Model-independent Bounds for Option Prices:

A Mass Transport Approach

Abstract.

In this paper we investigate model-independent bounds for exotic options written on a risky asset using infinite-dimensional linear programming methods. Based on arguments from the theory of Monge-Kantorovich mass-transport we establish a dual version of the problem that has a natural financial interpretation in terms of semi-static hedging. In particular we prove that there is no duality gap.

Keywords model-independent pricing, Monge-Kantorovich optimal transport, robust super-replication theorem

Mathematics Subject Classification (2010) 91G20, 91G80

JEL Classification C61, G13

P. Henry-Labordère, Global Markets Quantitative Research, Société Générale, pierre.henry-labordere@sgcib.com

F. Penkner, University of Vienna, Department of Mathematics, friedrich.penkner@univie.ac.at

The first author thanks the FWF for support through project p21209.

1. Introduction

Since the introduction of the Black-Scholes paradigm, several alternative models which allow to capture the risk of exotic options have emerged: stochastic volatility models, local volatility models, jump-diffusion models, mixed local stochastic volatility models. These models depend on various parameters which can be calibrated more or less accurately to market prices of liquid options (such as vanilla options). This calibration procedure does not uniquely set the dynamics of forward prices which are only required to be (local) martingales according to the no-arbitrage framework. This could lead to a wide range of prices of a given exotic option when evaluated using different models calibrated to the same market data.

In practice, it would be interesting to know lower and upper bounds for exotic options produced by models calibrated to the same market data, and therefore with similar marginals. If bounds are tight enough, they would be used to detect the possibility of arbitrage in market prices, provided these bounds have an interpretation as investment strategies. This problem has already been studied in the case of exotic options written on multi-assets observed at the same time [BP02, CDDV08, HLW05a, HLW05b, LW05, LW04]. Within the class of models with fixed marginals at , the search for lower/upper bounds involves infinite-dimensional linear programming issues. Analytical expressions have been obtained in the case of basket options [LW05, LW04]. These correspond to the determination of optimal copulas. In practice, these bounds are not tight as the information of marginals is not restrictive enough.

Here we focus on multi-period models and general path-dependent options. This problem is more involved as we have to impose that the asset price is a discrete time martingale111For the sake of simplicity, we assume zero interest rate and no cash/yield dividends. This assumption can be relaxed by considering the process introduced in [HL09] (see equation 14) which has the property to be a local martingale. satisfying marginal restrictions. We review the existing literature on the subject in Section 1.6 below.

In our setting the problem of determining the interval of consistent prices of a given exotic option can be cast as a (primal) infinite-dimensional linear programming problem. We propose a dual problem that has a practically relevant interpretation in terms of trading strategies and prove that there is no duality gap under rather mild regularity assumptions.

1.1. Setting

In the following, we fix an exotic option depending only on the value of a single asset at discrete times and denote by its payoff, where we suppose to be some measurable function. In the no-arbitrage framework, the standard approach is to postulate a model, that is, a probability measure on under which the coordinate process

is required to be a (discrete) martingale in its own filtration. By we denote the current spot price. The fair value of is then given as the expectation of the payoff

Additionally, we impose that our model is calibrated to a continuum of call options with payoffs at each date and price

| (1) |

Plainly (1) is tantamount to prescribing probability measures on the real line222The cumulative distribution function of can be read off the call prices through for . Concerning the mathematical finance application it would be sufficient to consider strikes and marginals which are concentrated on the positive half-line. We prefer to go with the more general case since the proofs are not more complicated. A technical difference is that call prices satisfy only rather than the simpler in the case where is assumed to be non-negative. such that the one dimensional marginals of satisfy

1.2. Primal formulation

For further reference, we denote by the set of all martingale measures on (the pathspace) having marginals and mean . Equivalently, we have if and only if for and for all and .

Following the tradition customary in the optimal transport literature we concentrate on the lower bound and consider the primal problem

| (2) |

1.3. Dual formulation

The dual formulation corresponds to the construction of a semi-static subhedging strategy consisting of the sum of a static vanilla portfolio and a delta strategy.333Similar strategies are considered in [DH07, Cou07] where they are used to subreplicate a European option based on finitely many given call options. More precisely, we are interested in payoffs of the form

| (3) |

where the functions are -integrable () and the functions are assumed to be bounded measurable ().444It might be expected that the delta strategy in (3) should also include a constant multiplier of corresponding to an initial forward position. However this term is not necessary as it can be subsumed into the term .

