions

1 Introduction

Let be a spectrally negative Lévy process defined on a filtered probability space satisfying the natural conditions; cf. bichteler , Section 1.3, page 39. For , denote by the probability measure under which starts at and for simplicity write . We associate with the maximum process given by for . The law under which starts at is denoted by .

In this paper we are mainly interested in the following optimal stopping problem:

| (1) |

where , and is the set of all finite -stopping times. Since the constant bounds the process from above, we refer to it as the upper cap. Due to the fact that the pair is a strong Markov process, (1) has also a Markovian structure and hence the general theory of optimal stopping peskir suggests that the optimal stopping time is the first entry time of the process into some subset of . Indeed, it turns out that under some assumptions on and , where is the Laplace exponent of [see ( ‣ 3.1), page ‣ 3.1, for a formal definition], the solution of (1) is given by

for some function which is characterised as a solution to a certain ordinary differential equation involving scale functions. The function is sometimes referred to as the optimal stopping boundary. We will show that the shape of the optimal boundary has different characteristics according to the path variation of . The solution of problem (1) is closely related to the solution of the Shepp–Shiryaev optimal stopping problem

| (2) |

which was first studied by Shepp and Shiryaev russianoption , anewlook for the case when is a linear Brownian motion and later by Avram, Kyprianou and Pistorius exitproblems for the case when is a spectrally negative Lévy process. Shepp and Shiryaev russianoption introduced the problem as a means to pricing Russian options. In the latter context the solution of (2) can be viewed as the fair price of such an option. If we introduce a cap , an analogous interpretation of the solution of (1) applies, but for a Russian option whose payoff was moderated by capping it at a certain level (a fuller description is given in Section 2).

Our method for solving (1) consists of a verification technique, that is, we heuristically derive a candidate solution and then verify that it is indeed a solution. In particular, we will make use of the principle of smooth and continuous fit peskir , mikhalevich , pesshir , someremarks in a similar way to russianoption , maximalityprinciple .

It is also natural to ask for a modification of (1) with a lower cap. Whilst this is already included in the starting point of the maximum process , there is a stopping problem that captures this idea of lower cap in the sense that the decision to exercise has to be made before drops below a certain level. Specifically, consider

| (3) |

where such that , and . In the special case of no cap (), this problem was considered by Shepp, Shiryaev and Sulem abarrierversion for the case where is a linear Brownian motion. Inspired by their result we expect the optimal stopping time to be of the form , where is the optimal stopping time in (1). Our main contribution here is that, with the help of excursion theory (cf. kyprianou , bertoinbook ), we find a closed form expression for the value function associated with the strategy , thereby allowing us to verify that it is indeed an optimal strategy.

This paper is organised as follows. In Section 2 we provide some motivation for studying (1) and (3). Then we introduce some more notation and collect some auxiliary results in Section 3. Our main results are presented in Section 4, followed by their proofs in Sections 5 and 6. Finally, some numerical examples are given in Section 7.

2 Application to pricing capped Russian options

Consider a financial market consisting of a riskless bond and a risky asset. The value of the bond evolves deterministically such that

| (4) |

The price of the risky asset is modeled as the exponential spectrally negative Lévy process

| (5) |

In order to guarantee that our model is free of arbitrage we will assume that . If , where is a standard Brownian motion, we get the standard Black–Scholes model for the price of the asset. Extensive empirical research has shown that this (Gaussian) model is not capable of capturing certain features (such as skewness and heavy tails) which are commonly encountered in financial data, for example, returns on stocks. To accommodate for these problems, an idea, going back to merton , is to replace the Brownian motion as the model for the log-price by a general Lévy process ; cf. chan . Here we will restrict ourselves to the model where is given by a spectrally negative Lévy process. This restriction is mainly motivated by analytical tractability. It is worth mentioning, however, that Carr and Wu carr as well as Madan and Schoutens madan have offered empirical evidence to support the case of a model in which the risky asset is driven by a spectrally negative Lévy process for appropriate market scenarios.

A capped Russian option is an option which gives the holder the right to exercise at any almost surely finite stopping time yielding payouts

The constant can be viewed as representing the “starting” maximum of the stock price (say, over some previous period . The constant can be interpreted as cap and moderates the payoff of the option. The value is also allowed and corresponds to no moderation at all. In this case we just get the normal Russian option. Finally, when it is necessary to choose strictly positive to guarantee that it is optimal to stop in finite time and that the value is finite; cf. Proposition 3.1.

Standard theory of pricing American-type options shirfin directs one to solving the optimal stopping problem

| (6) |

where the supremum is taken over all -valued -stopping times. In other words, we want to find a stopping time which optimises the expected discounted claim. The right-hand side of (6) may be rewritten as

where and .

In (6) one might only allow stopping times that are smaller or equal than the first time the risky asset drops below a certain barrier. From a financial point of view this corresponds to a default time after which all economic activity stops; cf. abarrierversion . Including this additional feature leads in an analogous way to the above optimal stopping problem (3).

