Semiparametric Additive Transformation Model under Current Status Data

Abstract

We consider the efficient estimation of the semiparametric additive transformation model with current status data. A wide range of survival models and econometric models can be incorporated into this general transformation framework. We apply the B-spline approach to simultaneously estimate the linear regression vector, the nondecreasing transformation function, and a set of nonparametric regression functions. We show that the parametric estimate is semiparametric efficient in the presence of multiple nonparametric nuisance functions. An explicit consistent B-spline estimate of the asymptotic variance is also provided. All nonparametric estimates are smooth, and shown to be uniformly consistent and have faster than cubic rate of convergence. Interestingly, we observe the convergence rate interfere phenomenon, i.e., the convergence rates of B-spline estimators are all slowed down to equal the slowest one. The constrained optimization is not required in our implementation. Numerical results are used to illustrate the finite sample performance of the proposed estimators.

Key Words: B-spline; Consistent variance estimation; Current status data; Efficient estimation; Semiparametric transformation models

1 Introduction

We consider the efficient estimation of the following semiparametric additive transformation model:

| (1) |

where is a monotone transformation function, ’s are smooth regression functions (with possibly different degrees of smoothness), and has a known distribution with support . A wide range of survival models and econometric models can be incorporated into the above general transformation framework, e.g., (Huang & Rossini, 1997; Shen, 1998; Huang, 1999; Banerjee et al., 2006, 2009). In particular, the model (1) can be readily applied to a failure time by letting . We can obtain the partly linear additive Cox model, i.e., Huang (1999), by assuming and , where is an unspecified cumulative hazard function. Specifically, the hazard function of , given the covariates , has the form

| (2) |

where is the baseline hazard function, and . However, if we change the form of to , the model (1) just becomes the partly linear additive proportional odds model.

Motivated by the close connection with survival models, we focus on the current status data in this paper which arises not only in survival analysis but also in demography, epidemiology, econometrics and bioassay. More specifically, we observe , where is a random examination time and . We assume that and are independent given . Under current status data, the model (1) is also related to the semiparametric binary model studied in econometrics. Using the link function , we assume that the probability of , given the covariates , is of the expression:

| (3) |

Note that Banerjee et al. (2006) and Banerjee et al. (2009) have done a great deal of statistical estimation and hypothesis testing on the model (3) (without terms) by assuming to be log-log function and logistic function, respectively. An extensive discussions on the relation between (3) and survival models can be found in Doksum & Gasko (1990). Recently a similar transformation model has been considered by Chen & Tong (2010) but for the right censored data. They showed that the monotone transformation function is root-n estimable which will never be achieved in the case of current status data. This is the key theoretical difference between the two types of survival data.

In this paper, we employ the B-spline approach to simultaneously estimate the vector , monotone and smooth ’s. The corresponding estimates are denoted as , and . In contrast, Ma & Kosorok (2005) apply the penalized NPMLE approach to (1) (with ) which yields a non-smooth step function and the penalized estimate . Our B-spline framework has the following theoretical and computational advantages over the existing penalized NPMLE approach:

-

1.

Our B-spline estimate is smooth and uniformly consistent. However, is always discontinues (regardless of the smoothness of its true function ) and has a bias which does not vanish asymptotically. More importantly, the convergence rate of our is shown to be faster than that of , i.e., . Therefore, we expect more accurate inferences drawn from .

-

2.

We are able to give an explicit B-spline estimate for the asymptotic covariance of based on which the asymptotic confidence interval of can be easily constructed. Under very weak conditions, its consistency is proven. However, the block jackknife approach in Ma & Kosorok (2005) requires more computation, and is even not theoretically justified.

-

3.

Our spline estimation algorithm requires much less computation than the isotonic type algorithm used in Ma & Kosorok (2005) since the order of jumps in the step function is supposed to be much larger than the order of knots we choose for estimating and ’s.

Despite the non-root-n convergence rates of and ’s, we are able to show that is root-n consistent, asymptotically normal and semiparametric efficient. We derive the efficient information bound by taking the general two-stage projection approach from Sasieni (1992) which is needed due to the involvement of multiple nonparametric functions in semiparametric models. Interestingly, we observe the convergence rate interfere phenomenon for the B-spline estimators, i.e., the convergence rates of nonparametric estimators are all slowed down to equal the slowest one. Moreover, by approximating with the B-spline, we can avoid the monotonicity constraint in the implementation, which is usually required in the literature, e.g., Zhang et al. (2010).

The remainder of the paper is organized as follows. Section 2 describes the B-spline estimation procedure. The asymptotic properties such as consistency and convergence rates of the estimates are obtained in Section 3. The asymptotic distribution of the parametric component is studied in Section 4, and its efficient information and the corresponding explicit B-spline estimate are given in Section 5. Simulation studies are presented in Section 6.1. We close with an appendix containing technical details.

2 Semiparametric B-spline Estimation

2.1 Assumptions

We first define some notations. For any vector , . The notations and mean greater than, or smaller than, up to a universal constant. We denote if and . The notations and are used for the empirical distribution and the empirical process of the observations, respectively. Furthermore, we use the operator notation for evaluating expectation. Thus, for every measurable function and true probability ,

We next present some model assumptions.

-

M1.

and are independent given .

-

M2.

(a) The covariates are assumed to belong to a bounded subset in , say . The support for is , where ; (b) The joint density for w.r.t. Lebesgue measure stays away from zero, and the joint density for stays away from infinity.

-

M3.

is strictly positive definite.

-

M4.

The residual error distribution is assumed to be known and has support . Denote the first, second and third derivative of as , and , respectively. We assume that (a) over the whole and stays away from zero in any compact set of ; (b) for all .

