BSDEs in Utility Maximization with BMO Market Price of Risk

Abstract

This article studies quadratic semimartingale BSDEs arising in power utility maximization when the market price of risk is of BMO type. In a Brownian setting we provide a necessary and sufficient condition for the existence of a solution but show that uniqueness fails to hold in the sense that there exists a continuum of distinct square-integrable solutions. This feature occurs since, contrary to the classical Itô representation theorem, a representation of random variables in terms of stochastic exponentials is not unique. We study in detail when the BSDE has a bounded solution and derive a new dynamic exponential moments condition which is shown to be the minimal sufficient condition in a general filtration. The main results are complemented by several interesting examples which illustrate their sharpness as well as important properties of the utility maximization BSDE.

keywords:

[class=MSC]keywords:

and t1C. Frei gratefully acknowledges financial support by the Natural Sciences and Engineering Research Council of Canada through grant 402585. t2Corresponding author: mocha@math.hu-berlin.de a We thank two anonymous referees for very helpful comments, which enabled us to improve the paper.

1 Introduction

In this article we study quadratic semimartingale BSDEs that arise in power utility maximization. More precisely, we consider the optimal investment problem over a finite time horizon for an agent whose goal is to maximize the expected utility of terminal wealth. Such a problem is classical in mathematical finance and dates back to Merton Me69 . For general utility functions (not necessarily power) the main solution technique is convex duality, see Karatzas and Shreve KS98 , Kramkov and Schachermayer KS99 as well as the survey article of Schachermayer S04 which gives an excellent overview of the ideas involved as well as many further references.

A second approach to tackling the above problem is via BSDEs, using the factorization property of the value process when the utility function is of power type. This allows one to apply the martingale optimality principle and, as shown in Hu, Imkeller and Müller HIM05 , to describe the value process and optimal trading strategy completely via a BSDE. Their article can be regarded as an extension of earlier work by Rouge and El Karoui REK00 as well as Sekine Se06 and relies on existence and uniqueness results for quadratic BSDEs first proved in Kobylanski K00 . Those existence results were subsequently extended by Morlais Mo09 , Briand and Hu BH06 ; BH08 , Delbaen, Hu and Richou DHR09 as well as Barrieu and El Karoui BEK11 . In particular, the assumption that the mean-variance tradeoff process be bounded has been weakened to it having certain exponential moments, see Mocha and Westray MW10 ; MW10a .

As previously stated, it is the BSDE approach to tackling the utility maximization problem which is studied in detail in the present paper. The key idea is to derive a BSDE whose solution provides a candidate optimal wealth process together with a candidate optimal strategy. Then a verification argument is applied, showing that these are in fact optimal, see Nutz Nu209 . This latter step is the difficult part and typically requires extra regularity of the BSDE solution which is guaranteed by the boundedness or existence of exponential moments of the mean-variance tradeoff. In particular, when one can show the existence of a bounded solution, verification is feasible. This is due to the fact that the martingale part of the corresponding BSDE is then known to be a BMO martingale. Motivated by the ease of verification given a bounded solution the main aim of this paper is to quantify, in terms of assumptions on the mean-variance tradeoff process, when one can expect a bounded solution. This natural question justifies the present study.

When the market is continuous (as assumed in this article) one can write the mean-variance tradeoff as for a continuous local martingale and predictable -integrable process . The assumption that the mean-variance tradeoff process be bounded or have all exponential moments implies that the minimal martingale measure is a true probability measure. In particular, the set of equivalent martingale measures is nonempty, so that there is no arbitrage in the sense of NFLVR, see Delbaen and Schachermayer DS98 . If the local martingale is instead assumed to be only a BMO martingale then from Kazamaki Ka94 the minimal martingale measure is again a true probability measure and NFLVR holds. In this case the mean-variance tradeoff now need not be bounded or have all exponential moments. A secondary objective of this paper is to study what happens to the solution of the BSDE in this situation. As discussed, such a condition on arises naturally from a no-arbitrage point of view, additionally however there is a known relation between boundedness of solutions to quadratic BSDEs and BMO martingales so that this question is also interesting from a mathematical standpoint.

The present article has three main contributions. Firstly in a Brownian setting, we show that the BSDE admits a continuum of distinct solutions with square-integrable martingale parts. This result provides square-integrable counterexamples to uniqueness of BSDE solutions. The spirit of our counterexamples is similar to that of Ankirchner, Imkeller and Popier AIP08 Section 2.2 except that we consider BSDEs related to the utility maximization problem. Our result stems from the fact that contrary to the classical Itô representation formula with square-integrable integrands, a “multiplicative” -analogue in terms of stochastic exponentials is not unique, see Lemma 3.4.

The second contribution is a thorough investigation of when the BSDE admits a bounded solution. If the investor’s relative risk aversion is greater than one and is a BMO martingale, this is automatically satisfied. For a risk aversion smaller than one the picture is rather different and we provide an example to show that even when the mean-variance tradeoff has all exponential moments and the process is a BMO martingale, the solution to the utility maximization BSDE need not be bounded. Building on this example our third and most important result is Theorem 6.5, which shows how to combine the BMO and exponential moment conditions so as to find the minimal condition which guarantees, in a general filtration, that the BSDE admits a bounded solution. We thus fully characterize the boundedness of solutions to the quadratic BSDE arising in power utility maximization. We mention that the limiting case of risk aversion equal to one, i.e. the case of logarithmic utility, is covered by our results.

The paper is organized as follows. In the next section we establish the link between the utility maximization problem and BSDEs for an unbounded mean-variance tradeoff. Then we analyze the questions of existence and uniqueness of BSDE solutions and in Section 4 turn our attention to the interplay between boundedness of solutions and the BMO property of . In Section 5 we develop some related counterexamples and then provide the characterization of boundedness in Section 6. In an additional appendix we collect some background material on quadratic continuous semimartingale BSDEs.

2 Power Utility Maximization and Quadratic BSDEs

Throughout this article we work on a filtered probability space satisfying the usual conditions of right-continuity and completeness. We assume that the time horizon is a finite number in and that is the completion of the trivial -algebra. In addition all semimartingales are assumed to be equal to their càdlàg modification. In a first step, we assume that the filtration is continuous in the sense that all local martingales are continuous. This condition is relaxed in Section 6 where we provide the main characterization result for a general filtration.

There is a market consisting of one bond, assumed constant, and stocks with price process , which we assume to have dynamics

where is a -dimensional continuous local martingale with , is a -dimensional predictable process, the market price of risk, satisfying

and denotes the diagonal matrix whose elements are taken from .

We consider an investor trading in the above market according to an admissible investment strategy . A predictable -dimensional process is called admissible if it is -integrable, i.e. a.s. and we write for the family of such investment strategies . Observe that each component represents the proportion of wealth invested in the th stock , . In particular, for some initial capital and an admissible strategy , the associated wealth process evolves as follows,

where denotes the stochastic exponential. The family of all such wealth processes is denoted by .

