Impact of heterogenous prior beliefs and disclosed insider trades ††thanks: For useful discussions, we thank Deqing Zhou and Bowen Shi. We also would like to thank Jiaan Yan, Jianming Xia and other seminar participants at the Institute of Applied Mathematics, Academy of Mathematics and Systems Science, Chinese Academy of Sciences. The first named author is grateful for financial support for National Natural Science Foundation of China (No.10721101) and China’s National 973 Project (No.2006CB805900). The second author also would like to thank Hengfu Zou, Zhixiang Zhang and other seminar participants at Central University of Finance and Economics.

Abstract

In this paper, we present a multi-period trading model by assuming that traders face not only asymmetric information but also heterogenous prior beliefs, under the requirement that the insider publicly disclose his stock trades after the fact. We show that there is an equilibrium in which the irrational insider camouflages his trades with a noise component so that his private information is revealed slowly and linearly whenever he is overconfident or underconfident. We also investigate the relationship between the heterogeneous beliefs and the trade intensity in the presence of trade disclosure, and show that the weights on asymmetric information and heterogeneous prior beliefs are opposite in sign and they change alternatively in the next period. Under the requirement of disclosure, the irrational insider trades more aggressively and leads to smaller market depth. Moreover, the co-existence of “public disclosure requirement” and “heterogeneous prior beliefs” leads to the fluctuant multi-period expected profits and a larger total expected trading volume which is positively related to the degree of heterogeneity. More importantly, even public disclosure may lead to negative profits of the irrational insider’s in some periods, inside trading remains profitable from the whole trading period.

Keywords. public disclosure; asymmetric information; insider trading; price discovery; heterogeneous prior beliefs.

JEL subject classifications: G12; G14

1 Introduction

Anybody, who has a casual look at the security or stock markets, would be amazed by the fluctuation features of financial markets, such as the fluctuation of the trading volume, the price and the short-term aggressive trading. But these fascinating features have rarely been studied in theoretical finance, perhaps for the reason that they seem close to the irrational behavior of traders and can not be explained in the rational expectations. In this paper, we try to study these fascinating features of the market and address the implications on financial market of irrational behavior, by developing a trading model to characterize the optimal behavior of an irrational insider who possesses long-lived private information about the fundamental value of a security under mandatory disclosure requirements.

In his pioneering and insightful paper, Kyle (1985) introduces a dynamic model of insider trading where an insider receives only one signal and the fundamental asset value does not change over time. Through trade, the insider progressively releases his private information to the market as he exploits his informational advantage. Kyle (1985) also points out that liquidity trading provides camouflage which conceals informed trading such that the informed trading is swamped by liquidity trading. Based on Kyle (1985), Huddart, Hughes and Levine (2001) consider the case of the same insider under disclosure requirement as mandated by US securities laws. The ex-post disclosure of the insider’s trades changes the equilibirum strategy of the insider, given that market makers can infer information from the insider’s previous trade before the next round of trading. Huddart, Hughes and Levine (2001) find that public disclosure of the insider’s traders nevertheless accelerates the price discovery process and lowers trading costs by comparison to the case with no disclosure requirement. Zhang (2004) extends Huddart, Hughes and Levine (2001) by incorporating the condition that the monopoly insider is risk-averse, and he finds that under disclosure requirements, the risk-averse insider is more concerned about the risk of sub-optimally revealing his information by mandatory disclosure and his private information is revealed slowly. Also, Zhang (2008) analyzes a dynamic market where outsiders share part of the information about a security with a corporate insider and update their incomplete information by learning from disclosed insider trades. Recently, Gong and Liu (2011) study the optimal behaviors of competitive insiders and their influences to the market under disclosure requirements. All the papers mentioned above have the assumption that the insider is rational. An interesting question is what the behavior of an irrational insider behavior under mandatory disclosure requirements.

In the past few years, lots of literatures have studied the behaviors of irrational traders and their influences to the market. Odean (1998) presents three different markets structures, two of which examine price-taking overconfident informed traders, and one which looks as Kyle (1985)’s setting. His results depend a lot on the specific assumptions about risk preferences of agents and competition. Benos (1998) explicitly models investor behavior in financial markets allowing for traits linked to a notion of imperfect rationality. He studies an extreme form of posterior over confidence where some risk neutral investors overestimate the precision of their private information. In addition, Kyle and Wang (1997) and Wang (1997) consider the case of heterogeneous prior beliefs. The former considers heterogeneous prior beliefs in their study of the survival of irrational traders in a duopoly context while the later examines the implication of overconfidence for delegated fund management in both learning and evolutionary game models. Harris and Raviv (1993) and Wang (1998) use heterogeneous prior beliefs to explain the enormity of volume traded each day. Specifically, Wang (1998) extends the model of Kyle (1985) by incorporating heterogeneous prior beliefs. He finds that in equilibrium, the informed trader, facing both asymmetric information and heterogeneous prior beliefs, smoothes out his trading on asymmetric information gradually over time, but concentrates his entire trading on heterogeneous beliefs toward the last few periods. Since under US securities laws insiders associated with a firm must report to the Securities and Exchange Commission trades they make in the stock of that firm, we try to study the optimal behaviors of an irrational insider, and address its impact to the market under the mandatory disclosure requirements in this paper, using the framework of Kyle (1985).

