Learning the Dependence Graph of Time Series with Latent Factors

Abstract

This paper considers the problem of learning, from samples, the dependency structure of a system of linear stochastic differential equations, when some of the variables are latent. In particular, we observe the time evolution of some variables, and never observe other variables; from this, we would like to find the dependency structure between the observed variables – separating out the spurious interactions caused by the (marginalizing out of the) latent variables’ time series. We develop a new method, based on convex optimization, to do so in the case when the number of latent variables is smaller than the number of observed ones. For the case when the dependency structure between the observed variables is sparse, we theoretically establish a high-dimensional scaling result for structure recovery. We verify our theoretical result with both synthetic and real data (from the stock market).

1 Introduction

Linear stochastic dynamical systems are classic processes that are widely used to model time series data in a huge number of fields: financial data [12], biological networks of species [28] or genes [2], chemical reactions [19, 21], control systems with noise [44], etc. An important task in several of these domains is learning the model from data [40]; doing so is often the first step in both data interpretation, and making predictions of future values or the effect of perturbations. Often one is interested in learning the dependency structure [25]; i.e. identifying, for each variable, which set of other variables it directly interacts with. For stock market data, for example, this can reveal which other stocks most directly affect a given stock.

We consider model structure learning in a particularly challenging yet widely prevalent setting: where (the time series of) some state variables are observed, and others are unobserved/latent. We are interested in learning the dependency structure between the observed variables. However, the presence of latent time series, if not properly accounted for by the model learning procedure, will result in the appearance of spurious interactions between observed variables – two observed variables that interact with the same unobserved variable may now be reported to be interacting. This happens, for example, if one uses the classic maximum-likelihood estimator [16], and persists even if we have observations over a long time horizon.

Suppose, for illustration, that we are interested in learning the dependency structure between the prices of a set of stocks via a linear stochastic model. Clearly, stock prices depend not only on each other, but are also jointly influenced by several variables that may not be part of our model, for example, currency markets, commodity prices etc.; these are latent time series. Their presence means that a naive structure learning algorithm (say max-likelihood) that takes as input only the stock prices, will report several spurious interactions; say, e.g. between all stocks that fluctuate with the price of oil.

Our work involves several significant differences from the large body of work on sparse recovery and graphical model learning. One is the fact that our samples are dependent on each other, with the degree of dependence governed by how finely the system is sampled. Another is the presence of latent variables. We put our work in context with related literature in Section 2.

Clearly there are several issues with regards to fundamental identifiability, and sample and computational complexity, that need to be defined and resolved. We do so below in the specific context of our model setting. We provide both theoretical characterization and guarantees of the problem, as well as numerical illustrations for both synthetic data and some real data extracted from stock market.

2 Related Work

We organize the most directly related work as follows (recognizing of course that these descriptions overlap).

Sparse Recovery and Gaussian Graphical Model Selection: It is now well recognized [39, 41, 33] that a sparse vector can be tractably recovered from a small number of linear measurements; and also that these techniques can be applied to do model selection (i.e. inferring the Markov graph structure and parameters) in Gaussian graphical models [33, 34, 13, 17, 45]. While ours problem is, in a sense, also one of sparse linear model selection, two differences between our setting and these papers is that they do not have any latent factors, and theoretical guarantees typically require independent samples. The simultaneous presence of both these characteristics is what makes ours a challenging setting. In particular, latent factors imply that these techniques will in effect attempt to find models that are dense, and hence not be able to have a high-dimensional scaling. Correlation among samples means we cannot directly use standard concentration results, and also brings in the interesting issue of the effect of sampling frequency; in particular, in our setting one can get more samples by finer sampling, but increased correlation means these do not result in better consistency.

Sparse plus Low-Rank Matrix Decomposition: Our results are based on the possibility of separating a low-rank matrix from a sparse one, given their sum (either the entire matrix, or randomly sub-sampled elements thereof) – see [9, 7, 11, 46, 6] for some recent results, as well as its applications in graph clustering [24, 23], collaborative filtering [37], image coding [20], etc. Our setting is different because we observe correlated linear functions of the sum matrix, and furthermore these linear functions are generated by the stochastic linear dynamical system described by the matrix itself. Another difference is that several of these papers focus on recovery of the low-rank component, while we focus on the sparse one. These two objectives have a very different high-dimensional scaling in our linear observation setting.

Inference with Latent Factors: In real applications of data driven inference, it is always a concern that whether or not there exist influential factors that have never been observed [31, 43]. Several approaches to this problem are based on Expectation Maximization (EM) [14, 35]; while this provides a natural and potentially general method, it suffers from the fact that it can get stuck in local optima (and hence is sensitive to initialization), and that it comes with weak theoretical guarantees. The paper [8] takes an alternative, convex optimization approach to the latent factor problem in Gaussian graphical models, and is of direct relevance to our paper. In [8], the objective is to find the number of latent factors in a Gaussian graphical model, given iid samples from the distribution of observed variables; they also use sparse and low-rank matrix decomposition. Differences between our paper and theirs is that we focus on recovering the support of the “sparse part”, i.e. the interactions between the observed variables exactly, while they focus on recovery the rank of the low-rank part (i.e. the number of latent variables). Our objective requires samples, theirs requires . Another major difference is that our observations are correlated, and hence sample complexity itself needs a different definition (viz. it is no more the number of samples, but rather the overall time horizon over which the linear system is observed).

