Dynamic Portfolio Optimization with a Defaultable Security and Regime Switching

Abstract

We consider a portfolio optimization problem in a defaultable market with finitely-many economical regimes, where the investor can dynamically allocate her wealth among a defaultable bond, a stock, and a money market account. The market coefficients are assumed to depend on the market regime in place, which is modeled by a finite state continuous time Markov process. We rigorously deduce the dynamics of the defaultable bond price process in terms of a Markov modulated stochastic differential equation. Then, by separating the utility maximization problem into the pre-default and post-default scenarios, we deduce two coupled Hamilton-Jacobi-Bellman equations for the post and pre-default optimal value functions and show a novel verification theorem for their solutions. We obtain explicit optimal investment strategies and value functions for an investor with logarithmic utility. We finish with an economic analysis in the case of a market with two regimes and homogenous transition rates, and show the impact of the default intensities and loss rates on the optimal strategies and value functions.

AMS 2000 subject classifications: 93E20, 60J20.

Keywords and phrases: Dynamic Portfolio Optimization, Credit Risk, Regime Switching Models, Utility Maximization, Hamilton-Jacobi-Bellman Equations.

1 Introduction

111This is an improved version of the original submission, where we fixed typos and updated references.Continuous time portfolio optimization problems are among the most widely studied problems in the field of mathematical finance. Since the seminal work of Merton (1969), who explored stochastic optimal control techniques to provide a closed form solution to the problem, a large volume of research has been done to extend Merton’s paradigm to other frameworks and portfolio optimization problems (see, e.g. Karatzas et al. (1996), Karatzas and Shreve (1998), and Fleming and Pang (2004)). Most of the models proposed in the literature rely on the assumption that the uncertainty in the asset price dynamics is governed by a continuous process, which is typically chosen to be a Brownian motion. In recent years, there has been an increasing interest in the use of regime switching model to capture the macro-economic regimes affecting the behavior of the market. More specifically, the price of the security evolves with a different dynamics, typically identified by the drift and the diffusion coefficient associated to the macro-economic regime in place. Although regime switching models arguably are able to incorporate a realistic description of market behavior, they pose challenges in the context of pricing because they lead to an incomplete market, as the regime uncertainty cannot be hedged away.

In the context of option pricing, Guo (2001) studies a two-regime switching model, where regimes represent the amount of information available to the market. Buffington and Elliott (2002-a) and Buffington and Elliott (2002-b) price European and American options under regime switching models, while Elliott et al. (2005) address the specification of an appropriate pricing martingale measure. Guo and Zhang (2004) provide an explicit optimal stopping rule when pricing perpetual American put options, while Guo et al. (2005) consider the relation between regime shifts and investment decision in the context of real options. Graziano and Rogers (2006) give a methodology to price barrier options with regime switching dividend process, while Gapeev and Jeanblanc (2010) obtain closed form expressions for European claims, assuming geometric Brownian motion dynamics with regime switching drifts.

Utility maximization problems under regime switching have been investigated in Sotomayor and Cadenillas (2009), who consider the infinite horizon problem of maximizing the expected utility from consumption and terminal wealth in a market consisting of multiple stocks and a money market account, where both short rate and stock diffusion parameters evolve according to Markov-Chain modulated dynamics. Similarly, Zariphopoulou (1992) considers an infinite horizon investment-consumption model where the agent can consume and distribute her wealth across a risk-free bond and a stock. Nagai and Runngaldier (2008) consider a finite horizon portfolio optimization problem for a risk averse investor with power utility, assuming that the coefficients of the risky assets in the economy are nonlinearly dependent on the Markov-chain modulated economic factors. Korn and Kraft (2001) relax the assumption of constant interest rate and derive expressions for the optimal percentage of wealth invested in the money market account and stock, under the assumption of a diffusive short rate process with deterministic drift and constant volatility.

Most of the research done on continuous time portfolio optimization has concentrated on markets consisting of a risk-free asset, and of securities which only bear market risk. These models do not take into account securities carrying default risk, such as corporate bonds, even though the latter represent a significant portion of the market, comparable to the total capitalization of all publicly traded companies in the United States. In recent years, portfolio optimization problems have started to incorporate defaultable securities, but assuming that the risky factors are modeled by continuous processes and more specifically by Brownian Itô processes. Bielecki and Jang (2006) derive optimal finite horizon investment strategies for an investor with CRRA utility function, who optimally allocates her wealth among a defaultable bond, risk-free account, and stock, assuming constant interest rate, drift, volatility, and default intensity. Bo et al. (2010) consider an infinite horizon portfolio optimization problem, where an investor with logarithmic utility can choose a consumption rate, and invest her wealth across a defaultable perpetual bond, a stock, and a money market. They assume that both the historical intensity and the default premium process depend on a common Brownian factor. Unlike Bielecki and Jang (2006), where the dynamics of the defaultable bond price process was derived from the arbitrage-free bond prices, Bo et al. (2010) postulates the dynamics of the defaultable bond prices partially based on heuristic arguments. Lakner and Liang (2008) analyze the optimal investment strategy in a market consisting of a defaultable (corporate) bond and a money market account under a continuous time model, where bond prices can jump, and employ duality theory to obtain the optimal strategy. Callegaro, Jeanblanc, and Runggaldier (2010) consider a market model consisting of several defaultable assets, which evolve according to discrete dynamics depending on partially observed exogenous factor processes. Jiao and Pham (2010) combine duality and dynamic programming to optimize the utility of an investor with CRRA utility function, in a market consisting of a riskless bond and a stock subject to counterparty risk. Bielecki et al. (2008) develop a variational inequality approach to pricing and hedging of a defaultable game option under a Markov modulated default intensity framework.

