CRRA Utility Maximization under Risk Constraints111

Santiago Moreno–Bromberg gratefully acknowledges financial support from the Deutsche

Forschungsgemeinschaft through the SFB 649 “Economic Risk” and from the Alexander von Humboldt Foundation via a research fellowship.

Traian A. Pirvu is grateful to NSERC through grant 5-36700 and MITACS through grant 5-26761.

Anthony Réveillac is grateful to the Deutsche

Forschungsgemeinschaft Research center MATHEON for financial support. The authors are very grateful to Jianing Zhang for his guidance concerning the numerical simulations.

| Santiago Moreno–Bromberg | Traian A. Pirvu | |

| Insitut für Banking und Finance | Mathematics and Statistics Department | |

| Universität Zürich | McMaster University | |

| Plattenstr. 32, 8032 Zürich | Hamilton, ON | |

| Switzerland | Canada | |

| santiago.moreno@bf.uzh.ch | tpirvu@math.mcmaster.ca |

Anthony Réveillac

Université Paris Dauphine

CEREMADE UMR CNRS 7534

Place du Maréchal De Lattre De Tassigny

75775 Paris Cedex 16

France

anthony.reveillac@ceremade.dauphine.fr

Abstract

This paper studies the problem of optimal investment with CRRA (constant, relative risk aversion) preferences, subject to dynamic risk constraints on trading strategies. The market model considered is continuous in time and incomplete. the prices of financial assets are modeled by Itô processes. The dynamic risk constraints, which are time and state dependent, are generated by risk measures. Optimal trading strategies are characterized by a quadratic BSDE. Within the class of time consistent distortion risk measures, a three–fund separation result is established. Numerical results emphasize the effects of imposing risk constraints on trading.

Preliminary - Comments Welcome

JEL classification: G10

Mathematics Subject Classification (2000): 91B30, 60H30, 60G44

Keywords: BSDE, CRRA preferences, constrained utility maximization, correspondences, risk measures.

1. Introduction

In this paper we consider the problem of a utility–maximizing agent, whose preferences are of of constant relative risk aversion (CRRA) type, and whose trading strategies are subject to risk constraints. We work on a continuous–time, stochastic model with randomness being driven by Brownian noise. The market is incomplete and consists of several traded assets whose prices follow Itô processes.

In practice, managers set risk limits on the strategies executed by their traders. In fact, the mechanisms used to control risk are more complex: financial institution have specialized internal departments in charge of risk assessments. On top of that there are external regulatory institutions to whom financial institutions must periodically report their risk exposure. It is natural, therefore, to study the portfolio problem with risk constraints, which has received a great deal of scrutiny lately. A very well known paper in this direction is [CK92]. The authors employ convex duality to characterize the optimal constrained portfolio. A more recent paper in the same direction is [HIM05]. Here the optimal constrained portfolio is characterized by a quadratic BSDE, which renders the method more amenable to numerical treatment. In these two (by now classical) papers the risk constraints are imposed via abstract convex (closed) sets. Lately, a line of research has been developed where the risk–constraint sets are specified employing a specific risk measure, e.g. VaR (Value at Risk). In the following we provide a brief overview of the related literature.

Existing Research: A risk measure that is commonly used by both practitioners and academics is VaR. Despite its success, VaR has as drawbacks not being subadditive and not recognizing the accumulation of risk. This encouraged researchers to develop other risk measures, e.g. TVaR (Tail Value at Risk). The works on optimal investment with risk constraints generated by VaR, TVaR (or other risk measures) split into two categories, which depend on whether or not the risk assessment is performed in a static or a dynamic fashion. Let us briefly touch on the first category. The seminal paper is [BS01], where the optimal dynamic portfolio and wealth-consumption policies of utility maximizing investors who use VaR to control their risk exposure is analyzed. In a complete–market, Itô-processes framework, VaR is computed in a static manner (the authors compute the VaR of the final wealth only). An interesting finding is that VaR limits, when applied only at maturity, may actually increase risk. One way to overcome this problem is to consider a risk measure that is based on the risk–neutral expectation of loss - the Limited Expected Loss (LEL). In [ESR01] a model with Capital–at–Risk (a version of VaR) limits, in the Black–Scholes–Samuelson framework is presented. The authors assume that portfolio proportions are held constant during the whole investment period, which makes the problem static. [DVLLLW10] extends [ESR01] from constant to deterministic parameters. In a market model with constant parameters, [GSW09] extends [BS01] to cover the case of bounded expected loss. In a general, continuous–time Financial market model, [GW06] considers the portfolio problem under a downside risk constraint measured by an abstract convex risk measure. [KP09] extends [ESR01] by imposing a uniform (in time) risk constraint.

