Default Swap Games Driven by Spectrally Negative LÉvy Processes∗

Abstract.

This paper studies game-type credit default swaps that allow the protection buyer and seller to raise or reduce their respective positions once prior to default. This leads to the study of an optimal stopping game subject to early default termination. Under a structural credit risk model based on spectrally negative Lévy processes, we apply the principles of smooth and continuous fit to identify the equilibrium exercise strategies for the buyer and the seller. We then rigorously prove the existence of the Nash equilibrium and compute the contract value at equilibrium. Numerical examples are provided to illustrate the impacts of default risk and other contractual features on the players’ exercise timing at equilibrium.

Keywords: optimal stopping games; Nash equilibrium; Lévy processes; scale function; credit default swaps

JEL Classification: C73, G13, G33, D81

Mathematics Subject Classification (2010): 91A15, 60G40, 60G51, 91B25

1. Introduction

Credit default swaps (CDSs) are among the most liquid and widely used credit derivatives for trading and managing default risks. Under a vanilla CDS contract, the protection buyer pays a periodic premium to the protection seller in exchange for a payment if the reference entity defaults before expiration. In order to control the credit risk exposure, investors can adjust the premium and notional amount prior to default by appropriately combining a market-traded default swaption with a vanilla CDS position, or use the over-the-counter traded products such as the callable CDSs (see [9, Chapter 21]). In a recent related work [27], we studied the optimal timing to step up or down a CDS position under a general Lévy credit risk model.

The current paper studies the game-type CDSs that allow both the protection buyer and seller to change the swap position once prior to default. Specifically, in the step-up (resp. step-down) default swap game, as soon as the buyer or the seller, whoever first, exercises prior to default, the notional amount and premium will be increased (resp. decreased) to a pre-specified level upon exercise. From the exercise time till default, the buyer will pay the new premium and the seller is subject to the new default liability. Hence, for a given set of contract parameters, the buyer’s objective is to maximize the expected net cash flow while the seller wants to minimize it, giving rise to a two-player optimal stopping game.

We model the default time as the first passage time of a general exponential Lévy process representing some underlying asset value. The default event occurs either when the underlying asset value moves continuously to the lower default barrier, or when it jumps below the default barrier. This is an extension of the original structural credit risk approach introduced by Black and Cox [8] where the asset value follows a geometric Brownian motion. As is well known [13], the incorporation of unpredictable jump-to-default is useful for explaining a number of market observations, such as the non-zero short-term limit of credit spreads. Other related credit risk models based on Lévy and other jump processes include [10, 19, 34].

The default swap game is formulated as a variation of the standard optimal stopping games in the literature (see, among others, [14, 17] and references therein). However, while typical optimal stopping games end at the time of exercise by either player, the exercise time in the default swap game does not terminate the contract, but merely alters the premium forward and the future protection amount to be paid at default time. In fact, since default may arrive before either party exercises, the game may be terminated early involuntarily.

The central challenge of the default swap games lies in determining the pair of stopping times that yield the Nash equilibrium. Under a structural credit risk model based on spectrally negative Lévy processes, we analyze and calculate the equilibrium exercise strategies for the protection buyer and seller. In addition, we determine the equilibrium premium of the default swap game so that the expected discounted cash flows for the two parties coincide at contract inception.

Our solution approach starts with a decomposition of the default swap game into a combination of a perpetual CDS and an optimal stopping game with early termination from default. Moreover, we utilize a symmetry between the step-up and step-down games, which significantly simplifies our analysis as it is sufficient to study either case. For a general spectrally negative Lévy process (with a non-atomic Lévy measure), we provide the conditions for the existence of the Nash equilibrium. Moreover, we derive the buyer’s and seller’s optimal threshold-type exercise strategies using the principle of continuous and smooth fit, followed by a rigorous verification theorem via martingale arguments.

For our analysis of the game equilibrium, the scale function and a number of fluctuation identities of spectrally negative Lévy processes are particularly useful. Using our analytic results, we provide a bisection-based algorithm for the efficient computation of the buyer’s and seller’s exercise thresholds as well as the equilibrium premium, illustrated in a series of numerical examples. Other recent applications of spectrally negative Lévy processes include derivative pricing [1, 2], optimal dividend problem [3, 24, 29], and capital reinforcement timing [16]. We refer the reader to [23] for a comprehensive account.

To our best knowledge, the step-up and step-down default swap games and the associated optimal stopping games have not been studied elsewhere. There are a few related studies on stochastic games driven by spectrally negative or positive Lévy processes; see e.g. [4] and [5]. For optimal stopping games driven by a strong Markov process, we refer to the recent papers by [17] and [31], which study the existence and mathematical characterization of Nash equilibrium. Other game-type derivatives in the literature include Israeli/game options [21, 22], defaultable game options [6], and convertible bonds [20, 33].

The rest of the paper is organized as follows. In Section 2, we formulate the default swap game under a general Lévy model. In Section 3, we focus on the spectrally negative Lévy model and analyze the Nash equilibrium. Section 4 provides the numerical study of the default swap games for the case with i.i.d. exponential jumps. Section 5 concludes the paper and presents some ideas for future work. All proofs are given in the Appendix.

2. Game Formulation

On a complete probability space , we assume there exists a Lévy process and denote by the filtration generated by . The value of the reference entity (a company stock or other assets) is assumed to evolve according to an exponential Lévy process , . Following the Black-Cox [8] structural approach, the default event is triggered by crossing a lower level . Without loss of generality, we can take by shifting the initial value . Henceforth, we shall work with the default time

where by convention. We denote by the probability law and the expectation with .

We consider a default swap contract that gives the protection buyer and seller an option to change the premium and notional amount before default for a fee, whoever exercises first. Specifically, the buyer begins by paying premium at rate over time for a notional amount to be paid at default. Prior to default, the buyer and the seller can select a time to switch to a new premium and notional amount . When the buyer exercises, she is incurred the fee to be paid to the seller; when the seller exercises, she is incurred to be paid to the buyer. If the buyer and the seller exercise simultaneously, then both parties pay the fee upon exercise. We assume that , , , , , (see also Remark 2.2 below).