Kyle (1985)’s model has been widely used to analyze financial market microstructure and the value of information. For example, Holden and Subrahmanyan (1992) and Foster and Viswanathan (1996) consider a market with multiple the competing insiders, and they show that competition among insiders accelerates the release of their private information. Back (1992) formalizes and extends the model by showing the existence of a unique equilibrium beyond the Gaussian-linear framework. Remarkable, when the asset value has a log-normal distribution, the price process becomes a geometric Brownian motion as is usually assumed in finance. Holden and Subrahmanyan (1994) assume the single informed trader is risk-averse. They show that both monopolistic and competing informed traders choose to exploit rents rapidly, causing market depth to be low in the initial periods and high in later periods and causing information to be revealed rapidly, unlike in the case of a risk-neutral monopolist considered by Kyle (1985). Gong and Zhou (2010) improve the Kyle (1985) model by loosing the assumption of constant pricing rule and give a new framework to analysis the insider’s behavior.111We will consider this problem using the new framework in other papers, and the purpose of this paper is to analysis the impact of heterogenous prior beliefs and disclosed insider trades to the market using the framework of Kyle (1985) so as to compare with the modified model. Also, Fishman and Hagerty (1992), Luo (2001), Rochet and Vila (1994), and Jain and Mirman (1999) e.t. have used variance of Kyle’s model to analyze and to explain real financial phenomena.

We consider a model in which traders face both asymmetric information and heterogeneous prior beliefs, with the requirement that the insider publicly disclose his stock trades after the fact. Heterogeneity arises because traders have different distribution assumptions about an informed trader’s private signal, that is to say traders agree to disagree with the precision of the signal. Using the same description as Wang (1998), a trader is overconfident if his distribution of the signal is too tight and underconfident if it is too loose.

We give the existence and the uniqueness of the insider’s equilibrium trading strategy in a multi-period rational expectation framework and give the analysis of the equilibrium. In equilibrium, the “trade public disclosure” and “heterogeneous prior beliefs” have great effects on the insider’s trading intensity, the market depth and the effectiveness of the price.

We obtain many new and interesting results on market characteristics and traders’ strategies. First, under disclosure requirement, the adverse selection decreases when there is an irrational informed trader participating in the market, and the descending range is positive related to the degree of heterogeneity. Since the insider trades more aggressive than he should rationally do, he submits larger orders. The market makers, realizing that the insider is irrational and aggressive behavior, increase market depth. While market makers decrease the market depth if there is no public disclosure requirements, even though the insider is irrational. That is to say, “public disclosure” leads to smaller market depth.

Also, under the disclosure requirement, the irrational insider’s private information is revealed slowly and linearly, for any degree of his heterogeneity. That is to say, under the public disclosure requirement, “heterogeneous beliefs” has no effect on the speed of revelation of information. While “heterogeneous beliefs” has great impacts on the trading behavior of irrational insiders and market structure. In particular, under the disclosure requirement, the insider dissembles his information by adding a random component to his trades in every round except the last one. Despite this, our analysis shows that the information is reflected more rapidly in price with disclosure of insider trades than without. An interesting finding is that when the insider is overconfident or underconfident, the trading intensity of the insider, the heterogeneity parameter and the expected profits all fluctuate greatly during all early auctions. We reveal the relationship between the heterogeneity and the trade intensity in the presence of information disclosure, which agrees with our intuition in the financial market. That is to say, if the underconfident insider puts a positive weight on asymmetric information this period, then he puts a negative weight on heterogeneous prior beliefs this period, and the case is inverse in the next period. We also show that the co-existence of public disclosure and heterogeneous prior beliefs leads to large and fluctuated trading volume and the fluctuation is positively related to the degree of the insider’s heterogeneity.

More importantly, the irrational insider’s profits of some trading rounds may be negative under the mandatory disclosure requirement. The expected profits fluctuate during all auctions, and the fluctuation which is positive related to the degree of heterogeneity is small at the early auctions and becomes larger as the trading goes by. Moreover, even though the irrational insider may get negative profits in some periods, he trades to make sure the profit of the last period and the whole trading profit are all positive.

This paper is structured as follows. In Section we introduce the model and in Section we make an analysis and give the two-period equilibrium of the models with and without disclosure of insider trades, respectively. In Section , we give the unique linear Nash equilibrium in multi-period framework and give the analysis of the equilibrium. Finally, the appendix contains the proof of some necessary propositions.

2 The model

We conform to the notation of Kyle (1985). A single risky asset with a terminal value , which is normally distributed with mean and variance , is traded in an -period sequential auction market among three kinds of risk-neutral traders: a monopolistic informed trader, noise traders and market makers. The monopolistic informed trader has a unique access to a private signal about . All market makers and the insider agree that the signal is a scalar multiple of the terminal value , but they disagree concerning the right scale, that is to say, the informed trader thinks while the market makers think , where and are different positive constants. If we consider a normalized signal , using the same analysis as Wang (1998) we know that each trader’s heterogeneous prior belief is characterized completely by a parameter , where is a positive constant. Then the informed trader thinks while the market makers think . If we consider the market maker’s beliefs (i.e., ) as the benchmark case, then the informed trader is “overconfident” if and “underconfident” if . The noise traders (uninformed liquidity traders) trade randomly; and market makers set prices efficiently in the semi-strong form sense, conditional on the total quantities traded by the informed trader and noise traders, but not each of them. We also assume that there is no discount across periods, i.e., the interest rate is normalized to zero. This market model has some game-theoretic features. We can view it as a game played by the insider and the market makers: the insider attempts to hide his private information and make the best use of his information to maximize his profit; the market makers attempt to learn the private information from the order and set prices as efficiently as possible in order to rule out the profit opportunities of the insider.

Let denote the market order submitted by the informed trader at the -th auction, conditional on his information, and let denote the random quantity traded by noise traders at the -th auction. We assume that is normally distributed with zero mean and variance and are mutually independent. So the total trading volume, denoted by , is given by The market makers set price in semi-strong form sense based on his information at the -th auction. Denote by and the expectation operators of the informed trader and the market makers, respectively. Then , .

