Tight Approximations of Dynamic Risk Measures

Abstract

This paper compares two different frameworks recently introduced in the literature for measuring risk in a multi-period setting. The first corresponds to applying a single coherent risk measure to the cumulative future costs, while the second involves applying a composition of one-step coherent risk mappings. We summarize the relative strengths of the two methods, characterize several necessary and sufficient conditions under which one of the measurements always dominates the other, and introduce a metric to quantify how close the two risk measures are.

Using this notion, we address the question of how tightly a given coherent measure can be approximated by lower or upper-bounding compositional measures. We exhibit an interesting asymmetry between the two cases: the tightest possible upper-bound can be exactly characterized, and corresponds to a popular construction in the literature, while the tightest-possible lower bound is not readily available. We show that testing domination and computing the approximation factors is generally NP-hard, even when the risk measures in question are comonotonic and law-invariant. However, we characterize conditions and discuss several examples where polynomial-time algorithms are possible. One such case is the well-known Conditional Value-at-Risk measure, which is further explored in our companion paper Huang et al. (2012). Our theoretical and algorithmic constructions exploit interesting connections between the study of risk measures and the theory of submodularity and combinatorial optimization, which may be of independent interest.

1 Introduction.

Measuring the intrinsic risk in a particular unknown outcome and comparing multiple risky alternatives has been a topic of central concern in a wide range of academic disciplines, resulting in the development of numerous frameworks, such as expected utility, stochastic ordering, and, in recent years, convex and coherent risk measures.

The latter class has emerged as an axiomatically justified and computationally tractable alternative to several classical approaches, and has provided a strong bridge across a variety of parallel streams of research, including ambiguous representations of preferences in economics (e.g., Gilboa and Schmeidler (1989), Schmeidler (1989), Epstein and Schneider (2003), Maccheroni et al. (2006)), axiomatic treatments of market risk in financial mathematics (Artzner et al. (1999); Föllmer and Schied (2002)), actuarial science (Wirch and Hardy (1999); Wang (2000); Acerbi (2002); Kusuoka (2001); Tsanakas (2004)), operations research (Ben-Tal and Teboulle (2007)) and statistics (Huber (1981)). As such, our goal in the present paper is not to motivate the use of risk measures – rather, we take the framework as given, and investigate two distinct ways of using it to ascribe risk in dynamic decision settings.

A first approach, prevalent among practitioners, entails applying a static risk measure to the total future costs accumulated over the remaining problem horizon, and conditioned on the available information. More formally, a decision maker faced with a future sequence of random costs , respectively dispensed over a finite horizon , would measure the risk at time by , where denotes the filtration containing all information at time , and is a static risk measure. In practice, the same is often used at every time , resulting in a risk preference that is easy to specify and calibrate. Apart from simplicity, the approach also has one other key advantage: when the risk measure used is convex, static decisions can be efficiently computed by combining simulation procedures with convex optimization (e.g., Rockafellar and Uryasev (2000), Ruszczynski and Shapiro (2006b)). This has lead to a wide adoption of the methodology in practice, as well as in several academic papers (see, e.g., Basak and Shapiro (2001), Cuoco et al. (2008) and references therein).

The paradigm above, however, is known to suffer from several serious shortcomings. It can result in inconsistent preferences over risk profiles in time, whereby a decision maker faced with two alternative cumulative costs and can deem riskier than in every state of the world at some time , but nonetheless deem riskier than at time . This dynamic or time inconsistency has been criticized from an axiomatic perspective, as it is a staple of irrational behavior (Epstein and Schneider, 2003; Roorda et al., 2005; Artzner et al., 2007). Furthermore, time inconsistent objectives couple risk preferences over time, which is very undesirable from a dynamic optimization viewpoint, since it prevents applying the principles of Dynamic Programming to decompose the problem in stages (Epstein and Schneider (2003); Ruszczynski and Shapiro (2006a); Nilim and El Ghaoui (2005); Iyengar (2005)).

In order to correct such undesirable effects, additional conditions must be imposed on the risk measurement process at distinct time periods. Such requirements have been discussed extensively in the literature, and it has been shown that any risk measure that is time consistent is obtained by composing one-step conditional risk mappings. More formally, a time consistent decision maker faced with costs would assess the risk at time by , for a set of suitable mappings (see, e.g., Epstein and Schneider (2003), Riedel (2004), Cheridito et al. (2006), Artzner et al. (2007), Roorda et al. (2005), Föllmer and Penner (2006), Ruszczyński (2010)). Apart from yielding consistent preferences, this compositional form also allows a recursive estimation of the risk, and an application of the Bellman principle in optimization problems involving dynamic risk measures (Nilim and El Ghaoui, 2005; Iyengar, 2005; Ruszczynski and Shapiro, 2006a).

From a pragmatic perspective, however, the compositional form entails a significantly more complicated risk assessment than the naïve inconsistent approach. A risk manager would need to specify single-period conditional risk mappings for every future time-point; furthermore, even if these corresponded to the same risk measure , the exact result of the composition would no longer be easily interpretable, and would bear no immediate relation to the original . Our conversations with managers also revealed a certain feeling that such a measurement could result in “overly conservative” assessments, since risks are compounded in time – for instance, by composing VaR, one would obtain extreme quantiles of quantities that are already extreme quantiles. This has been recognized informally in the literature by Roorda and Schumacher (2007, 2008), who proposed new notions of time consistency that avoided the issue, but without establishing formally if or to what degree the conservatism is actually true. Furthermore, it is not obvious how “close” a particular compositional measure is to a given inconsistent one, and how one could go about constructing the latter in a way that tightly approximates the former. This issue should be very relevant when considering dynamic decision problems under risk, but it seems to have been largely ignored by the literature (most papers examining operational problems under dynamic risk typically start with a set of given dynamic risk measures, e.g., Ahmed et al. (2007), Shapiro (2012), Choi et al. (2011)).

With this motivation in mind, the goal of the present paper is to better understand the relation and exact tradeoffs between the two measurement processes outlined above, and to provide guidelines for constructing and/or estimating safe counterparts of one from the other. Our contributions are as follows.

-

•

We provide several equivalent necessary and sufficient conditions guaranteeing when a time consistent risk measure always over (or under) estimates risk as compared with an inconsistent measure . We argue that iterating the same does not necessarily over (or under) estimate risk as compared to a single static application of , and this is true even in the case considered by Roorda and Schumacher (2007, 2008). We show that composition with conditional expectation operators at any stage of the measurement process results in valid, time consistent lower bounds. By contrast, upper bounds are obtained only when composing with worst-case operators in the last stage of the measurement process.

-

•

We formalize the problem of characterizing and computing the smallest and such that and , respectively. The smallest such factors, and , provide a compact notion of how closely a given can be multiplicatively approximated through lower (respectively, upper) bounding consistent measures , respectively. Since, in practice, may be far easier to elicit from observed preferences or to estimate from empirical data, characterizing and computing and can be seen as the first step towards constructing the time-consistent risk measure that is “closest” to a given .

-

•

Using results from the theory of submodularity and matroids, we particularize our results to the case when and are both comonotonic risk measures. We show that computing and is generally NP-hard, even when the risk measures in question are law-invariant. However, we provide several conditions under which the computation becomes simpler. Using these results, we compare the strength of approximating a given by time-consistent measures obtained through composition with conditional expectation or worst-case operators.

-

•

We characterize the tightest possible time-consistent and coherent upper bound for a given , and show that it corresponds to a construction suggested in several papers in the literature (Epstein and Schneider, 2003; Roorda et al., 2005; Artzner et al., 2007; Shapiro, 2012), which involves “rectangularizing” the set of probability measures corresponding to . This yields not only the smallest possible , but also the uniformly tightest upper bound among all coherent upper bounds.

