Penalty Methods for the Solution of Discrete HJB Equations – Continuous Control and Obstacle Problems

Abstract.

In this paper, we present a novel penalty approach for the numerical solution of continuously controlled HJB equations and HJB obstacle problems. Our results include estimates of the penalisation error for a class of penalty terms, and we show that

variations of Newton’s method can be used to obtain globally convergent iterative solvers for the penalised equations. Furthermore, we discuss under what conditions local quadratic convergence of the iterative solvers can be expected. We include numerical results demonstrating the competitiveness of

our methods.

Key Words: HJB Equation, HJB Obstacle Problem, Min-Max Problem, Numerical Solution, Penalty Method,

Semi-Smooth Newton Method, Viscosity Solution

2010 Mathematics Subject Classification: 65M12, 93E20

1. Introduction

Problems of optimal stochastic control arise numerously in the mathematical analysis of real-world phenomena (cf. [24, 36]), and, applying Bellman’s principle of optimality, they can often be reformulated as Hamilton-Jacobi-Bellman (HJB) equations (cf. [41]). Numerical approaches for solving HJB equations can roughly be split into two fields: Markov chain approximations (e.g. cf. [28, 29, 11]) and finite difference methods (see [1, 3, 2] and references therein). Even though both approaches can be found to be closely related (e.g. cf. [37]), there is a rather clear conceptual difference: Markov chain approximations make explicit use of the underlying stochastic model and solve for transition densities, while finite difference methods deal solely with the HJB equation and solve for the unique viscosity solution directly (cf. [19]).

We begin by introducing the two kinds of non-linear equations we aim to solve numerically in this paper. Initially, the problem formulations are slightly informal and primarily motivational, and any equation of the described type permitting a discretisation with certain properties fits into our framework.

Problem 1.1.

Let be a compact111Our results can trivially be extended to any finite union of compact intervals in , which, in particular, includes any finite set. For simplicity of presentation, we work with as given. interval. Let (with ) be an open set, and let , , be a given family of affine differential operators on . Find a function such that

| (1.1) |

Problem 1.2.

In the situation of Problem 1.1, let be an additional affine differential operator. Find a function such that

| (1.2) |

Equation (1.1) is a standard HJB equation as arising from many problems of stochastic optimal control (cf. [41, 33]); examples in which the control set is truly infinite and does not reduce to a finite set include problems of indifference pricing of financial derivatives (cf. [4] and references therein) and gas storage valuation (cf. [7, 5]). The second formulation, Problem 1.2, is an obstacle problem (cf. [9]) involving an HJB equation, and is a special case of an Isaacs’ equation (cf. [41, 19, 18]); considering an example from [31], we will later see that the computation of an early exercise indifference price in an incomplete market model leads to an equation of the form (1.2), a context in which the similarity to an obstacle problem can clearly be traced back to the American exercise feature (cf. [8]).

Evidently, if we replace (1.1) by

| (1.3) |

we can easily recover formulation (1.1) by moving inside the “inf” and defining , ; in some applications, the operator can be found to simply be the time derivative, i.e. , whereas in other cases it may constitute the main part of a considered equation.

In this paper, we are concerned with the finite difference approximation of equations (1.1) and (1.2). Based on the – most helpful – results in [1, 3, 2], it can be shown, for most HJB equations, that a monotone, stable, and consistent finite difference approximation converges to the unique viscosity solution, which is the correct notion of solution since it usually corresponds to the stochastic model. However, even if convergence can be guaranteed, one still has to solve the resulting non-linear discrete systems. The only exception are fully explicit time-stepping schemes, which generally suffer from undesirable stability constraints.

We assume a rather general class of discretisations, one that is likely to arise when applying the convergence results cited above, and we study how the discrete systems can be solved using penalty methods.

Existing work on the topic includes [12, 39, 14, 30, 15], where a policy iteration algorithm is used, and [40], where a penalty approximation for HJB equations is introduced. For the solution of the penalised equations, we consider Newton-like iterative solvers, many properties of which we prove based on results in [32, 34]. See also [22, 20, 21] regarding the use of semi-smooth Newton methods in the context of variational inequalities and their interpretation as primal-dual active set strategies, which in turn are closely related to the method of policy iteration.

We extend the previous results in two ways. First, we consider a compact set of controls; until now, except for [30], all algorithms were based on the assumption of a finite control set. Second, we also solve an HJB obstacle problem, which arises for example in mathematical finance when pricing early exercise claims in incomplete markets, e.g. in [31]; to the best of our knowledge, the only existing algorithm capable of handling this problem is the Ho-3 algorithm introduced in [30], which can be considered as a nested policy iteration. The discussed techniques have many applications in mathematical finance. Besides the applications already considered in [12, 14, 40], which include uncertain volatility models, transaction cost models, and unequal borrowing/lending rates and stock borrowing fees, our methods are applicable to many problems from portfolio optimisation, including indifference pricing [42, 4] and indifference pricing with early exercise features [31].

Structure of this Paper

We aim to devise numerical schemes for the solution of HJB equations and HJB obstacle problems. For a general overview of our numerical approach, we refer to Figure 1 in [40], where a similar conceptual structure is depicted.

Section 2

We relate the two non-linear equations of Problems 1.1 and 1.2 each to a non-linear discrete system; the latter are chosen such that they are monotone and correspond to what naturally arises when applying a fully implicit or weighted time stepping discretisation to the equations. Since implicit schemes are usually unconditionally stable and finite difference schemes are naturally consistent, this setup allows to conclude convergence to the unique viscosity solution whenever a strong comparison principle holds (cf. [1, 3, 2]). We proof existence and uniqueness of solutions to the discrete problems and present some further properties.

Section 3

We present a penalised problem which approximates the discrete HJB equation to an accuracy of , where is the penalty parameter. A similar approach was used in [13] for American options, and was extended to HJB equations in [40]. The novelty of the approach described in this paper is that we do not penalise for every control individually, as was done in [40], but only penalise the maximum violation; this significantly simplifies the penalty formulation and allows for compact control sets.

Section 4

We study the iterative solution of the penalised HJB equation presented in Section 3. We introduce two globally convergent Newton-type solvers, and we show that, when using a smooth penalty term, the classical Newton scheme can be expected to have local quadratic convergence.

Sections 5 and 6

In these two sections, we extend the techniques from Sections 3 and 4 to show that the use of penalisation (Section 5) with subsequent non-linear iteration (Section 6) is also a powerful strategy for the solution of the obstacle version of a continuously controlled HJB equation. In particular, in Section 6, we present two Newton-type iterative methods, one that converges globally and one that converges locally quadratically.

Section 7

The numerical strategies developed in Sections 3–6 are designed for HJB equations and HJB obstacle problems with a compact set of controls and continuous dependence of the differential operators on the controls. For some equations, it may be convenient to approximate the dependence on the controls, e.g. by piecewise linearisation; in this section, we prove that the previously introduced algorithms are stable with respect to such perturbations.

