Threshold estimation based on a -value framework in dose-response and regression settings

Abstract.

We use -values to identify the threshold level at which a regression function takes off from its baseline value, a problem motivated by applications in toxicological and pharmacological dose-response studies and environmental statistics. We study the problem in two sampling settings: one where multiple responses can be obtained at a number of different covariate-levels and the other the standard regression setting involving limited number of response values at each covariate. Our procedure involves testing the hypothesis that the regression function is at its baseline at each covariate value and then computing the potentially approximate -value of the test. An estimate of the threshold is obtained by fitting a piecewise constant function with a single jump discontinuity, otherwise known as a stump, to these observed -values, as they behave in markedly different ways on the two sides of the threshold. The estimate is shown to be consistent and its finite sample properties are studied through simulations. Our approach is computationally simple and extends to the estimation of the baseline value of the regression function, heteroscedastic errors and to time-series. It is illustrated on some real data applications.

1. Introduction

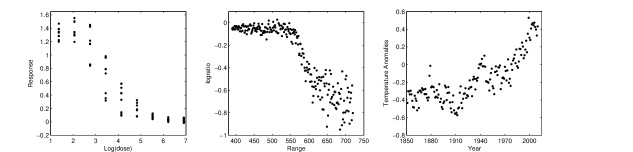

In a number of applications, the data follow a regression model where the regression function is constant at its baseline value up to a certain covariate threshold and deviates significantly from at higher covariate levels. For example, consider the data shown in the left panel of Fig. 1. It depicts the physiological response of cells from the IPC-81 leukemia rat cell line to a treatment, at different doses; more details are given in Section 3.2. The objective here is to study the toxicity in the cell culture to assess environmental hazards. The function stays at its baseline value for high dose levels which corresponds to the dose becoming lethal, and then takes off for lower doses, showing response to treatment. This problem requires procedures that can identify the change-point in the regression function, namely where it deviates from the baseline value. The threshold is of interest as it corresponds to maximum safe dose level beyond which cell cultures stop responding. Similar problems also arise in other toxicological applications (Cox, 1987).

Problems with similar structure also arise in other pharmacological dose-response studies, where quantifies the response at dose-level and is typically at the baseline value up to a certain dose, known as the minimum effective dose; see Chen & Chang (2007) and Tamhane & Logan (2002) and the references therein. In such applications, the number of doses or covariate levels is relatively small, say up to 20, and many procedures proposed in the literature are based on testing ideas (Tamhane & Logan, 2002; Hsu & Berger, 1999). However, in other application domains, the number of doses can be fairly large compared to the number of replicates at each dose. The latter is effectively the setting of a standard regression model. In the extreme case, there is a single observation per covariate level. Data from such a setting are shown in the middle panel of Fig. 1, depicting the outcome of a light detection and ranging experiment, used to detect the change in the level of atmospheric pollutants. This technique uses the reflection of laser-emitted light to detect chemical compounds in the atmosphere (Holst et al., 1996; Ruppert et al., 1997). The predictor variable, range, is the distance traveled before the light is reflected back to its source, while the response variable, logratio, is the logarithm of the ratio of received light at two different frequencies. The negative of the slope of the underlying regression function is proportional to mercury concentration at any given value of range. The point at which the function falls from its baseline level corresponds to an emission plume containing mercury and, thus, is of interest. An important difference between these two examples is that the former provides the luxury of multiple observations at each covariate level, while the latter does not.

Another relevant application in a time-series context is given in the right panel of Fig. 1, where annual global temperature anomalies are reported from 1850 to 2009. The study of such anomalies, temperature deviations from a base value, has received much attention in the context of global warming from both the scientific as well as the general community (Melillo, 1999; Delworth and Knutson, 2000). The figure suggests an initial flat stretch followed by a rise in the function. Detecting the advent of global warming, which is the threshold, is of interest here. While we take advantage of the independence of errors in the previous two datasets, this application has an additional feature of short range dependence which needs to be addressed appropriately.

Formally, we consider a function on with the property that for and for for some . As already mentioned, quantities of prime interest are and that need to be estimated from realizations of the model . We call the threshold of the function . Here is the global minimum for the function . To fix ideas, we work only with this setting in mind. The methods proposed can be easily imitated for the first data application where the baseline stretch is on the right as well as for the second data application where is the maximum.

In this generality, i.e., without any assumptions on the behavior of the function in a neighborhood of , the estimation of the threshold has not been extensively addressed in the literature. In the simplest possible setting of the problem posited, has a jump discontinuity at . In this case, corresponds to a change-point for and the problem reduces to estimating this change-point. Such models are well studied; see Mueller (1992), Loader (1996), Koul & Qian (2002), Pons (2003), Lan et al. (2009), Pons (2009) and the references therein. Results on estimating a change-point in a density can be found in Ibragimov & Khasminskii (1982).

The problem becomes significantly harder when is continuous at ; in particular, the smoother is in a neighborhood of , the more challenging the estimation. If is a cusp of of some known order , i.e., the first right derivatives of at equal 0 but the -th does not, so that is a change-point in the -th derivative, one can obtain nonparametric estimates for using either kernel based (Mueller, 1992) or wavelet based (Raimondo, 1998) methods. If the degree of differentiability of at is not known, this becomes an even harder problem. In fact, it was pointed out to us by one of the referees that if is unknown then there is no method for which the estimate, , will be uniformly consistent, i.e., for any , . Here, the supremum is taken over all choices of with a threshold at .