Let be the profit which accrues to the informed trader from the -th auction on, i.e., for . At each auction the informed trader maximizes his total expected profits of the current and the remaining rounds of trading conditional on his information, i.e.,

The equilibrium conditions are that the competition between market makers drives their expected profits to zero conditional on the order flow and the fact that the informed trader selects the optimal strategy conditional on his correct conjectures and his information at each auction. Following the convention in the existing literature, an equilibrium is said to be linear if the pricing rule is an affine function of the order flow. We will give the definition of equilibrium of two-period and N-period in the following sections, respectively.

3 Analysis

3.1 Two-period model without public disclosure of insider trades

In order to get a benchmark against which to compare an equilibrium for the case where the insider’s trade in the first period is publicly disclosed on completion of trading in that period, we first give the two-period equilibrium of the model without public disclosure of insider trades.

The proposition below is based on a special case of Theorem of Wang (1998).

Proposition 3.1.

Given no public disclosure of insider trades, for 222Just as the analysis in Wang (1998), the inequality condition means that if a rational informed trader thinks a risky asset is worth , then an irrational informed trader’s subjective value cannot be less than or more than for the equilibrium to exist. a subgame perfect linear equilibrium exists. In this equilibrium there are constants and such that

Given and , the above constants and satisfy:

the boundary condition is , and the second order condition is , where , and is the unique solution of the following equation

satisfying .

Proof.

See Appendix. ∎

3.2 Two-period model with public disclosure of insider trades

Using the same method by Huddart, Hughes and Levine (2001), we know that no invertible trading strategy can be part of an equilibrium in this case, and we show that there exists an equilibrium in which the insider’s first-period trade consists of an information-based linear component and a noise component , which is independently of and and normally distributed with mean and variance . For market makers, the public disclosure of allows them to update their beliefs based on the first period order flow. In particular, let be the expected value of given and . Thus, . In turn, replaces in the second period price .

Applying the principal of backward induction, we can write the insider’s second period optimization problem for given and as Since

| (3.1) |

the first order condition implies

| (3.2) |

and the second order condition is . So

| (3.3) |

and

| (3.4) |

Substituting the above into , and using , we obtain

| (3.5) |

Stepping back to the insider’s first period optimization problem, we have

and

| (3.6) |

The first order condition implies

| (3.7) | ||||

If our proposed mixed trading strategy is to hold in the equilibrium, we can seek values of , , and from Eq. such that , and

| (3.8) |

| (3.9) |

| (3.10) |

Combining Eqs. , with , we get

By the market’s efficient condition, we have

| (3.11) |

where

| (3.12) |

| (3.13) |

| (3.14) |

Note that

and

by the projection theorem, we know that is the projection of onto the two dimension space spanned by in which is the coefficient of the ed orthogonal basis Thus, we obtain

| (3.15) | ||||

Furthermore,

| (3.16) |

Then it is easy to get

| (3.17) |

where must satisfy

Next, we consider the effectiveness of the price, measured by Note that

| (3.18) |

Using , we obtain

| (3.19) |

i.e.,

| (3.20) |

By Eq. we get

i.e.,

Then Eq.(3.12) can be rewritten as

| (3.21) |

and thus

| (3.22) |

Eqs. , and yield

| (3.23) |

i.e.,

From the above we give the following proposition:

Proposition 3.2.

For , there exist a unique linear equilibrium in the two-period setting with public disclosure of the irrational insider’s trades, in which there are constants , and such that:

Given and , the constants , and are characterized as follows:

Proof.

See Appendix. ∎

Analysis of the equilibrium: The parameters and measure the intensity of trading due to asymmetric information and heterogeneous prior beliefs, respectively. In Proposition 3.2, we can have , which implies the intensity of trading on asymmetric information at the first period is lower than that at the second period (), no matter what the insider’s heterogeneous prior belief is. These are consistent with the absence of a concern for the effect of trading on future expected profits in the last period. It also implies that when the insider is underconfident (), he puts a positive weight on heterogeneous prior beliefs in the first period and negative weight in the second period, i.e., and . While the insider is overconfident, he does the opposite, that is to say, he puts a negative weight on heterogeneous prior beliefs in the first period and positive weight in the second period, i.e., and . These are consistent with our intuition.

The parameters , and characterize the pricing rule. The liquidity parameter is an inverse measure of market depth and the heterogeneous parameter measures the correction in the efficient price change per unit of the price in the previous period due to heterogeneous prior beliefs. The parameter measures the adjusted correction. From the proposition above, we know that the market liquidity are the same across the two periods, i.e. , no matter what the degree of the heterogenous belief is. equals the price adjustment based on the first period order flow and it increasing with .

The measure of the informativeness of price, , equals . That is to say, at the end of the first trading period, a half of the private information has been incorporated into the price. Setting serves to disguise the information based component of the insider’s trades once they are publicly disclosed. It is easy to see that is a decreasing function of the parameter , That is to say the more confident of the insider the less noise he puts in formulating his strategy.

It is worth noting that the insider’s expected profit at each period is not always positive as the existence literatures. The sign of the expected profit depends on the degree of heterogeneity. For example, the insider’s first period expected profit is , and when , .

The same exogenous parameters imply different values for the endogenous parameters depending not only on whether the insider must disclose his trader after the fact or not but also on the degree of heterogeneity. In order to distinguish these parameters, we add an upper bar to the endogenous parameters in the case of Huddart, Hughes and Levine (2001)’s model and a hat to the endogenous parameters in the case of Wang (1998). Note that when the above proposition is just Proposition of Huddart, Hughes and Levine (2001). The next proposition compares the endogenous parameters across Huddart, Hughes and Levine (2001)’s model and our model when

Proposition 3.3.

In the two-period setting, the endogenous parameters across Huddart, Hughes and Levine (2001)’s model and our model satisfy:

(i) when ,

when ,

(ii) for all ,

(iii) for all ,

(iv) when , is bigger or smaller than (the total profit of two period in the Huddart, et al. (2001)’s model) depends on the value of . Especially, when , , and when , .

