American Options Based on Malliavin Calculus and

Nonparametric Variance Reduction Methods

L. A. Abbas-Turki

Universit Paris-Est, Laboratoire d’Analyse et de Math matiques Appliqu es, Champs-sur-Marne, 77454 Marne-la-Vall e Cedex2, France.B. Lapeyre

Ecole des Ponts ParisTech, CERMICS Applied Probability Research Group, Champs-sur-Marne, 77455 Marne-la-Vall e cedex 2, France.

Abstract

This paper is devoted to pricing American options

using Monte Carlo and the Malliavin calculus. Unlike the majority of

articles related to this topic, in this work we will not use

localization fonctions to reduce the variance. Our method is based

on expressing the conditional expectation using the

Malliavin calculus without localization. Then the variance of the estimator of

is reduced using closed formulas, techniques based

on a conditioning and a judicious choice of the number of simulated paths.

Finally, we perform the stopping times version of

the dynamic programming algorithm to decrease the bias. On the one hand,

we will develop the Malliavin calculus tools for exponential multi-dimensional diffusions

that have deterministic and no constant coefficients. On the other hand, we will

detail various nonparametric technics to reduce the variance.

Moreover, we will test the numerical efficiency of our method

on a heterogeneous CPU/GPU multi-core machine.

keywords:

American Options, Malliavin Calculus, Monte Carlo, GPU.

AMS:

60G40, 60H07

Introduction and objectives

To manage CPU (Central Processing Unit) power dissipation, the

processor makers have oriented their architectures to multi-cores.

This switch in technology led us to study the pricing algorithms

based on Monte Carlo (MC) for multi-core architectures using CPUs

and GPUs (Graphics Processing Units) in [1] and [2].

In the latter articles we basically studied the impact of using

GPUs instead of CPUs for pricing European options using MC and

American options using the Longstaff and Schwartz

(LS) algorithm [3].

The results of this study proves that we can greatly decrease the

execution time and the energy consumed during the simulation.

In this paper, we explore another method to price American Options

(AO) and which is based on MC using the Malliavin calculus

(MCM). Unlike the LS method that uses a regression phase which is difficult

to parallelize according to [2], the MCM is a square111What

we mean by square Monte Carlo is not necessarily simulating a square number

of trajectories, but a Monte Carlo simulation that requires a Monte Carlo

estimation, for each path, of an intermediate value (here the continuation)

and this can be done by using the same set of trajectories as the first Monte

Carlo simulation. Monte Carlo method which is more adapted to

multi-cores than the LS method. Moreover, using MCM

without localization does not depend on parametric regression,

we can increase the dimensionality of the problem without any

constraints except for adding more trajectories if we aim at more

accurate results.

American contracts can be exercised at any trading date until

maturity and their prices are given, at each time , by

[4]

(2)

where is the set of stopping times

in the time interval , is the expectation

associated to the risk neutral probability knowing that

and and are respectively the risk neutral interest

rate and the payoff of the contract.

With Markovian models (which is the case in this article), to

evaluate numerically the price (2), we first need to approach stopping

times in with stopping times taking values in

the finite set . When we do this

approximation, pricing American options can be reduced to the

implementation of the dynamic programming algorithm [4].

Longstaff and Schwartz consider the stopping times formulation of

the dynamic programming algorithm which allows them to reduce the

bias by using the actual realized cash flow. We refer the reader

to [5] for a formal presentation of the LS algorithm and

details on the convergence. In (5), we rewrite the dynamic

programming principle in terms of the optimal stopping times ,

for each path, as follows

(5)

where the set and is the continuation value whose expression is

given by

(6)

Thus, to evaluate the price (2), we need to

estimate . Algorithms devoted to American pricing

and based on Monte Carlo, differ essentially in the way they

estimate and use the continuation value (6). For

example the authors of [6] perform a regression to estimate

the continuation value, but unlike [3], they use

instead of the actual realized cash flow

to update the price in (5).

