Random walks at random times: Convergence to iterated Lévy motion, fractional stable motions, and other self-similar processes

Abstract

For a random walk defined for a doubly infinite sequence of times, we let the time parameter itself be an integer-valued process, and call the orginal process a random walk at random time. We find the scaling limit which generalizes the so-called iterated Brownian motion.

Khoshnevisan and Lewis [Ann. Appl. Probab. 9 (1999) 629–667] suggested “the existence of a form of measure-theoretic duality” between iterated Brownian motion and a Brownian motion in random scenery. We show that a random walk at random time can be considered a random walk in “alternating” scenery, thus hinting at a mechanism behind this duality.

Following Cohen and Samorodnitsky [Ann. Appl. Probab. 16 (2006) 1432–1461], we also consider alternating random reward schema associated to random walks at random times. Whereas random reward schema scale to local time fractional stable motions, we show that the alternating random reward schema scale to indicator fractional stable motions.

Finally, we show that one may recursively “subordinate” random time processes to get new local time and indicator fractional stable motions and new stable processes in random scenery or at random times. When , the fractional stable motions given by the recursion are fractional Brownian motions with dyadic . Also, we see that “un-subordinating” via a time-change allows one to, in some sense, extract Brownian motion from fractional Brownian motions with .

doi:

10.1214/12-AOP770keywords:

[class=AMS]keywords:

abstractwidth280pt

and

t1Research started while at Sogang University and supported by Sogang University research Grant 200910039.

t2Supported by the Priority Research Centers Program through the National Research Foundation of Korea (NRF) funded by the Ministry of Education, Science and Technology (Grant #2009-0094070) and from Australian Research Council Grant DP0988483.

1 Introduction

Let , be three independent Brownian motions, and let a two-sided Brownian motion be defined by

| (1) |

In burdzy1992some , Burdzy studied the process which he called an iterated Brownian motion (IBM). It can be thought of as a two-sided Brownian motion which is nonmonotonically “subordinated” to another Brownian motion. This process was also used by Deheuvels and Mason deheuvels1992functional to study the Bahadur–Kiefer process. Also, a variant of IBM, where the pure imaginary process was substituted for , was utilized by Funaki funaki1979probabilistic to study the PDE

| (2) |

Recently, more general processes at random times called -time Brownian motions and -time fractional Brownian motions were introduced in nane2006laws , nane2011local . In these works (along with several references therein), the connection between processes at random times and various PDEs was studied, along with the local time and path properties of the iterated processes. In a different direction, the scaling and asymptotic density of a discretized version of IBM called iterated random walk was analyzed in the physics literature turban2004iterated .

In this work, we consider generalizations of the iterated random walk which we call random walks at random times (RWRT) and dependent walks at random times (DWRT) and relate them with a different portion of the probability literature concerning random walks in random scenery. This relation was first noted by Khoshnevisan and Lewis khoshnevisan1996iterated who stated that there was “a surprising connection between the variations (of IBM) and H. Kesten and F. Spitzer’s Brownian motion in random scenery.” Later, in khoshnevisan1999stochastic , a form of measure-theoretic duality was shown between the two processes. Here, we present a mechanism on the discrete level which shows a connection between the two processes.

We show that under suitable conditions, the scaling limits of RWRT and DWRT are (-sssi)-time -stable Lévy motions, a new class of processes at random times. If is a two-sided -stable Lévy motion defined similarly to (1), and is an independent -stable Lévy motion, then we call an iterated Lévy motion. If, more generally, is an independent -self-similar, stationary-increment process (sssi), then an (-sssi)-time -stable Lévy motion is given by . Assuming , we will see that is an -sssi process with Hurst exponent less than . They naturally complement stable processes in random scenery which are the limiting continuous processes of KS and Wang03 and which have Hurst exponents greater than (Wang Wang03 considered only the case , but this was extended to by Cohen and Dombry CD ).

Random walks in random scenery (RWRS) and their scaling limits, stable processes in random scenery, were first introduced independently in KS , Borodin . The purpose of KS was to introduce a new class of sssi processes given by the scaling limits of RWRS. The scaling limits have integral representations as stable integrals of local time kernels (of a process ). When the random scenery are -stable laws, they scale to the -stable random measure against which the local time kernel is integrated. In comparison, there is also an integral representation of (-sssi)-time -stable Lévy motions given by the stable integration of random kernels of type against -stable random measures.

When is a generic -sssi process, the stable processes in random scenery discussed above also include the model of Wang03 . Wang used “dependent walks” to collect the scenery, instead of random walks, leading to a dependent walk in random scenery (DWRS). In particular, the dependent walks he used were discrete-time Gaussian processes known to scale to fractional Brownian motion (fBm).

Random reward schema are sums of independent copies of discrete processes in random scenery. In CS , DG , CD it was shown that the random reward schema of RWRS and DWRS scale to -sssi symmetric -stable (SS) processes called local time fractional SS motions (with ). In this work, we show that the scaling limits of random reward schema for RWRT and DWRT are -sssi SS processes called indicator fractional SS motions (with ) which were introduced in jung2010indicator .

Note that fBm is the only sssi Gaussian process. Thus, when the scenery has finite variance and , local time fractional SS motions and indicator fractional SS motions reduce to fBm with and , respectively.

As will be seen in Section 2, the mechanism behind the connection between local time and indicator fractional stable motions is the same as the mechanism which connects Brownian motion in random scenery (BMRS) with IBM. In effect, the mechanism shows that the indicator kernels of the latter processes can be thought of as “alternating” versions of the local time kernels of the former.

