High-dimensional Instrumental Variables Regression and Confidence Sets

Abstract.

This article considers inference in linear instrumental variables models with many regressors, all of which could be endogenous. We propose the STIV estimator. Identification robust confidence sets are derived by solving linear programs. We present results on rates of convergence, variable selection, confidence sets which adapt to the sparsity, and analyze confidence bands for vectors of linear functions using bias correction. We also provide solutions to some instruments being endogenous. The application is to the EASI demand system.

1. Introduction

The high-dimensional paradigm concerns models in which the number of regressors is large relative to the number of observations but there is an unknown small set of relevant regressors. This can happen for various reasons. Researchers increasingly have access to large datasets and theory is often silent on the correct regressors. The number of observations can be limited because data is costly to obtain, because there simply exist few units (e.g., countries), or because the researcher is interested in a stratified analysis. The usual fixed large asymptotic framework does not necessarily provide a good approximation when there is high-dimensionality. A challenging situation is when is much larger than (). Comparing models for all subsets of regressors is impossible when is even moderately large. The main focus of the high-dimensional literature is therefore the analysis of computationally feasible methods. For high-dimensional regression, the Lasso [38] involves an -penalty. The Dantzig Selector [19] is a linear program (henceforth LP).

We study the high-dimensional linear instrumental variables (henceforth IVs) model where all regressors can be endogenous but the parameter is sparse, meaning it has few nonzero entries, or approximately sparse, meaning it is well approximated by a sparse vector. Sparsity can arise naturally when has an economic interpretation. Examples include social effects models with unobserved networks, models with uncertain exclusion restrictions, and treatment models with group heterogeneity in the treatment effect and many groups.

Approximate sparsity is more appropriate when a linear model is used to approximate a function and the regressors and IVs comprise functions (e.g., splines) of baseline regressors and IVs. This can arise due to linearization or the use of series. The latter is relevant if the structural model has a nonparametric component or such components arise by including controls to justify IV exogeneity.

With many endogenous regressors the number of IVs, , can be large. We allow for but of order less than . Strong IVs are often scarce, particularly when there are many endogenous regressors.

For these reasons, we pay attention to finite sample validity and robustness to identification. Indeed, if there are weak and/or many IVs, inference based on standard asymptotic approximations can fail even if is small. To achieve this, we use a -norm statistic derived from the moment condition. This is close in spirit to identification robust test inversion in which the exogeneity is the null hypothesis and a confidence set is formed by parameters which are not rejected. The Anderson-Rubin test is an example. In practice, such tests are conducted over a grid, which is only feasible for small . To allow for large , we use convex relaxations (linear or conic) instead. Our approach does not estimate reduced form equations and imposes no structure on them (e.g., sparsity).

We propose the Self Tuning Instrumental Variables (henceforth STIV) estimator and establish its error bounds, which are used to obtain confidence sets for a vector of functions of and rates of convergence.

Some confidence sets

are uniform over identifiable parameters and distributions of the data among classes which leave the dependence between the regressors and IVs unrestricted, implying robustness to identification. Under stronger assumptions, including on the joint distribution of the IVs and regressors, the STIV estimator can be a pilot estimator to perform variable selection, obtain confidence sets which adapt to the sparsity, and conduct joint inference on linear functions of based on a data-driven bias correction. We also propose solutions to the problem that, in this data rich environment, a few IVs can be endogenous. All of our methods are pivotal because they jointly estimate standard deviations of structural errors or moments, making the tuning parameters data-driven.

The application is to Engel curves in the EASI system of [33]. We show that the first-order in prices approximation error can be large and propose a second order approximation leading to a linear system with thousands of endogenous regressors. To achieve this, our theory allows for empirically relevant specificities, including knowledge of the relevance of certain regressors (e.g., price and quadratic expenditure), parameter restrictions (e.g., symmetry of the Slutsky matrix), approximation error, and systems of equations.

2. Preliminaries

Notations. To simplify the exposition we consider an i.i.d. sample of size . The population model comprises an outcome , regressors , and IVs of joint distribution . is the expectation under . For a mean zero random variable , . We denote stacked matrices in bold, e.g., , where is the set of matrices. For and a random vector , is the sample mean, is the diagonal matrix with entries for , and its population counterpart. For , , is the distribution of implied by , and . We write and . The set collects the indices of the regressors which are also IVs and of size collects those of the regressors of questionable relevance. When we make inference on a vector of functions, its dimension is . Some results are asymptotic in in which case , , and can increase with and triangular arrays are permitted. Inequality between vectors is entrywise. (resp. ) is the row (resp. column) of . is the indicator function. For , is its cardinality and its complement. For , and . is the -norm of or a vectorization if is a matrix.

Baseline moments model. The linear IV model is

| (1) | |||

| (2) |

where accounts for restrictions on

and is a nonparametric class, e.g.,

Class 1:

is symmetric for all and

where is a confidence level and the normal CDF. Other classes allow for non i.d. and dependent data, and asymmetry (see Section A.1.1). Their basic versions do not restrict the joint distribution of and .

All but Class 4 allow for conditional heteroscedasticity.

The set collects the vectors which satisfy (1)-(2). Our results are for all , hence for the true .

The -norm statistic. Our confidence sets and estimators use slack versions of (1) based on the statistic for . We use, for , the event . Taking , the base choice in the main text, and for Class 1,111 (because if ). yields for all and such that . Such a simple bound is possible due to the division by . The set is a confidence set but it is infeasible because it is nonconvex and is high-dimensional and (approximately) sparse. Class 4 determines by bootstrap under conditional homoscedasticity.

Sparsity certificate. A sparsity certificate is a bound on the sparsity and is the set of -sparse identifiable parameters. For asymptotic results and triangular arrays, can depend on . can be a singleton when and sparsity implies exogenous regressors have a zero coefficient (i.e., they are excluded). This occurs when exclusion restrictions are uncertain (see [32, 31]). When , is a singleton if there is a solution for only one of the overdetermined systems based on (1)-(2) and it is unique. Another condition (see [19]) is that all matrices formed from columns of have full rank.

Example SE. The outcome of individual depends on peer outcomes. When the peers are unknown and there are endogenous peer effects, a linear model is , where is the effect of on and are low-dimensional exogenous characteristics. If we set and all peers are unknown then , and is the set of ’s peers. If the network is sparse (e.g., due to costly link formation) then . A sparsity certificate is an upper bound on the number of peers. The IVs are , so . If there are also exogenous peer effects then is replaced by in the structural equation and .

Example NP. The model is with a nonparametric and an IV such that . Assuming no approximation error, which we cover in Section 6.2.1, (1) holds with and for approximating functions and .

Roadmap. The paper is organized to progressively strengthen the assumptions. Here, we summarize our methods with the simplifications , and, for all , is normally distributed with mean 0 and known variance . The simplifications permit to replace by and by of order .

A starting point is to find by minimizing subject to . A solution is obtained by solving a LP and is called the nonpivotal STIV estimator. STIV does not require a known and is introduced in Section 3. To analyze the estimation error and construct confidence sets, we introduce sensitivity characteristics in Section 3.1. To explain their role, we now take a . Since is a minimizer, on the event we can use , and . Letting , the first inequality implies

, hence , and by the triangle inequality

. The last two imply . For , we introduce a sensitivity

| (3) |

which gives . The first inequality holds if and otherwise follows by , homogeneity, and

Omitting the constraint from (3) leads to a smaller , hence wider confidence sets below. We do not know but if we know , we replace by a lower bound (see Section 3.2). Adding to yields and using , we obtain

| (4) |

This yields the bounds . is obtained by solving LPs so this is a computationally feasible confidence set. The coverage guarantee is uniform over such that for from Class 1. The set is robust to arbitrarily weak IVs because does not restrict the dependence between and . Also, need not be a singleton. In Section 3.3 we obtain rates of convergence for (possibly to a set) by replacing sensitivities with population analogues. A simple condition to analyze the rates is that, for every relevant regressor (i.e., ), there is a linear combination of IVs, where , which has low correlation (if ) with the other regressors relative to . This yields the rate

| (5) |

for all . Assuming the nonzero entries of are sufficiently large relative to the -rate, we obtain , and if they are larger still, for a thresholded estimator . We then build confidence sets based on

for such an estimator .

Our confidence sets need few assumptions, can be robust to identification, and are useful for inference on a function of the entire parameter . However they may be conservative when stronger assumptions can be maintained and the object of interest has dimension much smaller than . In Section 4 we present confidence bands for a vector of linear functions based on a bias correction of . A special case is a confidence interval. These are obtained by applying a variant of STIV to estimate satisfying , and then combining with .

In Section 5, we present a method to detect endogenous IVs. The basic idea is to use a variant of STIV to estimate the correlation of the IVs with the residuals (i.e., ) from a first-stage STIV estimator which uses only the IVs known to be exogenous.

In Section 6, we conduct simulations and apply STIV to build confidence bands around the EASI Engel curves. This is similar in spirit to Example NP, but the approximation error arises due to linearization rather than use of approximating functions. To make full use of economic theory, we require , a set based on theory, and a minor modification of STIV to permit approximation errors and systems of structural equations. Proofs are in the appendix.