Let be the set of all stopping times smaller than or equal to the default time. Denote the buyer’s candidate exercise time by and seller’s candidate exercise time by , and let be the positive risk-free interest rate. Given any pair of exercise times , the expected cash flow to the buyer is given by

| (2.1) |

To the seller, the contract value is . Naturally, the buyer wants to maximize over whereas the seller wants to minimize over , giving rise to a two-player optimal stopping game.

This formulation covers default swap games with the following provisions:

-

(1)

Step-up Game: if and , then the buyer and the seller are allowed to increase the notional amount once from to and the premium rate from to by paying the fee (if the buyer exercises) or (if the seller exercises).

-

(2)

Step-down Game: if and , then the buyer and the seller are allowed to decrease the notional amount once from to and the premium rate from to by paying the fee (if the buyer exercises) or (if the seller exercises). When , we obtain a cancellation game which allows the buyer and the seller to terminate the contract early.

Our primary objective is to determine the pair of stopping times , called the saddle point, that constitutes the Nash equilibrium:

| (2.2) |

Remark 2.1.

A related concept is the Stackelberg equilibrium, represented by the equality , where and . See e.g. [17] and [31]. These definitions imply that . The existence of the Nash equilibrium (2.2) will also yield the Stackelberg equilibrium via the reverse inequality:

Herein, we shall focus our analysis on the Nash equilibrium.

Our main results on the Nash equilibrium are summarized in Theorems 3.1-3.2 for the spectrally negative Lévy case. As preparation, we begin our analysis with two useful observations, namely, the decomposition of and the symmetry between the step-up and step-down games.

2.1. Decomposition and Symmetry

In standard optimal stopping games, such as the well-known Dynkin game [14], random payoffs are realized at either player’s exercise time. However, our default swap game is not terminated at the buyer’s or seller’s exercise time. In fact, upon exercise only the contract terms will change, and there will be a terminal transaction at default time. Since default may arrive before either party exercises the step-up/down option, the game may be terminated early involuntarily. Therefore, we shall transform the value function into another optimal stopping game that is more amenable for analysis.

First, we define the value of a (perpetual) CDS with premium rate and notional amount by

| (2.3) |

where

| (2.4) |

is the Laplace transform of . Next, we extract this CDS value from the value function . Let

| (2.5) |

Proposition 2.1 (decomposition).

For every and , the value function admits the decomposition

where is defined by

| (2.6) |

with

| (2.7) | ||||

| (2.8) | ||||

| (2.9) |

Comparing (2.3) and (2.7), we see that , which means that the buyer receives the CDS value at the cost of if she exercises before the seller. For the seller, the payoff of exercising before the buyer is . Hence, in both cases the fees and can be viewed as strike prices.

Since does not depend on , Proposition 2.1 implies that finding the saddle point for the Nash equilibrium in (2.2) is equivalent to showing that

| (2.10) |

If the Nash equilibrium exists, then the value of the game is , According to (2.5), the problem is a step-up (resp. step-down) game when and (resp. and ).

Remark 2.2.

If , then it follows from (2.7)-(2.9) that and

In this case, the choice of yields the equilibrium (2.10) with equalities, so the default swap game is always trivially exercised at inception by either party. For similar reasons, we also rule out the trivial case with or (even with ). Furthermore, we ignore the contract specifications with since they mean paying more (resp. less) premium in exchange for a reduced (resp. increased) protection after exercise. Henceforth, we proceed our analysis with and .

Next, we observe the symmetry between the step-up and step-down games.

Proposition 2.2 (symmetry).

For any , we have .

Applying Proposition 2.2 to the Nash equilibrium condition (2.10), we deduce that if is the saddle point for the step-down default swap game with , then the reversed pair is the saddle point for the step-up default swap game with . Consequently, the symmetry result implies that it is sufficient to study either the step-down or the step-up default swap game. This significantly simplifies our analysis. Henceforth, we solve only for the step-down game.

Also, we notice from (2.1) that if , then the seller’s benefit of a reduced exposure does not exceed the fee, and therefore, should never exercise. As a result, the valuation problem is reduced to a step-down CDS studied in [27], and so we exclude it from our analysis here. With this observation and Remark 2.2, we will proceed with the following assumption without loss of generality:

Assumption 2.1.

We assume that , and .

2.2. Candidate Threshold Strategies

In the step-down game, the protection buyer has an incentive to step-down when default is less likely, or equivalently when is sufficiently high. On the other hand, the protection seller tends to exercise the step-down option when default is likely to occur, or equivalently when is sufficiently small. This intuition leads us to conjecture the following threshold strategies, respectively, for the buyer and the seller:

for . Clearly, . For , we denote the candidate value function

| (2.11) |

for every . The last equality follows since implies that , and a.s.

In subsequent sections, we will identify the candidate exercise thresholds and simultaneously by applying the principle of continuous and smooth fit:

| (2.12) | ||||

| (2.13) |

if these limits exist.

3. Solution Methods for the Spectrally Negative Lévy Model

We now define to be a spectrally negative Lévy process with the Laplace exponent

| (3.1) |

where , is called the Gaussian coefficient, and is a Lévy measure on such that

. See [23, p.212]. It admits a unique decomposition:

| (3.2) |

where is the continuous martingale (Brownian motion) part and is the jump and drift part of . Moreover,

| (3.3) |

If this condition (3.3) is satisfied, then the Laplace exponent simplifies to

| (3.4) |

where . Recall that has paths of bounded variation if and only if and (3.3) holds. We ignore the case when is a negative subordinator (decreasing a.s.). This means that we require to be strictly positive if and (3.3) holds. We also assume the following and also Assumption 3.2 below.

Assumption 3.1.

We assume that the Lévy measure does not have atoms.

3.1. Main Results

We now state our main results concerning the Nash equilibrium and its associated saddle point. We will identify the pair of thresholds for the seller and buyer at equilibrium. The first theorem considers the case , where the seller exercises at a level strictly above zero.

Theorem 3.1.

Suppose . The Nash equilibrium exists with saddle point satisfying

| (3.5) |

Here as in (2.11) and can be expressed in terms of the scale function as we shall see in Subsection 3.2. In particular, the case reflects that and is the expected value when the buyer never exercises and the seller’s strategy is . The value function can be computed using (3.21) and (3.30) below.