If these functions lead to a strategy which is subhedging in the sense

we have for every pricing measure the obvious inequality

| (4) |

This leads us to consider the dual problem

| (5) |

which, by (4), satisfies

| (6) |

1.4. Semi-static subhedging

The dual formulation corresponds to the construction of a semi-static subhedging portfolio consisting of static vanilla options and investments in the risky asset according to the self-financing trading strategy

We note the financial interpretation of inequality (6): suppose somebody offers the option at a price . Then there exists with with price strictly larger than . Buying and going short in , the arbitrage can be locked in.

The crucial question is of course if (6) is sharp, i.e. if every option priced below allows for an arbitrage by means of semi-static subhedging. In Theorem 1 below we show that this is the case under relatively mild assumptions.

Of course it is a classical theme of Mathematical Finance that the extremal martingale prices of a financial derivative correspond to the minimal or maximal initial capital necessary for sub-/super-replication, respectively. This is precisely the replication theorem of mathematical finance, which is a corollary of the fundamental theorem of asset pricing. The novelty of our contribution is that we establish a robust, model-free version of this result.

1.5. Main result

Theorem 1.

Assume that are Borel probability measures on such that is non-empty. Let be a lower semi-continuous function such that

| (7) |

on for some constant . Then there is no duality gap, i.e. . Moreover, the primal value is attained, i.e. there exists a martingale measure such that .

The dual supremum is in general not attained (cf. Proposition 4.1 below).

Our approach to this result is based on the duality theory of optimal transport which is briefly introduced in Section 2; the actual proof will be given in Section 3 with the help of the Min-Max Theorem of decision theory. We conclude this introductory section by a short discussion of the content of Theorem 1.

The assumption excludes the degenerate case in which no calibrated market model exists. For the existence of a martingale measure having marginals it is necessary and sufficient that these measures possess the same finite first moments and increase in the convex order, i.e. for each convex function (cf. [Str65]).555In more financial terms this means that is increasing in for each fixed .

Having the financial interpretation in mind, it is important that the value of the dual problem remains unchanged if a smaller set of subhedging strategies is used. In the proof of Theorem 1 we show that it is sufficient to consider functions which are linear combinations of finitely many call options (plus one position in the bond resp. the stock); at the same time can be taken to be continuous and bounded. This means that for every there exist , such that

| (8) |

and the corresponding price

| (9) |

is -close to the primal value .

Condition (7) could be somewhat relaxed. For instance it is sufficient to demand that the function is bounded from below by a sum of integrable functions. However, in this case it is necessary to allow for dual strategies that use European options beyond call options and we will not pursue this further.

We conclude this introductory section by noting that an upper bound for the price of the option can be given by means of semi-static superhedging. Applying Theorem 1 to the function we obtain that this bound is sharp:

Corollary 1.1.

Assume that are Borel probability measures on such that is non-empty. Let be an upper semi-continuous function such that

| (10) |

on for some constant . Then there is no duality gap

| (11) | ||||

| (12) |

The supremum is attained, i.e. there exists a maximizing martingale measure.

1.6. Comparison with previous results

The main novelty of our approach is that we apply the theory of optimal transport in mathematical finance, more specifically, to obtain robust model-independent bounds on option prices. A time-continuous analysis of the present connection between optimal transport and mathematical finance is contained in the parallel work to the present one by Galichon, Henry-Labordère, Touzi [GHLT11] (see also [HLSTO12]) where a stochastic control approach is used.

We point out that the problem of model independent pricing is classically approached in the literature by means of the Skorokhod embedding problem, see the informative survey paper by Hobson [Hob11]. Also the notion of semi-static hedges is well-established (see for instance [Hob11, Section 2.6]).

The problem of robust pricing in a multi-period setting has previously been studied in the case of specific exotic options. Hodges and Neuberger [NH00] are mainly interested in the case of Barrier options. Albrecher, Mayer and Schoutens produce an explicit bound (based on conditioning arguments) in the case of an Asian option in discrete time and give a feasible subreplicating strategy associated to it [AMS08]. The problem to explicitly give the optimal lower/upper bounds seems harder and remains open to the best of our knowledge. A numerical implementation of our dual approach in the Asian option setting is given in [HL11].

