Non-invertibility Criteria in Some Heteroscedastic Models

Abstract

In order to calculate the unobserved volatility in conditional heteroscedastic time series models, the natural recursive approximation is very often used. Following Straumann and Mikosch (2006), we will call the model invertible if this approximation (based on true parameter vector) converges to the real volatility. Our main results are necessary and sufficient conditions for invertibility. We will show that the stationary GARCH(, ) model is always invertible, but certain types of models, such as EGARCH of Nelson (1991) and VGARCH of Engle and Ng (1993) may indeed be non-invertible. Moreover, we will demonstrate it’s possible for the pair (true volatility, approximation) to have a non-degenerate stationary distribution. In such cases, the volatility estimate given by the recursive approximation with the true parameter vector is inconsistent.

Key Words: Conditionally heteroscedastic time series, EGARCH, VGARCH, invertibility, Lyapunov exponent.

Journal Of Economic Literature Clasification: C14, C58.

1 Introduction

Since their introduction in the seminal papers of Engle (1982) and Bollerslev (1986), there has been a remarkable amount of interest in heteroscedastic models coming from researchers in econometrics and statistics and from financial market practitioners. Since then, many other similar models have been introduced to more accurately reflect different qualities of real data. For example, various authors have proposed a vast number of volatility expressions with asymmetries or thresholds, non-stationarities such as unit roots or time-varying parameters, or have considered multidimensional extensions and non-regular time intervals. We refer to two of more recent reviews Andersen et al. (2009) and Francq and Zakoian (2010) which discuss these and other examples and provide the necessary references.

Heteroscedastic models are used to analyze and forecast the unobserved volatility of different financial time series. It is common to construct predictions for current and future volatility values using a natural recursive volatility approximation. Let us recall its definition for a general conditional heteroscedastic model. We define such model as a solution of

| (1) |

where is the return process, is the volatility process, is a known function, , is the parameter vector taken from a set and are i.i.d. random variables on a probability space . More general versions of (1) are of course possible. Assume that are observed, fix and define the recursive volatility approximation by

for any . The quantity

| (2) |

is often used as an estimate of the volatility value at , where is any consistent estimator of . There are other possible definitions of . For example, Baillie et al. (1996) suggest using the sample mean of as a starting point instead of .

In order for approximations (2) to be consistent, it is natural to at least expect that the approximation (using the true parameter vector) converges to the unobserved value :

| (3) |

To describe models with property (3), we’ll re-use the following definition from Straumann and Mikosch (2006):

Definition 1.1

Note that many estimator types and tests are very commonly considered under the assumption of invertibility. Indeed, such estimators as the popular quasi-maximum likelihood estimator (QMLE) of Lee and Hansen (1994) and more recent GMM-type robust estimators of Boldin (2000) or minimum distance estimators as in Sorokin (2004) as well as many others are based on residuals . Their asymptotic properties are commonly established assuming convergence of residuals, therefore under invertibility. The same assumption is used for popular tests types such as goodness-of-fit and dimensionality tests (see Francq and Zakoian (2010)) and structural break tests (Boldin (2002), Horvath and Teyssiere (2001)). Therefore, the issue of non-invertibility is key for such procedures. The notable exception are estimators based on autocovariance function such as Whittle estimator applied in Giraitis and Robinson (2000) and Zaffaroni (2008).

For linear time series models such as ARMA the notion of invertibility is classic, see e.g. Brockwell and Davis (1991). For non-linear models, however, there seem to be more than one possible definition. The definition 1.1 is based on that of Granger and Andersen (1978). For detailed discussion and some further references, see Straumann and Mikosch (2006), subsection 3.2. A related definition of invertibility, in particular for bilinear models, was considered previously in Tong (1990). According to Tong’s definition, the model (1) is called invertible if is a.s. a measurable function of for any . We’ll refer to this notion as global invertibility (this is in contrast to local invertibility, see the next paragraph). Recently, there have been some further results on invertibility of non-linear models. The threshold MA models were investigated in Ling and Tong (2005) and Ling et al. (2007), and non-linear ARMA (NLARMA) models were discussed in Chan and Tong (2009).

