Rényi’s information transfer between financial time series

Abstract

In this paper, we quantify the statistical coherence between financial time series by means of the Rényi entropy. With the help of Campbell’s coding theorem we show that the Rényi entropy selectively emphasizes only certain sectors of the underlying empirical distribution while strongly suppressing others. This accentuation is controlled with Rényi’s parameter . To tackle the issue of the information flow between time series we formulate the concept of Rényi’s transfer entropy as a measure of information that is transferred only between certain parts of underlying distributions. This is particularly pertinent in financial time series where the knowledge of marginal events such as spikes or sudden jumps is of a crucial importance. We apply the Rényian information flow to stock market time series from world stock indices as sampled at a daily rate in the time period 02.01.1990 - 31.12.2009. Corresponding heat maps and net information flows are represented graphically. A detailed discussion of the transfer entropy between the DAX and S&P500 indices based on minute tick data gathered in the period from 02.04.2008 to 11.09.2009 is also provided. Our analysis shows that the bivariate information flow between world markets is strongly asymmetric with a distinct information surplus flowing from the Asia–Pacific region to both European and US markets. An important yet less dramatic excess of information also flows from Europe to the US. This is particularly clearly seen from a careful analysis of Rényi information flow between the DAX and S&P500 indices.

PACS numbers: 89.65.Gh, 89.70.Cf, 02.50.-r

Keywords: Econophysics; Rényi entropy; Information transfer; Financial time series

I Introduction

The evolution of many complex systems in natural, economical, and social sciences is usually presented in the form of time series. In order to analyze time series, several of statistical measures have been introduced in the literature. These include such concepts as probability distributions 1 ; 2 , autocorrelations 2 , multi-fractals 3 , complexity 4 ; 5 , or entropy densities 5 . Recently, it has been pointed out that the transfer entropy (TE) is a very useful instrument in quantifying statistical coherence between time evolving statistical systems schreiber ; marschinski ; kwon2 . In particular, in Schreiber’s paper schreiber it was demonstrated that TE is especially expedient when global properties of time series are analyzed. Prominent applications are in multivariate analysis of time series, including e.g., study of multichannel physiological data or bivariate analysis of historical stock exchange indices. Methods based on TE have substantial computational advantages which are particularly important in analyzing a large amount of data. In all past works, including vejmelka ; kwon2 ; lungarella , the emphasis has been on various generalizations of transfer entropies that were firmly rooted in the framework of Shannon’s information theory. These, so called Shannonian transfer entropies are, indeed, natural candidates due to their ability to quantify in a non-parametric and in explicitly non-symmetric way the flow of information between two time series. An ideal testing ground for various TE concepts are financial-market time series because of the immense amount of electronically recorded financial data.

Recently, economy has become an active research area for physicists. They have investigated stock markets using statistical-physics methods, such as the percolation theory, multifractals, spin-glass models, information theory, complex networks, path integrals, etc.. In this connection the name econophysics has been coined to denote this new hybrid field on the border between statistical physic and (quantitative) finance. In the framework of econophysics it has became steadily evident that the market interactions are highly nonlinear, unstable, and long-ranged. It has also became apparent that all agents (e.g., companies) involved in a given stock market exhibit interconnectedness and correlations which represent important internal force of the market. Typically one uses correlation functions to study the internal cross-correlations between various market activities. The correlation functions have, however, at least two limitations: First, they measure only linear relations, although it is clear that linear models do not faithfully reflect real market interactions. Second, all they determine is whether two time series (e.g., two stock-index series) have correlated movement. They, however, do not indicate which series affects which, or in other words, they do not provide any directional information about cause and effect. Some authors use such concepts as time-delayed correlation or time-delayed mutual information in order to construct asymmetric “correlation” matrices with inherent directionality. This procedure is in many respects ad hoc as it does not provide any natural measure (or quantifier) of the information flow between involved series.

In the present paper we study multivariate properties of stock-index time with the help of econophysics paradigm. In order to quantify the information flow between two or more stock indices we generalize Schreibers’ Shannonian transfer entropy to Rényi’s information setting. With this we demonstrate that the corresponding new transfer entropy provides more detailed information concerning the excess (or lack) of information in various parts of the underlying distribution resulting from updating the distribution on the condition that a second time series is known. This is particularly relevant in the context of financial time series where the knowledge of tale-part (or marginal) events such as spikes or sudden jumps bears direct implications, e.g., in various risk-reducing formulas in portfolio theory.

The paper is organized as follows: In Section II we provide some information-theoretic background on Shannon and Rényi entropies (RE’s). In particular, we identify the conditional Rényi’s entropy with the information measure introduced in Ref. JA . Apart from satisfying the chain rule (i.e., rule of additivity of information) the latter has many desirable properties that are to be expected from a conditional information measure. Another key concept — the mutual Rényi entropy, is then introduced in a close analogy with Shannon’s case. The ensuing properties are also discussed. Shannonian transfer entropy of Schreiber is briefly reviewed in Section III. There we also comment on effective transfer entropy of Marchinski et all. The core quantity of this work — the Rényian transfer entropy (RTE), is motivated and derived in Section IV. In contrast to Shannonian case, the Rényian transfer entropy is generally not positive semi-definite. This is because RE non-linearly emphasizes different parts of involved probability density functions (PDF’s). With the help of Campbell’s coding theorem we show that the RTE rates a gain/loss in risk involved in a next-time-step behavior in a given stochastic process, say , resulting from learning a new information, namely historical behavior of another (generally cross-correlated) process, say . In this view the RTE can serve as a convenient rating factor of a riskiness in inter-connected markets. We also show that Rényian transfer entropy allows to amend spurious effects caused by a finite size of a real data set which in Shannon’s context must be, otherwise, solved by means of the surrogate data technique and ensuing effective transfer entropy. In Section V we demonstrate the usefulness and formal consistency of RTE by analyzing cross-correlations in various international stock markets. On a qualitative level we use simultaneously recorded data points of the eleven stock exchange indices, sampled at a daily (end-of-trading day) rate to construct the heat maps and net flows for both Shannon’s and Rényi’s information flows. On a quantitative level we explicitly discuss time series from the DAX and S&P500 market indices gathered on a minute-tick basis in the period from December 1990 till November 2009 in the German stock exchange market (Deutsche Börse). Presented calculations of Rényi and Shannon transfer entropies are based on symbolic coding computation with the open source software . Our numerical results imply that RTE’s among world markets are typically very asymmetric. For instance, we show that there is a strong surplus of an information flow from the Asia-Pacific region to both Europe and the U.S. A surplus of the information flow can be also observed to exists from Europe to the U.S. In this last case the substantial volume of transferred information comes from tail-part (i.e., risky part) of underlying asset distributions. So, despite the fact that the U.S. contributes more than half of the world trading volume, this is not so with information flow.

Further salient issues, such as dependence of RTE on Rényi’s parameter or on the data block length are numerically also investigated. In this connection we find that the cross-correlation between DAX and S&P500 has a long-time memory which is around 200-300 mins. This should be contrasted with typical memory of stock returns which are of the order of seconds or maximally few minutes. Various remarks and generalizations are proposed in the concluding Section VI. For reader’s convenience we give in Appendix A a brief dictionary of market Indices used in the main text and in Appendix B we tabulate an explicit values of effective transfer entropies used in the construction of heat maps and net information flows.

II Information-theoretic entropies of Shannon and Rényi

In order to express numerically an amount of information that is shared or transferred between various data sets (e.g., two or more random processes), one commonly resorts to information theory and especially to the concept of entropy. In this section we briefly review some essentials of Shannon’s and Rényi’s entropy that will be needed in following sections.

II.1 Shannon’s entropy

The entropy concept was originally introduced by Clausius huang in the framework of thermodynamics. By analyzing a Carnot engine he was able to identify a new state function which never decreases in isolated systems. The microphysical origin of Clausius’ phenomenological entropy was clarified more than years later in works of Boltzman and (yet later) Gibbs who associated Clausius entropy with the number of allowed microscopic states compatible with a given observed macrostate. The ensuing Boltzmann–Gibbs entropy reads

| (1) |

where is Boltzmann’s constant, is the set of all accessible microstates compatible with whatever macroscopic observable (state variable) one controls and denotes the number of microstates.

