Hidden Markov Mixture Autoregressive Models: Stability and Moments

Abstract

This paper introduces a new parsimonious structure for mixture of autoregressive models. The weighting coefficients are determined through latent random variables, following a hidden Markov model. We propose a dynamic programming algorithm for the application of forecasting. We also derive the limiting behavior of unconditional first moment of the process and an appropriate upper bound for the limiting value of the variance. This can be considered as long run behavior of the process. Finally we show convergence and stability of the second moment. Further, we illustrate the efficacy of the proposed model by simulation and forecasting.

MSC: primary 62M10, 60J10 secondary 60G25

Keywords and phrases. Hidden Markov Model, Mixture Autoregressive Model, Stability, Dynamic Programming, Forecasting.

1 Introduction

The most frequently used approaches to time series model building assume that the data under study are generated from a linear stochastic process. Linear models provide a number of appealing properties (such as physical interpretations, frequency domain analysis, asymptotic results, statistical inference and many others)[7]. Despite those advantages, it is well known that real-life systems are usually nonlinear, and certain features, such as limit-cycles, asymmetry [13],[17], conditional heteroscedasticity [9], flat stretches, bursts [14] and jump phenomena cannot be correctly captured by linear statistical models.

Since the Mixture Transition Distribution (MTD) was originally introduced by Raftery [19] for modeling high order Markov chains in the discrete state space, the broad family of this model have been extended and applied for modeling conditional distribution of observations in the context of nonlinear time series with arbitrary state spaces [3]. This model also has been extended to the mixture transition of Gaussian distributions, known as GMTD, which contains autoregressive model as a special case, for modeling flat stretches, bursts and outliers [14]. Mixture of Autoregressive (MAR) model (which has been proposed by Wong and Li [21]) is a flexible generalization of GMTD to model processes with multimodal conditional distributions and conditional heteroscedasticity. The important feature of MAR model is that it can be considered as the mixture of some stationary and non-stationary AR processes and remains stationary. For time series , , the MAR() is defined as

| (1) |

in which denotes a realization of , and and is the conditional distribution of given information of . Also are the weighting coefficients (i.e. and .) and is the cumulative distribution function of the standard normal distribution. This model is a mixture of Gaussian AR(), models [21].

The mixture of autoregressive conditional heteroscedasticity model was also proposed by Wong and Li [22] to capture the squared autocorrelation structure of observations. Berchtold [2] also introduced a new approach for modeling heteroscedastic time series with MTD model in which the variances of each Gaussian distributions depends on the past time series observations. For exhaustive review of MTD model see [3].

In the MTD models the contribution of distributions are always fixed and it is not sensitive to the past observations. However for real processes one might expect better forecast interval if additional information from the past were allowed to affect [9]. Another approach to study mixture models is to introduce some latent variables , which are iid and given is independent of . Each variable has a discrete distribution with support with probability masses as the weighting coefficients in the mixture model. Since these models do not consider the dependency structure of latent variables, the dynamics of weighting coefficients can not be modeled. For finite state space time series, Bartolucci and Farcomeni [1] studied a generalization of mixture transition models with hidden Markov models.

In this paper, we propose a new approach to model conditional distribution of given past information for nonlinear time series in general state space (i.e. ). We use latent Markov process as an appropriate tool to consider the effect of past information and build a parsimonious model; the idea of Markov switching models (see Hamilton [12], Mcculloch and Tsay [18]) for process . Our new model includes the hidden Markov model (HMM) [6] as a special case and it also generalizes MAR model in a sensible way. This model makes use of the whole past information to maximize the posterior probability of (given observed ) and predicts the probability of by the Markov assumption of the latent process. Although using all past observations could increase the complexity of the model, we propose a dynamic programming algorithm which reduces the volume of calculations for forecasting. We derive the limiting behavior of the first unconditional moment of the process, and obtain an upper bound for the limit of variance. We also investigate the existence and stability of the second moment.