In the continuous-time setting, the problem has been treated for instance in the case of lookback options [Hob98], variance/volatility options [CL10, CW12, HK12] and double-(no) touch options [CO11b, CO11a]. These solutions are mainly based on Skorokhod-stopping techniques and differ from our approach also in that only the marginal at the maturity is incorporated. Extensions to the multi-marginal case are addressed in [BHR01, MY02, HP02, HLSTO12].

A result similar to our findings was recently proved for forward-start options by Hobson and Neuberger [HN12]. In the terminology of Corollary 1.1 they show that in the case where and the payoff function is given by

In contrast to our paper, their approach is more constructive and they obtain maximizers for the dual problem in particular cases. Here some care is needed in certain (pathological) situations, see Proposition 4.1 below.

2. Optimal Transport

In the usual theory of Monge-Kantorovich optimal transport666See [Vil03, Vil09] for an extensive account on the theory of optimal transportation. one considers two probability spaces , and the problem is to find a “cheap” way of transporting to . Following Kantorovich, a transport plan is formalized as probability measure on which has -marginal and -marginal .

We will come back to the two dimensional case in Section 4 below; for now we turn to the multidimensional version of the transport problem which will be the main tool in our proof of Theorem 1. Subsequently we consider probability measures on the real line777Most of the basic results are equally true for polish probability spaces , but we do not need this generality here. which have finite first moments. The set of transport plans consists of all Borel probability measures on with marginals . A cost function is a measurable function which is bounded from below in the sense that there exist -integrable functions , such that

| (13) |

where . Given a cost function and a transport plan the cost functional is defined as

| (14) |

Note that this integral is well defined (assuming possibly the value ) by (13). The primal Monge-Kantorovich problem is then to minimize over the set of all transport plans .

Given -integrable functions , , such that

| (15) |

we have for every transport plan

| (16) |

The dual part of the Monge-Kantorovich problem is to maximize the right hand side of (16) over a suitable class of functions satisfying (15).

Starting already with Kantorovich, there has been a long line of research on the question in which setting the optimal values of primal and dual problem agree, we refer the reader to [Vil09, p. 88f.] for an account of the history of the problem. For our intended application, we need to restrict the dual maximizers to functions in

i.e., we will employ the following Monge-Kantorovich duality theorem.

Proposition 2.1.

Let be a lower semi-continuous function satisfying

| (17) |

on for some constant and let be probability measures on having finite first moments. Then

The dual bound could be realized by holding a static position in European options with respective maturity date and payoff . This static portfolio with intrinsic value and market value subreplicates the payoff at maturity.

We postpone the proof of Proposition 2.1 to the Appendix and continue with our discussion.

The set of transport plans carries a natural topological structure: it is a compact convex subset of the space of finite (signed) Borel measures equipped with the weak topology induced by the bounded continuous functions . (Compactness of is essentially a consequence of Prokhorov’s theorem, for a proof we refer the reader to [Vil09, Lemma 4.4].)

Subsequently we want to study the set of transport plans which are also martingales. Therefore we will assume from now on that the measures are increasing in the convex order such that is a non-empty subset of . It will be crucial for our purposes that also is compact in the weak topology. To establish this we need two auxiliary lemmas.

Lemma 2.2.

Let be continuous and assume that there exists a constant such that

for all . Then the mapping

is continuous on

Proof.

Since we assume that have finite first moments, converges to uniformly in as . ∎

Lemma 2.3.

Let . Then the following are equivalent.

-

(1)

.

-

(2)

For and for every continuous bounded function we have

Proof.

Plainly, (1) asserts that whenever , is Borel measurable, then

Using standard approximation techniques one obtains that this is equivalent to (2). ∎

Proposition 2.4.

The set is compact in the weak topology.

3. Proof of Theorem 1

Our argument combines a Monge-Kantorovich duality theorem (in the form of Proposition 2.1) with the following Min-Max theorem of decision theory which we cite here from [Str85, Thm. 45.8] (another reference is [AH96, Thm. 2.4.1]).

Theorem 2.

Let be convex subsets of vector spaces resp. , where is locally convex and let . If

-

(1)

is compact,

-

(2)

is continuous and convex on for every ,

-

(3)

is concave on for every

then

of Theorem 1..

As we want to show that the subhedging portfolios can be formed using just call options, we will restrict ourselves to dual candidates satisfying (and ).