In the category of dynamic risk measurements we recall the seminal paper [CHI08]. Following the financial industry practice, the VaR (or some other risk measure) is computed (and dynamically re–evaluated) using a time window (2 weeks in practice) over which the trading strategies are assumed to be held constant for the purpose of risk measurement. The finding of the authors is that dynamic VaR and TVaR constraints reduce the investment (proportion wise) in the risky asset. [LVT06] studies the impact of VaR constraint on equilibrium prices and the relationship with the leverage effect. [BCK05] shows that, in equilibrium, VaR reduces market volatility. [PR10] finds that risk constraints may give rise to equilibrium asset pricing bubbles. Among others, [AP05], [P07], and [Y04] analyze the problem of investment and consumption subject to dynamic VaR constraints. [PZ09] considers maximizing the growth rate of the portfolio in the context of dynamic VaR, TVaR and LEL constraints. In a complete market model, [PS10] uses a martingale method to study the optimal investment under dynamic risk constraints and partial information.

Our Contribution: This paper extends the risk measurements introduced by [CHI08] by considering a relatively general class of risk measures (we only require them to be Carathéodory maps, and this class is rich enough to include many convex and coherent risk measures). The corresponding risk–constraint sets arising from such risk measures, and applied to the trading strategies, are time and state dependent. Moreover, they satisfy some important measurability properties.

We employ the method developed in [HIM05] in order to find the optimal trading strategies subject to the risk constraints. The main difference is that, unlike [HIM05], our constraint sets are time dependent, which renders the methodology developed in [HIM05] not directly applicable within our context. The difficulty stems from establishing the measurability of the BSDE’s driver (the BSDE which characterizes the optimal trading strategy). This is done by means of the Measurable Maximum Theorem and the Kuratowski–Ryll–Nardzewski Selection Theorem. After this step is achieved we apply results from [MO09] to get existence of solutions to the BSDE, which in turn yields the optimal trading strategy.

We then restrict our risk measures to the class of time consistent distortion risk measures. By doing so we observe that the risk constraints have a particular structure: they are compact sets (for a fixed time and state) and depend on two statistics (portfolio return and variance). This leads to a three–fund separation result. More precisely, an investor subject to regulatory constraints will invest her wealth into three–funds: a savings account and two index funds. One index fund is a mix of the stocks with weights given by the Merton proportion. This index fund is related to market risk and most of the portfolio separation results refer to it. The second index is related to volatility risk. In a market with non–random drift and volatility the second index is absent. Thus, the second index can be explained by the demand of hedging volatility risk.

Numerical results shed light into the structure of the optimal trading strategy. More precisely, using recent results concerning numerical methods for quadratic growth BSDEs, we present in Section 5 some numerical examples for value–at–risk, tail–value–at–risk and limited expected loss. Our simulations clearly exhibit the effect of the risk constraint on the optimal strategy and on the associated value function. More precisely from the plots we see that risk constraints reduce the gambling of the risky assets.

The paper is organized as follows: In Section 2 we introduce the basic model, the risk measures and the corresponding risk constraints. Section 3 presents measurability properties of the candidate optimal trading strategy and its characterization via a quadratic BSDE. In Section 4, time consistent distortion risk measures are considered. A three–fund separation result is obtained within this context. Numerical results are presented in Section 5. The paper ends with an appendix that contains some technical results.

2. Model Description and Problem Formulation

2.1. The Financial Market

Our model of a financial market, based on a filtered probability space that satisfies the usual conditions, consists of assets. The first one, , is a riskless bond with a strictly positive, constant interest rate . The remaining assets are stocks, and their prices are modeled by an –dimensional Itô–process . Their dynamics are given by the following stochastic differential equations, in which is a –dimensional standard Brownian motion:

where the –valued process is the mean rate of return, and is the variance–covariance process. In order for the equations (2.1) to admit unique strong solutions, we impose the following regularity conditions on the coefficient processes and :

Assumption 2.1.

All the components of the processes and are predictable, and

To ease the exposition, we introduce the following notation: for an integrable -valued process , and a sufficiently regular –valued process we write

Further, we impose the following condition on the variance–covariance process

Assumption 2.2.

The matrix has independent rows for all almost–surely.