3 Notation and auxiliary results

The purpose of this section is to introduce some notation and collect some known results about spectrally negative Lévy processes. Moreover, we state the solution of the Shepp–Shiryaev optimal stopping problem (2) which will play an important role throughout this paper.

3.1 Spectrally negative Lévy processes

It is well known that a spectrally negative Lévy process is characterised by its Lévy triplet , where and is a measure on satisfying the condition . By the Lévy–Itô decomposition, may be represented in the form

| (7) |

where is a standard Brownian motion, is a compound Poisson process with discontinuities of magnitude bigger than or equal to one and is a square integrable martingale with discontinuities of magnitude strictly smaller than one and the three processes are mutually independent. In particular, if is of bounded variation, the decomposition reduces to

| (8) |

where , and is a driftless subordinator. Furthermore, the spectral negativity of ensures existence of the Laplace exponent of , that is, for , which is known to take the form

| () |

Its right-inverse is defined by

for .

For any spectrally negative Lévy process having we introduce the family of martingales

defined for any for which , and further the corresponding family of measures with Radon–Nikodym derivatives

| (9) |

For all such the measure will denote the translation of under which . In particular, under the process is still a spectrally negative Lévy process; cf. Theorem 3.9 in kyprianou .

3.2 Scale functions

A special family of functions associated with spectrally negative Lévy processes is that of scale functions (cf. kyprianou ) which are defined as follows. For , the -scale function is the unique function whose restriction to is continuous and has Laplace transform

and is defined to be identically zero for . Equally important is the scale function defined by

The passage times of below and above are denoted by

We will make use of the following four identities. For and it holds that

| (10) | |||||

| (11) |

for and it holds that

| (12) |

and finally for we have

| (13) |

Identities (10) and (11) are Proposition 1 in exitproblems , identity (13) is Lemma 1 of exitproblems and (12) can be found in Theorem 8.1 in kyprianou . For each we denote by the -scale function with respect to the measure . A useful formula (cf. kyprianou ) linking the scale function under different measures is given by

| (14) |

for and .

We conclude this subsection by stating some known regularity properties of scale functions; cf. Lemma 2.4, Corollary 2.5, Theorem 3.10, Lemmas 3.1 and 3.2 of KuzKypRiv .

Smoothness: For all ,

Continuity at the origin: For all ,

| (15) |

Derivative at the origin: For all ,

| (16) |

where we understand the second case to be when .

For technical reasons, we require for the rest of the paper that is in [and hence ]. This is ensured by henceforth assuming that is atomless whenever has paths of bounded variation.

3.3 Solution to the Shepp–Shiryaev optimal stopping problem

In order to state the solution of the Shepp–Shiryaev optimal stopping problem, we introduce the function which is defined as

It can be shown (cf. page 6 of baurdoux ) that, when , the function is strictly decreasing to and hence within this regime

In particular, when , then if and only if . Also, note that the requirement implies . We now give a reformulation of a part of Theorem 1 in baurdoux .

Proposition 3.1

(b) If [and hence ], then the solution of (2) is given by and optimal strategy .

(c) If , then .

The result in part (b) of Proposition 3.1 is not surprising. If , then is necessarily of bounded variation with which implies that the process is pathwise decreasing. As a result we have for the inequality and hence (b) follows. An analogous argument shows that for with optimal strategy and for with optimal strategy . Therefore, we will not consider the regime in what follows. Note, however, that the parameter regime will not be degenerate for (1) and (3) due to the upper cap which prevents the value function from exploding.

4 Main results

4.1 Maximum process with upper cap

The first result ensures existence of a function which, as will follow in due course, describes the optimal stopping boundary in (1).

Lemma 4.1

Let be given. {longlist}[(b)]

If and , then .

If , then .

Under the assumptions in (a) or (b), there exists a unique solution of the ordinary differential equation

| (17) |

satisfying and .

Next, extend to the whole real line by setting for . We now present the solution of (1).

Theorem 4.2

Define the continuation region

and the stopping region . The shape of the boundary separating them, that is, the optimal stopping boundary, is of particular interest. Theorem 4.2 together with (15) and (17) shows that

Also, using (13) we see that

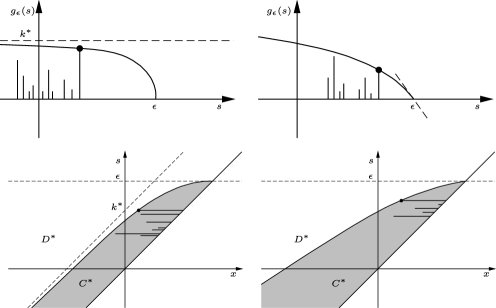

This (qualitative) behaviour of and the resulting shape of the continuation and stopping region are illustrated in Figure 1. Note in particular that the shape of at (and consequently the optimal boundary) changes according to the path variation of .