In this paper, we consider for the first time finite horizon dynamic portfolio optimization problems in defaultable markets with regime switching dynamics. We provide a general framework and explicit results on optimal value functions and investment strategies in a market consisting of a money market, a stock, and a defaultable bond. Similarly to Sotomayor and Cadenillas (2009), we allow the short rate and the drift and volatility of the risky stock to be all regime dependent. For the defaultable bond, we follow the reduced form approach to credit risk, where the global market information, including default, is modeled by the progressive enlargement of a reference filtration representing the default-free information, and the default time is a totally inaccessible stopping time with respect to the enlarged filtration, but not with respect to the reference filtration. We also make the default intensities and loss given default rates to be all regime dependent. The use of regime switching models for pricing defaultable bonds has proven to be very flexible when fitting the empirical credit spreads curve of corporate bonds as illustrated in, e.g., Jarrow et al. (1997), where the underlying Markov chain models credit ratings.

Our main contributions are discussed next. First, we rigorously derive the dynamics of the defaultable bond under the historical measure from the price process, defined as a risk neutral expectation. Secondly, after separating the utility maximization problem into a pre-default and post-default dynamic optimization problem, we give and prove verification theorems for both subproblems. We show that the regime dependent pre-default optimal value function and bond investment strategy may be obtained as the solution of a coupled system of nonlinear partial differential equations (satisfied by the pre-default value function) and nonlinear equations (satisfied by the bond investment strategy), each corresponding to a different regime. Moreover, we obtain the interesting feature that the pre-default optimal value function and bond investment strategy depend on the corresponding regime dependent post-default value function. Thirdly, we demonstrate our framework on the concrete case of an investor with logarithmic utility, and, show that both the optimal pre-default and post-default value functions amount to solving a system of ordinary linear differential equations, while the optimal bond strategy may be recovered as the unique solution of a decoupled system of equations, one for each regime. Under a two-regime market with homogenous transition rates, we are able to obtain explicit formulas, and illustrate the impact of default risk on the bond investment strategy and optimal value functions.

The rest of the paper is organized as follows. Section 2 introduces the market model. Section 3 derives the dynamics of the defaultable bond under the historical measure, starting from the risk-neutral bond price process. Section 4 formulates the dynamic optimization problem. Section 5 gives and proves the two verification theorems associated to the post-default and pre-default case. Section 6 specializes the theorems given earlier to the case of an investor with logarithmic utility. Section 7 summarizes the main conclusions of the paper. The proofs of the main theorems and necessary lemmas are deferred to the appendix.

2 The Model

Assume is a complete probability space, where is the real world probability measure (also called historical probability), is an enlarged filtration given by (the filtrations and will be introduced later). Let be a standard Brownian motion on , where is a suitable filtration satisfying the usual hypotheses of completeness and right continuity. We also assume that the states of the economy are modeled by a continuous-time Markov process defined on with a finite state space . Without loss of generality, we can identify the state space of to be a finite set of unit vectors , where and ′ denotes the transpose. We also assume that and are independent. Define to be the Markov chain transition matrix (also referred to as the infinitesimal generator). The following semi-martingale representation is well-known (cf. Elliott et al. (1994)):

| (1) |

where is a -valued martingale process under , and is the so-called generator of the Markov process. Specifically, denoting , for , and , we have that

cf. Bielecki and Rutkowski (2001). In particular, .

We consider a frictionless financial market consisting of three instruments: a risk-free bank account, a defaultable bond, and a stock. The dynamics of each of the following instruments will depend on the underlying states of the economy as follows:

Risk-free bank account. The instantaneous market interest rate at time is , where denotes the standard inner product in and are positive constants. This means that, depending on the state of the economy, the interest rate will be different; i.e., if then . The dynamics of the price process which describes the risk-free bank account is given by

| (2) |

Stock price. We assume that the stock appreciation rate and the volatility of the stock also depend on the economy regime in place in the following way:

| (3) |

where and are constants denoting, respectively, the values of drift and volatility which can be taken depending on the different economic regimes. Hence, we assume that

| (4) |

Risky Bond price. Unlike the previous two securities, where we have written directly the dynamics under the historical measure, here we need to infer the historical dynamics (i.e. dynamics under the actual probability measure ) from the bond price process, which is originally defined under a suitably chosen risk-neutral pricing measure . Before defining the bond price, we need to introduce a default process. Let be a nonnegative random variable, defined on , representing the default time of the counterparty selling the bond. Let be the filtration generated by the default process , after completion and regularization on the right, and also let be the filtration .

We use the canonical construction of the default time in terms of a given hazard process , which will also be assumed to be driven by the Markov process . Specifically, throughout the paper we assume that , where are positive constants. For future reference, we now give the details of the construction of the random time . We assume the existence of an exponential random variable defined on the probability space , independent of the process . We define by setting

| (5) |

It can be proven that is the -hazard rate of (see Bielecki and Rutkowski (2001), Section 6.5 for details). That is, is such that

| (6) |

is a -martingale under , where .

An important consequence of the previous construction is the following property. Let us fix and . For any , we have . Therefore, for any ,

Plugging inside the above expression, we obtain

| (7) |

It was proven in Bremaud and Yor (1978) that Eq. (7) is equivalent to saying that any -square integrable martingale is also a -square integrable martingale. The latter property is also referred to as the hypothesis, and we will make use of this property later on.

The final ingredient in the bond pricing formula is the recovery process , an -adapted right-continuous with left-limits process to be fully specified below. Then, the time- price of the risky bond with maturity is given by

| (8) |

where is the equivalent risk-neutral measure used in pricing. Furthermore, we adopt a pricing measure such that, under , is still a standard Wiener process and is a continuous-time Markov process (independent of ) with possibly different generator .