This paper develops a novel approach for the consistent estimation of in situations where single or multiple observations can be sampled at a given covariate value. The developed nonparametric methodology relies on testing for the value of at the design values of the covariate. The obtained test statistics are then used to construct -values which, under mild assumptions on , behave in markedly different manner on either side of the threshold and it is this discrepancy that is used to construct an estimate of . The approach is computationally simple to implement and does not require knowledge of the smoothness of at . In a dose-response setting involving several doses and large number of replicates per dose, the -values are constructed using multiple observations at each dose. The approach is completely automated and does not require the selection of any tuning parameter. In the case of limited or even single observation at each covariate value, referred to as the standard regression setting in this paper, the -values are constructed by borrowing information from neighboring covariate values via smoothing which only involves selecting a smoothing bandwidth. The first data application falls under the dose-response setting and the other two examples fall under the standard regression regime. We establish consistency of the proposed procedure in both settings.

An estimate of , say , by itself, fails to offer a satisfactory solution for estimating . Naive estimates, using , may be of the form or . The estimator performs poorly when is not monotone, and is close to at values to the far right of , e.g., when is tent-shaped. Also, , by itself, is not consistent and one would typically need to substitute with a , with at an appropriate rate, to attain consistency. In contrast, our approach does not need to introduce such exogenous parameters.

2. Formulation and Methodology

2.1. Problem Formulation

Consider a regression model , where is a function on and

| (1) |

for , with an unknown . The covariate is sampled from a Lebesgue density on and , for . We assume that is continuous and positive on and is continuous. No further assumptions are made on the behavior of , especially around . We have the following realizations:

| (2) |

with being the total budget of samples. The s are independent given and distributed like and the s are independent realizations from . Also, (2) with corresponds to the usual regression setting which simply has only one response at each covariate level.

We construct consistent estimates of under dose-response and standard regression settings. In the dose-response setting, we allow both and to be large and construct -values accordingly. We refer to the corresponding approach as Method 1 from now on. In the other setting, we consider the case when is much smaller compared to and extend our approach through smoothing. We refer to this extension as Method 2, which requires choosing a smoothing bandwidth. The two methods rely on the same dichotomous behavior exhibited by the approximate -values, although constructed differently.

2.2. Dose-Response Setting (Method 1)

We start by introducing some notation. Let and denote a generic value of the covariate. Let and denote the estimators of and respectively. For homoscedastic errors, is the standard pooled estimate, i.e., , while for the heteroscedastic case . Estimators of are discussed in Section 2.4. We seek to estimate by constructing -values for testing the null hypothesis against the alternative at each dose . The approximate -values are

Indeed, these approximate -values would correspond to the exact -values for the uniformly most powerful test if we worked with a known , a known and normal errors.

To the left of , the null hypothesis holds and these approximate -values converge weakly to a Uniform(0,1) distribution, for suitable estimators of . In fact, the distribution of s does not even depend on when . Moreover, to the right of , where the alternative is true, the -values converge in probability to . This dichotomous behavior of the -values on either side of can be used to prescribe consistent estimates of the latter. We can fit a stump, a piecewise constant function with a single jump discontinuity, to the s, , with levels 1/2, which is the mean of a Uniform (0,1) random variable, and 0 on either side of the break-point and prescribe the break-point of the best fitting stump (in the sense of least squares) as an estimate of . Formally, we fit a stump of the form , minimizing

| (3) |

over . Let . The success of our method relies on the fact that the s eventually show stump like dichotomous behavior. In this context, no estimate of could exhibit such a behavior directly. Our procedure can be thought of as fitting the limiting stump model to the observed s by minimizing an norm. In fact, the expression in (3) can be simplified, and it can be seen that , where The estimate can be computed easily via a simple search algorithm as it is one of the order statistics.

In heteroscedastic models, the estimation of the error variance can often be tricky. The proposed procedure can be modified to avoid the estimation of the error variance altogether for the construction of the -values, as the desired dichotomous behavior of the -values is preserved even when we do not normalize by the estimate of the variance. Thus, we can consider the modified -values and the dichotomy continues to be preserved as for a normally distributed with zero mean and arbitrary variance. In practice though, we recommend, whenever possible, using the normalized -values as they exhibit good finite sample performance.

Next, we prove the consistency of our proposed procedure when using the unnormalized -values. The technique illustrated here can be carried forward to prove consistency for other variants of the procedure, e.g., when normalizing by the estimate of the error variance, but require individual attention depending upon the assumption of heteroscedasticity/homoscedasticity.

Theorem 1.

Consider the dose-response setting of the problem and let denote the estimator based on the non-normalized version of -values, e.g., . Assume that i.e., given , there exists a positive integer , such that for , . Then,

2.3. Standard Regression Setting (Method 2)

We now consider the case when is much smaller than . Let denote the Nadaraya–Watson estimator, where and , with being a symmetric probability density or simply a kernel and the smoothing bandwidth. We take for . Let and denote estimators of and respectively. An estimate of can be constructed through standard techniques, e.g., smoothing or averaging the squared residuals , depending upon the assumption of heteroscedastic or homoscedastic errors.