Other methods use the Malliavin Calculus [7] or the quantization

method [8] for estimation. In

[2], we implement the LS method because it is gaining

widespread use in the financial industry. As far as this work

is concerned, we are going to implement MCM but unlike [7]

we use the induction (5) for the implementation and we

reduce the variance differently, without using localization.

Formally speaking, if , we can rewrite the continuation

using the Dirac measure at the point

(7)

The second equality is obtained using the Malliavin calculus and we will specify,

in section 2 expression (15), the value of by an integration by part argument for

the Multi-dimensional Exponential Diffusions with deterministic

Coefficients (MEDC) model

in the case of deterministic non-constant triangular matrix and when

with a fixed constant (The latter case will be used as a benchmark).

Instead of simulating directly the last term in (7), in section 3 we project

using a conditioning as follows

(8)

Then, in section 4, we estimate (8) by Monte Carlo simulation and we use the approximation

(9)

and . Thus, in section 4,

we provide another method to accelerate the convergence based on a choice of the appropriate relation between

and that reduces the variance of the quotient (9). Note that, even if one can reduce the variance by an "appropriate" control variable, we choose here not to implement this kind of method because it is not standard for American options.

In the last section, on the one hand, we provide the numerical result

comparison of LS and MCM. On the other hand, we study

the results of using the two variance reduction methods (8) and (9).

Finally, we test the parallel capabilities of MCM on a desktop computer that has the following

specifications: Intel Core i7 Processor 920 with 9GB of tri-channel memory at frequency 1333MHz.

It also contains one NVIDIA GeForce GTX 480.

Let us begin with section 1 in which we establish the notations, the

Malliavin calculus tools and the model used.

1 Notations, hypothesis and key tools

Let be the maturity of the American contract, a probability space on which we define an

-dimensional standard Brownian motion and

the

-completion of the filtration generated by until

maturity. Moreover, we denote by

the -completion of the filtration generated by

until the fixed time . The process models the price of a vector of

assets which constitute the solution of the following

stochastic differential equation ( ’ is the transpose operator)

(10)

where is a deterministic triangular matrix

(). We suppose that the matrix is invertible, bounded and

uniformly elliptic which insures the existence of the inverse matrix and

its boundedness.

We choose the dynamic (10) because it is largely used

for equity models, HJM interest rate models and variance swap models. Moreover, the case of

( is a constant) will be easily tested

in the section 5. One should notice that in the case where the dynamic of is given by

we can use, for instance, the following Euler scheme to reduce this model to the model (10)

Note that this scheme does not discretize the process but the process .

Throughout this article, we will use two operators: The Malliavin derivatives and the Skorohod integral

and we define them in the same way as in [9]. For a fixed , we define the subdivision

of the finite interval by: . Then we introduce the Schwartz space of infinitely

differentiable and rapidly decreasing functions on . Let , we define the set of simple

functionals by the following representation

One can prove that is a linear and dense subspace in and that the Malliavin

derivatives of defined by

represents a process of with values in . We associate to the norm defined by

Finally, the space is the closure of with respect to this norm and we say that

if there exists a sequence that converges to in and

that is a Cauchy sequence in .

Now we use the duality property between and to define the Skorohod integral .

We say that the process if

where is a positive constant that depends on the process .

If , we define the Skorohod integral by

(11)

is the inner scalar product on .

Below, we give some standard properties of the operators and :

1.

If the process is adapted, coincides with the It integral

.

2.

The Chain Rule: Let and

a continuously differentiable function with bounded partial derivatives. Then

and:

3.

The Integration by Parts: The IP formula will be extensively

used in the next section on the time intervals and with : Let ,

an adapted process and that .

For each we have the following equality

(12)

To simplify the notations, we denote

for the heaviside function of the difference between the stock and the

coordinate of the positive vector .

Throughout this article, we will suppose that is a measurable

function with polynomial growth

where is the set of measurable functions on . The elements of the set satisfy the finiteness of the expectations computed in this article.