System Identification: Linear dynamical system identification is a central problem in Control Theory [30]. There is a long line of work on this problem in that field including recent regularized convex optimization based approaches [15]. Recently, [3] considered the system identification problem as learning dependence graph of time series, without any latent variables. They implement the LASSO; the main contribution is characterizing sample complexity in the presence of sample dependence. In our setting, with latent variables, their method returns several spurious graph edges caused by marginalization of latent variables.

Time-series Forecasting: Motivated by finance applications, time-series forecasting has got a lot of attention during the past three decades [10]. In the model based approaches, it is assumed that the time-series evolves according to some statistical model such as linear regression model [4], transfer function model [5], vector autoregressive model [42], etc. In each case, researchers have developed different methods to learn the parameters of the model for the purpose of forecasting. In this paper, we focus on linear stochastic dynamical systems that are an instance of vector autoregressive models. Previous work toward estimating this model parameters include ad-hoc use of neural network [1] or support vector machine method [26], all without providing theoretical guarantees on the performance of the algorithm. Our work is different from these results because although our method provides better prediction comparing to similar algorithm, our main focus is sparse model selection not prediction. Perhaps, once a sparse model is selected, one can study the prediction quality as a separate subject.

3 Problem Setting and Main Idea

This paper considers the problem of structure learning in linear stochastic dynamical systems, in a setting where only a subset of the time series are observed, and others are unobserved/latent. In particular, we consider a system with state vectors and , for and dynamics described by

| (1) |

where, is an independent standard Brownian motion vector and are system parameters.

Task: We observe the process for some time horizon , but not the process . We are interested in learning the matrix , which captures the interactions between the observed variables.

We will also be interested in a similar objective for an analogous discrete time system with parameter :

| (2) |

for all . Here, is a zero-mean Gaussian noise vector with covariance matrix . The prameter can be thought of as the sampling step; in particular notice that as , we recover model (1) from model (2). The upper bound on ensures the stability of the discrete time system as required by our theorem. Intuitively, corresponds to the fastest convergence rate in the system and the upper bound on corresponds to the Nyquist minimum sampling rate required for the reconstruction of the signal. As done in [3], our proofs will initially focus on the discrete case (2), and derive results for (1) afterwards.

(A1) Stable Overall System: We only consider stable systems. In fact, we impose an assumption slightly stronger than the stability on the overall system. For the continuous system (1), we require . With slightly abuse of notation, for the discrete system (2), we require , where, .

As a consequence of this assumption, by Lyapunov theory, the continuous system (1) has a unique stationary measure which is a zero-mean Gaussian distribution with positive definite (otherwise, it is not unique) covariance matrix given by the solution of . Similarly, for the discrete time system (2), we have . This matrix has the form , where, and are the steady-state covariance matrices of the observed and latent variables, respectively, and is the steady-state cross-covariance between observed and latent variables. By stability, and .

Identifiability: Clearly, the above objective of identifying is in general impossible without some additional assumptions on the model; in particular, several different choices of the overall model (including different choices of ) can result in the same effective model for the process. would then be statistically identical under both models, and correct identification would not be possible even over an infinite time horizon. Additionally, it would in general be impossible to achieve identification if the number of latent variables is comparable to or exceeds the number of observed variables. Thus, to make the problem well-defined, we need to restrict (via appropriate assumptions) the set of models of interest.

3.1 Main Idea

Consider the discrete-time system (2) in steady state and suppose, for a moment, that we ignored the fact that there may be latent time series; in this case, we would be back in the classical setting, for which the (population version of) the likelihood is

Lemma 1.

For generated by (2), the the optimum is given by

Thus, the optimal is a sum of the original (which we want to recover) and the matrix that captures the spurious interactions obtained due to the latent time series. Notice that the matrix has the rank at most equal to number of latent time series. We will assume that the number of latent time series is smaller than the number of observed ones – i.e. – and hence is a low-rank matrix.

3.2 Identifiability

Besides identifying the effect of the latent time series, we would need the true model to be such that is uniquely identifiable from . We choose to study models that have a local-global structure where (a) each of the observed time series interacts with only a few other observed series, while (b) each of the latent series interacts with a (relatively) large number of observed series. In the stock market example, for instance, this would model the case where the latent series corresponds to macro-economic factors, like currencies or the price of oil, that affect a lot of stock prices.

In particular, let be the maximum number of non-zero entries in any row or column of ; it is the maximum number of other observed variables any given observed variable directly interacts with. Note that this means is a sparse matrix. Let and assume it has SVD , and recall that its rank is . Then, following [11], is said to be -incoherent if is the smallest real number satisfying

where, ’s are standard basis vectors and is vector 2-norm. Smaller values of mean the row/column spaces make larger angles with the standard bases, and hence the resulting matrix is more dense.

(A2) Identifiability: We require that the of the sparse matrix and the of the low-rank , which has rank , satisfy .

3.3 Algorithm

Recall that our task is to recover the matrix given observations of the process. We saw that the max-likelihood estimate (in the population case) was the sum of and a low-rank matrix; we subsequently assumed that is sparse. It is natural to use the max-likelihood as the loss function for the sum of a sparse and low-rank matrix, and separate appropriate regularizers for each of the components. Thus, for the continuous-time system observed up to time , we propose solving

| (3) | ||||

and for the discrete-time system given samples, we propose solving

| (4) |

Here is the norm (a convex surrogate for sparsity), and is the nuclear norm (i.e. sum of singluar values, a convex surrogate for low-rank). The optimum of (4) or (3) is our estimate of , and our main result provides conditions under which we recover the support of , as well as a bound on the error in values (maximum absolute value). We provide a bound on the error (spectral norm) for the low-rank part. Notice that the discrete objective function goes to the continuous one as .