Section 8

2. Problem Formulation

Following [10], we introduce , , to be the set of all real square matrices of dimension whose off-diagonal entries are all non-positive, i.e.

and define

to be the set of M-matrices in ; it can be found in [10] that for all matrices . Furthermore, we introduce the set

which has the following properties.

-

•

If, for , we replace the -th row of by the -th row of some , the resulting matrix will still be in .

-

•

for two matrices , .

Throughout this paper, the set will be one of our main building blocks since it allows us to deduce the M-matrix property of a matrix that was constructed from a number of other matrices.

Remark 2.1.

Let and define . Consider two vectors , and a matrix . For any , we denote by and the -th coordinate and the -th row of vector and matrix , respectively. When writing , we generally mean that for all , and we take to be the vector satisfying for all . The definitions extend trivially to other relational operators and to the maximum of two vectors.

Making use of the definition of , we assume, for now, that we can find sensible discretisations of Problems 1.1 and 1.2 of the following form; we will give a more rigorous justification of this assumption later on.

Problem 2.2.

Let

| (2.1) | ||||

| (2.2) |

be continuous functions, with , . Find such that

| (2.3) |

The continuity requirement of and above is to be understood in the sense of any vector norm, say or , in and . For example, for , the maps and will be of the form

respectively, with , , , , , .

Problem 2.3.

In the setting of Problem 2.2, let also and . Find such that

| (2.4) |

We will, without always mentioning so explicitly, make frequent use of the fact that every function which is continuous on a compact interval attains its minimum and maximum on the interval.

Proof.

Corollary 3.6 and Theorem 4.1 give the existence of a solution to Problem 2.2, and, similarly, Corollary 5.5 and Theorem 6.1 (or, alternatively, Ho-3 in [30]) give the existence of a solution to Problem 2.3. Hence, it remains to show the uniqueness of the solutions. To this end, suppose we have two solutions and to Problem 2.2. For every , there exists a such that

and we also have

Denote by the matrix consisting of the rows , . We have and , from which we get since . Conversely, using the same arguments but swapping and , we can also get , which then proves the uniqueness of a solution to Problem 2.2. Now, suppose we have two solutions and to Problem 2.3. For , let , be such that

| (2.5) |

From (2.4), we then get that, for , we have

| (2.6) |

We distinguish the following possible cases in (2.6).

-

(i)

We have .

-

(ii)

We have , in which case .

-

(iii)

We have , in which case .

-

(iv)

We have , in which case .

At this point, we can show the uniqueness of a solution to Problem 2.3 by arguing analogously to the first half of this proof (where we introduced the matrix and used its -matrix properties). ∎

Next, we show that the discretisation matrices appearing in (2.3) and (2.4) have some convenient boundedness properties.

Lemma 2.5.

For as in Problem 2.2, there exists a constant such that

Proof.

Since continuity of implies directly the existence of a constant such that for all , it only remains to prove the corresponding estimate for the inverse matrices. An M-matrix is, in particular, non-singular with positive determinant (cf. [10]), and, hence, we have that is a continuous and positive function on . As every continuous function on a compact interval assumes its minimum, there exists an such that for all . Now, in [10], it can be found that, for a square non-singular matrix , it is if we define

where is the cofactor of in the matrix . Since the calculation of the cofactor is, like the determinant, a continuous operation on the entries of the matrix, there exists a constant such that, for and , it is

This proves the lemma. ∎

Corollary 2.6.

Suppose that, in the situation of Problem 2.2, we define

| and |

where denotes the matrix having as -th row, , the -th row of . In this case, is a compact set, is a continuous function, and for every . Furthermore, there exists a constant such that

Proof.

The proof is identical to the one of Lemma 2.5, the only difference being that we have to deal with a continuous function instead of . ∎

3. Penalising the Discrete HJB Equation

We begin by studying Problem 2.2, which we call the HJB equation; for nominal differentiation, Problem 2.3, which we discuss subsequently, will be referred to as the HJB obstacle problem. The penalty approximation used in this paper is an extension of ideas used for discretely controlled HJB equations in [40] and for American options in [13]. The penalised equation is a non-linear equation itself and can be solved by an iterative scheme (cf. Section 4).

We introduce the penalty term

| (3.1) |

Assumption 3.1.

For , we take to be a non-decreasing function satisfying and .

Problem 3.2.

Let , . Find such that

| (3.2) |

In (3.2), contrary to [40], a penalty is applied only to the maximum violation of the constraints; since the solution to Problem 3.2 can be shown to be bounded independently of (cf. Lemma 3.4), this guarantees all constraints to be satisfied as (cf. Corollary 3.6).

We point out that, in Problem 3.2, does not require any further specification, and all the results of this section can be shown to hold for any choice of . In Section 8.1, we will study the practical effects of in a numerical example.

Lemma 3.3.

If there exists a solution to Problem 3.2, then it is unique.

Proof.

Suppose we have two solutions and . From (3.2), we get that

| (3.3) |

Now, let , and define , to be such that

For the second and third term in (3.3), we have

| (3.4) | ||||

At this point, the idea is that if there exists a matrix satisfying

then we can deduce since , and we get uniqueness as in Theorem 2.4. We distinguish between the following two cases.

- •

-

•

If , then , which is equivalent to , and we can set .

∎

In Section 4, we will discuss several choices of the penalty function that allow to conclude the existence of a solution to Problem 3.2. Here, we study the approximation of Problem 2.2 by Problem 3.2.

Lemma 3.4.

Suppose there exists a solution to Problem 3.2. There exists a constant , independent of and , such that .

Proof.

We rewrite (3.2) to get

| (3.5) |

Hence, for every component , we have that

Therefore, we may, for , define to be such that is satisfied, and, introducing to be the matrix having as -th row the -th row of , , and defining correspondingly, we have

From Corollary 2.6, we then get for some constant independent of and . To see that the negative part of is bounded as well, we note that, from (3.5), we have

in which . ∎

Lemma 3.5.

Suppose there exists a solution to Problem 3.2 for every . There exists a constant , independent of and , such that

| (3.6) |

Proof.

For the canonical choice , (3.6) reduces to

| (3.8) |

stating that satisfies Problem 2.2 to an order ; if the set is discrete, estimate (3.8) matches similar results in [13] and [40].

Corollary 3.6.

Proof.