Our investor has preferences modelled by a power utility function ,

Starting with initial capital , they aim to maximize the expected utility of terminal wealth. This leads to the following primal optimization problem,

| (2.1) |

Related to the above primal problem is a dual problem which we now describe. For we introduce the set

as well as the minimization problem

where is the conjugate (or dual) of given by , , where is the dual exponent to . There is a bijection between and so that in what follows we often state the results for rather than for .

It is shown in Kramkov and Schachermayer KS99 ; KS03 (among others) that for general utility functions (not necessarily power) the following assumption is the weakest possible for well posedness of the market model and the utility maximization problem.

Assumption 2.1.

-

(i)

The set of equivalent local martingale measures for is non-empty.

-

(ii)

If , there is an such that

Summarizing the results of KS99 we then have that there exists a strategy , independent of , which is optimal for the primal problem. In particular, for any other optimal strategy and we have that and are indistinguishable. On the dual side, given , there exists a which is optimal for the dual problem and unique up to indistinguishability. Finally, the functions and are continuously differentiable and conjugate and if then and the process is a martingale on , where we omit writing the dependence on the initial values.

Remark 2.2.

We also state here a representation of the dual optimizer shown in LZ07 when is one-dimensional and extended in MW10a to the current framework. Using the continuity of the filtration, there exists a continuous local martingale which is orthogonal to , i.e. for all , and such that .

Finally, we recall the BSDE satisfied by the so-called opportunity process from Nu109 , more precisely by its log-transform. We start with the solutions and to the above primal and dual problem (when ) and derive the BSDE satisfied by the following process

The logic is now very similar to the procedure in MS05 , we apriori obtained the existence of the object of interest. Imposing a suitable assumption we show that lies in a certain space in which solutions to (a special type of) quadratic semimartingale BSDE are unique. This approach of using BSDE comparison principles in utility maximization may be found in HIM05 and Mo09 . We observe that in these references the mean-variance tradeoff is bounded. In what follows we extend their reasoning to the unbounded case under exponential moments which was thoroughly investigated in MW10a where the corresponding assumption is

Assumption 2.3.

For all we have that

i.e., the mean-variance tradeoff has exponential moments of all orders.

The preceding assumption is compatible with Assumption 2.1 in the following sense.

Lemma 2.4 (MW10a Proposition 2.8).

For completeness let us also include the case , equivalently , which corresponds to the case of logarithmic utility, i.e. and , and for which the optimizers

have a simple structure. Namely, is the optimal strategy and is the dual optimizer. We also have so that . We mention that the Assumption 2.1 with item (ii) extended to is a sufficient condition for existence and uniqueness of the optimizers. In particular, Assumption 2.3 or the condition that be a BMO martingale, see below, are sufficient as can be deduced easily.

Before we discuss properties of the process we first fix some notation.

Definition 2.5.

Let denote the space of all processes on whose supremum has exponential moments of all orders, i.e. for all ,

We then recall from MW10a that if Assumption 2.3 holds and if is the solution to the primal and dual optimization problem, then . With regards to the derivation of the BSDE satisfied by , we note that, using the formulae for and ,

After the change of variables

a calculation shows that we have found a solution to the following quadratic semimartingale BSDE (written in the generic variables ),

| (2.2) |

where we refer to Definition A.1 for the notion of a solution to the BSDE (2.2). We summarize our findings in the following theorem, noting that it is uniqueness which requires the stronger Assumption 2.3, existence is guaranteed via Assumption 2.1.

Theorem 2.6.

Let Assumption 2.3 hold and be the solution pair to the primal/dual optimization problem i.e. for

Setting

then

-

(i)

The triple is the unique solution to the BSDE (2.2) where and and are two square-integrable martingales.

-

(ii)

In terms of the BSDE we may write as

with , a.s.

-

(iii)

The process is a martingale on .

Proof.

The content of item (i) follows from Theorem A.3 in the Appendix which summarizes the main results on quadratic semimartingale BSDEs under an exponential moments condition. A calculation yields the alternative formula for in item (ii) and the relation

gives the remaining assertion in item (iii). ∎

The statement of the above theorem is essentially known. In HIM05 and Mo09 the boundedness of the mean-variance tradeoff is used to ensure uniqueness, in MW10a this argument is extended to the unbounded case with exponential moments. Building on MT03 ; MT08 , the article Nu209 shows that in a general setting the opportunity process satisfies a BSDE which reduces to (2.2) under the additional assumption of continuity of the filtration. In particular, is identified there as the minimal solution to the corresponding BSDE.

Having identified candidate optimizers from the BSDE, a difficult task is then verification, i.e. showing that a solution to the BSDE indeed provides the primal and dual optimizers. A sufficient condition is that is a martingale as can be derived from Nu209 , see also Proposition 3.1 below. However, given a solution to the BSDE (2.2), this condition need not be satisfied, hence a solution to the BSDE (2.2) need not yield the optimizers even when and are square-integrable, as demonstrated in Subsection 3.2. In conclusion, if a solution triple exists, then under some conditions it provides the solution to the primal and dual problem and we have uniqueness to the BSDE within a certain class. This is in the spirit of MT08 Theorem 1.3.2 and Nu209 Theorem 5.2. However, above and in their theorems, the requirements imposed are not on the model. In contrast, our goal is to study which conditions on the model, i.e. on and , ensure such a BSDE characterization and the regularity of its solution in terms of a bounded dynamic value process.

3 Existence, Uniqueness and Optimality for Quadratic BSDEs

From Theorem 2.6 we see that under Assumption 2.3 one can connect the duality and BSDE approaches to solving the utility maximization problem. To analyze this connection in further detail, we consider in the present section a setting where the BSDE (2.2) is explicitly solvable. Proposition 3.1 gives a sufficient condition for a solution to the BSDE (2.2) to exist and provides an expression for in terms of .

We go on to study uniqueness and show in Theorem 3.6 that in general there are many solutions with square-integrable martingale part. This is a consequence of the fact that a multiplicative representation of random variables as stochastic exponentials need not be unique, which is the content of Lemma 3.4. Finally, a main aim in the present article is to study the boundedness of solutions to the BSDE (2.2) under the exponential moment and BMO conditions. This involves constructing counterexamples and some of the key techniques and ideas used for this are introduced in the current section. Therefore we restrict ourselves to the Brownian setting, which we assume to be one-dimensional for notational simplicity. Let be a one-dimensional Brownian motion under and its augmented natural filtration. In particular, is the unique local martingale orthogonal to . A generalization of the following results to the multidimensional Brownian framework is left to the reader.

3.1 Necessary Conditions for the Existence of Solutions to Quadratic BSDEs

Proposition 3.1.