It should be said that the passage from Boltzmann–Gibbs to Clausius entropy is established only when the conditional extremum of subject to the constraints imposed by observed state variables is inserted back into . Only when this maximal entropy prescription gibbs is utilized turns out to be a thermodynamic state function and not mere functional on a probability space.

In information theory, on the other hand, the interest was in an optimal coding of a given source data. By optimal code is meant the shortest averaged code from which one can uniquely decode the source data. Optimality of coding was solved by Shannon in his 1948 seminal paper shannon . According to Shannon’s source coding theorem shannon ; SW , the quantity

| (2) |

corresponds to the averaged number of bits needed to optimally encode (or “zip”) the source dataset with the source probability distribution . On a quantitative level (2) represents (in bits) the minimal number of binary (yes/no) questions that brings us from our present state of knowledge about the system to the one of certainty shannon ; renyi1 ; ash . It should be stressed that in Shannon’s formulation represents a discrete set (e.g., processes with discrete time), and this will be also the case here. Apart from the foregoing operational definitions, Eq. (2) has also several axiomatic underpinnings. Axiomatic approaches were advanced by Shannon shannon ; SW , Khinchin khinchin , Fadeev fadeev an others others . The quantity (2) has became known as Shannon’s entropy (SE).

There is an intimate connection between Boltzmann–Gibbs entropy and Shannon’s entropy. In fact, thermodynamics can be viewed as a specific application of Shannon’s information theory: the thermodynamic entropy may be interpreted (when rescaled to “bit” units) as the amount of Shannon information needed to define the detailed microscopic state of the system, that remains “uncommunicated” by a description that is solely in terms of thermodynamic state variables szilard ; brillouin ; jaynes .

Among important properties of SE is its concavity in , i.e. for any pair of distributions and , and a real number holds

| (3) |

Eq. (3) follows from Jensen’s inequality and a convexity of for . Concavity is an important concept since it ensures that any maximizer found by the methods of the differential calculus yields an absolute maximum rather than a relative maximum or minimum or saddle point. At the same time it is just a sufficient (i.e., not necessary) condition guarantying a unique maximizer. It is often customary to denote SE of the source as rather than . Note that SE is generally not convex in !

It should be stressed that the entropy (2) really represents a self-information: the information yielded by a random process about itself. A step further from a self-information offers the joint entropy of two random variables and which is defined as

| (4) |

and which represents the amount of information gained by observing jointly two (generally dependent or correlated) statistical events.

A further concept that will be needed here is the conditional entropy of given , which can be motivated as follows: Let us have two statistical events and and let event has a sharp value , then the gain of information obtained by observing is

| (5) |

Here the conditional probability . For general random one defines the conditional entropy as the averaged Shannon entropy yielded by under the assumption that the value of is known, i.e.

| (6) |

From (6), in particular, follows that

| (7) |

Identity (7) is known as additivity (or chain) rule for Shannon’s entropy. In statistical thermodynamics this rule allows to explain, e.g., Gibbs paradox. Applying Eq. (7) iteratively, we obtain:

| (8) | |||||

Another relevant quantity that will be needed is the mutual information between and . This is defined as:

| (9) |

and can be equivalently written as

| (10) |

This shows that the mutual information measures the average reduction in uncertainty (i.e., gain in information) about resulting from observation of . Of course, the amount of information contained in about itself is just the Shannon entropy:

| (11) |

Notice also that from Eq. (9) follows and so provides the same amount of information on as does on . For this reasons the mutual information is not a useful measure to quantify a flow of information. In fact, the flow of information should be by its very definition directional.

II.2 Rényi’s entropy

Rényi introduced in Refs. renyi ; renyi0 a one-parameter family of information measures presently known as Rényi entropies renyi ; JA . In practice, however, only a singular name — Rényi’s entropy — is used. RE of order of a distribution on a finite set is defined as

| (14) |

For RE (14) one can also formulate source coding theorem. While in the Shannon case the cost of a code-word is a linear function of the length — so the optimal code has a minimal cost out of all codes, in the Rényi case the cost of a code-word is an exponential function of its length campbell ; aczel ; bercher . This is, in a nutshell, an essence of the so-called Campbell’s coding theorem (CCT). According to this RE corresponds to the averaged number of bits needed to optimally encode the discrete source with the probability , provided that the codeword-lengths are exponentially weighted expweight . From the form (14) one can easily see that for RE depends more on the probabilities of the more probable values and less on the improbable ones. This dependence is more pronounced for higher . On the other hand, for marginal events are accentuated with decreasing . In this connection we should also point out that Campbell’s coding theorem for RE is equivalent to Shannon’s coding theorem for SE provided one uses instead of the escort distribution bercher :

| (15) |

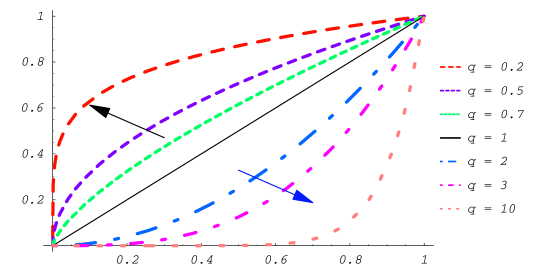

The PDF was first introduced by Rényi renyi0 and in the physical context brought by Beck, Schlögl, Kadanoff and others (see, e.g., Refs. beck ; kadanov ). Note (cf. Fig. 1)

that for the escort distribution emphasizes the more probable events and de-emphasizes more improbable ones. This trend is more pronounced for higher values of . For the escort distribution accentuates more improbable (i.e., marginal or rare) events. This dependence is more pronounced for decreasing . This fact is clearly seen on Fig. 2.

So by choosing different we can “scan” or “probe” different parts of the involved PDF’s.

It should be stressed that apart from CCT, RE has yet further operational definitions, e.g., in the theory of guessing arikan , in the buffer overflow problem jelinek or in the theory of error block coding csiszar . RE is also underpinned with various axiomatics renyi ; renyi0 ; daroczi . In particular, it satisfies identical Khinchin axioms khinchin as Shannon’s entropy save for the additivity axiom (chain rule) JA ; jizba2 ; jizba3 :

| (16) |

where the conditional entropy is defined with the help of the escort distribution (15) (see, e.g., Refs. JA ; tsallis ; beck ). For RE reduces to the Shannon entropy:

| (17) |

as one can easily verify with l’Hospital’s rule.

We define the joint Rényi entropy (or the joint entropy of order ) for two random variables and in a natural way as:

| (18) |

The conditional entropy of order of given is similarly as in the Shannon case defined as the averaged Rényi’s entropy yielded by under the assumption that the value of is known. As shown in Refs. JA ; jizba2 ; golshani this has the form

| (19) | |||||

In this connection it should be mentioned that several alternative definitions of the conditional RE exist (see, e.g., Refs. renyi0 ; cahin ; csiszar ), but the formulation (19) differs from other versions in a few important ways that will show up to be desirable in the following considerations. The conditional entropy defined in (19) has the following important properties, namely JA ; golshani

- –

-

, where is a number of elements in ,

- –

-

only when uniquely determines (i.e., no gain in information),

- –

-

,

- –

-

when and are independent then .

Unlike Shannon’s case one cannot, however, deduce that the equality implies independency between event and . Also the inequality (i.e., an extra knowledge about lessens our ignorance about ) does not hold here in general renyi0 ; JA . The latter two properties may seem as a serious flaw. We will now argue that this is not the case and, in fact, it is even desirable.

First, in order to understand why does not imply independency between and we define the information-distribution function

| (20) |

which represents the total probability caused by events with information content . With this we have

| (21) |

and thus

| (22) |

Taking the inverse Laplace transform with the help of the so-called Post’s inversion formula post we obtain

| (23) |

Analogous relation holds also for and associated . As a result we see that when working with of different orders we receive much more information on underlying distribution than when we restrict our investigation to only one (e.g., to only Shannon’s entropy). In addition, Eq. (23) indicates that we need all (or equivalently all , see note ) in order to uniquely identify the underlying PDF.

