Full characterization of the fractional Poisson process

Mauro Politi

Taisei Kaizoji

SSRI & Department of Economics and Business,

International Christian University, 3-10-2 Osawa, Mitaka, Tokyo, 181-8585 Japan.

Enrico Scalas

Dipartimento di Scienze e Tecnologie Avanzate,

Università del Piemonte Orientale “Amedeo Avogadro”,

Viale T. Michel 11, 15121 Alessandria, Italy.

(March 15, 2024)

Abstract

The fractional Poisson process (FPP) is a counting process with independent and identically distributed inter-event times following

the Mittag-Leffler distribution. This process is very useful in several fields of applied and theoretical physics including models for

anomalous diffusion. Contrary to the well-known Poisson

process, the fractional Poisson process does not have stationary and independent increments. It is not a Lévy process and it is

not a Markov process. In this letter, we present formulae for its finite-dimensional distribution functions, fully characterizing

the process. These exact analytical results are compared to Monte Carlo simulations.

Fractional Poisson process, Mittag-Leffler function

pacs:

02.50.Ey, 05.10.Ln

From a loose mathematical point of view, counting processes are stochastic processes that count the random number of points in a set .

They are used in many fields of physics and other applied sciences. In this letter, we will consider one-dimensional real sets with the

physical meaning of time intervals. The points will be incoming events whose duration is much smaller than the inter-event or

inter-arrival waiting time. For instance, counts from a Geiger-Müller counter can be described in this way. The number of counts, ,

in a given time interval is known to follow the Poisson distribution

(1)

where is the constant rate of arrival of ionizing particles. Together with the assumption of independent and stationary increments,

Eq. (1) is sufficient to define the homogeneous Poisson process. Curiously, one of the first occurrences of this process in the

scientific literature was connected to the number of casualties by horse kicks in the Prussian army cavalry Bortkiewicz (1898). The Poisson

process is strictly related to the exponential distribution. The inter-arrival times identically follow the exponential distribution and are independent random variables. This means that the Poisson process is a prototypical renewal process.

A justification for the ubiquity of the Poisson process has to do with its relationship with the binomial distribution. Suppose that the

time interval of interest is divided into equally spaced sub-intervals. Further assume that a counting event appears in such

a sub-interval with probability and does not appear with probability . Then, is a binomial distribution of parameters and and the expected number of events in the time interval is

given by . If this expected number is kept constant for , the binomial distribution converges to the

Poisson distribution of parameter , while, in the meantime, . However, it can be shown that

many counting processes with non-stationary increments converge to the Poisson process after a transient period. It is sufficient to require that

they are renewal process (i.e. they have independent and identically distributed (iid) inter-arrival times) and that .

In other words, many counting processes with non-independent and non-stationary increments behave as the Poisson process if observed

long after the transient period.

In recent times, it has been shown that heavy-tailed distributed inter-arrival times (for which ) do play a role in many phenomena such as blinking nano-dots Margolin and Barkai (2005); Margolin et al. (2006),

human dynamics Barabási (2005, 2010) and the related inter-trade times in financial markets Scalas et al. (2004a, 2006).

Among the counting processes with non-stationary increments, the so-called fractional Poisson process Laskin (2003), ,

is particularly important because it is the thinning limit of counting processes related to renewal processes with

power-law distributed inter-arrival times

Scalas et al. (2004b); Mainardi et al. (2004). Moreover, it can be used to approximate anomalous diffusion ruled by space-time fractional

diffusion equations Scalas et al. (2004b); Metzler and Klafter (2004); Heinsalu et al. (2006); Magdziarz et al. (2007); Fulger et al. (2008); Germano et al. (2009); Meerschaert et al. (2010).

It is a straightforward generalization of the Poisson process defined as follows.

Let be a sequence of independent and identically distributed positive random variables with

the meaning of inter-arrival times and let their common cumulative distribution function (cdf) be

(2)

where is the one-parameter Mittag-Leffler function, , defined in the complex plane as

(3)

evaluated in the point and with the prescription . In equation (3),

is Euler’s Gamma function. The sequence of the epochs, , is given by the sums of the inter-arrival

times

(4)

The epochs represent the times in which events arrive or occur. Let denote the probability

density function (pdf) of the inter-arrival times, then the probability density function of the -th epoch is simply given

by the -fold convolution of , written as . In Ref. Mainardi et al. (2004), it is shown that

(5)

where is the -th derivative of evaluated in .

The counting process counts the number of epochs (events) up to time , assuming that

is an epoch as well, or, in other words, that the process begins from a renewal point. This

assumption will be used all over this paper. is given by

(6)

In Ref. Scalas et al. (2004b), the fractional Poisson distribution is derived and it is given by

(7)

Eq. (7) coincides with the Poisson distribution of

parameter for .