This assumption makes it impossible for different stocks to have the same diffusion structure. Otherwise, the market would either allow for arbitrage opportunities or redundant assets would exist. As a consequence of Assumption 2.2 we have that - the number of risky assets does not exceed the number of “sources of uncertainty”. Also, the inverse is easily seen to exist. The equation

uniquely defines a predictable stochastic process , named the Merton–proportion process, where , with for . At this point we make another assumption on the market coefficients:

Assumption 2.3.

We assume that

and the stochastic process is uniformly bounded. In addition, we assume that there exists a constant such that

2.2. Trading strategies and wealth

Let denote the predictable –algebra on The control variables are the proportions of current wealth the investor invests in the assets. More precisely, we have the following formal definition:

Definition 2.4.

An –valued stochastic process is called an admissible portfolio–proportion process if it is predictable (i.e. -measurable) and it satisfies

Here denotes the transpose of is a –dimensional column vector all of whose coordinates are equal to , and is the standard Euclidean norm. The set of admissible strategies will be denoted by .

Given a portfolio–proportion process , we interpret its coordinates as the proportions of the current wealth invested in each of the stocks. In order for the portfolio to be self–financing, the remaining wealth is assumed to be invested in the riskless bond . If this quantity is negative, we are effectively borrowing at the rate . No short–selling restrictions are imposed, hence the proportions are allowed to be negative, and they are not a priori bounded. The equation governing the evolution of the total wealth of the investor using the portfolio–proportion process is given by

We recall that , with for , is the vector of excess rates of return. Under the regularity conditions (2.4) imposed on Equation (2.2) admits a unique strong solution given by

The initial wealth is considered to be exogenously given. As a consequence of Assumption 2.3, and using Expression (2.4), a strategy is admissible if and only if it is a predictable process such that

| (2.1) |

Indeed we have

by the Cauchy–Buniakowski–Schwarz inequality. Thus, inequality (2.1) follows from Assumption 2.3, Expression (2.4) and the Cauchy–Buniakowski–Schwarz inequality.

The expression appearing inside the first integral in (2.2) above will be given its own notation; the quadratic function is defined as

It is also useful to define the random field

It is clear from Expression (2.2) that the evolution of wealth process depends on the -dimensional process only through two “sufficient statistics”, namely

These will be referred to in the sequel as portfolio rate of return and portfolio volatility, respectively.

2.3. Projected distribution of wealth

For the purposes of risk measurement, it is common practice to use an approximation of the distribution of the investor’s wealth at a future date. Given the current time , and a length of the measurement horizon the projected distribution of the wealth from trading are calculated under the simplifying assumptions that

-

(1)

the proportions of the wealth invested in various securities, as well as

-

(2)

the market coefficients and

stay constant and equal to their present values throughout the time interval . The wealth Equations (2.2) and (2.2) yield that the projected wealth loss is - conditionally on - distributed as , where the law of is the one of

Here is a normal random variable with mean and standard deviation . The quantities and are the portfolio rate of return and volatility, defined in Equation (2.2). In the upcoming sections we turn our focus to risk measurements associated to the relative projected wealth gain, which will be defined as the distribution of the quantity

This is not a technical requirement, and the method developed in Sections 2.4 to 3 still holds for risk measurements in absolute terms. The economic implications, however, may be stark, and the definition of the risk constraints below would require a certain recursive structure. The latter in the sense that admissibility (risk–wise) at time will depend on the choice of the strategy at all previous times. We elaborate further on this in Remark 2.6. The measurement horizon and the market coefficients will play the role of “global variables”.

2.4. The risk constraints

In this section we introduce the risk constraints that will be imposed on the trading strategies. We keep the presentation as general as possible and make only sufficient assumptions on the risk measures. These allow us to show existence (and in some cases uniqueness) of optimal, constrained trading strategies. We begin by making precise how the risk of a given strategy is measured.

Let us define the gain over time interval by and let be a family of maps with

where

Notice that for all we have that We also define For a given admissible and we define the strategy as for and for By definition of the wealth process we obtain that moreover (under the assumptions made in Section 2.3) the quantity depends exclusively on and not on In order to establish the risk constraints, we define the acceptance sets

where is a real–valued, exogenous, predictable process that satisfies for all in , –almost surely. Notice that is in the constraint set. We observe that by construction, the sets are independent of and we shall simply write In analogous fashion we will slightly abuse notation and write for It follows from Equation (2.2) that in fact

where

Hence, the expressions for the sets of constraints may be rewritten as

Moreover, under the assumption that and remain (for the purpose of risk assessment) constant over we may write

and we shall denote by and the second and third factors of respectively.