The case may occur, which is more technical and may not yield the Nash equilibrium. To see why, we notice that a default happens as soon as touches zero. Therefore, in the event that continuously passes (creeps) through zero, the seller would optimally seek to exercise at a level as close to zero as possible. Nevertheless, this timing strategy is not admissible, though it can be approximated arbitrarily closely by admissible stopping times.

As shown in Corollary 3.1 below, the case is possible only if the jump part of is of bounded variation (see (3.3)). This is consistent with our intuition because if jumps downward frequently, then the seller has the incentive to step down the position at a level strictly above zero. On the other hand, when (with no Gaussian component), the process never goes through continuously the level zero, so even with the Nash equilibrium in Theorem 3.1 still holds. In contrast, if , then an alternative form of “equilibrium” is attained, namely,

| (3.6) |

where

Here, the functions and correspond to the limiting case where the seller exercises arbitrarily close to the default time . However, since the seller cannot predict the default time, this timing strategy is not admissible and (3.6) is not the Nash equilibrium. In practice, given the buyer’s strategy , the seller’s value function can be approximated with an -optimal strategy by choosing for a sufficiently low exercise level .

Let us summarize our equilibrium results for the case .

Theorem 3.2.

In the remainder of this section, we take the following steps to prove the existence of and Theorems 3.1-3.2:

-

(1)

In Section 3.2, we express the candidate value function in terms of the Lévy scale function.

-

(2)

In Section 3.3, we establish the sufficient conditions for continuous and smooth fit.

- (3)

-

(4)

In Section 3.5, we verify the optimality of the candidate optimal exercise strategies.

Furthermore, in Section 3.4 we provide an efficient algorithm to compute the pair and . Finally, with Theorems 3.1-3.2, the value of the step-down game is recovered by by Proposition 2.1 and that of the step-up game is recovered by by Proposition 2.2.

Remark 3.1.

For the fair valuation of the default swap game, one may specify as the risk-neutral pricing measure. The risk-neutrality condition would require that so that the discounted asset value is a -martingale. This condition is not needed for our solution approach and equilibrium results.

3.2. Expressing using the scale function.

In this subsection, we shall summarize the scale function associated with the process , and then apply this to compute the candidate value function defined in (2.11). For any spectrally negative Lévy process, there exists a function , which is zero on and continuous and strictly increasing on . It is characterized by the Laplace transform:

where is the right inverse of , defined by

The function is often called the (r-)scale function in the literature (see e.g. [23]).

With and , we can define the function by

| (3.7) |

As is well known (see [23, Chapter 8]), the function is increasing, and satisfies

| (3.8) |

From Lemmas 4.3-4.4 of [26], we also summarize the behavior of in the neighborhood of zero:

| (3.14) |

To facilitate calculations, we define the function

which satisfies that

| (3.15) |

see [23] Exercise 8.5. By Theorem 8.5 of [23], the Laplace transform of in (2.4) can be expressed as

| (3.16) |

Regarding the smoothness of the scale function, Assumption 3.1 guarantees that is differentiable on (see, e.g., [12]). By (3.16), Laplace transform function is also differentiable on , and so are the functions in (2.7)-(2.9). In this paper, we need the twice differentiability for the case of unbounded variation.

Assumption 3.2.

For the case is of unbounded variation, we assume that is twice differentiable on .

This assumption is automatically satisfied if as in [12], and the same property holds for , and . While this is not guaranteed for the unbounded variation case with , it is an assumption commonly needed when the verification of optimality requires the infinitesimal generator.

In applying the scale function to compute , we first consider the case and then extend to the cases and , namely,

| (3.19) |

For , define

| (3.20) | ||||

We observe that and are similar and they possess the common term .

Lemma 3.1.

For ,

| (3.21) | ||||

and

| (3.22) |

where

| (3.23) | ||||

| (3.24) | ||||

The function as in (3.23) will play a crucial role in the continuous and smooth fit as we discuss in Subsection 3.3 below and also in the proof of the existence of a pair as in Subsection 3.4.

Now we extend our definition of for and as in (3.19), and then derive the strategies that attain them. As we shall see in Corollary 3.1 below, our candidate threshold level for the seller is always strictly positive if is of unbounded variation whether or not there is a Gaussian component. For this reason, we consider the limit as only when (3.3) is satisfied.

In view of (3.21), the limits in (3.19) can be obtained by extending with and ; namely we take limits in (3.22). Here as in (3.23) explodes as and hence we define an extended version of by, for any (with the assumption for ),

| (3.27) |

where

and

| (3.28) |

Here, is finite if and only if (3.3) holds. Clearly, when . We shall confirm the convergence results and other auxiliary results below.

Lemma 3.2.

For any fixed ,

-

(1)

is monotonically decreasing in on ,

-

(2)

if , then ,

-

(3)

for every (extended to if ), .

Lemma 3.3.

-

(1)

We have for every (extended to if ).

-

(2)

When , for every and , respectively,

(3.29) and .

-

(3)

For every (extended to if ), .

Using the above, for , we obtain the limit

| (3.30) |

and, for ,

| (3.31) |

In summary, we have expressed including its limits in (3.19) in terms of the scale function.

Remark 3.2.

We note that is and in particular when is of unbounded variation. Indeed, is and in particular when is of unbounded variation. See also the discussion immediately before and after Assumption 3.2 for the same smoothness property on .

We now construct the strategies that achieve and . As the following remark shows, the interpretation of the former is fairly intuitive and it is attained when the buyer never exercises and his strategy is .

Remark 3.3.

On the other hand, is slightly more difficult to understand. Suppose we substitute directly into (3.20) (or the seller never exercises and her strategy is ), we obtain

As shown in Remark 3.4 below, matches if and only if there is not a Gaussian component. Upon the existence of Gaussian component, there is a positive probability of continuously down-crossing (creeping) zero, and the seller tends to exercise immediately before it reaches zero rather than not exercising at all.

Remark 3.4.

The right-hand limit is given by

| (3.32) |

Therefore, if and only if the Gaussian coefficient .