In view of Eq. (23) we see that the equality between and at some neighborhood of merely implies that for some . This naturally does not ensure independency between and . We need equality for all (or for all ) in order to secure that holds for all which would in turn guarantee that . Therefore, all RE with (or all with ) are generally required to deduce from an independency between and .

In order to understand the meaning of the inequality we first introduce the concept of mutual information. The mutual information of order between and can be defined as (cf. Eq. (10))

| (24) | |||||

which explicitly reads

| (25) | |||||

Note that we have again the symmetry relation as well as the consistency condition . So similarly as in the Shannon case, Rényi’s mutual information formally quantifies the average reduction in uncertainty (i.e., gain in information) about that results from learning the value of , or vice versa.

From Eq. (24) we see that the inequality in question, i.e., implies . According to (25) this can be violated only when

| (26) |

Here is an average with respect to the escort distribution (see Eq. (15)).

By taking into account properties of the escort distribution, we can deduce that when a larger probability events of receive by learning a lower value. As for the marginal events of , these are by learning indeed enhanced, but the enhancement rate is smaller than the suppression rate of large probabilities. For instance, this happens when

| (27) |

for

| (28) |

The inequality (28) ensures that holds. The left inequality in (28) saturates when , see also Fig. 3.

For is the situation analogous. Here properties of the escort distribution imply that when marginal events of get by learning a higher probability. The suppression rate for large (i.e. close-to-peak) probabilities is now smaller than the enhancement rate of marginal events. This happens, for example, for distributions,

| (29) |

with fulfilling again the inequality (28). This can be also directly seen from Fig. 3 when we revert the sign of . When we set then both inequalities (26) are simultaneously satisfied yielding — as it should.

In contrast to a Shannonian case where the mutual information quantifies the average reduction in uncertainty resulting from observing/learning a further information, in the Rényi case we should use Campbell’s coding theorem in order to properly understand the meaning of .

According to the CCT corresponds to the minimal average cost of a coded message with a non-linear (exponential) weighting/pricing of codeword-lengths. While according to Shannon we never increase ignorance by learning (i.e., possible correlations between and can only reduce the entropy), in Rényi’s setting extra knowledge about might easily increase the minimal price of coding because of the nonlinear pricing. Since the CCT penalizes long codewords which in Shannon’s coding have low probability, the price of the code may easily increase, as we have seen in examples (27) and (29).

In the key context of financial time series, the risk valuation of large changes such as spikes or sudden jumps is of a crucial importance, e.g., in various risk-reducing formulas in portfolio theory. The rôle of Campbell’s pricing can in these cases be interpreted as a risk-rating method which puts an exponential premium on rare (i.e., risky) asset fluctuations. From this point of view the mutual information represents a rating factor which rates a gain/loss in risk in resulting from learning a new information, namely information about .

The conditional mutual information of order between and given Z is defined as

| (30) |

Note that because of a validity of the chain rule (16), relations (8) and (13) also hold true for the RE.

To close this section, we shall stress that information entropies are primarily important because there are various coding theorems which endow them with an operational (that is, experimental) meaning, and not because of intuitively pleasing aspects of their definitions. While coding theorems do exist both for the Shannon entropy and the Rényi entropy there are (as yet) no such theorems for Tsallis’, Kaniadakis’, Naudts’ and other currently popular entropies. The information-theoretic significance of such entropies is thus not obvious. Since the information-theoretic aspect of entropies is of a crucial importance here, we will in the following focus only on the SE and the RE.

III Fundamentals of Shannonian transfer entropy

III.1 Shannonian transfer entropy

As seen in Section II.1, the mutual information quantifies the decrease of uncertainty about caused by the knowledge of . One could be thus tempted to use it as a measure of an informational transfer in general complex systems. A major problem, however, is that Shannon’s mutual information contains no inherent directionality since . Some early attempts tried to resolve this complication by artificially introducing the directionality via time-lagged random variables. In this way one may define, for instance, the time-lagged mutual (or directed Kullback–Leibler) information as

| (31) |

The later describes the average gain of information when replacing the product probability by the joint probability . So the information gained is due to cross-correlation effect between random variables and (respectively, ). It was, however, pointed out in Ref. schreiber that prescriptions such as (31), though directional, also take into account some part of the information that is statically shared between the two random processes and . In other words, these prescriptions do not produce statistical dependences that truly originate only in the stochastic random process , but they do include the effects of a common history (such as, for example, in the case of a common external driving force).

For this reason, Schreiber introduced in Ref. schreiber the concept of (Shannonian) transfer entropy (STE). The latter, apart from directionality, accounts only for the cross-correlations between statistical time series and whose genuine origin is in the “source” process . The essence of the approach is the following. Let us have two time sequences described by stochastic random variables and . Let us assume further that the time steps (data ticks) are discrete with the size of an elementary time lag and with ( is a reference time).

The transfer entropy can then be defined as

The last line of (LABEL:III.A.23a) indicates that represents the following.

| gain of information about caused by the whole history of and up to time | |

| gain of information about caused by the whole history of up to time | |

| gain of information about caused purely by the whole history of up to time . |

Note that one may equivalently rewrite (LABEL:III.A.23a) as the conditional mutual information

| (33) |

This shows once more the essence of Schreiber’s transfer entropy, namely, that it describes the gain in information about caused by the whole history of (up to time ) under the assumption that the whole history of (up to time ) is known. According to the definition of the conditional mutual information, we can explicitly rewrite Eq. (33) as

| (34) |

where and represent the discrete states at time of and , respectively.

In passing, we may observe from the first line of (LABEL:III.A.23a) that (any extra knowledge in conditional entropy lessens the ignorance). In addition, due to the Shannon–Gibbs inequality (see, e.g., Ref. jaynes ), only when

| (35) |

This, however, means that the history of up to time has no influence on the value of or, in other words, there is no information flow from to ; i.e., the and time series are independent processes. If there is any kind of information flow, then . is clearly explicitly non-symmetric (directional) since it measures the degree of dependence of on and not vice versa.

III.2 Effective transfer entropy

The effective transfer entropy (ETE) was originally introduced by Marchinski et al. in Ref. marschinski , and it was further substantiated in Refs. vejmelka ; kwon ; lungarella . The ETE, in contrast to the STE, accounts for the finite size of a real data set.

In the previous section, we have defined with the history indices and . In order to view as a genuine transfer entropy, one should really include in (33) the whole history of and up to time (i.e., all historical data that may be responsible for cross-correlations with ). The history is finite only if or/and processes are Markovian. In particular, if is a Markov process of order and and is of order , them is a true transfer entropy. Unfortunately most dynamical systems cannot be mapped to Markovian processes with finite-time memory. For such systems one should take limits and . In practice, however, the finite size of any real data set hinders this limiting procedure. In order to avoid unwanted finite-size effects, Marchinski proposed the quantity

| (36) |

where indicates the data shuffling via the surrogate data technique surrogate . The surrogate data sequence has the same mean, the same variance, the same autocorrelation function, and therefore the same power spectrum as the original sequence, but (nonlinear) phase relations are destroyed. In effect, all the potential correlations between time series and are removed, which means that should be zero. In practice, this shows itself not to be the case, despite the fact at there is no obvious structure in the data. The non-zero value of must then be a byproduct of the finite data set. Definition (36) then ensures that spurious effects caused by finite and are removed.

IV Rényian transfer entropies

There are various ways in which one can sensibly define a transfer entropy with Rényi’s information measure . The most natural definition is the one based on a -analog of Eqs. (LABEL:III.A.23a)-(33), i.e.,

| (37) | |||||

With the help of (25) and (30) this can be written in an explicit form as

| (38) |

Here, is the escort distribution (15). One can again easily check that in the limit we regain the Shanonnian transfer entropy (34).