3.4 High-dimensional setting

Note that when is a sparse matrix, the actual degrees of freedom between the observed variables is smaller than that evinced by the ambient dimension . Indeed, we will be interested in recovering with a number of samples that is potentially much smaller than (for small ). In the special case when we are in steady state and (i.e. large) the recovery of each row of is akin to a LASSO [39] problem (of sparse vector recovery from noisy linear measurements) with being the covariance of the design matrix. We thus require to satisfy incoherence conditions that are akin to those in LASSO (see e.g. [41] for the necessity of such conditions).

(A3) Incoherence: To control the effect of the irrelevant (not latent) variables on the set of relevant variables, we require

where, is the support of the row of and is the complement of that. The norm is the maximum of the -norm of the rows.

4 Main Results

In this section, we present our main result for both Continuous and Discrete time systems. We start by imposing some assumptions on the regularizers and the sample complexity.

(A4) Regularizers: We need to impose some assumptions on the regularizers to be able to guarantee our result. Let

be the constant capturing the effect of initial condition and latent variables through matrix . We impose the following assumptions on the regularizers:

(A4-1) .

(A4-2)

.

Note: In practice, we let and , with the constants chosen by cross-validation over prediction performance.

(A5) Sample Complexity: In our setting, samples are dependent; in particular, the smaller the the more dependent two subsequent samples. Sample complexity is thus governed by the total time horizon over which we observe the system, and not simply ; indeed finer sampling (i.e. smaller ) requires a larger number of samples. For a probability of failure , we require

Here, is a constant independent of any other system parameter; for example, suffices.

The above is required to ensure that the empirical covariance matrix is close to the steady-state . Of course the constraint ensures that the sampling intervals cannot be too large. Note that is the total time over which the system is observed; a finer sampling cannot yield a smaller horizon, because of increased dependence between samples.

Let and .

The following (unified) theorem states our main result for both discrete and continuous time systems.

Theorem 1.

If assumptions (A1)-(A5) are satisfied, then with probability , our algorithm outputs a pair satisfying

(a) Subset Support Recovery:

(b) Error Bounds:

(c) Exact Signed Support Recovery: If additionally we have that the smallest magnitude of a non-zero element of satisfies , then we obtain full signed-support recovery .

Note: Note that , as defined in (A4-1), depends on the sample complexity , and goes to as becomes large. Thus it is possible to get exact signed support recovery by making large.

Remark 1: Our result shows that, in sparse and low-rank decomposition for latent variable modeling, recovery of only the sparse component seems to be possible with much fewer samples – – as compared to, for example, the recovery of the exact rank of the low-rank part; the latter was show to require samples in [8].

Remark 2: The above theorem shows that, even in the presence of latent variables, our algorithm requires a similar number of samples (i.e. upto universal constants) as previous work [3] required in the absence of hidden variables. Of course, this is true as long as identifiability (A2) holds. Note that the absence of such identifiability conditions makes even simple sparse and low-rank matrix decomposition [9] ill-posed. Note also that the quantity , which characterizes the error in the low-rank term, goes to 0 as increases (which decreases ).

Remark 3: Although our theoretical result shows a scaling proportional for the sample complexity, the theoretical result suggests that the correct scaling factor is . We suspect our result as well as Bento et al. [3], can be tightened and we are currently working on that.

Illustrative Example: Consider a simple idealized example that helps give intuition about the above theorem. Suppose that we are in the continuous time setting, where each latent variable depends only on its own past, updating according to and for each observed variable depends only on its own past and a unique latent variable , i.e., . There are latent variables, and assume that each latent variable affects exactly observed variables in this way.

In terms of the matrix , the overall (observed + latent) system has the form given by the matrix below

![[Uncaptioned image]](/html/1106.1887/assets/x1.png)

Here , , and . This matrix satisfies stability assumption (A1). In the matrix , each column has exactly entries that are , and the remaining are . Each row of has exactly one entry that is , and the remaining are ; note that the columns of are orthogonal. We start from zero initial condition with (continuous time system). With this, and .

For this idealized setting, we can exactly evaluate all the quantities we need. In particular, it is not hard to show (done in Appendix) that the steady-state covariance matrices are and . The resulting low-rank matrix is , which gives ; the incoherence parameter , and hence we need by assumption (A2). Moreover, we can show that for this example and hence the assumption (A3) is also satisfied.

Similarly. evaluating the other parameters in Theorem 1, we get that the observation time should be for structure recovery with probability greater than . In this case, we also have and providing the error bounds and .

5 Proof of the Theorem

In this section, we first introduce some notations and definitions and then, provide a three step proof technique to prove the main theorem for the discrete time system. The proof of the continuous time system is done via a coupling argument in the appendix.

Before we proceed to the details, we would like to make a high level technical remark on the novelties of our proof. There are two key novel ingredients in the proof enabling us to get the low sample complexity result in our theorem. The first ingredient comes from our new set of optimality conditions inspired by [7]. This optimality conditions enable us to certify an approximation of while certifying the exact sign support of . The second ingredient comes from the bounds on the Schur complement of the perturbation of positive semi-definite matrices [38]. This result enables us to get a bound on the Schur complement of a perturbation of a positive semi-definite matrix of size with only samples.

Given a matrix , let be the subspace of matrices whose their support is a subset of the matrix . The orthogonal projection of a matrix to is denoted by . Denote the orthogonal complement space with with orthogonal projection .