For , the statistic converges to a normal distribution with zero mean and variance with . The approximate -value for testing against can then be constructed as:

where . It can be seen that these -values also exhibit the desired dichotomous behavior. Finally, an estimate of is obtained by maximizing

| (4) |

over . Let . Under suitable conditions on , this estimator can be shown to be consistent when grows large.

We have avoided sophisticated means of estimating , as our focus is on estimation of , and not particularly on efficient estimation of the regression function. Also, the Nadaraya–Watson estimate does not add substantially to the computational complexity of the problem and provides a reasonably rich class of estimators through choices of bandwidths and kernels.

In many applications, particularly when and under heteroscedastic errors, estimating the variance function accurately could be cumbersome. As with Method 1, Method 2 can also be modified to avoid estimating the error variance, e.g., the estimator constructed using (4), based on s, with . Next, we prove consistency for the proposed procedure when we do not normalize by the estimate of the variance. The technique illustrated here can be carried forward to prove consistency for other variants of the procedure. We make the following additional assumptions.

-

(a)

For some , the functions and , , are continuous.

-

(b)

The kernel is either compactly supported or has exponentially decaying tails, i.e., for some , and , and for all sufficiently large , , where has density . Also, .

Assumption (a) is very common in non-parametric regression settings for justifying asymptotic normality of kernel based estimators. Also, the popularly used kernels, namely uniform, Gaussian and Epanechnikov, do satisfy assumption (b).

Theorem 2.

Consider the standard regression setting of the problem with staying fixed and . Assume that as . Let denote the estimator computed using . Then,

Remark 1.

The model in (2) incorporates the situations with discrete responses. For example, we can consider binary responses with s indicating a reaction to a dose at level . We assume that the function , the probability that a subject yields a reaction at dose , is of the form (1) and takes values in so that . The results from this section as well as those from Section 2.2 will continue to hold for this setting.

Remark 2.

Our assumption of continuity of can be dropped and the results from this section as well as those from Section 2.2 will continue to hold provided that is bounded and continuous almost everywhere with respect to Lebesgue measure. This includes the classical change-point problem where has a jump discontinuity at but is otherwise continuous.

2.4. Estimators of

Suitable estimates of are required that satisfy the conditions stated in Theorems 1 and 2. In a situation where may be safely assumed to be greater than some known positive , an estimate of can be obtained by taking the average of the response values on the interval . The estimator would be -consistent and would therefore satisfy the required conditions. Such an estimator is seen to be reasonable for most of the data applications that are considered in this paper. In situations when such a solution is not satisfactory, we propose an approach to estimate that does not require any background knowledge, once again using -values.

We now construct an explicit estimator of in the dose-response setting, as required in Theorem 1, using -values. For convenience, let . Let . As increases, for , converges to 1 in probability, while for , converges to 0 in probability. For any , it is easy to see that always converges to 0, whereas when , converges to 0 for and converges to for . Thus, it is only when that s are closest to for a substantial number of observations. This suggests a natural estimate of :

| (5) |

Theorem 3 shows that under some mild conditions and homoscedasticity, is , a condition required for Theorem 1. This proof is given in Supplementary Material 1.

Theorem 3.

Consider the same setup as in Theorem 1. Assume that the errors are homoscedastic with variance . Further suppose that the regression function satisfies:

-

(A)

Given , there exists such that, for every ,

Also assume that , the density function of , converges pointwise to , the standard normal density. Then .

Remark 3.

Condition (A) is guaranteed if, for example, is strictly increasing to the right of although it holds under weaker assumptions on . In particular, it rules out flat stretches to the right of . The assumption that converges to is not artificial, since convergence of the corresponding distribution functions to the distribution function of the standard normal is guaranteed by the central limit theorem.

This approach in (5) can also be emulated to construct estimators of for the standard regression setting by just going through the procedure with s instead of s and it is clear that this estimator is consistent. However, the theoretical properties of this estimator, such as the rate of convergence, are not completely known. Nevertheless, the procedure has good finite sample performance as indicated by the simulation studies in Section 3. The estimator is positively biased. This is due to the fact that a value larger than is likely to minimize the objective function in (5) as it can possibly fit the -values arising from a stretch extending beyond , in presence of noisy observations. The values smaller than do not get such preference as the true function never falls below .

2.5. To smooth or not to smooth

The consistency of the two methods established in the previous sections justifies good large sample performance of the procedures, but does not provide us with practical guidelines on which method to use given a real application. In dose-response studies, it is quite difficult to find situations where both and are large. Typically, such studies do not administer too many dose levels which precludes from being large. So, we compare the finite sample performance of the two methods for different allocations of and to highlight their relative merits.

We study the performance of the two methods for three different choices of regression functions. All these functions are assumed to be at the baseline value 0 to the left of . Specifically, is a piece-wise linear function rising from 0 to 0.5 between and 1; , a convex curve, grows like a quadratic beyond , and reaches 0.5 at 1; rises linearly with unit slope for values ranging from to 0.8 and then decreases with unit slope for values between 0.8 and 1.0. So, and are strictly monotone to the right of and exhibit increasing level of smoothness at . On the other hand, is tent-shaped and estimating is expected to be harder for compared to .