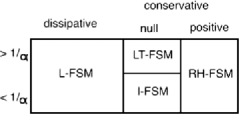

Together, local time fractional SS motions and indicator fractional stable motions form a class of fractional stable motions (-sssi SS processes) which may be thought of as one of several generalizations of fractional Brownian motion. Their increment processes are stationary and have the ergodic-theoretic property of being null conservative, a concept introduced in samorodnitsky2005null . This property distinguishes them from fractional stable motions which have dissipative or positive conservative increment processes. The most well-known examples of fractional stable motions with dissipative or positive conservative increment processes are the linear fractional stable motions and the real harmonizable stable motions, respectively, as can be seen in Figure 1.

We also consider single-scenery random reward schema introduced in dombry14functional . Here we again take sums of identically distributed RWRTs or DWRTs. However, the copies have a dependence structure since they use the same “single scenery.” This dependence will be made more explicit below. The scaling limits of single-scenery random reward schema of RWRS and DWRS no longer have stationary increments; however, they are easily seen to be -ss SS processes with . Similarly, the scaling limits of single-scenery random reward schema of RWRT and DWRT are -ss SS processes with .

Finally, we also present a recursive construction of some local time and indicator fractional stable motions. In particular, we show that at each step of the recursion, the local times exist and are in . The recursively defined processes give the first examples of local time fractional stable motions for which the processes collecting the scenery are neither fBm nor -stable Lévy motions. In the case , the processes are given by integrals against Gaussian random measures, and the recursion constructs fBm, of any dyadic Hurst parameter, using one Brownian motion and a countable family of independent random Gaussian measures.

As mentioned above, RWRT and, in particular, its scaling limit are in some sense nonmonotonically subordinated processes. Usually one may not undo a subordination—for example, one can embed a stable process in Brownian motion, but cannot extract Brownian motion from the stable process since the filtration is strictly smaller. However, we will see that when the scaling limit of the random time process, , is fBm, one can undo the subordination using the time-change . Extending such a time-change procedure to the kernels of indicator fractional stable motions when , we find that one can, in some sense, extract Brownian motion from fractional Brownian motions satisfying .

The rest of the paper is arranged as follows. In Section 2 we describe RWRTs and RWRSs. We also describe their respective random reward schema and scaling limits. The section ends with a statement describing new scaling limit results. The proofs of the scaling weak convergence results are given in Section 3. In Section 4, we describe the recursive construction mentioned above, and complete the nontrivial task of showing that the recursion produces processes that are well defined. The main component of this task is showing that the local times exist and are in . Finally, in Section 5 we explain how to extract Brownian motion from fBm with any Hurst parameter satisfying .

2 Discrete and continuous models

2.1 Random walks at random times and alternating random reward schema

We start with a simple description of RWRS. Let be a set of i.i.d. symmetric random variables in the domain of attraction of an SS law, with scale parameter . The family depicts the scenery associated to the vertices of . Let

| (3) |

be a symmetric random walk on with steps in the domain of attraction of an SS law, . The random walk roams amidst the scenery which are independent from the steps .

The cumulative scenery process

| (4) |

is called a random walk in random scenery. The scenery can alternatively be thought of as random reward collected by the random walk when it visits vertex .

We note that some authors call the pair a RWRS process (e.g., den2006random ). Since most of the papers cited in this work refer to (4) as the RWRS, we stick with this notation.

Wang Wang03 considered a slight modification of RWRS by using a discrete approximation of a Gaussian process instead of a random walk:

| (5) |

Here is the ceiling function, and is the partial sum of a stationary Gaussian process with correlations satisfying

| (6) |

where . In addition to (5), there have been myriad generalizations of (4), and we refer the reader to the introduction of guillotinlimit for a nice summary of such generalizations.

We refer to (5) as a dependent walk in random scenery (DWRS). In general, we consider for which the collecting process has stationary increments and also satisfies the following scaling limit properties:

| (SLP) |

where is equipped with the usual Skorohod topology (also called the -topology).

The condition that be sssi guarantees that scales to an sssi process as well, and this was in fact the original motivation of introducing in KS . Note that we use the stable parameter for the scenery/reward and consequently the increments of the RWRS/DWRS; however, we reserve the stable parameter for the increments of the collecting process (note that we require in order to guarantee ).

We introduce a variant of in which the reward alternate in sign and are associated with edges instead of vertices. In our variant of RWRS, we use symmetric reward together with signs , associated to the edge set of . At time zero, all signs are plus one, ; however, is a process determined by the collecting process in a manner discussed below.

Consider a discrete collecting process satisfying condition (SLP). Note that our definition allows to be greater than one. Let be the set of connected edges traversed on the th step of , that is, the set of edges between and [thus has cardinality ]. At the th step, the process :

-

•

earns the signed reward of all edges and then

-

•

reverses the sign of each so that it will receive the exact opposite reward the next time it traverses .

A (dependent) random walk at random time (DWRT/RWRT) with a nonmonotonic subordinating random time process is a process

| (7) |

where is the sign of at time .

To explain the name of the process, consider that in an RWRT, due to cancellation, each reward contributes either one or zero net terms to the sum (7). When is to the right of the origin, the number of net terms is one if and only if is to the right of , and when is to the left of the origin, the number of net terms is one if and only if is to the left of . It follows that

| (8) |

where means that lies between and regardless of the sign of . The partial sum of reward is just a random walk . If we let and extend the random walk to negative times in the natural way, then thinking of time being determined by the location of , we have

| (9) |

As an aside, if we take (8) as our initial definition rather than (7), then the reward may equally well be placed on the vertices instead of the edges. The reader may therefore choose to visualize this process in any of several ways according to his or her own aesthetic preference.

