111Supported by TUBITAK Project No. 109T665 Novel

Stochastic Processes for Stock Prices and their Limits

Stock Price Processes with Infinite Source Poisson Agents

M. Çağlar

mcaglar@ku.edu.trDepartment of Mathematics, Koç University,

Sariyer, 34450 Istanbul, Turkey

Abstract

We construct a general stochastic process and prove weak convergence

results. It is scaled in space and through the parameters of its

distribution. We show that our simplified scaling is equivalent to

time scaling used frequently. The process is constructed as an

integral with respect to a Poisson random measure which governs

several parameters of trading agents in the context of stock

prices. When the trading occurs more frequently and in smaller

quantities, the limit is a fractional Brownian motion. In contrast,

a stable Lévy motion is obtained if the rate of trading

decreases while its effect rate increases.

Weak convergence of scaled input processes has been studied

extensively over the last decade

[3, 10, 15, 18, 22, 25, 27, 28, 29, 31, 32, 35, 36]. The limit is a fractional

Brownian motion (fBm) or a Lévy process depending on the

particular scaling. While the motivation of such analysis originates

from data traffic in telecommunications, both fBm and Lévy

processes have recently become prevalent in finance. Thereby, we

construct a general stochastic process based on a Poisson random

measure , interpret it as stock price process and prove weak

convergence results.

We consider a

real valued process of the form

(1)

where is a deterministic function satisfying Lipschitz

condition, is a scaling sequence, and and are marks

of the resulting Poisson point process with denoting the time.

The mean measure on is either a probability measure or an

infinite measure on . The process

depends on the scaling parameter through not

only , but also through the mean

measure of which is taken to have a regularly

varying form in to comply with the long-range dependence

property of teletraffic or financial data. After centering the

process , we can obtain either an fBm or a stable Lévy

motion depending on the particular scaling of the mean measure of

and the factor as . While fBm is

a self-similar and long-range dependent model, a Lévy process

has independent increments and self-similarity exists without

long-range dependence.

Our main contribution is the generalization of the previous results

[25, 31] with a specific linear form for and

[29] with an increasing satisfying some other

technical conditions, to those with Lipschitz functions. In this

case, not only the proofs require more work, but we need Lipschitz

assumptions on the derivative of as well. We

also show that the time scaling used in previous work

can be replaced by parameter scaling

of the distributions of the relevant random

variables. The time scaling has been interpreted as ‘birds-eye’ description

of a process, which is not necessary when the scaling is interpreted

in terms of its parameters. Inspired by [9], we unify the results for

general forms of with less stringent conditions in some

cases. In [9], it is noted that a fractional

Brownian motion with can be approximated if the pulse

is continuous on

and has a compact support. As an alternative extension,

we consider continuous with no compact support while

constructing (1) with as a centered

process. A secondary generalization of previous work is the

consideration of as a more general process than workload which

would be positive by definition. We allow a signed process through

the choice of real valued rate .

In related work [15, 32], the Poisson random measure

is replaced by a general arrival process and a cluster Poisson

process, respectively. Ergodicity is required for the limit

theorems in the general arrival case as well. On the other hand,

most of the previous studies on scaled input processes are named

infinite source Poisson models due to the assumption of Poisson

arrivals.

As for application in finance, the process can be

interpreted as the price of a stock. The interpretation of

(1) as a stock price process has been first presented in

[1, 11]. Our aim is to construct a model

involving the behavior of agents

that can be parameterized and estimated from data, yet having

well-known stochastic processes as its limits. While the

limiting models fit well to financial data, they do not involve

the physical parameters of the trading agents. Agent based

modeling is widely used to find a model that best fits stock price

processes. In some studies, agents are divided into two groups,

mostly named as chartists and fundamentalists. In these studies,

the two agent groups have different demand functions for the stock

[14, 21, 23] and the

price is generally determined via the total excess demand

[7, 8, 13, 20, 34]. In (1), the

arrival time , the rate and the duration of the effect

of an order are all governed by the Poisson random measure. Under

the assumption of positive correlation

between the total net demand and the price change, we expect that a

buy order of

an agent increases the price whereas a sell order decreases it.

Each order has an effect proportional to its volume and duration.

The duration of the effect is assumed to follow a heavy tailed

distribution. This effect starts when the order is given,

increases to a maximum which is proportional to the total order

amount, and then starts decreasing until it vanishes after a

finite time. Alternatively, its effect may last for some time and

leave the price at a changed level on and after the time of

transaction. The logarithm of the stock price is found by

aggregating the incremental effects of orders placed by all active

agents in . As a semi-martingale, our process does not

allow for arbitrage. It is a novel model which is alternative to

existing agent based constructions that are semi-Markov processes

[3].