The horizontal and vertical lines in Figure 1 are meant to schematically indicate the trace of the excursions of away from the running maximum. We thus see that the optimal strategy consists of continuing if the height of the excursion away from the running supremum does not exceed ; otherwise we stop.

4.2 Maximum process with upper and lower cap

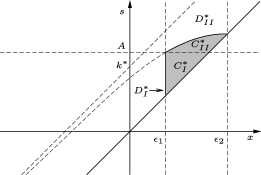

Inspired by the result in abarrierversion , we expect the strategy to be optimal, where is given in Theorem 4.2 and . This means that the optimal boundary is expected to be a vertical line at combined with the curve described by characterised in Lemma 4.1. Before we can proceed, we need to introduce an auxiliary quantity, namely the point on the -axis where the vertical line at and the optimal boundary corresponding to intersect; see Figure 2. If and or define the map by

. It follows by definition of that is continuous, strictly increasing and satisfies and . Therefore the intermediate value theorem guarantees existence of a unique such that . Our candidate optimal strategy splits into the stopping regions

and the continuation regions

Clearly, if , then the only stopping time in is and hence the optimal value function is given by . Furthermore, when we have , so that the optimality of in (1) implies . Consequently, the interesting case is really . The key to verifying that is optimal, is to find the value function associated with it.

Lemma 4.3

Let be given, and suppose that and or . Define

where is given in Theorem 4.2,

and is the unique constant such that . We then have, for ,

Our main contribution here is the expression for , thereby allowing us to verify that the strategy is still optimal. In fact, this is the content the following result.

Theorem 4.4

It is also possible to obtain the solution of (3) with lower cap only. To this end, define when and the constant function and .

Corollary 4.5

Let and suppose that , that is, there is no upper cap. {longlist}[(b)]

Assume that and that . Then the solution to (3) is given by

| (18) |

where is given in Proposition 3.1 and

The corresponding optimal strategy is given by , where is given in Proposition 3.1.

If , then for and otherwise.

Remark 4.6.

In Theorem 4.2 there is no lower cap, and hence it seems natural to obtain Theorem 4.2 as a corollary to Theorem 4.4. This would be possible if one merged the proofs of Theorems 4.2 and 4.4 appropriately. However, a merged proof would still contain the main arguments of both the proof of Theorem 4.2 and the proof of Theorem 4.4 (note that the proof of Theorem 4.4 makes use of Theorem 4.2). Therefore, and also for presentation purposes, we chose to present them separately.

Finally, if , where and is a standard Brownian motion, then Corollary 4.5 is nothing else than Theorem 3.1 in abarrierversion . However, this is not immediately clear and requires a simple but lengthy computation which is provided in Section 7.

5 Guess and verify via principle of smooth or continuous fit

Let us consider the solution to (1) from an intuitive point of view. We shall restrict ourselves to the case where and . It follows from what was said at the beginning of Section 3.3 that .

It is clear that if such that , then it is optimal to stop immediately since one cannot obtain a higher payoff than , and waiting is penalised by exponential discounting. If is much smaller than , then the cap should not have too much influence, and one expects that the optimal value function and the corresponding optimal strategy look similar to the optimal value function and optimal strategy of problem (2). On the other hand, if is close to the cap, then the process should be stopped “before” it is a distance away from its running maximum. This can be explained as follows: the constant in the solution to problem (2) quantifies the acceptable “waiting time” for a possibly much higher running supremum at a later point in time. But if we impose a cap, there is no hope for a much higher supremum and therefore “waiting the acceptable time” for problem (2) does not pay off in the situation with cap. With exponential discounting we would therefore expect to exercise earlier. In other words, we expect an optimal strategy of the form

for some function satisfying and .

This qualitative guess can be turned into a quantitative guess by an adaptation of the argument in Section 3 of maximalityprinciple to our setting. To this end, assume that is of unbounded variation (). We will deal with the bounded variation case later. From the general theory of optimal stopping (cf. peskir , Section 13) we informally expect the value function

to satisfy the system

| (19) | |||||

where is the infinitesimal generator of the process under . Moreover, the principle of smooth fit peskir , mikhalevich suggests that this system should be complemented by

| (20) |

Note that, although the smooth fit condition is not necessarily part of the general theory, it is imposed since by the “rule of thumb” outlined in Section 7 in someremarks it should hold in this setting because of path regularity. This belief will be vindicated when we show that system (5) with (20) leads to the solution of problem (1). Applying the strong Markov property at and using (10) and (11) shows that

Furthermore, the smooth fit condition implies

By (16) the first factor tends to a strictly positive value or infinity which shows that . This would mean that for such that we have

| (21) |

Having derived the form of a candidate optimal value function , we still need to do the same for . Using the normal reflection condition in (5) shows that our candidate function should satisfy the ordinary differential equation

If is of bounded variation (), we informally expect from the general theory that satisfies the first two equations of (5). Additionally, the principle of continuous fit someremarks , pesshir suggests that the system should be complemented by

A very similar argument as above produces the same candidate value function and the same ordinary differential equation for .