The representation (38) deserves a few comments. First, when the history of up to time has no influence on the next-time-tick value of (i.e., on ), then from the first line in (38) it follows that , which indicates that no information flows from to , as should be expected. In addition, as defined by (37) and (38) takes into account only the effect of time series (up to time ), while the compound effect of the time series (up to time ) is subtracted (though indirectly present via correlations that exist between time series and ). In the spirit of Section II.2 one may interpret the transfer entropy as a rating factor which quantifies a gain/loss in the risk concerning the behavior of at the future time after we take into account the historical values of a time series until .

Unlike in Shannon’s case, does not imply independence of the and processes. This is because can also be negative on account of nonlinear pricing. Negativity of then simply means that the knowledge of historical values of both and broadens the tail part of the anticipated PDF for the price value more than historical values of only would do. In other words, an extra knowledge of historical values of reveals a greater risk in the next time step of than one would anticipate by knowing merely the historical data of alone.

Note that, with our definition (37), is again explicitly directional since it measures the degree of dependence of on and not the other way around, though in this case we should indicate by an arrow whether the original risk rate about was increased or reduced by observing the historical values of .

At this stage, one may introduce the effective Rényi transfer entropy (ERTE) by following the same logic as in the Shannonian case. In particular, one can again use the surrogate data technique to define the ERTE as

| (39) |

Similarly to the RTE, also accentuates for the flow of information that exists between the tail parts of distributions; i.e., it describes how marginal events in the time series influence marginal events in the time series . Since most of historical data belong to the central parts of distributions (typically with well-behaved Gaussian increments), one can reasonably expect that for the transfer entropy , and the surrogate data technique is not needed. This fact is indeed confirmed in our data analysis presented in the following section.

V Presentation of the analyzed data

In the subsequent analysis, we use two types of data set to illustrate the utility of Rényi’s transfer entropy. The first data set consists of 11 stock exchange indices, sampled at a daily (end of trading day) rate. The data set was obtained from Yahoo financial portal (historical data) with help of the R-code program rproject for the period of time between 2 January 1998 and 31 December 2009. These data will be used to demonstrate quantitatively the statistical coherence of all the mentioned indices in the form of heat maps and net flows.

Because we also wish to illustrate our approach quantitatively, we use as a second data set time series of 183.308 simultaneously recorded data points from two market indices, namely from the DAX index and the S&P500 insex, gathered on a minute-tick basis in the period from 2 April 2008 to 11 September 2009. In our analysis, we use complete records, i.e., minute data where only valid values for both the DAX index and the S&P500 index, are admitted: periods without trading activity (weekends, nighttime, holidays) in one or both stock exchanges were excluded. This procedure has the obvious disadvantage that records substantially separated in a real time may become close neighbors in the newly defined time series. Fortunately, relatively the small number of such “critical” points compared to the regular ones prevents a statistically significant error. In addition, due to computer data massification one may reasonably expect that the trading activity responds almost immediately to external stimuli. For this reason we have synchronized the data series to an identical reference time, a master clock, which we take to be Central European Time (CET).

V.1 Numerical calculation of transfer entropies

In order to find the PDF involved in definitions (34) (respectively, (36)) and (38) (respectively, (39)) we use the relative-frequency estimate. For this purpose we divide the amplitude (i.e., stock index) axis into discrete amplitude bins and assign to every bin a sample data value. The number of data points per bin divided by the length of the time series then constitutes the relative frequency which represents the underlying empirical distribution. In order to implement the R-code in the ETE and ERTE calculations we partition the data into disjoint equidistant time intervals (blocks), which serve as a coarse-graining grid. The number of data points we employ in our calculations is constant in each block. In each block only the arithmetic mean price is considered in block-dependent computations.

It is clear that the actual calculations depend on the number of bins chosen (this is also known as the alphabet length). In Ref. marschinski , it was argued that, in large data sets such as our time series, the use of alphabets with more than a few symbols is not compatible with the amount of data at one’s disposal. In order to make a connection with existing results (see Refs. kwon2 ; marschinski ), we conduct calculations at fixed alphabet length .

For a given partition, i.e., fixed , is a function of the block length . The parameter is to be chosen as large as possible in order to find a stable (i.e., large independent) value for ; however, due to the finite size of the real time series , it is required to find a reasonable compromise between unwanted finite sample effects and a high value for . This is achieved by substituting with the effective transfer entropy. Surrogate data that are needed in definitions of the ETE (36) and the ERTE (39) are obtained by means of standard R routines rproject . The effective Rényi and Shannon transfer entropies themselves are explicitly calculated and visualized with the help of the open-source statistical framework R and its related R packages for graphical presentations. The calculations themselves are also coded in the R language.