We prove weak convergence results for the two different measures

used for the duration, separately. As for their connection, the

infinite measure being the limit of the probability measure is

proved in Theorem 1. Although a probability measure is appropriate

for the duration, its limiting form is able to capture the

essential tail behavior which represents long-range dependence and

self-similarity properties. Moreover, the scalings with the

limiting measure is simpler to interpret as follows. An fBm limit

is found as the frequency of trading increases and the price

effect of the orders decreases as shown in Theorem 3. In contrast,

a stable process which is a scaled version of a stable Lévy

motion is obtained in Theorem 5 when the rate of trading decreases

and the effect of the orders increases. Theorems 2 and 4 are

concerned with fBm and stable limits, respectively, for the case

of probability measure for the duration. The hypotheses in these

theorems involve extra scaling needed for obtaining the limiting

measure in addition to the scaling of the rates and effects. The

stable process obtained in the limit has a skewness parameter that

depends on the distribution of the rate as it can take

positive or negative values.

The paper is organized as follows. In Section 2, we define the

ingredients of the workload model, namely the random variables

associated with the process to be constructed.

The price process is defined in Section 3 with various

assumptions on the parameters of the Poisson random measure.

Section 4 includes limit theorems for fractional Brownian motion.

Finally, limit theorems for stable Lévy

motion are proved in Section 5.

2 Infinite Source Poisson Agents

In this section, we state our main assumptions and notation for

constructing a stock price process. We assume potentially an

infinite pool of agents and gather the agents’ trading processes

under a Poisson random measure. Each agent’s trading starts

according to the underlying Poisson process and it ends after

a random amount of time. Although the same agents may be returning

for further transaction, new arrivals are assumed to be

independent and identically distributed.

The agents are called infinite source Poisson as a term

borrowed from traffic modeling in telecommunications based on

Poisson random measures (e.g. [10, 31, 32]).

Since self-similarity and long-range dependence are common

statistical properties observed in both Internet traffic and financial data,

the stochastic models also have similar features.

In [3], a finite number of identically distributed

semi-Markov processes representing the trading states of the agents

over time are aggregated to form the price process. The number of

semi-Markov processes, equivalently, the number of agents has been

taken to infinity only in the limit. On the other hand, our price

model is a stationary process with an infinite source of agents

that arrive according to a Poisson process. We concentrate on

scaling the other parameters that have physical interpretations for

obtaining the limiting stochastic processes.

Let be a probability space. Let

denote the Borel -algebra on

. Let be a Poisson random measure on

with

mean measure

(2)

where

is the arrival rate of the underlying Poisson process,

, is the distribution of a random variable

and

is either a probability measure that satisfies

(3)

where is a slowly varying function at infinity, that is, is

such that

(4)

or a measure given by

(5)

Each atom of can be interpreted as an order

from an agent, where is the arrival time of the order,

is the duration of its effect on the price, and denotes its

rate which also plays the role of conversion to monetary units.

The sign of could be positive or negative depending on the

order being a buy or sell order, respectively. Under assumption

(5) for the measure , the duration is

obtained from a diffuse measure on with no

probability distribution. This case is studied for suppressing the

less significant details in the proofs of the convergence

theorems. In case of (3), follows a heavy tailed

distribution with finite mean but infinite variance, and the

convergence proofs involve the function . Although the latter

case is physically more meaningful, the scalings are more

involved as well in the limit theorems for the self-similar

processes fBm and stable Lévy motion.

Let

denote an effect function such that if

. The effect of an order starting at and ending at

depends on the rate of the effect and equals at

time provided that . The function can also be

interpreted as the local dynamics of a transaction as a result

of a buy or sell order. The rate will be connected to the quantity

of the order which will be elaborated further in the sequel. We specify

a general effect function that

determines by

(6)

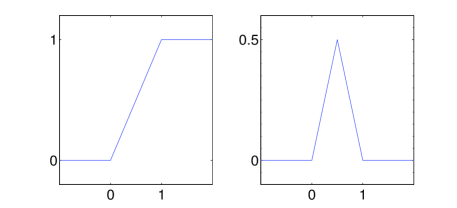

for , and for . We consider to be the

deterministic shape function, or pulse, for the effect which is then

shifted to the starting position , scaled and amplified for the

duration , and adjusted once more with the rate/conversion factor

, all randomized by .

The price process will be constructed as a sum of randomized pulses.

Characterization of that will yield an fBm or a Lévy motion

for the price process is of interest, provided that the parameters

in (2) are appropriately scaled. In the workload processes

studied in [25, 29, 31, 32], has the

following form

(7)

which represents an increasing input, or effect, with unit rate on

and remains constant thereafter. In [9], the pulse

(8)

is considered for the aim of approximating an fBm. It has a compact

support representing a limited effect that vanishes after the

duration of the pulse. These special pulses, in other words effect

functions, are sketched in Fig.1. General Lipschitz functions are

also considered in [9].

Figure 1: Sample pulses of different kind

The effect function is left unspecified in

[22, 27, 28] but with conditions on the tail properties

of its distribution for large times. The duration is not

parameterized in contrast to the present work. In [28], the

effect may last indefinitely although it decreases in time with a

regularly varying tail. In [22], each effect is assumed to

converge for large times to a finite random variable which has a

distribution with a regularly varying tail. The stable limits are

outlined in [27] with several interesting special cases. In

[29], the effect function is deterministic which is

randomized through a random variable for duration as in our case,

but with an additional assumption that the effect function itself

also has a regularly varying tail.