The relationship between and should be clear. In particular, when the collecting process is a simple random walk , a relation is made by using a bijection which assigns to each vertex either the edge lying to its left whenever the previous step of was in the positive direction (right), or the edge lying to its right whenever the previous step of was in the negative direction (left). To extend the relation to other random walks, one must use a modified version of which, when going from to on the th step, collects a reward not only from , but all vertices between and . In view of this relationship between and , if is the measure for the random scenery, and is the measure for , then the processes and can be defined on the same product space with measure .

There is a further relationship between and the variations of which mirrors the connection between BMRS and the variations of IBM as presented in khoshnevisan1999stochastic . In order to explain this relationship, it will be convenient to let the collecting walk be a simple random walk and to have the reward for both and be attached to the edges of , rather than to the vertices. For , let the th variation of be defined as

| (10) |

Theorem 2.1.

Suppose the i.i.d. reward are symmetric and have finite th moments. If is odd, then is another RWRT, while if is even, then is a RWRS. In both cases, the reward collected by the processes are given by where

For we let denote the edge between and . We then have

| (11) |

Note that

| (12) |

If is even, then the sign in (12) is irrelevant. Therefore,

| (13) |

Comparing with (11) shows this to be a RWRS with reward given by .

On the other hand, if is odd, then the sign in (12) causes the same cancellation as we have with RWRT, and since is symmetric, there is no longer a need to subtract the expectation. Thus, (12) yields

| (14) |

Comparing again with (11) shows this to be a RWRT with reward given by .

We now compare this with the results of khoshnevisan1999stochastic . Let denote an IBM, fix an interval , and let

| (15) |

where is an induced random partition of the interval ; see khoshnevisan1999stochastic , Section 1, for details. Among other things, Khoshnevisan and Lewis showed that, when properly renormalized, converges in distribution to IBM when is odd and BMRS when is even; see Theorems 3.2, 4.4, 4.5 and the discussion in the middle of page 631. If we consider the natural association between BMRS and RWRS on the one hand and between IBM and RWRT on the other, we see that the simple Theorem 2.1 provides an intuitive backdrop for the much more difficult results concerning the continuous case in khoshnevisan1999stochastic .

We now return to study of in the general case. We will need processes extended to noninteger times, and we will therefore denote the linear interpolation of as

| (16) |

Let us now describe the two different random reward schema we will use. Let us start with an alternating version of the random reward schema introduced in CS . Let be independent copies of which are also independent from independent copies of the reward . If is a sequence of integers such that , then

| (17) |

is an alternating random reward scheme.

If we instead follow the single-scenery schema of dombry14functional and use the same single copy of reward for each copy of , then

| (18) |

is a single scenery alternating random reward scheme.

2.2 Scaling limits of random reward schema

In this section we state some known results concerning the scalings of RWRS and DWRS to stable integral representations. These will motivate our results concerning the scalings of RWRT and DWRT.

Let us first recall an important definition. Suppose is a -finite measure on a measurable space , and that

Definition 2.2.

A SS random measure with control measure is a -additive set function on such that for all : {longlist}[(2)]

;

and are independent whenever , where is an SS random variable.

In particular, if , then

| (19) |

Section 3.3 of samorodnitsky1994stable contains an introduction to this topic. The immediate importance to us is that the scaling limits of RWRS and DWRS are integrals with respect to stable random measures, where the integral kernel is the local time of a properly scaled collecting process (linearly interpolated) which is either or with . The process converges weakly to a scaling limit, denoted by , which is, respectively, fBm- in or a -stable Lévy motion in . Let be the probability space of . It is known that has a jointly continuous local time ; this was shown for -stable Lévy motions in boylan1964local and for fBm in berman1974 . Moreover, for all and all , satisfies

| (20) |

by Theorem 3.1 in CS and Lemma 2.1 in DG . Here we interpret as the increasing family of random functions which satisfy the occupation time formula

| (21) |

for any Borel set .

Let be an SS random measure with Lebesgue control measure which is independent from . Throughout this subsection we will let

| (22) |

A stable process in random scenery is an -sssi SS process given by

| (23) |

which is well defined by (20); see Chapter 3 of samorodnitsky1994stable . Recall that is in the domain of attraction of an SS law. It was shown in KS , Wang03 , CD that the following weak convergence holds in :

| (24) |

Henceforth we will use for the Hurst parameter of the collecting process and for the Hurst parameter of the resulting stable process in random scenery.

The Hurst exponent can be explained by using the local time scaling relation

| (25) |

In CS , weak convergence in was shown for a properly normalized random reward scheme

where is the linear interpolation of in the same manner as (16). The

are independent copies of mean zero, finite variance random walks which have explaining the exponent . They collect independent copies of i.i.d. reward which are also independent from the random walks. Cohen and Samorodnitsky called the limiting process an fBm- local time fractional stable motion. In CD , the discrete collecting process was generalized to and convergence to fBm- local time fractional stable motions for any was proved. In DG , a collecting process scaling to -stable Lévy motion () was used, and consequently, other local time fractional stable motions were obtained in the limit. Let us now explicitly state these collective results.