In principle, equations (3) and (7) can be directly used to derive the fractional Poisson

distribution, but convergence of the series is slow. Fortunately, in a recent paper, Beghin and Orsingher proved that

(8)

where is the cdf of a stable random variable with index ,

skewness parameter , scale parameter and location Beghin and Orsingher (2009). The integral

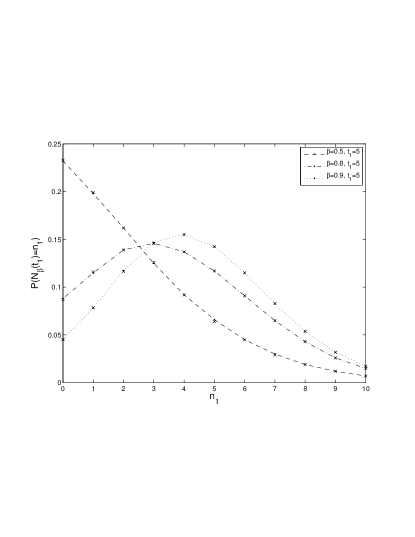

in equation (8) can be evaluated numerically and

Fig. 11 shows for three different values of . The Monte Carlo

simulation of the fractional Poisson process is based on the algorithm presented in equation (20) of Ref. Fulger et al. (2008).

Figure 1: as function of for three different values of . The crosses are estimations obtained

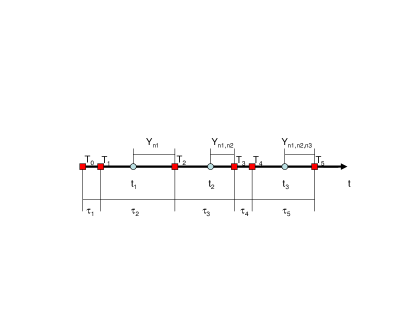

from Monte Carlo samples and the lines are given to guide the eye.Figure 2: (Color online) Pictorial illustration of the random variables used in the text. The light blue dots represent the observation points , and .

The red squares are the epochs . The conditional residual life-time is the time elapsed between

and the next epoch . It depends on previous values of , this is the number of events between and ,

with the event at not considered. Here, we have ,

and = 4. All the equations in this paper can be derived by analyzing this figure.

As a consequence of Kolmogorov’s extension theorem, in order to fully characterize the stochastic process , one has to

derive its finite dimensional distributions. A further requirement on the process’ paths

uniquely determines the process, namely that they are right-continuous step functions with left limits Billingsley (1986).

The finite-dimensional distributions are the multivariate probability distribution functions

with and .

We have already given the formula for the one-point functions in Eq. (7).

The general finite dimensional distribution can be computed observing that the event

is equivalent to

.

Therefore, we find

(9)

For instance, the two point function is given by

(10)

Let us focus on the two-point case for the sake of illustration.

As is a counting process, one has and, as a consequence of the

definition of conditional probability

(11)

For , when the fractional Poisson process coincides with the standard Poisson process, the increments are

iid random variables and one has

(12)

On the contrary, for , the increment and

are not independent. Note that can be seen

as an increment as by definition. However from Eq. (11), the conditional probability

of having epochs in the interval conditional on the observation of epochs in the interval

can be written

as a ratio of two finite dimensional distribution:

(13)

This probability can be evaluated by means of an alternative method, more appealing for a direct and

practical understanding of the dependence structure. Let

(14)

denote the residual lifetime at time (that is the time to the next epoch or renewal) conditional

on . With reference to Fig. 2, one can see that the conditional

probability is given by

the following convolution integral for

(15)

where is the pdf of . In the case , one has

(16)

where is the cdf of . The distribution of the conditional residual lifetime

can be evaluated in several ways. For instance, one can notice that it can be decomposed as follows

(17)

where is defined as

(18)

and is the position of the last epoch before conditional on , and

(19)

is the difference between and conditional on .

The pdf of is given by the following chain of equalities

(20)

where we used the independence between and and .

The pdf of is

that, together with Eq. (7), gives us the probability of the conditional

increments in Eq. (15). Notice that, for , one has and Eq. (23)

reduces to the familiar equation for the residual life-time pdf in the absence of previous renewals

(24)

This method can be applied to the general multidimensional case. As in Eq. (11) we can write

(25)

and the predictive probabilities can be evaluated as

(26)

where we defined

(27)

Again, we can use a decomposition of

(28)

where

(29)

and

(30)

The difference with the two-point case is that must be replaced by

(31)

The time between and the next renewal epoch is and it is independent from . Therefore,

the convolution

On the other hand, has the same functional form as given in Eq. (21) with

replacing . Therefore, has the following pdf

(34)

In practice, the random variable carries the memory of the observations made at times

; the knowledge of allows the computation of , and,

via Eqs. (25) and (26), the -dimensional distribution can be derived as well.