For each allocation pair and a choice of a regression function, we generate responses , with , the s being independent with . The s are sampled from Uniform(0,1). The performance for estimating is studied based on root mean square error computed over 2000 replicates, assuming a known variance and a known . For illustrative purposes, we use the Gaussian kernel for Method 2. Based on heuristic computations, a bandwidth of the form is chosen as it is expected to attain the minimax rate of convergence for estimating a cusp of order , as per Raimondo (1998). For and , = 1 while for , is 2. We report the simulations for the best which minimizes the average of the root mean square errors for the sample sizes considered, over a fine grid.

There are results in the literature which suggest a possibly different minimax rate of convergence based on calculations in a slightly different model (Neumann, 1997; Goldenshluger et al., 2006) and hence a possibly different choice of optimal bandwidth. But not much improvement was seen in terms of the root mean square errors for other choices of bandwidth.

The root mean square errors and the biases for each allocation pair are given in Table 1. Both procedures are inherently biased to the right as the -values are not necessarily close to zero to the immediate right of . When and are comparable, e.g., and , Method 2, which relies on smoothing, does not perform well compared to Method 1. However, when is much smaller than , e.g., and , smoothing is efficient and Method 2 is preferred over Method 1. When both and are large, both methods work well. As Method 1 does not require selecting any tuning parameter, we recommend Method 1 in such situations.

| Method 1 | Method 2 | Method 1 | Method 2 | Method 1 | Method 2 | |

| (5, 5) | 16.9, 4.5 | 18.0, 9.6 | 20.2, 11.6 | 21.8, 10.9 | 20.5, 7.5 | 23.7, 14.3 |

| (5, 10) | 15.7, 6.7 | 16.6, 9.1 | 21.8, 17.2 | 21.3, 11.5 | 20.1, 10.9 | 20.8, 12.4 |

| (10, 10) | 13.4, 3.3 | 14.1, 5.6 | 19.0, 13.9 | 19.3, 8.6 | 14.9, 4.6 | 15.6, 6.9 |

| (10, 15) | 11.8, 4.9 | 12.6, 5.2 | 18.7, 15.5 | 19.0, 7.8 | 12.2, 5.3 | 12.9, 5.8 |

| (10, 20) | 10.8, 6.2 | 10.9, 4.6 | 18.5, 16.7 | 17.6, 6.9 | 10.9, 6.4 | 11.0, 4.9 |

| (15, 10) | 12.5, 1.8 | 12.6, 4.0 | 17.7, 11.7 | 18.4, 7.0 | 13.5, 2.0 | 13.2, 4.6 |

| (15, 15) | 10.4, 3.8 | 10.9, 4.0 | 17.2, 14.0 | 17.5, 6.6 | 10.9, 3.8 | 11.2, 3.8 |

| (15, 20) | 9.4, 4.2 | 9.8, 3.8 | 17.0, 14.9 | 17.4, 5.9 | 9.2, 4.4 | 10.0, 3.6 |

| (20, 10) | 12.4, 1.0 | 12.3, 2.9 | 16.5, 11.2 | 17.5, 6.5 | 12.7, 0.7 | 12.3, 3.9 |

| (20, 15) | 10.2, 2.5 | 10.6, 2.5 | 16.2, 13.3 | 17.0, 5.8 | 10.3, 2.6 | 10.6, 2.7 |

| (20, 20) | 8.9, 3.3 | 9.7, 2.3 | 15.9, 13.9 | 16.1, 5.4 | 8.7, 3.6 | 9.3, 2.7 |

| (3, 80) | 16.2, 14.5 | 10.5, 8.0 | 26.9, 26.2 | 16.4, 9.3 | 19.7, 16.6 | 11.0, 8.3 |

| (3, 100) | 16.2, 14.6 | 9.9, 7.7 | 27.0, 26.5 | 15.9, 8.9 | 18.7, 15.9 | 9.8, 7.4 |

| (4, 80) | 14.1, 12.4 | 9.4, 6.9 | 24.8, 24.2 | 15.7, 8.6 | 15.0, 12.9 | 9.8, 6.8 |

| (4, 100) | 14.0, 12.5 | 8.8, 6.3 | 24.9, 24.4 | 14.8, 7.8 | 14.4, 12.5 | 8.7, 6.3 |

2.6. Extension to Dependent Data

The global warming data falls under the standard regression setup, but involves dependent errors. Moreover, the data arises from a fixed design setting, with observations recorded annually. Here, we discuss the extension of Theorem 2 in this setting. Under fixed uniform design, we consider the model . Under such a model, and must be viewed as triangular arrays. The estimator of the regression function is . For each , we assume that the process is stationary and exhibits short-range dependence. Under Assumptions 1-5, listed in Robinson (1997), it can be shown that , and , converge jointly in distribution to independent normals with zero mean. In this setting, the working -values, defined here to be , still exhibit the desired dichotomous behavior. To keep the approach simple, we have not normalized by the estimate of the variance as this would have involved estimating the auto-correlation function. The conclusions of Theorem 2 can be shown to hold when is constructed using (4) based on s. Here, is constructed via averaging the responses over an interval that can be safely assumed to be on the left of , as discussed in Section 2.4.