On the other hand, random effect functions have

been also considered also in [30] where central limit theorems are

proved under general conditions. As a special case,

the effect function could be a compound Poisson

process as in [10, 25]. This could be used to model the buy

or sell transactions in smaller quantities for a given order in the

present work. A semimartingale is assumed for the rate of the effect

in [3]. In applications, can be estimated to match

the local dynamics of the price change or the workload.

3 Price Process

Let the price process be given by where is the log-price process to be

constructed in this section. We aim to introduce a stochastic

process which is sufficiently general to approximate an fBm or a

Lévy motion, and has an adequate number of physical parameters

that can be estimated from data. The effect function and the Poisson

random measure described in Section 2 will be the main ingredients.

Remark 1

Previous models that involve heterogeneous agents usually classify

them into two separate groups as chartists and fundamentalists

according to their trading behavior [3]. This can

clearly be generalized to several types of agents.

The total effect from agents of type , ,

can be further aggregated to form as

Then, the price at time is given by as

before.

We form the log-price process by aggregating

the randomized effects. More precisely,

the difference in the effect amplitudes at times and are

integrated with respect to the Poisson random measure to yield

Since the underlying Poisson process has been going on long before

time 0, has stationary increments and by

construction. We think as the sum of all effects due

to all active agents between times 0 and . We assume that

has the form (6) as before, and write

(9)

The propositions below give the sufficient conditions for to be

well-defined for a finite measure and a specific -finite

measure in Equation (2), respectively. Let

denote the characteristic function of , that is, for .

Proposition 1

Suppose that is a probability measure

satisfying ,

and is a Lipschitz continuous function on with

for all and for all . Then,

, , is a finite random variable a.s. with

characteristic function

Proof: The integral of a deterministic

function with respect to a Poisson random measure defines a

finite random variable if where

is the mean measure. This is clearly satisfied if which also implies that the random variable has a

finite expectation [26]. Therefore, it is sufficient to

show that the expression

is finite for to be well defined as . Note

that

Considering the two different

regions and for

the first integral, and the regions

and for the second integral in

, we get

Due to the Lipschitz hypothesis on and since , we have

where . We apply integration by parts for the inner integrals

above. For , integration by parts yields

and we have where denotes the cumulative distribution

function (cdf) of and . For , we get

by integration by parts and we have . Putting all expressions together and

using , we simplify (3) as

Changing the order of integration, we get

which is finite by hypothesis as . The

characteristic function of can be found immediately from

formulae for integrals with respect to a Poisson random measure

[26].

The function characterized in Proposition 1

represents the local dynamics due to the effect of an individual

buy or sell order. The change in price, which can be

non-monotonic, occurs over a finite time and remains at the

same level thereafter. The specific shape of is left

unspecified, and so is its sign. In general, we expect a buy order

to increase the price and a sell order to decrease it. Therefore,

if is chosen to be an increasing function, then we could have

for a buy order and for a sell order. However, a

general form is assumed to leave room for modeling purposes in

view of real data and to provide mathematical generality. The

special case (7) used in [25, 32, 31]

is a linearly increasing pulse as stated in the following

corollary.

Corollary 1

Suppose that is a probability measure

satisfying , and

, . Then, , , is finite a.s. and

its characteristic function is given by

for .

Remark 2

The log-price process which is a semimartingale in

general,

becomes a martingale if its mean is zero. This would be

satisfied if , which corresponds to symmetric

effects from buy and sell orders, for example.

The following proposition is based on the results of [9].

The support of is chosen as [0,1] for simplicity without loss of generalization.

Proposition 2

Suppose that ,

and is

Lipschitz continuous with compact support . Then, is a

well-defined random variable with characteristic function

Proof: The Lipschitz assumption on and that

it has compact support imply and

(11)

for each , and in particular, by

[9, Prop.3.1]. We sketch the usual proof for defining

as an almost sure limit of zero mean random variables, as in

[9]. Let be a partition of .

Clearly,

for

, due to the form of the effect function and

boundedness of , and also for in view of (11).

Hence, the random variables

(12)

are well-defined, independent and have zero expectations. One can

show that the sum of their variances given by

(13)

is finite using (11) and the assumption that

. Therefore, the series

is a.s. convergent by [24, Lemma 3.16]. The limit is denoted

by (9) which is a stochastic integral in general since it may

be defined by an almost sure limit as above. Its characteristic

function at is the limit of the characteristic

functions of the partial sums of the random variables

(12), since almost sure convergence implies

convergence in distribution. Now, the characteristic function of

(12) can be written as

since (12) has zero mean. Using the

independence of (12) by disjointness of ,

, we can write the characteristic function of their

partial sums up to say as

Due to the inequality

for and by

finiteness of (13), dominated convergence theorem applies

and we get the result.