For any matrix , if the SVD is , then let denote the subspace spanned by all matrices that have the same column space or row space as . The orthogonal projection of a matrix to is denoted by . Denote the orthogonal complement space with with orthogonal projection . We define a metric to measure the closeness of two subspaces and as follows

Finally, let to shorten the notation and be a singular value decomposition.

The proof steps are as follows:

-

•

STEP 1: We construct a candidate primal optimal solution with the desired sparsity pattern using the restricted support optimization problem. We refer to this as oracle problem:

(5) This oracle is similar to the one used in [8]. Note that this is a proof technique, not a method to construct the solution.

-

•

STEP 2: We Write down a novel set of sufficient (stationary) optimality conditions for to be the unique solution of the (unrestricted) optimization problem (4):

Lemma 2.

If , then , the solution to the oracle problem (5), is the unique solution of the problem (4) if there exists a matrix such that

(C1) . (C2) .

(C3) . (C4) .

(C5) .

Upon existence of , the solution of the oracle problem not only is the solution to the original problem (4), but also satisfies the claim of the theorem.

Lemma 3.

Provided in Lemma 2 exists, we have

-

(a)

.

-

(b)

and

-

(c)

If then .

Part (a) is immediate by the constraints of the oracle problem and provided the bound in (b) and part (a), the result of part (c) naturally follows. We prove part (b) in the Appendix D. Now, it suffices to construct a dual variable .

-

(a)

-

•

STEP 3: Constructing a dual variable that satisfies the sufficient optimality conditions stated in Lemma 2. First notice that under assumption (A2), we have [11]. For matrices and , let

It has been shown in [11] that if then both infinite sums converge. Suppose we have the SVD decomposition . Let

where, is a matrix such that (C5) is satisfied. As a result of our construction, we have and by optimality of , we have . This entails that and hence (C1) is satisfied.

To show (C3) holds, we need the next lemma.

Lemma 4.

.

By our construction, we have by Lemma 4. Consequently, and hence (C3) is also satisfied, considering the oracle constraint bound .

It suffices to show that (C2) and (C4) are satisfied with high probability. This has been shown in the next Lemma.

Lemma 5.

Under assumptions (A1)-(A5), satisfies conditions (C2) and (C4) with probability for some positive constants and .

This concludes the proof of the theorem for the discrete time system.

-

•

STEP 4: Denote and let

Having the result for the discrete time system, it suffices (see proof of Theorem 1.1 in [3] for more details) to show that for a given continuous time system, there exists a discrete time system with and such that almost surely,

as for a fixed (and hence, ).

Let be the matrix satisfying the continuous time Lyapunov stability equation and be the matrix satisfying the discrete time Lyapunov stability equation . It is easy to see that as by the uniqueness of the stationary distribution. Moreover, by Lemma 12, we know that as .

Now, let the initial state of the discrete time system be

and the noise . It can be easily checked that if the continuous time is a Brownian motion. Thus, and are coupled and the almost sure convergence, follows from the convergence of random walks to Brownian motions [32]. This concludes the proof of the theorem for continuous time systems.

6 Experimental Results

6.1 Synthetic Data

Motivated by the example discussed in the paper, we simulate a similar (but different) dynamic system for the purpose of our experiments. Consider the system where each latent variable is only evolves by itself, i.e., and is a diagonal matrix. Moreover, assume that each observed variable is affected by exactly two latent variable, i.e., each column of has non-zeros and each row of has two non-zeros. We randomly select a support of size per row for and draw all the values of and i.i.d. standard Gaussian. To make the matrix negative definite (hence, stable), using Geršgorin disk theorem [18], we put a large-enough negative value on the diagonals of and .

We generate the data according to the continuous time model. The solution to the first order system can be written as

where, is a generalization of the exponential function to matrices. We sub-sample this system at points for , that is

The stochastic integral can be estimated by binning the interval and assuming the Brownian motion is constant over the bin and hence, can be estimated by a standard Gaussian. For more information on this integration method, we refer to Chapter 4 of Shreve [36].

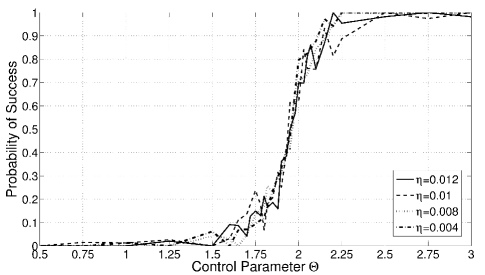

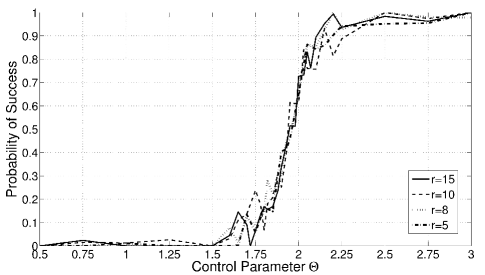

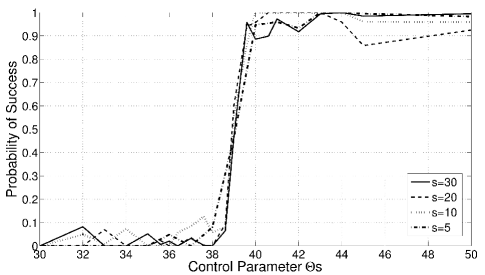

Using this data, we solve (4) using accelerated proximal gradient method [29]. Motivated by our Theorem, we plot our result with respect to the control parameter . We pick the values of and by dividing the training data into chunks each having consecutive samples and do the cross validation over those chunks. Note that this is different from the standard cross validation technique due to the dependency of samples.