Since is bounded (as seen in Lemma 3.4), it has a convergent subsequence, which we do not distinguish notationally; we denote the limit of this subsequence by . From Lemma 3.5, we may deduce that

| (3.9) |

Now, consider a component . Using again Lemma 3.5, we know that, for every , there exists a such that

| (3.10) |

Recalling that is compact and , we can then infer that there exists once more a subsequence of , again not notationally distinguished, and a such that ; hence, recalling the continuity of and in the definition of Problem 2.2, it follows from (3.10) that

| (3.11) |

Altogether, combining (3.9) and (3.11), we see that solves Problem 2.2. Since Problem 2.2 has a unique solution (cf. Theorem 2.4), the just given result holds not only for subsequences of , but the whole sequence converges. ∎

We have finally done enough preparatory work to show that – if we choose the penalty function correctly – the solution to Problem 3.2 is indeed a good approximation of the solution to Problem 2.2; in fact, we can obtain an approximation that is of first order in the penalty parameter.

Theorem 3.7.

Proof.

Without loss of generality, we may assume that . Let . We use as introduced in the proof of Corollary 3.6, which means, in particular, that (3.11) holds. Furthermore, for , we define to be such that

which means, as seen in the proof of Lemma 3.5, that

for some constant independent of and . Applying (3.10), (3.11) and the definition of , we now have that

and

Denoting by , the matrices having as -th row, , the -th rows of and , respectively, we get that

and, using Corollary 2.6, we may infer that

for some constant independent of and . ∎

4. Solving the Penalised HJB Equation by Iteration

In the previous section, we have seen how Problem 2.2 can be approximated by penalisation. We will now discuss iterative methods for the solution of the penalised problem, i.e. algorithms for the computation of satisfying (3.2).

Defining

we need to solve . For , , we define

and we assume that . For some of the following theorems, we require further that, for , ,

| (4.1) |

holds whenever is well defined, with ; the Jacobian of is then given by

| (4.2) |

for , ; if does not exist at 0, we set . For the numerical examples following later in this paper, (4.1) is generally satisfied.

The next theorem states that a globally convergent iterative scheme for the solution of Problem 3.2 exists whenever is a smooth and non-decreasing function.

Theorem 4.1.

Proof.

We will show that conditions - in Theorem 4 in [32] are satisfied. First of all, since is continuously partially differentiable, it is differentiable as a function , which, in particular, guarantees -differentiability of . In , we need to show that, for arbitrary , the set is bounded; since, for , we have , and either or , this can easily be inferred by applying Corollary 2.6. The partial derivatives of are non-negative, which means , , and, hence, holds. Given the continuity of the partial derivatives of , we can apply Lemma 1 and Theorem 2 in [32] to obtain . Finally, in , it is sufficient to show that, for any compact set , there exists a constant such that

| (4.3) |

for all , , . We prove (4.3) by contradiction, i.e. suppose there exist sequences and , for all , such that . Based on the boundedness of the sequences and , we infer the existence of subsequences – not notationally distinguished – converging to limits and , respectively, where , and we get . Now, from , , we have that , and we note that implies , which is a contradiction to . Hence, we may conclude that (4.3) must hold true, which completes the proof. ∎

Having seen that Newton’s method with line search can lead to a globally convergent scheme, we next come to look at Newton’s method in its classical form.

Algorithm 4.2.

(Newton’s Method for the pen. HJB Equation) Let be some starting value. Then, for known , , find such that

| (4.4) |

Theorem 4.3.

Proof.

If has a strong and non-singular -derivative at , then the result can be found in Theorem 3 in [32]. Given the continuity of the partial derivatives of , we can apply Theorem 2 in [32] to obtain the existence of a strong -derivative of , which coincides with . Since , , implies , the strong -derivative of at is indeed non-singular. ∎

Now, if we use (in which case, based on (4.2), is still well defined), (4.4) simplifies, and we get the following special case of Algorithm 4.2.

Algorithm 4.4.

(Newton-like Method for pen. HJB Eq.) For and , define to be such that

| (4.5) |

and set and to be matrix and vector consisting of

-

•

rows and , , respectively, if we have

-

•

and having zero rows if .

If , we now have , and (4.4) becomes

which is equivalent to

| (4.6) |

Lemma 4.5.

Let be some starting value, and let be the sequence generated by Algorithm 4.4. We have for .

Proof.

Writing for and , we obtain

and subtracting yields

| (4.7) |

In this, has a non-negative inverse, and, therefore, the proof is complete if we can show that the right-hand side of expression (4.7) is non-negative; to do this, we consider the rows of the right-hand side of (4.7) separately.

This completes the proof. ∎

Lemma 4.6.

Let be the sequence generated by Algorithm 4.4. There exists a constant such that, for every starting value , , .

Proof.

Theorem 4.7.

5. Penalising the Discrete Obstacle Problem

Having dealt with Problem 2.2 (termed HJB equation) in the previous sections, we now consider Problem 2.3 (termed HJB obstacle problem), which has to be treated differently due to the combination of “min” and “max” operators. We use the same penalty term as introduced in (3.1), and we again make Assumption 3.1.

Problem 5.1.

Let . Find such that

| (5.1) |

If one treats the “max” inside the “min” in (2.4) as if , then the penalty formulation (5.1) corresponds to the penalisation technique introduced in [13], and, thus, (5.1) has a heuristic interpretation; however, mathematically, the situation is a bit more subtle, and we will now study various properties of Problem 5.1.

Lemma 5.2.

If there exists a solution to Problem 5.1, then it is unique.

Proof.

Lemma 5.3.

Assume there exists a solution to Problem 5.1 for every . There exists a constant , independent of and , such that

Lemma 5.4.

Assume there exists a solution to Problem 5.1 for every . There exists a constant , independent of and , such that

| (5.2) |

Proof.

For the canonical choice , (5.2) becomes

meaning that satisfies Problem 2.3 to an order ; this property is consistent with the penalty approximation of the HJB equation discussed in Section 3.

Corollary 5.5.

Proof.

This can be shown by arguing as in the proof of Corollary 3.6. ∎

Theorem 5.6.

Proof.

We proceed similarly to the proof of Theorem 3.7. Without loss of generality, we may assume that . Let . Let be such that

Similarly, applying Lemma 5.4, let be such that

for some constant independent of and . Furthermore, as already in (2.5), let , such that and . We first consider , for which we distinguish two cases. ( , are taken to be constants independent of and .)

-

(i)

If , we have .

-

(ii)

If , we have .

Now, for the reverse case, , similar estimates can be obtained by swapping the roles of “” and “”. The proof can be completed by following the lines of the proof of Theorem 3.7. ∎

6. Solving the Penalised HJB Obstacle Problem by Iteration

In Section 4, we have discussed how to iteratively solve the penalty approximation of the discrete HJB equation. Similarly, in this section, we discuss iterative methods for the penalty approximation of the discrete HJB obstacle problem.

Defining

for , to solve (5.1), we need to compute such that . For , , we define

| (6.1) |

and we assume that , , and

| (6.2) |

for , . The Jacobian of is then given by

| (6.3) |

for , , whenever is well defined; if does not exist at 0, we set . Like in Section 4, we point out that, for the numerical examples following later in this paper, (6.2) is generally satisfied.