We make the following assumption on the family

Assumption 2.5.

The family of maps

satisfies that the mapping

is a Carathéodory function; that is, for every in , the map is continuous and for every in the map is –measurable.

An example of a family that satisfies Assumption 2.5 is the following: Let be a convex, non–decreasing continuous and non–constant function222Such functions are usually referred to as “loss functionals”. with . Assume that the filtration is generated by the Brownian motion and that and where and are deterministic Borelian functions. We set

so that , –almost surely. Then the family satisfies Assumption 2.5. Indeed, fix in and let in . Then, by monotonicity of the exponential and we have that:

Hence, Lebesgue’s Dominated Convergence Theorem implies that:

Finally, since the filtration we consider is the Brownian filtration, the stochastic process is predictable.

Remark 2.6.

If we were to consider risk constraints based not on the relative projected wealth loss, but only on the quantities then the acceptance sets defined in Expression 2.4 would depend on More precisely, the set of risk–admissible strategies would be

In the case where is a –coherent family, i.e. if for all then risk constraints in absolute terms are generated by inequalities of the form

This follows from the fact that the wealth level at time is a –measurable random variable. The structure then reverts to that of risk constraints in relative terms, except for a redefinition of the risk bound as Notice that if then would be a decreasing function of wealth. In other words, highly capitalized investors would face more stringent constraints. This could lend an approach to dealing with the too–big–to–fail problem, and could be further tweaked by allowing to depend on the state of nature. It is, however, beyond the scope of this paper to discuss such policy–making issues, and we shall stick to the relative–measures–of–risk framework.

Remark 2.7.

Note that is not stricto sensu a dynamic risk measure, since every is a priori not defined on the whole space . As we we have seen in the previous lines, defining the risk of every random variable in is not relevant for us, since we only need to evaluate the risk of the very specific random variables .

2.5. The optimization problem

We finish the section by formulating our central problem. Given a choice of a dynamic risk measure satisfying Assumption 2.5 and a final date we are searching for a portfolio–proportion process which maximizes the CRRA utility of the final wealth among all the portfolios satisfying the same constraint. In other words, for all and

| (2.2) |

This problem has the following economic motivation: Risk managers limit the risk exposure of their traders by imposing risk constraints on their strategies. This can be regarded as an external risk management mechanism. In our model this is represented by the risk measures. On the other hand, traders have their own attitudes towards risk, which are reflected by the risk aversion of the CRRA utility. However, is known to reflect a risk seeking attitude of the trader. The risk manager cannot constraint the trader’s risk preferences. In order to deal with this, risk constraints on the trader’s strategies must be imposed.

3. Analysis

In this section we prove the existence of an optimal investment strategy. For simplicity we consider the case (analogous arguments apply with minor modifications to ). In order to do so, we make use of the powerful theory of backward stochastic differential equations (BSDEs). Let

where is the set of admissible strategies in the sense of Definition 2.4. We recall that we consider the maximization problem

By means of Equation (2.2) we may write

In analogous fashion as done in [HIM05], let us introduce the auxiliary process

where is a solution to the BSDE

| (3.1) |

The function should be chosen in such a way that

-

a)

the process is a supermartingale, and for every ,

-

b)

there exists at least one element in such that is a martingale.

We shall verify ex–post that the function in question satisfies the measurability and growth conditions required to guarantee existence of solutions to Equation (3.1). Before going further we explain why achieving this would provide a solution to Problem (2.2). If we were able to construct such a family of processes then we would obtain that is an optimal strategy for Problem (2.2) with initial capital independent of . Indeed let any element of , then using (a) and (b) we have

This method is known as the martingale optimality principle. Let us now perform a multiplicative decomposition of into martingale and an increasing process. Given a continuous process we denote by its stochastic exponential:

where denotes the quadratic variation. Then

| (3.2) |

where

Since should be a supermartingale for every admissible (and a martingale for some element ), then has to be a non–positive process. With this in mind, a suitable candidate would be

which leads to

If in addition we let

then

with

The available results on existence of solutions to BSDEs require, to begin with, the predictability of the driver . In our case this is closely related to the predictability of in other words, to whether or not the candidate for an optimal strategy is acceptable.

Theorem 3.1.