Since we employ the smooth B-spline estimation rather than the penalized NPML estimation, our residue error Condition M4 is much less restrictive than that in Ma & Kosorok (2005), and may apply to more general class of semiparametric transformation models. Note that Condition M4(b) ensures the concavity of the function for .

It is easy to verify that the above Condition M4 is satisfied in the following two general classes of residue error distribution functions after some algebra.

-

F1.

for is a family of distributions, which includes the standard normal distribution after appropriate rescaling (). This corresponds to the probit model Kalbfleisch & Prentice (1980).

- F2.

2.2 B-spline Estimation Framework

From now on, we change the signs of and for simplicity of exposition. In addition, we re-center to so that for the purpose of identifiability. The additional parameter will be absorbed into the vector , i.e., the first coordinate of is set as one. Given a single observation at , the log-likelihood of model (1) is written as

| (4) | |||||

We assume that , which is a bounded open subset in , and that its true value is an interior point of . Before specifying the parameter spaces for and ’s, we first introduce the Hölder ball , which is a class of smooth functions widely used in the nonparametric estimation, e.g., Stone (1982, 1985). For any , it is times continuously differentiable on and its -th derivative is uniformly Hölder continuous with exponent , i.e.,

The functions in the Hölder ball can always be approximated by a basis expansion, i.e.,

| (5) |

where and . Actually, if the degree of the B-spline satisfies , we have

| (6) |

where denotes the supremum norm..

Assume the following parameter space Condition P1 for the smooth .

-

P1.

For and some known , we assume that the parameter space for is , where

and that the corresponding spline space is

based on a system of basis functions of degree .

As seen from the previous examples, it is reasonable to assume that is differentiable and strictly increasing over , i.e., . Considering that , we can thus write , where is well defined. Such reparametrization can get around the strict monotonicity and positivity constraints of , and thus avoids the constrained optimization in the computation. The parameter space Condition P2 for is specified below.

-

P2.

For some known , we assume that the parameter space for is , where

and that the corresponding spline space is

based on a system of basis functions of degree .

Similarly, we define . By some algebra, we can show that for some .

Remark 1.

Note that in the theoretical proofs and numerical calculations the exact values of are not necessary. Instead, only the boundedness condition, equivalently the compactness of parameter spaces and spline spaces, is needed. Here we assume this boundedness condition, which can be relaxed by invoking the chaining arguments, only for simplifying our theoretical derivations.

In this paper, we propose the B-spline approach to estimate and ’s as follows. Let and . Denote as and its true value as , where . The log-likelihood (4) for the observation can thus be reparametrized as

| (7) | |||||

The corresponding B-spline estimate is defined as

| (8) |

We can also write . Then, the estimate . Some tedious algebra reveals that the Hessian matrix of w.r.t. is indeed negative semidefinite under Condition M4(b) which guarantees the existence of . See more discussions on the computation feasibility in the simulation section. The above estimation procedure also applies to other linear sieves approximating the Hölder ball (or more generally Hölder space), e.g., wavelets.

3 Consistency and Rates of Convergence

In this section, we show that our B-spline estimate is consistent and the convergence rate of each nonparametric estimate appears to interfere with each other. Define

where is the norm. Now we give the main Theorem of this section.

Theorem 1.

Suppose that Conditions M1-M4 and P1-P2 hold. If for , then we have

| (9) |

More specifically, we further prove that

| (10) |

If we further require that for , then we have

| (11) |

where .

According to Theorem 1, the smooth can achieve the faster convergence rate, i.e., , than -rate derived in the penalized estimation context, see Ma & Kosorok (2005), when we assume that and ’s are all at least continuously differentiable, i.e., . More importantly, we can further show that is uniformly consistent, i.e., , by applying Lemma 2 in Chen & Shen (1998) that for any and noting that for some .

The above theorem also holds when we employ the constrained monotone B-spline to approximate , i.e., with . However, such constrained optimization usually requires additional computational effort, see Zhang et al. (2010).

Remark 2.

From the above Theorem 1, we observe the interesting convergence rate interfere phenomenon, i.e., the convergence rate for each B-spline estimate is forced to equal the slowest one. In Ma & Kosorok (2005), they also show that the convergence rate of the penalized estimate is unfortunately slowed down to by the NPMLE regardless of the smoothness degree of . One possible solution in achieving the optimal rate for each nonparametric estimate is to extend the most recent mixed rate asymptotic results Radchenko (2008) to the semiparametric setup.

Since we assume that , the convergence rate given in (11) is always . Such a rate is usually fast enough to guarantee the regular asymptotic behavior of , i.e., -consistency and asymptotic normality. Indeed, we will improve the current suboptimal rate of in (11) to the optimal rate, and further show that is semiparametric efficient in next section.

4 Weak Convergence of the Parametric Estimate

In this section, we study the weak convergence of the spline estimate in the presence of multiple nonparametric nuisance functions. We first calculate the semiparametric efficient information based on the projection onto the nonorthogonal sumspace.

Let

where . Denote as the true value of . The score functions (operators) for , and are separately calculated as

| (12) | |||||

| (13) | |||||

| (14) |

We assume that and so that all the score functions defined above are square integrable.

To calculate the efficient score function , we need to find the projection of onto the sumspace , where and . For simplicity, we define and as and , respectively. The same notation rule applies to and . We define

where and . And is the minimizer of

for . Similarly, denote and as and , respectively. By taking the two-stage projection approach from Sasieni (1992), we have

| (15) |

where satisfies

| (16) |

for every , and . By slightly modifying the proof of Lemma 4 in Ma & Kosorok (2005), we can show that the above nonorthogonal projection is well defined and exists by the alternating projection Theorem A.4.2 in Bickel et al. (1993).