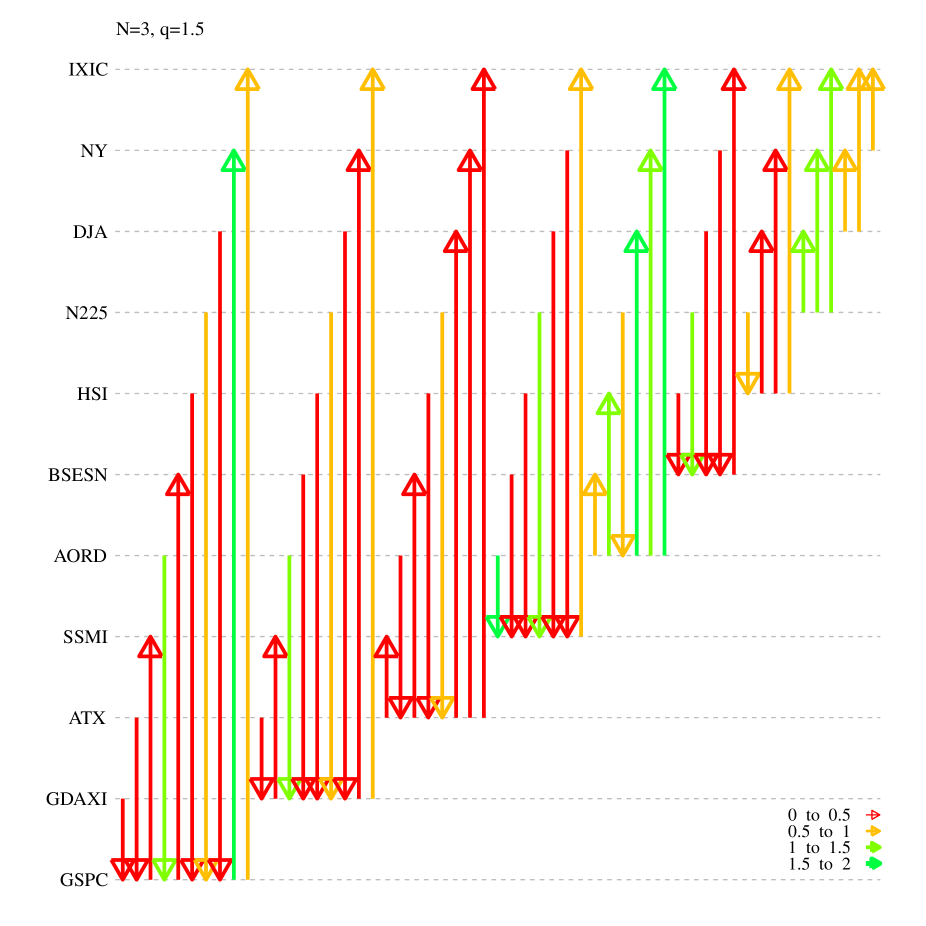

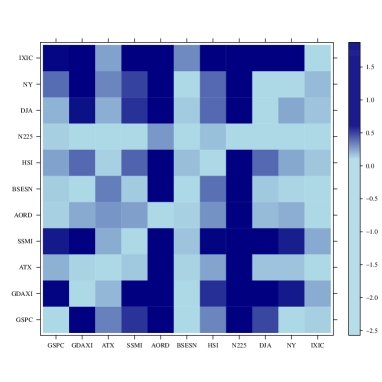

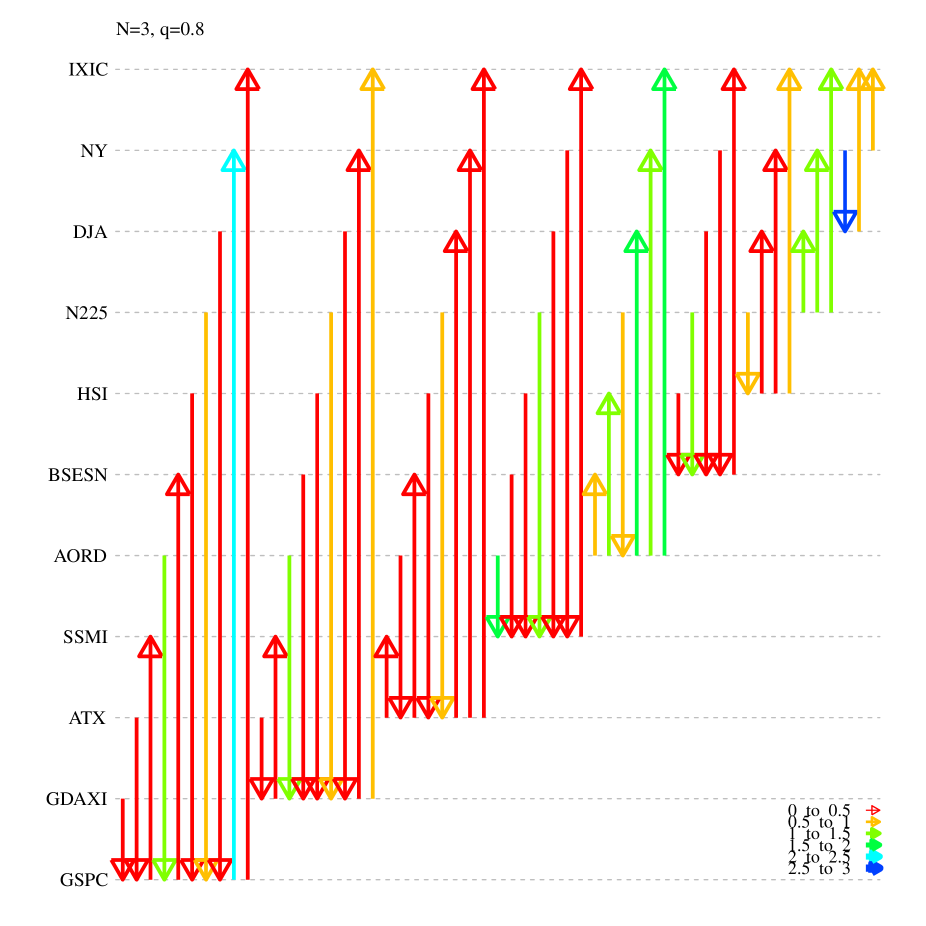

V.2 Analyzing the daily data — heat maps vs. net information flows

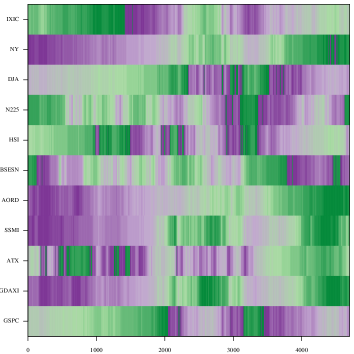

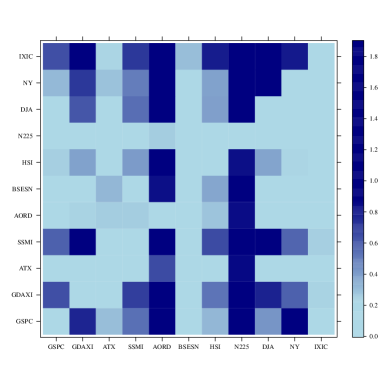

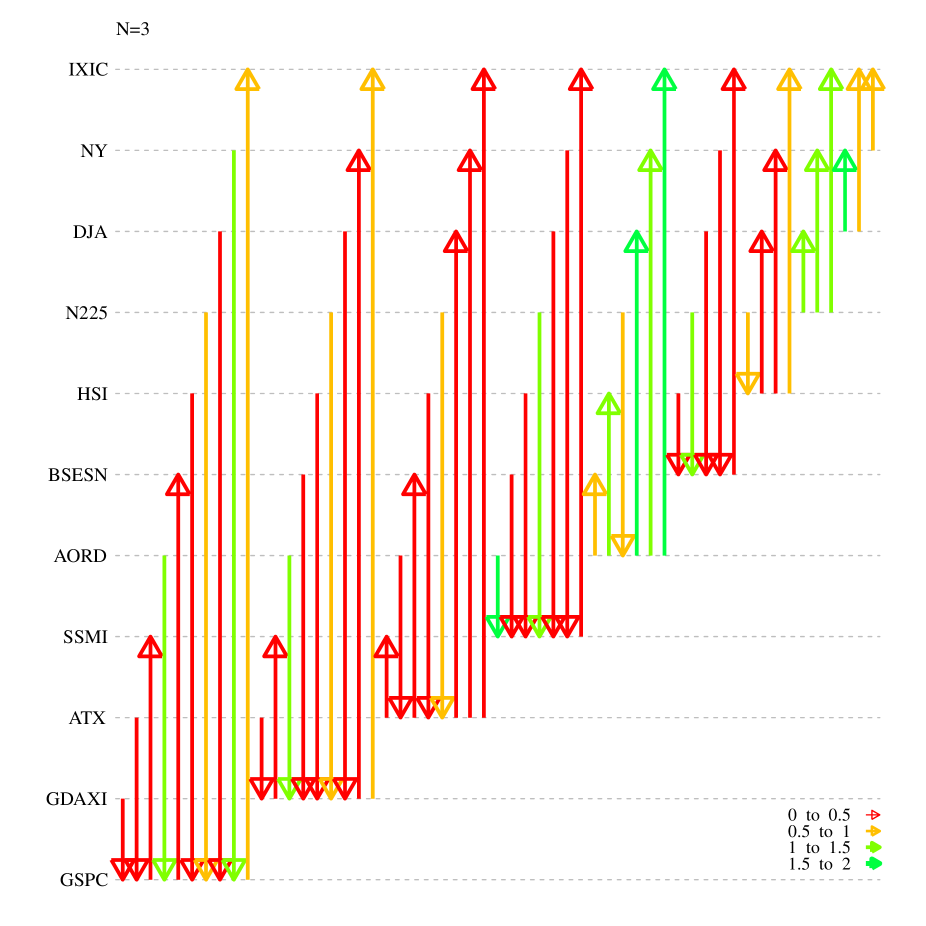

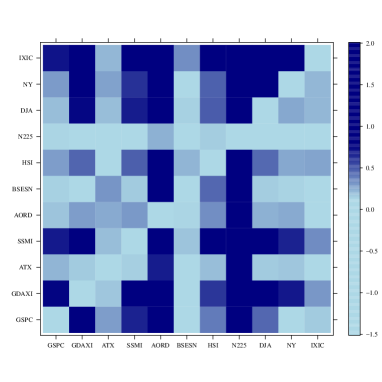

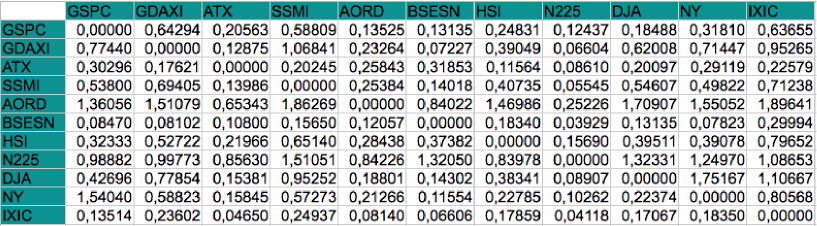

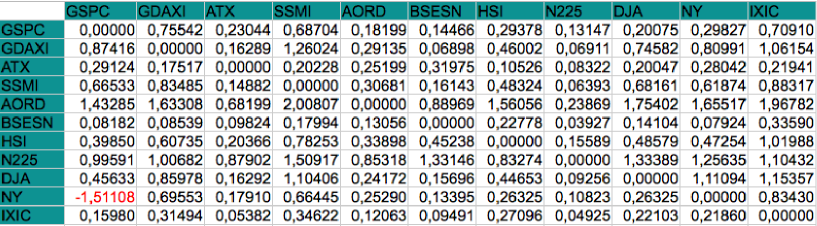

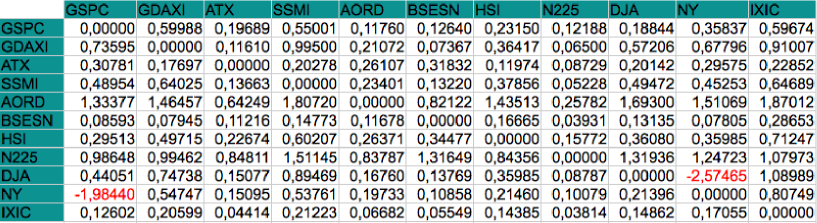

The effective transfer entropies and are calculated between 11 major stock indices (see the list in Appendix A). The results are collected in three tables in Appendix B and applied in the constructions of heat maps and net information flows in Figs. 7–13. In particular, Shannon’s information flow is employed in Figs. 8 and 9, while Rényi’s transfer entropy is used in construction of Figs. 10–13. The histogram-based heat map in Fig. 7 represents the overall run of the 11 aforementioned indices after the filtering procedure. We have used the RColorBrewer package RColorBrewer from the R statistical environment which employs a color-spectrum visualization for asset prices. In this case the color runs from the green, for higher prices, to dark purple, for low price values.

The heat map in Fig. 8 shows discloses that among the 11 selected markets a substantial amount of information flows between the Asia–Pacific region (APR) and the US. One can also clearly recognize the strong information exchanges between the APR and European markets and the subdominant information flow between the US and Europe. There is comparably less information flowing among European markets themselves. This can be credited to the fact that the internal European market is typically liquid and well equilibrated; similarly, a system in thermal equilibrium (far from critical points) has very little information flow among various parts. An analogous pattern (safe for the NY index) can also be observed among the US markets. In contrast, the markets within the APR mutually exchange a relatively large volume of information. This might be attributed to a lower liquidity and consequently less balanced internal APR market.

The heat maps in Figs. 10 and 12 bring further understanding. Notably, we can see that the information flow within APR markets is significantly more imbalanced between wings of the asset distributions (larger color fluctuations) than between the corresponding central parts. This suggests low liquidity risks. A similar though subordinate imbalance in the information transfer can also be observed between the US and APR markets.

Understandably more revealing are the net information flows presented in Figs. 9, 11 and 13. The net flow is defined as . This allows one to visualize more transparently the disparity between the and flows. For instance, in Fig. 9 we see that substantially more information flows from the APR to the US and Europe than vice versa. Figs. 11 and 13 then demonstrate more specifically that the APR Europe flow is evenly distributed between the central and tail distribution parts. From the net flow in Figs. 9, 11 and 13 we can also observe an important yet comparably weaker surplus of information flow from Europe towards the US. This interesting fact will be further addressed in the following subsection.