Upon the existence of a Gaussian component, , but there does not exist a seller’s strategy that attains . However, for any , the -optimal strategy (when the buyer’s strategy is ) can be attained by choosing a sufficiently small level. Without a Gaussian component, and the seller may choose .

3.3. Continuous and Smooth Fit

We shall now find the candidate thresholds and by continuous and smooth fit. As we will show below, the continuous and smooth fit conditions (2.12)-(2.13) will yield the equivalent conditions where

for all . Here the second equality holds because for every

| (3.33) | ||||

where the latter holds because on and is continuous on .

As in the case of , it can be seen that also tends to explode as with fixed. For this reason, we also define the extended version of by, for any (with the assumption for ),

| (3.36) |

The convergence results as and as well as some monotonicity properties are discussed below.

Lemma 3.4.

-

(1)

For fixed , is decreasing in on , and in particular when , .

-

(2)

For fixed (extended to if ), is decreasing in on and as .

-

(3)

The relationship also holds for any given where is defined as in (3.29) and

|

|

|

|

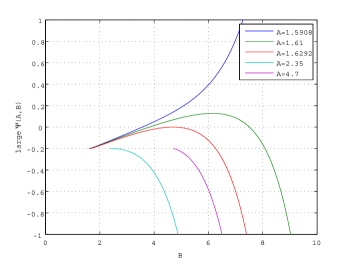

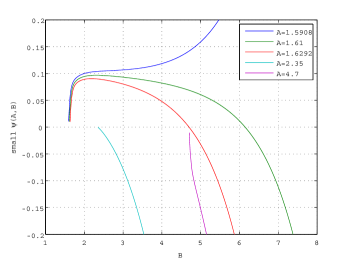

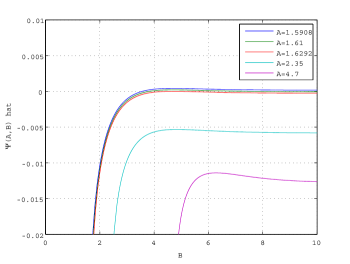

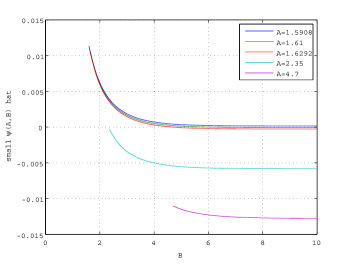

Figure 1 gives numerical plots of , , and for various values of . Lemma 3.4-(1,2) and the fact that imply that, given a fixed , there are three possible behaviors for :

-

(a)

For small , is monotonically increasing in .

-

(b)

For large , is monotonically decreasing in .

-

(c)

Otherwise first increases and then decreases in .

The behavior of has implications for the existence and uniqueness of and , as shown in Theorem 3.3 and Lemma 3.5 below. Besides, it can be confirmed that and converge as as in Lemmas 3.3-(1) and 3.4-(2). We shall see that the continuous/smooth fit conditions (2.12)-(2.13) require (except for the case or ) that , or equivalently . This is illustrated by the line corresponding to in Figure 1.

We begin with establishing the continuous fit condition.

Continuous fit at : Continuous fit at is satisfied automatically for all cases since exists and

| (3.37) |

which also holds when and given . This is also clear from the fact that a spectrally negative Lévy process always creeps upward and hence is regular for for any arbitrary level (see [23, p.212]).

Continuous fit at : We examine the limit of as , namely,

| (3.38) |

In view of (3.14), continuous fit at holds automatically for the unbounded variation case. For the bounded variation case, the continuous fit condition is equivalent to

| (3.39) |

We now pursue the smooth fit condition. Substituting (3.33) into the derivative of (3.22), we obtain

| (3.40) |

for every (extended to when ).

Smooth fit at : With (3.40), the smooth fit condition at amounts to

because

and

| (3.41) |

For the case and , the smooth fit condition requires , which is well-defined by Lemmas 3.3-(2) and 3.4-(1) and (3.41).

Smooth fit at : Assuming that it has paths of unbounded variation (), then we obtain

Therefore, (3.39) is also a sufficient condition for smooth fit at for the unbounded variation case.

We conclude that

-

(1)

if , then continuous fit at holds for the bounded variation case and both continuous and smooth fit at holds for the unbounded variation case;

-

(2)

if , then both continuous and smooth fit conditions at hold for all cases.

If both and are satisfied, then automatically follows by (3.41).

3.4. Existence and Identification of

In the previous subsection, we have derived the defining equations for the candidate pair . Nevertheless, the computation of is non-trivial and depends on the behaviors of functions and . In this subsection, we prove the existence of and provide a procedure to calculate their values.

Recall from Lemma 3.4-(1) that is decreasing in and observe that is also decreasing in . Hence, let and be the unique values such that

| (3.42) | ||||

| (3.43) |

upon existence; we set the former zero if for all and also set the latter zero if for any . Since and as , and are finite. In addition, implies that .

Define for every ,

| (3.44) | ||||

where we assume . For above, we recall from (3.41) that

| (3.45) |

Also, using Lemmas 3.3-(1) and 3.4-(2) and that (see (3.18), (3.27), and (3.36)), we obtain the limit

| (3.46) |

Next, we show that there always exists a pair belonging to one of the following four cases:

- case 1:

-

with ;

- case 2:

-

with and ;

- case 3:

-

with ;

- case 4:

-

with and .

Theorem 3.3.

-

(1)

If and , then there exists such that . This corresponds to case 1.

-

(2)

If and , then and satisfy the condition for case 2.

-

(3)

If , , and , then there exists such that . This corresponds to case 1.

-

(4)

Suppose (i) or (ii) and . If , then and satisfy the condition for case 3. If , then and satisfy the condition for case 4.

In particular, from (3.3) and (3.42) we infer that implies . This together with Theorem 3.3 leads to the following corollary.

Corollary 3.1.

If as in (3.2) has paths of unbounded variation, then and .

Remark 3.5.

In Theorem 3.3-(1,3), we need to further identify . To this end, we first observe

Lemma 3.5.

(1) increases in on , and (2) decreases in on .