For the BSDE (2.2) always admits a solution. For the BSDE (2.2) admits a solution if and only if

| (3.1) |

If there exists a solution, there is a unique solution with a martingale. Its first component is given by

| (3.2) |

In particular, solving (2.2) and setting as suggested by Theorem 2.6 gives the pair of primal and dual optimizers.

As a result, condition (3.1) is sufficient for existence and uniqueness of the optimizers and we mention that it corresponds to condition (10) in KS99 . Hence, the utility maximization problem is well-defined even if NFLVR (no free lunch with vanishing risk) does not hold. This is because FLVR strategies cannot be used beneficially by the CRRA-investor due to the requirement of having a positive wealth at any time.

Proof.

Let us first show that the BSDE (2.2) admits a solution if (3.1) holds. Observe that from Jensen’s inequality, for ,

so that (3.1) automatically holds in this case. For consider

| (3.3) |

Since we have

is a positive martingale so that by Itô’s representation theorem there exists a predictable process with a.s. such that . We set

and as in (3.2). A calculation then shows that solves the BSDE (2.2) with a martingale.

We now turn our attention to uniqueness. Let us assume that is a solution to (2.2) such that is a martingale. For a calculation gives

| (3.4) | ||||

so that we obtain

We derive that and are indistinguishable due to continuity. From (3.4) we then obtain that is uniquely determined, from which it follows that .

We now provide an explicit market price of risk for which condition (3.1) fails to hold, hence for which the BSDE (2.2) has no solution. While similar examples have been provided in Delbaen and Tang DT10 Theorem 2.8 as well as Frei and dos Reis FdR10 Lemma A.1, we give the full construction as it will be used throughout.

Proposition 3.2.

For every there exists such that is a bounded martingale and

Proof.

For define

where is the stopping time

Here, we define from time onwards to be consistent with the construction in Subsection 5.3. For the present proof, we could equally well replace by in the definitions of and . Observe that we have that due to continuity and the relation

By construction, is bounded by . We obtain, using Ka94 Lemma 1.3 similarly to the proof of FdR10 Lemma A.1,

from which the statement follows immediately. ∎

Let us make two points concerning the above example, firstly that when such a degeneracy cannot occur, as shown by Proposition 3.1. In fact for a BMO martingale there actually always exists a (then unique) bounded solution, as Corollary 4.2 below shows. We recall from Ka94 that a continuous martingale on the compact interval with is a BMO martingale if

where the supremum is over all stopping times valued in .

Secondly we point out that the martingale in the above proposition is bounded. Indeed, it is a leitmotiv of the present article that requiring (in addition) the martingale to be bounded does not improve the situation with respect to finiteness of a BSDE solution. This is because the key estimates are all on the quadratic variation process which in general does not inherit such properties.

Remark 3.3.

As described in the introduction, the assumption that is a BMO martingale is natural from a no-arbitrage perspective. We now give an additional financial interpretation of the BMO condition. Suppose for simplicity that is a geometric Brownian motion of the form

so that and . The Sharpe ratio, defined as , measures the return per unit of risk. A BMO condition on requires that the conditional expected integral of the squared Sharpe ratio be bounded, which implies a restriction on the asset not offering huge returns with tiny risk.

Developing this idea further, consider an investment strategy which in this remark represents the amount, not, as elsewhere, the proportion, of wealth invested in . We assume that and that is predictable and satisfies . From the stock dynamics

it follows that the expected gain (or loss) related to is given by

Using Pr05 Theorem IV.54, we deduce that is a BMO martingale if and only if there exists a constant such that

| (3.5) |

for all with . Using

we can view as a measure of risk in our portfolio. We see from (3.5) that the assumption of being a BMO martingale means that portfolios with bounded risk (in this -sense) always have bounded expected gains. Conversely, if the expected gains are bounded in terms of such risk uniformly over all investment strategies, then needs to be a BMO martingale.

3.2 Nonoptimality of BSDE Solutions

If a solution to the BSDE (2.2) does exist, it does not automatically lead to an optimal pair for the utility maximization problem. This is because it may fail to be in the right space (e.g. with respect to which uniqueness for BSDE solutions holds). We now provide a theoretical result to illustrate the problem. More precisely, in contrast to the classical Itô representation theorem with square-integrable integrands, an analogous representation of random variables in terms of stochastic exponentials is not unique.

Lemma 3.4.

Let be a random variable bounded away from zero and infinity, i.e. there are constants such that a.s. Then, for every real number , there exists a predictable process such that

| (3.6) |

However, there is only one pair which satisfies with a BMO martingale or, equivalently, with .

Remark 3.5.

Comparing the multiplicative representation (3.6) with the classical one, see KS91 Theorem 4.15, namely

we see that existence holds in both cases, whereas there is no uniqueness of in (3.6) despite the fact that , in contrast to the uniqueness of .

While in the standard Itô representation for -random variables the square-integrability and martingale property are equivalent, our result shows that in the multiplicative form does not guarantee uniqueness. The intuition for the difference between in the additive and in the multiplicative form is the following. Since is a square-integrable process, is a martingale, hence it must be the case that . In contrast, the square-integrability of is not sufficient for to be a martingale. Indeed, it can be that so that increasing may be offset by an appropriate choice of such that (3.6) still holds. A consequence of this is that uniqueness of holds if is a BMO martingale or equivalently (see Ka94 Theorem 3.4, using the boundedness of ) if is a martingale.

One could argue that a more natural condition in (3.6) is to assume that be a true martingale, however our aim is a characterization in terms of itself and thus we do not pursue this. Note that it is not possible to find such that (3.6) holds, because is always a positive local martingale, hence a supermartingale.

Proof.

We first define , , and apply Itô’s representation theorem to the stochastic logarithm of , which is a BMO martingale by Ka94 Theorem 3.4 since is bounded away from zero and infinity. This application yields a predictable process such that is a BMO martingale and . The uniqueness part of the statement is then immediate; if is a BMO martingale, we have and since is a martingale. Conversely, if the process is a supermartingale with constant expectation, hence a martingale. Indeed, we then have

and thus , which is the BMO martingale from above.

To construct we fix and define the stopping time

We argue that a.s. To this end consider

and observe that . If we define the time change by , then it follows from RY99 II.3.14. that

| (3.7) |

We deduce that , a.s. and a.s. from which it follows that indeed a.s.

We now define

which satisfies

where the second equality is due to the specific definition of the stopping time . Moreover, we have

which is finite because and is a BMO martingale. ∎

The standard method of finding solutions to quadratic BSDEs involves an exponential change of variables. A consequence of the preceding lemma is that the above type of nonuniqueness transfers to the corresponding BSDE solutions, in particular to those of the utility maximization problem. Observe that for each the process is square-integrable in contrast to classical locally integrable counterexamples. Indeed it is well known that without square-integrability even the standard Itô decomposition is not unique. In fact, for every there exists such that

see ESY83 Proposition 1. We are hence able to construct distinct solutions to the BSDE (2.2). This amounts to some of those solutions being nonoptimal by Proposition 3.1. Alternatively, uniqueness of the multiplicative decomposition holds under an additional BMO assumption which then implies the uniqueness of . We summarize these comments in the following theorem.