If the assertion of Theorem 1 holds true for a function and if then the assertion carries over to Therefore we may assume without loss of generality that .

Moreover for now we make the additional assumption that ; we will get rid of this extra condition later.

We will apply Theorem 2 to the compact convex set , the convex set of -tuples of continuous bounded functions on and the function

| (19) |

Clearly the assumptions of Theorem 2 are satisfied, the continuity of on being a consequence of Lemma 2.2.

We then find

| (20) | ||||

| (21) | ||||

| (22) | ||||

| (23) | ||||

| (24) |

Here Proposition 2.1 is applied to to establish the equality between (21) and (22) and the equality of (22) and (23) is guaranteed by Theorem 2. Finally let us justify the equality between (23) and (24): indeed if is not a martingale measure, then by Lemma 2.3 for some there is a function such that

does not vanish. By appropriately scaling the value of can be made arbitrarily large.

Next assume that is merely lower semi-continuous and pick a sequence of bounded continuous functions such that . In the following paragraph we will write , resp. to emphasize the dependence on the cost function. For each pick such that

Passing to a subsequence if necessary, we may assume that converges weakly to some . Then

| (25) | ||||

Since it follows that .

It remains to prove that the optimal value of the primal problem is attained. To establish this, we use the lower semi-continuity of on : if a sequence of measures in converges weakly to a measure , then

| (26) |

We refer the reader to [Vil09, Lemma 4.3] for a proof of this assertion.

If , the infimum is trivially attained, so assume and pick a sequence in such that . As is compact, converges to some measure along a subsequence and is a primal minimizer by (26). ∎

As we have just seen, the existence of a primal optimizer is basically a consequence of the compactness of the set of all martingale transport plans. The dual set of sub-hedges does not exhibit nice compactness properties and as we already mentioned the dual supremum is not necessarily attained (Proposition 4.1 below). Although we are not able to give a positive criterion in this direction, it seems worthwhile to comment on the consequences of attainment of the dual problem.

Assume that there exists a dual maximizer, i.e. that there exist integrable functions and continuous bounded functions such that the corresponding subhedge (cf. (3)) satisfies

| (27) |

and

Let be a primal optimizer, i.e. a martingale measure satisfying the given marginal constraints as well as . Then we have

As a consequence, equality holds -a.s. in (27). The financial interpretation is that under the market model , the payoff is perfectly replicated through the semi-static hedge corresponding to .

4. Further analysis in the two dimensional case.

Throughout this section we focus on the two-period case, i.e. . We start with two examples which illustrate (the general) Theorem 1. Then we show that the dual supremum is not necessarily attained. Finally we explain a conjugacy relation which is relevant for the dual problem and resembles a well-known concept from the classical theory of optimal transport.

4.1. A numerical example: forward-start options.

We consider the problem to find optimal upper and lower bounds for forward-start options with payoffs

Recently, Hobson and Neuberger [HN12] have obtained interesting results on model-independent bounds for the forward-start straddle . Since , this is equivalent to the case , . An unfortunate feature is that no fully explicit solution is known for generic measures and . In [HN12, Section 9] numerical upper bounds are obtained in the cases where are given as uniform resp. log-normal distributions.

We will consider the cases of different strikes and laws inferred from market data. By using a linear programming algorithm, we have computed numerically the optimal lower and upper bounds for different values of .

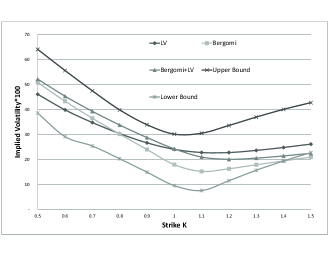

The measures and are deduced from the prices of call options written on the DAX (pricing date = 2nd Feb. 2012) with year and years with strikes ranging from to of the current spot price . The dual for the upper bound reads as (setting )