The existence of the measure in the previous paragraph follows from the theory of change of measures for denumerable Markov processes (see, e.g., Section 11.2 in Bielecki and Rutkowski (2001)). Concretely, for and some bounded measurable functions , define

| (9) |

and for , define

We also fix for . Now, consider the processes

| (10) |

where

| (11) |

The process is known to be a -martingale for any (see Lemma 11.2.3 in Bielecki and Rutkowski (2001)) and, since the -hypothesis holds in our default framework, they are also -martingales. Then, by virtue of Proposition 11.2.3 in Bielecki and Rutkowski (2001), the probability measure on with Radon-Nikodýn density given by

| (12) |

is such that is a Markov process under with generator . Without loss of generality, can be taken such that is still a Wiener process independent of under .

| (13) |

where is a -valued martingale under . In particular, note that

| (14) |

We emphasize that the distribution of the hazard rate process under the risk-neutral measure is different from that under the historical measure. Therefore, our framework allows modeling the default risk premium, defined as the ratio between risk-neutral and historical intensity, through the change of measure of the underlying Markov chain.

3 Defaultable bond price dynamics

We now proceed to obtain the bond price dynamics under both the risk-neutral and historical probability measures. Eq. (8) may be rewritten as

| (15) | ||||

which follows from Eq. (6), along with application of the following classical identity

where and is a -measurable random variable (see Bielecki and Rutkowski (2001), Corollary 5.1.1, for its proof).

We assume the recovery-of-market value assumption, i.e. , where is -predictable. As with the other factors in our model, we shall assume that is of the form for some constant vector . Under the recovery-of-market value assumption, it follows using a result in Duffie and Singleton (1999), Theorem 1, that

| (16) |

The following result gives the dynamics of the defaultable bond price process under the risk-neutral measure .

Theorem 3.1.

The proof is reported in Appendix A. We also have the following dynamics under the historical probability measure.

4 Optimal Portfolio Problem

We consider an investor who wants to maximize her wealth at time by dynamically allocating her financial wealth into (1) a risk-free bank account, (2) a risky asset, and (3) defaultable bond. The investor does not have intermediate consumption nor capital income to support her purchase of financial assets.

Let us denote by the number of shares of the risk-free bank account that the investor buys () or sells () at time . Similarly, and denote the investor’s portfolio positions on the stock and risky bond at time , respectively. The process is called a portfolio process. We denote the wealth of the portfolio process at time , i.e.

As usual, we require the processes , and to be -predictable. We also assume the following self-financing condition:

Given an initial state configuration , we define the class of admissible strategies to be a set of (self-financing) portfolio processes such that for all when , , and .

Let be defined as

| (22) |

if , while , when . The vector , called a trading strategy, represents the corresponding fractions of wealth invested in each asset at time . Note that if is admissible, then the dynamics of the resulting wealth process can be written as

under the convention that . This convention is needed to deal with the case when default has occurred (), so that =0 and we fix . Using the dynamics derived in Proposition 3.2 and that , we have the following dynamics of the wealth process

| (23) | |||||

under the actual probability .

4.1 The utility maximization problem

For an initial value and an admissible strategy , let us define the objective functional to be

| (24) |

i.e. we are assuming that the investor starts with dollars (its initial wealth), that the initial default state is ( means that no default has occurred yet), and the initial value for the underlying state of the economy is . The constraint is also called the budget constraint. As usual, we assume that the utility function is strictly increasing and concave.

Our goal is to maximize the objective functional for a suitable class of admissible strategies . Furthermore, we shall focus on feedback or Markov strategies of the form

for some functions such that .

As usual, we consider instead the following dynamical optimization problem:

| (25) |

for each , where

| (26) |

The class of processes is defined as follows:

Definition 4.1.

Throughout, denotes a suitable class of -predictable locally bounded feedback trading strategies

such that (26) admits a unique strong solution and for any when and . Throughout this paper, a trading strategy satisfying these conditions is simply said to be -admissible (with respect to the initial conditions , , and ).

Remark 4.1.

As it will be discussed below (see Eqs. (31), (32), and (66)), the jump of the process (26) at time is given by

| (27) |

Since for to be strictly positive, it is necessary and sufficient that for any a.s. (cf. (Jacod and Shiryaev, 2003, Theorem 4.61)), we conclude that in order for to be admissible, it is necessary that,

| (28) |

for any , , and , where we set if for all .

5 Verification Theorems

As it is usually the case, we start by deriving the HJB formulation of the value function (25) via heuristic arguments. We then verify that the solution of the proposed HJB equation (when it exists and satisfies other regularity conditions) is indeed optimal (the so-called verification theorem). Let us assume for now that is in and in for each and . Then, using Itô’s rule along the lines of Appendix B, we have that

where is the Markov process defined in (62), is the infinitesimal generator of given in Eq. (69), and is the martingale given by Eq. (70). Next, if , by virtue of the dynamic programming principle, we expect that

| (29) |

Therefore, we obtain with the inequality becoming an equality if , where denotes the optimum. Now, evaluating the derivative with respect to , at , we deduce the following HJB equation:

| (30) |

with boundary condition

In order to further specify (30), let us first note that the dynamics (26) can be written in the form

| (31) |

with coefficients

| (32) | ||||

where is defined as in (21). Using the expression for the generator in Eq. (69), the notation , and the relationship , (30) can be written as follows for each :

| (33) |

where

| (34) |

We can consider two separate cases

| (35) |

and

| (36) |

Section 5.1 give a verification theorem for the post-default case, while Section 5.2 gives a verification theorem for the pre-default case.

5.1 Post-Default Case

In the post-default case, we have that , for each . Consequently, for and, since , we can take as control.