(v) When , , and when ,

Proof.

: See the Appendix.

In our model, () characterize the degree of the dependence of the private information, from the Proposition 3.3 we know that under the requirement of trade disclosure, the underconfident insider’s first period trading intensity is bigger than the rational case, while the overconfident insider’s is smaller than the rational case. “Trade disclosure” makes the overconfident trader trade less aggressively than the underconfident trader in the first period. But in the second period, the trading intensity of the overconfident insider is bigger than the rational and the underconfident trader’s trading intensity. Not surprisingly, when the insider is irrational, whatever overconfident or underconfident, the “depth” of the market, i.e. the order flow necessary to induce prices to rise or fall by one dollar, is bigger than that of Huddart, et al. (2001)’s.

The measure of the informativeness of price equals . This means that in the two-period model “the public disclosure” and “heterogeneous prior beliefs” have no effect on the informativeness of the price, but it is not true when the trading period is bigger than two, which will be discussed in Section .

In order to disguise his trading, the insider puts a noise in formulating his strategy whose variance is . From in Proposition 3.3, we know that when the insider is underconfident the variance of the noise on his trading strategy is bigger than the rational trader, and when he is overconfident the variance of the noise on his trading strategy is smaller than the rational case. This coincides with our intuition.

The following proposition compares the endogenous parameters across the case of our model and Wang (1998)’s model. For convenience, we only analysis the cases of and , respectively.

Proposition 3.4.

In the two-period setting, the endogenous parameters across the case of our model and Wang (1998)’s model satisfy:

(i) When ,

(ii) When ,

is bigger or smaller than , depending on the values of and . So do and .

The above proposition implies that “public disclosure requirement” leads to more effectiveness of price and larger market depth, whenever the insider is overconfident or underconfident. If the insider is underconfident, he puts a smaller weight on his private information in the first period and a larger in the second period. However, the overconfident insider puts a larger weights in the two periods under the disclosure requirement. The proposition also implies even though “public disclosure requirement” may lead to negative profit in the first period the irrational insider can benefit from whole insider trading.

From the discussion above we can conclude that “the public disclosure” and “heterogeneous prior beliefs” have a great influence on the equilibrium.

4 A sequential auction equilibrium

In this section we generalize the model into -period trading where a number of rounds of trading with public disclosure take place sequentially. The model is structured such that the equilibrium price at each auction reflects the information contained in the past and the current order flow, and the insider maximizes his expected profits in the equilibrium taking into account his effect on price in both the current auction and the future auction.

4.1 The sequential equilibrium

Now, we represent a proposition which provides a difference equation system to characterize the equilibrium.

Proposition 4.1.

In the economy with one irrational informed traders , for , there exist a unique subgame perfect equilibrium and the equilibrium is a recursive equilibrium. In this equilibrium there are constants and , characterized by the following:

| (4.24) |

| (4.25) |

| (4.26) |

| (4.27) | ||||

| (4.28) |

Given and , and are the unique solution to the difference equation system

| (4.29) |

| (4.30) |

| (4.31) |

| (4.32) |

| (4.33) |

| (4.34) |

| (4.35) |

| (4.36) |

| (4.37) |

| (4.38) |

| (4.39) |

for all auction , and

| (4.40) |

| (4.41) |

Proof.

See the Appendix. ∎

As in Wang (1998), the inequality condition for the belief parameter , i.e., , is required in the above proposition. It results from the fact that the second order condition, which is given by Eq. (5.74), should be satisfied.

We will give the analysis of the equilibrium described by the proposition above in the following.

4.2 Equilibrium volume

Given the equilibrium of our model, we now investigate how “public disclosure” and “heterogeneous prior beliefs” affect the behavior of the trading volume.

Following Admati and Pfleiderer (1988), the total trading volume at the th auction denoted by , is defined by

| (4.42) |

Using the expressions of , and in Proposition 4.1, we can get the total expected trading volume as shown in the following proposition:

Proposition 4.2.

Both “public disclosure” and “heterogeneous prior beliefs” lead to a larger trading volume and the expected trading volume at the th () auction is

| (4.43) |

where

| (4.44) | ||||

| (4.45) | ||||

| (4.46) |

for And

| (4.47) |

| (4.48) |

| (4.49) |

Proof.

See the Appendix. ∎

Proposition 4.2 gives the contribution of each group of traders to the total trading volume. From the proof of the proposition 4.1, we know that when . Then the term in equation (4.45) and (4.44) vanishes when That is to say both the insider and the market makers trade a larger volume under heterogeneous prior beliefs and thus lead to an increase in total trading volume. Furthermore, in equation (4.45) and (4.44) vanishes if there is no public disclosure requirement, i.e., ‘public disclosure’ also makes both the insider and the market makers trade a larger volume and thus lead to an increase in total trading volume.

4.3 Properties of the sequential equilibrium

In order to analyze the properties of the equilibrium, we develop an algorithm that analytically solve the model’s unique equilibrium,333The algorithm here is different form that of Holden and Subrahmanyam (1992). as described in the following proposition.

Proposition 4.3.

Let , , , For the solution of the difference equation system in Proposition 4.1 is given by starting the boundary condition , , , and iterating backward for , and by using the following equation, for

| (4.50) |

| (4.51) |

| (4.52) |

where

| (4.53) | ||||

| (4.54) | ||||

Then starting from the exogenous values and , iterate forward for each of the following variables in the order listed

| (4.55) |

| (4.56) |

| (4.57) |

| (4.58) |

| (4.59) |

| (4.60) |

| (4.61) |

for all and when , the boundary condition is given by Eqs. and .

Proof.