3. Simulation Results and Data Analysis

3.1. Simulation Studies

We consider the same three choices of the regression function , and , as in Section 2.5. The data are generated for allocation pair and a choice of regression function, with the errors being independent , where . The s are again sampled from Uniform(0,1). We study the performance of the two methods when the estimates of are constructed using -values that are normalized by their respective estimates of variances.

Firstly, we consider Method 1. In Table 2, we report the root mean square error and the bias for the estimators of and , for different choices of and . For moderate sample sizes, shows greater root mean square errors in general than and as the signal is weak close to 1 for . For large sample sizes, the performance of the estimate is similar for and and is better than that for , which can be ascribed to being smoother at . The procedure is inherently biased to the right as -values are not necessarily close to zero to the immediate right of . Further, the estimator, on average, moves to the left with increase in as the desired dichotomous behavior becomes more prominent.

| (5, 5 ) | 25.5, 21.5 | 17.5, 9.9 | 28.2, 25.5 | 13.4, 6.0 | 31.2, 26.2 | 14.2, 8.4 |

| (5, 10 ) | 24.8, 20.5 | 14.3, 8.6 | 27.1, 22.3 | 10.2, 4.9 | 30.3, 24.3 | 11.2, 7.2 |

| (10, 10 ) | 20.7, 15.7 | 12.4, 6.7 | 24.6, 21.6 | 7.7, 3.5 | 27.2, 21.5 | 10.4, 6.9 |

| (10, 20 ) | 17.2, 13.9 | 9.0, 5.2 | 24.0, 22.4 | 5.4, 2.9 | 24.8, 19.8 | 8.6, 6.2 |

| (10, 50 ) | 13.6, 12.1 | 5.6, 3.8 | 23.5, 22.8 | 3.8, 2.7 | 18.6, 15.7 | 7.0, 5.8 |

| (20, 50 ) | 9.0, 7.6 | 3.1, 1.8 | 19.4, 18.7 | 2.5, 1.7 | 12.4, 10.0 | 5.0, 3.4 |

| (50, 100 ) | 5.0, 4.3 | 1.1, 0.7 | 15.2, 14.8 | 1.2, 0.9 | 5.2, 4.6 | 1.4, 0.9 |

Next, we study the performance of Method 2. As the estimation procedure is entirely based on , without loss of generality, we take to be 1. We again work with the Gaussian kernel with the smoothing bandwidth chosen in the same fashion as in Section 2.5. In Table 3, we report the root mean square error and the bias for the two estimators, for different choices of and . We see trends similar to those for Method 1, across the choices of the regression functions.

We studied the performance of the estimates under settings where is closer to the boundary of . Optimal allocation pairs were also computed for a given model and a fixed budget . These details are skipped here but can be found in Section 5.1 of the Supplementary Material 1. We also compared Method 1 to some competing procedures developed in the pharmacological dose-response setting to identify the minimum effective dose, namely the approaches in Williams (1971), Hsu & Berger (1999), Chen (1999) and Tamhane & Logan (2002). Method 1 was seen to perform well in comparison with these methods. For more details, see Section 5.2 of the Supplementary Material 1.

| 20 | 28.5, 17.9 | 20.9, 10.5 | 29.0, 17.8 | 14.7, 5.7 | 32.6, 22.4 | 17.4, 8.4 |

| 30 | 26.8, 15.5 | 18.4, 9.4 | 26.8, 14.6 | 12.2, 3.8 | 31.9, 21.8 | 15.1, 7.4 |

| 50 | 23.7, 13.8 | 15.8, 8.0 | 24.4, 12.4 | 9.9, 3.1 | 28.4, 18.7 | 13.1, 6.9 |

| 80 | 21.5, 11.2 | 13.7, 6.6 | 22.2, 8.4 | 7.8, 1.9 | 27.0, 17.8 | 11.7, 6.8 |

| 100 | 19.5, 9.6 | 12.5, 5.3 | 21.6, 8.2 | 7.5, 1.7 | 25.1, 14.7 | 10.9, 6.1 |

| 200 | 15.9, 6.2 | 8.8, 3.5 | 19.1, 6.0 | 4.9, 1.1 | 21.0, 12.2 | 9.2, 5.3 |

| 500 | 10.4, 0.6 | 4.6, 1.4 | 16.4, 3.9 | 2.7, 0.5 | 14.2, 5.4 | 6.0, 2.5 |

| 1000 | 9.5, 0.4 | 3.1, 0.7 | 15.0, 2.0 | 2.0, 0.4 | 10.5, 2.1 | 3.9, 1.2 |

| 1500 | 8.5, 0.3 | 2.3, 0.5 | 14.8, 1.5 | 1.8, 0.3 | 8.8, 0.8 | 2.8, 0.8 |

| 2000 | 7.2, 0.2 | 2.0, 0.5 | 13.8, 0.7 | 1.5, 0.2 | 8.1, 0.1 | 2.3, 0.5 |

Based on our simulation study, including results not shown here due to space considerations, the following practical recommendations are in order. In terms of optimal allocation under a fixed budget , it is better for one to invest in an increased number of covariate values , rather than replicates . In the case where the threshold is closer to the boundaries, investment in proves fairly important. Further, when the sample size is reasonably large, the procedure that avoids estimating the variance function and works with non-normalized -values, is competitive and is recommended in the regression settings with heteroscedastic errors and time-series.