This paper is organized as follows. Hidden Markov Mixture Autoregressive (HM-MAR) model is introduced in section 2. Section 3 is devoted to the statistical properties of the HM-MAR model. Section 4 analyzes the efficiency of the proposed model through simulation and comparison of the forecast errors with the MAR model. Section 5 concludes the paper.

2 Hidden Markov Mixture Autoregressive Model

Let be a sequence of random variables in where is a realization of . Also let and respectively represent the sigma-field of all information up to time , and the conditional distribution function of (given past information and ). In addition denotes a hidden or latent process, a positive recurrent Markov chain on a finite set . The initial conditional probabilities are

| (2) |

with transition probability matrix

| (3) |

in which

| (4) |

and invariant probability measure

| (5) |

where .

We consider to have a Hidden Markov-Mixture Autoregressive, HM-MAR(), model with normal distributions, lagged observations in the AR processes, if the conditional distribution of given is defined as follows:

-

i.

For

(6) -

ii.

For

(7)

where and is the standard normal distribution function.

In fact latent random variables determine the contribution of distributions in the mixture model and conditioning on . We assume is -tuple Markov, independent of . In other words, by conditioning on and , is independent of and .

The novelty of HM-MAR model is that the contribution of each distribution in the mixture structure is not of predefined fixed form. It makes use of the all past observations from up to . The hidden Markov assumption of the process , enables us to build a parsimonious model.

The MAR model [21] can be considered as a special case of such a HM-MAR model (6-7), in which the transition matrix of the process has identical rows (i.e. for all . That is are independent and identically distributed) with .

HM-MAR model will also lead to hidden Markov model in general state space where is considered to be zero in (7) (i.e. given , is independent of past observations).

3 Statistical Properties of the Model

In this section, we discuss the statistical properties of the HM-MAR model. We propose a dynamic programming approach to calculate conditional expectation and variance of the process. We also investigate the long run behavior of the first order HM-MAR() process, including limiting behavior of the unconditional first moment, and an appropriate upper bound for the limiting value of the variance. Finally convergence and stability of second moment is proved.

3.1 Forecasting

In HM-MAR model (6-7), the conditional expectation as the least square predictor (page 64 of [7]) of the process for is obtained by

| (8) |

where is measurable .

One of the main areas for modeling conditional heteroscedasticity (changes in the conditional variance) is the family of ARCH models [11], originally proposed by Engle [9] in the context of financial time series. In the class of MTD models, MAR [21] and MAR-ARCH [22] models also provide a mechanism to capture this effect. However in these models only changes in conditional mean of each distribution affect the conditional variance of process. The conditional variance of HM-MAR model is given by

| (9) | |||||

in which is the conditional mean of th distribution (i.e. ). Let be a random variable which takes values with probabilities for , then can be interpreted as the conditional variance of given all past observations. This amount is small (large) when all conditional means are equal (largely different). Relation (9) shows the impact of conditional mean and weighting coefficients on the value of conditional variance of given all past information. This is the merit of the HM-MAR model and its capability to model conditional heteroscedasticity as a function of simultaneous changes in the weighting coefficients as well as conditional mean of each distribution.

At each time step , (in equations (8) and (9)) can be determined via a dynamic programming method based on forward recursion algorithm, proposed in remark 3.1.

Remark 3.1.

Proof.

Another characteristic of HM-MAR is modeling the all past observations and benefits from a dynamic programming approach. This will in turn minimize the volume of calculations for forecasting. The intermediate results and in fact the last state is stored for different values of which could be used to update the process, see (10-11).

3.2 Stability

In this section, we investigate the stability of moments for the nonlinear process that admits a HM-MAR() model. This process is represented as a random coefficient autoregressive process of order one, in which the autoregressive coefficients are functions of the latent random variables ,, (see Equations (2)-(5)). Let random variables and respectively take values for , and , where and , are used in HM-MAR model (6-7) with . We consider

| (12) |

where is a Gaussian IID(0,1) process, independent of the hidden process . The conditional distribution of the process in Equation (12) is determined as

in which is given by remark 3.1. By the Gaussian distribution of in (12), we have

Notice that the process is not necessarily a Markov process, however the extended process with is Markov [23].