See the Appendix. ∎

Using formulas in the proposition we generate a series of numerical simulations. We first compare the interesting parameters , , and in our model with those of Huddart, Hughes and Levine (2001) and Wang (1998). As in Kyle (1985), the parameters and are the inverse measures of price efficiency and the market depth, respectively. denotes the profits of the -th auction, i.e., And denotes the variance of the noise that the insider put when he plays mixed strategy in the -th period.

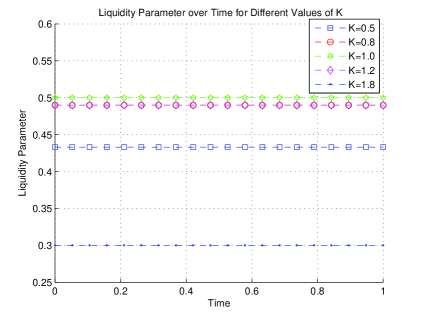

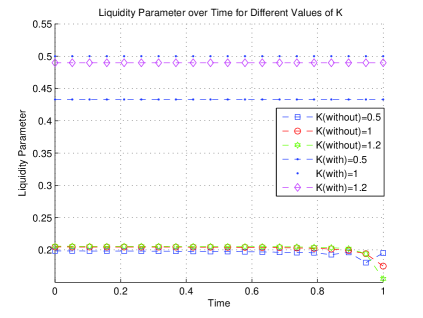

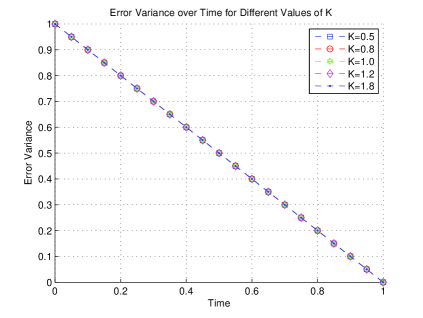

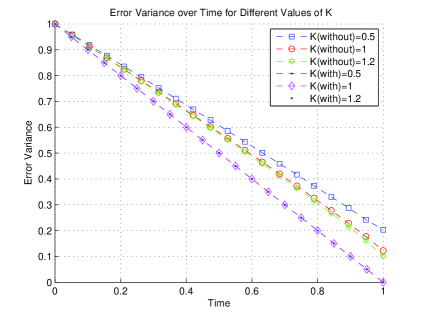

Figure and Figure plot the dynamic behavior of the liquidity parameter and the error variance of price , respectively, by holding constants , and fixed and varying the belief parameter , or Among them, the subfigures and plot the parameters and in our model respectively for different values , while the subfigures and contrast the parameters and , respectively, (i) when the insider must disclose each trade ex-post and (ii) when no such disclosures are made.

Figure shows the trajectory of the market maker’s price adjustment in our model for varying belief parameters. It indicates that the liquidity parameter is constant for any values of . This result is consistent with that of Huddart, Hughes and Levine (2001). It also indicates that the market depth, measured by , is positively related to the degree of heterogeneity, measured by . Figure indicates that “public disclosure” not only leads to constant market depth for any values of , but also makes the adverse selection (measured by ) higher than the case of without public disclosure requirements. This is because under the requirements of disclosure the information content of the order flow is high.

The pattern of is consistent with the released speed of the information of the insider, measured by , which is plotted in Figure . Figure indicates that when the insider must disclose, the value of following each disclosure declines linearly over time independent of periods and the values of . However, Figure indicates that less information asymmetry is present in the market with more aggressive informed trading, measured by the parameter , without public disclosure requirements.

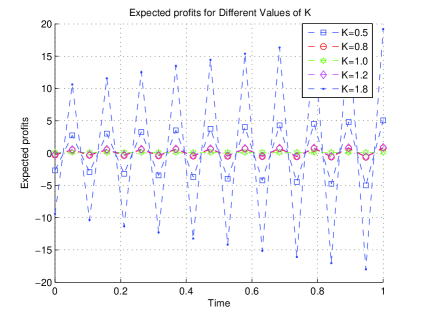

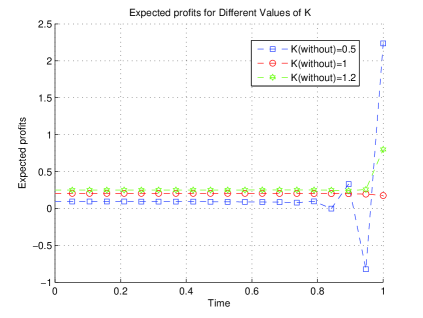

In order to see the differences between the heterogeneous priors case to the common priors case, and the cases with and without public disclosure requirements clearly, we plot the dynamic behavior of of the two cases, respectively, in Figure . Figure shows that the expected profits of the rational insider are constant over trading rounds. This is the result of Huddart, Hughes and Levine (2001). An interesting result can be get from Figure is that the insider’s profits fluctuate greatly if the insider is underconfident or overconfident. Specifically, the sign of the expected profit is alternating to ensure the last sign of the last period is not negative. Moreover, the dynamic pattern in Figure indicates that the fluctuation of the expected profits is positively related to the degree of heterogeneity, measured by . Even though “disclosure requirement” makes the profits of some trading rounds are negative, the insider trading can also profit from the whole trading process. While without the public disclosure of insider trades, the expected profit at each period is almost constant in all early auctions and becomes significant only in the last few ones.