The pulse (8) considered in [9] is a special

case for Proposition 2 where the process is a

zero-mean martingale. In fact, we have with

the particular pulse (8) which has the shape of an

isosceles triangle. In this case, the effect starts at time as

the buy or sell order is first given. It increases linearly as the

amount traded increases, reaches its maximum value at time

as the highest effect is reached and starts

decreasing from that point on until it vanishes at time and

brings the price level back to the original, locally. Such functions

represent the effect of an order which takes place over a

period, and then vanishes after a while. This scenario is a milder

and time limited version of the Poisson shot-noise of [28]

where a shock in the market changes the price through a jump, but

then it tends back to its initial level by an exponential decay of

the first effect. There is no need to get back the effect as in the

pulses of [9] for the limit theorems. The effect function

may leave the price in a level different from the one it found at an

arrival, in which case we consider the centered process.

We

can show the connection of the two measures in propositions

1 and 2 in the next theorem. We introduce a

scaling factor which will be taken to infinity in

the limit. An integral with respect to a probability measure

with regularly varying tail converges to an integral with

respect to the measure in the limit. We first

need the following lemma.

Lemma 1

Suppose is a Lipschitz continuous function

on with

for all and for all . Then,

(14)

for and such that .

Proof: Let us call the integral

(14) as . In view of the assumptions on , we have

which can be shown along the same lines as in the proof of

Proposition 1. Evaluating the above integrals, we find

that

Theorem 1

Suppose that is a probability measure

satisfying and has a regularly varying

tail as given in

(3), the function is Lipschitz

continuous with for all , for all

and is also differentiable with satisfying a

Lipschitz condition a.e., and

for some with . Let

where and

Then, converges in law to

the process

as , where

for a Poisson random measure with mean measure

.

Proof: For the convergence of finite dimensional distributions of

, consider the

characteristic function for ,

and . It is given by

(15)

We first show that the exponent in (15) is bounded and then

use bounded convergence theorem to take the limit. This theorem is a

generalization of [25, Thm.1] with the general effect function

. Although we follow the same approach as in [25, Thm.1],

there are more terms to bound in our case. Let

(16)

Using the random variable , we denote the left hand side of

(3) as below. By integration by parts, the

exponent in (15) is equal to

(17)

where is and the hypothesis that

is used.

a) Bound for the integrand of (17) for large

values of :

In view of Potter bounds

[6], for there exists

such that

for all and , that is, . Since

for some

, we have for all

for some . Note that

by (3). Assume for simplicity of notation.

Therefore, we get

Now, we can bound using the Lipschitz property of

and on different regions for and . Let and

stand for the Lipschitz constants of and ,

respectively, or their upper bound, whichever is larger. Let us

assume for simplicity of notation.

i) and

Since and , we have

and

due to the form of and Lipschitz assumptions. Therefore, we get

using the inequalities

and ,

[25], and the fact that . The index is replaced by in order to distinguish the

cross products of sums below. We further note that

(21)

since is bounded and , assuming for

simplicity of notation. Putting all terms together by (18),

(20), (21) and i)-iv), we find that (17)

is bounded as

where

(23)

and denote the regions in i)-iv).

Since , we can write

(24)

We keep the extra bounding term for , as the integration in

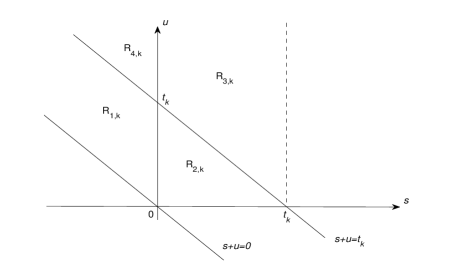

this region is more delicate. For fixed ,

are depicted in Fig.2. If we choose

such that

(25)

then the right hand side of (3) is finite as as shown in

Appendix A.

Figure 2: Subregions considered for

b) Bound for the integrand of (17) for small

values of :

We now consider as . We use Markov

inequality for as in [25], together with the

bounds (20), (21) and i)-iv) in our case. We have by Markov’s inequality. Therefore,

we get

since and for the slowly

varying function when is sufficiently large [25].

Using (27) to increase the righthand side of

(26) and in view of (24), we get

which is integrable over , as in part a), in view of the

computations in Appendix A.

As a result of a) and b), the integrand in (17) is

bounded by an integrable function. Therefore, we can use

dominated convergence theorem to find that

(28)

by (3) and (4), and then revert (17) by

another integration by parts to get the limit of (15) as

where is as in (16). It can be shown as in Proposition

2 that the above

characteristic function

and the corresponding process are well defined since

is bounded by . Hence, we have shown the convergence of finite

dimensional distributions.

To prove weak convergence in the Skorohod topology on

, we first observe that

by [25, Lemma 5]. By integration by parts and in view of

Potter bounds as before, for there exists such that the part of the integral for on

the right hand side of (3) is bounded from above by

(30)

We have

an upper bound for the absolute value of which is given by

(31)

by Lipschitz assumptions on and , where

are as in i) through iv) above, with . Substituting

(31) in (30) and starting the lower limit for from

0, we have an upper bound for the integral in (30) given by

which is finite when we choose

as in (25). On the other hand, for

, we use Markov’s inequality as before to get

Then, the

finiteness of the integrals in (3) is sufficient again for

the integrability of a dominating function for which

complements (30). It follows from dominated convergence

theorem that the limit of the right hand side of (3)

exists. Therefore, possibly for for some , the upper bound in (3) is further bounded by

a multiple of its limit given by

(33)

for some . In view of the proof of Lemma 1, the

integral in (33) is bounded by a constant multiple of

which clearly dominates

in (3)

for sufficiently large . Since the increments of

are stationary, this implies

that

(34)

for and some , by Cauchy-Schwarz inequality

and the assumption that . This concludes the proof

by [5, Thm.13.5 and Eqn.(13.14)] as .