6 Proofs of main results

{pf*}Proof of Lemma 4.1 The idea is to define a suitable bijection from to whose inverse satisfies the differential equation and the boundary conditions.

First consider the case and . It follows from the discussion at the beginning of Section 3.3 that and that the function is negative on . Moreover, and . These properties imply that the function defined by

is strictly decreasing. If we can also show that the integral tends to as approaches , we could deduce that is a bijection from to . Indeed, appealing to l’Hôpital’s rule and using (12) we obtain

Denote the term on the right-hand side by , and note that due to the fact that is strictly positive and increasing on and since for . Hence there exists a and such that for all . Thus

This shows that

The discussion above permits us to define . In particular, differentiating gives

for , and satisfies and by construction.

As for the case , note that by (12) and (13) we have

| (23) |

for which shows that . Moreover, (23) together with (13) implies that the map is negative on and satisfies and . Defining as in (6), one deduces similarly as above that is a continuously differentiable bijection whose inverse satisfies the requirements.

We finish the proof by addressing the question of uniqueness. To this end, assume that there is another solution . In particular, for and hence

which implies that . {pf*}Proof of Theorem 4.2 Define the function

for , and let , where is as in Lemma 4.1. Because of the infinite horizon and Markovian claim structure of problem (1) it is enough to check the following conditions: {longlist}[(iii)]

for all ;

is a right-continuous -supermartingale for ;

for all . To see why these are sufficient conditions, note that (i) and (ii) together with Fatou’s lemma in the second inequality and Doob’s stopping theorem in the third inequality show that for ,

which in view of (iii) implies and .

The remainder of this proof is devoted to checking conditions (i)–(iii). Clearly, condition (i) is satisfied since is bigger or equal to one by definition.

Supermartingale property (ii). Given the inequality

| (24) |

the supermartingale property is a consequence of the Markov property of the process . Indeed, for we have

We now prove (24), first under the assumption that , that is, is of unbounded variation. Let be the infinitesimal generator of and formally define the function by

For the quantity is well defined and . However, for one needs to check whether the integral part of is well defined. This is done in Lemma A.1 in the Appendix which shows that this is indeed the case. Moreover, as shown in Section 3.2 of pist , it holds that

Now fix and define the semimartingale . Applying an appropriate version of the Itô–Meyer formula (cf. Theorem 71, Chapter IV of protter ) to yields -a.s.

where

and . The fact that is not defined at zero is not a problem as the time spends at zero has Lebesgue measure zero anyway. By the boundedness of on the first two stochastic integrals in the expression for are zero-mean martingales, and by the compensation formula (cf. Corollary 4.6 of kyprianou ) the third and fourth term constitute a zero-mean martingale. Next, recall that and use stochastic integration by parts for semimartingales (cf. Corollary 2 of Theorem 22, Chapter II of protter ) to deduce that

| (26) | |||

where is a zero-mean martingale. The first integral is nonpositive since for all . The last integral vanishes since the process only increments when and by definition of . Thus, taking expectations on both sides yields

If (X has bounded variation), then the Itô–Meyer formula is nothing more than an appropriate version of the change of variable formula for Stieltjes integrals and the rest of the proof follows the same line of reasoning as above. The only change worth mentioning is that the generator of takes a different form. Specifically, one has to work with

which satisfies all the required properties by Lemma A.1 in the Appendix and Section 3.2 in pist .

This completes the proof of the supermartingale property.

Verification of condition (iii). The assertion is clear for . Hence, suppose that . The assertion now follows from the proof of the supermartingale property (ii). More precisely, replacing by in (6) and recalling that for shows that

Using that a.s. and dominated convergence, one obtains the desired equality. {pf*}Proof of Lemma 4.3 For we have so that

As for the case , write

and denote the first expectation on the right by and the second expectation by . An application of the strong Markov property at and the definition of (see Theorem 4.2) give

Recalling that and using the strong Markov property at yields

Next, we compute the expectation on the right-hand side of (6) by excursion theory. To be more precise, we are going to make use of the compensation formula of excursion theory, and hence we shall spend a moment setting up some necessary notation. In doing so, we closely follow pages 221–223 in exitproblems and refer the reader to Chapters 6 and 7 in bertoinbook for background reading. The process serves as local time at for the Markov process under . Write for the right-continuous inverse of . The Poisson point process of excursions indexed by local time shall be denoted by , where

whenever . Accordingly, we refer to a generic excursion as (or just for short as appropriate) belonging to the space of canonical excursions. The intensity measure of the process is given by , where is a measure on the space of excursions (the excursion measure). A functional of the canonical excursion that will be of interest is , where is the length of an excursion. A useful formula for this functional that we shall make use of is the following (cf. kyprianou , equation (8.18)):

| (28) |

provided that is not a discontinuity point in the derivative of [which is only a concern when is of bounded variation, but we have assumed that in this case is atomless and hence is continuously differentiable on . Another functional that we will also use is , the first passage time above of the canonical excursion . We now proceed with the promised calculation involving excursion theory. Specifically, an application of the compensation formula in the second equality and using Fubini’s theorem in the third equality gives

where in the first equality the time index runs over local times and the sum is the usual shorthand for integration with respect to the Poisson counting measure of excursions, and is an expression taken from Theorem 1 in exitproblems . Next, note that is a stopping time and hence a change of measure according to (9) shows that the expectation inside the integral can be written as