-

•

We summarize results from our companion paper (Huang et al., 2012), which applies the ideas derived here to the specific case when both and are given by Average Value at Risk, a popular measure in financial mathematics. In this case, the results take a considerably simpler form: analytical expressions are available for two-period problems, and polynomial-time algorithms are available for some multi-period problems. We give an exact analytical characterization for the tightest uniform upper bound to , and show that it corresponds to a compositional AVaR risk measure that is increasingly conservative in time. For the case of lower bounds, we give an analytical characterization for two-period problems. Interestingly, we find that the best lower-bounds always provide tighter approximations than the best upper bounds in two-period models, but are also considerably harder to compute than the latter in multi-period models.

The rest of the paper is organized as follows. Section 2 provides the necessary background in static and dynamic risk measures, and introduces the precise mathematical formulation for the questions addressed in the paper. Section 3 discusses the case of determining upper or lower bounding relations between two arbitrary consistent and inconsistent risk measures, and characterizes the resulting factors and . Section 4 discussed our results in detail, touching on the computational complexity, and introducing several examples of how the methodology can be used in practice. Section 5 concludes the paper and suggests directions for future research.

1.1 Notation.

With , we use to denote the index set . For a vector and , we use to denote the -th component of . For a set , we let . Also, we use to denote the vector with components for and otherwise (e.g., is the characteristic vector of the set ), and to denote the projection of the vector on the coordinates . When no confusion can arise, we denote by the vector with all components equal to 1. We use for the transpose of , and for the scalar product in .

For a set or an array , we denote by the set of all permutations on the elements of . or designate one particular such permutation, with denoting the element of appearing in the -th position under permutation .

We use to denote the probability simplex in , i.e., . For a set , we use to denote the set of its extreme points.

Throughout the exposition, we adopt the convention that .

2 Consistent and Inconsistent Risk Measures.

As discussed in the introduction, the goal of the present paper is to analyze two paradigms for assessing risk in a dynamic setting: a “naïve” one, obtained by applying a static risk measure to the conditional cumulative future costs, and a “sophisticated”, time-consistent method, obtained by composing one-period risk mappings.

In the present section, we briefly review the relevant background material in risk theory, describe the two approaches formally, and then introduce the main questions addressed in the paper.

2.1 Probabilistic Model.

We begin by describing the probabilistic model. Our notation and framework are closely in line with that of (Shapiro et al., 2009), to which we direct the reader for more details.

For simplicity, we consider a scenario tree representation of the uncertainty space, where denotes the time, is the set of nodes at stage , and is the set of children111In other words, is a partition of the nodes in . of node . We also use to denote the set of all leaves descending from node , i.e., with , we recursively define . Similarly, we define for any set .

With the set of elementary outcomes, we associate the -algebra of all its subsets, and we consider the filtration , where is the sub-algebra of that is generated by the sets , for any .

We construct a probability space by introducing a reference measure , assumed to satisfy222This is without loss of generality - otherwise, all arguments can be repeated on a tree where leaves with zero probability are removed. . On the space , we use to denote the space of all functions that are -measurable. Since is isomorphic with , we denote by the random variable, and by the vector in of induced scenario-values, and we identify the expectation of with respect to a measure as the scalar product . In a similar fashion, we introduce the sequence , where is the sub-space of containing functions which are -measurable. Note that any function is constant on every set , so that can also be identified with the vector . To this end, in order to simplify the notation, we identify any function with a set of functions, and we write , where . Furthermore, since all the functions of this form that we consider correspond to conditional evaluations on the nodes of the tree, we slightly abuse the notation and write , where .

2.2 Static Risk Measures.

Consider a discrete probability space , and let be a linear space of random variables on . In this setup, we are interested in appropriate ways of assessing the riskiness of a random cost (or loss) . The standard approach in the literature (Artzner et al., 1999; Föllmer and Schied, 2004) is to use a functional such that represents the minimal reduction making a cost acceptable to the risk manager. The following axiomatic requirements are typically imposed.

-

[P1]

Monotonicity. For any such that , .

-

[P2]

Translation invariance. For any and any , .

-

[P3]

Convexity. For any , and any , .

-

[P4]

Positive homogeneity. For any , and any , .

-

[P5]

Comonotonicity. for any that are comonotone, i.e., , for any .

-

[P6]

Law-invariance. for any such that .

Monotonicity requires that a larger cost should always be deemed riskier. Translation (or cash) invariance gives an interpretation as capital requirement: typically, a cost is deemed acceptable if , so cash invariance implies that , i.e., is the smallest amount of cost reduction making acceptable. Convexity suggests that diversification of costs should never increase the risk (or, conversely, that a convex combination of two acceptable costs and should also be acceptable), while positive homogeneity implies that risk should scale linearly with the size of the cost. Comonotonicity implies that the risk in costs that move together (i.e., are comonotone) cannot be diversified by mixtures, while law-invariance requires the risk measures to only depend on the probability distribution of the random costs. For an in-depth discussion and critique of these axioms, we direct the reader to (Artzner et al., 1999; Föllmer and Schied, 2004) and references therein.

Following the common terminology in the literature, we call any functional satisfying [P1-2] a risk measure. Any risk measure satisfying [P3] is said to be convex, and any convex risk measure that satisfies [P4] is said to be coherent. The main focus of the present paper are functionals that satisfy333It is known that comonotonicity actually implies positive homogeneity (Föllmer and Schied, 2004), so the we can define comonotonic risk measures as those satisfying [P1-3] and [P5] (the reverse is not true, i.e., not all coherent risk measures are comonotonic (Acerbi, 2004)). [P1-5], which are called comonotonic risk measures. Some of our results take a simpler form when further restricting attention to the class of distortion risk measures, which are all comonotonic risk measures additionally satisfying [P6]. Such measures have been examined in economics, actuarial science, and financial mathematics, and form a well-established class of risk metrics (see, e.g., (Schmeidler, 1986; Wang, 2000; Tsanakas, 2004; Cotter and Dowd, 2006; Kusuoka, 2001; Acerbi, 2002, 2004; Föllmer and Schied, 2004) for more references and details).

One of the main results in the literature is a universal representation theorem for any coherent risk measure, which takes a specialized form in the comonotonic case (Schmeidler, 1986; Föllmer and Schied, 2004).

Theorem 2.1.

A risk measure is coherent if and only if it can be represented as

| (1) |

for some . Furthermore, if is comonotonic, then , where is a Choquet capacity.

The result essentially states that any coherent risk measure is an expectation with respect to a worst-case probability measure, chosen adversarially from a suitable set of test measures (or generalized scenarios) . For comonotonic risk measures, this set is uniquely determined by a particular function , known as a Choquet capacity.

Definition 2.1.

A set function is said to be a Choquet capacity if it satisfies the following properties:

-

•

nondecreasing:

-

•

normalized: and

-

•

submodular: .

When a comonotonic risk measure is additionally law-invariant (i.e., it is a distortion measure), the Choquet capacities are uniquely determining by a concave distortion function, i.e.,

| (2) |

where is a concave, nondecreasing function satisfying and .

A popular example of comonotonic (in fact, distortion) risk measure, studied extensively in the literature, is Average Value-at-Risk at level (), also known as Conditional Value-at-Risk, Tail Value-at-Risk or Expected Shortfall. It is defined as

| (3a) | ||||

where is the Value at Risk at level . As the name suggests, represents an average of all VaR measures with level at most . When the underlying reference measure is non-atomic, it can be shown (Föllmer and Schied, 2004) that , which motivates the second and third names that the latter measure bears. While AVaR is a distortion measure, VaR is not even convex, since it fails requirement [P3].