References. High-dimensional estimation and inference has become an active field. To name a few; [3] uses Lasso type methods to estimate the optimal IV and make inference on a low-dimensional structural equation, [24] consider a nonconvex approach to IV estimation, [13, 14, 20] consider GMM with large dimensions but do not handle the high-dimensional regime. Inference for subvectors in high-dimension is an active topic related to Section 4 (see [5, 29, 40, 12], but also [27, 3, 10, 15] in the case of IVs. [7] reviews results based on the nonpivotal STIV and others. Our results are applied to social effects models with unknown networks in [36, 26] and [2].

3. Self-Tuning IV Estimator and Confidence Sets

Definition 3.1.

For , a STIV estimator is any solution of

| (6) |

where, for ,

| (7) |

The -norm is a convex relaxation of . The term favors small , hence increasing tightens the set . and guarantee invariance to scale of the regressors and IVs. If comprises linear (in)equality restrictions, a STIV estimator is computed by solving a convex (second-order) conic program, similarly to the Square-root Lasso of [4]. Linearity of (1) in is key to obtain such a simple program. and are estimators of the standard deviation of the structural error which need not be known. Taking in the nonpivotal STIV estimator gives the Dantzig Selector.

Minimizing trades-off least-squares and exogeneity of the IVs, which is desirable in the presence of weak IVs (see [1]). STIV implements this in high-dimension because

| (8) |

If were a differentiable and strictly convex function of and the entries of drawn from a continuous distribution, minimizers of (8) would be unique and one could obtain regularization paths (see [39]) for ad hoc determination of the penalty level. Our analysis is valid for all minimizers and determination of the penalty level is not an issue because STIV is pivotal. Non uniqueness also occurs for LIML, which minimizes the Anderson-Rubin statistic.

3.1. Sensitivity Characteristics

If , the minimal eigenvalue of can be used to obtain error bounds for quantities such as the mean squared error. It is the minimum of over , and is equal to zero if . Under sparsity,

can be replaced by a subset in the case of the Dantzig Selector and Lasso.

This is typically expressed via the restricted eigenvalue condition of [11].

The sensitivity characteristics introduced in this paper are core elements to analyze STIV and provide sharper results for the Dantzig Selector and Lasso (see Section O.1.1). They are

related to the action of on a subset for .

As in the Roadmap, we bound on .

To bound for a loss , we use a sensitivity

| (9) |

When we use the shorthand . We require that , where are the continuous functions from to which are homogeneous of degree 1. An important loss is for and . For and for , we use the shorthand notations and . The sensitivities for these losses can be related to one another as expressed in Proposition A.1. Due to the -norm in (9), additional IVs can only increase . Their cost is mild because it appears only through the factor in .

The cone for the nonpivotal STIV is modified to be

| (10) |

is used because, by convexity and since the regressors of index in are used as IVs, . when all regressors are endogenous.

Similarly to the Roadmap, for every , on the event , we have .

The error bounds for STIV in Proposition 3.1 are decreasing in the sensitivities, hence it is important that be small so that the sensitivities can be bounded away from zero. The researcher’s knowledge components , , and serve this purpose. When, e.g., comprises linear equalities , we add

to . Because is typical, accounting for yields a smaller set.

If we omit , take , , and replace by we obtain the simple cone of dominant coordinates

,

due to which has most of its -norm concentrated on the indices in .

This cone is if . Using the smaller is empirically relevant because

in practice we find that STIV performs better for . The constraint can be removed to obtain rates of convergence, but is useful to construct confidence sets which are as small as possible.

If is not sparse, can be large (e.g., when ), so

the sensitivities, denoted by instead of , are defined by replacing by

Due to the additional terms on the right-hand side, is larger than . However, in our analysis these sensitivities need not be computed at . The slackness allows on provided that is sufficiently small. The form of the additional terms is related to the factor 6 in the second inequality in Proposition 3.1.

Our results involve the weakly increasing function

where by convention . It is close to 1 for small and is when . We also let and .

Proposition 3.1.

For all such that , any STIV estimator, , , , and , we have, on ,

The first term in the minimum in the first inequality is used for confidence sets, and the second for rates of convergence. The second inequality is used when contains nonsparse vectors, and is the basis of the sparsity oracle inequality in Theorem 3.1 (iii). To obtain a confidence set one needs to circumvent the dependence of the sensitivities on the unknown in a computationally feasible way. This is the focus of Section 3.2. For rates of convergence one requires population analogues of the upper bounds. This is the focus of Section 3.3.

3.2. Computable Bounds on the Sensitivities and Confidence Sets

Confidence sets can be obtained by using lower bounds on the sensitivities. To obtain (4) in the Roadmap, we use a sparsity certificate . Alternatively, one replaces by such that with probability converging to 1. We explain how STIV can be used to obtain such in Section 3.3. We now present our base result, which provides bounds through LPs.

Proposition 3.2.

Using a sparsity certificate and

| (11) |

the confidence set for , where , denoted verifies

| (12) |

The set is robust to identification if, as for Class 1, does not restrict the dependence between and . Though we do not make it explicit, the bound in (11) depends on . Increasing decreases (by increasing the penalty on in the STIV objective function) but increases (by enlarging ). The set (11) can be made computationally feasible with correct coverage by replacing with a finite intersection. If and is a grid for , we can define the confidence set for , with

| (13) |

| Notes: is also bounded by (iv) in Proposition A.1. Bounds for (resp. ) replace (resp. ) by (resp. ) in the bounds for (resp. ). Section O.1.1 gives sharper but more computationally demanding bounds. | |||

We can replace by to obtain a larger but less computationally demanding set (i.e., with less LPs).

If , we use the loss , where for .

The above confidence sets are nonempty hyperrectangles, and are infinite if . This is unavoidable for sets which are robust to weak IVs (see [22]).

Section 6.1 provides a rule of thumb to determine a single value of . Even if is determined from the data, the set has coverage at least

due to (11). Because the researcher may be unsure about an appropriate value of , the minimum over in

(12) allows to construct nested sets over different values. This can be used to assess the information content of progressively stronger sparsity assumptions.

Example SE continued. A sparsity certificate (upper bound on the number of peers) yields a confidence set for the peer effects. By (12), the estimator of the peers satisfies . A subset is unavoidable because the peer effects can be arbitrarily close to zero, an issue to which we return in Section 3.3. A confidence interval for the average peer effect uses .

3.3. Deterministic Error Bounds, Model Selection, and Refined Confidence Sets

We give deterministic counterparts of the bounds in Proposition 3.1 based on an event , on which controls the deviation of the sample from the population, where

| (14) |

On , can be replaced by a deterministic upper bound (see (A.1), which also defines ) and and the sensitivities by population analogues and and , obtained by replacing by and , by , (see Lemma A.2). We restrict using Assumption A.1, which places mild restrictions on second moments and the tails of the IVs so that , where is defined in (A.2). Asymptotic statements allow to depend on . In the discussion of orders below Theorem 3.1 and in Section 4, and are assumed uniformly bounded, so under (14) and, for the choice of using classes 1-3, has same order as (i.e., ). Section A.1.1 presents the general case.

3.3.1. Deterministic Error Bounds and Rates of Convergence

The deterministic bounds below hold without additional assumptions. We leave the dependence between and unrestricted, allow for partial identification, and when , which works well in practice. For the bounds to be orders in probability, we replace the confidence level used to set by converging to 0, so

For a function from to and given , we set

Theorem 3.1.

Let and be such that Assumption A.1 holds.

-

(i)

For all such that and any STIV estimator, we have, on , for all ,

where for , .

-

(ii)

For all such that , where , and any STIV estimator, we have, on , .

-

(iii)

For all such that and any STIV estimator, we have, on , for all and ,

where (resp. ) replaces by in (resp. by in ).

Theorem 3.1 (i)-(ii) provide a bound and a model selection result suited to the sparse case.

Result (iii) gives an alternative bound better suited to approximate sparsity. The dependence of the bounds on the function is unavoidable. It means that they can be infinite, and so hold with high probability regardless of the dependence between and . Bounds for -loss are used in the next section, in which STIV is used as a pilot estimator. The loss for is used in (ii) with . It can be used to obtain uniform rates of convergence for the coefficients of index in (e.g., ). The bona fide loss for model selection is (see [34]).

Result (ii) means that, for all , STIV finds a superset of the regressors. The term corresponds to the upper bound on . Using in its definition allows a larger than using .

Due to (ii), the confidence set , where

| (15) |

is such that

| (16) |

It is not robust to identification because depends on the population sensitivities (which depend on ), hence on the joint distribution of and (recalling ). The condition in Theorem 3.1 (ii) is a beta-min condition. It requires that the nonzero entries of be large enough, and is interpretable if is a structural parameter. It is not intended to be used if the regressors are used to approximate a function as in Example NP.

Example SE continued. The beta-min condition means that the peer effects are sufficiently large so as to be distinguishable from zero. It is reasonable because a typical parameterization when the social effect is via the mean (see [9]) is where is a scalar, so when the network is sparse the relevant effects are bounded away from zero. STIV finds a superset of the peers with asymptotic (uniform) probability at least .

If is sparse, the upper bound in Theorem 3.1 (iii), which holds for all , also applies to , for which the second term in the maximum is zero. We are then left with a bound similar to the right-hand side of (i). When and , it is 6 times the error made when (estimating perfectly the components in ). In this sense the second term is an approximation error. STIV performs a data-driven trade-off for nonsparse parameter vectors. Result (iii) implies that, for an optimal set (not necessarily ),

| (17) |

This allows us to define formally approximately sparse parameter vectors as vectors which are sufficiently well approximated by a sparse vector so that the right-hand side of (17) is small.