Using the properties of the Poisson point process of excursions (indexed by local time) and with the help of (28) and (14) we may deduce

where denotes the excursion measure associated with under . By a change of variables and the fact that we further obtain

Integrating by parts on the right-hand side, plugging the resulting expression into (6) and finally adding and gives the result. {pf*}Proof of Theorem 4.4 Recall that and from Lemma 4.3 that, for ,

| (29) |

Similarly to the proof of Theorem 4.2, it is now enough to prove that: {longlist}[(ii)]

for all ;

is a right-continuous -supermartingale for all . Condition (i) is clearly satisfied, so we devote the remainder of this proof to checking condition (ii).

Supermartingale property (ii). Let for . Analogously to the proof of Theorem 4.2, it suffices to show that for we have the inequality

| (30) |

The latter is clear for . If , inequality (30) can be extracted from the proof of Theorem 4.2 where it is shown that the process is a -supermartinagle for all . In particular, the process is a -supermartingale for . The supermartingale property is preserved when stopping at and therefore we obtain, for ,

| (31) |

Thus, it remains to establish (30) for . To this end, we first prove that the process is a -martingale. The strong Markov property gives

By definition of we see that

which shows that the second term on the right-hand side of (6) equals

Thus, which implies the martingale property of . Again using the strong Markov property we further obtain for ,

where the inequality follows from (31) and the fact that on . Thus, for . This completes the proof. {pf*}Proof of Corollary 4.5 Part (a) follows from the proof of Theorem 4.4 by replacing with and by . For part (b), let be given and recall that due to the assumption we have . For an arbitrary , the uniqueness in Lemma 4.1 implies that

It follows that for and that . Hence, for , we have

On the other hand, if , then clearly . This completes the proof.

7 Examples

The solutions of (1) and (3) are given semi-explicitly in terms of scale functions and a specific solution and , respectively, of the ordinary differential equation (17). The aim of this section is to look at some examples where the solutions of (1) and (3) can be computed more explicitly. For simplicity, we will assume from now on that every spectrally negative Lévy process considered below is such that and . Also assume to begin with that there is an upper cap only.

A first step towards more explicit solutions of (1) is looking at processes where explicit expressions for and are available. In recent years various authors have found several processes whose scale functions are explicitly known (Example 1.3, Chapter 4 and Section 5.5 in KuzKypRiv , e.g.). Here, however, we would additionally like to find explicitly. To the best of our knowledge, we do not know of any examples where this is possible. One might instead try to solve (17) numerically, but this is not straightforward as there is no initial point to start a numerical scheme from and, moreover, the possibility of having infinite gradient at might lead to inaccuracies in the numerical scheme. Therefore, we follow a different route which avoids these difficulties. Instead of looking at , we rather focus on its inverse

| (33) |

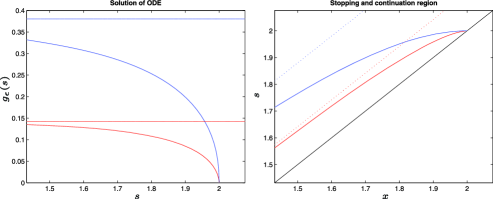

where is the unique root of . It turns out that in some cases (including the Black–Scholes model) can be computed explicitly. Since is the inverse of , plotting , yields visualisations of for ; see Figures 3–5.

Similarly, plotting , produces visualisations of the optimal stopping boundary in the -plane; see Figures 3–5. Unfortunately, it is often the

case that we cannot compute the integral in (33) explicitly in which case one might use numerical integration in Matlab to obtain an approximation of the integral. The procedure just described is carried out below for different examples of .

7.1 Brownian motion with drift and compound Poisson jumps

Consider the process

where , , is a standard Brownian motion, is a Poisson process with intensity and are i.i.d. random variables which are exponentially distributed with parameter . The processes and as well as the sequence are assumed to be mutually independent. The Laplace exponent of is given by

It is known (cf. Example 1.3 in KuzKypRiv and Section 8.2 of exitproblems ) that

| (34) |

where are the three real solutions of the equation , and that, for ,

| (35) |

where , and .