As already in Theorem 4.1, whenever is a smooth and non-decreasing function, we can find a globally convergent iterative scheme for the solution of Problem 5.1.

Theorem 6.1.

Proof.

The proof is a minor modification of the proof of Theorem 4.1. ∎

Knowing that Problem 5.1 has a solution for sufficiently smooth penalty terms , we can now proceed to showing that there also exists a solution if we penalise using the -function.

Corollary 6.2.

If , then there exists a solution to Problem 5.1.

Proof.

Let be a sequence of penalty functions satisfying , and for , , , and let be the sequence of solutions to Problem 5.1 corresponding to . Based on Lemma 5.3, we know that there exists a subsequence of , not notationally distinguished, that converges to a limit as . We aim to show that solves Problem 5.1 for . We have

in which we obtain

if we argue as in the proof of Corollary 3.6, and

as by the properties of ; hence, we have . ∎

Having established that Newton’s method with line search can be used to solve the penalised HJB obstacle problem, we proceed to Newton’s method in its classical form.

Algorithm 6.3.

(Newton’s Method for the pen. HJB Obstacle Prob.) Let be some starting value. Then, for known , , find such that

| (6.4) |

Theorem 6.4.

Proof.

The result follows from Theorem 3 in [32] if is -differentiable and has a strong and non-singular -derivative at . Recalling (6.2), we can argue as in the proof of Theorem 4.3 to obtain -differentiability of . From Theorem 2 in [32], it follows that has a strong -derivative, which is non-singular since for all . ∎

We point out that, based on the assumptions of Theorem 6.1, the Lipschitz property of , additionally required in Theorem 6.4, depends entirely on the regularity of in (6.2).

If we use (in which case, based on (6.3), is still well defined), (6.4) simplifies, and we get the following special case of Algorithm 6.3.

Algorithm 6.5.

From (6.5), it is easy to see that Algorithm 6.5 is well defined. The next theorem states that, given certain conditions on the matrix , local quadratic convergence of Algorithm 6.5 to the solution of Problem 5.1 for (see also Corollary 6.2) can be guaranteed.

Theorem 6.6.

Let be the sequence generated by Algorithm 6.5. There exists a constant such that, for every starting value , it is , . Furthermore, if , where denotes the identity matrix, then there exists a neighbourhood of such that, for any starting value , remains in and converges to the solution at a quadratic rate.

Proof.

The boundedness of follows from (6.5) by arguing as in the proof of Lemma 4.6. The quadratic local convergence property of follows from Theorem 3.2 in [34] if is semi-smooth and all are non-singular, where denotes the generalised Jacobian as introduced in [6]. By the assumptions at the beginning of this section, is continuously partially differentiable (and, in particular, semi-smooth) everywhere except on the set , since the only critical term is . Denoting the directional derivative at in direction by , it can easily be verified that

| (6.6) |

which, by Theorem 2.3 in [34], gives semi-smoothness on , and, since the generalised Jacobian at is given by

we see that all are in fact non-singular. ∎

7. Evaluating the Continuous Control in Practice

If we solve Problems 2.2 and 2.3 using penalisation, we have to numerically deal with the continuous control, e.g. when computing and in (4.5) and (6.1) for given and , respectively. Now, if the control is well behaved (as in the examples following later in this paper), the exact minimum/maximum can be found by differentiating and using analytical techniques; however, this is not necessarily always possible, i.e. we might have to approximate and by functions that are easier to handle numerically. The following remark states that such an approximation is legitimate within the framework of our algorithms.

Remark 7.1.

(Stability in the Control) Suppose we have families of functions and , , satisfying the following properties.

- •

-

•

For every , it is and .

Suppose we solve Problems 3.2 and 5.1 by using the approximations and for some , running any of the algorithms discussed in Sections 4 and 6, obtaining solutions and , respectively. In the limit , we have and , where and , respectively, denote the solutions to Problems 3.2 and 5.1 for and .

Proof.

For fixed , all results from the previous sections hold, and it only remains to show that and as . Since all involved functions are continuous on the compact interval , the convergence and is uniform in ; hence, we can reproduce results of Corollary 2.6 with constants independent of , which, following Lemmas 3.4 and 5.3, means that and are bounded independently of . We then infer the existence of converging subsequences, not notationally distinguished, of and , respectively. Since the convergence in is uniform in , we may swap “” and “” in expressions (3.2) and (5.1), and we see that the limits of the sequences and do indeed solve Problems 3.2 and 5.1, respectively. The uniqueness of the solutions (see Lemmas 3.3 and 5.2) means that not only subsequences but the whole sequences converge. ∎

We point out that the rather general definition of approximating functions used in the above remark includes most common numerical approximations, e.g. piecewise constant, piecewise linear and other finite subspace approximations.

8. Numerical Results

Finally, we come to test and analyse the applicability of the previously introduced numerical techniques by solving two models from mathematical finance, presented in Sections 8.1 and 8.2, which lead directly to equations as given in Problems 1.1 and 1.2, respectively.

8.1. Example: An Incomplete Market Investment Problem

In this section, we solve an incomplete market problem taken from [42]. More precisely, we look at an optimal investment model in which an agent has to distribute his money between a risk free bond and a risky stock; the market incompleteness arises from the stochastic volatility of the stock price process.

Let , , be bounded and globally Lipschitz functions, and suppose that there exists a constant , independent of , such that . Let be some finite time horizon. Let and , , . Suppose we have a bond price process , a stochastic volatility process and a stock price process solving, respectively,

where , , are two Brownian motions defined on a probability space with a correlation coefficient .

Staying exactly in the framework of [42], we consider an investor who can invest in the stock and in the bond. We suppose that the investor has initial wealth and that he may rebalance his portfolio at any time ; here, and denote the amounts invested, respectively, in the bond and in the stock. The investor’s wealth process solves

and must satisfy for every . We take the investor’s utility function to be of CRRA-type and given by

for some constant . Now, trying to maximise the final utility, the investor’s value function is given by

| (8.1) |

where is the set of admissible trading strategies (for details, see [42]). We cite the following result, which shows how this utility maximisation problem can be solved.

Proposition 8.1.

The value function introduced in (8.1) can be written as

where solves

| (8.2) |

with and an appropriately chosen compact set, and satisfies

| (8.3) |

The notion of solution used in this context has to be understood in the viscosity sense (cf. [19]), and , are the unique solutions to (8.2) and (8.3), respectively.

Proof.

In (8.2), we make the assumption of being a compact set since, for every time , the maximum in (8.2) is assumed at , where is the investor’s optimal trading policy (cf. [42]), which should not reach infinity in a meaningful financial model.

Clearly, from Theorem 8.1, to find , we need to compute or and solve either equation (8.3) or (8.2); we have deliberately chosen a problem which can be linearised such that we can obtain a reference solution by standard methods. In the next few sections, we will select parameters and present and compare several approaches of computing .