2 The expression of the continuation value

The first theorem of this section provides the expression

of the continuation (6) when using Malliavin

calculus for MEDC models. This theorem can be considered

as an extension of the log-normal multi-dimensional model

detailed in [7]. In Theorem 4, we provide

the expression of , introduced in Theorem 1,

without using Malliavin derivatives and this expression can be

computed using the relation (46). The last theorem is

a special case of the first one because we take

( is a constant) that will be used to test

numerically our nonparametric variance reduction methods

detailed in section 3 and section 4.

Theorem 1.

For any , and

(13)

with

(14)

where and can be computed by the following induction scheme

, for with

To prove Theorem 1, we need the following two lemmas which are proved in the appendix. Lemma 2 expresses the independence of the sum from the variable .

Lemma 2.

For any and then

(16)

The following lemma constitutes with equality (16) the two keys of the proof of Theorem 1.

Lemma 3.

For any , , and , we have

(19)

where is the inverse matrix .

Proof of Theorem 1.

To prove Theorem 1, it is sufficient to prove the following recursive relation

on the parameter for each and

(20)

Indeed, if it is the case then by density of in , one can approximate

by and pass to the limit on the left and on the right

term of (20) using Cauchy-Schwarz inequality and the dominated convergence theorem.

Let us now consider the singularity due to the heaviside, let be a mollifier function with

support equal to and such that , then for any we define

On the one hand, converges to except at and the absolute continuity of the

law of ensures that converges almost surely to .

Using the dominated convergence theorem, we prove the convergence of to in for . By Cauchy-Schwarz inequality, we prove the convergence

On the other hand, . Moreover, we observe that, according to our assumption, the distribution of the vector

admits a density with respect to the Lebesgue mesure on we denote it by

with and , thus

Because converges to , we have

which concludes the first part of this proof.

To prove the induction (20), we introduce the following notations:

The case is given by

where we replaced by in the first equality and

by its value in the second equality. Using Lemma 3 with

and the fact that does not depend on the coordinate of the Brownian motion yields

(27)

Besides using Lemma 2 for the Malliavin derivative of , we get for

Thus, the value of the last term of (27) is given by

And by duality (11) we remove the Malliavin derivative of in the last term

of the previous equality

Regrouping all terms together

Let us suppose that (20) is satisfied for and prove it for , thus

where we replaced by in the second equality.

Using Lemma 3 with

and the fact that does not depend on the coordinate () of the Brownian motion yields

(34)

Besides, if for we denote , the Malliavin derivative

of the last term of (34) provides

Using Lemma 2 for the Malliavin derivative in the two last terms, we get

Thus, introducing the random variable and using (34)

(41)

where we used the fact (37) that does not depend on .

Let us develop the last term of (41)

We applied (11) in the third equality to remove the Malliavin derivative of .

We also used (12) in the last equality. To complete the proof, we should remark that

and because is an -measurable random variable

Theorem 4 provides the expression of

in (47) without using the Malliavin derivatives

and which can be efficiently computed using (46).

We will use in Theorem 4 the set of the second order permutations

defined as the following

(44)

where is the set of permutations on and is the

identity application. By induction, one can easily prove that

(45)

with as the transition application on . We also denote by

the determinant that involves only the permutations of ,

that is to say, the associated to the matrix is given by

where is the associated to the obtained from by suppressing the

line and the column as well as the line and the column . Based on the development

according to the first line, relation (46) provides a recursive formula even more efficient than the determinant formula.

Of course, we can generalize the relation (46) to the one that

involves the development according to a line or a column

with .

Theorem 4.

Based on the assumptions and the results of Theorem 1,

for the value of is given by

(47)

with as the signature of the permutation , defined in

(44) and

where is the covariance of and .

Proof.

We prove (47) by a decreasing induction. For , the

expression (47) is clearly satisfied. We suppose that (47)

is satisfied for and we prove it for . According to Theorem 1,

,

but

the second equality is due to the fact that is a constant except for . Subsequently

Finally

The last equality is due to the development of according to the line of which can be justified by (45).

∎

As a corollary of Theorem 1 and Theorem 4, we obtain the following result.