2.3 Dynamic Risk Measures.

As stated in the introduction, the main focus of the present paper are dynamic risk measures, i.e., risk measures defined for cash streams that are received or dispensed across several time-periods. More precisely, a dynamic risk measure entails the specification of an entire sequence of risk measures , such that maps a future stream of random costs into risk assessments at .

Following a large body of literature (Riedel, 2004; Artzner et al., 2007; Detlefsen and Scandolo, 2005; Roorda et al., 2005; Cheridito et al., 2006; Föllmer and Penner, 2006; Ruszczynski and Shapiro, 2006a; Ruszczyński, 2010; Cheridito and Kupper, 2011), we furthermore restrict the risk measurements at time to only depend on the cumulative costs in the future, i.e., we take , and the risk of is . While such measures have been criticized for ignoring the timing when future cashflows are received, they are consistent with the assumptions in many academic papers focusing on portfolio management under risk (Basak and Chabakauri, 2010; Cuoco et al., 2008), as well as with current risk management practice (Jorion, 2006), and provide a natural, simpler first step in our analysis.

In this framework, we introduce the first way of measuring dynamic risk, whereby is obtained by applying a static risk measure, conditioned on information available at time . In the context of the probabilistic space of Section 2.1, this can be formalized as follows.

Definition 2.2.

A time inconsistent (dynamic) risk measure is any set of mappings of the form , where is a risk measure, for any node .

In other words, conditional on reaching node at time , the risk of a future cashflow is given by , where every is a static risk measure, which can be furthermore required to satisfy additional axiomatic properties, as per Section 2.2.

The choice above is eminently sensible - the specification of risk can be done in a unified fashion, by means of a single risk measure at every node and time. This makes for a compact representation of risk preferences, which can be more easily calibrated from empirical data, more readily comprehended and adopted by practitioners, and more uniformly applied across a variety of businesses and products. For instance, it is by far the most common paradigm in financial risk management, where a 10-day VaR is typically calculated at level , assuming the trading portfolio remains fixed during the assessment period (Jorion, 2006).

However, as the name suggests, such risk measures readily result in time inconsistent behavior. To see this, consider the following example, adapted from Roorda et al. (2005).

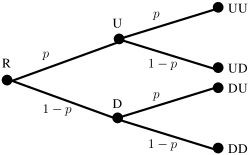

Example 2.1.

Consider the tree in Figure 1, with the elementary events . Consider the risk measure given by

where contains two probability measures, one corresponding to , and the other to . Clearly, all correspond to coherent risk measures. For the random cost such that , and , we have , and . Therefore, is deemed strictly riskier than a deterministic cost in all states of nature at time , but nonetheless is deemed riskier than at time .

We note that there is nothing peculiar in the choices above, in that similar counterexamples can be constructed for any risk measures , even when the latter are comonotonic. Rather, the issue at play is the key feature distinguishing dynamic from static risk assessment, namely the consistency in the risk preference profile over time. This is summarized in the axiom444We note that there are several notions of time consistency in the literature (see Penner (2007); Acciaio and Penner (2011); Roorda and Schumacher (2007) for an in-depth discussion and comparison). The one we adopt here is closest in spirit to strong dynamic consistency, and seems to be the most widely accepted notion in the literature. of time (or dynamic) consistency, which asks that a dynamic risk measure should satisfy, for all and all ,

This is a requirement on the particular functional forms that can be considered for , which is typically violated by the naïve dynamic measures of Definition 2.2. A central result in the literature (Riedel, 2004; Artzner et al., 2007; Detlefsen and Scandolo, 2005; Roorda et al., 2005; Cheridito et al., 2006; Roorda and Schumacher, 2007; Penner, 2007; Föllmer and Penner, 2006; Ruszczyński, 2010) is the following theorem, stating that any consistent measure has a compositional representation in terms of one-period risk mappings.

Theorem 2.2.

Any dynamic risk measure that is time consistent can be written as

| (4) |

where are a set of single-period conditional risk mappings.

This leads us to define the second way of measuring dynamic risk on the scenario tree of Section 2.1, by means of composing risk measures.

Definition 2.3.

A set of mappings is said to be a time consistent (dynamic) risk measure if for any , where , and are risk measures, for any .

We say that is a time-consistent, coherent (comonotonic) risk measure if every is coherent (respectively, comonotonic), for any and .

Apart from being axiomatically justified, this compositional form has the advantage of allowing a recursive estimation of the risk, and an application of the Bellman optimality principle in optimization problems involving dynamic risk measures (Nilim and El Ghaoui, 2005; Iyengar, 2005; Ruszczynski and Shapiro, 2006a; Ruszczyński, 2010). This has lead to its adoption in actuarial science (Hardy and Wirch, 2004; Brazauskas et al., 2008), as well as in several recent papers that re-examine operational problems under coherent measures of risk (Ahmed et al., 2007; Choi et al., 2011).

The main downside of the compositional form is that it requires a specification of all the mappings , which furthermore no longer lends itself to an easy interpretation, particularly as seen from the perspective of time . In particular, even if corresponded to the same primitive risk measure , the overall compositional measure555Here and throughout the paper, we use the shorthand notation with the understanding that the elementary risk measure is applied in stages in a conditional fashion. would bear no immediate relation to . As an example, when , the overall corresponds to the so-called “iterated CTE” (Hardy and Wirch, 2004; Brazauskas et al., 2008; Roorda and Schumacher, 2007), which does not lend itself to the same simple interpretation as a single AVaR. Furthermore, practitioners often feel that the overall risk measure is overly conservative, since it composes what are already potentially conservative risk evaluations backwards in time – for instance, for the iterated TCE, one is taking tail conditional expectations of tail conditional expectations. This has been recognized informally in the literature by Roorda and Schumacher (2007, 2008), who propose new notions of time consistency that avoid the issue, but without establishing precisely whether or to what extent the conservatism is actually true. From a different perspective, it is not obvious how “close” a particular compositional measure is to a given inconsistent one, and how one could go about constructing the latter in a way that tightly approximates the former.

2.4 Main Problem Statement.

In this context, the goal of the present paper is to take the first step towards better understanding the tradeoffs between the two ways of measuring risk. More precisely, we consider dynamic risk as viewed from the perspective of time , and examine two potential metrics: a time-inconsistent (comonotonic) risk measure , and a time-consistent (comonotonic) risk measure . For two such metrics, we seek to address the following related problems.

Problem 1.

Given and , test whether

Problem 2.

Given , , find the smallest and such that

| (5a) | ||||

| (5b) | ||||

A satisfactory answer to Problem 1 would provide a test for whether one of the formulations is always over or under estimating risk as compared to the other. As we show, consistent measures obtained by iterating the same primitive measure do not necessarily over (or under) estimate risk as compared to , and this is true even when , the case considered in (Roorda and Schumacher, 2007, 2008). However, by composing with conditional expectation operators, one always obtains lower bounds to the static risk measurement under . For instance, and are both lower bounds to a given static evaluation by . By contrast, upper bounds are obtained only when composing with worst-case operators in the final periods of the horizon: e.g., is necessarily an upper bound for , but is not.

To understand the relevance of Problem 2, note that the minimal factors and satisfying (5a) and (5b), respectively, provide a compact notion of how closely can be approximated through lower or upper bounding consistent measures , respectively. Since, in practice, it may be far easier to elicit or estimate a single static risk measure , characterizing and computing and constitutes the first step towards constructing the time-consistent risk measure that is “closest” to a given . We note that a similar concept of inner and outer approximations by means of distortion risk measures appears in (Bertsimas and Brown, 2009). However, the goal and analysis there are quite different, since the question is to approximate a static risk measure by means of another static distortion risk measure.