This lemma implies that (i) if , then must lie on and (ii) if , then must lie on . By Lemma 3.5 and Theorem 3.3, the following algorithm, motivated by the bisection method, is guaranteed to output the pair . Here let be the error parameter.

- Step 1:

-

Compute and .

- Step 1-1:

-

If (i) or (ii) and , then stop and conclude that this is case 3 or 4 with and .

- Step 1-2:

-

If and , then stop and conclude that this is case 2 with and .

- Step 2:

-

Set .

- Step 3:

-

Compute and .

- Step 3-1:

-

If , then stop and conclude that this is case 1 with and (or ).

- Step 3-2:

-

If and , then set and go back to Step 2.

- Step 3-3:

-

If and , then set and go back to Step 2.

3.5. Verification of Equilibrium

We are now ready to prove Theorems 3.1-3.2. Our candidate value function for the Nash equilibrium is given by (2.11) and (3.19) with and obtained by the procedure above. By Lemma 3.1,

| (3.47) | ||||

where

| (3.52) |

When , is the candidate saddle point that attains . When , can be approximated by for sufficiently small . The value of can be computed by (3.22), (3.30) and (3.31).

The proof of Theorems 3.1-3.2 involves the crucial steps:

-

(i)

Domination property

-

(a)

for all ;

-

(b)

for all ;

-

(a)

-

(ii)

Sub/super-harmonic property

-

(a)

for every ;

-

(b)

for every ;

-

(c)

for every .

-

(a)

Here is the infinitesimal generator associated with the process

applied to any bounded and sufficiently smooth function that is when is of unbounded variation and otherwise.

After establishing (i)-(ii) above, we will apply them to establish (2.10) by showing for the candidate optimal thresholds that

| (3.53) |

Remark 3.6.

In fact, it is sufficient to show (3.53) holds for all and , where

| (3.54) | ||||

Indeed, for any candidate , it follows that where , so the buyer’s optimal exercise time must belong to . This is intuitive since the seller will end the game as soon as enters and hence the buyer should not needlessly stop in this interval and pay . Similar arguments apply to the use of . Then, using the same arguments as for (2.11), we can again safely eliminate the term in (2.6) and write

We prove properties (i)-(ii) above using the following lemmas.

Lemma 3.6.

For every , the following inequalities hold:

| (3.55) | ||||

| (3.56) |

where it is understood for the case and that the above results hold with .

Lemma 3.7.

Fix .

-

(1)

For every , when

and when ,

-

(2)

For every ,

where it is understood for the case and that the above holds with .

Lemma 3.8.

-

(1)

When , we have for every .

-

(2)

We have for every .

-

(3)

When , we have for every .

The domination property (i) holds by applying discounting and expectation in Lemma 3.7. The sub/super-harmonic property (ii) is implied by Lemma 3.8. By Ito’s lemma, this shows that the stopped processes and are, respectively, a supermartingale and a submartingale. In turn, we apply them to show for any arbitrary , and for any arbitrary , that is, the Nash equilibrium. We provide the details of the proofs for Theorems 3.1-3.2 in the Appendix.

4. Exponential Jumps and Numerical Examples

In this section, we consider spectrally negative Lévy processes with i.i.d. exponential jumps and provide some numerical examples to illustrate the buyer’s and seller’s optimal exercise strategies and the impact of step-up/down fees on the game value. The results obtained here can be extended easily to the hyperexponential case using the explicit expression of the scale function obtained by [15], and can be used to approximate for a general case with a completely monotone density (see, e.g., [15, 18]). Here, however, we focus on a rather simple case for more intuitive interpretation of our numerical results.

4.1. Spectrally Negative Lévy Processes with Exponential Jumps

Let be a spectrally negative Lévy process of the form

Here is a standard Brownian motion, is a Poisson process with arrival rate , and is an i.i.d. sequence of exponential random variables with density function , , for some . Its Laplace exponent (3.1) is given by

For our examples, we assume . In this case, there are two negative solutions to the equation and their absolute values satisfy the interlacing condition: . For this process, the scale function is given by for every

| (4.1) | ||||

for some and (see [15] for their expressions). In addition, applying (4.1) to (3.7) yields

with the limit , which equals by (3.8).

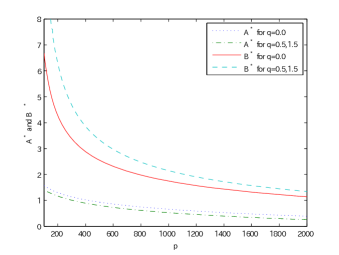

Recall that, in contrast to and , and do not explode. Therefore, they are used to compute the optimal thresholds and and the value function . Below we provide the formulas for and . The computations are very tedious but straightforward, so we omit the proofs here.

4.2. Numerical Results

Let us denote the step-up/down ratio by We consider four contract specifications:

-

(C)

cancellation game with (position canceled at exercise),

-

(D)

step-down game with (position halved at exercise),

-

(V)

vanilla CDS with (position unchanged at exercise),

-

(U)

step-up game with (position raised at exercise).

The model parameters are , , , , , and bps, unless specified otherwise. We also choose so that the risk-neutral condition is satisfied.

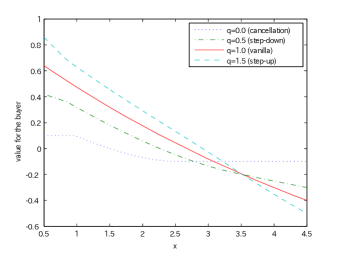

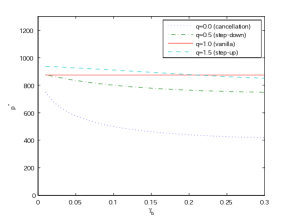

Figure 2 shows for all four cases the contract value to the buyer as a function of given a fixed premium rate. It is decreasing in since default is less likely for higher value of . For the cancellation game, takes the constant values bps for and bps for since in these regions immediate cancellation with a fee is optimal.

|

In Figure 3, we show the optimal thresholds and and the value with respect to . The symmetry argument discussed in Section 2 applies to the cases (D) and (U). As a result, the in (D) is identical to the in (U), and the in (D) is identical to the in (U). In all four cases, both and are decreasing in . In other words, as increases, the buyer tends to exercise earlier while the seller tends to delay exercise. Intuitively, a higher premium makes waiting more costly for the buyer but more profitable for the seller. The value in the cancellation game stays constant when is sufficiently small because the seller would exercise immediately; it also becomes flat when is sufficiently high because the buyer would exercise immediately.