Recall that is the probability space of . Suppose is an SS random measure that has control measure , but lives on some other probability space . As above, is either or with . Letting be as in (22), in light of (20) we define a local time fractional stable motion as the process

| (26) |

Let be an integer sequence with , and let be independent copies of i.i.d. reward in the domain of attraction of an SS law. The following weak convergence holds in as :

| (27) |

Let be a stable random measure with Lebesgue control measure with the restriction that , and again let be as in (22). We may use (20) and Hölder’s inequality to define

| (28) |

Note that the scale parameter at time for (28) is

| (29) |

versus for (26). For , a convergence result (in finite-dimensional distributions) with respect to the single scenery case was given in Theorem 4.2 of dombry14functional :

| (30) |

As stated earlier, the process on the right-hand side is -ss, but using (29) one can see that this process does not in general have stationary increments.

It is convenient to write (26) and (28) as renormalized sums of (23) which appeal to the stable central limit theorem and the law of large numbers, respectively; see CD , DG , dombry14functional . The former renormalization is applied to the entire integral in (23), and the convergence is in whereas the latter renormalization applies only to the integral kernel

| (31) | |||||

| (32) |

2.3 Scaling limits of alternating random reward schema

We are now ready to state our results concerning the scaling limits of and its associated random reward schema (17) and (18).

Throughout this subsection we assume that the discrete collecting process is extended to continuous time by linear interpolation and that it has the scaling limit as given in condition (SLP). Independent copies of i.i.d. reward are, as usual, in the domain of attraction of an SS law (scale parameter ) and independent from the random walks. The space supports , and the SS random measures are as in the previous subsection. Define the processes

| (33) | |||||

| (34) | |||||

| (35) |

The above are all self-similar with common index , and (34) and (35) are SS processes. One can also observe (see Theorem 2.2 in jung2010indicator ) that both (33) and (34) have stationary increments. We call (33) an (-sssi)-time -stable Lévy motion or more generally a stable process at random time. If is a two-sided -stable Lévy motion, then we may also write (33) as . The process (34) is an indicator fractional stable motion as introduced in jung2010indicator . The process (35) is the alternating analog of the scaling limit of a single scenery random reward scheme introduced in dombry14functional .

Theorem 2.3.

Let , and let as .

-

•

The following convergence holds in f.d.d.:

(36) If the reward are symmetric with finite variance (), and converges weakly in (), then (36) also holds weakly in (, resp.).

-

•

If is uniformly integrable, then

-

•

If , then

(38)

The interest of the first convergence result [to (-sssi)-time -stable Lévy motion] lies in the fact that this seems to be the first such Donsker-type theorem for iterated processes where the random time process is not a subordinator, that is, not an increasing Lévy process. In the case where the random time process is a subordinator, similar convergence results are well known. In fact, in Section 2.2 of nane2011local , such results are extended to the case where the scenery have a certain dependence structure. Their Donsker-type theorem shows convergence to an -time fractional Brownian motion.

It is not hard to see that , and are all continuous in probability. However, by Theorem 10.3.1 in samorodnitsky1994stable , when , and are not sample continuous. In those cases, the best we can hope for is weak convergence in . We will see in the remark at the end of Section 3, that even this is a lot to ask. In that remark, it is argued that even in the simplest cases, is not even in . In particular, the weak convergence in and given in the first part of Theorem 2.3 depends heavily on the fact that . In this case, the scaling limit of is continuous since it is simply Brownian motion.

The condition that is uniformly integrable holds when is either or , . The former follows from a Gaussian concentration inequality which bounds in for all (see ledoux1991probability , page 60), and the latter follows from equation (5.s) in legall1991range and the bound .

3 Proof of Theorem 2.3

A convenient tool in proving convergence of the finite-dimensional distributions is a diagonal convergence theorem of dombrySWN . In order to state this theorem, we require some definitions.

As usual is in the domain of attraction of the SS law with scale parameter , and it is the reward on the edge between and . For fixed positive , define to be the random signed measure on which is a.s. absolutely continuous with respect to Lebesgue measure and whose random density is given by

| (39) |

For a locally integrable function , define

| (40) |

For , we will say that converges to in if the following two conditions hold:

-

•

for any compact , converges to in ;

-

•

there is some such that and as .

Let if and if . The following diagonal convergence is shown in Proposition 3.1 of dombrySWN ; see also Proposition 3.1 of dombry14functional .

Proposition 3.1 ((Dombry)).

Suppose is an -stable random measure, and converges to in . If as , then the random variables converge weakly as and in particular,

| (41) |

We now start by showing convergence in f.d.d. for Theorem 2.3. However, to reduce notation and simplify the presentation, we only prove convergence of the one-dimensional distributions for some fixed . The extension to f.d.d. in all three cases follows easily using the Cramér–Wold device; see, e.g., Theorem 3.9.5 in durrett2010probability .

Also without loss of generality we use instead of the linear interpolation since they differ by at most which goes a.s. to as .

Convergence in f.d.d. for (36)

Fix . Let . According to assumption (SLP), . By Skorohod’s representation theorem, there is a common probability space on which , live and such that for all (note that the bar includes the dependence on ).

Fix an and recall that and that for , we let . We have

| (42) | |||

By Proposition 3.1 and the fact that in , we have that the one-dimensional distributions of converge to those of .

Convergence in f.d.d. for (38)

For multiple independent walkers in the same scenery, we follow the arguments of Proposition 2.4 in dombry14functional . Fix . As in the proof of (36), using Skorohod’s representation theorem and Proposition 3.1, we have for ,

where for each and for all (the bar includes the dependence on ).