Remark 3

We consider the scaled measure as a scaling of the

parameters of . For instance, if was the Pareto

distribution for , with parameters

and , we

would have for

, which would amount to scaling the scale parameter as

. This

leads to the limiting infinite measure on as the cutoff

parameter decreases. Although similar interpretations are possible for other

probability measures as well, the scaling

is essentially a time scaling. The random

variable , the duration of the sessions, has time

interpretation. We look at the workload of individual pulses

over shorter time periods by scaling as .

Note that the limiting process given in Theorem 1,

specifically with of (7), is obtained as a limit

of sums of scaled renewal processes in [18] as shown in

[19].

4 Fractional Brownian Motion Limit

Fractional

Brownian motion is a mean zero Gaussian process on

with and covariance

In this section, we scale the log-price process as follows to

approximate a fractional Brownian motion in the limit. Let the rate

be scaled as which can be interpreted as a decrease in the

effect of an order in absolute value as increases. This decrease

may have arised from an underlying decrease in the volume of the

transaction, for example. On the other hand, we will let the arrival

rate of orders increase with a factor which is a function

of . For each , let

denote the Poisson random measure with scaled mean measure that involves the

scaled arrival rate and possibly further scalings.

In the following theorems, we prove convergence of

to fBm

with a properly scaled measure for

a finite measure as in (3)

and with as in (5). Compensated Poisson random

measure is used when does not exist.

Lemma 2

Let be a strictly positive real sequence and

. If , then

Proof: Consider the Taylor expansion [17, pg.184-186] of the

function around 0 on the disk

. We have

where is the remainder after 3 terms. For fixed with

, we can express as

By continuity of , there exists such that

for all , in particular for . Clearly,

since is positive. Then,

we have the following bound for :

Taking the limit as , we obtain

.

Theorem 2

Suppose that is a probability measure

satisfying and has a regularly varying

tail as given in

(3), the function is Lipschitz

continuous with for all , for all

and is also differentiable with satisfying a

Lipschitz condition a.e., and . Let

and

where and . Then, the process

converges in law to an fBm

with variance parameter

as .

Proof: The characteristic function

for , and is given by

(35)

The same approach will be followed as in the proof of Theorem

1. By integration by parts, we find that the exponent of

(35) is given by

(36)

Using Potter bounds [6] and Lipschitz conditions on

and , we get an inequality similar to (3) for given by

where is similar to (23) but with by

hypothesis, and and . Precisely,

If we choose such that

then the right hand side of (4) is finite along the

same lines of the proof of Theorem 1 with . On

the other hand, we can bound (36) for

similarly. Therefore, we can use dominated convergence theorem. We

have

As an example, the continuous flow rate model studied in

[25] is given by

(40)

with replaced by the special form (7) in

(9). In [25, Thm.2], the limit is studied when the

speed of time increases in proportion to the intensity of Poisson

arrivals. To balance the increasing trading intensity ,

time is speeded up by a factor and the size is normalized by

a factor provided that

. We can let

with . Taking

, we show the equivalence of the scaling of

[25, Thm.2] to the scaling in Theorem 2. Note that

. The scaled and centered process has the

form

(41)

where we have written an effect function in general. Then, we

can make change of variables and to get

(42)

where the mean measure is

(43)

In Theorem 2, we start with the scaled process

(42) essentially. This can be observed by the fact that

for a Poisson random measure with mean measure

by definition of a Poisson random measure

[24],[12, Def.V.2.2]. Equivalence of the

scalings in Theorem 2 and [25, Thm.2] is in

distributional sense. However, this is sufficient for equivalence as

the convergence results are in distribution rather than almost sure

sense.

Therefore, we can apply Theorem

2 to obtain the limit as a fBm with variance parameter

It is shown in [25] that the asymptotic behavior of the

ratio determines the type of the limit

process when time is speeded up by a factor . For a choice of

sequences and , the random variable

denotes the number of effects still active

at time n. It measures the amount of very long pulses that are

alive and how much they contribute to the total price. The

expected value of the random variable is

for large . The limit is considered in the cases where this value

tends to a finite positive constant, to infinity, or to zero as

and go to infinity. We have already studied the case

of finite constant in Theorem 1 and infinity in Theorem

2, the so-called intermediate and fast connection rates,

respectively, in view of telecommunication applications. As shown

above, our scalings do not involve time scaling. They can be

physically understood as scalings of the parameters of the log-price

process. The slow connection rate will be investigated similarly in

terms of the model parameters in Theorem 4 in the next

section.

The next theorem is a simpler version of Theorem 2 due to

the form of the measure .

Note that

(43) can be approximated as

for large . This scaling is used below with the simpler form of

. It can be interpreted as half way in taking the more involved

limit of Theorem 2.