Remark 3.1.

Theorem 3.1 applies if is not a singleton, in which case, for a given , one can take the infimum over on both sides of the inequality in (i) and (iii). The left-hand side can be viewed as the distance to a set, and the right-hand side defines the elements of to which is closest. The discussion below uses such . For a model which is not indexed by , if there is such that, for a constant , for large enough, , then converges to such . It will become apparent from the lower bounds on that these are usually sparse vectors in . When are coefficients of a function on a collection of simple functions and increases with , due to (iii), can converge to the coefficients of a smooth function and the population sensitivities vary with . It is typically the case in nonparametric IV that the coefficients decay rapidly to zero (see Example NP continued below).

Remark 3.2.

We now discuss rates of convergence based on the bounds in Theorem 3.1, which depend on the population sensitivities. For ease of exposition we focus on explaining (i). Proposition A.2 relates the population sensitivities to one another, so we start by considering the following alternative expression for for all ,

| (18) |

which has a natural interpretation as a measure of the strength of the IVs for the regressors in . If the IVs are centered, the second minimum in (18) is a maximum absolute normalized partial covariance between regressor and the IVs, where the partialling-out of the other regressors is restricted (i.e., is constrained). Ignoring for the moment the constraints on , the second minimum in (18) is zero if lies in a vector space of dimension at most of Lebesgue measure zero if . The vector space has a smaller maximum dimension for . This contrasts with the restricted and sparse eigen and singular values (see [11, 3]) which can be zero even if (else are always zero) and depend on only via its size.

For simplicity of exposition we now use Condition IC (see the appendix for the general case), under which we provide interpretable conditions to derive explicit rates.

Condition IC. and is a constant such that .

Under Condition IC, by Proposition A.2, we have, for all and ,

| (19) | |||

| (20) |

where . Due to the form of and (19), the upper bound in Theorem 3.1 (i) and (ii) is finite if

| (21) |

Sufficient conditions for consistency can be obtained based on the easier to interpret . If (as when both are ), we can further interpret the expression of in (18) due to the constraints on . The constraints (20), , and imply that the subvector of appearing in has -norm . Also, if , the subvector with indices in has -norm larger than and -norm smaller than 1. This restricts the set of vectors used to perform the partialling-out to have mass at most , predominantly concentrated on (e.g., ). Moreover, by Proposition A.2 (v)

| (22) | ||||

| where | ||||

Assumption C. Condition IC holds, , satisfies Assumption A.1, , and

-

(i)

for all if (resp. for all if ), ,

-

(ii)

for large enough,

-

(iii)

if , else .

Corollary 3.1.

Let , , and . For all satisfying Assumption C, , and any STIV estimator, we have, for large enough,

| (23) |

Taking and yields rates for the -loss and upper bounds on in Theorem 3.1 (ii) (see also (A.7)). For simplicity, the discussion now uses the word ‘correlation’ as if the IVs and/or regressors were mean zero. Assumption C() (i) means that for regressor there exists a nonempty set of linear combinations of the IVs of small enough relative absolute correlation with the other regressors. It is similar to the coherence condition for symmetric matrices of [21], but more general because it allows for rectangular matrices and linear combinations of the IVs (i.e., rather than for ). The coherence condition is used to study -norm convergence rates and model selection in [34]. Item (ii) is introduced to guarantee (21) and (iii) for consistency. They require that for each regressor of index (but not for the other regressors), there is a linear combination of the IVs, which does not need to be known, of large enough absolute correlation with . If then, by (iii), (ii) holds for all for large enough. Consistency can hold with .

Remark 3.3.

Assume is fixed, we add to Assumption C that, for all , contains the vectors from the canonical basis of with a 1 at the indices of the largest entries in absolute value of , and where does not vary with . STIV is consistent when , where . Assume , so the IVs are equally relevant. If then STIV is consistent if . Like 2SLS, it may not be consistent if converges to a nonzero constant. When but , 2SLS is consistent (see [16]) but STIV may not be. If then, for each relevant regressor, all but one of the IVs can be arbitrarily irrelevant and STIV is consistent when with .

Remarkably, for , (23) is not affected if all IVs are irrelevant for an irrelevant regressor. This is important to handle ill-posed inverse problems such as the following.

Example NP continued. Assume the baseline endogenous regressor and IV are related via and the approximating functions are and for , where is the Hermite polynomial. If, for simplicity, follows a standard normal distribution, is diagonal with (see Section O.1.2), so the -rate depends on the exponentially small for the largest . Due to Theorem 3.1 (iii), a bound on the -rate without sparsity is

| (24) |

Assumption C (i) is in line with the common empirical practice of, for each endogenous regressor, finding an IV which is correlated more specifically with that regressor, and arises naturally in our application. To obtain adaptive nonparametric estimators in statistical inverse problems using series, it is common to use basis functions adapted to the operator so that is (nearly) diagonal (see, e.g., [28] and [25] in conjunction with wavelet/needlet thresholding and Galerkin approximation), and so Assumption C (i) is not restrictive.

For the sake of comparison, we present an assumption similar to that in [3].

Assumption SV. Condition IC holds, , satisfies Assumption A.1, , and

-

(i)

is an integer smaller than and

(25) where and are respectively the smallest and largest singular values of and is the submatrix obtained by extracting the rows in and columns in ,

-

(ii)

,

-

(iii)

.

By adapting the proofs to apply to population sensitivities and all , we obtain

Corollary 3.2.

Let , , , , and . For all satisfying Assumption SV, and any STIV estimator, we have

| (26) |

For , plays the same role as under C. Item (ii) guarantees (21) and (iii) gives consistency. Assumption SV can be more appealing than C (i). However, can be small (even 0) due to one irrelevant regressor. For example, suppose there is such that . Taking in the first inequality of (25), , hence (unlike (23)) the upper bound in (26) does not converge to 0. The fundamental issue is that Assumption SV provides a rate based on the worst-case subset of regressors, regardless of their relevance. This is less costly for regression (i.e., ) than for IV because exogenous regressors have higher correlation with the IVs than do endogenous regressors, and given many endogenous regressors it is likely that one is weakly correlated with the IVs.

Example NP continued. The bound on the rate in (26) is while is replaced by under Assumption C.

3.3.2. Selection of Variables and Confidence Sets with Estimated Support

Theorem 3.1 (ii) provides a superset of the relevant regressors. Under a stronger beta-min condition exact selection can be performed. For this purpose, we use a purely data-driven thresholded STIV estimator which uses a sparsity certificate. It is defined by

| (27) |

for . The following theorem shows that this estimator achieves sign consistency and hence, for all . It uses , where , and makes use of the population counterparts, for all ,

Theorem 3.2.

Let and be such that Assumption A.1 holds. For all such that and any STIV estimator, we have, on , .

Example SE continued. By Theorem 3.2, the peers are exactly recovered with asymptotic probability at least if the endogenous effects are sufficiently large.

Theorem 3.2 yields a confidence set by replacing by in (15), which satisfies (16) with in place of . The value of can be large (possibly ). The set’s width matches the error bound in Proposition 3.1 with respect to , hence it adapts to the sparsity. To achieve this we remove a small set from (vectors too close to -sparse vectors).

4. Confidence Bands using Bias Correction

Confidence sets for , where , can be robust to identification and are particularly useful when one is interested in a feature of the whole parameter vector such as the network in Example SE. But they can be conservative when stronger assumptions on the data generating process can be maintained and is small relative to . The confidence bands below address this. Using yields a confidence interval (e.g., for the average peer effect in Example SE). Using one can build a confidence band for a structural function such as in Example NP or the Engel curves in Section 6.2. A first estimator is the plug-in . Another uses

| (28) |

Indeed, by (1), for all and which solves (28), . (28) is a system of equations of the same form as the following equation derived from (1)

| (29) |

A STIV estimator is obtained by solving (31). For simplicity, we assume (28) holds exactly but, as in Section 6.2.1, one can handle an approximation error going to zero with .

Using either plug-in strategy poses problems because STIV is ”biased” towards zero and can converge slowly. To deal with this we combine the two to form the bias corrected estimator

| (30) |

and build a confidence band around .

Remark 4.1.

(30) is close in spirit to the bias correction in [29]. Another motivation for it is that has zero partial derivatives at, respectively, identified and (due to (28) and (29)) and . This is a type of double-robustness (see [17]). In this paper appears in a structural equation and our analysis does not involve machine learning for regressions.

Definition 4.1.

To choose , one uses one of classes 1-3, replacing by and by . If and , is an approximate inverse of , which improves on the CLIME estimator of [12] by estimating standard errors. BC-STIV differs from STIV in that it is for a system of (rather than 1) equations, each with (rather than 1) second-order cones, making it more computationally intensive. We provide a computational solution and its analysis in Section A.1.2. The counterpart of is , where is a class for the distribution of . Asymptotically uniformly valid confidence bands are obtained as

| (32) |

where is the quantile of given (obtained by simulation), , is a standard Gaussian vector independent of , and is a positive sequence.

Theorem 4.1.