As a first example consider . In this case reduces to a quadratic equation, and one can calculate explicitly

Moreover, it follows that

Using elementary algebra and integration one finds, for ,

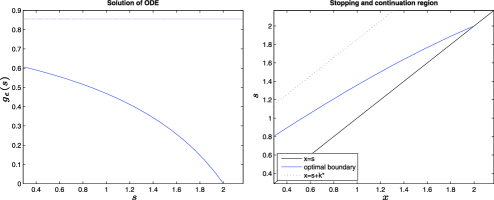

where and . An example for a certain choice of parameters is given in Figure 3.

Next, assume and ; that is, is a linear Brownian motion. In particular, this includes the Black–Scholes model. Again, as explained in Example 1.3 of KuzKypRiv , the equation reduces to a quadratic equation and and , where

Furthermore, (34) and (35) may be rewritten on as

and one can compute

| (37) |

Using elementary algebra in the first and formula 2.447.1 of gradshteyn in the second equality one obtains, for ,

where . An example for a certain parameter choice is provided in Figure 4.

In the next example we combine the first example with the second one. More precisely, suppose that and , that is, a linear Brownian motion with exponential jumps. In this case we are unable to compute and explicitly. We therefore find numerically and use numerical integration to obtain an approximation of and , respectively; see Figure 4.

7.2 Stable jumps

Suppose that is an -stable process, where with Laplace exponent . It is known (cf. Example 4.17 of KuzKypRiv and Section 8.3 of exitproblems ) that, for ,

where is the two-parameter Mittag–Leffler function which is defined for as

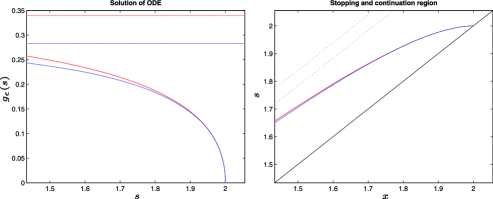

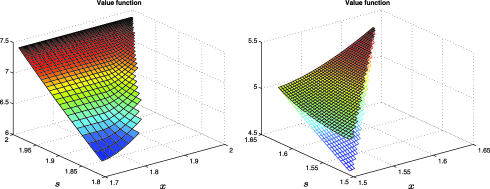

Again, using numerical integration and a Matlab function that computes the Mittag–Leffler function (cf. mittaglefflerfunction ) one may approximate and , respectively; see Figure 5. Additionally, we have computed the value function for a choice of parameters (Figure 6).

If one considers a lower cap and an upper cap , then the only thing that changes for the optimal boundary is that one has to include an additional vertical line at the value of the lower cap . However, introducing a lower cap will make a difference, that is, the value functions and will be different for ; see Theorems 4.2 and 4.4. Exploiting the fact that is the inverse of in a similar way as above, one may also obtain numerical approximations of the value functions and ; see Figure 6.

7.3 Maximum process with lower cap only

Assume the same setting as in the second example above, that is, . The scale functions and are given by (7.1) and (37), respectively. If we suppose that there is a lower cap and no upper cap (), then Corollary 4.5 can be rewritten more explicitly as follows.

Lemma 7.1

The and part of the optimal value function are given by

and

where and .

The proof of this result is a lengthy computation provided in Appendix B. Finally, if we set , for some and for some we recover Theorem 3.1 of abarrierversion .

Appendix A Complementary results on the infinitesimal generator of

In this section we provide some results concerning the infinitesimal generator of when applied to the scale function .

First assume that is of unbounded variation, and define an operator as follows. stands for the family of functions such that the integral

is absolutely convergent for all . For any , we define the function by

Similarly, if is of bounded variation, then stands for the family of such that the integral

is absolutely convergent for all , and for , we define the function by

In the sequel it should always be clear from the context in which of the two cases we are and therefore there should be no ambiguity when writing and .

Lemma A.1

We have that and the function is continuous on .

We prove the unbounded and bounded variation case separately.

Unbounded variation: To show that it is enough to check that the integral part of is absolutely convergent since . Fix and write the integral part of as

where the value is chosen such that . For the monotonicity of implies

| (38) |

and for , using the mean value theorem, we have

| (39) | |||

Using these two estimates and defining , we see that

For continuity, let and choose such that as well as a sequence converging to . Moreover, let such that for all we have . In particular, it holds that for and hence, using the estimates in (38) and (A), we have for all

Since the last term is -integrable, the continuity assertion follows by dominated convergence and the fact that .

Bounded variation: To show that it is enough to show that the integral part of is absolutely convergent since . Using the monotonicity and the definition of , it is easy to see that for fixed ,

The continuity assertion follows in a straightforward manner from dominated convergence and the fact that .

Appendix B A lengthy computation

Proof of Lemma 7.1 The first part is a short calculation using the definition of , , , and that and . As for the second part, recall that, for ,

It is easy to see that

which, after a change of variables, gives

where and . Denote the first integral on the right-hand side and the second integral . After some algebra one sees that equals

Next, note that the last line in (B) can be rewritten as

where the equality follows from evaluating . Plugging this into (B) and simplifying yields

Rearranging the terms completes the proof.