Theorem 3

Let

where and

Suppose that and is a Lipschitz continuous function satisfying either of

the following conditions

i.

for all and for all , or

ii.

has a compact support.

Then, the process , for ,

converge in law to an fBm with variance parameter

as .

Proof: Although it can be found from the

characteristic function of in Proposition 2 that

for all under assumption ii, we form

as above since may not exist with

assumption i. For the convergence of finite dimensional

distributions of , consider the

characteristic function for , and . It is given by

(44)

where is given in (16). Note that the characteristic

function exists since are well defined in view of

(14) which follows from Lemma 1 with

under assumption i, and by Proposition 2 under

assumption ii. As , we will show that the above

characteristic function converges to

(45)

Due to the

inequality for , the

integrand in (45) is an upper bound to

Therefore,

dominated convergence theorem allows us to take the limit inside the

integral in (44). That is, we must find

which is now equal to

(46)

by Lemma 2. This shows that (44)

converges to (45) as by

the continuity of the exponential function. The variance is

evaluated in the proof of Theorem 2.

To complete the proof, we need to show convergence in

with Skorohod topology. This is straight forward

since the variance of is

already free of and is bounded by a constant multiple of

by the proof of Lemma 1.

Remark 4

Theorem 3 with condition ii. is Theorem 3.1 of

[9] where it is noted that a fractional Brownian motion

with can be approximated if the pulse is continuous and has

a compact support. Condition i. above considers an effect function

which is continuous, but with no compact support as an alternative.

5 Lévy Process Limit

A process with stationary and independent increments is called

a Lévy process [4, 37]. The results of this section

concerns a particular class of Lévy processes, namely stable

Lévy motion [33]. Let

, and let ,

and be the index of

stability and skewness parameter, respectively. Then, a

-stable Lévy motion with mean 0 can be defined

through its characteristic function

for , where is a scale parameter.

In this section, we prove that the limiting process is a -stable Lévy

motion under different scalings of the price process. Theorem

4 considers a probability measure and Theorem

5 starts with its limiting form. For simplicity of

notation, we take in the effect function.

Lemma 3

Let be a Poisson random measure with mean measure

and

. Then,

where ,

, and and

are independent -stable Lévy motions with mean 0,

skewness intensity equal to 1 and , respectively, and

scale parameter

Proof: Putting , we get

where we have put

and

It is easy to verify that both and are Poisson

random measures with means , , respectively. What is more, they are independent as

their domains are disjoint. Making another change of variable for in respective integrals in

(5), we get

(48)

where and are independent -stable Lévy

motions with skewness parameter and scale parameter

where is also a -stable Lévy motion since

is a Poisson

random measure on with mean

measure , but skewness parameter

[33, pg.5]. We can take and the result

follows.

Theorem 4

Suppose that is a probability measure

satisfying and has a regularly varying

tail as given in

(3), the function is Lipschitz

continuous with for all , for all

and is also differentiable with satisfying a

Lipschitz condition a.e., and

for some

such that . Let

and

where and .

Then, the process , for

, converges in law to

as , where and

are independent -stable Lévy motions with mean 0, and

skewness intensity and , respectively.

Proof: The characteristic function of the scaled process is given by

where is as in (16). By integration by parts, we get

(49)

since . Making a change of variable to

, the logarithm of (49) is equal to

(50)

Using Potter bounds and Lipschitz conditions on and , we

get an inequality similar to (3). We can bound

as

in (18) and consider

separately. As a result, for fixed , there exists

such that for all with

, we have the following upper bound for

the absolute value of (50) when evaluated over

and are analogous to with replaced by . The right

hand side of (5) is integrable when is

chosen as in (25) as shown in Appendix B.

For , we can find a dominating function

for the integrand in (50) using Markov’s inequality. As

in the proof of Theorem 1, we have

(52)

where satisfies (51). Using (51) and using an

inequality similar to (27) in view of the assumption , we can increase the righthand side of

(52) as

which is integrable over in view of Appendix B.

We can now use the dominated convergence theorem. Note that

where is given by

(55)

and we have

(56)

To see (56), one takes the limit in regions , separately. Fig.3 illustrates the function

over these regions where we consider as

. By (28), (5),

(55) and (56), we take the limit of

(50) and then revert the integration by parts to get

the limiting characteristic function as

But, this is the characteristic function of , where

for a Poisson random measure with mean measure , and . This

characterizes the limiting process by Lemma 3.

To complete the proof of weak convergence, it is sufficient to show

that for

some and in view of the proof of Theorem 1. In

the present theorem, we need a finer estimate given in [38, Lemma

2] and used in [25, Lemma 6]. We have

(57)

where

and , which is

finite with . Substituting and applying

integration by parts, we get

(58)

where

(59)

For latter use, the partial derivative of in is found as

Note the similarity of to (50). Moreover, the

inequality holds since

leading to estimates as in

(20) and (21). It follows that

is an upper bound to when it is evaluated over where and are as above and

For evaluating for smaller values of , we have a bound similar

to (5). Therefore, is bounded by an integrable

function uniformly over in view of the analogous computations in

Appendix B. By dominated convergence theorem, let .