Below, denotes the sharpe ratio of the risky asset under the state of economy and denotes the class of functions such that

for each . We have the following verification result, whose proof is reported in Appendix C:

Theorem 5.1.

Suppose that there exist a function that solve the nonlinear Dirichlet problem

| (37) |

for any and , with terminal condition . We assume additionally that satisfies

| (38) |

for some locally bounded functions . Then, the following statements hold true:

- (1)

-

(2)

The optimal feedback control , denoted by , can be written as with

(40)

5.2 Pre-Default Case

In the pre-default case (), we take and as our controls. We then have the following verification result:

Theorem 5.2.

Suppose that the conditions of Theorem 5.1 are satisfied and, in particular, let be the solution of (37). Assume that and , , solve simultaneously the following system of equations:

| (41) | ||||

| (42) |

for , with terminal condition . We also assume that satisfies (28) and (39) (uniformly in and ) and satisfies (38). Then, the following statements hold true:

-

(1)

coincides with the optimal value function in (25), when is constrained to the class of -admissible feedback controls such that

for each , satisfies (39) for a locally bounded function , and satisfies (28) and (39) (uniformly in ). If the solution is non-negative, then these bound conditions are not needed.

-

(2)

The optimal feedback controls are given by and with

(43) (44)

6 Application to Logarithmic Utility

The objective of this section is to specialize the framework developed in the previous sections to concrete choices of utility functions. We focus on the logarithmic utility function . The framework, however, can be applied to other concave utility functions, such as power or negative exponential utilities. For the sake of clarity and conciseness, the details of the numerical implementation for other HARA functions is being deferred to the follow-up paper Capponi, Figueroa-López, and Nisen (2011).

6.1 Explicit Solutions

Let us recall that the investor’s horizon is assumed to be less than the maturity of the defaultable bond. Before proceeding, we state without proof a fundamental result from the theory of ordinary differential equations.

Lemma 6.1 (Codd (1961)).

Suppose that the matrix and the vector , are both continuous on an interval . Let . Then, for every choice of the vector , we have that the system

has a unique vector-valued solution that is defined on the same interval .

We first give a lemma, which will be used later to derive the dynamics of the optimal value functions, and relations satisfied by the optimal investment strategies.

Lemma 6.2.

The system of equations

| (45) |

for , admits a unique real solution in the interval , where is defined as in (28). Moreover, if for each , and are continuous functions, then is a continuous function of .

The proof of this lemma is reported in Appendix D. The following is our main result in this section.

Proposition 6.3.

Assume that the ’s and ’s are continuous in . Let be the unique continuous solution in of the nonlinear system of equations (45). Then, the following statements hold true:

-

(1)

The optimal post-default value function is given by

where , and is the unique solution of the linear system of first order differential equations

(46) with terminal conditions , for .

-

(2)

The optimal percentage of wealth invested in stock is given by , where , .

-

(3)

The optimal percentage of wealth invested in the defaultable bond is , while the optimal pre-default value function is

where is the unique solution of the linear system of first order differential equations

(47) with terminal conditions , for .

The proof of this proposition is reported in Appendix D. We notice that the only difference between the pre-default and post-default optimal value function lies in the time and regime component. Moreover, we obtain that the optimal proportion of wealth invested in stocks is constant in every economic regime, and does not depend on the time or on the current level of wealth. This is consistent with the findings in Sotomayor and Cadenillas (2009) and Bo et al. (2010). We also find that the optimal proportion of wealth allocated on the defaultable bond is time and regime dependent, but independent on the current level of wealth. Bo et al. (2010) find that the optimal allocation only depends on time through the default risk premium.

In the case where the rate matrix is homogenous (i.e. ) and the number of regimes is , we can obtain closed form expressions for the optimal pre-default value function, post-default value function, and optimal bond fraction . Let us introduce the following notation:

for . We have the following result:

Corollary 6.4.

From the formulas given above, we can notice that for any given value of the historical intensity , the optimal bond strategy is independent of the value of the historical intensity , associated with the other regime. A symmetric argument applies to , thus showing that each strategy depend on the other regime only through the risk-neutral loss and default intensity associated to the other regime. This is not surprising, given that an investor would base his decision to buy or sell a defaultable bond on the market perception of default risk (i.e. based on the risk-neutral default intensity parameters) rather than on the number of defaults experienced by the corporation in the past.

6.2 Economic Analysis

The objective of this section is to measure the impact of the default parameters over the value functions and the optimal bond strategy via numerical analysis. We fix the interest rate, drift, and volatility regime parameters as indicated in Table 1. We choose the transition rates of the chain to be the same under both probability measures. In order to evaluate , we use the analytical expression for the probability density of the time spent in state by a two-regime continuous time Markov Chain, for a given time interval , when the chain starts in state at time 0. Such formulas have been provided in Kovchecova et al. (2010). Applying these formulas to our setting, for a given , we obtain

where denotes the Dirac delta function and is a modified Bessel function of first kind. When applying this formula to our case, we have

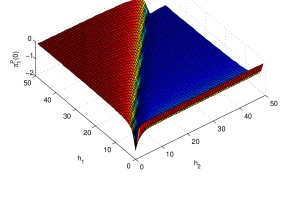

We plot the behavior of and with respect to and . It appears from Figure 1 that the strategies are not very sensitive to the starting regime when the ratio is close to one, with and not too large. This is consistent with intuition, because in such a scenario, the default intensity is the same and small under both regimes, thus the default probability is also small and, consequently, the slightly different risk neutral loss rates in Table 1 do not affect much the investment choice. As the gap between and increases, the strategies and behave differently. This is because a larger risk-neutral intensity translates into a larger risk-neutral default probability, and given that the risk-neutral transition rates of the chain are not large, the starting regime matters.