| (28) | ||||

| s.t. | ||||

| (29) |

The additional term has been incorporated by considering a vanilla option at with a zero strike. Note that the function is piecewise linear with respect to and therefore attains its extremal values at the points , , , . The above constraints therefore reduce to constraints parametrized by . As a consequence this low-dimensional linear program can be efficiently implemented by using a classical simplex algorithm [PTVF07] and by discretizing the spot value on a space grid. We have compared the upper and lower bounds against the prices produced by models commonly used by practitioners (see Fig. 1): the local volatility model (in short LV) [Dup94], Bergomi’s model [Ber05] which is a two-factor variance curve model and finally the local Bergomi model [HL09] which has the property to be perfectly calibrated to vanilla smiles at and . The LV and local Bergomi models have been calibrated to the DAX implied volatility market. The Bergomi model has been calibrated to the variance-swap term structure. As expected, the prices as produced by the LV and local Bergomi models – consistent with the marginals and – are within our bounds.888We would like to emphasize that the lower/upper bounds corresponding to different strikes are attained by different martingale measures. This is not the case if we do not include the martingality constraint as in this case the upper/lower bounds are attained by the co-monotone resp. anti-monotone coupling for each strike (see for instance [Vil03, Section 2.2.2]).

.

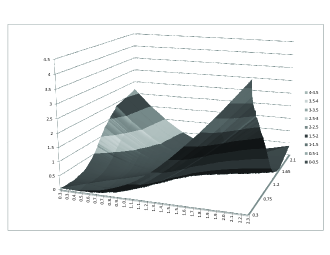

We have also plotted as a function of and for the at-the-money forward-start option (i.e. , see Fig. 2) to check the super-replication strategy.

Our result shows that forward-start options are poorly constrained by vanilla smiles. As a conclusion, the practice in the old-quant community to calibrate stochastic volatility models on vanilla smiles to price exotic options (depending strongly on forward volatility) is inappropriate.

Additional numerical examples are investigated in a companion paper [HL11]. In the case of Asian options the bounds are tighter, indicating that this option can be fairly well hedged with vanilla options.

We would like to highlight that for general exotic options, our dual bound can be framed into a large-scale semi-infinite linear program whose numerical implementation requires advanced simplex algorithm such as a primal-dual algorithm within a cutting-plane algorithm [HL11].

4.2. Analysis of a theoretical example

We consider a forward-start straddle with payoff function ; as above we assume that the marginal laws are fixed. As mentioned before, Hobson and Neuberger [HN12] treat the problem to find a market model which maximizes the price ; specific examples are worked out in detail.

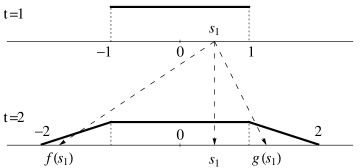

Here we focus on the problem to minimize in a concrete example. The marginals are defined by the respective densities (where we write for the Lebesgue measure)

cf. Figure 3 below. Recall that the primal, resp. dual problem is then given by

By Theorem 1 we know that there is no duality gap, i.e. . Our aim is to determine the primal minimizer as well as dual maximizers . We follow the common procedure of guessing and verification: i.e. making various (unjustified) assumptions we will first produce explicit candidates. Then it is possible to verify rigorously that these candidates indeed solve the given problem.

Due to Hobson [Hob12] (see also ([BJ12, Section 6]) one expects that the primal minimizer has a very particular structure: Writing for the disintegration999In probabilistic terms, the measure is the conditional distribution of under given that . of w.r.t. , each measure will be concentrated on three points. More specifically we guess101010We emphasize that while this simple guess works in the present setting, the situation is more subtle for general distributions. that there exist monotone decreasing functions such that .

Figure 3 depicts the measures and for each particle starting in the possible positions at time .

I.e., as much mass as possible remains at its place, the rest is either moved to the interval on the left of (via ), or to the right (via ). For , we write the measure as

Taking for granted that are sufficiently smooth, the marginal conditions on translate to

Thus and can be expressed in terms of the functions , i.e.

From , we obtain for the equation

| (30) |

The martingale property is expressed by . In terms of this amounts to

| (31) |

Adding the initial conditions and , the differential equations (30), (31) have the unique solution

| (32) |

These functions determine a martingale measure which is our candidate optimizer for the primal problem.

A dual optimizer consists of functions satisfying

| (33) |

for all . From the considerations at the end of Section 3 we know that equality should hold in (33) for all in the support of the primal minimizer. Since we anticipate that is this minimizer, we expect equality in (33) for . Writing , and , this amounts to

| (34) | ||||

for . Furthermore it is reasonable to assume that for fixed , the affine function is tangent to the function if equals resp. . This leads us to identify the slope of this affine function with the derivatives of the right hand side for

| (35) | ||||

The equations (34) resp. (35) are solved by

Setting , we have thus found a “reasonable” candidate solution for the dual problem. It is then straightforward to verify that is admissible, i.e., satisfies (33).