We find that

by using the same approach for taking the limit of the

characteristic function of the finite dimensional distributions

above. Then, we can write

(60)

for sufficiently large , by (57), since is

increasing in . Simplifying further, we have

where the second equality follows by a change of variable to

. Define the constant so that . Now, substituting in (60) and

changing to , we get

which concludes the proof as .

Figure 3: Graphs of in different subregions for

. The function is arbitrary provided

that its derivative and itself are Lipschitz continuous almost

everywhere.

Remark 5

Note that the stable process obtained in the limit is stable

with a skewness parameter that depends on the distribution of the

rate . Moreover, it has stationary and independent increments.

Therefore, it is also a -stable Lévy motion

[33, Def.7.5.1], but with scale parameter

and skewness parameter

by [33, pg.s 10,11], where and , see also [4, pg.217]. In the context of supply and

demand, one can interpret as the skewness caused by demand and

by supply since they are expected to increase and decrease the

price, respectively.

Remark 6

The weak convergence result given in Theorem 4 is proved with

Skorohod’s topology. In [25], the analogous result

based on (7) has been omitted. The convergence is shown

with topology instead of in [36] where

the effect function is assumed to be monotone increasing in the

context of workload input to the system. The authors heuristically

argue that some of the individual loads are too large

[36, Rmk.4.2].

On the other hand, [22] proves weak convergence with

topology considering that the limit process has jumps.

However, topology also works as shown above. The interplay

between and is discussed in [2] for sums of

moving averages. It is proved that convergence cannot hold

because adjacent jumps of this process can coalesce in the limit.

An intuitive explanation is

given as the jump of the limiting process occurring from a

staircase of several jumps. Under certain conditions,

convergence is shown instead. We have a simpler situation where

each arrival of the scaled process generates a jump of the limit

process as evident from (56).

The following theorem is based on the simpler form of the mean

measure.

Theorem 5

Suppose the function is Lipschitz

continuous with for all , for all

and is also differentiable with satisfying a

Lipschitz condition a.e., and for

some with . Let

where and

Then, the process

, for , converges in law to

as , where and

are independent -stable Lévy motions with mean 0, and

skewness intensity and , respectively.

Proof: We will give only a sketch of the proof due to its similarities

with the previous theorem. The characteristic function for the

finite dimensional distributions of can be written as

with as in (16). Making a change of variable to

, we get

(61)

Now, is similar to (55) and we take a

similar limit to (56) with

replaced by . This is justified by dominated convergence

theorem

since the integrand in (61) can be bounded as in the

proof of Theorem 4. Convergence in follows

along the same lines, this time with in of

(59).

The simpler form of scalings in Theorems 3 and 5 facilitate neat

interpretations in terms of the parameters of the price process. In

Theorem 3, is scaled as and is scaled as

, which means that the trading occurs more frequently, but in

smaller quantities and yields a fractional Brownian motion limit. In

contrast, a stable process is obtained if the rate of trading

decreases while its effect rate increases since is scaled

as and is scaled as in Theorem 5.

References

[1] Z. Akçay, M. Çağlar, An Agent Based Stock Price Model, SPA

2007, Illinois, USA.

[2] F. Avram, M. Taqqu, Weak Convergence of Sums of

Moving Averages in the -Stable Domain of Attraction, The

Annals of Probability, 20 (1992), 483-503.

[3] E. Bayraktar , U. Horst, R. Sircar,

A limit Theorem for Financial Markets with Inert Investors,

Mathematics of Operations Research, 31 (2006), 789-810.

[4] J. Bertoin, L’evy Processes, 2007,

Cambridge University Press.

[5] P. Billingsley, Convergence of Probability

Measures, 1999, Second Edition, John Wiley.

[7] G.-I. Bischi, M. Gallegati, L. Gardini, R.

Leombruni, A. Palestrini, Herd behavior and nonfundamental asset

price fluctuations in financial markets, Macroeconomic Dynamics, 10

(2006), 502-528.

[8] D. Challet, A. Chessa, M. Marsili and Y.-C.

Zhang, From Minority Games to real markets, Quantitative Finance

Volume 1 (2001), 168-176.

[9] R. Cioczek-Georges, B. B. Mandelbrot,

Alternative Micropulses and Fractional Brownian Motion, Stochastic

Processes and their Applications, 64 (1996), 143-152.

[10] M. Çağlar,

A Long-Range Dependent Workload Model for Packet Data Traffic.

Mathematics of Operations Research, 29 (2004), 92-105.

[11] M. Çağlar, Weak Limits of Infinite Source Poisson

Pulses, 7th World Congress in Probability and Statistics, 2008,

Singapore.

[12] E. Çınlar, Lecture Notes in Probability

Theory, Princeton University, 2003. Probability and Stochastics,

Springer (to appear, 2010).

[13] G. Iori, A microsimilation of traders activity

in the stock market: the role of heterogeneity, agents’ interactions

and trade frictions, Journal of Economic Behavior and Organization,

49 (2002), 269-285.