| Regime ‘1’ | Regime ‘2’ | |

|---|---|---|

| 0.03 | 0.03 | |

| 0.07 | 0.02 | |

| 0.2 | 0.2 |

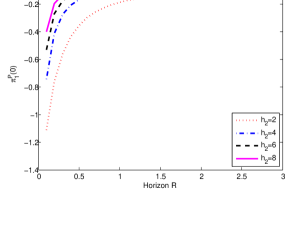

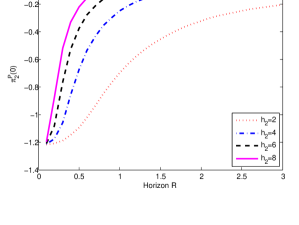

We next show the behavior of the optimal bond strategy over time. It appears from the left panels of Fig. 2 that the number of bond units sold decrease as the investment horizon increases. It can be noticed that, the riskier the corporate bond, the smaller the number of units sold. This is negatively correlated with the regime conditioned bond prices, as it can be checked from Fig. 2, showing that riskier bonds have smaller prices, and shorter maturity bonds have larger prices. Moreover, since the second regime is riskier and the transition rate from the second to the first regime very small, the price decay over time of the bond is faster when the Markov chain starts in the second regime (), thus leading to a larger number of bond units sold when the chain starts in the second regime.

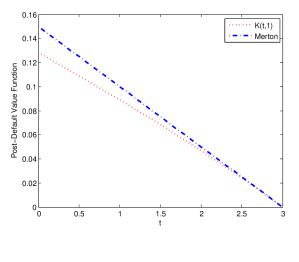

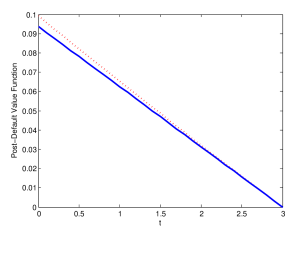

We next inspect the behavior of the time components, and , of the optimal post-default value function over time, for a fixed investment horizon . We report the results in Figure 3, and in each plot we superimpose the time component of the optimal value function obtained in the Merton model. The latter is well known from the work of Merton (1969), and in our specific case obtained assuming that for each regime , the market model consists of a stock and a money market account with parameters , , and . It appears from the plots that both post-default value functions decrease with time. Moreover, they differ at times far from the investment horizon due to possibility of regime shifts, and start converging to each other when the time to horizon is small. This is because the chain spends the largest fraction of its time in the starting regime due to the small transition rates ( and ), and consequently for short times to the horizon, the wealth process of our regime switching model approaches the wealth process in the Merton model.

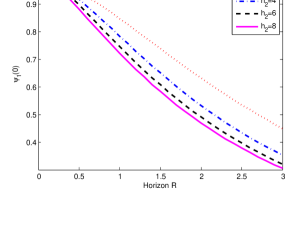

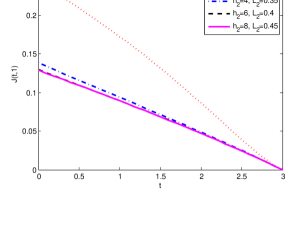

We finally evaluate the behavior of the time components, and , of the optimal pre-default value function over time, assuming again a fixed investment horizon . We report the results in Figure 4, where we vary , keeping fixed. We notice from the plots that the pre-default value function is decreasing with time, and very sensitive to the default risk level.

7 Conclusions

We considered the continuous time portfolio optimization problem in a defaultable market, consisting of a stock, defaultable bond, and money market account. We assumed that the price dynamics of the assets are governed by a regime switching model. We derived the dynamics of the defaultable bond under the historical measure from the risk neutral price process. We have shown that the utility maximization problem may be separated into a pre-default and a post-default optimization subproblem, and proven verification theorems for both cases under the assumption that the solutions are monotonic and concave in the wealth variable . The post-default verification theorem shows that the optimal value function is the solution of a nonlinear Dirichlet problem with terminal condition. The pre-default verification theorem shows that the optimal pre-default value function and the optimal bond investment strategy can be obtained as the solution of a coupled system of nonlinear partial differential equations with terminal condition (satisfied by the pre-default value function) and nonlinear equations (satisfied by the bond investment strategy). Each equation is associated to a different regime, and the dependence of a regime from another regime comes through the Markov transition rates and the ratio between the defaultable bond prices in regime and regime . Our results imply that the pre-default optimal value function and the bond investment strategy depend on the optimal post-default value function.

We demonstrated our framework on the concrete case of an investor with logarithmic utility, and shown that both the optimal pre-default and post-default value function can be obtained as the solution of a linear system of first order ordinary differential equations, while the optimal bond strategy can be uniquely recovered as the solution of a decoupled system of nonlinear equations, one for each regime. We have also performed an economic analysis on a two-regime market model with homogenous transition rates, and investigated the impact of default risk on the optimal strategy and value functions. Our analysis has shown that the optimal number of bond units sold in each regime decreases with the riskiness of the bond perceived by the market, and that the number of bond units sold is smaller for larger investment horizons. Although we have specialized our framework to the specific case of logarithmic utility, it is flexible enough to accommodate any concave increasing utility function. Therefore, the results derived in the verification theorems can be used to derive explicit or numerical solutions for pre-default and post-default value functions, as well as optimal investment strategies, corresponding to a wide range of utilities of practical interest, such as the ones in the HARA family.

Appendix A Risk-neutral and historical bond dynamics

The following result states that the process introduced in (6) is also a -martingale. However, in order to indicate in the sequel when certain dynamics are being taken under or under , we will introduce a new notation . We should keeping in mind through the proof below that .