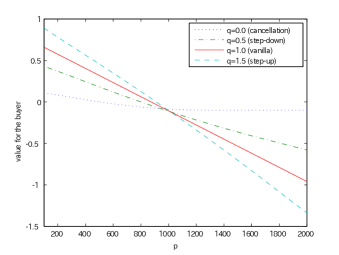

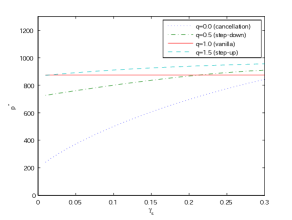

Note that the value function and the optimal stopping strategies depend on the premium rate . In particular, we call the equilibrium premium rate if it yields , where we emphasize the saddle point corresponds to . Hence, under the equilibrium premium rate, the default swap game starts at value zero, implying no cash transaction between the protection buyer and seller at contract initiation. As illustrated in Figure 3-(b), the value (from the buyer’s perspective) is always decreasing in . Using a bisection method, we numerically determine the equilibrium premium so that . We illustrate in Figure 4 the equilibrium premium as a function of and . As is intuitive, the equilibrium premium is increasing in and decreasing in .

5. Conclusions

We have discussed the valuation of a default swap contract where the protection buyer and seller can alter the respective position once prior to default. This new contractual feature drives the protection buyer/seller to consider the optimal timing to control credit risk exposure. The valuation problem involves the analytical and numerical studies of an optimal stopping game with early termination from default. Under a perpetual setting, the investors’ optimal stopping rules are characterized by their respective exercise thresholds, which can be quickly determined in a general class of spectrally negative Lévy credit risk models.

For future research, it is most natural to consider the default swap game under a finite horizon and/or different credit risk models. The default swap game studied in this paper can potentially be applied to approximate its finite-maturity version using the maturity randomization (Canadization) approach (see [11, 25]). Another interesting extension is to allow for multiple adjustments by the buyer and/or seller prior to default, which can be modeled as stochastic games with multiple stopping opportunities. Finally, the step-up and step-down features also arise in other derivatives, including interest rate swaps.

Appendix A Proofs

Proof of Proposition 2.1.

First, by a rearrangement of integrals and (2.5), the expression inside the expectation in (2.1) can be written as

Taking expectation, (2.1) simplifies to

| (A.1) | ||||

Here, the last two terms do not depend on nor and they constitute . Next, using the fact that for every and the strong Markov property of at time , we express the first term as

where the second equality holds because (i) or implies , and (ii) by we have a.s. ∎

Proof of Proposition 2.2.

Proof of Lemma 3.1.

Recall that is given by the first expectation of (A.1), and note that implies . For every , equals

which equals . Since , , the second claim of (3.21) is immediate.

The proof of the second claim amounts to proving the following: for ,

| (A.2) | ||||

The first two equalities follow directly from the property of the scale function (see, for example, Theorem 8.1 of [23]). Notice here that if and only if it up-crosses before down-crossing while or if and only if it down-crosses before up-crossing .

For the third equality, we require the overshoot distribution that is again obtained via the scale function. Let be the Poisson random measure for the jumps of and and be the running maximum and minimum, respectively, of . By compensation formula (see e.g. Theorem 4.4 of [23]), we have

| (A.3) | ||||

Recall that, as in Theorem 8.7 of [23], the resolvent measure for the spectrally negative Lévy process killed upon exiting is given by

Hence

when , and it is zero otherwise. Therefore, for , we have

since is zero on . Therefore, . Finally, substituting (A.2) in (3.20), the proof is complete. ∎

Proof of Lemma 3.2.

(1) The monotonicity is clear because for any .

(2) By (3.8), we have for any

Therefore,

| (A.4) |

Using this with the dominated convergence theorem yields the limit:

which is finite.

(3) For all

Therefore, the dominated convergence theorem yields the limit:

where the last equality holds by (3.15), and

∎

Proof of Lemma 3.3.

Proof of Remark 3.4.

By Theorem 8.1 of [23], we obtain the limits:

By the construction of as seen in (A.3) above, we deduce that

Applying these to the definition (3.20) yields:

By [23] Exercise 7.6, a spectrally negative Lévy process creeps downward, or , if and only if there is a Gaussian component. This completes the proof. ∎

Proof of Lemma 3.4.

We first show the following.

Lemma A.1.

If , then we have for any .

Proof.

Fix . We have

| (A.5) |

For any , we have by the mean value theorem,

which is finite because and . Hence we conclude.∎

(1) Suppose . Since is increasing in on , it follows that

and is decreasing in on . The result for is immediate because is decreasing.

For the convergence result for (when ), we have

which is bounded by Lemma A.1. Hence by the dominated convergence theorem,

The convergence result for is clear because .

(2) Suppose . Look at (3.36) and consider the derivative with respect to ,

where is the density of . Moreover, for all ,

by (3.17). Therefore, is decreasing in . This result can be extended to as in part (1).

For the convergence result for , the dominated convergence theorem yields

Proof of Theorem 3.3.

(1) In view of (a)-(c) in Subsection 3.3, we shall show that (i) monotonically increases while (ii) monotonically decreases in .

(i) By the assumption , we have . This coupled with the fact that is decreasing in by Lemma 3.4-(2) shows that or for every and hence is monotonically increasing in on (recall ). Furthermore, implies that (note ). This together with implies that is monotonically increasing in to .

(ii) Because , we obtain and hence . This together with the fact that is decreasing in by Lemma 3.4-(2) shows that , or , for every . Consequently, is monotonically decreasing in on . Furthermore, because by Lemma 3.3-(3), never up-crosses the level zero.

By (i) and (ii) and the continuity of and with respect to both and , there must exist and such that (with ).