In a different sense, the smallest could be used to scale up risk measurements according to in order to turn them into “safe” (i.e., conservative) estimates of measurements according to . Scaling risk assessments by particular factors is actually common practice in financial risk management: according to the rules set forth by the Basel Committee for banking regulation, banks are required to report the 10-day VaR calculated at level, which is then multiplied by a factor of 3 to provide the minimum capital requirement for regulatory purposes; the factor of 3 is meant to account for losses occurring beyond VaR, and also for potential model misspecification (see Chapter 5 of (Jorion, 2006)). Therefore, this usage of could integrate well with practice.

We conclude the section by a remark pertinent to the two problems and our analysis henceforth.

Remark 2.1.

On first sight, the requirement of non-negative in the text of Problem 2 might seem overly restrictive. However, note that, if we insisted on holding for any cost , and if were allowed to take both positive and negative values, then the questions in Problem 2 would be meaningless, in that no feasible values would exist satisfying (5a) or (5b). To this end, we are occasionally forced to make the assumption that the stochastic losses are non-negative. This is not too restrictive whenever a lower bound is available for . By using the cash-invariance property ([P2]) of the risk measures involved, one could reformulate the original question with regards to the random loss , which would be nonnegative. Furthermore, in specific applications (e.g., multi-period inventory management (Ahmed et al., 2007)), is the sum of intra-period costs that are always non-negative, so requiring to be nonnegative is quite sensible.

3 Bounds for Coherent and Comonotonic Risk Measures.

In this section, we seek appropriate answers to Problem 1 and Problem 2, with the end-goal of characterizing the tightest multiplicative approximation of a given inconsistent risk measure by means of lower (or upper) bounding consistent risk measures.

To keep the discussion compact and avoid repetitive arguments, we first treat an abstract setting of comparing two coherent measures on the same space of outcomes. The conditions that we derive will be quite general, since no further structure will be imposed on the two measures. Section 3.2 will then discuss in detail the comparison between a time-inconsistent, comonotonic risk measure and a consistent, comonotonic risk measure , deriving particular forms for the results and conditions. In Section 3.3, we derive the main technical result needed to obtain multiplicative bounds on inconsistent, comonotonic risk measures, which we then use in Section 3.2 to address the main problems of interest.

Consider a discrete probability space , and let be the space of all random variables on (isomorphic with ). On this space, we are interested in comparing two coherent risk measures given by polyhedral sets of measures, i.e.,

where are (bounded) polyhedra666Several of the results discussed here readily extend to arbitrary closed, convex sets of representing measures. We restrict attention to the polyhedral case since it captures the entire class of comonotonic risk measures, it is simpler to describe, and computationally advantageous, since evaluating the risk measure entails solving a linear program.. Our main focus is on (1) characterizing conditions such that , and (2) finding the smallest factor such that

In this context, the risk measure can be identified as the support function of the convex set , so that the following standard result in convex analysis (see, e.g., (Rockafellar, 1970, Corollary 13.1.1)) can be invoked to test whether one risk measure dominates the other.

Proposition 3.1.

The inequality holds if and only if .

The usefulness of the latter condition critically depends on the representation of the sets of measures . For instance, if are polytopes, the containment problem is co-NP-complete when is given by linear inequalities and is given by its extreme points, but it can be solved in polynomial time, by linear programming (LP), for all the other three possible cases (Freund and Orlin, 1985).

Proposition 3.1 also sheds light on the second question of interest, through the following corollary.

Corollary 3.1.

There does not exist any such that .

Proof.

Proof. For any , the condition is equivalent to . Since , the containment cannot hold for any . ∎∎

This result prompts the need to restrict the space of random losses considered. As suggested in Section 2.4, an eminently sensible choice is to take , which is always reasonable when a lower bound on the losses is available. This allows us to characterize the desired conditions by examining inclusions of down-monotone closures of the sets . To this end, we introduce the following two definitions (see Section 6.1 of the Appendix for more details and references).

Definition 3.1.

A non-empty set is said to be down-monotone if for any and any such that , we also have .

Definition 3.2.

The down-monotone closure of a set , denoted by , is the smallest down-monotone set containing , i.e.,

When restricting attention to nonnegative losses, one can readily show that a coherent risk measure can be obtained by evaluating the worst case over an extended set of generalized scenarios, given by the down-monotone closure of the original set. This is summarized in the following extension of representation Theorem 2.1.

Proposition 3.2.

Let be a coherent risk measure. Then,

| (6) |

Proof.

Proof. The inequality follows simply because . To prove the reverse, consider any and let be the maximizer of . By Definition 3.2, there exists such that . Then:

∎

In view of this result, one can readily show that testing whether a risk measurement dominates another can be done equivalently in terms of the down-monotone closures of the representing sets of measures, as stated in the next result.

Lemma 3.1.

The inequality holds if and only if .

Proof.

Figure 2 depicts examples of the sets and their down-monotone closures and , respectively. Note that the conditions provided by Lemma 3.1 hold for any cost , i.e., non-negativity is not needed; they may also be more efficient in practice than directly checking , in cases when a suitable representation is available for , but not for (Freund and Orlin, 1985).

By considering down-monotone closures and restricting to nonnegative losses, we can also address the second question of interest, namely retrieving the smallest scaling factor such that . The following result characterizes any such feasible .

Proposition 3.3.

The inequality holds for all if and only if .

Proof.

In view of this result, the minimal exactly corresponds to the smallest inflation of the down-monotone polytope that contains the down-monotone polytope . This identification leads to the following characterization of the optimal scaling factor.

Theorem 3.1.

Let denote the smallest value of such that .

-

1.

If , where , then

(7) -

2.

If , then is the smallest value such that the optimal value of the following bilinear program is at most zero:

(8)

Proof.

Proof. The first claim is a known result in combinatorial optimization – see Theorem 6.1 in the Appendix and Theorem 2 in (Goemans and Hall, 1996) for a complete proof.

To argue the second claim, note that the smallest can be obtained, by definition, as follows:

The first equality follows by strong LP duality applied to the maximization over , which always has a finite optimum since is bounded. The second equality follows by replacing the inner minimization with a maximization, switching the order of the maximizations, and eliminating the variables . ∎∎

The results in Theorem 3.1 give a direct connection between the problem of computing and the representations available for the sets and . More precisely,

-

•

If a polynomially-sized inequality description is available for , then can be obtained by solving the small number of LPs in (7). Every such LP essentially entails an evaluation of the risk measure , leading to an efficient overall procedure.

-

•

If a compact inequality representation is available for , then can be found by bisection search over , where in each step the bilinear program in (8) is solved. Since bilinear programs can be reformulated as integer programs (Horst and Tuy, 2003), for which powerful commercial solvers are available, this approach may lead to a scalable procedure, albeit not one with polynomial-time complexity.

Our observations concerning the complexity of testing are summarized in Table 1 below. When or have polynomially-sized vertex descriptions, the test simply requires checking containment for a finite set of points, and when has a polynomially-sized description, the results of Theorem 3.1 apply. We conjecture that all the remaining cases are NP-complete, but do not pursue a formal analysis in the present paper. Section 4.1 revisits the question of computational complexity in the context of comonotonic risk measures, and argues that the general containment problem is NP-hard.

| Poly | Poly | Poly | Poly | |

|---|---|---|---|---|

| Poly | P | P | P | P |

| Poly | P | |||

| Poly | P | P | P | P |

| Poly | P |

We conclude our general discussion by noting that the tightest scaling factor can also be used to directly re-examine the first question of interest, namely testing when a given coherent risk measure upper bounds another. This is formalized in the following corollary, which is a direct result of Lemma 3.1 and Proposition 3.3.

Corollary 3.2.

The inequality holds if and only if .