Define and as the projection operators

respectively. Define

We say a function belongs to a uniform Hölder ball in relative to if it is continuously differentiable w.r.t. and its -th partial derivative satisfies, with ,

Define , and , where , and are the conditional densities of given , given and given w.r.t. Lebesgue measure, respectively.

Here, we assume some model assumptions implying that both and belong to some Hölder balls for any and .

-

M5.

We assume that , in relative to and in relative to for some and .

-

M6.

We assume that and in relative to for some .

Note that we can simplify to in Condition M5 and simplify to in Condition M6 when we assume that and are independent and that is pairwise independent.

Theorem 2.

Suppose that Conditions M1-M6 and P1-P2 hold. If and is invertible, then we have

| (17) |

where is the efficient information matrix defined as .

5 B-spline Estimate of the Efficient Information

In this section, we give an explicit B-spline estimate for the efficient information as a by-product of the establishment of asymptotic normality of . Indeed, it is simply the observed information matrix if we treat the semiparametric model as a parametric one after the B-spline approximation, i.e., and . Specifically, we treat defined in (7) as if it were a parametric likelihood .

We construct the corresponding information estimator for :

where , for , and

The parametric inferences imply that the information estimator for is of the form

| (18) |

Some calculations further reveal that

| (19) |

where for and where represents the -vector with its -th element as one and others as zeros. We will use (18) as our estimator for .

We need the following additional assumption for Theorem 3.

-

M7.

We assume that

Theorem 3.

Under Conditions M1-M7 and P1-P2, we have .

6 Numerical Results

6.1 Simulations

We perform a Monte-Carlo study to assess the finite-sample performance of our proposed method. To compare with the penalized NPMLE in Ma & Kosorok (2005), we adopt the same setting used in their paper. We simulate the current status data from the partly linear additive Cox model which is a special case of general transformation model. We choose where with . The errors follow an extreme value distribution with . The regression coefficients and . The covariate is Uniform and is Bernoulli with success probability . We choose as Uniform and . Censoring times are standard exponential distribution conditional on being in the interval . The sample sizes are and . We simulate realizations for both sample sizes.

In practice, the numbers of knots for and need to be determined. Common variable selection methods such as the Akaike information criterion (AIC), and the Bayesian information criterion (BIC) can be employed for selecting the optimal number of knots. In this paper, we determine by the AIC given by