(2) Using the same argument as in (1)-(i) above, is increasing in on . Moreover, the assumption means that . This together with shows . By (3.18) and (3.46), and this implies that for all by virtue of Lemma 3.4-(2), and hence .

(3) Recall Lemma 3.4-(3). We have if and only if , and hence attains a global maximum and it is strictly larger than zero because . Furthermore, is monotonically decreasing in on and as in (1)-(ii). This together with the same argument as in (1) shows the result.

(4) First, implies . This also means that or is decreasing on . This together with Lemma 3.3-(3) shows . Now, for both (i) and (ii) for every , because , we must have . This shows that . It is clear that this is case 3 when whereas this is case 4 when . ∎

Proof of Lemma 3.5.

(1) With , it is sufficient to show is decreasing in on for every fixed . Indeed, the derivative

| (A.6) | ||||

| (A.7) |

is negative for every by the definition of . Part (2) is immediate from Lemma 3.4-(1). ∎

Proof of Lemma 3.6.

(1) Fix . First, suppose . We compute the derivative:

Using (A.7), the last two terms of the above cancel out and

On the right-hand side, the derivative is given by

which is negative according to (3.17) by . Now suppose . We have

By (3.27), the first term becomes

and by using the last equality of (A.7) (with replaced with ), we obtain

Hence,

where because is increasing.

Now in order to show is increasing in on , it is sufficient to show for every . This is true for by and Lemma 3.5-(1). This holds also for . Indeed, is decreasing in because, for any , and Lemma 3.4-(2) imply . Furthermore, Lemma 3.3-(3) shows that . Hence or .

Proof of Lemma 3.7.

Proof of Lemma 3.8.

(1) First, Lemma 3.4 of [27] shows that . Therefore, using (3.47) and that on , we have

| (A.8) |

Since , we must have by construction and and consequently, . Furthermore, is decreasing in and hence . Applying this to (A.8), for , it follows that .

(2) When , by the strong Markov property,

Taking expectation on both sides, we see that is a -martingale and hence on (see Remark 3.2 and the Appendix of [7]).

(3) Suppose , i.e. there is a Gaussian component. In this case, is continuous on and on , and we have

We show . To this end, we suppose and derive contradiction. The fact that by smooth fit implies that for some . However, since , this would contradict (3.56). Consequently, , implying . When , by continuous and smooth fit.

As a result, for all cases, we conclude that . Now it is sufficient to show that is decreasing on . Recall the decomposition (3.47). Because , we shall show is decreasing on .

Now because on ,

Since , we must have that on (or the integrand of the above is non-negative). In order to show that this is decreasing, we show that in (3.52) is decreasing on . By continuous fit at (when ), it is sufficient to show that is decreasing for every . By Remark 3.5-(3), we must have , and hence by (3.17) and because as in Remark 3.5-(1),

After multiplying by on both sides and observing is decreasing in by Lemma 3.4, we get , which matches in (3.40). Hence, is decreasing, as desired.∎

Proof of Theorem 3.1.

(i) We show that for every . As is discussed in Remark 3.6, we only need to focus on the set .

In order to handle the discontinuity of at zero, we first construct a sequence of functions such that it is continuous on , on and (c) pointwise for every fixed . Notice that is uniformly bounded because and are. Hence, we can choose so that is also uniformly bounded for every fixed . Because and on and on , we have

| (A.9) |

We have for any , where is the maximum difference between and . Using as the Poisson random measure for the jumps of and as the running minimum of , by the compensation formula [23, Theorem 4.4],

Therefore, uniformly for any ,

| (A.10) | ||||

By applying Ito’s formula to (here we assume ), we see that

| (A.11) |

is a local martingale. Here the () condition at for the case is of unbounded (bounded) variation can be relaxed by a version of Meyer-Ito formula as in Theorem IV.71 of [32] (see also Theorem 2.1 of [30]).

Suppose is the corresponding localizing sequence, namely,

Now by applying the dominated convergence theorem on the left-hand side and Fatou’s lemma on the right-hand side via for every thanks to (A.9) and Lemma 3.8-(2,3), we obtain

Hence (A.11) is a supermartingale.

Now fix . By optional sampling theorem, we have for any

where the last inequality holds by Lemma 3.8-(2,3). Applying the dominated convergence theorem on both sides via (A.10), we obtain the inequality:

| (A.12) |

We shall take on both sides. For the left-hand side, the dominated convergence theorem implies

For the right-hand side, we again apply the dominated convergence theorem via (A.10) to get

| (A.13) |

Now fix -a.e. . By (A.10) dominated convergence yields . Finally, since for Lebesgue-a.e. on , and by the dominated convergence theorem, . Hence, the limit (A.13) vanishes. Therefore, by taking in (A.12) (note ), we have

This inequality and Lemma 3.7-(1) show that for any arbitrary .

(ii) Next, we show that for every . Similarly to (i), we only need to focus on the set . We again use defined in (i). Using the same argument as in (i), we obtain

| (A.14) | ||||

uniformly for any .

Because is not assumed to be nor at zero, we follow the approach by [28]. Fix . By applying Ito’s formula to , we see that

| (A.15) |

is a local martingale. Suppose is the corresponding localizing sequence, we have

where we can split the expectation by (A.14). Now by applying the dominated convergence theorem on the left-hand side and the monotone convergence theorem and the dominated convergence theorem respectively on the two expectations on the right-hand side (using respectively Lemma 3.8-(1,2) and (A.14)), we obtain

Hence (A.15) is a martingale.

Now fix . By the optional sampling theorem, we have for any using Lemma 3.8-(1,2)

Applying the dominated convergence theorem on both sides by (A.14), we have

Because ( ) a.s., the bounded convergence theorem yields

Finally, we can take on both sides along the same line as in (i) and we obtain

This together with Lemma 3.7-(2) shows that for any arbitrary . ∎

Proof of Theorem 3.2.