Let be a predictable process such that

then for the mapping

where is as in Equation (3), is predictable. In addition there exists a predictable process in such that

and

Proof. Let us define for

The purpose of artificially bounding the values of is to make use of the theory of compact–valued correspondences (see Appendix A). It follows from Lemma A.1 that for all and for all the set is non–empty and compact. Moreover, Proposition A.3 guarantees that for all and the correspondence is weakly –measurable (see Definition in the Appendix for the definition of weakly measurability). Let denote the space of non–empty, compact subsets of equipped with the Hausdorff metric. This is a complete, separable metric space, in which takes its values. Theorem A.4 then states that for and the distance mapping

is a Carathéodory one. Since the process is predictable and is continuous for all the map

is –measurable. Finally

thus the mapping is predictable as the pointwise infimum of predictable ones. We now turn our attention to the second claim. First we observe that since is closed (and contained in ), the set

is compact. It follows from the Measurable Maximum Theorem ([AB06], page 605) that the correspondence is weakly –measurable. It is then implied by the Kuratowski–Ryll–Nardzewski Selection Theorem that admits a measurable selection in other words, there exists a predictable process such that

Finally using the fact that the strategy belongs to we have that

| (3.4) | |||||

To finalize, we must show that the quadratic–growth BSDE (3.1) admits a solution. In the following we will make use of the notion of BMO–martingale.

Definition 3.2.

A continuous martingale is a BMO–martingale, if there exists a positive constant such that for every stopping time ,

We will use the following property of BMO–martingales (which can be found in [KA94]): if is a BMO–martingale then is a true martingale.

We require the following result of Morlais [MO09, Theorem 2.5 and Lemma 3.1], which extends the results of Kobylanski [K00]:

Theorem 3.3.

Let be measurable. Assume that there exist a predictable process and positive constants satisfying and

If is such that

-

(1)

is continuous

-

(2)

then the BSDE (3.1) with driver admits a solution where and are predictable processes with bounded and satisfying . In addition, the process is a BMO martingale and hence is a true martingale.

The previous result allows us to show that the BSDE (3.1) with driver given by Equation (3) admits a unique solution. Note that the fact that is a true martingale is essential in our approach since it basically allows the process to be a (true) martingale for some element .

Corollary 3.4.

Proof. We apply Theorem 3.3, and measurability of is guaranteed by Theorem 3.1. The continuity in of the driver is straightforward, as are the growth conditions, given Assumption 2.3. Again by Theorem 3.3, is a BMO–martingale which by definition, means that there exists a positive constant such that for every stopping time ,

Hence, by Estimate (3.4), we have for any stopping time that

showing that is a BMO–martingale since is uniformly bounded by Assumption 2.3.

We conclude with the existence of an optimal strategy to Problem (2.2).

Theorem 3.5.

Under the assumptions made above there exists an acceptable strategy that solves Problem (2.2). If we define the value function as:

with the set of admissible -valued predictable processes such that for all in and then it holds that

Here is a solution to the BSDE (3.1) with driver given by Equation (3) and

Proof. The existence of a solution to the BSDE (3.1) is guaranteed by Corollary 3.4. Furthermore, the process

is a true martingale since and are BMO–martingales (with given as in Theorem 3.1) by Corollary 3.4. Now, as in [HIM05, Theorem 14], for any admissible , the process given by Equation (3.2) is a supermartingale. Indeed, by construction is non-positive and the stochastic exponential is local martingale. Let be a localizing sequence associated to it. We have for every (and ) that: and is a non–negative process. Thus, Fatou’s Lemma implies that

Using the martingale optimality principle, we have that the processes are well–defined and satisfy requirements (a) and (b). In addition, by construction, the processes such that is a martingale are those such that . Theorem 3.1 yields that these elements are admissible strategies, thus optimal. Take such an optimal strategy . We have that

The previous result admits a dynamic version:

Theorem 3.6.

Proof. Let any element of and such that the associated is a martingale. Then by definition of the processes, we have that since for and so

Hence, .

Remark 3.7.

Remark 3.8.

The stochastic process in the expression of the value function is sometimes called the opportunity process, since it gives the value of the optimal wealth with initial capital one unit of currency (see [N10]).

Remark 3.9.

Notice that for the sake of the explanation, we have chosen to fix the risk aversion coefficient in but we can also consider the case where . Then the driver given by Equation (3) has to be modified suitably.