To verify that resp. are in fact solutions of the primal resp. dual problem we evaluate the corresponding functionals

Hence and we conclude that resp. are indeed the desired solutions.

4.3. Non-Existence of dual maximizers

In the classical optimal transport problem, the optimal value of the dual problem is attained provided that the cost function is bounded ([Kel84, Theorem 2.14]) or satisfies appropriate moment conditions ([AP03, Therorem 2.3]).

This is not the case in our present setting as Proposition 4.1 shows that the dual supremum (5) is not necessarily attained even if are compactly supported. Our counterexample fits into the framework111111Formally Hobson and Neuberger are interested to maximize the payoff of while we are interested to minimize the payoff . Mathematically, the two problems are of course the same. We haven chosen the latter formulation to be consistent with the notation in our main result Theorem 1. of [HN12], i.e. we consider two periods and an exotic option with payoff .

Proposition 4.1.

Let be the uniform distribution on the interval and

There exists a measure , concentrated on countably many atoms, such that the (finite) dual value is not attained.

Moreover, there do not exist functions such that

| (36) | ||||

where is a minimizer of the primal problem.

In the proof of Proposition 4.1 we will use the following auxiliary result.

Lemma 4.2.

Assume that are probability measures on having finite first moments, let and fix . The following are equivalent.

-

(i)

The call prices and are equal.

-

(ii)

If , then and if then , -a.s.

In particular, if (ii) holds for one measure in , then it applies to all elements of .

Proof.

We also make the following trivial observation:

Lemma 4.3.

Let , let be a measure on and set . Then the product-measure is the unique measure on which has as first marginal and as second marginal.

of Proposition 4.1..

Denote by the Lebesgue measure on the real line and set . Define

| (39) | ||||

| (40) | ||||

| (41) |

We claim that consists of the single element

| (42) |

Note that is defined to be the midpoint of the interval , ; likewise is the midpoint of . Therefore is indeed an element of .

To prove that is the only element of we first observe that for

| (43) |

Lemma 4.2 yields that (43) applies to an arbitrary measure . As is countable, it follows that

We also note that

Applying Lemma 4.3 with resp. it follows that is the only measure satisfying and having marginals . Since , we conclude that . Thus we have indeed .

According to the short discussion preceding Proposition 4.1 it is sufficient to show that (36) cannot be verified. Striving for a contradiction, we assume that there exist such that (36) (with respect to the measure ) holds true.

Setting , we obtain

| (44) |

for with equality holding for -almost all . Applying this with and , respectively yields

| (45) | ||||

Note that as these inequalities appeal to piecewise linear functions it is not necessary to exclude exceptional null-sets, in particular

for It follows that the slope of is smaller or equal than the one of at the point , i.e.

| (46) |

Hence

Arguably, the counterexample obtained in Proposition (4.1) is rather artificial. In particular a crucial property is that the problem consists of infinitely many problems which are mutually not connected: there exist infinitely many intervals which intersect only in boundary points such that every is concentrated on the union of the squares-products of these intervals. By Lemma 4.2 this is reflected in the prices of European calls by the property

whenever the strike is the endpoint of some interval.

Clearly it would be desirable to find conditions which guarantee that the dual supremum is attained. However we are not able to do so at the present stage.121212Some progress in this direction is made in [BJ12, Appendix A]. (Note added in revision.)

4.4. A c-convex approach

In the dual part of the usual transport problem it suffices to maximize over all pairs of functions where is the conjugate of with respect to , i.e., satisfies

(We refer the reader to [Vil03, Section 2.4], [Vil09, Chapter 5] for details on this topic.)

An analogous result holds true in the present martingale setup. Its relevance stems from the fact that it simplifies the construction of hedging strategies for options depending on two future time points. Unfortunately we are not aware of a generalization to the multi-period case.

Given a function , we write for its convex envelope131313I.e. is the largest convex function smaller than or equal to .. For , let be the function satisfying

for every . (It is straight forward to prove that is Borel measurable resp. lower semi-continuous whenever is.)

Proposition 4.4.

Let be a lower semi-continuous function such that and assume that there is some satisfying . Then

| (49) |

(In the course of the proof we will see that for every choice of the first integral in (49) is well defined, assuming possibly the value .)

Proof.