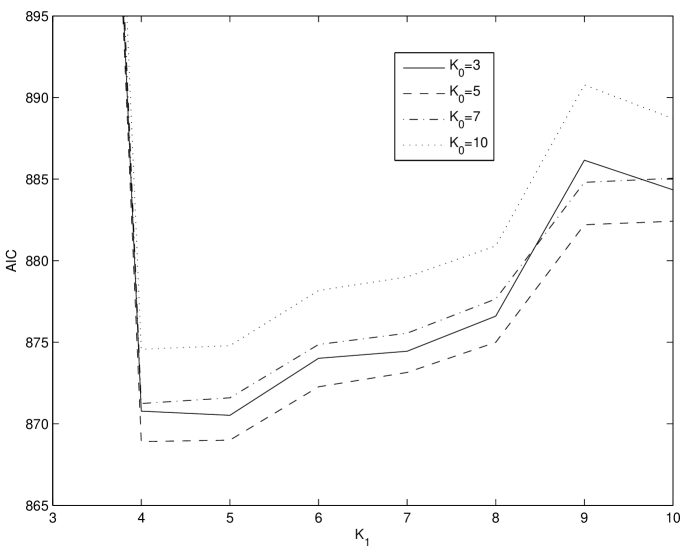

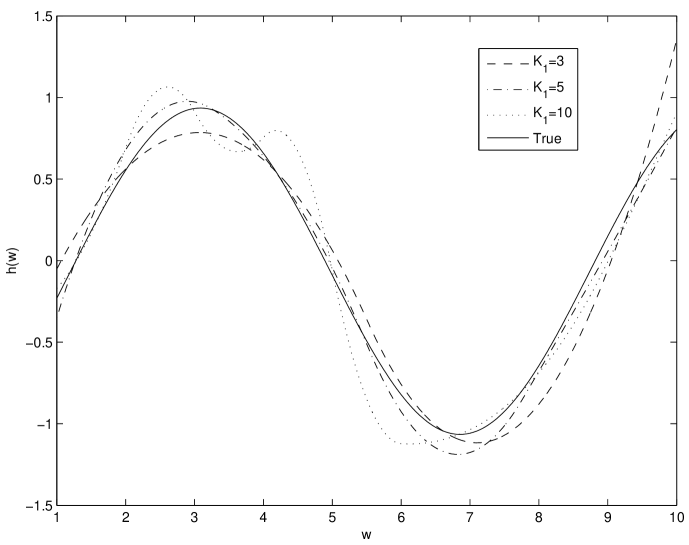

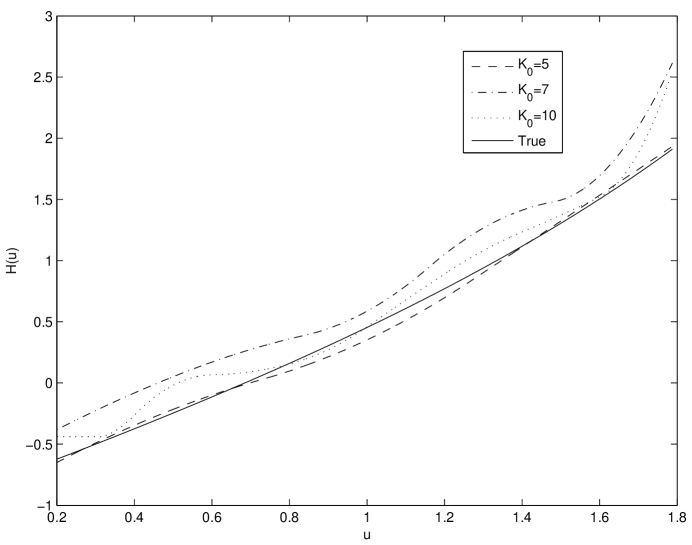

In our simulation, we use a quadratic spline to approximate both function and function in . Then, . Based on our experiences, it is generally adequate to choose less than ten knots to achieve reasonable approximation, provided that and are not overly erratic. Figure 1 shows the AIC scores under different combinations of and for one realization of the simulation with the sample size . It shows that the optimal choices for and are and , respectively. The estimated and with various values of and are plotted in Figure 2. In the left panel of Figure 2, we fix and plot the estimated with . When is small (e.g., ), there seems be to a big bias in our estimator. On the other hand, when is large (e.g., ), the estimator displays a wiggly behavior. In the right panel of Figure 2, we fix and plot the estimated with . As the number of knots is increasing, the estimated shows a similar wiggly shape. Hence, the numbers of knots should be chosen with caution.