Lemma A.1.

The process

| (49) |

is also a (local) martingale.

Proof.

By the definition of and the fact that is a -martingale (see the paragraph before (12)), it suffices to prove that is a -martingale under . From Itô’s formula and the definition of in (12), we have the process

From (6), (12), and (49), can be written as

where . Since the first two terms on the right-hand side of the previous equality are (local) martingales under , it remains to show that the last term vanishes. But, given that at , the summation in the last term above will be provided that a.s. In order to show this, let us recall that by definition has no fixed-jump times; i.e. for any fixed time . Also, using the definition of given in Eq. (5), , where is an exponential random variable independent of . Then, conditioning on , Denoting the transition times of the Markov chain , is given by

where the last equality follows from the independence of and , and the fact that is a continuous random variable. ∎

Lemma A.2.

Proof.

Define functions such that

We also let for and , so that is a valid generator of a homogeneous Markov process with transition times determined by a homogeneous Poisson process and an embedded Markov chain with transition probabilities for . Now, let us define a probability measure with Radon-Nikodýn density given by

| (51) |

where and we used notation (11). By virtue of Proposition 11.2.3 in Bielecki and Rutkowski (2001), is a continuous Markov process with generator under . Next, note that is such that

| (52) |

But also, changing into the probability measure , we can write

and, hence, we have the following representation for :

Recall that the solution of (51) can be written as

Let and be defined by

Then, we have

where denotes the transpose of . Next, using that is a homogeneous Markov process under ,

where we used the notation . Furthermore, in terms of the transition times of , the embedded Markov chain of , and the number of transitions by time of , can be written as

where . Using that is a Poisson process under and conditioning on , we have

where , are the ordered statistics of i.i.d. uniform variables independent of , , and . From the previous expression, we see that it suffices to show that

| (53) |

is continuously differentiable in for each , and that there exists a sequence such that

We now show that (i)-(iii) are satisfied provided that

are satisfied. The latter conditions directly follow from (17). Denoting the random function inside the expectation in (53), one can check that

| (54) |

for a constant . Also, is continuously differentiable and

where . In particular, there exists a constant such that

| (55) |

By the formal definition of the derivative and the dominated convergence theorem, one can check that (54-55) will suffice for (i)-(iii). ∎

We are ready to give the proofs of the bond price dynamics:

Proof of Theorem 3.1.

We first write the pre-default dynamics of the bond price under the risk neutral measure (i.e. on the event ). From Eq. (16), we have

Define and so that In terms of (19), note that , where is given as in (19). In particular, since is continuous in light of Lemma A.2. Next, let us introduce the -martingale and the process . Then, has dynamics This leads to

| (56) |

By virtue of the identity and similar arguments to those in the proof Lemma A.1, we have that

Thus, (56) simplifies as follows:

| (57) |

Let us now try to find the dynamics of . Since , where is given as in (19), Itô’s formula leads to

where we had used the differentiability proved in Lemma A.2 and the semi-martingale representation formula of our Markov chain given in Eq. (13). As is a -(local) martingale, its drift term is zero and, therefore, we obtain the dynamics

| (58) |

and all together, we get

| (59) |

By the Doob-Meyer decomposition of Lemma A.1, we have . The last step follows from the fact that on the event , we have , by definition of , and also . Therefore, we can write the pre-default risk-neutral dynamics of the bond as

| (60) |

∎

Appendix B Derivation of the generator of

We start by changing our notation to be more consistent with the framework in Bielecki and Rutkowski (2001). To this end, let

| (62) |

Note that is a Markov process with values in and infinitesimal generator . In particular, for any function ,

is a martingale under , where we have used the notation

c.f. Proposition 11.2.2 in Bielecki and Rutkowski (2001). Note that this result follows directly from the semimartingale decomposition (1) by multiplying (from the left) both sides there by . In particular, also note that

| (63) |

where we used notation (11). Let us assume that admits the following Markov-modulated dynamics:

| (64) |

where are deterministic smooth functions in for any and , and all the coefficients in (64) are evaluated at . In terms of the processes (10)-(11) and using (63), we first note that

| (65) | |||

and, in particular,

| (66) |

where Next, let , for each and . We want to find the semimartingale decomposition of . Applying the Itô’s formula (seeing as simply a bounded variation process), we have that

| (67) | ||||

Since is not a transition time of a.s., we can write the last term in the above equation as follows:

Next, using the local martingales (6) and (10), we have

where we had also used that , , and a.e. and, hence, the integrands in the last two integrals with respect to can be evaluated at instead of . All together, we have the semimartingale decomposition

| (68) |

where is a local martingale and is the so-called generator of defined by

| (69) |

for each . The local martingale component in (68) takes the form:

| (70) |

where the functions , , and are evaluated at and we used the notation (11).

Appendix C Proof of the verification theorems

Proof of Theorem 5.1.

We first note that in the post-default case, the process (26) takes the form

| (71) | ||||

Define the process

| (72) |

for an admissible feedback control . For simplicity, through this part we sometimes write or instead of . We prove the result through the following steps:

By the semimartingale decomposition (68), it follows that

where

| (73) | |||||

| (74) | |||||

We have that is a concave function in since, by assumption, . If we maximize as a function of for each , we find that the optimum is given by (40). This implies that

where the last equality follows from Eq. (37). Next, let us introduce the stopping times for fixed . Then, using the notation , we get the inequality

with equality if . Since

for some constants , we conclude that with equality if .

In this step, we show that

| (75) |

where . Note that (38-i) implies

for some constants . Next, we note that satisfies (39) since

in light of (38-ii). Hence, we can apply Lemma C.1 below (with ) and obtain

Using Corollary 7.1.5 in Chow and Teicher (1978), we conclude (75).