3.2. Data Applications

The first data application deals with a dose-response experiment that studies the effect on cells from the IPC-81 leukemia rat cell line to treatment with 1-methyl-3-butylimidazolium tetrafluoroborate, at different doses measured in M, micro mols per liter (Ranke et al., 2004). The substance treating the cells is an ionic liquid and the objective is to study its toxicity in a mammalian cell culture to assess environmental hazards. The question of interest here is at what dose level toxicity becomes lethal and cell cultures stop responding.

It can be seen from the physiological responses shown in the left panel of Fig. 1, that there is a decreasing trend followed by a flat stretch. Hence, it is reasonable to postulate a response function that stays above a baseline level until a transition point beyond which it stabilizes at its baseline level. We assume errors to be heteroscedastic, as the variability in the responses changes with level of dose, with more variation for moderate dose levels compared to extreme dose levels. This is the small case with and being comparable; in fact, . Hence we apply Method 1 to this problem. The estimate of was constructed using the procedure based on -values as described in Section 2.4. We get with the corresponding , the third observation from right. We believe that this is an accurate estimate of , since the cell-cultures exhibit high responses at earlier dose levels and no significant signal to the right of the computed .

The second example, as discussed in the introduction, involves measuring mercury concentration in the atmosphere through the light detection and ranging technique. There are 221 observations with the predictor variable range varying from 390 to 720. As supported by the middle panel of Fig. 1, the underlying response function is at its baseline level followed by a steep descent, with the point of change being of interest. There is evidence of heteroscedasticity and hence, we employ Method 2 without normalizing by the estimate of the variance. It is reasonable to assume here that till the range value 480 the function is at its baseline. The estimate of is obtained by taking the average of observations until range reaches 480, which gives The estimates , computed for bandwidths varying from 5 to 30, show a fairly strong agreement as they lie between 534 and 547, with the estimates getting bigger for larger bandwidths. The cross-validated optimal bandwidth for regression is 14.96 for which the corresponding estimate of is 541.

The global warming data contains global temperature anomalies, measured in degree Celsius, for the years 1850 to 2009. These anomalies are temperature deviations measured with respect to the base period 1961–1990. The data are modeled as described in Section 2.6. As can be seen in the right panel of Fig. 1, the function stays at its baseline value for a while followed by a non-decreasing trend. The flat stretch at the beginning is also noted in Zhao and Woodroofe (2011) where isotonic estimation procedures are considered in settings with dependent data. The estimate of the baseline value, after averaging the anomalies up to the year 1875, is . With the dataset having 160 observations, estimates of the threshold were computed for bandwidths ranging from 5 to 30. The estimates varied over a fairly small time frame, 1916–1921. This is consistent with the observation on page 2 of Zhao and Woodroofe (2011) that global warming does not appear to have begun until 1915. The optimal bandwidth for regression obtained through cross-validation is 13.56, for which is 1920.

3.3. Extensions

Here we discuss some of the possible extensions of our proposed procedure.

(i) Fixed design setting: Although the results in this paper have been proven assuming a random design, they can be easily extended to a fixed design setup. Consistency of the procedures will continue to hold.

(ii) Unequal replicates: In this paper, we dealt with the case of a balanced design with a fixed number of replicates for every dose level . The case of varying number of replicates can be handled analogously. In the dose-response setting, Theorem 1 will continue to hold provided the minimum of the s goes to infinity. In the standard regression setting, Theorem 2 can also be generalized to the situation with unequal number of replicates at different doses.

(iii) Adaptive stump model: The use of 1/2 and 0 as the stump levels may not always be the best strategy. The -values to the right of may not be small enough to be well approximated by 0 for small . One can deal with this issue by using a more adaptive approach which keeps the stump-levels unspecified and estimates them from the data. For example, in the dose-response setting, one can define,

Please see pages 5 and 16 in Supplementary Material 1 for more details on this estimator.

4. Concluding Discussion

We briefly discuss a few issues, some of which constitute ongoing and future work on this topic. While we have developed a novel methodology for threshold estimation and established consistency properties rigorously, a pertinent question that remains to be addressed is the construction of confidence intervals for . A natural way to approach this problem is to consider the limit distribution of our estimators for the two settings and use the quantiles of the limit distribution to build asymptotically valid confidence intervals. This is expected to be a highly non-trivial problem involving hard non-standard asymptotics. The rate of convergence crucially depends on the order of the cusp, , at . As mentioned earlier, the minimax rate for this problem is as per Raimondo (1998). This is in disagreement with the faster rates obtained in Neumann (1997) for a change-point estimation problem in a density deconvolution model. There are recent results (Goldenshluger et al., 2006, 2008) which suggest that Neumann’s rate should be optimal, but an asymptotic equivalence between the density model in Neumann (1997) and the regression model assumed in Raimondo (1998) and our paper has not been formally established. Based on preliminary calculations, it is expected that our procedure will, at least, attain a rate of , under optimal allocation between and for Method 1 and for a suitable choice of bandwidth for Method 2.

In this paper, we have restricted ourselves to a univariate regression setup. Our approach can potentially be generalized to identify the baseline region, the set on which the function stays at its minimum, in multi-dimensional covariate spaces. This is a special case of level sets estimation, a problem of considerable interest in statistics and engineering. The -values, constructed analogously, will continue to exhibit a limiting dichotomous behavior which can be exploited to construct estimates of the baseline region. Procedures that look for a jump in the derivative of a certain order of (Mueller, 1992; Raimondo, 1998) do not have natural extensions to high dimensional settings as the order of differentiability can vary from point to point on the boundary of the baseline region.