The sequence restricts and on which uniformity over distributions and parameters holds. We denote by (resp. ) the deterministic upper bound on (resp. on , see Proposition A.3), where is the maximum row-wise -norm. These bounds hold on an event of probability at least , where is defined in Assumption A.2, converging to one, and and can depend on . Proposition A.3 is the analogue of Theorem 3.1. It provides deterministic upper bounds for useful losses and characterizes the limit of when there are multiple solutions to (28), as discussed for in Remark 3.1.

For the discussion, we now take (e.g., ), to which converges, and assume and are uniformly bounded. Assumption A.3 holds if

| (33) |

The requirement on is mild. It can be logarithmic if is of polynomial order in . When (i.e., a confidence interval) and we use , we can obtain similar upper bounds on as on under Condition IC in Section 3.3 because the set used to analyze is equal to the set in (20), replacing by and by . The key difference is that and switch roles and is replaced by in assumptions C and SV for . So plays the role of under sparsity, and otherwise bounds in the spirit of (24) can be derived under approximate sparsity. The requirement on is also mild if the rows of are (approximately) sparse. For example, if , is of order at most . Hence, if grows slowly the rate of estimation of could also be logarithmic. We provide alternative confidence bands under conditional homoscedasticity and their analysis in Section O.1.5.

5. Endogenous IVs

With many endogenous regressors and IVs, the exogeneity of some IVs could fail. We now consider a high-dimensional framework for the problem of IV exogeneity (see, e.g., [37]). Introducing to account for the possible failure of (1), we replace (1)-(2) by

| (34) | |||

| (35) |

where means that is endogenous, is the distribution of implied by and encodes restrictions on . For example, the sign of the correlation of a regressor and the structural error could be known. Another restriction is for of cardinality which indexes the IVs known to be exogenous. The counterpart of , denoted by , collects the vectors which satisfy (34)-(35), , and , where is a sparsity certificate for the possibly endogenous IVs.

To detect endogenous IVs, we use a variant of STIV to estimate by replacing by the residuals from a pilot STIV estimator which uses only the IVs in and (in place of ) based on , which differs from by using only moments and (in place of ). Based on STIV, one then computes and such that for all such that , on

| (36) | ||||

| (37) |

Though the analysis does not require the sparsity certificate approach, if we can use

| (38) |

where the lower bound on , the sensitivity for the loss in the first inequality of (36),222The sensitivities of the pilot STIV replace (resp. ) by (resp. ) in (9) (resp. in in (10)). is obtained by linear programming. Unlike the Hansen-Sargan test, we can use a pilot STIV estimator when and with an approximately sparse reduced form.

Definition 5.1.

For , a NV-STIV estimator is any solution of

| (39) |

where, for ,

To set to control (see (A.9)), we use one of classes 1-3, replacing by and by . in (35) combines the classes for and . For deterministic bounds, it is further restricted using a minor modification of Assumption A.1 and we modify the event of probability accordingly (see Section A.1.3). We still refer to them as Assumption A.1 and in Theorem 5.1. Also, for a function from to and given , we set . The definitions of and used below are in Section A.1.3 and .

Theorem 5.1.

For all and , such that , and and any NV-STIV estimator, we have, on ,

| (40) |

For fixed , , and , if we restrict so that Assumption A.1 holds, then, for all , if , then . If , then , where on . Setting to , we have .

The first statement of Theorem 5.1 provides a confidence band based on (40). As for the STIV set in (11), uniformity in and permits intersection over a grid. As in Example SE in Section 3.2, it provides such that . The second statement of Theorem 5.1 concerns model selection. If the endogenous IVs induce a large enough violation of (1) then either superset or exact recovery of is achieved. We provide NV-STIV rates of convergence in Section A.1.3. The C-STIV in Section O.1.4 is an extension estimating simultaneously and allowing for unknown .

6. Inference In Practice

6.1. Monte-Carlo

We study model (1)-(2) with and , set and let be a standard Gaussian vector in . The exogenous regressors are the first IVs. For an endogenous we set where and . We let be a mean zero Gaussian vector in with variance having entries .05 but in the diagonal where the first entry is 1 and the others are .

| p2.5 | p50 | p97.5 | p2.5 | p50 | p97.5 | p2.5 | p50 | p97.5 | p2.5 | p50 | p97.5 | |

| 0.8 | 0.88 | 0.95 | 0.74 | 0.82 | 0.91 | 0.67 | 0.78 | 0.88 | 0.27 | 0.55 | 0.78 | |

| -1.9 | -1.83 | -1.75 | -1.9 | -1.83 | -1.75 | -1.9 | -1.82 | -1.74 | -1.89 | -1.81 | -1.73 | |

| -0.41 | -0.33 | -0.26 | -0.41 | -0.33 | -0.26 | -0.41 | -0.33 | -0.26 | -0.41 | -0.32 | -0.25 | |

| 0.01 | 0.08 | 0.16 | 0.01 | 0.08 | 0.16 | 0 | 0.08 | 0.16 | 0 | 0.08 | 0.16 | |

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| 1 | 1.05 | 1.1 | 1.01 | 1.06 | 1.12 | 1.02 | 1.07 | 1.13 | 1.05 | 1.12 | 1.2 | |

| 0.15 | 0.2 | 0.25 | 0.16 | 0.21 | 0.27 | 0.17 | 0.23 | 0.33 | 0.23 | 0.45 | 0.73 | |

| 0 | 0 | 0.03 | 0 | 0 | 0 | 0 | 0 | 0.03 | 0 | 0.17 | 0.39 | |

| .98 | .98 | .98 | .96 | |||||||||

| .62 | .95 | .91 | .06 | |||||||||

| 0 | 0.79 | 0.96 | 0 | 0.78 | 0.96 | 0 | 0.79 | 0.98 | 0 | 0.8 | 0.98 | |

| -1.93 | -1.83 | -1.5 | -1.91 | -1.83 | -1.48 | -1.9 | -1.83 | -1.47 | -1.93 | -1.83 | -1.49 | |

| -0.39 | -0.32 | 0 | -0.4 | -0.34 | 0 | -0.4 | -0.34 | 0 | -0.4 | -0.33 | 0 | |

| 0 | 0.08 | 0.18 | 0 | 0.07 | 0.18 | 0 | 0.08 | 0.16 | 0 | 0.07 | 0.15 | |

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| 1 | 1.09 | 3.3 | 0.99 | 1.09 | 3.42 | 0.99 | 1.08 | 3.4 | 0.98 | 1.08 | 3.38 | |

| 0.15 | 0.24 | 1 | 0.15 | 0.23 | 1 | 0.15 | 0.23 | 1 | 0.15 | 0.24 | 1 | |

| 0 | 0.02 | 0.42 | 0 | 0.02 | 0.43 | 0 | 0.02 | 0.45 | 0 | 0.02 | 0.43 | |

| .82 | .82 | .80 | .78 | |||||||||

| .49 | .45 | .47 | .46 | |||||||||

| Notes: 1000 replications. . | ||||||||||||

We set so that for and , hence all regressors have unit variance. Since the IVs are uncorrelated with one another, the concentration matrix has diagonal elements close to and the degree of endogeneity is (see [1]). In low dimensions the IVs could be considered strong. However, the first-stage is not approximately sparse so even a first-stage Lasso would not be consistent (so it is impossible to estimate the concentration matrix and apply a method akin to 2SLS) and most of the IVs are weakly correlated with the endogenous regressors. We take . For the remaining entries we set

This means that there is one stronger IV and weaker IVs for each endogenous regressor. Though each weaker IV accounts for a small fraction of their variance, collectively the weaker IVs account for fraction . If each IV has a stronger correlation with one regressor.

| STIV | SC 4 | SC 5 | SC 6 | SC 10 | ES | Bias-corrected STIV | CB | |||||

| p2.5 | p50 | p97.5 | Median width/2 | p2.5 | p50 | p97.5 | Width/2 | |||||

| 0.9 | 0.95 | 0.99 | 0.8 | 1.02 | 1.32 | 6.07 | 0.33 | 0.94 | 1 | 1.06 | 0.1 | |

| -1.95 | -1.9 | -1.85 | 0.58 | 0.73 | 0.94 | 4.55 | 0.26 | -2.04 | -1.99 | -1.95 | 0.07 | |

| -0.45 | -0.4 | -0.36 | 0.57 | 0.73 | 0.94 | 4.64 | 0.26 | -0.54 | -0.49 | -0.45 | 0.07 | |

| 0.11 | 0.15 | 0.19 | 0.57 | 0.73 | 0.95 | 4.65 | 0.26 | 0.2 | 0.24 | 0.29 | 0.07 | |