Acknowledgements

I would like to thank A. E. Kyprianou and two anonymous referees for their valuable comments which led to improvements in this paper.

References

- (1) {barticle}[mr] \bauthor\bsnmAlili, \bfnmL.\binitsL. and \bauthor\bsnmKyprianou, \bfnmA. E.\binitsA. E. (\byear2005). \btitleSome remarks on first passage of Lévy processes, the American put and pasting principles. \bjournalAnn. Appl. Probab. \bvolume15 \bpages2062–2080. \biddoi=10.1214/105051605000000377, issn=1050-5164, mr=2152253 \bptokimsref \endbibitem

- (2) {barticle}[mr] \bauthor\bsnmAvram, \bfnmF.\binitsF., \bauthor\bsnmKyprianou, \bfnmA. E.\binitsA. E. and \bauthor\bsnmPistorius, \bfnmM. R.\binitsM. R. (\byear2004). \btitleExit problems for spectrally negative Lévy processes and applications to (Canadized) Russian options. \bjournalAnn. Appl. Probab. \bvolume14 \bpages215–238. \biddoi=10.1214/aoap/1075828052, issn=1050-5164, mr=2023021 \bptokimsref \endbibitem

- (3) {barticle}[mr] \bauthor\bsnmBaurdoux, \bfnmE. J.\binitsE. J. and \bauthor\bsnmKyprianou, \bfnmA. E.\binitsA. E. (\byear2009). \btitleThe Shepp–Shiryaev stochastic game driven by a spectrally negative Lévy process. \bjournalTheory Probab. Appl. \bvolume53 \bpages481–499. \bptokimsref \endbibitem

- (4) {bbook}[mr] \bauthor\bsnmBertoin, \bfnmJean\binitsJ. (\byear1996). \btitleLévy Processes. \bseriesCambridge Tracts in Mathematics \bvolume121. \bpublisherCambridge Univ. Press, \blocationCambridge. \bidmr=1406564 \bptokimsref \endbibitem

- (5) {bbook}[mr] \bauthor\bsnmBichteler, \bfnmKlaus\binitsK. (\byear2002). \btitleStochastic Integration with Jumps. \bseriesEncyclopedia of Mathematics and Its Applications \bvolume89. \bpublisherCambridge Univ. Press, \blocationCambridge. \biddoi=10.1017/CBO9780511549878, mr=1906715 \bptokimsref \endbibitem

- (6) {barticle}[auto:STB—2013/01/29—08:09:18] \bauthor\bsnmCarr, \bfnmP.\binitsP. and \bauthor\bsnmWu, \bfnmL.\binitsL. (\byear2003). \btitleThe finite moment log stable process and option pricing. \bjournalJ. Finance \bvolume58 \bpages753–778. \bptokimsref \endbibitem

- (7) {barticle}[mr] \bauthor\bsnmChan, \bfnmTerence\binitsT. (\byear1999). \btitlePricing contingent claims on stocks driven by Lévy processes. \bjournalAnn. Appl. Probab. \bvolume9 \bpages504–528. \biddoi=10.1214/aoap/1029962753, issn=1050-5164, mr=1687394 \bptokimsref \endbibitem

- (8) {bbook}[mr] \bauthor\bsnmGradshteyn, \bfnmI. S.\binitsI. S. and \bauthor\bsnmRyzhik, \bfnmI. M.\binitsI. M. (\byear2007). \btitleTable of Integrals, Series, and Products, \bedition7th ed. \bpublisherElsevier, \blocationAmsterdam. \bidmr=2360010 \bptokimsref \endbibitem

- (9) {bmisc}[auto:STB—2013/01/29—08:09:18] \bauthor\bsnmKuznetsov, \bfnmA.\binitsA., \bauthor\bsnmKyprianou, \bfnmA. E.\binitsA. E. and \bauthor\bsnmRivero, \bfnmV.\binitsV. (\byear2011). \bhowpublishedThe theory of scale functions for spectrally negative Lévy processes. Available at arXiv:\arxivurl1104.1280v1 [math.PR]. \bptokimsref \endbibitem

- (10) {bbook}[mr] \bauthor\bsnmKyprianou, \bfnmAndreas E.\binitsA. E. (\byear2006). \btitleIntroductory Lectures on Fluctuations of Lévy Processes with Applications. \bpublisherSpringer, \blocationBerlin. \bidmr=2250061 \bptokimsref \endbibitem

- (11) {bmisc}[auto:STB—2013/01/29—08:09:18] \bauthor\bsnmMadan, \bfnmD. B.\binitsD. B. and \bauthor\bsnmSchoutens, \bfnmW.\binitsW. (\byear2008). \bhowpublishedBreak on through to the single side. J. Credit Risk 4(3). \bptokimsref \endbibitem