Theorem 3.6.

For all and with bounded, there exists a continuum of distinct solutions to the BSDE (2.2), parameterized by , satisfying the following properties:

-

(i)

The martingale part is square-integrable for all .

-

(ii)

The process is a martingale if and only if .

-

(iii)

Defining as suggested by the formula in Theorem 2.6, the admissible process is the optimal strategy if and only if .

It is known from AIP08 Section 2.2 that quadratic BSDEs need not have unique square-integrable solutions. These authors present a specific example of a quadratic BSDE which allows for distinct solutions with square-integrable martingale part. In contrast, Theorem 3.6 shows that every BSDE related to power utility maximization with bounded mean-variance tradeoff has no unique square-integrable solution, independently of the value of . This underlines the importance of being able to find a solution to the BSDE (2.2) with a BMO martingale in HIM05 and Mo09 .

Proof.

We set and define the measure change

so that is an equivalent probability measure under which is a Brownian motion on where

Observe that this measure change is implicitly already present in the proof of Proposition 3.1, see (3.3). We now apply Lemma 3.4 to the triple noting that in its proof we may use Itô’s representation theorem in the form of KS98 Theorem 1.6.7, i.e. we can write any -martingale as a stochastic integral with respect to , although may not generate the whole filtration . For every real number we then derive the existence of a predictable process such that

For we then set

so that solves the BSDE

Using the transformations , and we arrive at the BSDE (2.2),

which admits a continuum of distinct solutions, parameterized by . We show that each martingale part is additionally square-integrable under . This follows from the inequality

Note that the second term on the right hand side is finite since from (3.7) in the proof of Lemma 3.4 we have that . Moreover, using from this proof, is a BMO martingale (under ), hence has an exponential -moment of some order by Ka94 Theorem 2.2, see also Lemma 6.1 and the comments thereafter. To derive that the first term is finite we use that

Clearly, the Assumption 2.3 is satisfied, hence our previous analysis applies. However, there is a continuum of distinct solutions to the BSDE (2.2) since for every we have that . From Ka94 Theorem 3.6 we have that is a BMO martingale under if and only if is a BMO martingale under . This last condition holds if and only if is a BMO martingale under . We conclude that is a martingale if . It cannot be a martingale for since otherwise would coincide with . The last assertion is then immediate. ∎

4 Boundedness of BSDE Solutions and the BMO Property

Thus far we have worked under an exponential moments assumption on the mean-variance tradeoff which provides us with the existence of the primal and dual optimizers as well as a link between these optimizers and a special quadratic BSDE. We now connect the above study to the boundedness of solutions to quadratic BSDEs which we show to be intimately related to the BMO property of the martingale part and the mean-variance tradeoff.

For and under the assumption that is a BMO martingale, we show that the BSDE (2.2) has a bounded solution. This follows as a consequence of existence results and a priori estimates for a general class of BSDEs as described below. We consider the BSDE

| (4.1) |

where, as in the appendix, is a nondecreasing bounded process such that for a predictable process valued in the space of matrices. We assume that is a bounded random variable and that the driver is continuous in and satisfies

| (4.2) | |||

are constants, is a deterministic continuous nondecreasing function with , and , are processes such that , are BMO martingales. If , we additionally assume that there exists a constant such that for all , and we set . For the notion of solution to (4.1), see Appendix A.

Theorem 4.1.

Proof.

(i) Using the assumption , we can argue similarly to the proof of DHR09 Theorem 2.1. That proof is given in a Brownian setting but translates correspondingly to our semimartingale model similarly to MW10 . With and based on (4.2), this yields the existence of a solution satisfying

Since and is a BMO martingale, the latter inequality shows that is bounded from below. From the former inequality, we obtain

by the John-Nirenberg inequality; see Lemma 6.1. This shows that is bounded from above due to the assumptions and . Hence, is bounded, which concludes the proof of (i).

For (ii), let first be a solution to (4.1) with bounded . The BMO properties of and follow from MS05 Proposition 7, using that (4.2) with implies

Conversely, if and are BMO martingales, then is bounded. This follows by taking the conditional -expectation in the integrated version of (4.1) and estimating the remaining finite variation parts with the help of the norms of , , and , uniformly in .

Finally, the statement (iii) is an immediate consequence of the items (i) and (ii). ∎

Let us now apply this result to the specific BSDE (2.2) related to power utility maximization.

Corollary 4.2.

Proof.

By Appendix A, the BSDE (2.2) is of the form (4.1) with the driver given by

Using , we can show by an elementary calculation that

so that (4.2) is satisfied. Thus we can apply Theorem 4.1 (iii) to obtain that there exists a solution triple such that the process is a BMO martingale. We derive that is a BMO martingale which, by Ka94 Theorem 2.3, shows that is a true martingale. We then deduce that solving the BSDE with a bounded gives rise to an optimal pair for the primal and dual problem. ∎

Remark 4.3.

Instead of applying Theorem 4.1, which holds for a more general class of BSDEs, Corollary 4.2 can also be shown as follows using specific results related to power utility maximization. Since is a BMO martingale, defines an equivalent local martingale measure for so that Assumption 2.1 is satisfied, where we use an easy calculation to extend its item (ii) to . By Ka94 Corollary 3.4, if , the process satisfies the reverse Hölder inequality. This means that there is constant (which depends on ) such that for all stopping times valued in ,

The assertion of Corollary 4.2 then follows from Nu109 Proposition 4.5 and from the explicit formula that holds in the case .

Proposition 3.1 shows that in a Brownian framework the BSDE (2.2) always admits a solution if . In view of Corollary 4.2 this property extends to the general framework under the condition that is a BMO martingale. In particular, there is a unique bounded solution and it is given by the opportunity process for the utility maximization problem.

Let us now contrast this with the situation when . The example in Subsection 3.1 provides a bounded BMO martingale such that the corresponding BSDE admits no solution. For this example the utility maximization problem satisfies and is thus degenerate ().

The question now becomes whether, given an arbitrary such that is a BMO martingale and , we can still guarantee a bounded solution to the BSDE (2.2) when the utility maximization problem is nondegenerate. We settle this question negatively in the next section providing an example for which Assumption 2.3 as well as the BMO property of hold, but the BSDE (2.2) does not have a bounded solution.

To counterbalance this negative result in Section 6 we provide, via the John-Nirenberg inequality, a condition on the order of the dynamic exponential moments of the mean-variance tradeoff that guarantees boundedness of . This is accompanied by a further example showing that this condition cannot be improved. To conclude, Corollary 4.2 and Theorem 6.5 provide a full characterization of the boundedness of solutions to the BSDE (2.2) in terms of the dynamic exponential moments of for a BMO martingale .