| Sample size | Sample size | ||

|---|---|---|---|

| Bias | 0.0318 | 0.0100 | |

| SD | 0.2919 | 0.1246 | |

| ESD | 0.3102 | 0.1325 | |

| Coverage | 0.9620 | 0.9690 | |

| Bias | 0.0168 | 0.0074 | |

| SD | 0.1533 | 0.0797 | |

| ESD | 0.1612 | 0.0803 | |

| Coverage | 0.9710 | 0.9680 | |

| Joint | Coverage | 0.9620 | 0.9550 |

SD: Standard error; ESD: Estimated standard error

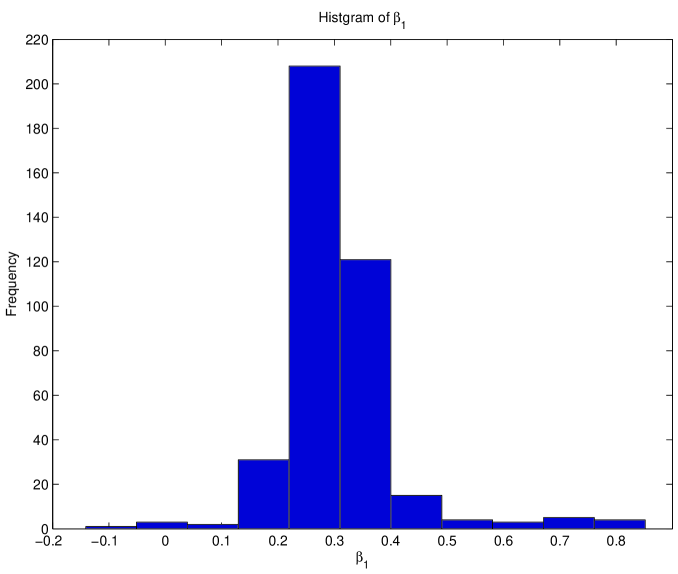

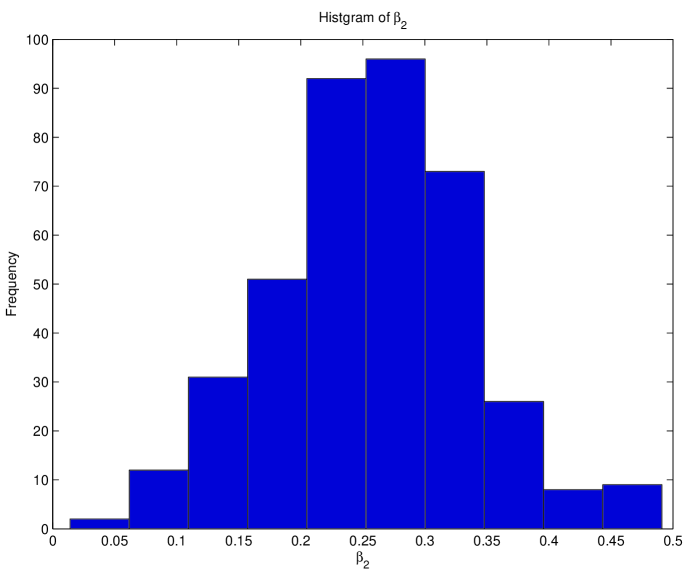

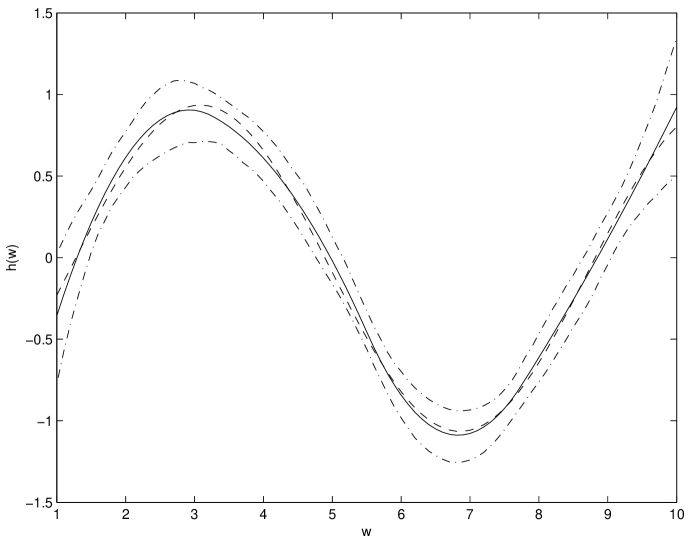

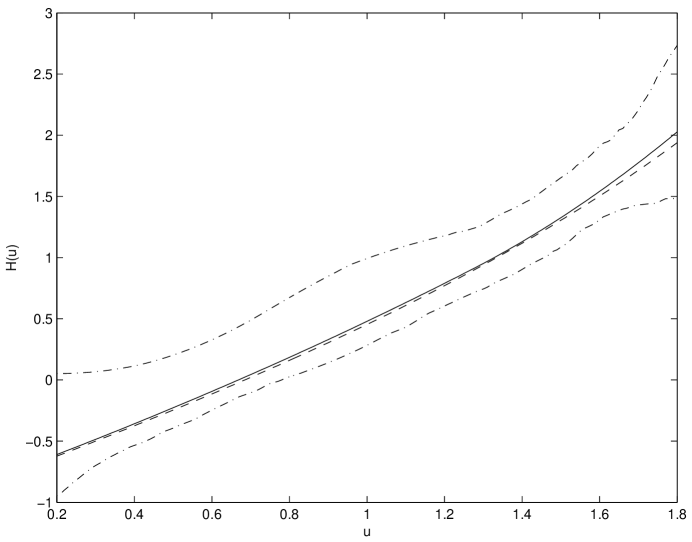

Simulation results show that our B-spline estimation procedure performs quite well in the semiparametric transformation model. The bias and standard errors of the spline estimates of and are given in Table 1. The table shows that the sample biases of both and are small. The ratio of the standard errors for the two sample sizes is close to , a result consistent with a -convergence rate for and . The estimated standard errors from (18) (denoted as ESD) are also displayed in Table 1, which are very close to the simulation results. Although our proposed method tends to overestimate the standard error slightly but the overestimation lessens as sample size increases. The 95% confidence interval constructed from (18) generally have coverage close to the nominal value. Histograms of and are shown in Figure 3. It is clear that the marginal distributions of and are Gaussian. The left panel of Figure 4 displays the spline estimate of and the monotone estimate is given in the right panel of Figure 4. The dashed line is the true function, the solid line is the average estimate over realizations, and the dash-dotted line is the 95% pointwise confidence band for or when we know the true model, which is obtained by taking percentile and percentile of these estimates at each or .

To compare our spline based method with the penalized method in Ma & Kosorok (2005), there are four obvious advantages of our method. First, the computational cost of our spline estimate is much less expensive than that used in Ma & Kosorok (2005), i.e. the cumulative sum diagram approach. This is because the number of basis B-splines (thus the number of knots), e.g., and , is often taken much smaller than the sample size , thus the dimension of the estimation problem is greatly reduced. Secondly, our estimate of the transformation function is smooth with a higher convergence rate. We obtain a narrower confidence interval for shown in the right panel of Figure 4. Thirdly, we can obtain an explicit consistent estimate . However, the block jackknife approach proposed in Ma & Kosorok (2005) is not theoretically justified. At last, we do not require the constrained optimization in our implementations.

6.2 Application: Calcification data

| extreme value distribution | logistic distribution | |

|---|---|---|

| ESD() | ||

| ESD() |

ESD: Estimated standard error

We illustrate the proposed method in a dataset from the calcification study. Yu et al. (2001) investigated the calcification of intraocular lenses, which is an infrequently reported complication of cataract treatment. Understanding the effect of some clinical variables on the time to calcification of the lenses after implantation is the objective of the study. The patients were examined by an ophthalmologist to determine the status of calcification at a random time ranging from zero to thirty six months after implantation of the intraocular lenses. The severity of calcification was graded into five categories ranging from zero to four. In our analysis, we simply treat those with severity as calcified and those with severity as not calcified. This dataset can be treated as the current status dataset because only the examination time and the calcification status at examination are available. The interesting covariates include incision length, gender ( for female and for male), and age at implantation/10. The original dataset has records. We remove the one record with missing measurement, resulting the sample size . This dataset has been studied by Xue et al. (2004), Lam & Xue (2005), and Ma (2009). Xue et al. (2004) and Lam & Xue (2005) modeled the event time directly and did not use any transformation. A straightforward estimation of the hazard function is not available. Ma (2009) used the cure model to fit the data, and assumed a generalized linear model for the cure probability. For subjects not cured, the linear and partly linear Cox proportional hazards models are used to model the survival risk.