[14] J. D. Farmer, S. Joshi, The Price dynamics of

common trading strategies, Journal of Economic Behavior and

Organization, 49 (2002), 149-171.

[15] V. Fasen, G. Samorodnitsky A Fluid Cluster Poisson

Process Can Look Like a Fractional Brownian Motion Even in the Slow

Growth Regime, Advances in Applied Probability, 41 (2009), 393-427.

[16] W. Feller, An Introduction to Probability Theory

and its Applications, Vol.2, 2nd edn, 1971, Wiley, New

York.

[17] W. Fulks, Complex Variables, Marcel Dekker,

Inc., 1993.

[18] R. Gaigalas, I. Kaj, Convergence to Scaled

Renewal Processes and a Packet Arrival Model, 9 (2003), 671-703.

[19] R. Gaigalas, A Poisson Bridge between Fractional Brownian Motion

and Stable Lévy Motion, Stochastic Processes and their

Applications, 116 (2006), 447-462.

[20] F. Ghoulmie, R. Cont and J.-P. Nadal,

Heterogeneity and feedback in an agent-based market model, Journal

of Physics: Condensed Matter, 17 (2005), S1259-S1268.

[21] I. Giardina, J-P. Bouchaud, M. Mézard,

Microscopic models for long ranged volatility correlations, Physica

A, 299 (2001), 28-39.

[22] W. Jedidi, J. Almhana, V. Choulakian, R. McGorman,

The Poisson Shot Noise Traffic Model, and

Functional Convergence to Stable Processes, (2010), Preprint.

[23] X-Z. He, F. H. Westerhoff, Commodity markets,

price limiters and speculative price dynamics, Journal of Economic

Dynamics and Control, 29 (2005), 1577-1596.

[24] O. Kallenberg Foundations of Modern Probability,

1997, Springer.

[25] I. Kaj and M. S. Taqqu, Convergence to fractional Brownian motion and

to the Telecom process: the integral representation approach,

Brazilian Probability School, 10th anniversary volume, Eds. M.E.

Vares, V. Sidoravicius, 2007, Birkhauser.

[27] C. Klüppelberg, T. Mikosch and A. Scharf,

Regular Variation in the Mean and Stable Limits for Poisson Shot

Noise, Bernoulli, 9 (2003), 467-496.

[28] C. Klüppelberg and C. Kühn, Fractional

Brownian motion as a weak limit of Poisson shot noise processes-

with applications to finance, Stochastic Processes and their

Applications, 113 (2004), 333-351.

[29] T. Konstantopoulos and S. Lin . Macroscopic Models for

Long-Range Dependent Network Traffic, Queueing Systems, 28 (1998)

215-243.

[30] T. Kurtz . Limit Theorems for Workload Input Models. F.P.

Kelly, S. Zachary, I. Ziedins, Eds., Stochastic Networks: Theory

and Applications, 1996, Clarendon Press, Oxford.

[31] T. Mikosch, S. Resnick, H. Rootzén and A. Stegeman .

Is Network Traffic Approximated by Stable Lévy Motion or

Fractional Brownian Motion? Annals of Applied Probability, 12

(2002) 23-68.

[32] T. Mikosch and G. Samorodnitsky,

Scaling Limits for Cumulative Input Processes, Mathematics of

Operations Research, 32 (2007), 890-918.

Samorodnitsky and Taqqu [1994]

G. Samorodnitsky and M.S. Taqqu Stable Non-Gaussian Random

Processes, 1994, Chapman & Hall.

[34] K. S. Sznajd-Weron, R. Weron, A simple model

of price formation, International Journal of Modern Physics C, 13

(2002), 115-123.

[35] V. Pipiras, M.S. Taqqu, J.B. Levy, Slow, Fast and

Arbitrary Growth Conditions for Renewal-Reward Processes When Both

the Renewals and the Rewards Are Heavy-Tailed, Bernoulli, 10 (2004),

121-163.

[36] S. Resnick, E. van den Berg, Weak Convergence of

High-Speed Network Traffic Models, J. Appl. Prob., 37 (2000),

575-597.

[37] K. Sato, Lévy Processes and Infinitely Divisible

Distributions, 1999, Cambridge University Press.

[38] B. von Bahr, C.G. Esseen, Inequalities for the

rth Absolute Moment of a Sum of Random Variables, , Ann. Math. Stat., 36 (1965), 299-303.

Appendix A

We show that the right hand side of (3) is finite.

When the right hand

side of (3) is splitted over different regions, checking

the finiteness of the integrals over

reduces to showing that

is finite. This is indeed true when we choose such that

(62)

In region , we have

(63)

If , it can be observed from Fig.2 that the integral

reduces to that over region . If , then the

integral over yields an upper bound. That is, we can

replace by the constant function and get

In this part, we show that (51) is integrable with respect to

. Substituting

the limits of integration in regions

shown by , respectively, we have

where we put . The integrals

are finite for

since

for and , where

. In , we have

As in Appendix A, we consider two intervals and

to evaluate this integral. Over the first interval,

it is finite for , and over the latter,

it is proportional to which is

bounded by 1. As a result, (51) is finite if we choose

such that