Finally, if is non-negative, then Fatou’s Lemma implies that

for every admissible feedback control . For a general function (not necessarily non-negative), we proceed along the lines of step (2) above to show

for any feedback control satisfying (39). ∎

Proof of Theorem 5.2.

We prove the result through the following steps:

Define the process

| (76) |

where is the solution of Eq. (26) for an admissible feedback control

For simplicity, we only write . Using the same arguments as in Eq. (65) and the decomposition (6), the process (26) can be written as

| (77) | ||||

for , with the initial condition , where is defined in (34). By the semimartingale decomposition (68) with the coefficients given by (32) and

it follows that

Here, is given by

| (78) |

where and

Similarly, is defined as in (74) with , while

| (79) |

Note that, under our assumptions, admits a unique maximal point for each , since , , and . Indeed, follows from our assumption that , while is evident from the calculation

and the fact that . The optimum is given by Eq. (44) with defined implicitly by Eq. (41). In light of Eqs. (37)-(42),

Let

for a small enough . Using similar arguments to those in the proof of Theorem 5.1, we can show that

with equality if and .

We now show that

| (80) | ||||

| (81) |

where . Note that (80-81) will imply that

We only prove (80) ((81) can be treated similarly). Note that (38-i) implies

for some constants . Next, we note that satisfies (39) since both and satisfies (38-ii) by assumption. Also, satisfies (28) by assumption. Hence, we can applying Lemma C.1 below and obtain

Using Corollary 7.1.5 in Chow and Teicher (1978), we conclude (80).

Lemma C.1.

Proof.

For simplicity, we write instead of . Let us start by recalling that we can write (77) in the form

| (83) |

taking the coefficients as in (32). Due to (28) and (39), we can see that for a locally bounded function . Hence, by Jensen’s inequality and the previous linear growth,

for any , where and denote a generic constant that may change from line to line. Similarly, denoting () and using Burkhölder-Davis-Gundy inequality (see Theorem 3.28 in Karatzas and Shreve (1998) or Theorem IV.48 in Protter (1990)) and Jensen’s inequality,

We can then again use (39) to show that

Next, using again Burkhölder-Davis-Gundy inequality (see, e.g., Theorem 23.12 in Kallenberg (1997)),

Using (28),

Then, we can proceed as before to conclude that

Using a similar argument, we can also obtain that

Putting together the previous estimates, we conclude that the function can be bounded as follows: By Gronwall inequality, we have

and (82) is obtained by making . ∎

Appendix D Proof of Explicit Constructions

Proof of Lemma 6.2.

For fixed and , consider the function

We first observe that is a continuous function of in the interval . Indeed, we can write the above summation as

and since when , we have for . Moreover, the previous decomposition also shows for each fixed , is strictly decreasing in from onto . This implies the existence of a unique such that , for any . In light of Kumagai (1980) implicit theorem, we will also have that is continuous if we prove that is continuous in . The latter property follows because, by assumption, and are continuous, which implies directly the continuity of the functions . The continuity of the functions will follow from a similar argument to that of Lemma A.2. ∎

Proof of Proposition 6.3.

It can be checked that the function solves the Dirichlet problem (37), if the functions , satisfy the system given by Eq. (46), which may be written in matrix-vector form as

| (84) |

where and . As is continuous in by hypothesis, we have that the system admits a unique solution in by Lemma 6.1, where . Moreover, due to concavity and increasingness of the logarithmic function, and, under the choice and , the function satisfies the conditions in (38). Therefore, applying Theorem 5.1, we can conclude that, for each , is the optimal post-default value function.

Plugging the expression for inside Eq. (40), we can conclude immediately that .

It can be checked that the vector of functions , where , and the vector solving the nonlinear system of equations (45) simultaneously satisfy the system composed of Eq. (41) and Eq. (42) if the vector of functions solves the system (47), which may be written in matrix form as

It remains to show that such solution vector is unique. As we know that is continuous in , then we have that each entry is a continuous function of . Moreover, the vector is continuous, as it solves the system of differential equations given by (84). As is continuous by assumption, then ’s are continuous, thus is continuous, and consequently is continuous in . Using Lemma 6.1, we obtain that the solution vector must be unique. Moreover, under the choice of and , we have that satisfies the conditions in (38). As the logarithmic function is increasing and concave in , then , therefore it must be the optimal pre-default value function by Theorem 5.2. ∎

References

- Arzner and Delbaen (1995) Artzner, P. and Delbaen, F. Default Risk Insurance and Incomplete Markets. Mathematical Finance 5, 187-195.

- Bielecki et al. (2008) Bielecki, T., Crepey, S., Jeanblanc, M., and Rutkowski, M. Defaultable Options in a Markov intensity model of credit risk. Mathematical Finance 18, 4, 493-518, 2008.

- Bielecki and Jang (2006) Bielecki, T., and Jang, I. Portfolio optimization with a defaultable security. Asia-Pacific Financial Markets 13, 2, 113-127, 2006.

- Bielecki and Rutkowski (2001) Bielecki, T., and Rutkowski, M. Credit Risk: Modelling, Valuation and Hedging, Springer, New York, NY, 2001.

- Bo et al. (2010) Bo, L., Wang, Y., and Yang, X. An Optimal Portfolio Problem in a Defaultable Market. Advances in Applied Probability 42, 3, 689-705, 2010.

- Bremaud and Yor (1978) Bremaud, P., and Yor, M. Changes of filtration and of probability measures. Z.f.W. 45, 269-295, 1978.

- Buffington and Elliott (2002-a) Buffington, J., and Elliott, R. Regime switching and European options. In Lawrence, K.S. (ed). Stochastic theory and control. Proceedings of a Workshop, 73-81, Berline Heidelberg New York: Springer, 2002.