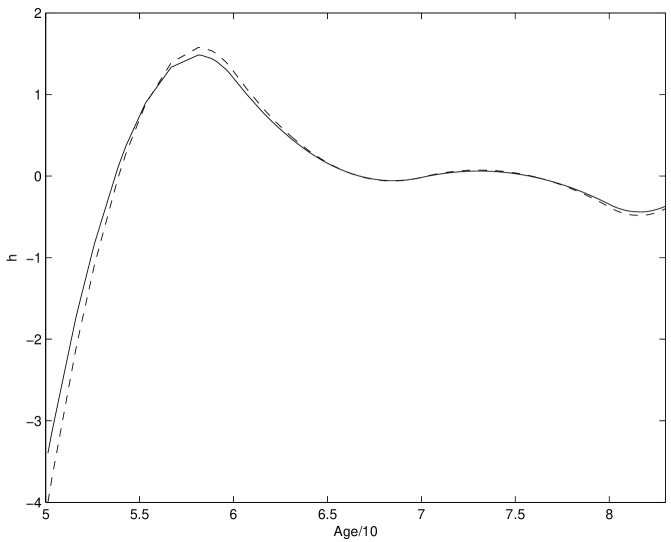

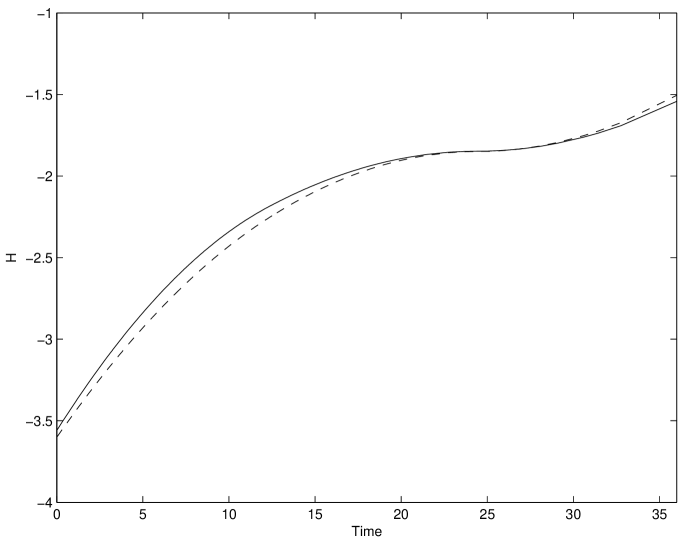

We fit this dateset using the semiparametric additive transformation model. We assume the error distribution to be one of the two distributions: extreme value distribution and logistic distribution. We approximate and by quadratic splines. The optimal choices of knots for and are and , respectively. The estimates and their corresponding estimated standard errors for the parametric part are summarized in Table 2. The estimates for based on different error distributions are displayed in the left panel of Figure 5, and the estimates of are plotted in the right panel of Figure 5. The analysis shows very similar results for these two error distributions. From Table 2, both incision length and gender are insignificant at the 5% level of significance. From the left panel of Figure 5, increases steadily from age 50, achieving a peak at age 60, decreasing gradually thereafter, which means that patients ages around 60 tend to enjoy a longer time to calcification. The estimated transformation function in the right panel of Figure 5 displays a nonlinear behavior and it shows that the transformation is necessary.

We can incorporate an unknown scale parameter into to the residual error distribution to further improve the above analysis. Our general B-spline estimation framework can also handle this type of transformation models easily.

Acknowledgement

The first author’s research is supported by the National Science Foundation under grant DMS-0906497. The second author’s research is supported by the National Science Foundation under grant CMMI-1030246 and DMS-1042967. The authors would like to thank Professor Alexis K. F. Yu for providing the Calcification data and thank Professors Michael Kosorok and Donglin Zeng for many helpful comments and suggestions to improve the paper.

Appendix

Some useful Lemmas

We define -covering number (-bracketing number) as (). The corresponding -entropy (-bracketing entropy) is defined as (). Define and . Obviously, and . Lemma 1 follows from the B-spline approximation property (6). Lemma 2 is directly implied by Lemma 2.5 in (Van de Geer, 2000). Lemma 4 is adapted from Proposition 1 in (Cheng & Huang, 2010).

Lemma 1.

There exist and such that

| (A.1) | |||||

| (A.2) | |||||

| (A.3) | |||||

| (A.4) |

where .

Lemma 2.

| (A.5) | |||||

| (A.6) |

for .

Lemma 3.

Let . Define , where the form of is defined in (A.11). We have

| (A.7) |

Proof: Define . The construction of implies that

| (A.8) |

based on (A.2), (A.4) and M4. Thus, is bounded away from zero for sufficiently large .

For any , and , we have

| (A.9) | |||||

The first and second inequalities in the above follow from the fact that is strictly positive for sufficiently large by (A.8), and Condition M4(a), respectively. As shown in (A.9), the functions in the class are Lipschitz continuous in . Therefore, by combining Lemma 2 and Theorem 2.7.11 in (Van de Geer & Wellner, 1996), we obtain that

where . In the end, we apply Lemma 3.4.2 in (Van de Geer & Wellner, 1996) to this uniformly bounded class of functions to obtain (A.7).

Lemma 4.

Suppose the following Conditions (B1)-(B3) hold.

-

B1.

, and ;

-

B2.

;

-

B3.

for satisfying .

If is consistent and is invertible, then we have

Lemma 5.

(i) If in relative to and , then in relative to .

(ii) If in relative to , then in relative to .

(iii) If in relative to and , then in relative to .

Proof: Let be the largest integer smaller than . Denote the -th derivative of w.r.t. as for .

(i) Note that is bounded for , by the dominated convergence theorem, we can take derivative inside the integral to obtain

which implies that is bounded for . Using this and the fact that

for all and , we conclude that in relative to for some .

(ii) The result is true because

is bounded for . Also we note that for ,

It can then be easily verified that

(iii) When , the result follows from the observation that

Using the chain rule, the above observation and part (ii) of the lemma, the desired result can be obtained by induction for general .

Denote

where . Let and .

Lemma 6.

Under Conditions M1-M7 & P1-P2, we have

| (A.10) |

for all and .

Proof: In view of (12)-(14) , we can bound the left hand side of (A.10) by

after some algebra. The compactness of and imply that the third and fifth term in the above are both of the order . For the second term, we can further bound it by

Considering the compactness of and , we know the second term is also of the order . Assumption M4(a) together with Cauchy-Schwartz inequality implies that . Since we assume that the density for is bounded away from zero and infinity, we have that considering the identifiability condition . Assumption M7 implies that the fourth term is of the order . Considering the form of , we conclude the whole proof.