Corollary 5.

For any , and , if then

with

(52)

and

3 Variance reduction method based on conditioning

In this section, we show that one can reduce the variance by a projection on and by using a closed formula of .

Like in section 2, we give in Theorem 6 the results of the special case

( is a constant)

that will be used to test our variance reduction method.

We begin with , we can compute the explicit value of this function of .

The closed formula can be got, for instance, from a change of probability. Indeed,

we define the probability which yields

is a deterministic normalization coefficient such that

is an exponential martingale with . Under , has the same law as a polynomial of Gaussian variables which is sufficient to conduct the computations.

Let us now denote

In what follows, we are going to prove that the function

can be explicitly known if, for each , the matrix

is invertible. First, please remark that according to our notations

and are the indices of the element in the matrix (we will use

similar convention also for , , and ). Also we notice that

the condition of invertibility of is not an important constraint, because one can choose a time

discretization such that the matrices fulfill this

condition222Nevertheless, this is a difficult task when the dimension is sufficiently big..

The computation of is based

on a regression of Gaussian variables according to the

Gaussian variables . First,

we perform a linear regression of according to

(53)

with as a Gaussian vector which is orthogonal to .

Using It isometry twice and the orthogonality of and , we obtain

If we denote and ,

we get

In the same way, we perform a linear regression of according to

(54)

with as a Gaussian vector which is orthogonal to .

Using It isometry twice and the orthogonality of and , we obtain

If we denote , we get

Now using (53), (54) and the value of and , the covariance matrices , and are given by ()

Using (53) and (54), we express and according to , and then we conduct standard Gaussian computations to obtain the expression of 333One can use Mathematica to compute it formally.. In Theorem 6, we give an explicit expression of and

in the case of multi-dimensional B&S models with independent coordinates.

We can see that now that we know the explicit value of and

, subsequently, we should choose between the simulation of:

P1)

paths of then set the continuation to the value

P2)

paths of and paths of

then set the continuation to the value

Based on a variance reduction argument, Theorem 9 will indicate the preferable

method to use.

Theorem 6.

For any , and , if then the

conditional expectation given in Theorem 5 can be reduced to

with

where

Proof.

We simplify the constant in (52) from the denominator and the numerator of

the conditional expectation ,

then we use the independence of the coordinates to obtain

Afterwards, we use the independence of the increments to obtain

where the random variable has a standard normal distribution.

Moreover we have the following equality in distribution

Computing the expectation we obtain

(56)

with .

Regarding the numerator, we condition according to and we

use the independence of coordinates

with

(57)

Knowing and , when we fix

the random variable and has a standard normal

distribution. Also, we have the following equality in distribution

for : and . Then we compute (57) which yields:

(58)

with .

Using (56) and (58) we obtain the

requested result.

∎

4 Advanced variance reduction method

We present, in this section, a less intuitive idea of variance

reduction that is based on an appropriate relation between

and in (9). This method can be applied

independently from conditioning detailed in previous section.

Lemma 7.

Let be a sequence of independent -valued

random variables that have the same law. We suppose that is square

integrable and we denote , .

Let , and

such that , then

we have the following limits when

such that

(59)

Proof.

The almost sure convergence of results from the law of the large numbers and from

the continuity of in . For the same reasons, the gradient vector converges a.s. to

. Besides and using the Slutsky Theorem, with

•

converges in law to

.

•

converges in law to .

Finally, because and are continuous, then converges in law to .

∎

Let us denote as the quotient given by

(60)

If , according to Lemma 7 converges to .

In the following two theorems we will prove that we can accelerate the speed of convergence when acting

on the relation between and . We analyze the two cases:

We almost proved this theorem, indeed, one can easily verify that

is the minimum of and is the minimum

of . To conclude we verify that

if and only if .