We need only show the following converges in probability to zero as :

| (43) |

where for fixed , the random variables are i.i.d. Also, for each fixed , converges a.s. to . We first show that as ,

| (44) | |||

Consider a triangular array such that for each fixed , there are i.i.d. random variables

in each row, and for each fixed , the column of random variables converges weakly to zero. For such triangular arrays, the following weak law holds (see Proposition 2.4 in dombry14functional ):

| (45) |

thus proving (3).

Since , the strong law of large numbers for Banach space valued random variables implies that the following converges a.s. in :

| (46) |

thus completing the proof of one-dimensional weak convergence for (38).

Convergence in f.d.d. for (• ‣ 2.3)

We will mimic the arguments of KS , DG , CD . Let

Using the last equality in (3), we have

| (47) | |||

where is the real-valued characteristic function of a symmetric reward and

| (48) |

Suppose is the characteristic function of the SS law of scale parameter . We show that the following asymptotic holds as :

| (49) |

If and are sequences in with only finitely many terms not equal to one, then

| (50) |

Letting

| (51) |

we have

| (52) | |||

By assumption, converges weakly and is bounded in , so to prove (49) we need only show that is bounded and converges in probability to . Since is in the domain of attraction of the SS law with , by the stable central limit theorem, we have that as ,

Thus is bounded, continuous and vanishes at . Equation (49) follows since goes to zero.

Let be independent copies of i.i.d. reward such that has an SS law with scale parameter . Using (49), the th root of (3) is equal to

| (53) | |||

If is such that , then . Letting

and using the assumption of uniform integrability, we have that

| (54) |

as required.

Tightness in and for (36)

Suppose that so that converges weakly in to a two-sided Brownian motion . By (SLP) and the independence of and , the joint process

converges weakly to in . The weak convergence of in therefore follows from the continuous mapping theorem, provided that is continuous from to .

The topologies on and are first countable, so proving sequential continuity suffices. Suppose in and in , and let be a continuity point of . By the definition of convergence on , we must show that there is a sequence of homeomorphisms from onto such that converges uniformly to the identity and converges uniformly to .

Let be given. Since in , there are homeomorphisms from onto such that converges uniformly to the identity, and converges uniformly to . The set is bounded, so converges uniformly to on . Thus, is uniformly continuous on , and thus on .

Choose such that for and . Next, find such that whenever , and find such that whenever . Then, whenever , we have

| (55) | |||

for all . Thus, converges uniformly to showing continuity of the composition map. The same argument holds if converges weakly in , except that proving the continuity of the composition map on is even simpler. {remark*} We thank an anonymous referee for the above tightness proof which simplifies our original proof. The referee also noticed the following informative observation. If , then scales to an -stable Lévy motion, . Fix and let be the first positive time such that . Consider the simple case where scales to a Brownian motion, . Let be the first time hits . As is well known, oscillates around immediately, thus does not exist a.s. This argument, which can be made rigorous, shows that even in the elementary case where the collecting process scales to Brownian motion, the process is not cadlag.

4 A recursive construction of some fractional stable motions

Throughout this section we will suppose that . We present two related recursive constructions of some -sssi processes. The first recursion produces stable processes in random scenery, while the second recursion produces local time and indicator fractional stable motions. Note that only the second recursion leads to SS processes. Since fBm is the only sssi Gaussian process, when the second construction gives us fBm. In particular, if on the first step of the recursion we use Brownian motion as the collecting process (or random time process), then we obtain fBm of any dyadic Hurst parameter.

Although the first construction does not in general lead to -stable processes, we will see that the finite-dimensional distributions of the processes have finite moments, and thus one can appeal to the stable central limit theorem and normalize partial sums of independent copies of the stable processes in random scenery in order to get honest stable processes [in a manner similar to (31)].

Let be an -sssi process satisfying the four conditions of Theorem 4.1 below. Consider the vector with coordinates . Let us use the notation to denote truncated by removing the last element, that is, . The empty set will denote the empty vector.

We define the process recursively from and an -stable random measure , with , assumed to be independent from . If , we let

| (56) |

and if , we let

| (57) |

The second recursive procedure is defined similarly. We again use vectors, now denoted , with coordinates taking one of two different values. However, in order to distinguish between the two procedures, we let . As before, we let .

Once again is defined recursively from and an -stable random measure with ; however, the control measure of is no longer Lebesgue measure as it was in the case of . Suppose that is the probability space of . Then, just as in (26), has control measure and lives on some other probability space . If , we let

| (58) |

and if , we let

| (59) |

We must show that the above recursions makes sense, that is, that the integrals are well defined. In general, it is known that -sssi SS processes have local times almost surely. This almost gets us to where we want to be; however, there are two separate issues with which we must deal.

According to (19) we need that the integral kernels of (56) and (57) are in [which easily follows if they are in ], but (56) and (57) are not in general SS processes, and thus we need an extra argument to show that they have local times almost surely.

The second issue concerns (58) and (59) which are SS processes, but are well defined only if the local times are in . In other words, we will need the th moment of the local times to be integrable. To solve these two issues, we use the following result.

Theorem 4.1.

Suppose is an -sssi process which satisfies:

[(a)]

.

has a local time satisfying .

has a bounded continuous density.

. Then the processes

| (60) | |||||

| (61) | |||||

| (62) | |||||

| (63) |

are well-defined -sssi processes satisfying (b)–(d), where for and and for and . Moreover, all four processes have finite moments which implies they also satisfy (a).

(1) For the proof, we need that satisfies the occupation time formula

for any Borel set . This follows from definition (21).