The latter result suggests that characterizing and computing the tightest scaling factor is instrumental in answering all questions relating to the approximation of a coherent risk measure by means of another. In particular, given and , by determining the scaling factors and , we can readily test domination and also approximate one measure by the other, as follows:

-

•

If , then .

-

•

If , then .

3.1 Tightest Time Consistent and Coherent Upper Bound.

The results and exposition in the prior section made no reference to the way in which the coherent risk measures were obtained, as long as the sets of representing measures were polyhedral. In this section, we discuss some of these results in the context of Section 2.4 – more precisely, we take as the time-inconsistent risk measure , while denotes the compositional measure .

Our goal is to show that, when is coherent, a complete characterization of the tightest possible uniform upper bound to is readily available, and is given by a popular construction in the literature (Epstein and Schneider, 2003; Roorda et al., 2005; Artzner et al., 2007; Shapiro, 2012). This not only yields the tightest possible factor , but also considerably simplifies the test , for any coherent .

The next proposition introduces this construction for an arbitrary coherent measure .

Proposition 3.4.

Consider a risk measure , and define the risk measure , where the mappings are given by

| (9) | ||||

| (10) |

Then, is a time-consistent, coherent risk measure, and .

As mentioned, this construction has already been considered in several papers in the literature, and several authors have recognized that it provides an upper bound to . It is known that is time-consistent, and has a representation of the form , where the set has a product or rectangular structure. Note that it is obtained by computing products of the sets of single-step conditional probabilities obtained by marginalization at each node in the tree. Furthermore, , and therefore (Epstein and Schneider, 2003; Roorda et al., 2005; Shapiro, 2012).

Theorem 3.2 (Example 2.1 Revisited.).

To understand the construction, consider again Example 2.1. The set yielding the inconsistent measure at the root node R is given by two probabilities, corresponding to and , i.e.,

The sets of conditional one-step probabilities corresponding to nodes U, D, and R are then:

This yields a set containing eight different probability measures, for all possible products of one-step measures chosen from . More precisely,

In this context, we claim that actually represents the tightest upper bound for , among all possible coherent and time-consistent upper bounds. This is formalized in the following result.

Lemma 3.2.

Consider any risk measure , and let be the corresponding risk measure obtained by the construction in Proposition 3.4. Also, consider any time-consistent, coherent risk measure , where are given by

for some closed and convex sets . Then, the following results hold:

-

1.

If , then

(11) -

2.

holds if and only if

(12)

Proof.

Proof. [1] Since is a coherent risk measure, it can always be written as . Furthermore, it is known that the set of representing measures is obtained by taking products of the sets (see, e.g., Roorda et al. (2005) or Föllmer and Schied (2004)). Due to this property, is closed under the operation of taking marginals and computing the product of the resulting sets of conditional one-step measures (Epstein and Schneider, 2003; Roorda et al., 2005; Artzner et al., 2007), i.e.,

| (13) |

Since , we must have . But then, from (10) and (13), we obtain that . This readily implies that , and hence . The inequality for the multiplicative factors follows from the definition.

[2] For the second result, note that the “” implication has already been proved in the first part. The reverse direction follows trivially since implies that , and, since , we have . ∎∎

The result above is useful in several ways. First, it suggests that the tightest time-consistent, coherent upper bound for a given is . This not only yields the smallest possible multiplicative factor , but the upper-bound is uniform, i.e., for any loss . Also, is a lower bound on the best possible when the consistent measures are further constrained, e.g., to be comonotonic.

The conditions (13) also prescribe a different way of testing , by examining several smaller-dimensional tests involving the sets . This will also prove relevant in our subsequent analysis of the case of comonotonic risk measures.

3.2 The Comonotonic Case.

The results introduced in Section 3 and Section 3.1 become more specific when the risk measures and are further restricted to be comonotonic. We discuss a model with , but the approach and results readily extend to a finite number of time periods, a case which we revisit in Section 3.4.

We start by characterizing , with its set of representing measures and its down closure . The central result here, formalized in the next proposition, is the identification of with the base polytope corresponding to a particular Choquet capacity . This analogy proves very useful in our analysis, since it allows stating all properties of by employing known results for base polytopes of polymatroid rank functions777We note that, with the exception of the normalization requirement that is unimportant for analyzing fundamental structural properties, the definition of a Choquet capacity is identical to that of a rank function of a polymatroid (Fujishige, 2005, Chapter 2). Therefore, we use the two names interchangeably throughout the current paper., a concept studied extensively in combinatorial optimization (see Section 6.2 of the Appendix for all the results relevant to our treatment, and (Fujishige, 2005; Schrijver, 2003) for a comprehensive review).

Proposition 3.5.

Consider a naïve dynamic comonotonic risk measure , with . Then, there exists a Choquet capacity such that

-

1.

The set of measures is given by the base polytope corresponding to , i.e.,

(14) -

2.

The down-monotone closure of is given by the polymatroid corresponding to , i.e.,

(15)

Proof.

Proof. By Theorem 2.1 for comonotonic risk measures, there exists a Choquet capacity such that . Since , this set can be rewritten equivalently as the base polytope corresponding to (also refer to Corollary 6.1 of the Appendix for the argument that ). For the second claim, we can invoke a classical result in combinatorial optimization, that the downward monotone closure of the base polytope is exactly given by the polymatroid corresponding to the rank function , i.e., (see Theorem 6.3 in Section 6.2). ∎∎

In particular, both sets and are polytopes contained in the non-negative orthant, and generally described by exponentially many inequalities, one for each subset of the ground set . However, evaluating the risk measure for a given can be done in time polynomial in , by a simple Greedy procedure (see Theorem 6.4 in the Appendix or Lemma 4.92 in (Föllmer and Schied, 2004)).

In view of the results in Section 3.1, one may also seek a characterization of the tightest upper bound to , i.e., , or of its set of representing measures . Unfortunately, this seems quite difficult for general Choquet capacities – a particular case when it is possible is when is given by , a case discussed in our companion paper Huang et al. (2012). However, the result in Lemma 3.2 nonetheless proves useful for several of the results in this section.

The following result provides a characterization for the time-consistent and comonotonic risk measure as a coherent risk measure, by describing its set of representing measures and its down-monotone closure .

Proposition 3.6.

Consider a two-period consistent, comonotonic risk measure , where . Then,

-

1.

There exists such that .

-

2.

The set of measures is given by

where and are Choquet capacities, and are the base polytopes corresponding to and , respectively.

-

3.

The downward monotone closure of is given by

where and are the polymatroids associated with and , respectively.

Proof.

As expected, the set of product measures and its down-monotone closure have a more complicated structure than and , respectively. However, they remain polyhedral sets, characterized by the base polytopes and polymatroids associated with particular Choquet capacities and . The inequality descriptions of and involve exponentially many constraints, but evaluating at a given can still be done in time polynomial in , by using the Greedy procedure suggested in Theorem 6.4 in a recursive manner.

Because and are polytopes, they can also be described in terms of their extreme points. The description of the vertices of polymatroids and base polytopes has been studied extensively in combinatorial optimization (see Theorem 6.5 in the Appendix or (Schrijver, 2003) for details). Here, we apply the result for the case of , and extend it to the special structure of the set .

Proposition 3.7.

Consider two risk measures and , as given by Proposition 3.5 and Proposition 3.6. Then,

-

1.

The extreme points of are given by

where is any permutation of the elements of .

-

2.

The extreme points of are given by

where is any permutation of the elements of , and is any permutation of the elements of (for each ).

Proof.

Proof. Part (1) follows directly from the well-known characterization of the extreme points of an extended polymatroid, summarized in Theorem 6.5.