5 Counterexamples to the Boundedness of BSDE Solutions

We know that an optimal pair for the utility maximization problem gives rise to a triple solving the BSDE (2.2). Conversely, under suitable conditions, BSDE theory, based on BH08 , K00 or the results stated in the appendix, provides solutions to the BSDE with bounded (in ), with uniqueness in the class of bounded processes (in ). We now present an example of a BMO martingale which satisfies Assumption 2.3 and for which the BSDE (2.2) related to the utility maximization problem has an unbounded solution for a given .

We develop this example in three steps. Firstly, we show that Assumption 2.3 alone (rather unsurprisingly) is not sufficient to guarantee a bounded BSDE solution. The corresponding involved is however not a BMO martingale. The second example is of BMO type, but lacks finite exponential moments of a sufficiently high order. It resembles the example provided in Subsection 3.1. Finally, we combine these two examples to construct a BMO martingale such that has all exponential moments, but for which the BSDE does not allow for a bounded solution. Although this last step leaves the first two obsolete, we believe that the outlined presentation helps the reader in gaining insight into the nature of the degeneracy. In addition it hints at the minimal sufficient condition in Theorem 6.5 below. Namely, instead of simply requiring both the BMO and the exponential moments properties, they should be combined into a dynamic condition. While there is no reason to have a bounded solution if one requires only the BMO and the exponential moments properties, e.g. see the a priori estimate for general BSDEs in MW10 Proposition 3.1, constructing counterexamples appears to be nontrivial and similar ideas will be used to show sharpness of the dynamic condition in Section 6. Since in the present section we construct suitable counterexamples, let be again a one-dimensional -Brownian motion in its augmented natural filtration.

5.1 Unbounded Solutions under All Exponential Moments

Let us assume the market price of risk is given by so that the stock price dynamics read as follows,

Note that in the above definition “” is motivated by economic rationale, to simulate a certain reverting behaviour of the returns. Assumption 2.3 is satisfied since

and by Doob’s inequality, for ,

Now let so that and let be the optimizers of the utility maximization problem, where and . Since we are in a complete Brownian framework we have that . If denotes the optimal investment strategy we derive from Theorem 2.6 that is the unique solution to the BSDE (2.2) where and . According to Nu109 Proposition 4.5 is bounded if and only if satisfies the reverse Hölder inequality

| (5.1) |

for some positive constant and all stopping times valued in , which we show is not the case.

The family is uniformly integrable since , so we may apply the stochastic Fubini theorem (Be06 Lemma A.1) to get, for some , via Jensen’s inequality,

Since the last random variable is unbounded it cannot be the case that (5.1) holds, hence cannot be bounded.

However, from this example is not a BMO martingale since for ,

which shows that cannot be finite.

5.2 Unbounded Solutions under the BMO Property

We continue with a BMO example for which the solution to the BSDE (2.2) is unbounded. The idea is the following, from Proposition 3.2, for , there exists with a BMO martingale such that the BSDE (2.2) has no solution (in any class of possible solutions). Replacing this by for a constant , it follows from (6.9) below that the BSDE has either no solution (for ) or has a solution which is bounded and fulfills a BMO property (for ). This dichotomy is in line with the fact that for a BMO martingale the set of all such that satisfies the reverse Hölder inequality is open; compare Lemma 6.3 below. The insight then is to make a random variable in order to construct such that the BSDE (2.2) has a solution which is not bounded. More precisely, we have the following result.

Proposition 5.1.

For every there exists a with a BMO martingale such that,

- (i)

-

(ii)

There does not exist a solution to (2.2) with a BMO martingale or bounded.

Proof.

For we set

where

for the standard normal cumulative distribution function and the stopping time from the proof of Proposition 3.2,

| (5.2) |

Note that is uniformly distributed on and that is valued in a.s. It follows immediately that is bounded by , in particular it is a BMO martingale.

Using Ka94 Lemma 1.3 in the same way as in the proof of FdR10 Lemma A.1, we obtain that

so that Proposition 3.1 gives the first assertion. Due to the -measurability of and the -independence of , we have

This shows that

which is unbounded by the uniform distribution of .

For item (ii) assume that there exists a solution to (2.2) with a BMO martingale or bounded. By Theorem 4.1(ii) we can restrict ourselves to assuming that is bounded, which implies that is a BMO martingale so that is a martingale. By uniqueness, coincides with in contradiction to the unboundedness of . ∎

5.3 Unbounded Solutions under All Exponential Moments and the BMO Property

The two previous subsections raise the question whether we can find a BMO martingale such that its quadratic variation has all exponential moments and the BSDE (2.2) has only an unbounded solution. Roughly speaking, the idea is to combine the above two examples by translating the crucial distributional properties of and into the corresponding properties of a suitable stopping time . This guarantees that the BMO property and the exponential moments condition are satisfied simultaneously, while we can also achieve the unboundedness of the BSDE solution by using independence. Table 1 summarizes the key properties.

| Form of | Crucial properties | |

|---|---|---|

| First example (see 5.1) | is unbounded, | |

| has all exponential moments | ||

| Second example (see 5.2) | , , | |

| Combination | , , | |

| has all exponential moments |

Theorem 5.2.

For every , there exists a such that,

-

(i)

The process is a BMO martingale.

-

(ii)

For all we have .

- (iii)

-

(iv)

There does not exist a solution to (2.2) with a BMO martingale or bounded.

Proof.

Let us first construct with the desired distributional properties. We define the nonnegative continuous function , , where is a constant such that We then consider the strictly increasing function , and its inverse . We set

so that is an -measurable random variable with values in and cumulative distribution function . Now define for ,

where is the stopping time from (5.2). It follows immediately that is bounded by , hence a BMO martingale.

Let us now show that has all exponential moments. Take and an integer. We derive

where in the last equality we used the representation of the incomplete gamma function at integer points (or, directly, integration by parts). A standard argument then shows that see the proof of Theorem 6.5(i) below. It follows from the Proposition 3.1 that there exists a unique solution to the BSDE (2.2) such that is a martingale and the first component is given by

We deduce that a.s.

because is -measurable and is independent from . From monotone convergence, it follows that

| (5.3) |

We now fix and take such that

which is possible by (5.3). This implies since , in particular is unbounded. The last item then follows as in the previous proof. ∎

Remark 5.3.

It is interesting to compare, for different constants , the above different definitions of regarding the behaviour of the solution to the BSDE

| (5.4) |

In the example of Proposition 3.2 is of the form , while in Subsection 5.2 equals , which we modified to in the above discussion. Table 2 shows that by introducing additional random variables in the construction of , the BSDE (5.4) becomes solvable for bigger values of , but the solution for is unbounded. The assertions of Table 2 can be deduced from the arguments in the above proofs together with the additional calculation given in (6.11) below.

Remark 5.4.