- (12) {barticle}[auto:STB—2013/01/29—08:09:18] \bauthor\bsnmMerton, \bfnmR. C.\binitsR. C. (\byear1969). \btitleLifetime portfolio selection under uncertainty: The continuous-time case. \bjournalRev. Econ. Stat. \bvolume1 \bpages247–257. \bptokimsref \endbibitem

- (13) {barticle}[auto:STB—2013/01/29—08:09:18] \bauthor\bsnmMikalevich, \bfnmV. S.\binitsV. S. (\byear1958). \btitleBaysian choice between two hypotheses for the mean value of a normal process. \bjournalVisn. Kiiv. Univ. Ser. Fiz.-Mat. Nauki \bvolume1 \bpages101–104. \bptokimsref \endbibitem

- (14) {barticle}[mr] \bauthor\bsnmPeskir, \bfnmGoran\binitsG. (\byear1998). \btitleOptimal stopping of the maximum process: The maximality principle. \bjournalAnn. Probab. \bvolume26 \bpages1614–1640. \biddoi=10.1214/aop/1022855875, issn=0091-1798, mr=1675047 \bptokimsref \endbibitem

- (15) {bbook}[mr] \bauthor\bsnmPeskir, \bfnmGoran\binitsG. and \bauthor\bsnmShiryaev, \bfnmAlbert\binitsA. (\byear2006). \btitleOptimal Stopping and Free-Boundary Problems. \bpublisherBirkhäuser, \blocationBasel. \bidmr=2256030 \bptokimsref \endbibitem

- (16) {barticle}[mr] \bauthor\bsnmPeskir, \bfnmG.\binitsG. and \bauthor\bsnmShiryaev, \bfnmA. N.\binitsA. N. (\byear2000). \btitleSequential testing problems for Poisson processes. \bjournalAnn. Statist. \bvolume28 \bpages837–859. \biddoi=10.1214/aos/1015952000, issn=0090-5364, mr=1792789 \bptokimsref \endbibitem

- (17) {barticle}[mr] \bauthor\bsnmPistorius, \bfnmM. R.\binitsM. R. (\byear2004). \btitleOn exit and ergodicity of the spectrally one-sided Lévy process reflected at its infimum. \bjournalJ. Theoret. Probab. \bvolume17 \bpages183–220. \biddoi=10.1023/B:JOTP.0000020481.14371.37, issn=0894-9840, mr=2054585 \bptokimsref \endbibitem

- (18) {bmisc}[auto:STB—2013/01/29—08:09:18] \bauthor\bsnmPodlubny, \bfnmI.\binitsI. (\byear2012). \bhowpublishedMittag-Leffler function [Matlab code]. Available at http://www.mathworks.com/matlabcentral/fileexchange/8738. \bptokimsref \endbibitem

- (19) {bbook}[mr] \bauthor\bsnmProtter, \bfnmPhilip E.\binitsP. E. (\byear2005). \btitleStochastic Integration and Differential Equations, \bedition2nd ed. \bseriesStochastic Modelling and Applied Probability \bvolume21. \bpublisherSpringer, \blocationBerlin. \bidmr=2273672 \bptokimsref \endbibitem

- (20) {barticle}[mr] \bauthor\bsnmShepp, \bfnmLarry\binitsL. and \bauthor\bsnmShiryaev, \bfnmA. N.\binitsA. N. (\byear1993). \btitleThe Russian option: Reduced regret. \bjournalAnn. Appl. Probab. \bvolume3 \bpages631–640. \bidissn=1050-5164, mr=1233617 \bptokimsref \endbibitem

- (21) {barticle}[auto:STB—2013/01/29—08:09:18] \bauthor\bsnmShepp, \bfnmL. A.\binitsL. A. and \bauthor\bsnmShiryaev, \bfnmA. N.\binitsA. N. (\byear1993). \btitleA new look at pricing of the “Russian option.” \bjournalTheory Probab. Appl. \bvolume39 \bpages103–119. \bptokimsref \endbibitem

- (22) {bincollection}[mr] \bauthor\bsnmShepp, \bfnmL. A.\binitsL. A., \bauthor\bsnmShiryaev, \bfnmAlbert N.\binitsA. N. and \bauthor\bsnmSulem, \bfnmA.\binitsA. (\byear2002). \btitleA barrier version of the Russian option. In \bbooktitleAdvances in Finance and Stochastics \bpages271–284. \bpublisherSpringer, \blocationBerlin. \bptokimsref \endbibitem

- (23) {bbook}[mr] \bauthor\bsnmShiryaev, \bfnmAlbert N.\binitsA. N. (\byear1999). \btitleEssentials of Stochastic Finance: Facts, Models, Theory. \bseriesAdvanced Series on Statistical Science & Applied Probability \bvolume3. \bpublisherWorld Scientific, \blocationRiver Edge, NJ. \biddoi=10.1142/9789812385192, mr=1695318 \bptokimsref \endbibitem