Part (2) follows by a repeated application of Theorem 6.5 to both and in the description of of Proposition 3.6. In particular, any value of can be expressed as a convex combination of the extreme points of such that for appropriate . Now, for each the value can be similarly expressed as a convex combination of the extreme points for an appropriate set of convex weights , such that

The proposition then follows directly from the fact that are themselves convex combination coefficients, and are extreme points. ∎∎

3.3 Computing the Optimal Bounds and .

With the representations provided above, we now derive our main technical result, establishing a method for computing the tightest multiplicative bounds for a pair of consistent and inconsistent comonotonic risk measures. The following theorem summarizes the result.

Theorem 3.3.

For any pair of risk measures and as introduced in Section 3.2,

| (16) | ||||

| (17) |

Furthermore, the value for remains the same if the outer maximization over is done over or , and corresponding statements hold for .

Proof.

Proof. To prove the first result, recall from Proposition 3.3 that for any ,

Consider an arbitrary . Any feasible scaling must satisfy that . Using the representation for in Proposition 3.6, this condition yields

The second set of constraints implies that any feasible satisfies . Corroborated with the first set of constraints, this yields

Since this must be true for any , the smallest possible is given by maximizing the expression above over , which leads to the result (16).

The expression for is a direct application of the second part of Theorem 3.1, by identifying with and using the compact representation for from Proposition 3.5.

The claim concerning the alternative sets follows by recognizing that the function maximized is always nondecreasing in the components of , so that can be replaced with , and it is also convex in , hence reaching its maximum at the extreme points of the feasible set. ∎∎

From Theorem 3.3, it can readily seen that, when , the optimal will always be at least , and can be whenever the dimension of the polytope is strictly smaller than that of . Similarly, when , the optimal is always at least , and can be when the dimension of the polytope is smaller than . To avoid the cases of unbounded optimal scaling factors, one can make the following assumption about the Choquet capacities.

Assumption 3.1 (Relevance).

This ensures that both risk measures consider all possible outcomes in the scenario tree, and is in line with the original requirement of relevance in (Artzner et al., 1999), which states that, for any random cost such that and , any risk measure should satisfy . In this case, the polytopes and are both full-dimensional (see (Balas and Fischetti, 1996) and Appendix A), which leads to finite minimal scalings.

As suggested in our general exposition at the beginning of Section 3, determining the optimal scaling factors and also leads to direct conditions for determining whether lower bounds or viceversa. The following corollary states these in terms of optimization problems.

Corollary 3.3.

For any pair of risk measures and as introduced in Section 3.2,

-

1.

The inequality holds if and only if

-

2.

The inequality holds if and only if

Proof.

The results in Corollary 3.3 are stated in terms of non-trivial optimization problems. It is also possible to write out the conditions in a combinatorial fashion, using the analytical description of the extreme points of and , as summarized in the following corollary.

Corollary 3.4.

For any pair of risk measures and as introduced in Section 3.2,

-

1.

The inequality holds if and only if

where denotes any permutation of the elements of , and for any .

-

2.

The inequality holds if and only if

Proof.

Proof. The proof is slightly technical, so we defer it to Section 6.3 of the Appendix. ∎∎

The above conditions are explicit, and can always be checked when oracles are available for evaluating the relevant Choquet capacities. The main shortcoming of that approach is that the number of conditions to test is generally exponential in the size of the problem, even for a fixed : for , and for , respectively, where . However, under additional assumptions on the Choquet capacities or the risk measures, it is possible to derive particularly simple polynomially-sized tests. We refer the interested reader to the discussion in Section 4.1 and the example in Section 4.3.

We note that the reason the conditions for take a decoupled form and result in a smaller overall number of inequalities is directly related to the results of Lemma 3.2, which argues that testing can be done by separately examining conditions at each node of the scenario tree.

3.4 Multi-stage Extensions.

Although we focused our discussion thus far on a setting with , the ideas can be readily extended to an arbitrary, finite number of periods. We briefly outline the most relevant results in this section, but omit including the proofs, which are completely analogous to those for .

In a setting with general , our goal is to compare a comonotonic with a time-consistent, comonotonic . The former is exactly characterized by Proposition 3.5, while the representation for the latter can be summarized in the following extension of Proposition 3.6.

Proposition 3.8.

Consider a time-consistent, comonotonic risk measure . Then,

-

1.

There exists such that .

-

2.

The set of measures is given by

(18) where are Choquet capacities with corresponding base polytopes , for every and for every .

-

3.

The downward monotone closure of is obtained by replacing with and with the polymatroid in equation (18).

The proof exactly parallels that of Proposition 3.6, and is omitted due to space considerations. With this result, we can now extend our main characterization in Theorem 3.3 for the optimal multiplicative factors to a multi-period setting, as follows.

Theorem 3.4.

For any comonotonic measure and time-consistent comonotonic measure ,

| (19) |

where , and . Also,

| (20) |

Furthermore, the value for would remain the same if the outer maximization were taken over or . Corresponding statements hold for .

The proof follows analogously to that of Theorem 3.3, by using the expressions for and provided by Proposition 3.5 and Proposition 3.8, respectively, to analyze the conditions or vice-versa. We omit it for brevity.

By comparing (22) and (20) with their two-period analogues in (16) and (17), respectively, it is interesting to note that the complexity of the formulation for remains the same, while the optimization problems yielding get considerably more intricate. Section 4 contains a detailed analysis of the computational complexity surrounding these problems.

For completeness, we remark that direct multi-period counterparts for Corollary 3.3 and Corollary 3.4 can be obtained, by recognizing that is equivalent to , and by using the results in Theorem 3.4 and Lemma 3.2 to simplify the latter conditions. We do not include these extensions due to space considerations.

4 Discussion of the Results.

In view of the results in the previous section, several natural questions emerge. What is the computational complexity of determining the optimal scaling factors and for coherent/comonotonic risk measures? If this is generally hard, are there special cases that are easy, i.e., admitting polynomial-time algorithms? What examples of time-consistent risk measures can be derived starting with a given , and how closely do they approximate the original measure?

The goal of the present section is to address these questions in detail. As we argue in Section 4.1, computing the scaling factors is hard even when restricting attention to distortion risk measures – a proper subclass of comonotonic measures. However, several relevant cases are nonetheless tractable. Section 4.2 introduces examples obtained by composing with the conditional expectation operator “” or conditional worst-case operator “”, and compares them in terms of their approximation strength. Section 4.3 then summarizes the case when and correspond to the AVaR risk measure, and shows how many of the results drastically simplify.

4.1 Computational Complexity.

As argued in Section 3, computing the optimal scaling factors and entails solving the optimization problems in (16) and (17). We now show that this is NP hard even for a problem with , and even when only examining distortion risk measures. We use a reduction from the SUBSET-SUM problem, which is NP hard (Cormen et al., 2001) and is defined as follows.

Definition 4.1 (SUBSET-SUM).

Given a set of integers , is there a subset that sums to ?

This following result is instrumental in showing the complexity of computing the optimal scalings and .

Theorem 4.1.

Consider two arbitrary distortion risk measures . Then, it is NP-hard to decide if , for any . The problem remains NP-hard even when , for all .

Proof.

Proof. We use the representation of distortion risk measures to show the reduction from the SUBSET-SUM problem. By the representation Theorem 2.1 written for the specific case of distortion measures yields, , where

and , where are concave, increasing functions satisfying . Because both and are polymatroids and downward monotone, the second result in Theorem 3.3 can be further simplified to:

| (21) |

Now, consider a SUBSET-SUM problem with values and a value such that , where . Construct the functions and as follows:

Since both , satisfy the conditions of distortion risk measures, any SUBSET-SUM problem can be reduced to the problem of computing the optimal scale of two distortion risk measures.