Figure 1(c) shows the phase transition of the probability of success in recovering the exact sign support of the matrix . We ran three different experiments, each investigating the effect of one of the three key parameters of the system (sampling frequency), (number of latent variables) and (sparsity of the model). These three figures show that the probability of success curves line up if they are plotted versus the correct control parameter. The first two curves for and line up versus , indicating that our theorem suggests the correct scaling law for the sample complexity. However, from this experiment, it seems that the phase transition probability scales with not . Perhaps the result of our theorem and also Bento et al. [3] (for ) can be tightened.

6.2 Stock Market Data

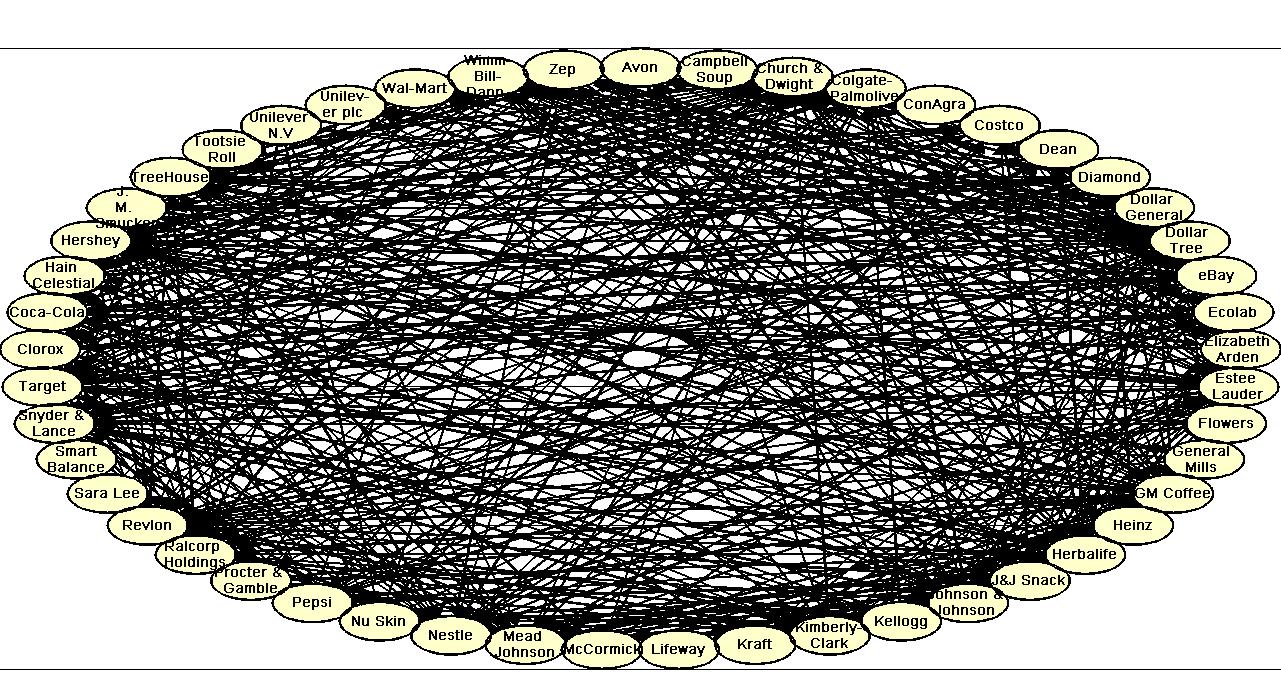

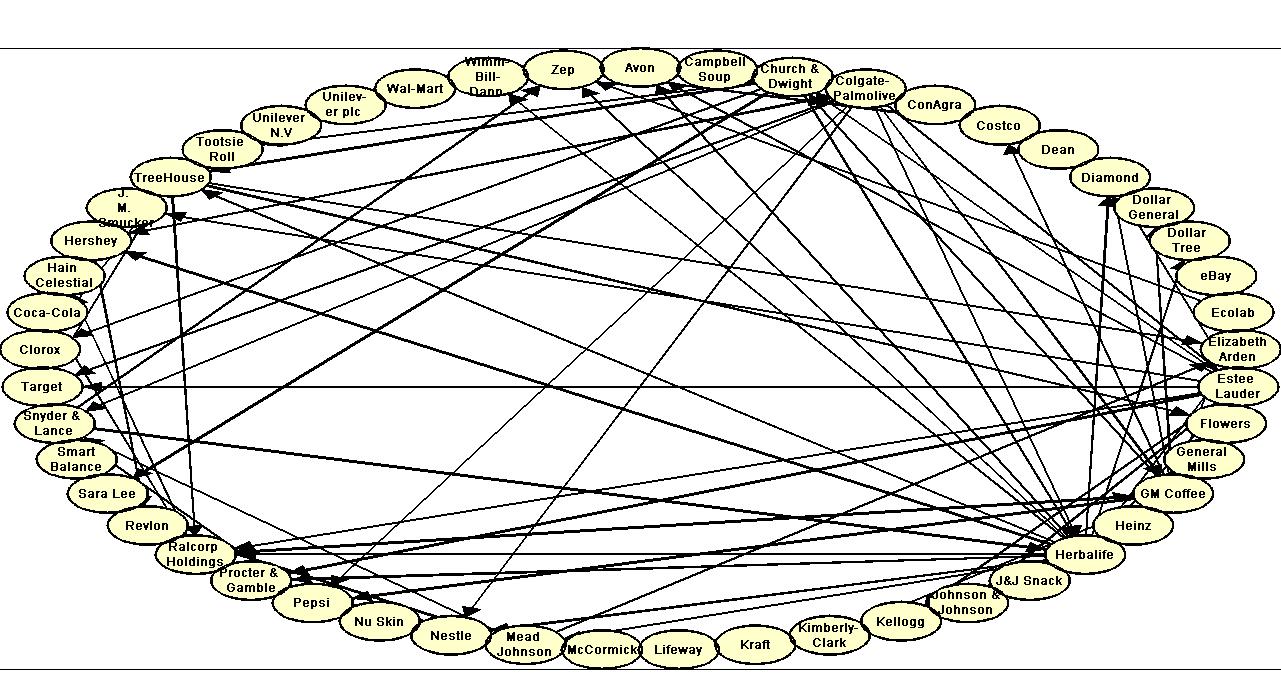

We take the end-of-the-day closing stock prices for 50 different companies in the period of May 17, 2010 - May 13, 2011 ( business days). These companies (among them, Amazon, eBay, Pepsi, etc) are consumer goods companies traded either at NASDAQ or NYSE in USD. The data is collected from Google Finance website. Our goal is to observe the stock prices for a period of time and predict it for the entire days of the next month with small error.

Applying our method and pure LASSO [3] to the data, we recover the structure of the dependencies among stocks. We represent the result as a graph in Fig 2(b); where each company is a node in this graph and there is an edge between company and if . This result shows that the recovered dependency structure by our algorithm is order of magnitude sparser than the one recovered by pure LASSO.

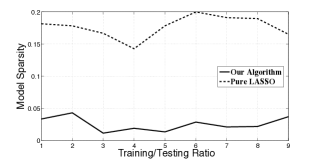

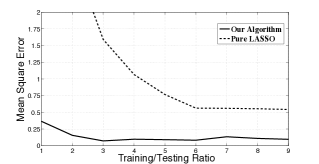

To show the usefulness of our algorithm for prediction purposes, we apply our algorithm to this data and try to learn the model using the data for (consecutive) days and then compute the mean squared error in the prediction of the following month ( business days). We randomly pick an starting day between day and day . Then we learn the model using the data from the day to the day (total of days). Then, we test our data on the consecutive days. Finally, we average the error over different starting points for each value of . We pick the regularizers by the semi-cross validation process explained in the previous section. The ratio shows the ratio of training sample size to the testing sample size.

Figure 3(b) shows the prediction error for both our method and pure LASSO [3] method as the train/test ratio increases. It can be seen that our method not only have better prediction, but also is more robust. Our algorithm requires only 3 months of the past data to give a robust estimation of the next month; in contrast with almost 6 months requirement of LASSO. However, the error of our algorithm is much smaller (by a factor of 6) than LASSO even in the steady state. Figure 3(a) shows the sparsity level for our model and the LASSO model. The number of latent variables our model finds varies from for different train/test ratios. As Figure 3(a) illustrates, our estimated is order of magnitude sparser than the one estimated by LASSO.