∎

What is really appealing, in this theorem, is the fact that even if ,

one should use or depending on whether or not. Nevertheless,

in order to apply the results of either this theorem or Theorem 9, we should have a "sufficiently good" approximation

of , , , and . With our model is explicitly known

and we can have in the same fashion as . In section 5, procedure P2 is implemented

by using the closed expression of and and simulating , , to get an approximation of

or that we use to re-simulate . In the case where and are not known,

we can implement one of the two methods that are also efficient:

M1)

Using all the simulated paths , we approximate the values of

, , , and then we compute or

that we use to re-simulate .

M2)

A fixed point alike method: Using all the simulated paths , we approximate the values of

, , , and then fix a threshold and test the condition

:

If

: Use the previous approximations except that will be

simulated using paths, such that is reached when

If

: Use the previous approximations except that will be

simulated using paths, such that is reached when

In the following theorem, we will answer on whether we should implement the simulation procedure P1 or P2.

Theorem 9.

Based on what was defined above and on the values of and given in Theorem 8, if

1. and

then .

2. and

then .

Proof.

1.

If :

then we look for the condition on that allows that the trinomial

is negative.

2.

We go through the same argument as in 1.

∎

Theorem 9 tells us that, even though we can compute explicitly the expression of , according to the correlation,

one can accelerate the convergence when using the quotient of two Monte Carlo estimators.

5 Simulation and numerical results

In this section we test our simulations on a geometric average payoff that has the following payoff

(63)

In addition, we will test the American put on minimum and the American call

on maximum that have the following payoffs

(64)

The parameters of the simulations are the following: The strike ,

the maturity , the risk neutral interest rate ,

the time discretization is defined using the time steps that is

given as a parameter in each simulation, and

with .

The model considered is a multidimensional log-normal model

All the prices and the standard deviations are computed using a sample of simulations. Besides,

the true values, to which we compare our simulation results, are set

using:

•

the one-dimensional equivalence and a tree method [10], available in Premia [11], for options with as payoff,

•

the Premia implementation of a finite difference algorithm [12] in two dimensions for and .

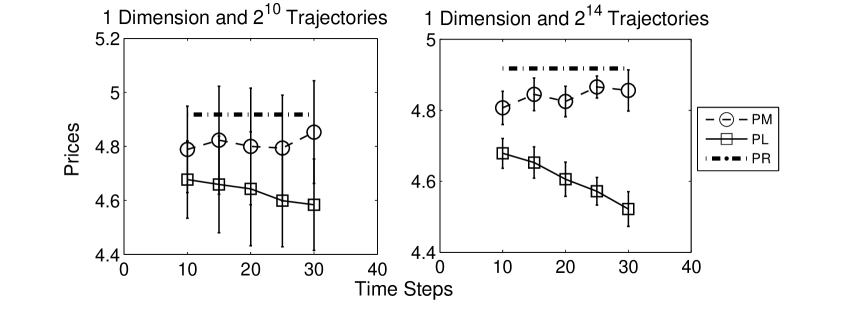

In Figure 1, we compare the P2 () version of MCM with a standard

LS algorithm. The LS is implemented using linear regression for multidimensional contracts

and using up to three degree monomials for the one-dimensional contract. The reason behind

the choice of linear regression in the multidimensional case is the fact that the regression

phase of LS can really increase the execution time without a significant

amelioration of the prices tested.

In Figure 1, even if all the prices are sufficiently good,

we see that MCM provides better prices than those of LS. Also

when we increase the time steps, MCM is more stable than LS. However, for

and time steps , we remark that one should simulate trajectories to stablize MCM. This

fact is expected due to the important variance of the ten dimension contract and that one should simulate

more trajectories, on the one hand, to have an asymptotically good approximation of the relation between and

and, on the other, to have a sufficient number of trajectories for the approximation of the continuation.

The executions of MCM and LS with trajectories are carried out in less than one second.

Moreover, using trajectories the LS and MCM are executed within seconds ().

As a conclusion from this figure, MCM provides better results than LS in approximately the same

execution time. When we increase the simulated trajectories to , the MCM prices

are stabilized for high dimensions and are always better than LS prices.

Fig. 1: MCM Vs. LS for :

PR is the real price. PM and PL are the prices obtained

respectively by MCM and LS represented with their standard deviations.