Now, the optimal value of (21) is upper bounded as:

The maximum is achieved when there exists such that . To show this, consider as a function of . This function is: (1) non-decreasing on the interval and non-increasing on the interval , (2) strictly greater than one for , (3) equal to 1 for , and (4) continuous. Therefore, the SUBSET-SUM problem has a subset that sums to if and only if the optimal value of (21) is . Finally, the result also holds when , since our choice already has for all , which implies . ∎∎

The complexity of computing the optimal scalings and readily follows as a direct corollary of Theorem 4.1.

Corollary 4.1.

Under a fixed and for any given , it is NP-complete to decide whether for an arbitrary inconsistent distortion measure and a consistent distortion measure . The result remains true even when and are such that for all . Similarly, it is NP-complete to decide whether , and the result remains true even when .

Proof.

Proof. First, note that finding the scaling factors for any is at least as hard as for . This can be seen by setting for all . The NP-hardness then follows from Theorem 4.1 by setting and . The membership in NP follows by checking the inequality (16) for every extreme point , subset , and the appropriate subsets . The second result follows analogously.∎∎

Corollary 4.1 argues that computing the optimal scaling factors for arbitrary distortion risk measures cannot be done in polynomial time. While the NP-hardness may be somewhat disappointing, solving the two optimization problems in Theorem 3.3 is nonetheless clearly preferable to simply examining all possible values of .

While the problem of computing the scaling factors is hard for general distortion measures, polynomial-time algorithms are possible when the representations of or fall in the tractable cases discussed in Table 1 of Section 3.

In fact, some of the results of Table 1 can even be strengthened - one such case is when a vertex description for the polytope is available, and problem (22) can be solved in time polynomial in , under oracle access to the Choquet capacities yielding the measure .

Lemma 4.1.

If the polytope is specified by a polynomial number of extreme points, then can be computed in time polynomial in .

Proof.

Proof. Consider the specialization of (22) for a fixed :

| (22) |

where , and .

Note that each value and also can be written as:

For any , the constraint can be checked in polynomial time, since the set function on the left-hand side is submodular in , and can be minimized with a polynomial number of function evaluations (Schrijver, 2003). ∎∎

The result above is slightly stronger than what Table 1 suggests, since the representation of can still be exponential both in terms of extreme points and vertices, as long as oracle access to is available.

4.2 Examples.

To see how our results can be used to examine the tightness of particular dynamically consistent risk measures, we now consider several constructions suggested in the literature. The starting point is typically a single distortion risk measure , denoting the inconsistent evaluation. This is then composed with other suitable measures (for instance, with itself, with the conditional expectation and/or the conditional worst-case operator), to obtain time-consistent risk measures that are derived from . The questions we would like to address here is which of these measures lower-bound or upper-bound the inconsistent evaluation , and what can be said about the relative tightness of the various formulations.

In order to construct dynamically-consistent measures by composing , we must first specify the conditional one-step risk mappings corresponding to , formally denoted by and . When is a distortion risk measure, this can be done in a natural way in terms of the corresponding concave distortion function. To this end, recall that, by the representation Theorem 2.1, any distortion measure is uniquely specified by the concave function yielding its set of representing measures, through the Choquet capacity . The conditional one-step risk mappings and are then obtained by applying the same distortion function to suitable conditional probabilities. More precisely, and are the distortion risk measures corresponding to the Choquet capacities:

The conditional risk mappings and can be used to define dynamic time-consistent risk measures, either alone or by composition with other conditional risk mappings. In particular, all of the following dynamic time-consistent risk measures have been considered in the literature:

where denotes the conditional expectation operator, and is the conditional worst-case operator. Whenever the meaning is clear from context, we sometimes omit the time-subscript, and use shorthand notation such as , , etc., although we are formally referring to compositions with and/or .

4.2.1 Time-Consistent Lower Bounds Derived From a Given .

We begin by discussing two choices for lower-bounding consistent risk measures derived from . The following proposition formally establishes the first relevant result.

Proposition 4.1.

Consider any distortion risk measure , and the time-consistent, comonotonic measures and . Then, for any cost ,

Proof.

This is not a surprising result, since the operator is known to be a uniform lower bound for any static coherent risk measure (Föllmer and Schied, 2004). We confirm that the same remains true in dynamic settings, provided that the risk measure is applied in a single time step, and conditional expectation operators are applied in other stages.

Since both and are lower bounds for , a natural question is whether one provides a “better” approximation than the other. More precisely, the following are questions of interest:

-

1.

For a given , is it true that (or vice-versa)?

-

2.

Is it true that for any distortion measure (or vice-versa)?

Clearly, a positive answer to the first question would provide a very strong sense of tightness of approximation. However, as the following example shows, neither inequality holds in general.

Example 4.1.

Consider a scenario tree with , , under uniform reference measure. Introduce the following two random costs (specified as vectors in ):

With , and , it can be checked that , while .

Insofar as the second question is concerned, we note that it can always be answered for a specific distortion measure , by calculating the optimal scalings, so that it really makes sense when posed for all risk measures. Unfortunately, our computational experiments show that counterexamples can be constructed for this claim, as well, and that any one of the scaling factors can be better than the other. However, it would be very interesting to characterize conditions (on the risk measures, the underlying probability space, or otherwise) under which a particular compositional form always results in a smaller scaling factor. The following result, which we prove in the Appendix, is a potential first step in this direction, suggesting that the two lower bounds can result in equal tightness of approximation in certain cases of interest.

Theorem 4.2.

Consider a uniform scenario tree, i.e., , under a uniform reference measure. Then, for any distortion risk measure , we have

4.2.2 Time-Consistent Upper Bounds Derived From a Given .

In an analogous fashion to the previous discussion, one can ask what time-consistent upper bounds can be derived from a distortion measure . In particular, a natural supposition, analogous to the results of Section 4.2.1, may be that and are upper bounds to , since is the most conservative risk mapping possible (Föllmer and Schied, 2004). The following result shows that, unlike in the lower bound setting, only one of the two composed measures is a valid upper bound.

Proposition 4.2.

Consider any distortion risk measure , and the time-consistent, comonotonic measures and , where denotes the conditional worst-case operator. Then:

-

(i)

For any cost , .

-

(ii)

There exists a choice of and of random costs such that and .

Proof.

Proof. The proof for Part (i) entails checking the conditions of Corollary 3.4. Since it is rather technical in nature, we leave it for Section 6.3 of the Appendix of the paper.

To show Part (ii), consider a uniform scenario tree with , and let the reference measure be . For simplicity, assume the first two components of correspond to nodes in the same child. Then, for the risk measure , and the costs and , it can be checked that , but . ∎∎

The result in Proposition 4.2 also suggests that upper bounds to can be derived by composing with more conservative mappings in later time periods. This intuition is sharpened in Section 4.3 and our companion paper (Huang et al., 2012), which show that, when , all upper bounds of the form must have , and, in many practical settings, , i.e., worst-case as the second-stage evaluation.

Since is an upper bound for a given , one can also turn to the question of comparing the resulting scaling factor with the factors of the previous section, namely or . Our computational tests show that there is no general relation between these, even when the scenario tree and the reference measure are uniform, a claim due to the following result, whose proof is included in the paper’s Appendix.

Proposition 4.3.

Consider a uniform scenario tree, i.e., , under a uniform reference measure. Then, for any distortion risk measure , we have

Corroborating this result with the expression in Theorem 4.2 for , one can readily find simple examples of distortions such that either the latter or the former scaling factor is smaller.

An opinion often held among practitioners, and informally argued in the literature (Roorda and Schumacher, 2007, 2008) is that composing a risk measure with itself would compound the losses, resulting in a larger evaluation of risk, i.e., that should over-bound . For instance, if – the case considered in (Roorda and Schumacher, 2007) – the compositional measure corresponds to the so-called “iterated tail-CTE”, which takes tail conditional expectations of quantities that are already tail conditional expectations. We show by means of an example that this informal belief is actually not true, even in the case of AVaR.