Appendix A Proof of Lemma 1

Ignoring the term which is independent of , minimization of with this infinite sample size is equivalent to

Here we ignored the term due to the fact that it is zero mean and independent of and . This implies that the asympotatic optimizer of satisfies . This concludes the proof of the lemma.

Appendix B Illustrative Example

In this section, we analyze the illustrative example discussed in Sec 4. For that example, Lyapunov stability equation requires

This entails that and with . It can be easily checked that . Thus, the low-rank matrix of interest is

Taking singular value decomposition of this matrix, we get and hence . Considering , the identifiability assumption (A2) becomes or equivalently, .

Considering assumption (A3), note that is just an scalar since . Moreover, is a vector with all entries equal to and hence .

Appendix C Proof of Lemma 2

Suppose and . From condition (C5), is the subgradient of the loss function at and hence,

| (6) |

Let with . Notice that and . For is in the subgradient of , we have

| (7) |

Suppose and are SVD decompositions. Now, let with and . In this construction, we have

-

(a)

and and .

-

(b)

and by Lemma 6.

Let and notice that . Here, we have and by Lemma 6. Hence, our constructed is in the subgradient of , i.e.,

| (8) |

Provided , we arrive to a contradiction with the optimality of and the result follows.

Notice that by first order optimality condition, we have . Hence, for some , we have

| (9) | ||||

Similarly, by first order optimality condition, and by our construction, . Hence, we get

| (10) | ||||

This concludes the proof of the lemma.

Lemma 6.

For and constructed above, we have and .

Proof.

First, notice that for all , and hence,

Using this, we can bound both and . For , we have

Since , we can establish

This concludes the proof of the lemma.

∎

Appendix D Proof of Lemma 3

General Notation: For a matrix , we use to denote rows, to denote columns and to denote entries. Also, for the sets of indecies and , the matrix represents the sub-matrix of consisting of the rows and columns corresponding to index sets and .

We prove part (b) of the lemma. By triangle inequality, we have

Hence,

| (11) |

Let and . Substituting and in (C5), we get

| (12) |

We can rewrite this equation as

| (13) |

Let us only focus on the row of the system of equations (12). We can break down (12) on the row into two sets of linear equations as follows:

| (14) | ||||

From the first line, we get

By Lemma 8, we have

Thus, by Lemma 9 and (C1), we get

| (15) | ||||

The last inequality follows from the definition of . This concludes the proof of the lemma.

Lemma 7 (Convex Optimality).