We start to show that the primal value is greater or equal than the right hand side of (49). Let be a -integrable function. For satisfying we have

| (50) | ||||

| (51) | ||||

where the inequality between (50) and (51) holds due to Jensen’s inequality. This proves the first inequality.

To establish the reverse inequality, we make a simple observation. Let and be some function. Suppose that for there exists such that

for all . Then

Applying this for to the function we obtain

| (52) | ||||

| (53) | ||||

| (54) |

where we tacitly assumed that the suprema are taken over -integrable functions and that is bounded measurable. ∎

Summary

This paper focusses on robust pricing and hedging of exotic options written on one risky asset.

Given call prices at finitely many time points the set of martingale models calibrated to these prices leads to an interval of consistent prices of a pre-specified exotic option. Theorem 1 resp. Corollary 1.1 assert inter alia that every price outside this interval gives rise to a model-independent arbitrage opportunity. This arbitrage can be realized through a semi-static sub/super-hedging strategy consisting in dynamic trading in the underlying and a static portfolio of call options.

Our approach to these results is based on the duality theory of mass transport.

Acknowledgements

We thank the associate editor and the extraordinarily careful referees for their comments and in particular for pointing out a mistake in an earlier version of this article. We also benefitted from remarks by Johannes Muhle-Karbe.

Appendix

As a special case of [Kel84, Theorem 2.14] we have the duality equation

for every lower semi-continuous cost function . The main task in the subsequent proof of Proposition 2.1 is to show that the duality equation is obtained if one restricts to functions in the class in the dual problem.

of Proposition 2.1.

As in the proof of Theorem 1, it is sufficient to prove the duality equation in the case .

Given a bounded continuous function and , then for every there is some such that and . Therefore we may change the class of admissible functions from to , i.e. it suffices to prove

| (55) |

We will first show this under the additional assumption that . By [Kel84, Theorem 2.14] we have that for each there exist -integrable functions , such that

and Note that the latter inequality implies that are uniformly bounded since is uniformly bounded from above.

To replace by a function in we consider and define

| (56) |

for . We claim that is (uniformly) continuous. Indeed, as is uniformly continuous, for every there exists such that whenever , , then

Thus we obtain

whenever . By definition is also bounded from below and satisfies as well as

Iteratively replacing the functions in the same fashion, we obtain (55) in the case .

Using precisely the same argument as in the proof of Theorem 1, we obtain the duality relation in the case of a general, lower semi-continuous function . ∎

References

- [AH96] D.R. Adams and L.I. Hedberg. Function spaces and potential theory, volume 314 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer-Verlag, Berlin, 1996.

- [AMS08] H. Albrecher, P.A. Mayer, and W. Schoutens. General lower bounds for arithmetic Asian option prices. Appl. Math. Finance, 15(1-2):123–149, 2008.

- [AP03] L. Ambrosio and A. Pratelli. Existence and stability results in the theory of optimal transportation. In Optimal transportation and applications (Martina Franca, 2001), volume 1813 of Lecture Notes in Math., pages 123–160. Springer, Berlin, 2003.

- [Ber05] L. Bergomi. Smile dynamics II. Risk, 18(10):67–73, 2005.

- [BHR01] H. Brown, D. Hobson, and L.C.G. Rogers. The maximum maximum of a martingale constrained by an intermediate law. Probab. Theory Related Fields, 119(4):558–578, 2001.

- [BJ12] M. Beiglböck and N. Juillet. On a problem of optimal transport under marginal martingale constraints. ArXiv e-prints, arXiv:1208.1509:1–51, 2012.

- [BP02] D. Bertsimas and I. Popescu. On the relation between option and stock prices: a convex optimization approach. Oper. Res., 50(2):358–374, 2002.

- [CDDV08] X. Chen, G. Deelstra, J. Dhaene, and M. Vanmaele. Static super-replicating strategies for a class of exotic options. Insurance Math. Econom., 42(3):1067–1085, 2008.

- [CL10] P. Carr and R Lee. Hedging variance options on continuous semimartingales. Finance Stoch., 14(2):179–207, 2010.

- [CO11a] A.M.G. Cox and J. Obłój. Robust hedging of double touch barrier options. SIAM J. Financial Math., 2:141–182, 2011.

- [CO11b] A.M.G. Cox and J. Obłój. Robust pricing and hedging of double no-touch options. Finance Stoch., 15(3):573–605, 2011.