8.1.1. Choosing Model Parameters and Functions

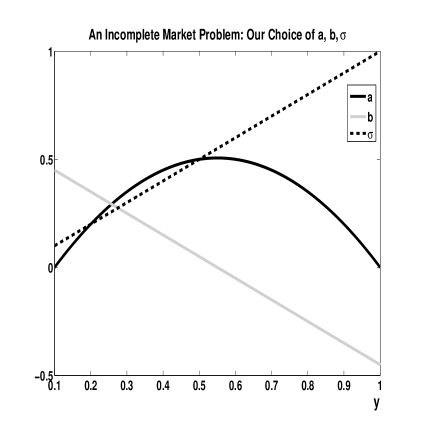

We set , , , , and . Furthermore, we introduce and , and, for , we use

Functions , and are shown in Figure 1; they satisfy the technical conditions listed in the previous section and guarantee .

8.1.2. Discretisation of the Continuous Equations

Numerically, we solve equations (8.3) and (8.2) backwards in time, starting at expiry , on a grid , where and . We perform a fully implicit finite difference discretisation, using one-sided differences for all first derivatives (including the time derivative) and central differences for all second derivatives. (For a general overview of basic finite difference concepts for PDEs, e.g. see [35].) In particular, when discretising (or ), where denotes the combined coefficient of the first -derivative in (8.3) (or (8.2)), we switch between left-sided and right-sided differences in accordance with a positive or negative sign of the coefficient ; this way, we can guarantee the following two properties.

-

•

The tridiagonal discretisation matrix implied by our fully implicit scheme has positive entries on the diagonal and non-positive entries on the upper/lower diagonals.

-

•

Since and , the boundary conditions at and are replaced by finite differences pointing inwards. (cf. [38]).

Proceeding as just described, the linear parabolic PDE in (8.3) is approximated by a simple linear system of equations. Furthermore, taking to be , with , our discretisation of equation (8.2) matches Problem 2.2, with (2.1) and (2.2) satisfying all assumptions.

Remark 8.2.

Based on our choice of functions and (cf. Figure 1), the diffusion will always stay in . Conceptually, this means that no ‘outside’ information – like Dirichlet boundary conditions – is required for the PDE to be completely specified on the interval , since the flow of information can be thought of as coming from ‘within’. Mathematically, this means that, by taking , , and using one-sided inwards pointing finite difference stencils at and 1, we obtain a consistent (and monotone) discretisation scheme without requiring any Dirichlet boundary conditions.

Remark 8.3.

It is generally non-trivial to prove convergence of finite difference schemes applied to a (possibly nonlinear) PDE for which only viscosity solutions can be shown to exist. The standard reference is [1], where – loosely speaking – it is shown that every stable and monotone discretisation converges if the equation satisfies a strong comparison principle (cf. [19]); other (more specific) approaches include [27, 2, 23, 26, 3, 25]. For the current example, consistency is straightforward to prove (e.g. cf. [40]), stability can be shown following [12] since we have what they call a “positive coefficient discretisation”, and a strong comparison result can be found in [3]; hence, altogether, the results of [1] are applicable and convergence to the unique viscosity solutions of (8.3) and (8.2) can be guaranteed.

8.1.3. Solution of the Discrete Systems

In this section, we will compare the following three ways of numerically solving the incomplete market problem represented by the equations in Theorem 8.1. All computations are done in Matlab.

-

•

We solve the linear system of equations resulting – for every time step – from a discretisation of the linear parabolic PDE in (8.3).

- •

The use of policy iteration has been studied in [12, 30] and is briefly summarised in Appendix A. Following Section 7, we approximate by , thereby discretising by using a very fine grid of 1001 points. (Effectively, in the notation of Remark 7.1, we approximate and by piecewise constant functions.) Numerically, when computing candidate solutions to equations (2.3) and (3.2) by policy iteration and Algorithm 4.4, respectively, we terminate the iterations according to the following two checks of accuracy, using 1e-08.

- •

- •

Figure 2 shows the impact of the a priori unspecified parameter in Problem 3.2 on the penalisation error. We first remark that, if could be chosen to be the optimal control of the discretised problem, the penalisation error in Problem 3.2 would be identical to zero by construction. Now, clearly, the optimal control is unknown, and generally a function of the state variable and time, and, therefore, a constant value generally gives a non-zero (in fact, negative) penalisation error, which we know to converge to zero of first order in . This is the underlying convergence mechanism of the proposed method and does not require a cunning choice of . Figure 2 does show, however, that the penalisation error for fixed can be reduced by diligent choice of . It is thereby sufficient to choose of the same order of magnitude as the optimal control. One can thus take advantage of a priori knowledge of the approximate control size. If such an estimate is not available, one might first determine a rough approximation by producing a crude version of Figure 2 on a coarse mesh – coarse in parameter space as well as time and state space – which is computationally cheap, and pick accordingly. We do not take advantage of this information in the following computations, and, throughout, we use , which appears to be the worst-case choice. We also tested the impact of on the Newton method, and found the required number of iterations virtually unaffected in all settings.

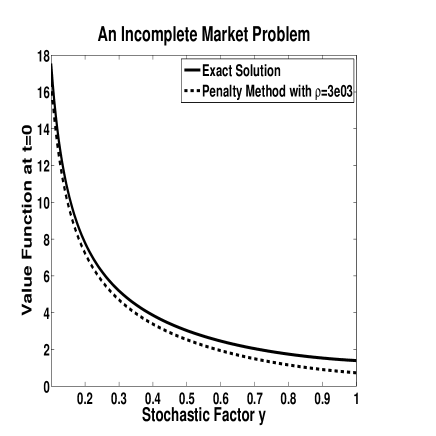

We use the numerical solution of the linear parabolic PDE (8.3) as a reference solution for the incomplete market problem. For and , measured in the maximum norm, the difference between the numerical solution of (8.3) and the penalty approximation (3.2) is 2e-03, and the difference between the penalty approximation (3.2) and the policy iteration solution of (2.3) is 2e-04.