(2) The processes and are not generally stable. However, as mentioned above, when they have finite moments, one can use the stable central limit theorem and normalize partial sums of independent copies of these processes to get stable processes. {pf*}Proof of Theorem 4.1 Well-defined -sssi processes with finite th moments. To see that the are well defined and satisfy (a), we have

| (64) |

which is positive and finite since satisfies (a). Also,

| (65) |

To see that (65) is finite and nonzero, note that by the occupation time formula and by (b), thus for .

To see that the are -sssi, we refer the reader to Theorem 3.1 in CS and Theorem 2.2 in jung2010indicator .

Property (b). Next we use Theorem 21.9 of geman1980occupation which implies condition (b) under the assumption that

| (66) |

Let us show (b) for . We have

| (67) |

Using and

| (68) |

we see that

Substituting we get that (66) equals

| (70) |

which is finite since by the occupation time formula.

Substituting and integrating we obtain, for some constant ,

| (72) |

To show that this is finite we need only show that . We have for

| (73) |

so by Holdër’s inequality,

By the occupation time formula, the left-hand side of (4) equals a.s. so that

| (75) |

Property (d) of completes the proof of (b) for .

Finally, let us consider . We may mimic steps (67) through (72) in order to reduce (66) to showing

| (78) |

But this follows from assumption (c) on , since we may simply integrate against the bounded continuous density of which will give a finite value. This establishes (b) for .

Property (c). In the course of showing property (b) for , we showed that in all cases possesses a nonnegative and integrable characteristic function, and thus (c) follows from Theorem 3.3.5 in durrett2010probability .

Property (d). Consider first . Property (d) is known for and since they are sssi Gaussian processes, that is, fractional Brownian motions.

For , let be a two-sided Brownian motion. We use Proposition 2.2 in khoshnevisan1998law which is essentially a corollary of Slepian’s lemma. It implies that for each fixed ,

| (79) |

Integrating over , property (d) for follows from property (d) for .

For , let , and . We have

The last inequality follows since the integral in the second to last line is just a two-sided Brownian motion at time and . We thus get property (d) for since property (d) holds for .

Let us now suppose that . Theorem 10.5.1 of samorodnitsky1994stable states that if

| (81) |

for some family of functions , where is the control measure of , then there is a constant such that

| (82) |

for any .

5 Brownian motion extracted from fBm,

Suppose . Then the family of stochastic integrals, , is an -sssi Gaussian process, thus it is precisely fBm with Hurst exponent . In this section, we show that Brownian motion can be extracted from by time-changing its integral kernels. In order to motivate our time-changed kernels, we first show that Brownian motion can also be extracted from a stable process at random time, , using a time-change.

To keep things simple, we assume in this section that the random time process is itself an fBm. Thus it is a.s. continuous and satisfies the property that for each ,

| (86) |

Heuristically, time-changing the kernel of undoes the subordination of to the process , leaving us with a process . We then observe that for , and that is linearly increasing (here is the control measure). One need only check that such a procedure gives us what we want, by looking at the finite-dimensional distributions. Since our interest is in the case , we have that , are Gaussian random measures on and , respectively, and we in fact need only check covariances.

Let us start by presenting the time-change of .

Proposition 5.1.

Let the random time process be a fractional Brownian motion. If is defined as in (61) with , then is a Brownian motion.

We have

| (87) |

where is a two-sided Brownian motion. For the covariances, if , we have

In the case of

we cannot look at “” since lives on the same probability space as . We address this issue by instead time-changing the kernel . Let us define

| (89) |

A good way to think about the above integral is in terms of a central limit theorem similar to (31):

| (90) |

Here, is measurable with respect to the -field of . By Proposition 5.1, the are independent Brownian motions. The next proposition shows that the right-hand side is also a Brownian motion thus proving (90).

Proposition 5.2.

Let the random time process be a fractional Brownian motion. If is defined as in (63) with , then is a Brownian motion.

We have

which is a Gaussian random variable with variance . For the covariances we analyze second moments. If , we have

as required.

Acknowledgments

We thank Clement Dombry, Harry Kesten and Gennady Samorodnitsky for helpful email correspondence. We also thank anonymous referees for careful readings, nice suggestions and corrections.

Part of this work was done when P. Jung was visiting Pohang University of Science and Technology and also IPAM at UCLA. He thanks both institutions for their hospitality. G. Markowsky thanks Sogang University for hospitality during which some of this work was done.

References

- (1) {barticle}[mr] \bauthor\bsnmBerman, \bfnmSimeon M.\binitsS. M. (\byear1974). \btitleLocal nondeterminism and local times of Gaussian processes. \bjournalIndiana Univ. Math. J. \bvolume23 \bpages69–94. \bidissn=0022-2518, mr=0317397 \bptokimsref \endbibitem

- (2) {barticle}[mr] \bauthor\bsnmBorodin, \bfnmA. N.\binitsA. N. (\byear1979). \btitleLimit theorems for sums of independent random variables defined on a transient random walk. \bjournalZap. Nauchn. Sem. Leningrad. Otdel. Mat. Inst. Steklov. (LOMI) \bvolume85 \bpages17–29, 237, 244. \bnoteInvestigations in the theory of probability distributions, IV. \bidissn=0207-6772, mr=0535455 \bptokimsref \endbibitem

- (3) {barticle}[mr] \bauthor\bsnmBoylan, \bfnmEdward S.\binitsE. S. (\byear1964). \btitleLocal times for a class of Markoff processes. \bjournalIllinois J. Math. \bvolume8 \bpages19–39. \bidissn=0019-2082, mr=0158434 \bptokimsref \endbibitem