4. Time Consistent Distortion Risk Measures

In this section we define a broad class of families of risk measures that are time consistent. We show that, under the constrains imposed by members of this class, optimal investment strategies follow a three–fund separation behavior. Let

where

and

Here a distortion risk measure, i.e.

where is the inverse CDF of and is a distortion, i.e., it is right–continuous, increasing on and The choice yields VaRα and yields TVaR LELα can be recovered by choosing (since LELα is TVarα computed under one of the risk neutral probability measures). Distortion risk measures form a rich class, which contains: proportional hazards, proportional odds, Wang transform, positive Poisson mixture, etc. It follows from direct computations that

In the light of this, one can see that Assumption (2.5) holds true. From this point on we work under the assumption that This implies (quite naturally) that the risk should be smaller than the current position.

4.1. A common form of the risk constraints

Below we present some properties of the constraint sets

Proposition 4.1.

Each constraint set can be expressed as

for some function which satisfies

Proof. The function is defined by

so it follows that In the light of

it follows that

The choice of the threshold and Proposition 4.1 yield the compactness of the constraint sets associated with the risk measures considered in this section.

4.2. A Three-Fund Separation Result

In this section we further characterize the optimal investment strategy. Let us recall that it is given by

Compactness of leads to compactness of which in turn yields the existence of the projection.

Theorem 4.2.

Proof. We cover the case only (the case can be obtained by an analogous argument). Let recall that for a fixed path the optimal strategy solves

The convex, quadratic functional

is minimized over the constraint set at a point which is either an absolute minimum or else should be on the boundary of Thus, for a fixed path, minimizes over the constraint The solution is not the zero vector, since the zero vector is not an absolute minimum and For , it follows that

where and stand for the partial derivatives of function . According to the Karush–Kuhn Tucker Theorem, either or else there is a positive such that

| (4.2) |

In both cases, straightforward computations, show that should have the form given in Equation (4.1).

Theorem 4.2 is a three-fund separation result. It states that a utility–maximizing investor who is subject to regulatory constraints will invest his wealth into three-funds: 1. the savings account; 2. a risky fund with return 3. a risky fund with return Most of the results in the financial literature are two–funds separation ones (optimal wealth being invested into a saving account and a risky fund). We would obtain such a two–funds separation result if we restricted our model to one in which stocks returns and volatilities were deterministic. It is a consequence of the randomness of the stocks returns and volatilities that the optimal investment includes an extra risky fund. Investment in the latter fund can be regarded as a hedge against risk implied by stochastic stock returns and volatilities.

Remark 4.3.

For the special case of TVaRα the associated acceptance set is convex; this is also the case when VaR whenever The convexity of implies the uniqueness of optimal trading strategy a fact that turns out to be useful in numerical implementations.

5. A numerically implemented example

In this section we present numerical simulations for the constrained optimal strategies and the associated constrained opportunity processes. Recall that by opportunity process we mean the process which appears in the value function in Theorem 3.6; that is . The opportunity process represents the value function of an investor with initial capital one dollar. It is a stochastic process and in the figures below we present one sample path. For simplicity and the numerical tractability of the analysis we assume that we deal with one risky asset (), one bond with rate zero () and one Brownian motion (). In addition, we assume that the risky asset is given by the following SDE:

Our simulation relies on numerical schemes for quadratic growth BSDEs. We use the scheme of Dos Reis and Imkeller [DRI10, DR10]. The latter, in a nutshell, relies on a truncation argument of the driver, and it reduces the numerical–simulation problem to one of a BSDE with a Lipschitz–growth driver . Here we use the so–called forward scheme of Bender and Denk [BD07].