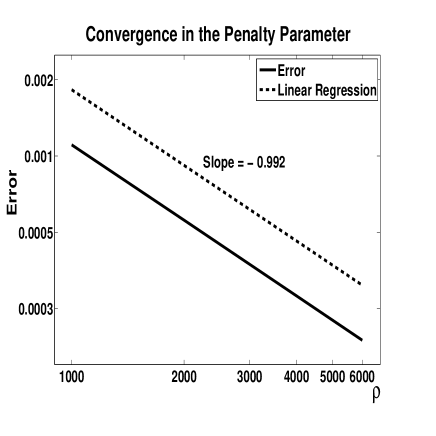

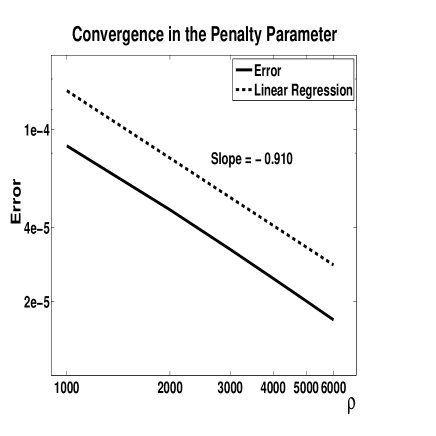

In Figure 3, we see the penalty approximation for . Given that the penalty parameter is still relatively small, the penalty approximation is still below the reference solution, but, clearly, the curves are similarly shaped already. In Figure 4, we measure rate of the convergence in ; more precisely, for different sizes of , starting out with the value of the reference solution (i.e. the value at the penultimate time step), we compute a time zero value using the penalty scheme (thus solving exactly one discrete LCP) and compare it to the time zero value of the reference solution. As expected, based on Theorem 3.7, the convergence in is of first order. In Table 1, we see the number of iterations needed by Algorithm 4.4 and policy iteration, averaged over all time steps; for the two schemes, the numbers are almost identical, and – in both cases – we never need more than two iterations to reach the desired accuracy . Finally, in Table 2, we see the computation times for the two schemes, which, as is to be expected based on the iteration numbers, are virtually the same.

| Policy Iteration | ||

|---|---|---|

| , | 6 | 94 |

| , | 11 | 89 |

| , | 53 | 47 |

| , | - | 100 |

| Penalty Method | ||

| , | 8 | 92 |

| , | 13 | 87 |

| , | 49.5 | 50.5 |

| , | - | 100 |

| Penalty Method | ||

| , | 6 | 94 |

| , | 11 | 89 |

| , | 55 | 45 |

| , | - | 100 |

| Grid Size | Policy | Penalty | Penalty |

|---|---|---|---|

| , | 1.08 | 1.08 | 1.09 |

| , | 35.07 | 34.76 | 35.16 |

| , | 2.74 | 2.82 | 2.76 |

| , | 10.89 | 10.88 | 10.91 |

8.2. Example: Early Exercise Options in an Incomplete Market

In this section, we value an early exercise contract in an incomplete market, in which the incompleteness stems from the fact that the asset on which the early exercise contracts are written is not traded; the example in its entirety is taken from [31], and we use it to demonstrate that the arising non-linear equations can be solved by a fully implicit finite difference scheme when using the results of Section 5.

Let , be bounded and globally Lipschitz functions. Let be some finite time horizon. Let , and , . Suppose we have a traded asset price process and a non-traded asset price process solving, respectively,

where , , are two Brownian motions defined on a probability space with a correlation coefficient . Additionally, we assume the existence of a riskless bond with interest rate .

Similar to the previous example, we consider an investor who can invest in the traded asset and in the bond. We suppose that the investor has initial wealth and that he may rebalance his portfolio at any time ; here, and denote the amounts invested, respectively, in the bond and in the stock. The investor’s wealth process solves

We take the investor’s utility function to be of exponential type and given by

with risk aversion parameter . Now, we suppose the investor holds an early exercise contract with payoff , , on the non-traded asset, and we would like to find the indifference price (cf. [31]) of the instrument; we cite the following result.

Proposition 8.4.

The buyer’s early exercise indifference price , where , is the unique bounded viscosity solution to

| (8.6) |

where and

Proof.

It can easily be shown that , and, if we assume to be bounded, (8.6) can be rewritten as

| (8.7) |

where is a suitably chosen compact set and, for , we define

Hence, to compute the early exercise indifference price of the considered option, we have to solve (8.7), which has the same structure as (1.2).

8.2.1. Choosing Model Parameters and Functions

We set , , and . Furthermore, we introduce and , and, for , we use

In particular, the choice of means that we are dealing with an American put with strike one.

8.2.2. Discretisation of the Continuous Equations and Solution of the Discrete Systems

Numerically, we solve (8.6) and (8.7) similarly to Section 8.1.2, i.e. we proceed backwards in time, starting at expiry , on a grid , where and . In space, we again apply a finite difference discretisation guaranteeing for the discretisation matrices to be in . Since we are dealing with a put option, we use and as boundary conditions, and we take the set in (8.7) to be . We compare the following three numerical approaches in Matlab.

-

•

For (8.6), we use an explicit time stepping scheme, meaning all non-linearities can be dealt with easily.

- •

As already in Section 8.1.3, we employ Remark 7.1 and approximate by . When solving the penalised equation (5.1) by Algorithm 6.5, we use a test for accuracy of the kind (8.5), setting 1e-08 as before. Similarly, we use a test for accuracy of the kind (8.4) with the same tolerance when solving an equation of the form (2.4) by policy iteration.

Remark 8.5.

As already in Remark 8.3, convergence of the fully implicit discretisation of (8.7) to the unique viscosity solution can be guaranteed by noting that we have stability, monotonicity, and consistency of the discretisation, and by using a strong comparison principle (cf. [3]). The fully explicit discretisation of (8.6) converges similarly provided we have stability.

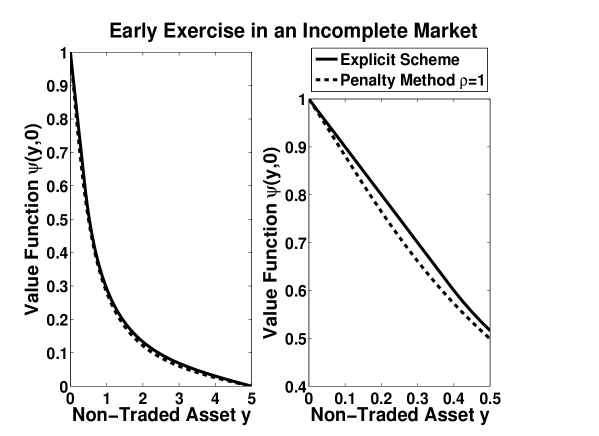

In our numerical tests, we find the explicit scheme to require a relatively large number of time steps for stability, making it difficult to use. In Table 3, fixing 1e06, we see the difference between the explicit scheme and the penalty approximation for different grid sizes; for the explicit scheme, for a given space discretisation, we always choose the number of time steps such that the solution plot does not show any instabilities, whereas for the penalty scheme we take identical numbers of time and space steps. For and , the explicit and the penalty scheme differ by e-03 and e-04 in the -norm, respectively (cf. Table 3). We point out that the explicit scheme runs substantially longer due to the high number of time steps required for stability; picking the time and space steps proportional to each other for the fully implicit scheme is optimal experimentally because of the observed first order convergence in both time and space. In Figure 5, we see the penalty approximation for and the explicit solution; even though the penalty parameter is very small, the two graphs are extremely close. The difference in the -norm between the policy iteration and penalty approximation solutions is e-05 and e-05 for grid sizes and , respectively. In Table 4, for different grid sizes and penalty parameters, we see the maximum and the average number of iterations needed by Algorithms 6.5 (penalty approximation) and B.1 (policy iteration) for solving the discrete systems at every time step, as well as the corresponding runtimes for the full schemes. (In case of Algorithm B.1, we count one iteration whenever line (B.2) is executed.) Throughout, the average numbers of iterations are small, and both schemes run very fast, with the penalty scheme being faster by about a factor two; the effect appears to be due to the fact that – whilst the average number of iterations is small – policy iteration requires a large number of iterations in a few instances (as seen by the in Table 4); we will investigate this effect more closely below. Finally, in Figure 4, we measure the rate of convergence in , and confirm first order convergence as predicted by Theorem 5.6; the implementation is precisely as in Section 8.1, except that we use a penalty approximation as reference solution; as before, the error is measured in the -norm.

