This study presents a method to predict the growth fluctuation of firms interdependent in a network economy. The risk of downward growth fluctuation of firms is calculated from the statistics on Japanese industry.

1 Introduction

Does an abrupt ill health of one firm have a big impact on the health of others?

Many firms ended in disastrous failure during the worldwide financial crisis in 2008. Since then, risk managers, executives, and investors have been strongly interested in the transmission of distress and the knock-on defaults between firms which are interdependent in a network economy [May 2010]. In this study, a model for such firms is formulated with stochastic differential equations. Probability parameters on trades between firms can be inferred statistically, and the time evolution of the net-worth of the firms can be predicted. The conditional value at risk of the downward growth fluctuation of firms is calculated from the statistics on Japanese industry in 2005.

2 Stochastic model

A stochastic model for firms is presented. Time dependent variables for is the net-worth of the -th firm at time . The interplay between the firms governs the time evolution of . The income by the sales to others lets increase. Its rate of change is given by where the probability parameters are constant. The expenditure on the purchases from others and labor wages lets decrease. The rate is where is constant. This is a special case (linear production function) of the model for the financial accelerator in credit networks [Delli Gatti 2010]. It is also similar to the model for evolutionary autocatalytic sets [Mehrotra 2009].

The stochasticity of the time evolution ensues from an unpredictably irregular pattern of trades between firms. The number of trades obeys a Poisson distribution if the probability of a trade per unit time is constant. The amplitude of fluctuation is nealy the square root of the average. The time evolution of is given by a system of stochastic differential equations in eq.(1). The functional form of the Gaussian white noises and is not known.

(1)

Eq.(1) is equivalent to the Fokker-Planck equation in eq.(2). It is a partial differential equation, which describes the time evolution of the joint probability density function of probability variables at .

(2)

The drift and diffusion coefficients in eq.(2) are given by eq.(3) and (4).

(3)

(4)

Predicting , given and , is a forward problem. Inferring the value of and from the observation on statistically is an inverse problem [Maeno 2010]. These problems are mixed under practical conditions. The values of some parameters are known, and some data on are given. Eq.(2) is converted to a system of ordinary differential equations in eq.(5) and (6), which describe the time evolution of the 1st and 2nd order moments and .

(5)

(6)

Generally, the time evolution of the -th order moments is given by a system of linear differential equations in eq.(7). The elements of the vector are . The matrix , and matrix are calculated from and .

(7)

The solution of eq.(7) with the initial conditions is given by eq.(8).

(8)

Approximately, is a multi-variate normal distribution with the mean and covariance . The exact formula for is obtained by the Edgeworth series. It is an asymptotic expansion of in terms of cumulants. The logarithmic likelihood function is obtained immediately, once eq.(2) is solved, given a dataset at for the observations . It is given by eq.(9). The estimators and are those which maximize .

(9)

3 Growth fluctuation

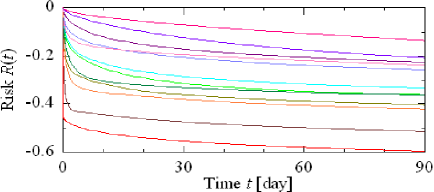

Figure 1: Risk of the representative firms as a function of . The -th sector is Transportation equipment. The -th sector is one of 12 selected sectors.

The risk of firms are defined, and calculated with the Leontief coefficients in the input-output model for Japanese industry sectors in 2005111Ministry of Internal Affairs and Communications, 2005 Input-Output Tables for Japan. http://www.stat.go.jp/english/data/io/io05.htm.. The quantile value at risk of the -th firm at is defined by eq.(10) [Martinez-Jaramillo 2010]. It is the net-worth at which the cumulative density is . is the marginal probability density function of .

(10)

The conditional value at risk which the ill health of the -th firm imposes on the -th firm at is defined by eq.(11). is the probability density function of conditioned on the value of . Note .

(11)

The quantity is the risk of downward fluctuation from the expected growth at . If is a multi-variate normal distribution, is given by eq.(12) where . For example, for 5 percentile and for 1 percentile.

(12)

The Leontief coefficients determine . The past growth rates of the sectors are used to obtain . Suppose a representative firm in each industry sector whose share of production is . Figure 1 shows of the firms in 12 selected sectors () as a function of . The -th sector is Transportation equipment. The risk increases as time goes by. The representative firm in Mining have the largest risk, at a quarter later ( days), when the representative firm in Transportation equipment falls ill. It is followed by the firms in Office supplies, Textile products, Non-ferrous metals, Electronic parts, Finance and insurance, Precision instruments, Iron and steel, Chemical products, Commerce, and Public administration. The firm in Medical service, health, social security and nursing care has the smallest risk.

References

[Delli Gatti 2010] D. Delli Gatti, M. Gallegati, B. Greenwald, A. Russo, and J. E. Stiglitz, The financial accelerator in an evolving credit network, J. Econ. Dyn. Control 34, 1627-1650 (2010).

[Maeno 2010] Y. Maeno, Discovering network behind infectious disease outbreak, Physica A 389, 4755-4768 (2010).

[Martinez-Jaramillo 2010] S. Martínez-Jaramillo, O. P. Pérez, F. A. Embriz, and F. L. G. Dey, Systemic risk, financial contagion and financial fragility, J. Econ. Dyn. Control 34, 2358-2374 (2010).

[May 2010] R. M. May, and N. Arinaminpathy, Systemic risk: The dynamics of model banking systems, J. R. Soc. Interface 7, 823-838 (2010).

[Mehrotra 2009] R. Mehrotra, V. Soni, and S. Jain, Diversity sustains an evolving network, J. R. Soc. Interface 6, 793-799 (2009).