Note also that , and have negative values. These exceptional behaviors can be partly attributed to the fact that both the SP&500 and DJ indices are built from indices that are also present in the NY index and hence one might expect unusually strong coherence between these indices. From Section IV we know that negative values of the ERTE imply a higher risk involved in a next-time-step asset-price behavior than could be predicted (or expected) without knowing the historical values of the source time series. The observed negativity of thus means that when some of the ignorance is elevated by observing the time series a higher risk reveals itself in the nearest-future behavior of the asset price . Analogously, negativity of corresponds to a risk enhancement of the non-risky (i.e. close-to-peak) part of the underlying PDF.

V.3 Minute-price information flows

Here we analyze the minute-tick historic records of the DAX and S&P500 indices collected over the period of 18 months from 2 April 2008 to 11 September 2009. The coarse-grained overall run of both indices after the filtering procedure is depicted in the histogram-based heat map in Fig. 7.

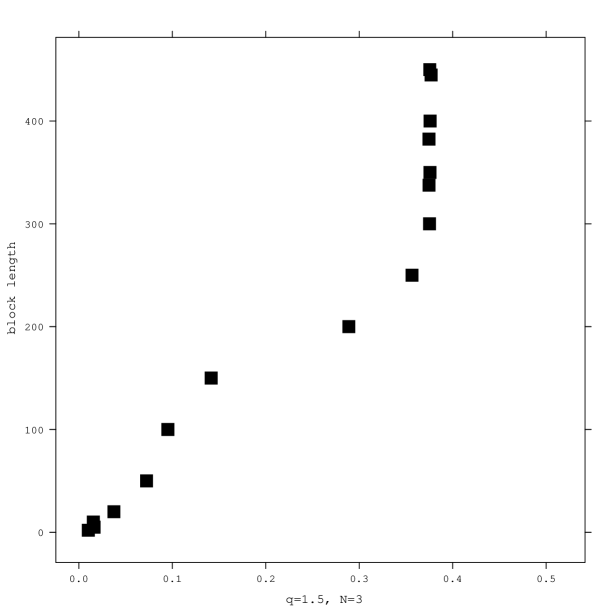

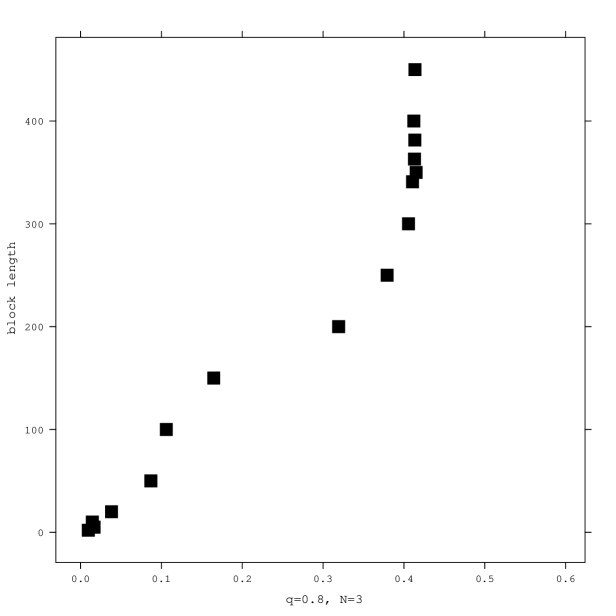

Without any a prior knowledge about the Markovian (or non-Markovian) nature of the data series, we consider the order of the Markov process for both the DAX and S&P500 stocks to be identical, i.e., the price memory of both indices is considered to be the same. The latter may be viewed as a “maximally unbiased” assumption. At this stage we eliminate the surrogate data and consider the RTE alone. The corresponding RTEs for and as functions of block lengths are shown in Figs. 14 and 15, respectively. There we can clearly recognize that for minutes there are no new correlations between the DAX and S&P500 indices. So, the underlying Markov process has order (or memory) roughly minutes.

The aforementioned result is quite surprising in view of the fact that autocorrelation functions of stock market returns typically decay exponentially with a characteristic time of the order of minutes (e.g., 4 mins for the S&P500 mategna ; jizba4 ), so the returns are basically uncorrelated random variables. Our result, however, indicates that two markets can be intertwined for much longer. This situation is actually not so surprising when we realize that empirical analysis of financial data asserts (see, e.g., Liu ) that autocorrelation functions of higher-order correlations for asset returns have longer decorrelation time which might span up to years (e.g., a few months in the case of volatility for the S&P500 jizba4 ). It is indeed a key advantage of our approach that the nonlinear nature of the RTE naturally allows one to identify the existing long-time cross-correlations between financial markets.