In the Subsections 3.1, 5.2 and above we constructed several counterexamples to the boundedness of BSDE solutions. Such examples can also be given in Markovian form using Azéma-Yor martingales. More precisely, for let

and as in (5.2), noting that . If () denotes the running minimum (maximum) of , then

are continuous local martingales on by Azéma and Yor AY79 . To close the continuity gap at consider and set . A calculation then shows that

for

For the analogue of Proposition 3.2 we could now take the three-dimensional from above, but actually the one-dimensional local martingale turns out to be sufficient. We obtain that for every there exists a predictable process which is a function of such that is a bounded martingale satisfying Indeed, gives the claim. For the analogues of Proposition 5.1 and Theorem 5.2 we set and , where

which again prove to be Markovian in and for which the statements of the cited results remain valid.

6 Characterization of Boundedness of BSDE Solutions

We have already shown that for a BMO martingale and the BSDE (2.2) allows for a unique bounded solution. In the previous section we gave some examples to show that for the situation is different. In this section we complete the analysis by developing a sufficient condition that guarantees (necessarily unique) bounded solutions to (2.2). It is also shown that this particular condition cannot be improved. More precisely, we consider here a more general situation where is not necessarily a continuous filtration, but only a filtration satisfying the usual conditions. We assume that the local martingale is still continuous. In this case the BSDE (2.2) is replaced by

| (6.1) |

We mention that all the results which depend only on the specific continuous local martingale also hold in this more general setting. In particular, the statements of Nu109 Proposition 4.5 and our Corollary 4.2 continue to hold for the BSDE (6.1) in place of the BSDE (2.2).

6.1 The critical exponent of a BMO martingale

We will see that the boundedness of BSDE solutions depends crucially on the so-called critical exponent of the market price of risk. After defining the critical exponent of a general BMO martingale, we give some properties which will be exploited later. We then explain for a general BSDE how the critical exponent is related to boundedness. In addition to the counterexamples in Section 5, this gives a motivation for our main result, Theorem 6.5, about how to characterize bounded solutions.

We recall the John-Nirenberg inequality for the convenience of the reader. In what follows is an arbitrary continuous martingale on with .

Lemma 6.1 (Kazamaki Ka94 Theorem 2.2).

If then for every stopping time valued in

| (6.2) |

Using the definition of Ka94 and the terminology of Schachermayer Sch96 , we define the critical exponent via

| (6.3) |

where the supremum inside the brackets is over all stopping times valued in . We refer to this inner supremum as a dynamic exponential moment of of order . A consequence of Lemma 6.1 is then that a martingale is a BMO martingale if and only if . In addition, the following lemma shows that the supremum in (6.3) is never attained.

Lemma 6.2.

Let and be a continuous martingale with

| (6.4) |

Then there exists such that

and hence .

Proof.

Inspired by Ka94 Corollary 3.2 we aim to apply Gehring’s inequality. To this end, fix a stopping time and set for . For each , we then define the stopping time . It follows from and the continuity of that

| (6.5) |

Since is nondecreasing, we have that and this event is -measurable. Therefore, we obtain

where we used (6.4) and denoted its left-hand side by . Fix now . Using (6.5), we derive

and conclude that

It follows from the probabilistic version of Gehring’s inequality given in Ka94 Theorem 3.5, however see Remark 6.4 below, that there exist and (depending on and only) such that

To obtain the conditional version, we take and derive from the same argument and Jensen’s inequality that

so that

Since this holds for any stopping time , we conclude the proof by setting . ∎

We present another auxiliary result that will be applied in the next subsection.

Lemma 6.3.

Proof.

Remark 6.4.

We mention that in the formulation of Ka94 Theorem 3.5 as well as the proof of Ka94 Corollary 3.2 there is a small gap which can be easily filled. Namely, for a nonnegative random variable and positive constants , and the author requires Gehring’s condition

| (6.6) |

to hold for all , which cannot be satisfied for unless a.s. This is because for an integrable the right-hand side tends to zero as whereas the left-hand side tends to . However, an inspection of the proof reveals that (6.6) is needed only for , i.e. Ka94 Theorem 3.5 should be stated for instead of . If this is the case it then can be applied in the proof of Ka94 Corollary 3.2, where for the following stopping time is considered, for a continuous local martingale , see also the proof of Lemma 6.2. Then, the desired estimate is derived, but the latter holds for only, since for we obtain that which in turn gives .

To illustrate how dynamic exponential moments lead to boundedness and help motivate our next theorem, consider the following BSDE in a continuous filtration

| (6.7) |

where is a bounded random variable. We assume that the driver is continuous and satisfies

for all and , where are constants and is a BMO martingale such that for .

From MW10 Theorem 4.1 (noting that convexity of in is not needed by MW10 Remark 4.3), we obtain that there exists a solution to (6.7) which satisfies

We see immediately that if , then is bounded. Applying this to the specific BSDE (2.2) related to power utility maximization for and using Lemma A.2 (ii) in the appendix, we obtain that the solution to (2.2) has a bounded first component if or, equivalently,

Choosing the minimizing , the right hand side equals

| (6.8) |

so that implies existence of a solution with bounded first component.

Contrary to this result, the specific example of a BMO martingale that does not yield a bounded solution to the BSDE in Subsection 5.2 exhibits

recalling that (and where the first equality can be shown using (6.11) below). The following questions arise.

-

•

Which boundedness properties do hold for solutions to the BSDE (6.1) for those with ?

-

•

Can we use the critical exponent to characterize boundedness of solutions to the BSDE (6.1)?

We answer these questions in the next subsection by showing that the bound is indeed the minimal one which guarantees boundedness, hence cannot be improved. In doing so we provide a full description of the boundedness of solutions to the quadratic BSDE (6.1) with a BMO martingale in terms of the critical exponent in a general filtration.

6.2 Boundedness under Dynamic Exponential Moments

We have seen that neither the BMO property of nor an exponential moments condition guarantees the boundedness of a BSDE solution. While a counterexample showed that a simple combination of the two conditions does not suffice, we next see that a dynamic combination provides the required characterization. In particular, while the existence of all exponential moments of the mean-variance tradeoff is sufficient for the existence of a unique solution to (2.2) with , the existence of all dynamic exponential moments is sufficient for the existence of a unique solution with bounded, and in general this requirement cannot be dropped. We recall that by Lemma 6.2 any requirement on the dynamic exponential moments may be cast in terms of a condition on the critical exponent .

Theorem 6.5.

Fix , i.e. , and define as in (6.8). Then,

- (i)

-

(ii)

For a one-dimensional Brownian motion and every , there exists a BMO martingale with such that the solutions to the primal and dual problem exist and the corresponding triple is a solution to the BSDE (6.1) with unbounded.

-

(iii)

For a one-dimensional Brownian motion , there exists a BMO martingale with such that the solutions to the primal and dual problem exist and the corresponding triple is the unique solution to the BSDE (6.1) with bounded.