| 0 | 0 | 0 | 0.8 | 1.02 | 1.31 | 6.03 | 0 | -0.05 | 0 | 0.06 | 0.1 | |

| 0 | 0 | 0 | 0.57 | 0.73 | 0.95 | 4.62 | 0 | -0.04 | 0 | 0.04 | 0.07 | |

| 1 | Cover | 1 | 1 | 1 | 1 | .98 | .94 | |||||

| .98 | (.996,1) | (.97,.98) | (.92,.95) | |||||||||

| 0.84 | 0.9 | 0.96 | 0.24 | 0.94 | 0.99 | 1.05 | 0.07 | |||||

| -1.96 | -1.91 | -1.87 | 0.2 | -2.04 | -2 | -1.95 | 0.07 | |||||

| -0.47 | -0.43 | -0.39 | 0.2 | -0.54 | -0.5 | -0.46 | 0.07 | |||||

| 0.13 | 0.18 | 0.23 | 0.2 | 0.2 | 0.25 | 0.3 | 0.07 | |||||

| 0 | 0 | 0 | 0 | -0.03 | 0.02 | 0.08 | 0.1 | |||||

| 0 | 0 | 0 | 0 | -0.04 | 0 | 0.04 | 0.07 | |||||

| 1 | Cover | 1 | 1 | 1 | 1 | 1 | .93 | |||||

| .96 | (.996,1) | (.91,.95) | ||||||||||

| 0.98 | 1.02 | 1.07 | 1.55 | 2.31 | 3.78 | 0.43 | 0.92 | 1 | 1.07 | 0.12 | ||

| -1.95 | -1.9 | -1.86 | 0.85 | 1.26 | 2.08 | 0.27 | -2.04 | -1.99 | -1.95 | 0.07 | ||

| -0.45 | -0.4 | -0.36 | 0.86 | 1.27 | 2.1 | 0.27 | -0.54 | -0.49 | -0.45 | 0.07 | ||

| 0.11 | 0.16 | 0.2 | 0.85 | 1.26 | 2.08 | 0.26 | 0.2 | 0.24 | 0.29 | 0.07 | ||

| 0 | 0.03 | 0.07 | 1.56 | 2.32 | 3.78 | 0 | -0.07 | 0 | 0.07 | 0.12 | ||

| 0 | 0 | 0 | 0.85 | 1.26 | 2.1 | 0 | -0.04 | 0 | 0.04 | 0.07 | ||

| 1 | Cover | 1 | 1 | 1 | 1 | .75 | .95 | |||||

| .13 | (.996,1) | (.72,.77) | (.93,.96) | |||||||||

| 1 | 1.05 | 1.09 | 0.31 | 0.99 | 1.03 | 1.08 | 0.03 | |||||

| -1.97 | -1.93 | -1.88 | 0.2 | -2.04 | -1.99 | -1.95 | 0.07 | |||||

| -0.47 | -0.42 | -0.38 | 0.2 | -0.54 | -0.49 | -0.45 | 0.07 | |||||

| 0.13 | 0.18 | 0.22 | 0.2 | 0.2 | 0.25 | 0.29 | 0.07 | |||||

| 0 | 0.05 | 0.09 | 0 | -0.03 | 0.03 | 0.09 | 0.1 | |||||

| 0 | 0 | 0 | 0 | -0.04 | 0 | 0.04 | 0.07 | |||||

| 1 | Cover | 1 | 1 | 1 | 1 | 1 | .50 | |||||

| .02 | (.996,1) | (.47,.53) | ||||||||||

| Notes: 1000 replications. ‘SC ’ use sparsity certificate . ‘ES’ use estimated support. ‘CB’ use . SC/ES use one grid point for . For (resp. 2050) (resp. 0.094). ‘STIV’ uses . For SC/ES (resp. CB) ‘Cover’ is the frequency with which lies in the bounds defined in (13) (resp. (32)). 0.95 confidence intervals for the coverage are in parentheses (see [41]). | ||||||||||||

We construct 0.95 confidence sets and bands for . For sets we use from Class 3 with and set 333This is possible under Assumption O.1, which permits rather than , delivering a smaller value of , which we find works better in practice.. We consider sparsity certificates . is a singleton for each sparsity certificate and below. We construct the bounds in (13), replacing with a grid, the construction of which is discussed below. For computational reasons (to allow sufficiently many replications) we limit the grid to at most two points. Using more points (and/or loss functions) could lead to narrower sets. We follow the same approach to construct the confidence set in (15) based on an estimated support, taking equal to the first grid point and to be the indices of the elements of with absolute value larger than . For the confidence bands we use STIV for the pilot and Class 4 to set . Since the IVs are uncorrelated, the values of for classes 3 and 4 are nearly identical. We use the STIV estimator with for the pilot and set and use Class 3 to estimate .

| STIV | SC 4 | SC 5 | SC 6 | SC 7 | SC∗ 7 | SC 10 | ES | |||

| p2.5 | p50 | p97.5 | Median width/2 | |||||||

| 0.87 | 0.91 | 0.94 | 0.65 | 1.08 | 2.66 | 97.7 | 0.22 | |||

| -1.96 | -1.93 | -1.90 | 0.40 | 0.59 | 1.29 | 42.84 | 0.17 | |||

| -0.46 | -0.43 | -0.39 | 0.40 | 0.60 | 1.29 | 42.51 | 0.17 | |||

| 0.14 | 0.18 | 0.21 | 0.40 | 0.59 | 1.29 | 41.89 | 0.17 | |||

| 0 | 0 | 0 | 0.65 | 1.09 | 2.68 | 97.37 | 0 | |||

| 0 | 0 | 0 | 0.40 | 0.60 | 1.29 | 43.32 | 0 | |||

| 1 | Cover | 1 | 1 | 1 | 1 | 1 | 1 | .97 | ||

| .99 | (.98,1) | (.94,.99) | ||||||||

| 1.02 | 1.05 | 1.08 | 3.52 | 18.64 | 0.65 | |||||

| -1.96 | -1.93 | -1.90 | 1.56 | 7.02 | 0.4 | |||||

| -0.46 | -0.43 | -0.4 | 1.57 | 6.97 | 0.4 | |||||

| 0.15 | 0.18 | 0.21 | 1.55 | 6.99 | 0.4 | |||||

| 0.02 | 0.05 | 0.08 | 3.58 | 19.18 | 0 | |||||

| 0 | 0 | 0 | 1.57 | 7.05 | 0 | |||||

| 1 | Cover | 1 | 1 | 1 | 1 | 1 | 1 | .97 | ||

| .01 | (.98,1) | (.94,.99) | ||||||||

| Notes: 200 replications. ‘SC ’ use sparsity certificate . ‘ES’ use estimated support. ‘CB’ use . SC/ES use one grid point for . .‘STIV’ uses . ‘Cover’ is the frequency with which lies in the bounds defined in (13). †: The frequency of replications with sets of finite width is 0.03. ∗: Sets using two grid points for . | ||||||||||

| NV-STIV | SC 4,1 | SC 4,2 | SC 4,3 | SC 4,5 | SC 4,7 | SC 4,10 | |||

| p2.5 | p50 | p97.5 | Median width/2 | ||||||

| 0.55 | 0.6 | 0.65 | 0.53 | 0.53 | 0.53 | 0.53 | 0.54 | 0.54 | |

| 0 | 0 | 0 | 0.53 | 0.53 | 0.53 | 0.53 | 0.54 | 0.54 | |

| 1 | Power | .95 | .94 | .94 | .93 | .92 | .91 | ||

| 1 | (.93,.96) | (.92,.95) | (.92,.95) | (.91,.94) | (.9,.93) | (.89,.92) | |||

| Notes: 1000 replications. ‘SC ’ use sparsity certificates . SC use one grid point for . is from Class 3 with , and . is from Class 3 with . Confidence sets use a grid of 19 points for . ‘NV-STIV’ uses . ‘Power’ is the frequency with which the confidence sets do not include . | |||||||||

Rule of Thumb for . We apply STIV with , corresponding to the least shrinkage. As decreases STIV is almost unchanged, until a point after which increases discontinuously. We recommend this for a single value of . As decreases further, STIV is almost unchanged until a point after which there is another increase in . This gives a second grid point, and so on. This rule means that we take the smallest (yielding the largest sensitivities) for each .

Estimation. We consider the challenging setting with . We set , and and , hence there are 250 endogenous regressors. Table 2 reports the results. For sufficiently large , STIV performs well in terms of selecting nonzero entries, and does not select those with values of zero. Due to the shrinkage, STIV is biased towards zero with bias decreasing in .

Confidence Sets and Bands. We set , , , and make inference on . This design is challenging since there are two endogenous regressors and either or . We limit so as to permit application of all of our methods to the same design over 1000 replications. Below we modify the design to allow for .

Table 3 reports the results. Sets based on a sparsity certificate are nested. If , they can be informative on the sign of the first three entries of . Though robust to identification, the sets can be conservative, are infinite if and have coverage close to 1 if . STIV performs well in selecting the nonzero parameters, resulting in less conservative sets based on estimated support. These are narrower than with sparsity certificate as they use information on both the number and identities of relevant regressors. Coverage is below 0.95 when and because STIV using the rule of thumb value of can fail to distinguish from zero. In the other designs, the sets can be informative on the signs of the first three entries of . The bias correction reduces the shrinkage and centers STIV on . For , there exists a sparse verifying (28), with nonzero entries out of . The bands are narrower than the sets but have coverage slightly below 0.95 due to shrinkage when estimating . For , there does not exist verifying (28), leading to coverage below 0.95, significantly so for .

Confidence Sets with . We set , , and . Bands are infeasible since requires second-order cones. Table 4 reports the results. If , sets using a small sparsity certificate are informative on the signs. For , the set is infinite if one grid point over is used but finite with two. STIV performs well in terms of selection, translating into narrower sets based on estimated support. Reducing the strength of the IVs () increases the width of the sets but coverage remains above 0.95.