Acknowledgement

We thank Harsh Jain for bringing to our attention a threshold estimation problem that eventually led to the formulation and development of this framework. The work of the authors were partially supported by NSF and NIH grants.

Supplementary Material

The proof of Theorem 3, an extensive simulation study and a discussion on other variants of the proposed methods are given in Supplementary Material 1 available at http://arxiv.org/PScache/arxiv/pdf/1008/1008.4316v1.pdf.

Appendix

Proofs

We start with establishing an auxiliary result used in the subsequent developments.

Theorem 4.

Let be an indexing set and a family of real-valued stochastic processes indexed by . Also, let be a family of deterministic functions defined on , such that each is maximized at a unique point . Here is a metric space and denote the metric on by . Let be a maximizer of . Assume further that:

(a) , and

(b) for every , , where denotes the open ball of radius around .

Then, (i) . Furthermore, if is a metric space and is continuous in , then (ii) , provided converges to . In particular, if the s themselves are deterministic functions, the conclusions of the theorem hold with the convergence in probability in (i) and (ii) replaced by usual non-stochastic convergence.

Proof.

We provide the proof in the case when is a sub-interval of the real line, the case that is relevant for our applications. However, there is no essential difference in generalizing the argument to metric spaces - euclidean distances simply need to be replaced by the metric space distance and open intervals by open balls.

Given , we need to deal with , where is the outer probability. The event implies that for some , and therefore This is equivalent to Now, and the left side of the above inequality is bounded above by

implying that which, in turn, implies that by definition. Hence By assumptions (a) and (b), goes to 0 and therefore so does . ∎

Remark 4.

We will call the sequence of steps involved in deducing the inclusion:

as generic steps. Very similar steps will be required again in the proofs of the theorems to follow. We will not elaborate those arguments, but refer back to the generic steps in such cases.

of Theorem 1.

To exhibit the dependence on the baseline value (or its estimate), we use notations of the form and . For convenience, let and . As changes, the distribution of changes, and so we effectively have a triangular array , say. Using empirical process notation, , where denotes the empirical measure of the data. Firstly, we find the limiting process for . Define where can be simplified as

| (6) |

where . Observe that for , as , converges in distribution to for and , in probability, for . Thus, for all , where . Let be the same expression for in (6) with replaced by , e.g., . Observe that for , for all , and . Also, it is easy to see that is the unique maximizer of . Now, the difference , can be bounded by which goes to 0 by the dominated convergence theorem. As the bound does not depend on , we get , where denotes the supremum. By Theorem 4, as . It would now suffice to show that is .

Fix and consider the event . Since maximizes and maximizes , by arguments analogous to the generic steps in the proof of Theorem 4, we have:

where .

We claim that there exists and an integer such that for all . To see this, let us bound below by . As as , it is enough to show that there exists such that for all sufficiently large , . We split into two parts as . Notice that by the continuity of , the second term goes to . To handle the first term, notice that is a continuous function with a unique maximum at . There exists such that for all , we have as . So, for , . As is continuous, this infimum is attained in the compact set and is strictly positive. Thus, a positive choice for , as claimed, is available.

The claim yields,

For the first term, notice that, . This is bounded above by . As , for , is bounded by , which goes in probability to zero.

To show that the last term in (of Theorem 1.) goes to zero, consider the class of functions with the envelope . The class is formed by multiplying a fixed function with a bounded Vapnik- Chervonenkis classes of functions and therefore satisfies the entropy condition in the third display on page 168 of van der Vaart & Wellner (1996). It follows that satisfies the conditions of Theorem 2.8.1 of van der Vaart & Wellner (1996) and is therefore uniformly Glivenko–Cantelli for the class of probability measures , i.e.,

for every as . Thus, we get . This completes the proof of the theorem. ∎

Recall that . The following standard result from non-parametric regression theory is useful in proving Theorem 2. The proof follows, for example, from the results in Section 2.2 of Bierens (1987).

Lemma 1.

Assume that and is continuous on . is continuous on [0,1]. We then have:

-

(i)

For and ,

in distribution.

-

(ii)

For , in probability.

Proof of Theorem 2. Let and be as defined in proof of Theorem 1, e.g., . For notational convenience, let . We eventually show that converges to 0 in probability and then apply argmax continuous mapping theorem to prove consistency. By calculations similar to those in the proof of Theorem 1, , which converges to 0 in probability. So, it suffices to show that converges to 0 in probability. We first establish marginal convergence. We have

The first term, both in the numerator and the denominator of the argument, is asymptotically negligible and thus, the expression in (Proofs) equals . Using Lemma 1, this converges to , by definition of weak convergence. As , we get which converges to . Further, The first term in this expression goes to zero as . For , by calculations similar to (Proofs), . Using Lemma 1, and are asymptotically independent. Thus, by taking iterated expectations, it can be shown that . This justifies pointwise convergence, e.g., , for . Further, as , for , we have

The above two terms, under expectation, are independent and thus, the expression is bounded by . As is continuous on , . Thus, the processes are tight in using Theorem 15.6 in Billingsley (1968). So, converges weakly to as processes in . As the limiting process is degenerate and the map is continuous, by continuous mapping, we get converges in probability to zero. As is the unique maximizer of the continuous function and is tight as . Hence, by argmax continuous mapping theorem in van der Vaart & Wellner (1996), we get the result.