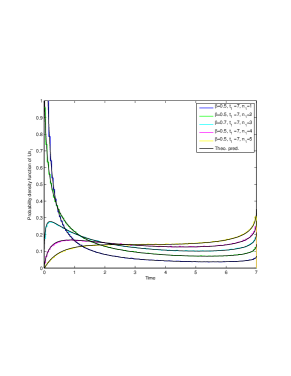

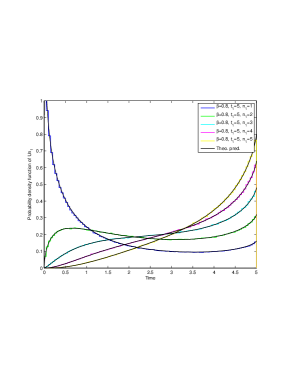

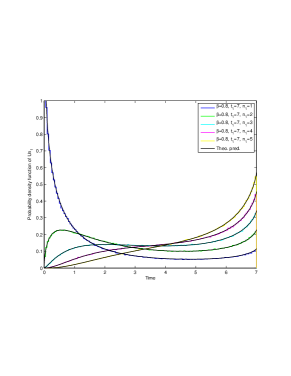

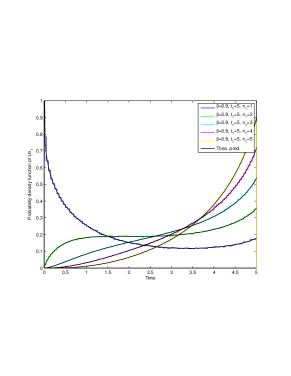

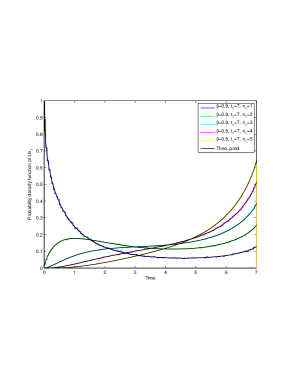

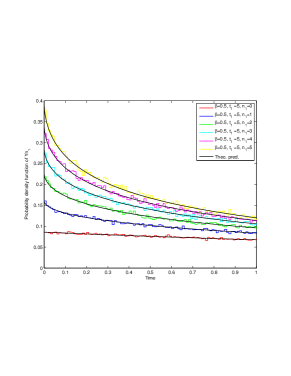

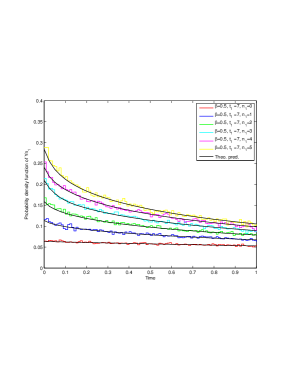

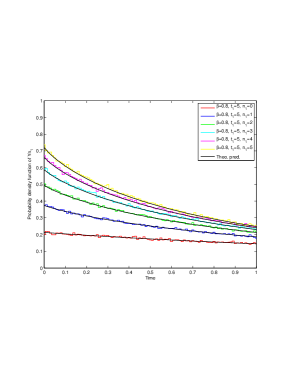

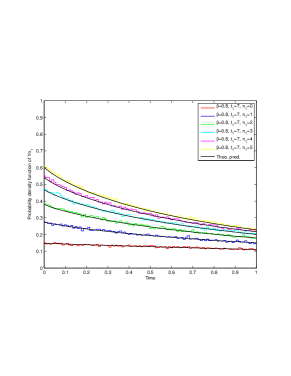

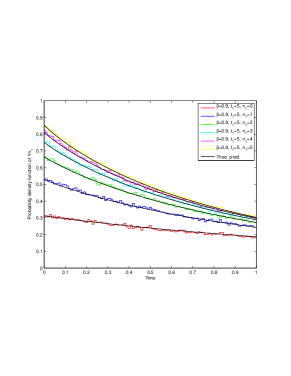

Figs. 3 and 4 compare the theoretical results of Eqs. (20), (23)

and (24) with those of a Monte Carlo simulation based on the algorithm presented in equation (20) of Ref. Fulger et al. (2008).

Figure 3: (Color online) Pdf of the random variable as given in Eq. (20) (solid black lines) compared

to Monte Carlo simulations (colored step lines) for three values of and two different values of .

different paths were simulated for each value of and the bin width is 0.05. Time is in arbitrary units.

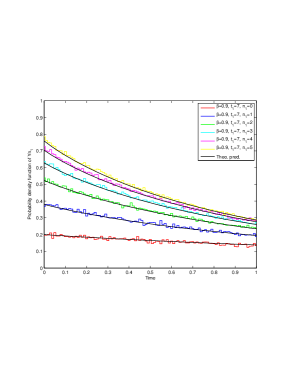

Figure 4: (Color online) Pdf of the random variable as given in Eqs. (23) and (24) (solid black lines)

compared to Monte Carlo simulations (colored step lines) for three values of and two different values of .

different paths were simulated for each value of and the bin width is 0.01. Time is in arbitrary units.

The Japanese Society for the Promotion of Science (grant N. PE09043) supported MP during his stay at the International Christian University

in Tokyo, Japan.

References

Bortkiewicz (1898)L. J. Bortkiewicz, Das Gesetz der

kleinen Zahlen (B. G. Teubner, 1898).

Margolin and Barkai (2005)G. Margolin and E. Barkai, Physical Review Letters 94, 080601 (2005).

Margolin et al. (2006)G. Margolin, V. Protasenko, M. Kuno, and E. Barkai, Journal of

Physical Chemistry B 110, 19053 (2006).