If is a solution of (4) then there exists a matrix , called dual variable, such that and and

| (16) |

Proof.

The proof follows from the standard first order optimality argument.

∎

Appendix E Proof of Lemma 4

The result follows from our construction of , and in the proof of Lemma 2. With our dual construction, we have and hence, and by construction, which entails . This concludes the proof of the lemma.

Appendix F Proof of Lemma 5

Substituting from the first equation in the second in (14), we get

By triangle inequality, we get

Hence, condition (C2) is satisfied.

To show (C4) also holds, notice that from (13), we have

The last inequality follows from Lemmas 10 and 11 and the fact that on the support is invertible for the given sample complexity due to Lemma 9.

Next, notice that and hence the row-space of is the column/row space of and consequently, for any matrix , we have . Thus, by triangle inequality, we have

Hence, condition (C4) is also satisfied. This concludes the proof of the lemma.

Appendix G Concentration Results

In this section we prove the concentration results used throughout the paper. Before, we state the results, we want to introduce some useful notations and inequalities used to get the results. By the dynamics of the system, we have

Lemma 8.

Under assumptions (A3) and (A5), for any with , with high probability we have

Proof.

The result follows from Lemma 12. This concludes the proof of the lemma.

∎

Lemma 9.

Under assumption (A5), for any with , with high probability, we have

Proof.

Lemma 10.

Under assumptions (A4) and (A5), with high probability, we have

Proof.

Let . According to the dynamics of the system, we have

We bound these two terms separately. Notice that is distributed independent of and ’s. Given , we have

By stability assumption, we have and hence,

Consequently, by standard concentration of Gaussian random variables and union bound, we get

With similar analysis, we get

The last inequality follows from the concentration of random variables [27], in particular,

Finally, we get

The result follows for . This concludes the proof of the lemma.

∎

Lemma 11.

Under assumptions (A4) and (A5), with high probability, we have

Proof.

We can establish

We bound these two terms separately. For the first term, we have

For the second term, we have

The result follows from Lemma 13. This concludes the proof of the lemma.

∎

Lemma 12.

Under assumption (A5), with high probability, we have

Proof.

Let . Let (clearly, ). We have

We bound these three terms, separately. For the first term, we have

For the second term, notice that by independency assumption on , we have

On the other hand, we have

In the above inequalities, we interchanged limit and expectation as a result of Gaussianity assumption and the stability of the system. Finally we get

To bound the third term, notice that

By Lemma 1 in [34], we have

Consequently, we get

Thus, we conclude

We want this probability to be less than . Putting all thre parts together, we get

| (17) |

For and , the result follows, provide that the probabilities go to zero, i.e.,

For large enough values of , this lower bound dominates the earlier lower bound of , hence, we ignore that one. This concludes the proof of the lemma.

∎

Lemma 13.

Under assumptions (A4) and (A5), with high probability, we have

Proof.

According to (17), the result follows if assuming is large enough.

∎

Lemma 14.

For sample complexity

with high probability, we have

Proof.

Since and are positive semi-definite matrices and

The result directly follows from Theorem in [38] for considering the fact that .

∎

References

- Azoff [1994] E.M. Azoff. Neural Network Time Series Forecasting of Financial Markets. John Wiley & Sons, Inc., 1994.

- Bar-Joseph [2004] Z. Bar-Joseph. Analyzing time series gene expression data. Bioinformatics, Oxford University Press, 20:2493–2503, 2004.

- Bento et al. [2010] J. Bento, M. Ibrahimi, and A. Montanari. Learning networks of stochastic equations. In NIPS, 2010.

- Bowerman and O’Connell [1993] B.L. Bowerman and R.T. O’Connell. Forecasting and time series: An applied approach. Duxbury Press, 1993.

- Box et al. [1990] G.E.P. Box, G.M. Jenkins, and G.C. Reinsel. Time-series Analysis: Forecasting and Control. John Wiley & Sons, Inc., 1990.

- Candes and Plan [2010] E. J. Candes and Y. Plan. Matrix completion with noise. In IEEE Proceedings, volume 98, pages 925 – 936, 2010.

- Candes et al. [2009] E. J. Candes, X. Li, Y. Ma, and J. Wright. Robust principal component analysis? In Available at arXiv:0912.3599, 2009.

- Chandrasekaran et al. [2010] V. Chandrasekaran, P. A. Parrilo, and A. S. Willsky. Latent variable graphical model selection via convex optimization. In Available at arXiv:1008.1290, 2010.

- Chandrasekaran et al. [2011] V. Chandrasekaran, S. Sanghavi, P. A. Parrilo, and A. S. Willsky. Rank-sparsity incoherence for matrix decomposition. SIAM Journal on Optimization, 2011.

- Chatfield [2000] C. Chatfield. Time-series Forecasting. Chapman & Hall, 2000.

- Chen et al. [2011] Y. Chen, A. Jalali, S. Sanghavi, and C. Caramanis. Low-rank matrix recovery from errors and erasures. In ISIT, 2011.

- Cochrane [2005] J. H. Cochrane. Time Series for Macroeconomics and Finance. University of Chicago, 2005.

- d’Aspremont et al. [2007] A. d’Aspremont, O. Bannerjee, and L. El Ghaoui. First order methods for sparse covariance selection. SIAM Journal on Matrix Analysis and its Applications, 2007. To appear.

- Dempster et al. [1977] A.P. Dempster, N.M. Laird, and D.B. Rubin. Maximum-likelihood from incomplete datavia the em algorithm. Journal of Royal Statistics Society, Series B., 39, 1977.