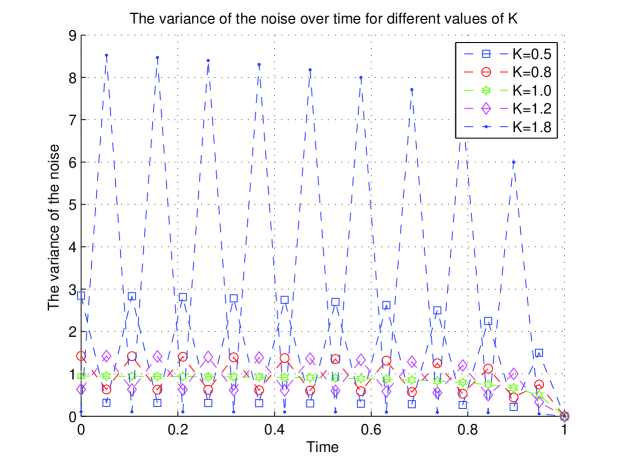

Figure indicates that the fluctuation of the noise’s variance is bigger at the beginning few periods and becomes smaller gradually if the the insider is irrational. The degree of noise variance’s fluctuation is positively related to the degree of heterogeneity, measured by . Figure also indicates that more overconfident insider puts an smaller noise at the first period and then put a bigger one, while the more under confident insider does the opposite.

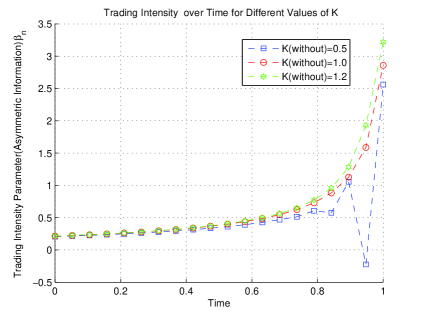

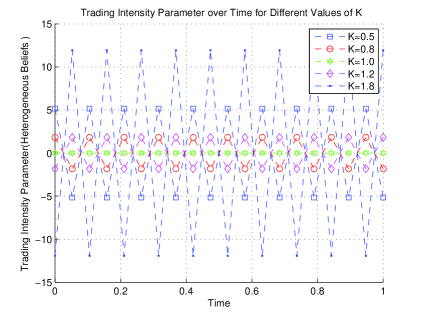

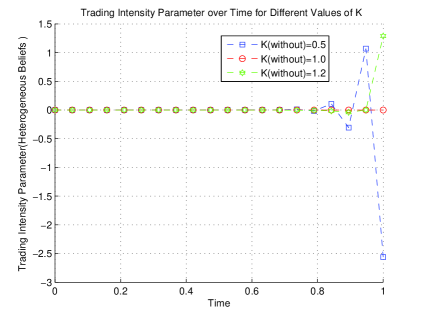

Next, we compare parameters , , and between the case of with and without disclosure of insider trades for varying numbers of trading rounds, by holding constants , and fixed and varying the belief parameter , , , , or As in Wang (1998), measures the trading intensity on the asymmetric information, measures the trading intensity on heterogeneous beliefs, and are heterogeneity parameters, and measures the total expected trading volume.

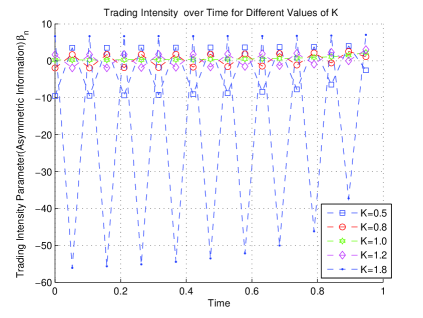

Figure indicates that under the disclosure requirement the irrational informed trader’s intensity of trading on asymmetric information, measured by , fluctuates greatly during all early auctions and becomes subdued gradually in the last few rounds of trades. The fluctuation is also positively related to the degree of the heterogeneity. This result is intuitive since the more heterogeneous informed trader is the more he will be influenced by the “trade disclosure” and more aggressively he will trade. Figure also indicates if the insider is overconfident the intensity of trading is positive at the first period and negative at the second period, and the sigh changes alternatively, while the underconfident insider does the opposite. This result is very differently from the case of no disclosure requirement, which is given in Figure .

Figure shows that the irrational informed trader’s intensity of trading on heterogeneous prior beliefs, measured by , also fluctuates greatly during all early auctions and the fluctuation is also positively related to the degree of heterogeneity, but the direction of fluctuation is opposite to that of . That is to say if the irrational insider puts a positive weight on asymmetric information this period, then he puts a negative weight on heterogeneous prior beliefs, and the case is inverse in the next period. While Figure shows that the informed trader trades on differences in beliefs only in the last few auctions since the intensity of trading on heterogeneous prior beliefs is negligible in all early auctions, which is the result of Wang (1998). Comparing the Figure with Figure , and with Figure we know that ‘trade disclosure’ has a big influence on the insider’s strategy, whenever the insider is underconfident or overconfident.