- (4) {bincollection}[mr] \bauthor\bsnmBurdzy, \bfnmKrzysztof\binitsK. (\byear1993). \btitleSome path properties of iterated Brownian motion. In \bbooktitleSeminar on Stochastic Processes, 1992 (Seattle, WA, 1992). \bseriesProgress in Probability \bvolume33 \bpages67–87. \bpublisherBirkhäuser, \blocationBoston, MA. \bidmr=1278077 \bptnotecheck year\bptokimsref \endbibitem

- (5) {barticle}[mr] \bauthor\bsnmCohen, \bfnmSerge\binitsS. and \bauthor\bsnmDombry, \bfnmClément\binitsC. (\byear2009). \btitleConvergence of dependent walks in a random scenery to fBm-local time fractional stable motions. \bjournalJ. Math. Kyoto Univ. \bvolume49 \bpages267–286. \bidissn=0023-608X, mr=2571841 \bptokimsref \endbibitem

- (6) {barticle}[mr] \bauthor\bsnmCohen, \bfnmSerge\binitsS. and \bauthor\bsnmSamorodnitsky, \bfnmGennady\binitsG. (\byear2006). \btitleRandom rewards, fractional Brownian local times and stable self-similar processes. \bjournalAnn. Appl. Probab. \bvolume16 \bpages1432–1461. \biddoi=10.1214/105051606000000277, issn=1050-5164, mr=2260069 \bptokimsref \endbibitem

- (7) {bincollection}[mr] \bauthor\bsnmDeheuvels, \bfnmPaul\binitsP. and \bauthor\bsnmMason, \bfnmDavid M.\binitsD. M. (\byear1992). \btitleA functional LIL approach to pointwise Bahadur–Kiefer theorems. In \bbooktitleProbability in Banach Spaces, 8 (Brunswick, ME, 1991). \bseriesProgress in Probability \bvolume30 \bpages255–266. \bpublisherBirkhäuser, \blocationBoston, MA. \bidmr=1227623 \bptokimsref \endbibitem

- (8) {bincollection}[mr] \bauthor\bparticleden \bsnmHollander, \bfnmFrank\binitsF. and \bauthor\bsnmSteif, \bfnmJeffrey E.\binitsJ. E. (\byear2006). \btitleRandom walk in random scenery: A survey of some recent results. In \bbooktitleDynamics & Stochastics. \bseriesInstitute of Mathematical Statistics Lecture Notes—Monograph Series \bvolume48 \bpages53–65. \bpublisherInst. Math. Statist., \blocationBeachwood, OH. \biddoi=10.1214/lnms/1196285808, mr=2306188 \bptokimsref \endbibitem

- (9) {bmisc}[auto:STB—2012/08/23—07:51:16] \bauthor\bsnmDombry, \bfnmC.\binitsC. (\byear2011). \bhowpublishedDiscrete approximation of stable white noise: Applications to spatial linear filtering. Preprint. \bptokimsref \endbibitem

- (10) {barticle}[mr] \bauthor\bsnmDombry, \bfnmC.\binitsC. and \bauthor\bsnmGuillotin-Plantard, \bfnmN.\binitsN. (\byear2009). \btitleDiscrete approximation of a stable self-similar stationary increments process. \bjournalBernoulli \bvolume15 \bpages195–222. \biddoi=10.3150/08-BEJ147, issn=1350-7265, mr=2546804 \bptnotecheck year\bptokimsref \endbibitem

- (11) {barticle}[mr] \bauthor\bsnmDombry, \bfnmC.\binitsC. and \bauthor\bsnmGuillotin-Plantard, \bfnmN.\binitsN. (\byear2009). \btitleA functional approach for random walks in random sceneries. \bjournalElectron. J. Probab. \bvolume14 \bpages1495–1512. \biddoi=10.1214/EJP.v14-659, issn=1083-6489, mr=2519528 \bptokimsref \endbibitem

- (12) {bbook}[mr] \bauthor\bsnmDurrett, \bfnmRick\binitsR. (\byear2010). \btitleProbability: Theory and Examples, \bedition4th ed. \bpublisherCambridge Univ. Press, \blocationCambridge. \bidmr=2722836 \bptokimsref \endbibitem

- (13) {barticle}[mr] \bauthor\bsnmFunaki, \bfnmTadahisa\binitsT. (\byear1979). \btitleProbabilistic construction of the solution of some higher order parabolic differential equation. \bjournalProc. Japan Acad. Ser. A Math. Sci. \bvolume55 \bpages176–179. \bidissn=0386-2194, mr=0533542 \bptokimsref \endbibitem

- (14) {barticle}[mr] \bauthor\bsnmGeman, \bfnmDonald\binitsD. and \bauthor\bsnmHorowitz, \bfnmJoseph\binitsJ. (\byear1980). \btitleOccupation densities. \bjournalAnn. Probab. \bvolume8 \bpages1–67. \bidissn=0091-1798, mr=0556414 \bptokimsref \endbibitem

- (15) {barticle}[mr] \bauthor\bsnmGuillotin-Plantard, \bfnmNadine\binitsN. and \bauthor\bsnmPrieur, \bfnmClémentine\binitsC. (\byear2010). \btitleLimit theorem for random walk in weakly dependent random scenery. \bjournalAnn. Inst. Henri Poincaré Probab. Stat. \bvolume46 \bpages1178–1194. \biddoi=10.1214/09-AIHP353, issn=0246-0203, mr=2744890 \bptokimsref \endbibitem