References

- Bierens (1987) Bierens, H. J. (1987). Kernel Estimators of Regression Functions, in: T. F. Bewley, ed., Advances in Econometrics, 1, (Cambridge University Press), 99-144.

- Billingsley (1968) Billingsley, P. (1968). Convergence of probability measures. Wiley, New York.

- Chen (1999) Chen, Y. (1999). Nonparametric Identification of the Minimum Effective Dose. Biometrics, 55, 1236–1240.

- Chen & Chang (2007) Chen, Y. & Chang, Y. (2007). Identification of the minimum effective dose for right-censored survival data. Comp. Statist. Data Ana., 51, 3213- 3222.

- Cox (1987) Cox, C. (1987). Threshold dose-response models in toxicology. Biometrics, 43, 511- 523.

- Delworth and Knutson (2000) Delworth, T.L. and Knutson, T.R. (2000). Simulation of early 20th century global warming. Science, 287, 2246- 2250.

- Goldenshluger et al. (2006) Goldenshluger, A. Tsybakov, A. and Zeevi, A. (2006). Optimal change–point estimation from indirect observations Ann. Statist., 34, 350–372.

- Goldenshluger et al. (2008) Goldenshluger, A., Juditsky, A. Tsybakov, A. and Zeevi, A. (2008). Change–point estimation from indirect observations. 1. Minimax Complexity. Ann. Inst. Henri Poincaré Probab. Stat., 44, 787–818.

- Holst et al. (1996) Holst, U., Hossjer, O., Bjorklund, C., Ragnarson, P. and Edner, H. (1996). Locally weighted least squares kernel regression and statistical evaluation of LIDAR measurements, Environmetrics, 7, 401 -416.

- Hsu & Berger (1999) Hsu, J. & Berger, R. (1999). Stepwise confidence intervals without multiplicity adjustment for dose–response and toxicity studies. J. Amer. Statist. Assoc., 94, 468 -482.

- Ibragimov & Khasminskii (1982) Ibragimov, I. A., and Khasminskii,R. Z. (1981). Statistical Estimation: Asymptotic Theory. Springer, New York.

- Koul & Qian (2002) Koul, H. L. and Qian, L. (2002). Asymptotics of maximum likelihood estimator in a two-phase linear regression model. C. R. Rao 80th birthday felicitation volume, Part II. J. Statist. Plann. Infer., 108, 99–119.

- Lan et al. (2009) Lan, Y., Banerjee, M. and Michailidis, G. (2009). Change-point estimation under adaptive sampling, Ann. Statist., 37, 1752–1791.

- Loader (1996) Loader, C. R. (1996). Change point estimation using nonparametric regression. Ann. of Statist., 24, 1667–1678.

- Melillo (1999) Melillo, J.M. (1999). Climate change: warm, warm on the range. Science, 283, 183 -184.

- Mueller (1992) Mueller, H. G. (1992). Change-points in nonparametric regression analysis. Ann. Statist., 20, 737–761.

- Neumann (1997) Neumann, M. H. (1997). Optimal change point estimation in inverse problems. Scand. J. Statist., 24, 503–521.

- Pons (2003) Pons, O. (2003). Estimation in a Cox regression model with a change–point according to a threshold in a covariate Ann. Statist., 31, 442–463.

- Pons (2009) Pons, O. (2009). Estimation and tests in distribution mixtures and change–points models. Paris.

- Raimondo (1998) Raimondo, M. (1998). Minimax estimation of sharp change points. Ann. Statist., 26, 1379–1397.

- Ranke et al. (2004) Ranke, J., Molter, K., Stock, F., Bottin–Weber, U., Poczobutt, J., Hoffmann, J., Ondruschka, B., Filser, J. and Jastorff B. (2004) Biological effects of imidazolium ionic liquids with varying chain lengths in acute Vibrio fischeri and WST-1 cell viability assays. Ecotoxicology and Environmental Safety, 28, 396 -404.

- Robinson (1997) Robinson, P. M. (1997). Large-sample inference for nonparametric regression with dependent errors. Ann. Statist., 25, 2054-2083

- Ruppert et al. (1997) Ruppert, D., Wand, M.P., Holst, U. and Hossjer, O. (1996). Local polynomial variance function estimation. Technometrics, 39, 262 -273.

- Tamhane & Logan (2002) Tamhane, A. and Logan, B. (2002). Multiple test procedures for identifying the minimum effective and maximum safe doses of a drug. J. Amer. Statist. Assoc., 97, 293–301.

- van der Vaart & Wellner (1996) van der Vaart, A. W. & Wellner, J. A. (1996). Weak Convergence and Empirical Processes. Springer, New York.

- Williams (1971) Williams, D. A. (1971). A Test for Differences between Treatment Means When Several Dose Levels are Compared with a Zero Dose Control. Biometrics, 27, 103–117.

- Zhao and Woodroofe (2011) Zhao, O. and Woodroofe, M.W. (2011). Estimating a monotone trend. To appear in Stat. Sinica.