| Explicit Scheme | Time | Penalty | Time | Difference |

|---|---|---|---|---|

| , | 0.78s | , | 0.23s | 1.3e-03 |

| , | 16.49s | , | 3.71s | 3.5e-04 |

| Policy Iteration | Max Iterations | Iterations | Runtime |

|---|---|---|---|

| , | 4 | 2.20 | 0.38s |

| , | 11 | 2.17 | 6.42s |

| , | 4 | 1.83 | 0.86s |

| , | 18 | 2.88 | 2.12s |

| Penalty Method | Max Iterations | Iterations | Runtime |

| , | 3 | 1.98 | 0.25s |

| , | 3 | 1.21 | 4.09s |

| , | 3 | 1.15 | 0.66s |

| , | 4 | 2.16 | 1.47s |

| Penalty Method | Max Iterations | Iterations | Runtime |

| , | 2 | 1.10 | 0.17s |

| , | 3 | 1.08 | 3.82s |

| , | 2 | 1.02 | 0.61s |

| , | 4 | 1.38 | 1.13s |

8.2.3. Sensitivity with Respect to the Initial Guess

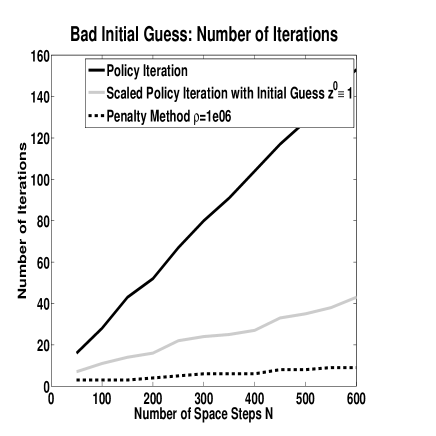

We have seen above that, unlike penalty approximation, policy iteration requires many iterations in a few instances and that this effect appears to correlate with the grid size (cf. Table 4). To investigate if the phenomenon relates to the quality of the initial guess for the non-linear iterations, we set and consider different grids sizes ; the results can be seen in Figure 7. (Since, in our implementations, we use the solution from the previous time step as initial guess for the next, setting can be interpreted as solving a single non-linear discrete system with a poor initial guess.) Clearly, the number of Newton iterations for the penalised system is almost unaffected by the increase of , whereas the number of iterations of the policy iterations grows linearly in . (In [30], it has already been observed that even for a simple American option problem, the best obtainable bound on the number of iterations of policy iteration is linear, i.e. .)

Now, it is easy to see that equation (B.1) is scalable, i.e., for any , it can equivalently be rewritten as

and it has been pointed out in [15, 17, 16] that a different choice of will generally lead to different policy iterations; more precisely, in our context, depending on the choice of , we obtain different adaptations of Algorithm B.1, all converging to the same solution. For theoretical considerations on the best choice of , we refer to [17]; numerically, we find the following.

-

•

Simply introducing a scaling factor does not yield an improvement.

-

•

Changing the initial guess from the payoff to does not yield an improvement.

-

•

Using a scaling factor e06, combined with initial guess , significantly reduces the number of iterations needed (cf. Figure 7).

Further analysis shows that a large scaling factor yields an improvement whenever the initial guess is such that , which is necessary for the multiplication by the scaling factor to have an effect.

In summary, we can conclude that the penalty approximation appears to have a generic advantage when dealing with poor starting values, whereas – to obtain equally good results by policy iteration – prudent implementation is inevitable. The main reason for the different performance of policy iteration seems to be that it does show Newton-type behaviour, i.e. it does not converge to the solution in steps with rapidly decreasing size; in particular, when using the payoff as initial guess, it shifts the solution upwards node by node until the free boundary is found, resulting in the linear dependence on observed in Figure 7.

9. Conclusion

In this paper, we consider the numerical solution of continuously controlled HJB equations and HJB obstacle problems – which trivially includes finitely controlled equations – and we show that penalisation is a powerful means for solving the non-linear discrete problems resulting from implicit finite difference discretisations. Generally, this can be done by policy iteration or – as we show – by penalisation combined with a Newton-type iteration. For both penalty approaches, we show that the achieved accuracy is , where is the penalty parameter. We include numerical examples from (early exercise) incomplete market pricing, demonstrating the competitiveness of our algorithms as fast and easy-to-use numerical schemes. An interesting open problem is the extension of our approach to more general Isaacs equations.

Appendix A Policy Iteration for the HJB Equation

We briefly recap the policy iteration algorithm for HJB equations as introduced in [12] and [30]. Recall that we want to solve Problem 2.2, i.e. we are trying to find such that

| (A.1) |

Algorithm A.1.

(Policy Iteration for HJB Eq.) For and , define to be such that

and set and to be matrix and vector consisting of rows and , , respectively. Let be some starting value. Then, for known , , find such that

| (A.2) |

Theorem A.2.

Appendix B Policy Iteration for the HJB Obstacle Problem

We briefly recap the method of policy iteration algorithm for HJB obstacle problems that was introduced in [30]. Recall that we want to solve Problem 2.3, i.e. we are trying to find such that

| (B.1) |

Now, for , we define and , and we define and correspondingly. Using these new definitions, (B.1) is equivalent to

Algorithm B.1.

(Policy Iteration for HJB Obstacle Prob.) For and , define such that

Let be some starting value. Then, for known , , find such that

| (B.2) |

Theorem B.2.

Proof.

See [30]. ∎

References

- [1] G. Barles. Convergence of numerical schemes for degenerate parabolic equations arising in finance. In L. C. Rogers and D. Talay, editors, Numerical Methods in Finance, pages 1–21. Cambridge: Cambridge University Press, 1997.

- [2] G. Barles and E. R. Jakobsen. On the convergence rate of approximation schemes for Hamilton-Jacobi-Bellman equations. Mathematical Modelling and Numerical Analysis, 36(1):33–54, 2002.