- (16) {barticle}[mr] \bauthor\bsnmJung, \bfnmPaul\binitsP. (\byear2011). \btitleIndicator fractional stable motions. \bjournalElectron. Commun. Probab. \bvolume16 \bpages165–173. \biddoi=10.1214/ECP.v16-1611, issn=1083-589X, mr=2783337 \bptokimsref \endbibitem

- (17) {barticle}[mr] \bauthor\bsnmKesten, \bfnmH.\binitsH. and \bauthor\bsnmSpitzer, \bfnmF.\binitsF. (\byear1979). \btitleA limit theorem related to a new class of self-similar processes. \bjournalProbab. Theory Related Fields \bvolume50 \bpages5–25. \bptokimsref \endbibitem

- (18) {barticle}[mr] \bauthor\bsnmKhoshnevisan, \bfnmDavar\binitsD. and \bauthor\bsnmLewis, \bfnmThomas M.\binitsT. M. (\byear1998). \btitleA law of the iterated logarithm for stable processes in random scenery. \bjournalStochastic Process. Appl. \bvolume74 \bpages89–121. \biddoi=10.1016/S0304-4149(97)00105-1, issn=0304-4149, mr=1624017 \bptokimsref \endbibitem

- (19) {bincollection}[mr] \bauthor\bsnmKhoshnevisan, \bfnmDavar\binitsD. and \bauthor\bsnmLewis, \bfnmThomas M.\binitsT. M. (\byear1999). \btitleIterated Brownian motion and its intrinsic skeletal structure. In \bbooktitleSeminar on Stochastic Analysis, Random Fields and Applications (Ascona, 1996). \bseriesProgress in Probability \bvolume45 \bpages201–210. \bpublisherBirkhäuser, \blocationBasel. \bidmr=1712242 \bptnotecheck year\bptokimsref \endbibitem

- (20) {barticle}[mr] \bauthor\bsnmKhoshnevisan, \bfnmDavar\binitsD. and \bauthor\bsnmLewis, \bfnmThomas M.\binitsT. M. (\byear1999). \btitleStochastic calculus for Brownian motion on a Brownian fracture. \bjournalAnn. Appl. Probab. \bvolume9 \bpages629–667. \biddoi=10.1214/aoap/1029962807, issn=1050-5164, mr=1722276 \bptokimsref \endbibitem

- (21) {barticle}[mr] \bauthor\bsnmLe Gall, \bfnmJean-François\binitsJ.-F. and \bauthor\bsnmRosen, \bfnmJay\binitsJ. (\byear1991). \btitleThe range of stable random walks. \bjournalAnn. Probab. \bvolume19 \bpages650–705. \bidissn=0091-1798, mr=1106281 \bptokimsref \endbibitem

- (22) {bbook}[mr] \bauthor\bsnmLedoux, \bfnmMichel\binitsM. and \bauthor\bsnmTalagrand, \bfnmMichel\binitsM. (\byear1991). \btitleProbability in Banach Spaces: Isoperimetry and Processes. \bseriesErgebnisse der Mathematik und Ihrer Grenzgebiete (3) [Results in Mathematics and Related Areas (3)] \bvolume23. \bpublisherSpringer, \blocationBerlin. \bidmr=1102015 \bptokimsref \endbibitem

- (23) {barticle}[mr] \bauthor\bsnmNane, \bfnmErkan\binitsE. (\byear2006). \btitleLaws of the iterated logarithm for -time Brownian motion. \bjournalElectron. J. Probab. \bvolume11 \bpages434–459 (electronic). \biddoi=10.1214/EJP.v11-327, issn=1083-6489, mr=2223043 \bptokimsref \endbibitem

- (24) {barticle}[mr] \bauthor\bsnmNane, \bfnmErkan\binitsE., \bauthor\bsnmWu, \bfnmDongsheng\binitsD. and \bauthor\bsnmXiao, \bfnmYimin\binitsY. (\byear2012). \btitle-time fractional Brownian motion: PDE connections and local times. \bjournalESAIM Probab. Stat. \bvolume16 \bpages1–24. \biddoi=10.1051/ps/2011103, issn=1292-8100, mr=2900521 \bptnotecheck year\bptokimsref \endbibitem

- (25) {barticle}[mr] \bauthor\bsnmSamorodnitsky, \bfnmGennady\binitsG. (\byear2005). \btitleNull flows, positive flows and the structure of stationary symmetric stable processes. \bjournalAnn. Probab. \bvolume33 \bpages1782–1803. \biddoi=10.1214/009117905000000305, issn=0091-1798, mr=2165579 \bptokimsref \endbibitem

- (26) {bbook}[mr] \bauthor\bsnmSamorodnitsky, \bfnmGennady\binitsG. and \bauthor\bsnmTaqqu, \bfnmMurad S.\binitsM. S. (\byear1994). \btitleStable Non-Gaussian Random Processes: Stochastic Models with Infinite Variance. \bpublisherChapman & Hall, \blocationNew York. \bidmr=1280932 \bptokimsref \endbibitem

- (27) {barticle}[auto:STB—2012/08/23—07:51:16] \bauthor\bsnmTurban, \bfnmL.\binitsL. (\byear2004). \btitleIterated random walk. \bjournalEurophysics Letters \bvolume65 \bpages627. \bptokimsref \endbibitem

- (28) {barticle}[mr] \bauthor\bsnmWang, \bfnmWensheng\binitsW. (\byear2003). \btitleWeak convergence to fractional Brownian motion in Brownian scenery. \bjournalProbab. Theory Related Fields \bvolume126 \bpages203–220. \biddoi=10.1007/s00440-002-0249-8, issn=0178-8051, mr=1990054 \bptokimsref \endbibitem