- Fazel et al. [2011] M. Fazel, T.K. Pong, D. Sun, and P. Tseng. Hankel matrix rank minimization with applications in system identification and realization. In Available at http://faculty.washington.edu/mfazel/Hankelrm9.pdf, 2011.

- Fisher [1925] R. A. Fisher. Theory of statistical estimation. In Proceedings of Cambridge Philosophy Society, volume 22, pages 700–725, 1925.

- Friedman et al. [2007] J. Friedman, T. Hastie, and R. Tibshirani. Sparse inverse covariance estimation with the graphical lasso. BioStatistics, 9:432–441, 2007.

- Geršgorin [1931] S. Geršgorin. Uber die abgrenzung der eigenwerte einer matrix. Bulletin de l’Académie des Sciences de l’URSS. Classe des sciences mathématiques et na, 7:749–754, 1931.

- Gillespie [2007] D.T. Gillespie. Stochastic simulation of chemical kinetics. Annual Review of Physical Chemistry, 58:35–55, 2007.

- Hazan et al. [2005] T. Hazan, S. Polak, and A. Shashua. Sparse image coding using a 3d non-negative tensor factorization. In ICCV, 2005.

- Higham [2008] D. Higham. Modeling and simulating chemical reactions. SIAM Review, 50:347–368, 2008.

- Horn and Johnson [1985] R. A. Horn and C. R. Johnson. Matrix Analysis. Cambridge University Press, Cambridge, 1985.

- Jalali and Srebro [2012] A. Jalali and N. Srebro. Clustering using max-norm constrained optimization. In Available at arXiv:1202.5598, 2012.

- Jalali et al. [2011] A. Jalali, Y. Chen, S. Sanghavi, and H. Xu. Clustering partially observed graphs via convex optimization. In ICML, 2011.

- Jordan [1998] M. I. Jordan. Learning in Graphical Models. Kluwer Academic Publishers, Netherland, 1998.

- Kim [2003] K. Kim. Financial time series forecasting using support vector machines. Elsevier Neurocomputing, 55:307–319, 2003.

- Laurent and Massart [1998] B. Laurent and P. Massart. Adaptive estimation of a quadratic functional by model selection. Annals of Statistics, 28:1303–1338, 1998.

- Lawrence et al. [2010] N. D. Lawrence, M. Girolami, M. Rattray, and G. Sanguinetti. Learning and Inference in Computational Systems Biology. MIT Press, 2010.

- Lin et al. [2009] Z. Lin, A. Ganesh, J. Wright, L. Wu, M. Chen, and Y. Ma. Fast convex optimization algorithms for exact recovery of a corrupted low-rank matrix. In UIUC Technical Report UILU-ENG-09-2214, 2009.

- Ljung [1999] L. Ljung. System identification: Theory for the user. Prentice Hall, 1999.

- Loehlin [1984] J.C. Loehlin. Latent Variable Models: An introduction tofactor, path, and structural analysis. L. Erlbaum Associates Inc. Hillsdale, NJ, USA, 1984.

- Marchal [2003] P. Marchal. Constructing a sequence of random walks strongly converging to brownian motion. In Discrete Mathematics and Theoretical Computer Science Proceedings, pages 181–190, 2003.

- Meinshausen and Buhlmann [2006] N. Meinshausen and P. Buhlmann. High-dimensional graphs and variable selection with the lasso. Annals of Statistics, 34(3):1436–1462, 2006.

- Ravikumar et al. [2008] P. Ravikumar, M. J. Wainwright, G. Raskutti, and B. Yu. High-dimensional covariance estimation by minimizing -penalized log-determinant divergence. Technical Report 767, UC Berkeley, Department of Statistics, 2008.

- Redner and Walker [1984] R. Redner and H. Walker. Mixture densities, maximum likelihood and the em algorithm. SIAM Review, 26, 1984.

- Shreve [2004] S. E. Shreve. Stochastic Calculus for Finance II: Continuous-Time Models. Springer, 2004.

- Srebro and Jaakkola [2003] N. Srebro and T. Jaakkola. Weighted low rank approximation. In ICML, 2003.

- Stewart [1995] G. W. Stewart. On the perturbation of schur complements in positive semidefinite matrices. Technical Report, University of Maryland, College Park, 1995.

- Tibshirani [1996] R. Tibshirani. Regression shrinkage and selection via the lasso. Journal of Royal Statistical Society, Series B, 58:267–288, 1996.

- Vapnik [1998] V. N. Vapnik. Statistical Learning Theory. John Wiley and Sons, Inc., New York, 1998.

- Wainwright [2009] M. J. Wainwright. Sharp thresholds for noisy and high-dimensional recovery of sparsity using -constrained quadratic programming (lasso). IEEE Trans. on Information Theory, 55:2183–2202, 2009.

- Wei [1994] W.W.S. Wei. Time Series Analysis: Univariate and Multivariate Methods. Addison Wesley, 1994.

- West [2003] Mike West. Bayesian factor regression models in the ”large p, small n” paradigm. In Bayesian Statistics, pages 723–732. Oxford University Press, 2003.

- Young [1984] P. Young. Recursive estimation and time-series analysis. Springer - Verlag, 1984.

- Yuan and Lin [2007] M. Yuan and Y. Lin. Model selection and estimation in the Gaussian graphical model. Biometrika, 94(1):19–35, 2007.

- Zhou et al. [2010] Z. Zhou, X. Li, J. Wright, E. Candes, and Y. Ma. Stable principal component pursuit. In ISIT, 2010.