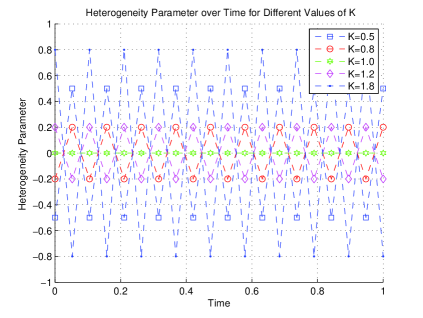

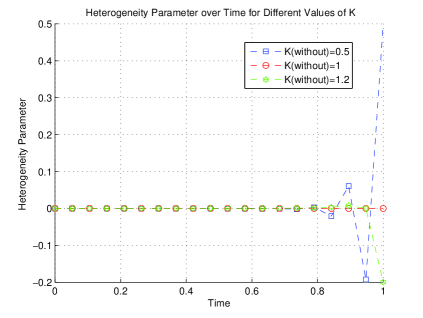

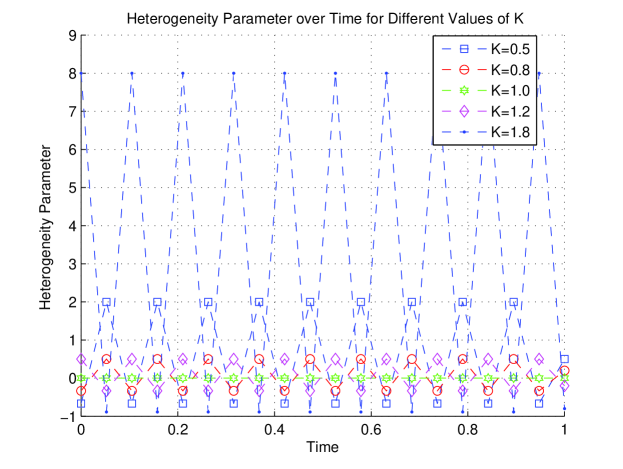

Figure and Figure plot the heterogeneity parameters and , respectively. They indicate that and all also fluctuate according to the degree of heterogeneity. This pattern is consistent with the informed trader’s strategies. Market makers can correctly predict that “heterogeneous prior beliefs” and “trade disclosure” have big impacts on the trader’s strategies at each auction, market makers choose a non-zero to account for the adverse selection problem properly, and adjust to correctly after observing the insider’s trading. This intuition is further confirmed by the fact that the patterns in Figure and Figure are exactly the opposites of the pattern in Figure .

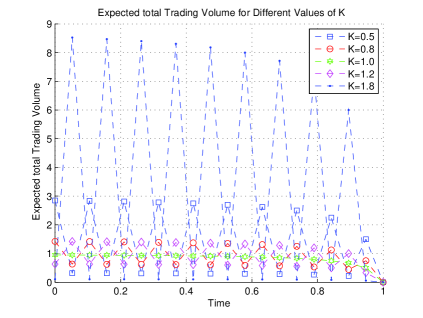

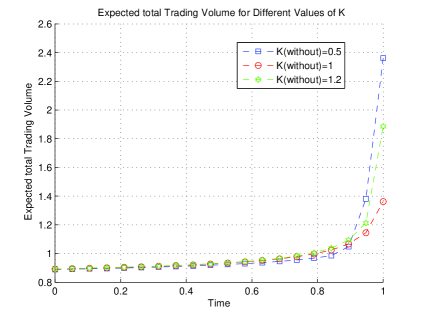

Figure indicates that the total expected trading volume , is positively related to the degree of heterogeneity, measured by The fluctuation is greatly during all early auctions and becomes subdued gradually in the last few rounds of trades, this pattern is consistent with that of the trading strategy of the insider. Comparing Figure with Figure , we how that under the requirement of public disclosure, the expected trading volume is dramatically big. This result vividly confirms Proposition 4.2 which shows that not only “heterogeneous prior beliefs” but also “public disclosure” lead to a larger volume.

5 Conclusions

In this paper, we have characterized the dynamically optimal trading strategies of an irrational insider under ex-post disclosure requirement, and addressed the impacts on the financial markets.

In contrast to the case of an irrational insider who restricts his intensity of trading on private information, during all early auctions and becomes aggressive only in the last few rounds of trades in a setting under no disclosure requirement, we show that the irrational insider under disclosure requirement employs a mixed strategy and trades more aggressive on private information from the beginning to the end. In particular, under disclosure requirements, insider puts the weights on asymmetric information and heterogeneous prior beliefs are opposite in sign, and the sighs change alternatively in the next period. Since on one hand the irrational insider is overconfident or underconfident about his signal and on the other hand he wants to dissimulates his information, he trades more aggressively than he rational does. The market makers, realizing the heterogeneity and that a part of total order flow is due to aggressive behavior, increases market depth. Also, under disclosure requirement, the market depth is positive related to the degree of the heterogeneity.

Our model indicates that despite the irrational insider dissembles his information by adding a random component to his trades, the information is reflected more rapidly in price with the disclosure of insider trades than without. An interesting find is that “public disclosure” makes the revelation speed of the information are the same, whenever the insider is overconfident or underconfident. In equilibrium, we also show that while “public disclosure” may lead to negative profits at some trading rounds, insider trading remains profitable from the whole trading time. The irrational insider trades to make sure his profit at the last period is positive. Furthermore, the heterogeneity beliefs and public disclosure all lead to larger trading volume. The co-existence of the heterogeneity beliefs and public disclosure makes the trading volume fluctuate greatly, and the fluctuation is positive related to the degree of the insider’s heterogeneity. This result can explain the trading fluctuation in the real finance in some sense.

Appendix

Proof of Proposition 3.1: Let the in Theorem of Wang (1998) equal and equal , we have the following relationships:

By we can get

From the second order condition, , we can get . From the above we know that if we get , then we can get , and all the coefficients of the second period is known. But in order to get , we first solve . Combing the expression of and , we get

| (5.62) |

The expression of and imply

| (5.63) |

where .

Substitute the expression of and into , we obtain

When , , i.e.

By the expression of , we get

Since , we have

i.e.

and satisfy

, From we get

. In order to explain the root that satisfy the

condition is unique, let . It

is easy to know , ,

so the needed root is unique. Q.E.D.

Proof of Proposition 3.2: In order to get the proposition, we only need to compute and

Using Eq. (3.3), we can get

| (5.64) | ||||

Substitute the expression of and into the above equation, yields

| (5.65) | ||||

Eq. (3.6) implies

| (5.66) | ||||

while

| (5.67) | ||||

| (5.68) |

Q.E.D.

Proof of Proposition 3.3: From Proposition 3.2, it is easy to get

and the total expected profit is

By Proposition in Huddart, et al.(2001), we get

and the total expected profit is

Comparing the corresponding parameters respectively, it is easy to

get the conclusion.Q.E.D.

Comparing the corresponding parameters respectively, it is easy to get the conclusion.Q.E.D.