Endogenous Instruments. We take , , and . There are 10 possibly endogenous IVs with indices and is endogenous, where is an independent standard Gaussian. This preserves the variance of but implies that has one nonzero entry given by . There are as many known exogenous IVs as regressors. We apply the NV-STIV estimator, using STIV for the first stage and taking from Class 3 with and . For the NV-STIV estimator we take from Class 3 with . As both stages use we construct 0.95 sets. We use sparsity certificates for and for . The sets are intersected over a grid of points for . Table 5 reports results. Due to shrinkage, NV-STIV is centred on 0.6. The endogenous IV is detected with frequency 0.95 for and 0.91 for .

6.2. EASI Demand System

The EASI demand system of [33] implies the vector of expenditure shares for goods consumed by a household satisfies

| (41) | |||

| (42) |

where is nominal expenditure, is deflated expenditure, is log-prices, is household characteristics, and are structural errors. Log-prices are normalized to be zero for a subset of households. The parameters are for , and . Theory imposes restrictions such as (1) expenditure shares sum to one and (2) Slutsky symmetry, hence

| (43) |

Because depends on the parameters, the system (41) is nonlinear, so difficult to estimate. [33] propose an approximate system, replacing with its first-order in prices approximation , which is nominal expenditure deflated by a Stone price index. To reduce approximation error, we consider a second-order approximation and inject

| (44) |

(derived from (42)) into (41). An approximation error arises due to the second term in (44), but it is small due to the normalization on log-prices. Our approximation depends on products of parameters, violating linearity. We replace each by a new parameter, restricted using (43).

6.2.1. Systems with Approximation Error

Our results can be applied to estimate the system one equation at a time, ignoring cross-equation restrictions and approximation error. This does not make proper use of the underlying economic theory and would not allow a comparison with [33]. For this reason, we make some minor modifications to STIV. We allow for an approximation error by adding an additional (unobserved) term to the structural equation such that . The practical implication is a minor modification to the IV-constraint, replacing with in (7), where decays to zero with . This allows for other models with approximation error including nonparametric IV (e.g., Example NP with approximation error) or when a fraction of the data is bracketed (in which case is random). To allow for a system of equations, the STIV objective function is summed and the IV-constraint is intersected over the equations, and is replaced by . The latter allows the structural errors to be dependent across equations, and can depend on . The bias correction and confidence bands are easily modified, and we also allow for approximation error in (i.e., the function of interest is approximately linear). Further details and analysis are provided in Section A.1.4.

6.2.2. Implementation and Results

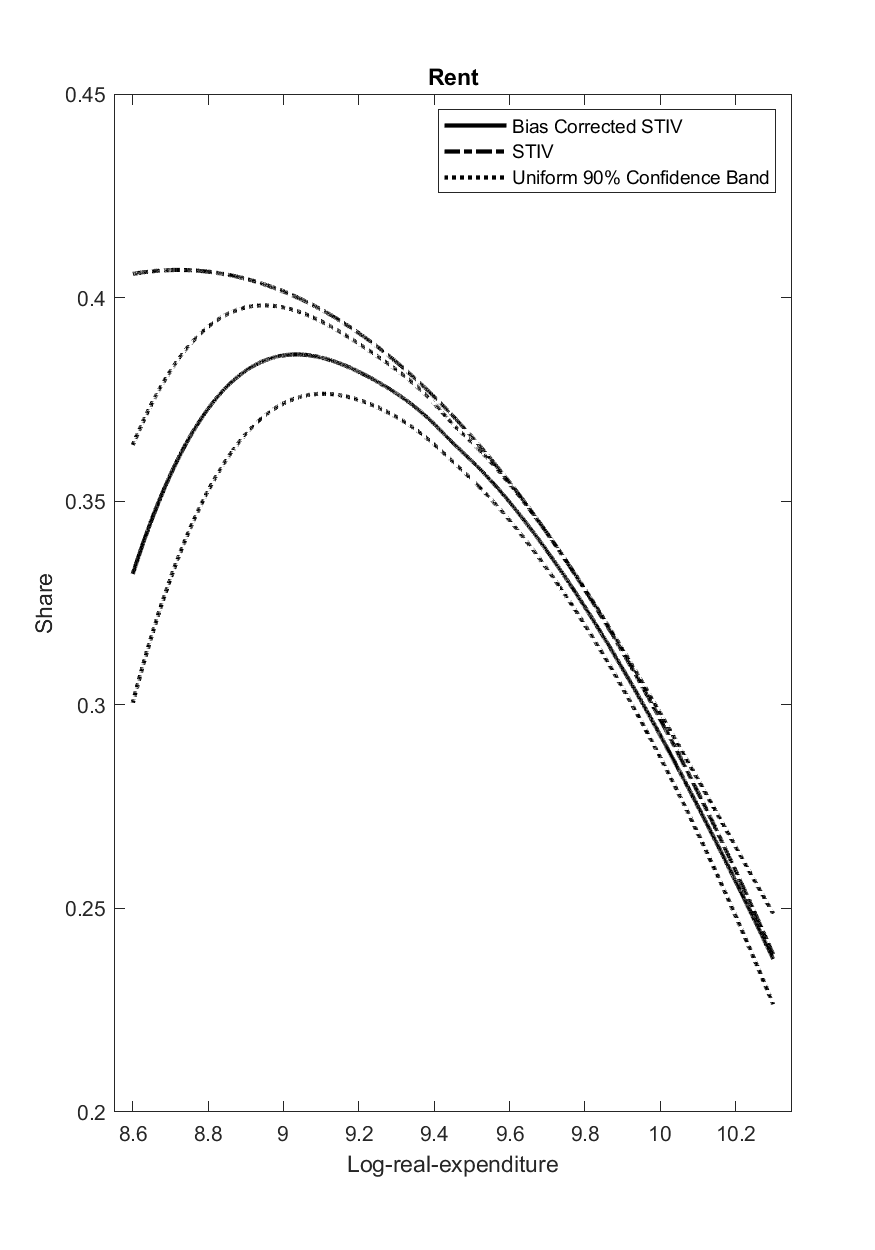

We use the Canadian data of [33] for rental-tenure single-member households with expenditure on rent, recreation and transportation. The goods are: food consumed at home, food consumed out, rent, clothing, household operation, household furnishing/equipment, transportation operation, recreation, and personal care. Individual characteristics are: age, gender, a dummy for car nonownership equal to one if real gasoline expenditure (at 1986 prices) is less than $50, a social assistance dummy equal to one if government transfers are greater than 10 percent of gross income, and a linear time trend. Following [33], we use for the degree of the expenditure polynomial. Each equation has parameters. Log-prices are normalized to zero for residents of Ontario in 1986. The approximation error from the second order approximation is likely small because . In contrast, , and the mean share for 5 goods is less than 0.1, suggesting a large first-order approximation error. Since depends on , the regressors which depend on are endogenous. We construct IVs by replacing by (i.e., replacing individual by average shares).

The IVs are strong and and so we apply Section 4 to construct uniform 0.9 confidence bands for the Engel curves based on grid points. In the first step, we apply STIV, adjusting according to Class 4, taking , and for all . We choose to exempt the constant, linear, and quadratic parts of the Engel curves () and the linear price parameters () from the penalty. It is reasonable to expect that the rest of the parameter be approximately sparse, particularly for the second-order approximation terms.

For brevity, we do not present in full because it has elements. Instead, we summarize its support. Of parameters in , only 47 are estimated as nonzero, 22 of which are due to the second-order approximation. To build confidence bands for Engel curves, we obtain using from Class 3 with and . Figure 1 depicts the preliminary estimator for rent, its bias corrected counterpart and confidence bands. The second-order approximation yields a different curve to the that of [33], which peaks at a higher expenditure level. The bias correction is large as the preliminary estimator lies outside the band. The band is wider at the end points, most likely due to lack of data. Engel curves for the remaining goods are available on request. The bias correction is large for household operation, clothing, personal care and transportation operation. The bands are marginally wider than those of [33] because we construct uniform bands rather than pointwise intervals and use a more flexible second-order approximation.

Appendix

A.1. Complements

The proofs of the results below are in Section O.2. We denote by , , and (resp. ) the quantile function of (resp. of given ). When a random vector is a function of an estimator as in , is still used to denote .

A.1.1. Complements on Section 3

Proposition A.1.

Let , , and . For all , , and ,

-

(i)

If , ;

-

(ii)

;

-

(iii)

, ;

-

(iv)

,

where and if and else and .

We emphasize 3 more baseline classes which we further restrict when need be. Some confidence sets require very mild assumptions on while deterministic bounds require working within subsets of these classes.

The baseline classes are identification robust because they do not restrict the joint distribution of . Let, for ,

be the diagonal matrix with positive diagonal elements for , where , , . The value of for classes 1-3 is obtained using a union bound and the results in [35, 8, 30].

Class 2:

and . We set

.

Class 3:

There exists in and such that

and

.

We set

.

Here and , where is an unknown universal constant, is a finite sample bound on coverage error. For classes 1 and 2, , so we set . For classes 3-4, (12) is modified to replace by .

We use concentration arguments which involve for (Theorem 2.2 in [23]). For random and and sequences , , and which can depend respectively on , , and , denote by

-

(N.i)

,

-

(N.ii)

,

-

(N.iii)

,

, , and . When depends on or but we omit it from the definition of and , it means that the same sequence is used for all , hence restricting . When in (N.iii) is a matrix, everything holds for the vectorization.