In Table 1, we remain with the same payoff but this

time we compare the different nonparametric methods of implementing MCM. In P2()

and P2(Opt), we use the same P2 method but with for the first

one and for the second (The relation between and is detailed in pages 16 and 17).

First, we remark that P2() is not stable in the multidimensional

case and can give wrong results if the time steps . However the P2 method is stabilized

when we implement the version of the advanced variance reduction

method detailed in section 4. Also when we use trajectories,

P1 and P2(Opt) are almost similar. Nevertheless, with trajectories,

P2(Opt) outperforms P1 which indicates that we fill the conditions of Theorem 9

and we have an asymptotically good approximation of the relation between and . As far as the execution

time is concerned, the time consumed by P2(Opt) is not much different from P1 when we use trajectories. In addition, using trajectories, the computations of the relation between and can be performed on the CPU when the rest of the simulation is done on the GPU. The latter fact allows a similar overall execution time for P2(Opt) and P1 (within seconds).

Table 1: P1 Vs. P2 for : The real

values are equal to , and for dimensions

one, five and ten respectively

Simulated

Dim

Time

Price

Std Deviation

Paths

n

Steps

P1

P2()

P2(Opt)

P1

P2()

P2(Opt)

Because of the bad results obtained previously with P2(), we eliminate

this method and we only consider P2(Opt) and P1. In Table

2, we analyze the American put on minimum and the American call

on maximum in two dimensions. As far as is concerned,

P2(Opt) outperforms P1 even when we use only .Regarding , P1 performs better than P2(Opt) for trajectories

which indicates that, because of the big variance produced by relatively to

, the relation between and is not well estimated.

Simulating trajectories, we obtain similar results for P1 and P2(Opt)

for .

Table 2: P1 Vs. P2 for and :

The real values are equal to and respectively

Simulated

The

Time

Price

Std Deviation

Paths

Payoff

Steps

P1

P2(Opt)

P1

P2(Opt)

Fig. 2: The speedup of using all the CPU cores

according to the number of trajectories.

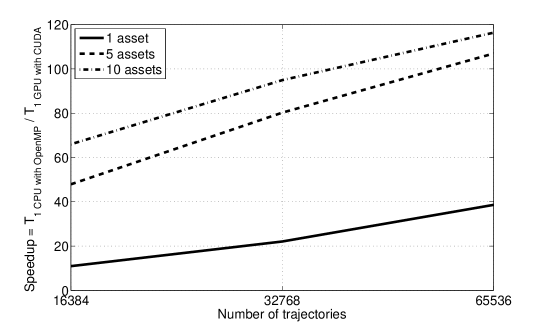

Let us now study the parallel adaptability of MCM for parallel architectures. In Figure

2, we present the speedup of parallelizing444We use OpenMP directives.

MCM on the four cores of the CPU instead of implementing it on only one core. We notice that

the speedup increases quickly according to the number of the simulated trajectories and it

reaches a saturation state for trajectories. For a large dimensional problem, the maximum speedup obtained is

approximately equal to the number of logical cores on the CPU which indicates that MCM is very

appropriate for parallel architectures. We point out, however, that our parallelization

of MCM is done on the trajectories555which is the most natural procedure of parallelizing

Monte Carlo., so the speedup is invariable according to dimensions and time steps.

Fig. 3: The speedup of using the GPU instead of

the CPU cores according to the number of trajectories.

Regarding GPU implementation, we also use a path parallelization of simulations.

In Figure 3, we present the speedup of parallelizing666We use CUDA language.

MCM on the GPU instead of implementing it on the four cores of the CPU. The speedup increases quickly

not only according to the number of simulated trajectories, but also according to the dimension

of the contract. The latter fact can be easily explained by the memory hierarchy of the GPU. The

speedups provided in Figure 3 prove, once again, the high adaptability of MCM

on parallel architectures.