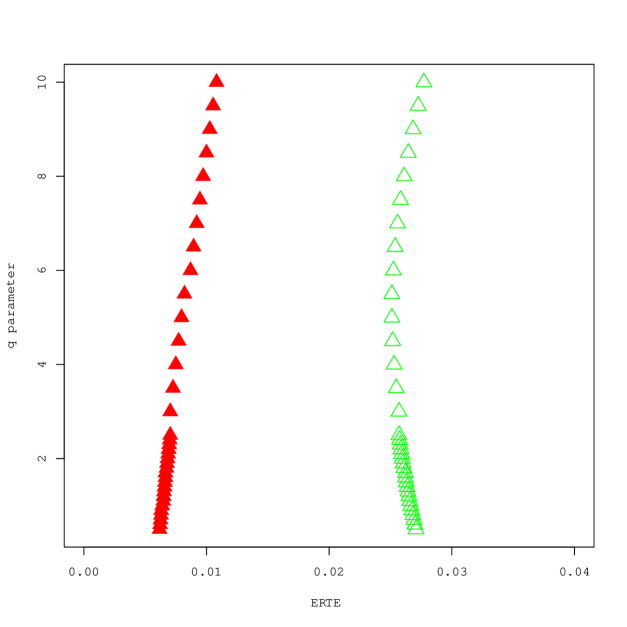

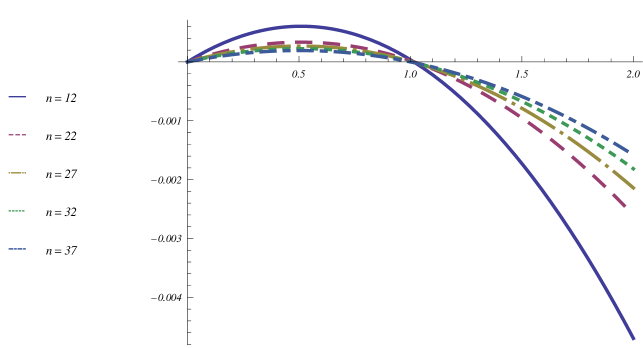

In Fig. 16, we depict the empirical dependence of the ERTE on the parameter . Despite the fact that the RE itself is a monotonically decreasing function of (see, e.g., Ref. renyi0 ) this is generally not the case for the ERTE (nor for the conditional RE). Indeed, the ERTE represents a difference of two REs with an identical (see Eq. (37)), and as such it may be neither monotonic nor decreasing. The functional dependence of the ERTE on nevertheless serves as an important indicator of how quickly REs involved change with .

The results reproduced in Fig. 16 quantitatively confirm the expected asymmetry in the information flow between the US and European markets. However, since the US contributes more than half of the world’s trading volume, it could be anticipated that there is a stronger information flow from big US markets towards both European and APR markets. Yet, despite the strong US trading record, our ERTE approach indicates that the situation is not so straightforward when the entropy-based information flow is considered as a measure of market cross-correlation. Indeed, from Figs. 9, 11 and 13 we could observe that there is a noticeably stronger information flow from the European and APR markets to the U.S. markets than than vice versa. Fig. 16 extends the validity of this observation also to short time scales of the order of minutes. In particular, from Fig. 16 we clearly see that flow from the DAX to the S&P500 is stronger than the reverse flow. It is also worth of noting that this Europe–US flow is positive for all values of , i.e., for all distribution sectors, with a small bias towards tail parts of the underlying distribution.

VI Concluding remarks

Transfer entropies have been repeatedly utilized in the quantification of statistical coherence between various time series with prominent applications in financial markets. In contrast to previous works in which transfer entropies have been exclusively considered only in the context of Shannon’s information theory, we have advanced here the notion of Rényi’s (i.e. non-Shannonian) transfer entropy. The latter is defined in a close analogy with Shannon’s case, i.e., as the information flow (in bits) from to ignoring static correlations due to the common historical factors such as external agents or forces. However, unlike Shannon’s transfer entropy, where the information flow between two (generally cross-correlated) stochastic processes takes into account the whole underlying empirical price distribution, the RTE describes the information flow only between certain pre-decided parts of two price distributions involved. The distribution sectors in question can be chosen when Rényi’s parameter is set in accordance with Campbell’s pricing theorem. Throughout this paper we have demonstrated that the RTE thus defined has many specific properties that are desirable for the quantification of an information flow between two interrelated stochastic systems. In particular, we have shown that the RTE can serve as an efficient rating factor which quantifies a gain or loss in the risk that is inherent in the passage from to when a new information, namely historical values of a time series until time , is taken into account. This gain/loss is parameterized by a single parameter, the Rényi parameter, which serves as a “zooming index” that zooms (or emphasizes) different sectors of the underlying empirical PDF. In this way one can scan various sectors of the price distribution and analyze associated information flows. In particular, the fact that one may separately scrutinize information fluxes between tails or central-peak parts of asset price distributions simply by setting or , respectively, can be employed, for example, by financial institutions to quickly analyze the global (across-the-border) information flows and use them to redistribute their risk. For instance, if an American investor observes that a certain market, say the S&P500, is going down and he/she knows that the corresponding NASDAQ ERTE for is low, then he/she does not need to relocate the portfolio containing related assets rapidly, because the influence is in this case slow. Slow portfolio relocation is generally preferable, because fast relocations are always burdened with excessive transaction costs. Let us stress that this type of conduct could not be deduced from Shannon’s transfer entropy alone. In fact, the ETE suggests a fast (and thus expensive) portfolio relocation as a best strategy (see Figs. 9,11 and 13).

Let us stress that applications of transfer entropies presented quantitatively support the observation that more information flows from the Asia–Pacific region towards the US and Europe than vice versa, and this holds for transfers between both peak parts and wing parts of asset PDFs; i.e., the US and European markets are more prone to price shakes in the Asia–Pacific sector than the other way around. Besides, information-wise the US market is more influenced by the European one than in reverse. This interesting observation can be further substantiated by our DAX versus S&P500 analysis, in which we have seen that the influx of information from Europe is to a large extend due to a tail-part transfer. The peak-part transfer is less pronounced. So, although the US contributes more than half of the world’s trading volume, our results indicate that this is not so with information flow. In fact, the US markets seem to be prone to reflect a marginal (i.e., risky) behavior in both European and APS markets. Such a fragility does not seem to be reciprocated. This point definitely deserves further closer analysis.

Finally, one might be interested in how the RTE presented here compares with other correlation tests. The usual correlation tests take into account either the lower-order correlations (e.g., time-lagged cross-correlation test and Arnhold et al. interdependence test) or they try to address the causation issue between bivariate time series (e.g., Granger causality test or Hacker and Hatemi-J causality test). Since the RTE allows one to compare only certain parts of the underlying distributions it also works implicitly with high-order correlations, and for the same reason it cannot affirmatively answer the causation issue. In many respects such correlation tests bring complementary information with respect to the RTE approach. More detailed discussion concerning multivariate time series and related correlation tests will be presented elsewhere.

Acknowledgments

This work was partially supported by the Ministry of Education of the Czech Republic (research plan MSM 6840770039), and by the Deutsche Forschungsgemeinschaft under grant Kl256/47.