Taking yields . Assumption O.1 permits to work with the smaller . The union bound used for in classes 1-3 does not account for dependence over of , and so can be larger than necessary. To account for dependence, we consider Class 4 presented in Section O.1.1 under which where and . Section O.1.1 also points to useful results for dependent data.

We now provide probabilistic conditions under which we can replace random quantities appearing in the right-hand sides in Proposition 3.1 by deterministic ones. These are , , and the sensitivities. For classes 1-3 we set

| (A.1) |

and, for Class 4, is defined in Section O.1.1 and . for all , . We further restrict the class and add:

Assumption A.1.

If is sub-Gaussian, can be proportional to , where the constants and of proportionality depend on tail parameters of the sub-Gaussian distribution. Section O.1.1 presents the adjustments for classes 1-3 with assumptions A.1 and O.1.

The population counterparts of and replace in by , which we denote by :

| (A.3) | ||||

Lemma A.2.

On the event , we have, for all ,

| (A.4) | |||

| (A.5) |

where is the population analogue of . Under Assumption A.1, for classes 1-4, we have .

Proposition A.2.

We have, for all , , and ,

-

(i)

,

-

(ii)

, ,

-

(iii)

under Condition IC,

-

(iv)

,

-

(v)

if ,

-

(vi)

and ,

where and if , else and .

Moreover, if then

| (A.6) |

The above statements hold if we replace by and by , the definition of which is the same but replacing by and by . We also have .

A.1.2. Complements on Section 4

Estimation of is more computationally intensive than STIV because there are second-order cones (STIV has 1). For STIV we use the MOSEK solver, but if and are very large, MOSEK can fail. For this reason we use an iterative procedure, which alternates between updating and . Updating is more computationally demanding, so we apply FISTA with partial smoothing ([1, 2]). Details are in Section O.1.4.

We now analyze , which is a special case of the C-STIV estimator presented in Section O.1.4, applied to a system of equations. We also allow for approximation error, as in Section A.1.4. We denote by and

The cones used to establish the rate of convergence of are sets of such that

where follows the obvious modification to our notation in which one sums the absolute values of the entries of . We use to denote the population sensitivities using the cones above defined identically to , replacing by . Since can have more than one column, we use the operator norm from to which we denote by . We denote the population sensitivities for those losses by . We also define as replacing (resp. ) by (resp. ) and the distribution of .

Assumption A.2.

Let , , , , , such that , , and and a prior value of the parameter of Class , such that, for all such that : , and ,

Proposition A.3.

We denote by and the upper bounds on the right of (i) and (ii) (taking for , in Section O.1.5, and multiplying both sides by in case (ii)) which can depend on . For coverage guarantees we use:

Assumption A.3.

is such that Assumption A.2 holds and, for all , we have

-

(i)

;

-

(ii)

;

where , , , is obtained like for Class 1 replacing by and by , and

The coverage result that we obtain is more general than stated in Theorem 4.1. It is for approximately linear functions for and is stated as

We provide analysis under conditional homoskedasticity in Section O.1.5.

A.1.3. Complements on Section 5

We denote by , , and

| (A.9) |

We modify Assumption A.1 by replacing by and adding , (N.iii) for and , and . Theorems 5.1 and A.1 use vectors of functions which have as arguments and we denote the evaluation using 4 arguments. The population sensitivities and their lower bounds replace (resp. ) by (resp. ), is defined in Lemma A.2, and is defined similarly from .

Theorem A.1.

Let , , , and . If is such that Assumption A.1 holds then, for all such that , and any NV-STIV estimator, on ,

| (A.10) |

where , , and .

By (N.ii) for (which is part of Assumption A.1) and the computations in (O.30), on , . Recall also that under Condition IC, otherwise it depends on the LP used to compute . For the second statement in Theorem 5.1, is obtained by replacing and in the definition of by their deterministic upper bounds. For we use . The deterministic upper bounds on and hold on and are obtained using Lemma O.2.

A.1.4. Systems of Equations with Approximation Errors

To allow for approximation error we use and suppose that (1) holds with in place of and is a small approximation error, for which we assume that , for decaying to zero with . The assumptions previously made on are made on and is modified accordingly and incorporates . The model with approximation errors allows for the structural equation

| (A.11) |

where , and for functions and a decreasing sequence ,

| (A.12) |

The rate of decay of is usually taken slow so can be large. It corresponds to minimum smoothness but can lie in a class of smoother functions. The model with approximation error involves , , and . is the error made by approximating the function in the high-dimensional space, and for large enough. For well chosen classes and functions , the vector is approximately sparse. We use IVs which are functions of .

We consider a system where , , , , and for all . This is the setup of Section 6.2 where is used in all equations. Else, a simple modification applies. We now define:

Definition A.1.

For , the E-STIV estimator is any solution of

| (A.13) |

where, setting for all and , ,

For a nonparametric model (A.11) one can take . The E-STIV can also be used when, for , the outcomes are bracketed. Then, we let for be the observed outcome and , while, for , is the midpoint of the bracket. One has , where are half-widths of the brackets, and we let and . With equations, we allow for cross-equation restrictions, and the number of equations can depend on . The E-STIV estimator is used in Section 6.2.

To allow for approximation error, we modify so that plays the role of . For simplicity we only analyze classes 1-3. We choose and as in Section A.1.1 replacing by and use and is defined in Section A.1.1 replacing by , where the probability in the definition of is replaced by . The population sensitivities are obtained replacing by , and by and where the right-hand side is , , and replaces in the sensitivities.

Proposition A.4.

For all such that , assuming as well on and all solution of (A.13), the following hold on

-

(i)

For a sparse matrix , for all , we have

-

(ii)

For all , and , we have

In a model with , we take and can derive the same results as for the STIV estimator, including the confidence sets. The confidence bands of Section 4 are easily adapted. For the equation confidence band , we use E-STIV for and replace by in equation (32). Assumption A.3 uses and replaces quantities on the right-hand side which are specific to equation by the maximum over . Theorem 4.1 is modified to replace by . The term for is the equation approximately linear function (see the proof of Theorem 4.1). The proof of Theorem 4.1 allows for approximation error and extension to systems is straightforward. Proposition O.5 considers losses useful for a system of nonparametric IV equations and rates of estimation of for the confidence bands under conditional homoskedasticity in Section O.1.5.

A.2. Proofs of the Results in the Main Text

Proof of Proposition 3.1. First prove the first inequality. Take and set . By definition of and , on , we have . Also, on ,

| (A.14) |

Also, minimizes the criterion . Thus, on , we have

| (A.15) |

This implies, on ,

| (A.16) | ||||

The last inequality holds because by construction . Since is convex and

we have

.

Now, for all , we have

on . This is because these regressors serve as their own IV and, on , . Also, for all rows of index in the set ,

due to the Cauchy-Schwarz inequality. Finally, we obtain

| (A.17) |

Combining (A.17) with (A.16), on we have . Using (A.14) and (A.17), we find

| (A.18) |

The definition of the sensitivities yield, on , , hence

| (A.19) |

(A.19) and the definition of the sensitivities yield the first upper bound. For the second, we use (A.14) and item (i) in Lemma O.1. We now prove the second inequality. Take and . Acting as in (A.16), on ,

This yields

. We show the first inequality by considering two cases.

Case 1: , then . From this and the definition of

, we get the upper bound corresponding to the first term in the minimum. To obtain the second term we use the first upper bound in item (ii) in Lemma O.1.

Case 2:

, so

.

In conclusion, is smaller than the maximum of the two bounds.

Proof of Proposition 3.2. We use . The last constraint gives rise to the union of sets involving the linear constraint , hence the second minimum. We conclude from the definition of the sensitivities, the cones , and the fact that minimizing on a larger set yields lower bounds on the sensitivities.

Proof of Theorem 3.1. (i) and (iii) follow from the second bounds in Proposition 3.1 and Lemma A.2. Part (ii) follows from (i) and (iii) with and the fact that the assumption on implies: for (resp., as defined at the end of Section 3.3.1).

Proof of Theorem 3.2. Fix and in

and work on . Using lemmas A.2, LABEL:thrm:DLBsensitivitiesO, and O.2 (i),

we obtain

.

The following two cases can occur.

First, if

(so that ) then, using the bound in (11) for defined by we obtain

, which implies

.

Second, if , then

again by (11), we get

. Since for , we obtain , so that

.

Proof of Theorem 4.1. The elements relative to assumptions and estimation of are in Appendix A.1.2, some of which are used below. Take and let

We use and, for all , ,

We now work on of probability at least . For all , we have

We have obtained .

On , and

,

,

so

.

Also, on of probability at least , and by convexity

hence . By Assumption A.3 (ii), we have and the same replacing by .

Using (ii) and where and

is a Gaussian vector of covariance , by (O.4) (which hold with obvious modifications), we get and .

The second inequality uses the Markov inequality and the law of iterated expectations. We conclude like in Section O.1.5 and the proof of Class 4 (see Section O.1.1).

References

- [1] Andrews, D. W. K. and Stock, J. H. (2007). Inference with weak instruments. Advances in Economics and Econometrics Theory and Applications, Ninth World Congress, Blundell, R., W. K. Newey, and T. Persson, Eds, 3, 122–174, Cambridge University Press.