We can summarize this result as follows: Item (i) gives a sufficient condition for boundedness of BSDE solutions in terms of dynamic exponential moments, which is less restrictive than a bound on the BMO2 norm. Item (ii) shows that this condition is sharp in the sense that it cannot be improved. In particular, the critical exponent from (6.3) characterizes the boundedness property of solutions to the BSDE (6.1) that stem from the utility maximization problem. Item (iii) gives information about the critical point in the interval It yields that the converse of item (i) does not hold.

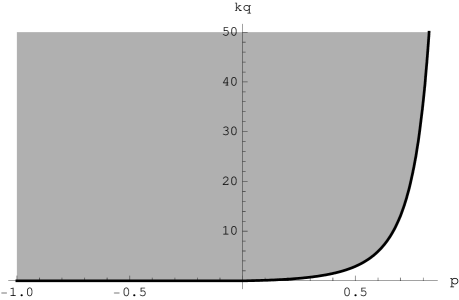

The following Figure 1 provides a visualization of this discussion, it depicts the value as a function of . Let us now discuss it briefly, fix and assume that we are on the critical black line, i.e. we have a specific with . Note that the black line is included in the area that ensures boundedness because a finite dynamic exponential moment of order is equivalent to by Lemma 6.2. Now choosing such that we can derive the statement of Theorem 6.5 (i) for the corresponding . However, depends on the specific choice of and therefore, it is not possible to shift the whole black line uniformly for all processes .

Items (ii) and (iii) of the above theorem rely on the construction of a specific example which we provide in the following auxiliary lemma.

Lemma 6.6.

Let be a one-dimensional Brownian motion. Then, for every , there exists a predictable process such that is a BMO martingale and

| (6.9) |

where is the probability measure given by .

Proof.

We proceed similarly to the example from Subsection 5.2 and define for ,

| (6.10) |

where is as in the proof of Proposition 5.1 and where is now the stopping time

for which again . Then is bounded by . If we derive from

that the continuous local martingale is bounded from below, hence a supermartingale. It then follows from the Optional Sampling Theorem, see Karatzas and Shreve KS91 Theorem 1.3.22, that for any stopping time valued in ,

In particular, is a BMO martingale. A similar reasoning applies if and the claim is immediate for . We hence may consider the measure given by under which is a Brownian motion.

Now, for a stopping time valued in and for and , we set

where we extend the -Brownian motion to .

Let . Since vanishes on and on , for the first assertion of (6.9), it is enough to consider stopping times valued in . Using the -measurable random variable we have that a.s. Moreover, is -independent of since it is -measurable. We thus obtain

| (6.11) | ||||

where we applied Ka94 Lemma 1.3 in a similar way as in the proof of FdR10 Lemma A.1 and used that and have the same distribution under . This gives an upper bound for (6.9) in the case .

If , we note that from a.s. and the definition of ,

| (6.12) |

which is unbounded and this concludes the proof of Lemma 6.6. ∎

We are now ready to provide the proof of Theorem 6.5.

Proof of Theorem 6.5.

For item (i) we proceed similarly to the proof of Lemma 2.4 by choosing the sharpest possible version of Hölder’s inequality in the sense that the condition on the norm of is the least restrictive; this is how is selected. We set , then with , the dual number to , we have that for any stopping time valued in ,

| (6.13) |

for some constant , where we used Hölder’s inequality, the supermartingale property of , the definition of the constants and . Assumption 2.1 holds because is a martingale by Ka94 Theorem 2.3. Moreover, using and in the previous calculation, we obtain

For the uniqueness statement we assume that , , , and are as in Theorem 2.6. Then is a solution to the BSDE (6.1) where the process is bounded. This is due to Nu109 Proposition 4.5. Conversely, if the triple is a solution to the BSDE (6.1) with bounded, we can identify it with by Nu209 Corollary 5.6 provided that the utility maximization is finite for some , which is a consequence of Lemma 6.3.

For item (ii) observe that since

there exists an such that

| (6.14) |

Choose such an and then set . We mention that the need for two parameters and stems from the fact that we have two conditions which must both be satisfied, the first concerns the finiteness of exponential moments and the second relates to the (un)boundedness of . We then define and as in Lemma 6.6 and observe that contrary to the previous examples the measure change is now part of the construction. Finally, we set and deduce for that,

where we used the boundedness of and , together with . By (6.12), this shows that is unbounded, whereas we have since , see the proof of Proposition 5.1. Proposition 3.1 now yields the existence of a solution and the identification with the primal and dual problems. The conclusion is that is unbounded. Moreover, using the boundedness of again, we have

This is finite by (6.9) since the relation is equivalent to

which is inequality (6.14).

The proof of item (iii) is similar to that of item (ii). We use the same definitions subject to the modification that now we must choose and such that

This choice ensures the existence of the optimizers and guarantees the boundedness of , again thanks to Proposition 3.1 and (6.9). Note that now a dynamic exponential moment of order will not exist.

The above equation is satisfied for if , and then the inequality reads as . This last relation holds for any choice of since we have . ∎

A consequence of Theorem 6.5 is the following result.

Corollary 6.7.

- (i)

-

(ii)

The converse statement, however, is not true. More precisely, if is a BMO martingale such that for all the solutions to the primal and dual problem exist with bounded, the critical exponent need not satisfy .

Proof.

The first part is an immediate consequence of Theorem 6.5 (i). For the second part, we proceed similarly to the proof of its item (ii). Taking a one-dimensional Brownian motion , we define via (6.10) with and . By construction, is bounded by so that for

Hence, for all , the solutions to the primal and dual problem exist and the corresponding triple is the unique solution to the BSDE (6.1) with bounded. For the estimate on the process we have

The right hand side is when by (6.9), this implies actually, despite the fact that is bounded for arbitrary . ∎

Remark 6.8.

Corollary 6.7 is based on the fact that is stronger than requiring that satisfies the reverse Hölder inequality for all . However, there exists an equivalence between and a strengthened reverse Hölder condition. It follows from DT10 Theorem 4.2 that holds if and only if for some (or equivalently, all) and all there exists such that

for all stopping times valued in .

Appendix A Quadratic Continuous Semimartingale BSDEs under Exponential Moments

In this appendix we provide a short introduction to quadratic semimartingale BSDEs as described in Mo09 ; MW10 . In particular we show that all the assumptions of MW10 are satisfied and summarize the main results therein which are pertinent to the present study. Let us consider the BSDE (2.2) on ,

| (A.1) |

To prove existence and uniqueness one must first factor the process . We set so that is bounded by and derive the absolute continuity of each of the , , with respect to from the Kunita-Watanabe inequality in order to get the existence of a predictable process valued in the space of matrices such that . The BSDE (2.2) then becomes

| (A.2) |

where is a random predictable function, called the driver, which in (A.1) is given by

Since the results in MW10 only depend on the boundedness of , in a -dimensional Brownian setting we may set for and the identity matrix.

Definition A.1.