Proof of Theorem 1

Recall that . Denote , and as the corresponding true value, B-spline approximation and sieve estimate, respectively. Recall that is bounded away from zero for sufficiently large as implied by (A.8). Then, by the definition of , we have

which implies that, by the inequality that for any and ,

| (A.11) |

Lemma 3 implies that since for any . Thus, based on (A.11). Let . Based on (A.8) we know , which further implies by the concavity of . This in turn implies that . This forces by the strict concavity of , Conditions M4(a), P1 and P2. It is easy to verify that if . Thus, we further have

Combining the above equation with the identifiability condition M3, we can show . This, in turn, implies that

Since we assume that the joint density of is bounded away from zero in M2(b), we have

Considering that for and that the joint density of is bounded away from infinity, we have . The spline approximation result (A.2) and (A.3) conclude the proof of (9).

We next verify the conditions of Theorem 3.2.5 in Van de Geer & Wellner (1996) to establish the convergence rate result (11). Recall that . Denote as its sieve estimate. Following similar arguments in proving the consistency, it suffices to show that

| (A.12) |

where . We first need to show that

| (A.13) |

for every in the neighborhood of . Define and as its second derivative w.r.t. . Since maximizes , we have

where is on the line segment between and . The compactness of the parameter spaces imply that . This completes the proof of (A.13). We next calculate the order of as a function of , denoted as , by the use of Lemma 3.4.2 of Van de Geer & Wellner (1996). Let . Using the same argument as that in the proof of Lemma 3, we obtain that is bounded by . This leads to

The compactness of and implies the uniform boundedness of any . Thus, Lemma 3.4.2 of Van de Geer & Wellner (1996) gives . By solving , we get

| (A.14) |

In the end, we show that , where . The definition of implies that

where and . A straightforward Taylor expansion gives

where is the Fréchet derivative of w.r.t. the -th argument. Considering (A.2), (A.3) and the fact that for in some compacta of , we have

| (A.15) |

for any . Let . Similar analysis in Lemma 3 show that the bracketing entropy integral (in terms of ) for is finite, thus yields that is P-Donsker. Combining this P-Donsker result and (A.15), we use Corollary 2.3.12 of Van de Geer & Wellner (1996) to conclude that . By choosing some proper satisfying , we have . We can also show by similar analysis of (A.13). This shows that

| (A.16) |

Proof of Theorem 2

We apply Lemma 4 to prove this theorem. We first check Condition B1. Obviously, since maximizes , is consistent and is an interior point of . Following the analysis in Page 2282 of Ma & Kosorok (2005), we can write, with ,

According to Lemma 5 and dominated convergence theorem, we know that under Condition M5, and (thus is uniformly bounded) for some . Then, for each , there exists a such that

| (A.17) |

by (6) and the assumption that .

Since for any , it suffices to show that

| (A.18) |

We can decompose the left hand side of (A.18) as , where

By Cauchy-Schwartz Inequality, we have based on Conditions M4(a), P1 & P2. Thus, (A.12) and (A.17) imply that since . Define and for some . As for the term , we first consider the following class of functions:

For simplicity, we write the function in as . Let . It is easy to verify that, for every ,

| (A.19) |

where for . Let and be the -cover for and , respectively. Thus, we can construct the bracket covering . The bracket size is . Hence, we obtain

based on Lemma 2. We next apply Lemma 3.4.2 in Van de Geer & Wellner (1996) to show which yields . We first calculate the -bracketing entropy integral

Note that and for any , and thus and in Lemma 3.4.2 of Van de Geer & Wellner (1996) are both chosen as , i.e., . Then, by Lemma 3.4.2 of Van de Geer & Wellner (1996) and some algebra, we have that

We have thus verified that .

We next show that by similar arguments. Similarly, we have

Recall that . Under Condition M6 and the assumption that , we can show that , which implies that for some , based on Lemma 5. We next show that and , where

and satisfies for any . Similarly, by Cauchy-Schwartz Inequality, we can show that

by choosing . Following similar arguments in analyzing , we can show that . Thus, we have verified Condition B1 in Lemma 4. We again apply Lemma 3.4.2 of Van de Geer & Wellner (1996) to verify Assumption B2. The details are skipped due to the similarity of the previous analysis.

It remains to verify Assumption B3. This can be easily established using the Taylor expansion in Banach space. However, we first need to reparameterize the efficient score function as

where , and . We first derive two useful equalities (A.23)-(A.24). Let be the expectation corresponding to the reparametrized likelihood under the parameter . Since , we have

| (A.20) |

where . Define and as the first derivative of w.r.t. and (along the direction ), respectively. By setting and , respectively, some calculations reveal that

| (A.21) | |||||

| (A.22) |

based on (A.20). By considering the orthogonal property of and the above reparametrization, we obtain the following two useful facts:

| (A.23) | |||

| (A.24) |

Define as the second order Fréchet derivative of w.r.t. along the direction at the point . The same notation rule applies to and . Now we are ready to express the Taylor expansion as follows.

where and lies between and . The last equation in the above follows from (A.23) & (A.24). Now we only need to show that the second term in the last equation is of the order

Let and . After some algebra, we obtain

where lies between and . Considering the assumption that and the previously shown result that and are both uniformly bounded, we can verify Assumption B3 based on the above expressions. This completes the proof of Theorem 2.