Appendix A

In this appendix we provide a brief glossary of the indices used in the main text. The notation presented here conforms with the notation typically listed in various on-line financial portals (e.g., Yahoo financial portal).

| Indices | Description | Country |

|---|---|---|

| GSPC | Standard and Poor 500 (500 stocks actively traded in the U.S.) | USA |

| GDAXI | Dax Indices (stock of 30 major German companies) | Germany |

| ATX | The Austrian Traded Index is the most important stock market index of the Wiener Börse. The ATX is a price index and currently consists of 20 stocks. | Austria |

| SSMI | The Swiss Market Index is a capitalization-weighted index of the 20 largest and most liquid stocks. It represents about 85% of the free-float market capitalization of the Swiss equity market. | Swiss |

| AORD | All Ordinaries represents the 500 largest companies in the Australian equities market. Index constituents are drawn from eligible companies listed on the Australian Stock Exchange | Australia |

| BSESN | The BSE Sensex is a market capitalized index that tracks 30 stocks from the Bombay Stock Exchange. It is the second largest exchange of India in terms of volume and first in terms of shares listed. | India |

| HSI | The Hang Seng Index denoted in Hong Kong stock market. It is used to record and monitor daily changes of the largest companies of the Hong Kong stock market. It consist of 45 Companies. | Hong Kong |

| N225 | Nikkei 225 is a stock market index for the Tokyo Stock Exchange. It is a price-weighted average (the unit is yen), and the components are reviewed once a year. Currently, the Nikkei is the most widely quoted average of Japanese equities, similar to the Dow Jones Industrial Average. | Japan |

| DJA | The Dow Jones Industrial Average also referred to as the Industrial Average, the Dow Jones, the Dow 30, or simply as the Dow; is one of several U.S. stock market indices. First published in 1887. | USA |

| NY | iShares NYSE 100 Index is an exchange trading fund, which is a security that tracks a basket of assets, but trades like a stock. NY tracks the SE U.S. 100; this equity index measures the performance of the largest 100 companies listed on the New York Stock Exchange (NYSE). | USA |

| IXIC | The Nasdaq Composite is a stock market index of all of the common stocks and similar securities (e.g., ADRs, tracking stocks, limited partnership interests) listed on the NASDAQ stock market, it has over 3.000 components. | USA |

Appendix B

In this appendix we specify explicit values of effective transfer entropies that are employed in Section V. These are calculated for alphabet with .

References

- (1) J.-S. Yang, W. Kwak, T. Kaizoji and I.-M. Kim, Eur. Phys. J. B61 (2008) 389; K. Matal, M. Pal, H. Salunkay and H.E. Stanley, Europhys. Lett. 66 (2004) 909; H.E. Stanley, L.A.N. Amaral, X. Gabaix, P. Gopikrishnan and V. Plerou, Physica A299 (2001) 1.

- (2) J.-S. Yang, S. Chae, W.-S. Jung and H.-T. Moon, Physica A363 (2006) 377.

- (3) K. Kim and S.-M. Yoon, Physica A344 (2004) 272.

- (4) J.B. Park, J.W. Lee, J.-S. Yang, H.-H. Jo and H.-T. Moon, Physica A379 (2007) 179.

- (5) J.W. Lee, J.B. Park, H.-H. Jo, J.-S. Yang and H.-T. Moon, physics/0607282 (2006).

- (6) T. Schreiber, Phys. Rev. Lett. 85 (2000) 461.

- (7) O. Kwon and J.-S. Yang,Eur. Phys. Lett. 82 (2008) 68003.

- (8) R. Marschinski and H. Kantz, Eur. Phys. J. B30 (2002) 275.

- (9) M. Paluš and M. Vejmelka, Phys. Rev. E75 (2007) 056211.

- (10) M. Lungarella, A. Pitti and Y. Kuniyoshi, Phys. Rev. E76 (2007) 056117.

- (11) P. Jizba and T. Arimitsu, Ann. Phys. (N.Y.) 312 (2004) 17.

- (12) K. Huang, Statistical Mechanics, (John Wiley&Sons, New York, 1963).

- (13) Maximal entropy principle was in statistical thermodynamic introduced by J.W. Gibbs under the name: “The fundamental hypothesis of equal a priori probabilities in the phase space”.

- (14) C.E. Shannon, Bell Syst. Tech. J. 27 (1948) 379; 623.

- (15) C.E. Shannon and W. Weaver, The Mathematical Theory of Communication, (University of Illinois Press, New York, 1949).

- (16) A. Rényi, A diary on information theory, (John Wiley & Sons, New York, 1984).

- (17) R. Ash, Information Theory, (Wiley, New York, 1965).

- (18) A.I. Khinchin, Mathematical Foundations of Information Theory, (Dover Publications, Inc., New York, 1957).

- (19) A. Feinstein, Foundations of information theory, (McGraw Hill, New York, 1958).

- (20) T.W. Chaudy and J.B. McLeod, Edinburgh Mathematical Notes 43 (1960) 7; for H. Tverberg’s, P.M. Lee’s or D.G. Kendall’s axiomatics of Shannon’s entropy see e.g., S. Guias, Information Theory with Applications, (McGraw Hill, New York, 1977).

- (21) L. Szilard, Z. Phys. 53 (1929) 840.

- (22) L. Brillouin, J. Appl. Phys. 22 (1951) 334.

- (23) E.T. Jaynes, Papers on Probability and Statistics and Statistical Physics, (D. Reidel Publishing Company, Boston, 1983).

- (24) I. Csiszár and P.C.. Shields, Information Theory and Statistics: A Tutorial, (Now Publishers Inc., Boston, 2004).

- (25) A. Rényi, Probability Theory, (North-Holland, Amsterdam, 1970).

- (26) A. Rényi, Selected Papers of Alfred Rényi, (Akademia Kiado, Budapest, 1976), Vol. 2.

- (27) L.L. Campbell, Information and Control 8 (1965) 423.

- (28) J. Aczél and Z. Daróczy, Measures of Information and Their Characterizations, (Academic Press, New York, 1975).

- (29) J.-F. Bercher, Phys. Lett. A373 (2009) 3235.

- (30) This exponential weighting is also known as a Kolmogorov–Nagumo averaging. While the linear averaging is given by , the exponential weighting ia defined as with . The factor is known as Campbell exponent.

- (31) C. Beck and F. Schlögl, Thermodynamics of Chaotic Systems, (Cambridge University Press, Cambridge, 1993).

- (32) T.C. Halsey, M.H. Jensen, L.P. Kadanoff, I. Procaccia, B.I. Schraiman, Phys. Rev. A33 (1986)

- (33) E. Arikan, IEEE Trans. Inform. Theory 42 (1996) 99.

- (34) F. Jelinek, IEEE Trans. Inform. Theory IT-14 (1968) 490.

- (35) I. Csiszár, IEEE Trans. Inform. Theory 41 (1995) 26.

- (36) Z. Daróczy, Acta Math. Acad. Sci. Hungaricae 15 (1964) 203.

- (37) P. Jizba and T. Arimitsu, Physica A365 (2006) 76.

- (38) P. Jizba and T. Arimitsu, Physica A340 (2004) 110.

-

(39)

C. Tsallis, J. Stat. Phys. 52 (1988) 479;

Bibliography URL: http://tsallis.cat.cbpf.br/biblio.htm. - (40) L. Golshani, E. Pasha and G. Yari, Information Science 179 (2009) 2426.

- (41) C. Cahin, Entropy measures and unconditional security in cryptography, PhD Thesis, Swiss Federal Institute of Technology, Zurich, 1997.

- (42) E. Post, Trans. Am. Math. Soc. 32 (1930) 723.

- (43) One can map with to with via duality that exists between and . In fact, we can observe that and . So with and with carry equal amount of information.

- (44) O. Kwona and J. Yanga, Physica A387 (2008) 2851.

- (45) J. Theiler, S. Eubank, A. Longtin, B. Galdrikian, and J.D. Farmer, Physica D58 (1992) 77.

-

(46)

R Development Core Team, R: A language and environment for

statistical computing,

(R Foundation for Statistical Computing, Vienna, 2008);

URL http://www.R-project.org. -

(47)

E. Neuwirth, RColorBrewer: ColorBrewer.org Palettes, R package version 1.0-5, 2011;

URL http://CRAN.R-project.org/package=RColorBrewer. - (48) R.N. Mantegna and H.E. Stanley, An Introduction to Econophysics, (Cambridge University Press, Cambridge, 2000).

- (49) P. Jizba, H. Kleinert and P. Haener, Physica A388 (2009) 3503.

- (50) Y. Liu, P. Cizeau, M. Meyer, C.-K. Peng, H.E. Stanley, Physica A245 (1997) 437; Physica A245 441; Y. Liu, P. Gopikrishnan, P. Cizeau, M. Mayer, C.-K. Peng, H.E. Stanley, Phys. Rev. E60 (1999) 1390.