Timmermann [20] derived the moments of a class of stationary Markov switching models with state-dependent autoregressive dynamics and conditional mean, . Our approach for deriving the limiting behavior of first and second moments of the process is not based on the stationary assumption of the model.

Let’s define the diagonal matrixes

for possible values of random variables and in equation (12) where is a vector.

Lemma 3.1.

Let be a HM-MAR() process defined by (12), then for

| (16) |

Proof.

By the Markov property of we have that

So

So for vector of conditional expectations of given different values of , we have the following recursive equation

| (23) | |||

| (27) | |||

| (31) | |||

| (41) | |||

| (45) |

in which the recursion starts at as

| (52) | |||||

| (59) | |||||

Thus the solution of recursive equation (45) is given by

| (73) |

∎

Lemma 3.2.

Proof.

Lemma 3.3.

If all eigenvalues of lie inside the unite circle then under conditions of lemma 3.2

-

i.

-

ii.

Also if all eigenvalues of lie inside the unite circle then

-

i.

-

ii.

Proof.

Lemma 3.4.

If then under conditions of lemma 3.3

Proof.

Theorem 3.1.

Let follows the HM-MAR() model, defined by (12), and the following assumptions hold

-

i.

is an ergodic Markov chain starting from its invariant probability measure specified in equation (5),

-

ii.

,

-

iii.

All eigenvalues of and lie inside the unit circle,

then the process is asymptotically stable in mean and

| (84) |

Proof.

One interesting feature of Theorem 3.1 is that HM-MAR model could consist of some explosive (with ) and non-explosive autoregressive processes and it remains asymptotically stable in mean.

Definition 3.1.

Let be the spectral radius of

Lemma 3.5.

Proof.

By definition of spectral radius wee have that the absolute values of all eigenvalues of are less than or equal to , so by the lemma assumption about , we have that for all values of , thus by the method of iterative conditioning

| (89) | |||||

in which . Iterating (89) we get

| (90) |

thus

| (91) |

Now by Cauchy Schwarz inequality,

thus

and summing up for different values of to ,

| (92) |

Theorem 3.2.

Proof.

Using (86) we have

| (95) | |||||

by independence of Gaussian IID(0,1) process, from , (as indicated in (12)), we have

| (96) |

Remark 3.2.

Theorem 3.3.

Proof.

Let random variable be defined as

By monotone convergence theorem (theorem 16.2 of [5]) . By the assumption of theorem 3.2, we deduce that spectral radius of lies inside the unit circle, so by a similar method as used to obtain (88) in lemma 3.5, we have

| (99) |

So by (99),lemma 3.5 and Cauchy Schwarz inequality we have that

| (100) | |||||

By the assumption, all eigenvalues of lie inside the unit circle, so by a similar method as used to obtain (83) we have that

Therefor using inequality (100) instead of (96) in the proof of theorem 3.2 , relation (94) changes to , we get

Thus is integrable, so is integrable. Also by triangular inequality we have for all and thus for all , , where

So by continuous mapping theorem [4] we have that almost surely. Finally implies that , so by the integrability of , and dominated convergence theorem (theorem 16.4 of [5]) we conclude that exists and

∎

4 Simulation

The hidden process in (6-7) is assumed to follow a first order Markov structure, so HM-MAR can be considered as a generalization of MAR model. Clarifying, MAR model can be considered as HM-MAR model with independent hidden process . However, HM-MAR model is more complex, using the past observations to determine the next coefficients, and demanding a longer calculation to estimate the parameters and dynamically updating the weighting coefficients.