We will use the backward induction method to prove that the unique linear equilibrium exists. Suppose that there exist constants and such that

Applying the principal of backward induction, we can write the insider’s last period (th period) optimization problem for given as

where

The first order condition implies

| (5.69) |

and the second order condition is

From Eq. (5.69), we know that

| (5.70) |

and

| (5.71) | ||||

so

| (5.72) |

Since , , by the market efficient condition, we have

| (5.73) | ||||

so

Substitute Eq. (5.70) into the above expression, we have

| (5.74) |

and combing the above with the second order condition, we get

| (5.75) |

So the should satisfied Eq. (5.70) and imply

Substitute the above to Eq. (5.72), we have

| (5.76) |

| (5.77) |

| (5.78) |

Since

| (5.79) | ||||

we have

Since we have

| (5.80) | ||||

The first order condition is

| (5.81) | ||||

In the rational sense, is independent with . If our suppose mixed strategy hold, then we have

| (5.82) |

| (5.83) |

| (5.84) |

Since , and , we have

| (5.85) |

Combing the market efficient condition with Eq. , we have

| (5.86) | ||||

and

| (5.87) | ||||

so

| (5.88) |

| (5.89) |

Combing Eqs. and

Eqs. , and yield

| (5.90) |

i.e.

| (5.91) |

Substitute the above formula into the Eq. , it is easy to get

| (5.92) |

and

| (5.93) |

Since , we have

| (5.94) |

Using Eqs. (5.94) and the projection theorem for normally distributed random variables, we obtain

| (5.95) |

Since the strategy of the insider is , we have

| (5.96) | ||||

thus we obtain that , , and are given by Eqs. , respectively.

We have proved that the difference equation system given by Eqs. - describes a linear equilibrium of the model, next we prove that this equilibrium is the unique linear equilibrium with the boundary condition

Given and and are uniquely determined by Eqs. and . Furthermore, given , , , , and , we can obtain , , , , , , , , from Eqs. -. Thus we can iterate the system backwards one step. Given the the boundary condition the backward iteration procedure yields a family of solutions to the difference equation system parameterized by the terminal value But is proportional to in any solution and consequently there is a unique solution given the initial value .

Proof of Proposition 4.2 Note that ,, and are normally distributed with zero mean, we have

| (5.97) |

where , , and .

We only need to calculate and , and the rests are similar and easy. By definition, and Eq. (4.24)

| (5.98) |

for and

| (5.99) |

Taking variance on both sides of Eqs. (5.98) and (5.99), respectively, we obtain

| (5.100) |

| (5.101) |

Proof of Proposition 4.3 Since

| (5.102) |

The boundary conditions Eqs. and imply , , . Substitute Eq. into Eqs. , , , , and respectively, we can get Eqs. -. And Eq. implies Eq. . Using Eq. we can obtain

| (5.103) |

where is given by . And using , we can have

| (5.104) |

where is given by . Using Eqs. and , we can get and .

References

- 1 Admati, A.R., Pfleiderer, P., 1988. A theory of intraday patterns: volume and price variability. Review of Financial Studies 1, 3-40.

- 2 Back, K., 1992. Insider trading in continuous time. Review of Financial Studies 5(3), 387-409.

- 3 Benos, A.V., 1998. Aggressiveness and survival of overconfident traders. Journal of Financial Markets 1, 353-383.

- 4 Fishman, M.J., Hagerty, K.M., 1992. Insider trading and efficiency of stock prices. RAND Journal of Economics 23, 106-122.

- 5 Foster, F. D., Viswanathan, S., 1996. Strategic trading when agents forecast the forecasts of others. Journal of Finance 51, 1437-1478.

- 6 Gong, F., Liu, H., 2011. Inside trading, public disclosure and imperfect competition. arXiv:1103.0894v1 [q-fin.TR].

- 7 Gong, F., Zhou, D., 2010. Insider trading in the market with rational expected price. arXiv:1012.2160v1 [q-fin.TR].

- 8 Harris, M., Raviv, A., 1993. Differences of opinion make a horse race. Review of Financial Studies 6, 473-506.

- 9 Holden, C.W., Subrahmanyam, A., 1992. Long-lived private information and imperfect competition. Journal of Finance 47, 247-270.

- 10 Holden, C.W., Subrahmanyam, A., 1994. Risk aversion, imperfect competition and long lived information. Economics Letters 44, 181-190.

- 11 Huddart, S., Hughes, J.S. and Levine C.B., 2001. Public disclosure and dissimulation of insider traders. Econometrica, Vol.69, No.3, 665-681.

- 12 Jain, N., Mirman, L.J., 1999. Insider trading with correlated signals. Economic Letters 65, 105-113.

- 13 Kyle, A.S., 1985. Continuous auctions and insider trading. Econometrica 53, 1315-1335.

- 14 Kyle, A.S., Wang, F.A., 1997. Speculation duopoly with agreement to disagree: can overconffidence survive the market test? Journal of Finance 52, 2073-2090.

- 15 Odean, T., 1998. Volume, volatility, price and profit when all traders are above average. Journal of Finance 53, 1887-1934.

- 16 Luo, S., 2001. The impact of public information on insider trading. Economics Letters 70, 59-68.

- 17 Rochet, J.C., Vila, J.L., 1994. Insider trading without normality. Review of Economic Studies 61, 131-152.

- 18 Wang F.A., 1998. Strategic trading, asymmetric information and heterogeneous prior beliefs. Journal of Financial Markets 1, 321-352.

- 19 Wang, F.A., 1997. Overconffidence, delegated fund management, and survival. Working paper, Columbia University, New York.

- 20 Zhang, W.D., 2004. Risk aversion, public disclosure and long-lived information. Economic Letters, 85, 327-334.

- 21 Zhang, W.D., 2008. Impact of outsiders and disclosed insider trades, Economic Letters, 5, 137-145.