Smile dynamics – a theory of the implied leverage effect: ERRATUM

We discovered a very unfortunate mistake in our paper “Smile dynamics – a theory of the implied leverage effect” Paper , where the predictions for the change of implied volatility for a fixed strike and for a fixed moneyness got mixed up. When the return of the underlying is , the theory predicts that the at-the-money (ATM) implied volatility for fixed moneyness should evolve as:

| (1) |

where is the leverage correlation function of returns . This expression should be compared to the original expression in Paper :

| (2) |

which instead holds for the implied volatility of a fixed strike option with a moneyness close to zero.

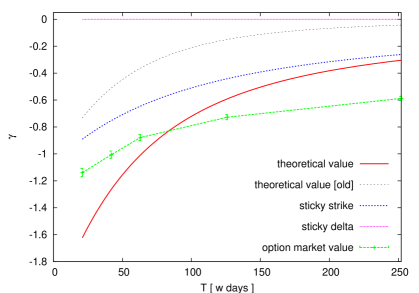

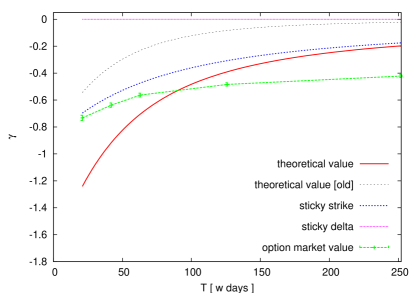

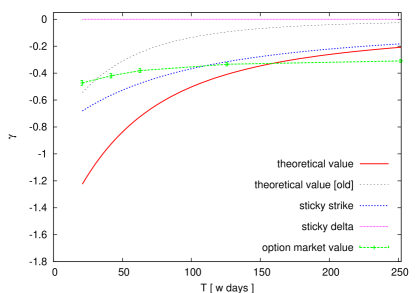

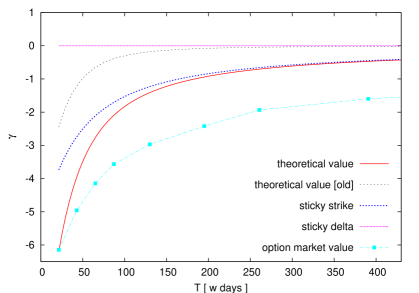

The correct comparison with empirical data on the OEX index, large cap, mid cap and small cap stocks, is given in Figs. 1-4, where we show the implied leverage coefficient as a function of maturity. The implied data is obtained by regressing the relative daily change of ATM implied vols on the corresponding stock or index return, for each maturity. The result is then averaged over all stocks within a given tranche of market capitalisation. The three curves correspond to (a) the correct theoretical prediction computed using the historically determined leverage correlation ; (b) the original theoretical prediction; (c) the “sticky strike” procedure. We also show the line corresponding to “sticky delta”.

We see that for the OEX index, the implied volatility overreacts to changes of prices compared to the prediction calibrated on the historical leverage effect, except for the shortest maturities where the prediction is right on the empirical value. For single stocks, small maturity options tend to underreact, whereas longer maturities tend to overreact. As mentionned in Paper , the empirical curves for the OEX and for large caps appear to be well fitted by a sticky-strike prediction, but with amplitude of the leverage correlation substantially larger than its historical value. This would be compatible with the fact that market makers use a simple sticky strike procedure, but with a smile that is significantly more skewed than justified by historical data, or else that the a local volatility model is used, since this leads to a factor 2 amplification of the sticky-strike prediction Bergomi .

The other results of the paper, in particular the empirical work, is unaffected by the above blunder. We thank V. Vargas and L. De Leo for discussions.

References

- (1) S. Ciliberti, J.P. Bouchaud, M. Potters, Smile dynamics – a theory of the implied leverage effect, Wilmott Journal Volume 1, Issue 2, pages 87-94, April 2009

- (2) see e.g. L. Bergomi, Smile Dynamics IV, Risk Magazine, December 2009.