- [3] G. Barles and E. R. Jakobsen. Error bounds for monotone approximation schemes for parabolic Hamilton-Jacobi-Bellman equations. Mathematics of Computation, 76(260):1861–1893, 2007.

- [4] R. Carmona, editor. Indifference pricing: theory and applications. Princeton, N.J., Oxford: Princeton University Press, 2009.

- [5] Z. Chen and P. A. Forsyth. A semi-Lagrangian approach for natural gas storage valuation and optimal operation. SIAM Journal on Scientific Computing, 30(1):339–368, 2007.

- [6] F. H. Clarke. Optimization and nonsmooth analysis. Philadelphia: SIAM, 1990.

- [7] M. Thompson, M. Davison and H. Rasmussen. Natural gas storage valuation and optimization: A real options application. Naval Research Logistics, 56(3):226–238, 2009.

- [8] P. Wilmott, J. Dewynne and S. Howison. Option pricing: mathematical models and computation. Oxford: Oxford Financial Press, 1993.

- [9] C. M. Elliott and J. R. Ockendon. Weak and variational methods for moving boundary problems. Boston: Pitman Advanced Publishing Program, 1982.

- [10] M. Fiedler. Special matrices and their applications in numerical mathematics. Lancaster: Nijhoff, 1986.

- [11] W. H. Fleming and H. M. Soner. Controlled Markov processes and viscosity solutions. New York: Springer, 2nd edition, 2005.

- [12] P. A. Forsyth and G. Labahn. Numerical methods for controlled Hamilton-Jacobi-Bellman PDEs in finance. The Journal of Computational Finance, 11(2):1–44, 2007.

- [13] P. A. Forsyth and K. R. Vetzal. Quadratic convergence for valuing American options using a penalty method. SIAM Journal on Scientific Computing, 23(6):2095–2122, 2002.

- [14] P. A. Forsyth and K. R. Vetzal. Numerical methods for nonlinear PDEs in finance. Working paper, University of Waterloo, http://www.cs.uwaterloo.ca/paforsyt/entry.pdf, 2010.

- [15] Y. Huang, P. A. Forsyth and G. Labahn. Combined fixed point iteration for HJB equations in finance. Working paper, University of Waterloo, https://www.cs.uwaterloo.ca/paforsyt/hjbcombined.pdf, 2010.

- [16] Y. Huang, P. A. Forsyth and G. Labahn. Inexact arithmetic considerations for direct control and penalty methods: American options under jump diffusion. Working paper, University of Waterloo, https://www.cs.uwaterloo.ca/paforsyt/inexact.pdf, 2011.

- [17] Y. Huang, P. A. Forsyth and G. Labahn. Methods for pricing American options under regime switching. Working paper, University of Waterloo, https://www.cs.uwaterloo.ca/paforsyt/regimeamerican.pdf, 2011.

- [18] R. Isaacs. Differential games. A mathematical theory with applications to warfare and pursuit, control and optimization. New York: John Wiley and Sons, 1965.

- [19] M. G. Crandall, H. Ishii and P.-L. Lions. User’s guide to viscosity solutions of second order partial differential equations. Bulletin of the American Mathematical Society, 27(1):1–67, 1992.

- [20] K. Ito and K. Kunisch. Semi-smooth Newton methods for variational inequalities of the first kind. Mathematical Modelling and Numerical Analysis, 37(1):41–62, 2003.

- [21] K. Ito and K. Kunisch. On a semi-smooth Newton method and its globalization. Mathematical Programming, 118(2):347–370, 2007.

- [22] M. Hintermüller, K. Ito and K. Kunisch. The primal-dual active set strategy as a semismooth newton method. SIAM Journal on Optimization, 13(3):865–888, 2002.

- [23] E. R. Jakobsen. On the rate of convergence of approximation schemes for Bellman equations associated with optimal stopping time problems. Mathematical Models and Methods in Applied Sciences, 13(5):613–644, 2003.

- [24] I. Karatzas and S. E. Shreve. Methods of mathematical finance. New York: Springer, 1998.

- [25] E. R. Jakobsen, K. H. Karlsen and C. La Chioma. Error estimates for approximate solutions to Bellman equations associated with controlled jump-diffusions. Numerische Mathematik, 110(2):221–255, 2008.

- [26] N. V. Krylov. The rate of convergence of finite-difference approximations for Bellman equations with Lipschitz coefficients. Applied Mathematics and Optimization, 52(3):365–399, 2005.

- [27] N.V. Krylov. On the rate of convergence of finite-difference approximations for Bellman’s equations with variable coefficients. Probability Theory and Related Fields, 117(1):1–16, 2000.

- [28] H. J. Kushner. Numerical methods for stochastic control problems in continuous time. SIAM Journal on Control and Optimization, 28(5):99–1048, 1990.

- [29] H. J. Kushner and P. G. Dupuis. Numerical methods for stochastic control problems in continuous time. New York: Springer, 2nd edition, 2001.

- [30] O. Bokanowski, S. Maroso and H. Zidani. Some convergence results for Howard’s algorithm. SIAM Journal on Numerical Analysis, 47(4):3001–3026, 2009.

- [31] A. Oberman and T. Zariphopoulou. Pricing early exercise contracts in incomplete markets. Computational Management Science, 1(1):75–107, 2003.

- [32] J.-S. Pang. Newton’s method for B-differentiable equations. Mathematics of Operations Research, 15(2):311–341, 1990.

- [33] H. Pham. Continuous-time stochastic control and optimization with financial applications. London: Springer, 2009.

- [34] L. Qi and J. Sun. A nonsmooth version of Newton’s method. Mathematical Programming, 58:353–367, 1993.

- [35] R. Seydel. Tools for computational finance. Universitext. Berlin: Springer, 3rd edition, 2006.

- [36] S. Shreve. Stochastic calculus for finance II: continous-time models. New York: Springer, 2008.

- [37] Q. S. Song. Convergence of Markov chain approximation on generalized HJB equation and its applications. Automatica, 44(3):761–766, 2008.

- [38] J. C. Strikwerda. Finite difference schemes and partial differential equations. Philadelphia: Society for Industrial and Applied Mathematics, 2nd edition, 2004.

- [39] J. Wang and P. Forsyth. Maximal use of central differencing for Hamilton-Jacobi-Bellman PDEs in finance. SIAM Journal on Numerical Analysis, 46(3):1580–1601, 2009.

- [40] J. H. Witte and C. Reisinger. A penalty method for the numerical solution of Hamilton-Jacobi-Bellman (HJB) equations in finance. SIAM Journal on Numerical Analysis, 49(1):213–231, 2011.

- [41] J. Yong and X. Y. Zhou. Stochastic controls: Hamiltonian systems and HJB equations. New York, London: Springer, 1999.

- [42] T. Zariphopoulou. A solution approach to valuation with unhedgeable risks. Finance and Stochastics, 5(1):61–82, 2001.