Proof of Theorem 3

For simplicity, we write and as and , respectively. Based on the definitions of and (19), we know their -th entry can be written as

| (A.25) | |||||

| (A.26) |

where and . It is easy to show that

| (A.27) |

since and are both assumed to be compact. Note that (A.27) implies that is P-Glivenko-Cantelli. Then, we know that, uniformly over ,

| (A.28) | |||||

by considering Corollary 9.27 of Kosorok (2008). Uniformly over , we have

| (A.29) |

where the last inequality follows from (A.10) (together with the consistency of ) & (A.27). Combining (A.28) and (A.29), we have obtained that

| (A.30) |

which implies that

| (A.31) |

To finish the proof, we need to introduce as a bridge. Now, it remains to show that

| (A.32) | |||||

| (A.33) |

We first consider (A.32). By similar analysis applied to (A.29), we know that (A.32) holds if . Denote and as and , respectively. The definition of further implies that

where the second equality follows from (A.30). By the definitions of and , we have

Therefore, we conclude the proof of (A.32) by applying (A.30) to the above inequality. We next consider (A.33). Again, by the form of given in (A.25) and similar analysis in (A.32), we only need to show . By the definitions of and , we have

where the last inequality trivially follows from the form of and . According to the analysis in the proof of Theorem 2, we know that and . Thus, we have based on the last inequality in the above. This completes the whole proof.

References

- Banerjee et al. (2006) Banerjee, M., Biswas, P. and Ghosh, D. (2006). A Semiparametric Binary Regression Model involving Monotonicity Constraints. Scandinavian Journal of Statistics, 33 673–697.

- Banerjee et al. (2009) Banerjee, M., Mukherjee, D. and Mishra, S. (2009). Semiparametric Binary Regression Models under Shape Constraints with an Application to Indian Schooling Data. Journal of Econometrics. 149 101-117.

- Bickel et al. (1993) Bickel, P., Klaassen, C.A., Ritov, Y. and Wellner, J.A. (1993). Efficient and Adaptive Estimation for Semiparametric Models. Johns Hopkins Univ. Press

- Chen & Tong (2010) Chen, K. and Tong, X. (2010). Varying Coefficient Transformation Models with Censored Data. Biometrika, 97 969–976.

- Chen & Shen (1998) Chen, X. and Shen, X. (1998). Sieve Extremum Estimates for Weakly Dependent Data. Econometrica, 66 289–314.

- Cheng & Huang (2010) Cheng, G. and Huang, J. (2010). Bootstrap Consistency for General Semiparametric M-estimation. Annals of Statistics, 38, 2884-2915.

- Dabrowska & Doksum (1988a) Dabrowska, D.M. and Doksum, K.A. (1988). Partial Likelihood in Transformation Models with Censored Data. Scandinavian Journal of Statistics, 15 1–23.

- Dabrowska & Doksum (1988b) Dabrowska, D.M. and Doksum, K.A. (1988). Estimation and Testing in a Two-Sample Generalized Odds Rate Model. Journal of American Statistical Association, 83 744–749.

- Doksum & Gasko (1990) Doksum, K.A. and Gasko, M. (1990). On a Correspondence between Models in Binary Regression Analysis and in Survival Analysis. Journal of American Statistical Association, 83 744–749.

- Huang & Rossini (1997) Huang, J. and Rossini, A.J. (1997). Sieve Estimation for the Proportional-Odds Failure-Time Regression Model with Interval Censoring. Journal of American Statistical Association, 92 960–967.

- Huang (1999) Huang, J. (1999). Efficient Estimation of the Partly Linear Additive Cox Model. Annals of Statistics, 27 1536–1563.

- Kalbfleisch & Prentice (1980) Kalbfleisch, J.D. and Prentice, R.L. (1980). The Statistical Analysis of Failure Time Data. John Wiley and Sons, New York.

- Kosorok (2008) Kosorok, M.R. (2008). Introduction to Empirical Processes and Semiparametric Inference. Springer, New York.

- Lam & Xue (2005) Lam, K.F. and Xue, H. (2005). A semiparametric regression cure model with current status data. Biometrika, 92, 573-586.

- Ma (2009) Ma, S. (2009). Cure model with current status data. Statistica Sinica, 19, 233-249.

- Ma & Kosorok (2005) Ma, S. and Kosorok, M.R. (2005). Penalized Log-likelihood Estimator for Partly Linear Transformation Models with Current Status Data. Annals of Statistics, 33 2256–2290.

- Radchenko (2008) Radchenko, P. (2008). Mixed-Rates Asymptotics. Annals of Statistics, 36 287–309.

- Sasieni (1992) Sasieni, P. (1992b). Nan-orthogonal Projections and Their Application to Calculating the Information in a Partly Linear Cox Model. Scandinavian Journal of Statistics 19 215–233.

- Shen (1998) Shen, X. (1998). Proportional Odds Regression and Sieve Maximum Likelihood Estimation. Biometrika, 85 165–177.

- Stone (1982) Stone, C. (1982). Optimal Global Rates of Convergence for Nonparametric Regression. Annals of Statistics, 10 1040–1053.

- Stone (1985) Stone, C. (1985). Additive Regression and Other Nonparametric Models. Annals of Statistics, 13 689–705.

- Van de Geer (2000) Van de Geer, S. (2000). Empirical Processes in M-Estimation. Cambridge University Press.

- Van de Geer & Wellner (1996) van der Vaart, A. W., and Wellner, J. A. (1996). Weak Convergence and Empirical Processes: With Applications to Statistics. Springer, New York

- Xue et al. (2004) Xue, H., Lam, K.F., and Li, G. (2004). Sieve maximum likelihood estimator for semiparametric regression models with current status data. Journal of the American Statistical Association, 99, 346-356.

- Yu et al. (2001) Yu, A.K.F., Kwan, K.Y.W., Chan, D.H.Y., and Fong, D.Y.T. (2001). Clinical features of 46 eyes with calcified hydrogel intraocular lenses. Journal of Cataract and Refractive Surgery, 27, 1596-1606.

- Zhang et al. (2010) Zhang, Y., Hua, L. and Huang, J. (2010). A Spline-based Semiparametric Maximum Likelihood Estimation Method for the Cox Model with Interval-Censored Data, Scandinavian Journal of Statistics 37 338-354.