- [2] Barrenho, E., Gautier, E., Miraldo, M., Propper,C., and Rose, C. (2019). Peer and network effects in medical innovation: the case of laparoscopic surgery in the English NHS. HEDG Working Papers 19 650–659.

- [3] Belloni, A., Chen, D., Chernozhukov, V. and Hansen, C. (2012). Sparse models and methods for optimal IVs with an application to eminent domain. Econometrica 80 2369–2429.

- [4] Belloni, A., Chernozhukov, V. and Wang, L. (2011). Square-root lasso: pivotal recovery of sparse signals via conic programming. Biometrika 98 791–806.

- [5] Belloni, A., Chernozhukov, V., and Hansen, C. (2014). Inference on treatment effects after selection among high-dimensional controls. The Review of Economic Studies 81 608–650.

- [6] Belloni, A., Chernozhukov, V., Hansen, C., and Newey, W. (2018). High-dimensional linear models with many endogenous variables. Preprint 1712.08102.

- [7] Belloni, A., Chernozhukov, V., Chetverikov, D., Hansen, C., and Kato, K. (2018b). High-dimensional econometrics and regularized GMM. Preprint 1806.00666.

- [8] Bertail, P., Gauthérat, E. and Harari-Kermadec, H. (2008). Exponential inequalities for self normalized sums. Electronic Communications in Probability 13 628–640.

- [9] Bramoullé, Y., Djebbari, H., and Fortin, B. (2009). Identification of peer effects through social networks, J. Econometrics 150 41–55.

- [10] Breunig, C., Simoni, A., and Mammen, E. (2018). Ill-posed estimation in high-dimensional models with instrumental variables. Preprint 1806.00666.

- [11] Bickel, P., Ritov, Y., and Tsybakov, A. (2009). Simultaneous analysis of lasso and Dantzig selector. Annals of Statistics 37 1705–1732.

- [12] Cai, T., Liu, W. and Luo, X. (2011). A constrained minimization approach to sparse precision matrix estimation. Journal of the American Statistical Association 106 594–607.

- [13] Caner, M. (2009). Lasso type GMM estimator. Econometric Theory 25 1–23.

- [14] Caner, M. and Zhang, H. (2014). Adaptive elastic net for generalized methods of moments. Journal of Business and Economics Statistics 32 30–47.

- [15] Caner, M. and Kock, A. B. (2019). High dimensional GMM. Preprint 1811.08779.

- [16] Chao, J. and Swanson, N. (2005). Consistent estimation with a large number of weak instruments. Econometrica 73 1673–1692.

- [17] Chernozhukov, V., Chetverikov, D., Demirer, M., Duflo, E., Hansen, C., Newey, W., and Robins, J. (2018). Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal 21 C1–C68.

- [18] Chernozhukov, V., Chetverikov, D., and Kato, K. (2013). Gaussian approximations and multiplier bootstrap for maxima of sums of high-dimensional random vectors. Annals of Statistics 41 2786–2819.

- [19] Candès, E, and Tao, T. (2007). The Dantzig selector: statistical estimation when is much larger than . Annals of Statistics 35 2313–2351.

- [20] Cheng, X. and Liao, Z. (2015). Select the valid and relevant moments: an information-based lasso for GMM with many moments. Journal of Econometrics 186, 443–464.

- [21] Donoho, D. L., Elad, M., and Temlyakov, V. N. (2006). Stable recovery of sparse overcomplete representations in the presence of noise. IEEE Transactions on Information Theory 52 6–18.

- [22] Dufour, J.-M. (1997). Impossibility theorems in econometrics with applications to structural and dynamic models. Econometrica 65 1365–1387.

- [23] Dümbgen, L., van de Geer, S., Veraar, M., and Wellner, J. (2010). Nemirovski’s inequalities revisited. American Mathematical Monthly 117 138–160.

- [24] Fan, J. and Liao, Y. (2014). Endogeneity in high dimensions. Annals of Statistics 42 872–917.

- [25] Gautier, E. and Le Pennec (2018). Adaptive estimation in the nonparametric random coefficients binary choice model by needlet thresholding. Electronic Journal of Statistic 12 277–320.

- [26] Gautier, E. and Rose, C. (2017). Inference on social effects when the network is sparse and unknown. Working paper.

- [27] Gold, D., Lederer, J., and Tao, J. (2017). Inference for high-dimensional instrumental variables regression. Preprint 1708.05499.

- [28] Hoffmann, M. and Reiss, M. (2008). Nonlinear estimation for linear inverse problems with error in the operator. Annals of Statistics 36 310–336.

- [29] Javanmard, A. and Montanari, A. (2014). Confidence intervals and hypothesis testing for high-dimensional regression. Journal of Machine Learning Research 15 2869–2909.

- [30] Jing, B.-Y., Shao, Q. M., and Wang, Q. (2003). Self-normalized Cramér-type large deviations for independent random variables. Annals of Probability 31 2167–2215.

- [31] Kang, H., Zhang, A., and Cai, T. and Small, D. (2016). Instrumental variables estimation with some invalid IVs and its application to mendelian randomization. Journal of the American Statistical Association 111 132–144.

- [32] Kolesár, M., Chetty, R., Fiedman, J., Glaseser, E., and Imbens, G. (2015). Identification and inference with many invalid IVs. Journal of Business & Economic Statistics 33 474–484.

- [33] Lewbel, A. and Pendakur, K. (2009). Tricks with hicks: the EASI demand system. American Economic Review 99 827–863.

- [34] Lounici, K. (2008): Sup-norm convergence rate and sign concentration property of the lasso and Dantzig selector. Electronic Journal of Statistics 2 90–102.

- [35] Pinelis, I. (1994). Probabilistic problems and Hotelling’s test under a symmetry condition. Annals of Statistics 22 357–368.

- [36] Rose, C. (2016): Identification of spillover effects using panel data. Job Market Paper.

- [37] Sargan, J. (1958). The estimation of economic relationships using instrumental variables. Econometrica 26 393–415.

- [38] Tibshirani, R. (1996). Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B 58 267–288.

- [39] Tibshirani, R. J. (2013). The lasso problem and uniqueness. Electronic Journal of Statistics 7 1456–1490.

- [40] van de Geer, S., Bühlmann, P., Ritov, Y., and Dezeure, R. (2014). On asymptotically optimal confidence regions and tests for high-dimensional models. Annals of Statistics 42 1166–1202.

- [41] Wilson, E.B. (1927). Probable inference, the law of succession, and statistical inference. Journal of the American Statistical Association 22 209–212.

Online Appendix

O.1. Complements

O.1.1. Complements on Section A.1.1

The following propositions establish lower bounds on when , , . Let and . We have

We define the following generalizations of the restricted eigenvalue (RE) constants

Proposition O.1.

For any , we have

Proof. For such that we have . Thus, one obtains

Taking the infimum over ’s proves the first two inequalities of the proposition. The second inequality uses the fact that from Hölder’s inequality .

We now obtain bounds for sensitivities with . For any , we consider the restricted eigenvalue constant: .

Proposition O.2.

For any such that and , we have

where .

Proof. For and a set , let be the subset of indices in corresponding to the largest in absolute value components of outside of . Define . If we have . It is easy to see that the largest absolute value of elements of satisfies . Thus,

For , this implies

where . Therefore, using that we get, for ,

so

| (O.1) |

Using (O.1) and for , we get

Using we have proved the result.

We conclude this section by mentioning that, without endogeneity, the sensitivity shares similarities with the characteristic introduced independently in [10]. It differs in the definitions of and and in that it does not involve scaling by . Moreover [7] shows that previously introduced measures are computationally infeasible to verify but that the sensitivities that we introduce in this paper have desirable average-case perspective relative to NP-hardness in addition to them being weaker and more general than the others.

To tighten the bounds in Table 1, one can specify a small set and include the additional constraint , in the LPs of Table 1, where is the sign of . Since the signs are unknown, one replaces by in Table 1. This augments the number of LPs by a factor of . In our simulations we take to construct lower bounds based on a sparsity certificate. The design is such that . If constructing lower bounds using of small cardinality, we use .

Other bounds can be derived from Proposition A.1 and the following Proposition. Similar bounds can be obtained for the sensitivities based on (see [8]).

Proposition O.3.

Let , , and . We have

| (O.2) | ||||

| (O.3) |

In the cases where which we consider, we can use and , when , and , when .

When , we have , where

and

and . To compute a lower bound on , one can rely on (iv) in Proposition A.1 to obtain a lower bound on and multiply it by . To compute a lower bound on , one can use .

The lower bounds in Proposition 3.2 can be adapted to the sensitivities

using sets instead of involving the restrictions

and

for and for .

We now present the adjustments for classes 1-3 with assumptions A.1 and O.1 under independence between IVs and structural errors.

Assumption O.1.

This is a condition of type (N.i). Assumption O.1 permits to work with , which is smaller than as in the main text, and have

where , because

Combining Assumption O.1 with any of classes 1-3 yields an upper bound on the coverage error, also denoted by , which is the one above plus .

We now present Class 4.

Class 4: , , and a sequence such that . For all : and ,

-

(C4.i)

;

-

(C4.ii)

(N.i) holds for , and , ;

-

(C4.iii)

;

-