When , then the same results as (i) of the proof of Theorem 3.1 hold by replacing with and with . Now suppose . Using the same argument as in the proof of Theorem 3.1 with replaced with and the argument with as in (ii) of the proof of Theorem 3.1, the supermartingale property of holds. This together with Lemma 3.7-(1) shows, for any ,

As in the proof of Lemma 3.8-(2), is a martingale. This together with Lemma 3.7-(2) shows that for all . ∎

Acknowledgements. This work is supported by NSF Grant DMS-0908295, Grant-in-Aid for Young Scientists (B) No. 22710143, the Ministry of Education, Culture, Sports, Science and Technology, and Grant-in-Aid for Scientific Research (B) No. 23310103, No. 22330098, and (C) No. 20530340, Japan Society for the Promotion of Science. We thank two anonymous referees for their thorough reviews and insightful comments that help improve the presentation of this paper.

References

- [1] L. Alili and A. E. Kyprianou. Some remarks on first passage of Lévy processes, the American put and pasting principles. Ann. Appl. Probab., 15(3):2062–2080, 2005.

- [2] F. Avram, A. E. Kyprianou, and M. R. Pistorius. Exit problems for spectrally negative Lévy processes and applications to (Canadized) Russian options. Ann. Appl. Probab., 14(1):215–238, 2004.

- [3] F. Avram, Z. Palmowski, and M. R. Pistorius. On the optimal dividend problem for a spectrally negative Lévy process. Ann. Appl. Probab., 17(1):156–180, 2007.

- [4] E. Baurdoux and A. Kyprianou. The McKean stochastic game driven by a spectrally negative Lévy process. Electron. J. Probab., 13:173–197, 2008.

- [5] E. Baurdoux, A. Kyprianou, and J. Pardo. The Gapeev-Kühn stochastic game driven by a spectrally positive Lévy process. Stochastic Process. Appl., 121(6):1266–1289, 2011.

- [6] T. Bielecki, S. Crepey, M. Jeanblanc, and M. Rutkowski. Arbitrage pricing of defaultable game options with applications to convertible bonds. Quant. Finance, 8(8):795–810, 2008.

- [7] E. Biffis and A. E. Kyprianou. A note on scale functions and the time value of ruin for Lévy insurance risk processes. Insurance Math. Econom., 46(1):85–91, 2010.

- [8] F. Black and J. Cox. Valuing corporate securities: Some effects of bond indenture provisions. J. Finance, 31:351–367, 1976.

- [9] D. Brigo and F. Mercurio. Interest rate models – theory and practice with smile, inflation and credit. Springer, 3rd edition, 2007.

- [10] J. Cariboni and W. Schoutens. Pricing credit default swaps under Lévy models. J. Comput. Finance, 10(4):1–21, 2007.

- [11] P. Carr. Randomization and the American put. Rev. Finan. Stud., 11(3):597–626, 1998.

- [12] T. Chan, A. Kyprianou, and M. Savov. Smoothness of scale functions for spectrally negative Lévy processes. Probab. Theory Relat. Fields, 150:691–708, 2011.

- [13] D. Duffie and K. Singleton. Credit risk: Pricing, measurement, and management. Princeton University Press, Princeton NJ, 2003.

- [14] E. Dynkin and A. Yushkevich. Theorems and Problems in Markov Processes. Plenum Press, New York, 1968.

- [15] M. Egami and K. Yamazaki. Phase-type fitting of scale functions for spectrally negative Lévy processes. arXiv:1005.0064, 2012.

- [16] M. Egami and K. Yamazaki. Precautionary measures for credit risk management in jump models. Stochastics, forthcoming.

- [17] E. Ekström and G. Peskir. Optimal stopping games for Markov processes. SIAM J. Control Optim., 47(2):684–702, 2008.

- [18] A. Feldmann and W. Whitt. Fitting mixtures of exponentials to long-tail distributions to analyze network performance models. Perform Evaluation, (31):245–279, 1998.

- [19] B. Hilberink and C. Rogers. Optimal capital structure and endogenous default. Finance Stoch., 6(2):237–263, 2002.

- [20] J. Kallsen and C. Kühn. Convertible bonds: Financial derivatives of game type. In A. Kyprianov, W. Schoutems, and P. Willmott, editors, Exotic Option Pricing and Advanced Lévy Models, pages 277–292. Wiley, NY, 2005.

- [21] Y. Kifer. Game options. Finance Stoch., 4:443–463, 2000.

- [22] A. E. Kyprianou. Some calculations for Israeli options. Finance Stoch., 8(1):73–86, 2004.

- [23] A. E. Kyprianou. Introductory lectures on fluctuations of Lévy processes with applications. Universitext. Springer-Verlag, Berlin, 2006.

- [24] A. E. Kyprianou and Z. Palmowski. Distributional study of de Finetti’s dividend problem for a general Lévy insurance risk process. J. Appl. Probab., 44(2):428–448, 2007.

- [25] A. E. Kyprianou and M. R. Pistorius. Perpetual options and Canadization through fluctuation theory. Ann. Appl. Probab., 13(3):1077–1098, 2003.

- [26] A. E. Kyprianou and B. A. Surya. Principles of smooth and continuous fit in the determination of endogenous bankruptcy levels. Finance Stoch., 11(1):131–152, 2007.

- [27] T. Leung and K. Yamazaki. American step-up and step-down credit default swaps under Lévy models. Quant. Finance, forthcoming.

- [28] R. Loeffen. An optimal dividends problem with a terminal value for spectrally negative Lévy processes with a completely monotone jump density. J. Appl. Probab., 46(1):85–98, 2009.

- [29] R. L. Loeffen. On optimality of the barrier strategy in de Finetti’s dividend problem for spectrally negative Lévy processes. Ann. Appl. Probab., 18(5):1669–1680, 2008.

- [30] B. Øksendal and A. Sulem. Applied Stochastic Control of Jump Diffusions. Springer, New York, 2005.

- [31] G. Peskir. Optimal stopping games and Nash equilibrium. Theory Probab. Appl., 53(3):558–571, 2009.

- [32] P. Protter. Stochastic integration and differential equations. Springer, 2005.

- [33] M. Sirbu and S. Shreve. A two-person game for pricing convertible bonds. SIAM J. Control Optim., 45(4):1508–1539, 2006.

- [34] C. Zhou. The term structure of credit spreads with jump risk. J. Banking Finance, 25:2015–2040, 2001.