A solution to the BSDE (A.2) is a triple of processes valued in satisfying the equation (A.2) a.s. such that:

-

(i)

The function is continuous a.s.

-

(ii)

The process is predictable and satisfies , a.s. hence is -integrable.

-

(iii)

The local martingale is continuous and orthogonal to each component of , i.e. for all .

-

(iv)

We have that a.s.

The process is called the martingale part of a solution.

We collect some properties of the driver of (A.1) in the following lemma whose proof is left to the reader.

Lemma A.2.

We have that a.s.

-

(i)

The function is continuously differentiable for all .

-

(ii)

The function has quadratic growth in , i.e. for arbitrary and all we have

where

-

(iii)

We have a local Lipschitz condition in , i.e. for all and ,

-

(iv)

The driver is convex in for all . More precisely, its Hessian with respect to is given by , a positive semidefinite matrix.

Then, recalling Assumption 2.3 on the exponential moments of , we find MW10 Assumption 2.2 verified. The following theorem collects together MW10 Theorems 2.4, 2.5 and Corollary 4.2 (ii).

Theorem A.3.

Suppose Assumption 2.3 holds.

References

- (1) S. Ankirchner, P. Imkeller, and A. Popier. On measure solutions of backward stochastic differential equations. Stochastic Process. Appl., 119(9):2744–2772, 2009.

- (2) J. Azéma and M. Yor. Une solution simple au problème de Skorokhod. Séminaire de Probabilités, 13:90–115, 1979.

- (3) P. Barrieu and N. El Karoui. Monotone stability of quadratic semimartingales with applications to general quadratic BSDEs and unbounded existence result. Working Paper, 2011. arXiv:1101.5282v1.

- (4) D. Becherer. Bounded solutions to backward SDE’s with jumps for utility optimization and indifference hedging. Ann. Appl. Probab., 16(4):2027–2054, 2006.

- (5) P. Briand and Y. Hu. BSDE with quadratic growth and unbounded terminal value. Probab. Theory Related Fields, 136(4):604–618, 2006.

- (6) P. Briand and Y. Hu. Quadratic BSDEs with convex generators and unbounded terminal conditions. Probab. Theory Related Fields, 141(3-4):543–567, 2008.

- (7) F. Delbaen, Y. Hu, and A. Richou. On the uniqueness of solutions to quadratic BSDEs with convex generators and unbounded terminal conditions. Ann. Inst. Henri Poincaré Probab. Stat., 47(2):559–574, 2011.

- (8) F. Delbaen and W. Schachermayer. The fundamental theorem of asset pricing for unbounded stochastic processes. Math. Ann., 312(2):215–250, 1998.

- (9) F. Delbaen and S. Tang. Harmonic analysis of stochastic equations and backward stochastic differential equations. Probab. Theory Related Fields, 146:291– 336, 2010.

- (10) M. Émery, C. Stricker, and J. Yan. Valeurs prises par les martingales locales continues à un instant donné. Ann. Probab., 11(3):635–641, 1983.

- (11) C. Frei and G. dos Reis. A financial market with interacting investors: Does an equilibrium exist? Math. Finan. Econ., 4(3):161–182, 2011.

- (12) Y. Hu, P. Imkeller, and M. Müller. Utility maximization in incomplete markets. Ann. Appl. Probab., 15(3):1691–1712, 2005.

- (13) I. Karatzas and S. E. Shreve. Brownian motion and stochastic calculus, volume 113 of Graduate Texts in Mathematics. Springer-Verlag, New York, second edition, 1991.

- (14) I. Karatzas and S. E. Shreve. Methods of mathematical finance, volume 39 of Applications of Mathematics. Springer-Verlag, New York, 1998.

- (15) N. Kazamaki. Continuous Exponential Martingales and BMO, volume 1579 of Lecture Notes in Mathematics. Springer-Verlag, Berlin, 1994.

- (16) M. Kobylanski. Backward stochastic differential equations and partial differential equations with quadratic growth. Ann. Probab., 28(2):558–602, 2000.

- (17) D. Kramkov and W. Schachermayer. The asymptotic elasticity of utility functions and optimal investment in incomplete markets. Ann. Appl. Probab., 9(3):904–950, 1999.

- (18) D. Kramkov and W. Schachermayer. Necessary and sufficient conditions in the problem of optimal investment in incomplete markets. Ann. Appl. Probab., 13(4):1504–1516, 2003.

- (19) K. Larsen and G. Žitković. Stability of utility-maximization in incomplete markets. Stochastic Process. Appl., 117(11):1642–1662, 2007.

- (20) M. Mania and M. Schweizer. Dynamic exponential utility indifference valuation. Ann. Appl. Probab., 15(3):2113–2143, 2005.

- (21) M. Mania and R. Tevzadze. A unified characterization of -optimal and minimal entropy martingale measures by semimartingale backward equations. Georgian Math. J., 10(2):289–310, 2003.

- (22) M. Mania and R. Tevzadze. Backward stochastic partial differential equations related to utility maximization and hedging. J. Math. Sc., 153(3):291–380, 2008.

- (23) R. C. Merton. Lifetime portfolio selection under uncertainty: the continuous time case. Rev. Econom. Statist., 51(3):247–257, 1969.

- (24) M. Mocha and N. Westray. Sensitivity analysis for the cone constrained utility maximization problem. Working Paper. arXiv:1107.0190v1.

- (25) M. Mocha and N. Westray. Quadratic semimartingale BSDEs under an exponential moments condition. Working Paper, 2011. arXiv:1101.2582v1.

- (26) M.-A. Morlais. Quadratic BSDEs driven by a continuous martingale and applications to the utility maximization problem. Finance Stoch., 13(1):121–150, 2009.

- (27) M. Nutz. The opportunity process for optimal consumption and investment with power utility. Math. Finan. Econ., 3(3):139–159, 2010.

- (28) M. Nutz. The Bellman equation for power utility maximization with semimartingales. Forthcoming in Ann. Appl. Probab., 2011.

- (29) P. E. Protter. Stochastic integration and differential equations, volume 21 of Applications of Mathematics (New York). Springer-Verlag, Berlin, second edition, 2004. Stochastic Modelling and Applied Probability.

- (30) D. Revuz and M. Yor. Continuous Martingales and Brownian Motion, volume 293 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer-Verlag, Berlin, third edition, 1999.

- (31) R. Rouge and N. El Karoui. Pricing via utility maximization and entropy. Math. Finance, 10(2):259–276, 2000.

- (32) W. Schachermayer. A characterisation of the closure of in . Séminaire de Probabilités, 30:344–356, 1996.

- (33) W. Schachermayer. Utility maximisation in incomplete markets. In Stochastic methods in finance, volume 1856 of Lecture Notes in Math., pages 255–293. Springer, Berlin, 2004.

- (34) J. Sekine. On exponential hedging and related quadratic backward stochastic differential equations. Appl. Math. Optim., 54:131–158, 2006.