In this section, we investigate the efficiency of these models for time series where follow a first order Markov process. To this end, observations are generated from the following HM-MAR model:

with , (that is starting from the first model ,) , and transition probability matrix . We used EM [16] algorithm to estimate the conditional probability of hidden variable given (i.e. ), and Baum-Welch [15] algorithm to estimate the joint conditional probability of given (i.e. . Using these estimations we get the following HM-MAR model

with and , and

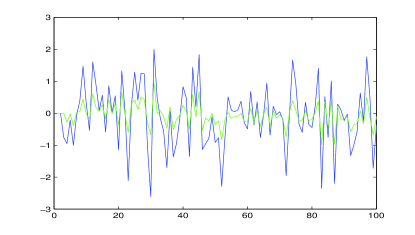

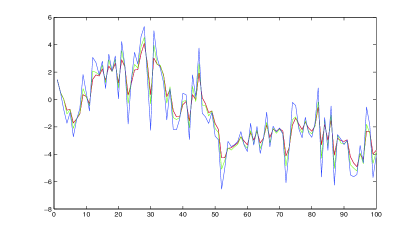

is the estimated MAR model. In figure 1, the left figure shows the sample path of forecasting errors by MAR model(blue) and forecasting errors by HM-MAR model(green). The right one presents the sample path of simulated HM-MAR model(red), forecasted observations by MAR(blue) and forecasted observations by HM-MAR model(green). We observe that HM-MAR model produces significantly smaller forecasting errors than MAR model and a better approximation for the time series. In table 1 sum of the absolute forecast errors for MAR and HM-MAR models for ten iterations are presented.

| Iterations | 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|---|

| HM-MAR | 27.7559 | 27.7590 | 27.7560 | 27.7559 | 27.7576 | |

| MAR | 75.1827 | 75.0973 | 75.2079 | 75.0839 | 75.2378 | |

| Iterations | 6 | 7 | 8 | 9 | 10 | |

| HM-MAR | 27.7580 | 27.7567 | 27.75657 | 27.7566 | 27.7569 | |

| MAR | 75.1054 | 75.1464 | 75.1338 | 75.09641 | 75.2176 |

5 Summary and discussions

We proposed HM-MAR model as a flexible structure for modeling conditional distribution of given past observations in a nonlinear time series. We considered HM-MAR model as the mixture of some Gaussian distributions where the mean of each distribution follows an AR(p) model. Unlike the ordinary mixture models, the weighting coefficients determining the contribution of distributions are not of predefined fixed form (constant values). These values are conditional probabilities of a latent variable given past observations . At each time step , the coefficients are determined through maximizing the posterior probability of latent variable given past information. Latent variables are assumed to follow a Markov process to build a parsimonious model. A suitable application for HM-MAR model is when the process is a result of some processes, and the contribution of each process changes over time. If such effects are not present in time series then our model automatically will reduce to the ordinary mixture models. HM-MAR model will also lead to hidden Markov model for continuous process where is zero (i.e. given , is independent of past observations).

Although modeling the effect of all past information makes the model complicated, a dynamic programming method is proposed for forecasting. It is worth mentioning that it is still possible to study some properties of , such as asymptotic behavior of first moment, existence and finiteness of second moment and deriving the upper bound of asymptotic variance of process. Although the variances of each distribution in the mixture model are constant, the conditional variance of the process in HM-MAR model is not fixed. This feature can be used to model conditional volatility effects frequently presented in financial time series. Another interesting feature is that the first order HM-MAR() model can be considered as a mixture of some explosive autoregressive processes (i.e. ) and the non-explosive ones (i.e. ). However, it is still asymptotically stable in first and second order.

This work has the potential to be applied in the context of nonlinear time series by imposing hidden Markov property for the weighting coefficients of mixture model. Also it can elaborate further researches for extending the stability results to the case of HM-MAR(), where the lag of autoregressive processes is of order . Stationarity and ergodicity are two major aspects. Finally this area of research can be expanded by considering other distributions besides the Gaussian as the underling distribution of mixture model.