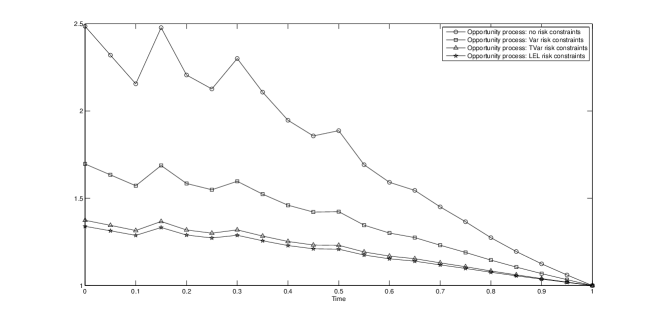

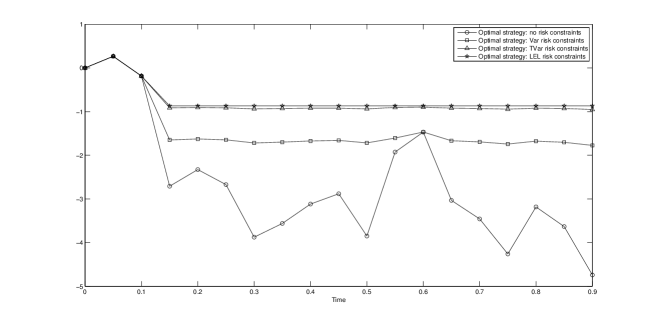

In Figure 1 we illustrate the opportunity processes arising from imposing VaR , TVar and LEL. We have used the following set of parameters: =0.85, =0.10, =0.3 and . The time discretization is and =1/15. The unconstrained opportunity process is also presented. The corresponding trading strategies are presented in Figure 2. We observe a spike in the opportunity process that may be explained by gambling; indeed looking at the TVaR constrained optimal strategy we see that it differs considerably from the unconstrained one (in which the stock is shorted). This finding supports the idea that risk constraints reduce speculation.

6. Conclusions

We have analyzed, within an incomplete–market framework, the portfolio–choice problem of a risk averse agent (who is characterized by CRRA preferences), when risk constraints are imposed continuously throughout the investment phase. Using BSDE technology, in the spirit of [HIM05], has enabled us to allow for a broad range of risk measures that give rise to the risk constraints, the latter being (possibly) time–dependent. In order to use such technology, we have made use of Measurable Selections theory, specifically when addressing the issue of the driver of the BSDE at hand. We have characterized the optimal (constrained) investment strategies, and in the case of distortion risk measures we have provided explicit expressions for them. Here we have shown that optimal strategies may be described as investments in three funds, which is in contrast with the classical two–fund separation theorems. Finally, using recent results in [DRI10], we have provided some examples that showcase the way in which our dynamic risk constraints limit investment strategies and impact utility at maturity.

Appendix A Properties of the constraint sets

Several analytical properties of the (instantaneous) constraint sets are established in this section. The analysis requires some core concepts of the theory of measurable correspondences333For a comprehensive overview of the theory of measurable correspondences, we refer the reader to [AB06].. We require the following auxiliary correspondences:

The purpose of artificially bounding the values of is to make use of the theory of compact–valued correspondences, which exhibit many desirable properties.

Lemma A.1.

For any the correspondence is non–empty and compact valued for almost all

Proof. The non–vacuity follows from the fact that i.e. no wealth invested in risky assets, is an acceptable position. To show closedness of the sets fix and consider a sequence such that Using Assumption 2.5 it holds that

holds for all and which implies that The latter, together with the fact that finalizes the proof.

Definition A.2.

A correspondence between a measurable space and a topological space is said to be weakly measurable if for all closed, the lower inverse of defined as

belongs to

In the case of compact–valued correspondences, weak–measurability and Borel measurability (in terms of the Borel –algebra generated by the Hausdorff metric) are equivalent notions. Given a correspondence we define the corresponding closure correspondence via For notational purposes let

Recall that denotes the predictable –algebra on The function is a Carathéodory function with respect to i.e. it is continuous in and –measurable in

Proposition A.3.

For any the correspondence is weakly

–measurable.

Proof. Let be closed and consider dense. For let

We have that

The second equality holds because is continuous in is dense and is open. Since is Carathéodory, then hence for all the correspondence is weakly –measurable. Next we have

where the second inclusion follows again from the continuity of in This implies that

and

The graph of the closure of a weakly–measurable correspondence is measurable, hence is measurable, by virtue of being the (denumerable) intersection of measurable graphs. Since a compact–valued correspondence with a measurable graph is itself weakly–measurable (see Lemma 18.4 (part 3) and Corollary 18.8 in [AB06]), we conclude that the correspondence has such property.

The following theorem, whose proof can be found in [AB06], page 595, plays an important role in the proof of predictability of our BSDE’s driver:

Theorem A.4.

A nonempty–valued correspondence mapping a measurable space into a separable, metrizable space is weakly–measurable if and only if its associated distance function is a Carathéodory function.

References

- [AB06] C. Aliprantis and K. Border, Infinite Dimensional Analysis, a Hitchhiker’s guide (3rd. edition), Springer Verlag, 2006.

- [AP05] C. Atkinson and M. Papakokinou, Theory of optimal consumption and portfolio selection under a capital-at-risk (car) and a value-at-risk (var) constraint,, IMA Journal of Management Mathematics (2005), no. 16, 37–70.