- Buffington and Elliott (2002-b) Buffington, J., and Elliott, R. American options with regime switching. International Journal of Theoretical and Applied Finance 5, 497-514, 2002.

- Callegaro, Jeanblanc, and Runggaldier (2010) Callegaro, G., Jeanblanc, M., and Runggaldier, W. Portfolio optimization in a defaultable market under incomplete information. Forthcoming in Decisions in Economics and Finance.

- Capponi, Figueroa-López, and Nisen (2011) Capponi, A. , Figueroa-López, J.E., and Nisen J. Numerical Schemes for Portfolio Optimization in Defaultable Markets under Regime Switching. In preparation, 2011.

- Chow and Teicher (1978) Chow, Y., and Teicher, H. Probability Theory, Springer-Verlag, New York, NY, 1978.

- Codd (1961) Coddington, E. An Introduction to Ordinary Differential Equations, Prentice-Hall, 1961.

- Duffie and Singleton (1999) Duffie, J.D., and Singleton, K.J. Modeling term structures of defaultable bonds. Review of. Financial Studies 12, 687-720, 1999.

- Elliott et al. (1994) Elliott, R. J., Aggoun, L., and Moore, J. B. Hidden Markov models: estimation and control. Berlin Heidelberg NewYork: Springer, 1994.

- Elliott et al. (2005) Elliott, R.J., Chan, L., and Siu, T.K. Option pricing and Esscher transform under regime switching. Annals of Finance 1, 423-432, 2005.

- Fleming and Pang (2004) Fleming, W., and Pang, T. An application of stochastic control theory to financial economics. SIAM Journal on Control and Optimization 43, 502-531, 2004.

- Gapeev and Jeanblanc (2010) Gapeev, P., and Jeanblanc, M. Pricing and filtering in a two-dimensional dividend switching model. International journal of theoretical and applied finance 13, 7, 1001-1017, 2010.

- Graziano and Rogers (2006) Di Graziano, G., and Rogers, L.C. Barrier Option Pricing for Assets with Markov-modulated dividends. Journal of Computational Finance 9, 4, 2006.

- Guo (2001) Guo, X. Information and Option Pricings. Quantitative Finance 1, 28-44, 2001.

- Guo et al. (2005) Guo, X., Miao, J., and Morellec, E. Irreversible investment with regime shifts. Journal of Economic Theory 122, 1, 37-59, 2005.

- Guo and Zhang (2004) Guo, X., and Zhang, Q. Closed-form solutions for perpetual American put options with regime switching, SIAM Journal on Applied Mathematics 64, 6, 2034-2049, 2004.

- Jacod and Shiryaev (2003) Jacod, J., and Shiryaev, A. Limit Theorems for Stochastic Processes, Springer-Verlag, New York, NY, 2003.

- Jarrow et al. (1997) Jarrow, R., Lando, D., and Turnbull, S. A Markov Model for the Term Structure of Credit Spreads, Review of Financial Studies 10, 481-523, 1997.

- Jiao and Pham (2010) Jiao, Y., and Pham, H. Optimal investment with counterparty risk: a default density approach, Finance and Stochastics, Forthcoming.

- Kallenberg (1997) Kallenberg, O. Foundations of Modern Probability. New York: Springer, 1997.

- Karatzas et al. (1996) Karatzas, I., Lehoczky, J., Sethi S., and Shreve S. Explicit Solution of a General Consumption/Investment Problem. Mathematics of Operations Research 11, 261-294, 1996.

- Karatzas and Shreve (1998) Karatzas, I., and Shreve S. Methods of Mathematical Finance. New York: Springer, 1998.

- Korn and Kraft (2001) Korn, R., and Kraft, H. A Stochastic Control Approach to Portfolio Problems with Stochastic Interest Rates. Siam Journal on Control and Optimization, 40, 2, 2001.

- Kovchecova et al. (2010) Kovchegova, Y., Mereditha, N., and Nirc, E. Occupation times and Bessel densities. Statistics and Probability Letters 80, 104-110, 2010.

- Kumagai (1980) Kumagai, S. An implicit function theorem: Comment. Journal of Optimization Theory and Applications 31, 2, 285-288, 1980.

- Lakner and Liang (2008) Lakner, P., and Liang W. Optimal Investment in a Defaultable Bond. Mathematics and Financial Economics 1, 3, 283-310, 2008.

- Merton (1969) Merton, R. Lifetime Portfolio Selection Under Uncertainty: The Continuous-time case, Review of Economics and Statistics 51, 247-257, 1969.

- Nagai and Runngaldier (2008) Nagai, H., and Runggaldier, W. PDE Approach to Utility Maximization for Market Models with Hidden Markov Factors. In Seminars on Stochastics Analysis, Random Fields, and Applications V, Progress in Probability, 59, R.C.Dalang, M.Dozzi, and F.Russo, eds Basel: Birkhuser Verlag, 493-506, 2008.

- Pham (2002) Pham, H. Smooth solution to optimal investment method with stochastic volatilities and portfolio constraints. Applied Mathematics and Optimization 46, 1, 55-78, 2002.

- Protter (1990) Protter, P. Stochastic Integration and Differential Equations: A New Approach, Springer-Verlag, 1990.

- Sotomayor and Cadenillas (2009) Sotomayor, L., and Cadenillas, A. Explicit Solutions of Consumption investment problems in financial markets with regime switching. Mathematical Finance 19, 2, 251–279,2009.

- Zariphopoulou (1992) Zariphopoulou, T. Investment-Consumption Models with Transaction Fees and Markov-Chain Parameters. Siam Journal on Control and Optimization 30, 3, 613-636.