References

- [1] Francesco Bartolucci and Alessio Farcomeni, A note on the mixture transition distribution and hidden markov models, Journal of Time Series Analysis 31 (2010), no. 2, 132–138.

- [2] Andr Berchtold, Mixture transition distribution (mtd) modeling of heteroscedastic time series, Computational Statistics & Data Analysis 41 (2003), no. 3-4, 399 – 411.

- [3] Andr Berchtold and Adrian E. Raftery, The mixture transition distribution model for high-order markov chains and non-gaussian time series, Statistical Science 17 (2002), no. 3, pp. 328–356 (English).

- [4] P. Billingsley, Convergence of probability measures, Wiley series in probability and statistics: Probability and statistics, Wiley, 1999.

- [5] , Probability and Measure, 3rd ed., Wiley India Pvt. Ltd., 2008.

- [6] C.M. Bishop, Pattern recognition and machine learning, Information science and statistics, Springer, 2006.

- [7] P.J. Brockwell and R.A. Davis, Time Series: Theory and Methods, Springer Series in Statistics, Springer, 2009.

- [8] K.B. Datta, Matrix and Linear Algebra, Prentice-Hall Of India Pvt. Ltd., 2004.

- [9] Robert F Engle, Autoregressive conditional heteroscedasticity with estimates of the variance of united kingdom inflation, Econometrica 50 (1982), no. 4, 987–1007.

- [10] J. Fan and Q. Yao, Nonlinear time series: nonparametric and parametric methods, Springer series in statistics, Springer, 2005.

- [11] C. Francq and J.M. Zakoian, GARCH Models: Structure, Statistical Inference and Financial Applications, John Wiley & Sons, 2010.

- [12] James D. Hamilton, Analysis of time series subject to changes in regime, Journal of Econometrics 45 (1990), no. 1-2, 39–70.

- [13] Tze Leung Lai and Samuel Po-Shing Wong, Stochastic neural networks with applications to nonlinear time series, Journal of the American Statistical Association 96 (2001), no. 455, pp. 968–981 (English).

- [14] Nhu D. Le, R. Douglas Martin, and Adrian E. Raftery, Modeling flat stretches, bursts, and outliers in time series using mixture transition distribution models, Journal of the American Statistical Association 91 (1996), no. 436, pp. 1504–1515 (English).

- [15] I.L. MacDonald and W. Zucchini, Hidden Markov and other models for discrete-valued time series, Monographs on statistics and applied probability, Chapman & Hall, 1997.

- [16] G.J. McLachlan and T. Krishnan, The EM algorithm and extensions, Wiley series in probability and statistics, Wiley-Interscience, 2008.

- [17] M.C. Medeiros and A. Veiga, A hybrid linear-neural model for time series forecasting, Neural Networks, IEEE Transactions on 11 (2000), no. 6, 1402 – 1412.

- [18] McCulloch R. E. and Tsay R. S., Statistical analysis of economic time series via markov switching models, Journal of Time Series Analysis 15 (1994), no. 6, 523 – 539.

- [19] Adrian E. Raftery, A model for high-order markov chains, Journal of the Royal Statistical Society. Series B (Methodological) 47 (1985), no. 3, pp. 528–539 (English).

- [20] Allan Timmermann, Moments of markov switching models, Journal of Econometrics 96 (2000), no. 1, 75–111.

- [21] Chun Shan Wong and Wai Keung Li, On a mixture autoregressive model, Journal of the Royal Statistical Society. Series B (Statistical Methodology) 62 (2000), no. 1, pp. 95–115 (English).

- [22] , On a mixture autoregressive conditional heteroscedastic model, Journal of the American Statistical Association 96 (2001), no. 455, pp. 982–995 (English).

- [23] J.-F. Yao and J.-G. Attali, On stability of nonlinear ar processes with markov switching, Advances in Applied Probability 32 (2000), no. 2, pp. 394–407 (English).