- [BCK05] A. Berkelaar, P. Cumperayot, and R. Kouwenberg, The effect of var-based risk management on asset prices and volatility smile, Europen Financial Management (2005), no. 8, 65–78.

- [BS01] S. Basak and A. Shapiro, Value-at-risk-based risk management: optimal policies and asset prices,, Rev. Financial Studies (2001), no. 14, 371–405.

- [BD07] C. Bender and R. Denk, A forward scheme for backward SDEs., Stochastic Processes Appl., Volume 117, Number 12 (2007), 1793–1812.

- [BH08] P. Briand and Y. Hu, Quadratic BSDEs with convex generators and unbounded terminal conditions, Probab. Theory Relat. Fields (2008), no. 141, 543–567.

- [CHI08] D. Cuoco, H. He, and S Issaenko, Optimal dynamic trading strategies with risk limits, Operation Research, 56 no. 2, 358-368.

- [CK92] J. Cvitanić and I. Karatzas, Convex Duality in Constrained Portfolio Optimization, Ann. Appl. Probab. Volume 2, Number 4 (1992), 767-818.

- [DR10] G. dos Reis, On some properties of solutions of quadratic growth BSDE and applications in finance and insurance, PhD Thesis, Humboldt University in Berlin (2010), available at http://www.math.tu-berlin.de/dosreis/publications/GdosReis-PhD-Thesis.pdf.

- [DRI10] G. dos Reis and P. Imkeller, Path regularity and explicit convergence rate for BSDE with truncated quadratic growth, Stochastic Processes Appl. Volume 120, Number 3 (2010), 348-379.

- [DVLLLW10] G. Dmitrasinović-Vidović, A. Lari-Lavassani, X. Li, and T. Ware, Dynamic portfolio selection under capital at risk, Journal of Probability and Statistics (2010), 1-26.

- [ESR01] C. Klüppelberg, S. Emmer. and R. Korn , Optimal portfolios with bounded capital at risk, Mathematical Finance (2001), no. 11, 365–384.

- [GSW09] A. Gabih, J. Sass and R. Wunderlich, Utility maximization under bounded expected loss, Stochast. Models (2009), no. 25, 375-409.

- [GW06] A. Gundel and S. Weber, Robust utility maximization with limited downside risk in incomplete markets, Stochastic Processes and their Applications (2007), no. 117, 1663–1688.

- [HIM05] Y. Hu, P. Imkeller and M. Müller, Utility Maximization in Incomplete Markets, The Annals of Applied Probability (2005), Vol. 15, no. 3, 1961–1712.

- [KA94] N. Kazamaki, Continuous exponential martingales and BMO, Vol. 1579 of Lecture Notes in Mathematics, Springer-Verlag, Berlin, (1994).

- [K00] M. Kobylanski, Backward stochastic differential equations and partial differential equations with quadratic growth, Ann. Probab. (2000) 28, no. 2, 558-602.

- [KP09] C. Klüppelberg and S. Pergamenchtchikov, Optimal Consumption and Investment with Bounded Downside Risk for Power Utility Functions, F. Delbaen et al. (eds.), Optimality and Risk Modern Trends in Mathematical Finance, Springer-Verlag Berlin Heidelberg 2009

- [LVT06] M. Leippold, P. Vanini and F. Trojani, Equilibrium impact of value-at-risk, Journal of Economic Dynamics and Control (2006), 1277-1313.

- [MO09] M.-A. Morlais, Quadratic BSDEs driven by a continuous martingale and applications to the utility maximization problem, Finance and Stochastics (2009), Vol. 13, no. 1, 121–150.

- [N10] M. Nutz, The Opportunity Process for Optimal Consumption and Investment with Power Utility, Mathematics and Financial Economics, 3 (2010), no. 3, 139-159.

- [P07] T. A. Pirvu, Portfolio optimization under the Value-at-Risk constraint, Quantitative Finance, 7 (2007), 125-136.

- [PZ09] T. A. Pirvu and G. Zitkovic, Maximizing the growth rate under risk constraints, Mathematical Finance, 19 (2009), no. 3, 423-455.

- [PR10] R., Prieto, Dynamic Equilibrium with Heterogeneous Agents and Risk Constraints (2010), Preprint.

- [PS10] W. Putschögl and J. Sass, Optimal investment under dynamic risk constraints and partial information, Quantitative Finance, (2010), 1-18.

- [Y04] K. F. C. Yiu, Optimal portfolios under a value-at-risk constraint, Journal of Economic Dynamics& Control (2004), no. 28, 1317–1334.