- [Cou07] L. Cousot. Conditions on option prices for absence of arbitrage and exact calibration. Journal of Banking & Finance, 31(11):3377–3397, 2007.

- [CW12] A. M. G. Cox and J. Wang. Root’s Barrier: Construction, Optimality and Applications to Variance Options. Ann. Appl. Prob., to appear, 2012.

- [DH07] M.H.A. Davis and D. Hobson. The range of traded option prices. Math. Finance, 17(1):1–14, 2007.

- [Dup94] B. Dupire. Pricing with a smile. Risk, 7(1):18–20, 1994.

- [GHLT11] A. Galichon, P. Henry-Labordère, and N. Touzi. A Stochastic Control Approach to No-Arbitrage Bounds Given Marginals, with an Application to Lookback Options. SSRN eLibrary, 2011. Submitted.

- [HK12] D. Hobson and M. Klimmek. Model independent hedging strategies for variance swaps. Finance and Stochastics, 16(4):611–649, oct 2012.

- [HL09] P. Henry-Labordère. Calibration of local stochastic volatility models to market smiles. Risk, pages 112–117, sep 2009.

- [HL11] P. Henry-Labordère. Automated Option Pricing: Numerical Methods. SSRN eLibrary, 2011.

- [HLSTO12] P. Henry-Labordère, P. Spoida, N. Touzi, and J. Obłój. Maximum Maximum of Martingales Given Marginals. SSRN eLibrary, 2012. Submitted.

- [HLW05a] D. Hobson, P. Laurence, and T.H. Wang. Static-arbitrage optimal subreplicating strategies for basket options. Insurance Math. Econom., 37(3):553–572, 2005.

- [HLW05b] D. Hobson, P. Laurence, and T.H. Wang. Static-arbitrage upper bounds for the prices of basket options. Quant. Finance, 5(4):329–342, 2005.

- [HN12] D. Hobson and A. Neuberger. Robust bounds for forward start options. Mathematical Finance, 22(1):31–56, dec 2012.

- [Hob98] D. Hobson. Robust hedging of the lookback option. Finance and Stochastics, 2:329–347, 1998. 10.1007/s007800050044.

- [Hob11] D. Hobson. The Skorokhod embedding problem and model-independent bounds for option prices. In Paris-Princeton Lectures on Mathematical Finance 2010, volume 2003 of Lecture Notes in Math., pages 267–318. Springer, Berlin, 2011.

- [Hob12] D. Hobson. Personal communication, feb 2012.

- [HP02] D. Hobson and J.L. Pedersen. The minimum maximum of a continuous martingale with given initial and terminal laws. Ann. Probab., 30(2):978–999, 2002.

- [Kel84] H.G. Kellerer. Duality theorems for marginal problems. Z. Wahrsch. Verw. Gebiete, 67(4):399–432, 1984.

- [LW04] P. Laurence and T.H. Wang. What’s a basket worth? Risk, pages 73–77, feb 2004.

- [LW05] P. Laurence and T.H. Wang. Sharp Upper and Lower Bounds for Basket Options. Applied Mathematical Finance, 12(3):253–282, 2005.

- [MY02] D.B. Madan and M. Yor. Making Markov martingales meet marginals: with explicit constructions. Bernoulli, 8(4):509–536, 2002.

- [NH00] A. Neuberger and S.D. Hodges. Rational Bounds on the Prices of Exotic Options. SSRN eLibrary, 2000.

- [PTVF07] W.H. Press, S.A. Teukolsky, W.T. Vetterling, and B.P. Flannery. Numerical recipes. The art of scientific computing. Cambridge University Press, Cambridge, third edition, 2007.

- [Str65] V. Strassen. The existence of probability measures with given marginals. Ann. Math. Statist., 36:423–439, 1965.

- [Str85] H. Strasser. Mathematical theory of statistics. Statistical experiments and asymptotic decision theory, volume 7 of de Gruyter Studies in Mathematics. Walter de Gruyter & Co., Berlin, 1985.

- [Vil03] C. Villani. Topics in optimal transportation, volume 58 of Graduate Studies in Mathematics. American Mathematical Society, Providence, RI, 2003.

- [Vil09] C. Villani. Optimal Transport. Old and New, volume 338 of Grundlehren der mathematischen Wissenschaften. Springer, 2009.