6 Conclusion

In this article we provided, on the one hand, theoretical results that deal with

the continuation computations using the Malliavin calculus and how one can reduce the

Monte Carlo variance when simulating this continuation. On the other hand, we

presented numerical results related to the accuracy of the prices obtained and the

parallel adaptability of the MCM method on multi-core architectures.

As far as the theoretical results are concerned, based on the Malliavin calculus, we provided

a generalization of the value of the continuation for the multi-dimensional models with

deterministic and non a constant triangular matrix . Moreover, we pointed out that

one can effectively reduce the variance by a simple conditioning method. Finally,

we presented a less intuitive but very effective variance reduction method based on

an appropriate choice of the number of trajectories used to approximate the quotient

of two expectations.

Regarding the numerical part, we proved that the one who looks for instantaneous simulations

can obtain better and sufficiently good prices with MCM than with LS using only trajectories.

Also, unlike LS, our nonparametric variance reduction implementation of MCM does

not require parametric regression. Thus we improve the results of the simulation

by only increasing the number of trajectories. Finally, increasing the number of trajectories

is time consuming but MCM can be effectively parallelized on multi-core CPUs and GPUs. Indeed,

the MCM simulation of trajectories using the GTX 480 GPU can be performed within seconds ().

Appendix

Proof of Lemma 2.

The equality (16) can be easily proved. Indeed, using the chain rule

Besides, we assumed that which completes the proof.

Moreover, the fact that and are two triangular matrices

such that simplifies the last term which can

be also rewritten using the Malliavin derivative

This provides the required result.

Acknowledgment: We started this work in

the ANR GCPMF project, and it is supported now by CreditNext

project. The authors want to thank Professor Damien Lamberton for his

review of our work and Professor Vlad Bally for his valuable advice.

References

[1]

L. A. Abbas-Turki, S. Vialle, B. Lapeyre, and P. Mercier, “High dimensional

pricing of exotic european contracts on a GPU cluster, and comparison to a

CPU cluster,” Parallel and Distributed Computing in Finance, in IEEE

International Parallel & Distributed Processing Symposium, May 2009.

[2]

L. A. Abbas-Turki and B. Lapeyre, “American options pricing on multicore

graphic cards,” IEEE The Second International Conference on Business

Intelligence and Financial Engineering, July 2009.

[3]

F. A. Longstaff and E. S. Schwartz, “Valuing American options by simulation:

A simple least-squares approach,” The Review of Financial Studies,

vol. 14, no. 1, pp. 113–147, 2001.

[4]

P. Glasserman, Monte Carlo Methods in Financial Engineering.

Applications of Mathematics, Springer, 2003.

[5]

E. Clément, D. Lamberton, and P. Protter, “An analysis of a least squares

regression algorithm for American option pricing,” Finance and

Stochastics, vol. 17, pp. 448–471, 2002.

[6]

J. Tsitsiklis and B. V. Roy, “Regression methods for pricing complex

American-style options,” IEEE Transactions on Neural Networks,

vol. 12, no. 4, pp. 694–703, 2001.

[7]

V. Bally, L. Caramellino, and A. Zanette, “Pricing American options by

Monte Carlo methods using a Malliavin calculus approach,” Monte

Carlo Methods and Applications, vol. 11, pp. 97–133, 2005.

[8]

V. Bally and G. Pagès, “A quantization algorithm for solving

multidimensional discrete-time optimal stopping problems,” Bernoulli,

vol. 9, no. 6, pp. 1003–1049, 2003.

[9]

V. Bally, “An elementary introduction to Malliavin calculus,” INRIA

Rapport de Recherche, vol. 4718, 2003.

[10]

M. Broadie and J. Detemple, “American option valuation: new bounds,

approximations, and a comparison of existing methods securities using

simulation,” The Review of Financial Studies, vol. 9, pp. 1221–1250,

1996.

[11]

“http://www-roc.inria.fr/mathfi/Premia/,”

[12]

S. Villeneuve and A. Zanette, “Parabolic ADI methods for pricing American

options on two stocks,” Mathematics of Operations Research, vol. 27,

pp. 121–149, 2002.