Example 4.2 (Iterated AVaR).

Consider a uniform scenario tree (i.e., ), and a uniform reference measure. Furthermore, consider the risk measure , and the following two costs (specified as real vectors in , with components split in the four sub-trees of stage ):

When , it can be readily checked888For the case of discrete probability measures, one has to be careful in defining , since it is no longer exactly given by the conditional expectation of the loss exceeding . The precise concepts are presented and discussed at length in (Rockafellar and Uryasev, 2002), which we follow here. that , while .

The example shows that the iterated AVaR is neither an upper nor a lower bound to the static AVaR. We direct the interested reader to our companion paper (Huang et al., 2012), which is focused specifically on the AVaR case, and discusses the exact necessary and sufficient conditions for when one of the two dominates the other.

4.2.3 The Tightest Possible Time-Consistent Upper-bound.

A natural time-consistent upper bound to a given is the measure , obtained by the rectangularization procedure in Proposition 3.4. It is the tightest possible coherent upper bound to , both in a uniform and multiplicative-alpha sense. The main potential drawback in using is that it may not satisfy additional axiomatic properties, and it typically bears no interpretation in terms of . For instance, starting with a comonotonic does not generally result in a comonotonic , and is usually not given by compositions of one-step risk measures that correspond to . Determining conditions that guarantee the latter two properties is an interesting question, which we do not pursue further in the present paper. However, we note that this is possible in at least one case of practical interest: when , one can show that always corresponds to a composition of one-step AVaR measures, at appropriate levels – see our discussion in Section 4.3 and the detailed treatment in our companion paper (Huang et al., 2012).

For completeness, we also note that the ordering relation between the scaling factor and scalings derived from lower-bounding measures is generally not obvious: our computational experiments suggest that either one could dominate the other. However, more can be said in particular settings, such as the case of AVaR, which we discuss next.

4.3 The Case of AVaR.

In this section, we discuss how several of the results introduced throughout the paper can be considerably simplified when the risk measures in question correspond to AVaR. In particular, analytical expressions or polynomial-time procedures can be derived for computing and and for testing or viceversa. Furthermore, one can consider designing the risk measures that provide the tightest possible lower or upper approximations to a given .

The case is discussed at length in our companion paper (Huang et al., 2012), to which we direct the interested reader for any technical details and proofs. Our goal for the remainder of the section is to outline the main results, and briefly discuss the implications.

To start, we consider a uniform scenario tree under uniform reference measure (, and ), and the following choice of risk measures:

| (23a) | |||||

| (23b) | |||||

Note that the restriction on and is without loss of generality, since with is identical to the worst-case risk measure, rendering the case analogous to .

In this setup, we can revisit our main results in Theorem 3.3, and provide the following expressions for the tightest factors and for the case .

Theorem 4.3.

Note that the above result has several immediate implications. First, it readily allows checking whether (or vice-versa), since the latter conditions are equivalent to (respectively, ). This leads to the following simple tests.

Corollary 4.2.

The latter result confirms the observation in Example 4.2 that the iterated AVaR, i.e., , is generally neither an upper nor a lower bound to the inconsistent choice . By (26), is always a feasible option, but one must take . In fact, as argued in (Huang et al., 2012), most relevant choices of would actually lead to taking , i.e., the worst-case operator in the second stage.

The analytical results above can also be used to optimally design the compositional risk measure that is the tightest approximation to a given . More precisely, one can characterize the choice of (i.e., levels ) that results in the smallest possible factor among all compositional AVaR that are lower bounds for , and, similarly, the values yielding the smallest possible among all upper-bounding compositional AVaRs. The optimal choices satisfy several interesting properties:

-

•

for values of that are common in financial applications, i.e., satisfying (Jorion, 2006), the optimal is obtained by taking , corresponding to an iterated AVaR measure.

-

•

the optimal requires choosing and . Typical values of used in practice would entail , i.e., the worst-case scenario in the second stage.

-

•

the optimally designed is always smaller than , i.e., for every and , which suggests that starting with an under-estimating results in tighter dynamically consistent approximations for AVaR.

The results discussed in Theorem 4.3 for can also be (partially) extended to a case of an arbitrary , which is summarized in the following claim.

Theorem 4.4.

It is interesting to note that computing , and hence also testing , remains as easy for general as for : an analytical expression is available, which actually holds in considerably more general settings (arbitrary tree and reference measure). By contrast, computing and testing now requires an algorithm that is polynomial only for a fixed . In light of our earlier result, this suggests that, although starting with lower-bounds for may lead to a tighter approximating , the gain does not come for free, as the computation of the resulting is typically harder than that for .

In a multiperiod setting, the question of designing the tightest possible lower-bounding approximation to a given becomes harder – even computing one scaling factor requires a polynomial-time algorithm. By contrast, a complete characterization of the tightest upper-bound is available! Quite surprisingly, it turns out that this choice exactly corresponds to the risk measure introduced by the construction in Proposition 3.4, by expanding the set of measures of . This is summarized in the following result (for a proof, see (Huang et al., 2012)).

Theorem 4.5.

Consider the risk measure , under an arbitrary reference measure , and the construction for the risk measure characterized in Proposition 3.4. Then, , where , and

Here, , and is computed under the conditional probability induced by , i.e., .

This result, which holds under any reference measure , suggests that starting with and expanding its set of representing probability measures until it becomes rectangular exactly results in a risk measure that is a composition of one-step AVaRs. These one-step AVaRs are computed under levels that can be different at each node in the tree, and under the natural conditional probability induced by the reference measure .

There are several immediate implications. First, since is the tightest possible coherent upper-bound for any given coherent (see Lemma 3.2), this implies that the tightest possible choice for a compositional AVaR that upper bounds a given is exactly . In a different sense, this also provides an instance when starting with a comonotonic (in fact, distortion) risk measure results in a comonotonic (distortion) risk measure , which furthermore belongs to the same class as .

Lastly, the theorem confirms that the best possible compositional AVaR that upper bounds does involve compositions with the worst-case operator, in any node that has probability at most . Furthermore, it suggests, in a precise sense, that the compositional AVaR gets increasingly conservative as the risk measurement process proceeds in time: note that , and once node requires a worst-case operator, so will any descendant of , since . In particular, all future stages are more conservative than the measurement at time (i.e., the root node), which exactly corresponds to the inconsistent evaluation .

This last point may be of particular relevance when designing risk measures for use in dynamic financial settings: it suggests that regulators looking for safe counterparts (i.e., upper-bounds) for a static should use risk measurement processes that are compositions of increasingly conservative measurements.

5 Conclusions.

In this paper, we examined two different paradigms for measuring risk in dynamic settings: a time-consistent formulation, whereby the risk assessments are designed so as to avoid naïve reversals of preferences in the measurement process, and a time-inconsistent one, which is easier to specify and calibrate from preference data. We discussed necessary and sufficient conditions under which one measurement uniformly bounds the other from above or below, and provided a notion of the multiplicative tightness with which one measure can be approximated by the other. We also showed that it is generally hard to compute the scaling factors even for distortion risk measures, but provided concrete examples when polynomial-time algorithms are possible.

6 Appendix

6.1 Submissives, Downward Monotone Closures and Anti-blocking Polyhedra.

In the current section, we discuss the important notion of the down monotone closure of a polytope, also known as its anti-blocking polyhedron or its submissive. Our exposition mostly follows Chapter 9 in Schrijver (2000), to which we direct the interested reader for a more comprehensive treatment and references to related literature.

A polyhedron in is said to be down-monotone or of anti-blocking type if