The main goal of this paper is to show that some heteroscedastic models (for example, EGARCH of Nelson (1991) and VGARCH of Engle and Ng (1993)) may in general be non-invertible, even if the model has a strictly stationary solution. Moreover, we will provide necessary and sufficient conditions for invertibility for such models. We will demonstrate that if a model is locally invertible (see Definition 2.5 below, also Chan and Tong (2009) for the similar definition), it is also invertible. On the other hand, we’ll prove that under a slightly more restricting condition than a lack of local invertibility the model is also non-invertible. Moreover, we will show that on an extended probability space there exists a random variable , independent with , such that for the process

is stationary but

To the best of our knowledge, this is the first use of the notion of local invertibility in the literature on heteroscedastic models. Its usefulnes is that it’s much easier to check that invertibility itself, this will be discussed below. The used method is general and may be applied to many other heteroscedastic models.

The rest of the paper is organized as follows: in the subsection 2.1 we provide necessary definitions and discuss non-invertibility in more detail. The main results of the paper are given in the section 3. As a fact of independent interest and an illustration of non-invertibility, we provide the results of numerical simulations showing that it is possible to have deterministic chaos (in the sense of Devaney (1989)) in EGARCH in subsection 3.2. Finally, section 4 contains proofs.

2 Prelimiaries

2.1 Stationarity and Invertibility

Let us recall the definition of the GARCH(, ) model of Bollerslev (1986). It is defined as a solution of particular case of (1) with and

| (4) |

where

We’ll be interested in the strictly stationary solution of (4). The necessary and sufficient condition for the existence and uniqueness of such a solution was found in Bougerol and Picard (1992b). For simplicity, let’s consider a case . Then the condition reads

Condition 2.1

Here and in the rest of the paper we denote the natural logarithm .

It is easy to see that in GARCH(, ) model strict stationarity implies invertibility. Indeed, Condition 2.1 implies that . Then

therefore

implying invertibility. Using the multidimensional version of Condition 2.1, one can check that the same implication is also true for the general GARCH(, ).

However, the stationarity does not imply invertibility for other heteroscedastic models. Notably, it turns out this relation fails for the EGARCH model of Nelson (1991) and the VGARCH model of Engle and Ng (1993). For simplicity, we’ll consider only 1-dimensional models of those types.

The general model (1) for the 1-dimensional case may be written as

| (5) |

Definition 2.1

EGARCH is defined as a solution of

| (6) |

where is the parameter vector and are i.i.d.

Definition 2.2

VGARCH is defined as a solution of

| (7) |

where is the parameter vector and are i.i.d.

In order to make the models meaningful, we need to enforce certain restriction on parameter values. For EGARCH, we assume that (see Straumann and Mikosch (2006), p. 20 for discussion of why this is reasonable, note somewhat different notation) and that . For VGARCH, we demand that .

It follows from the Theorem 2.5 from Bougerol and Picard (1992a) that a necessary and sufficient conditions for the existence of a strictly stationary solution to (6) and (7) are given by

Condition 2.2

Condition 2.3

respectively. We will assume these conditions to hold throughout the rest of the paper, and denote the stationary solution of either (6) or (7) by .

The issue of invertibility is, however, more complicated. First, let’s consider the explicit expressions for . Since the sequence of random variables is unobservable, it needs to be approximated. Commonly this is done using the residuals

For EGARCH, we define recursively as a solution of

| (8) |

For VGARCH are given by

| (9) |

In both cases, we have

where is a sequence of random transformations , defined for the general model (5) by

Crucially, the random transformations defining (cf. (6), (7)) and those defining (cf. (8), (9)) are different. Indeed, for the general model (5) we have

| (10) |

Note that the right-hand side of the second equation in (10) depends not only on , but also on .

For a general heteroscedastic model invertibility holds if the top Lyapunov exponent of the corresponding sequence is negative (Proposition 3.7 of Straumann and Mikosch (2006)). Let us recall the definition of Lyapunov exponent of a family of transformations:

Definition 2.3

Assume is a stationary ergodic family of functions, such that

where is the Lipchitz norm,

Then the quantity

is called the top Lyapunov exponent.

However, estimating top Lyapunov exponent for nonlinear systems is not straightforward (and therefore checking whether the sufficient condition for invertibility holds is hard, p. 21 of Straumann and Mikosch (2006)). Note that the second equation of (10) could be nonlinear in even if the first one is linear! Therefore, the results of Bougerol and Picard (1992a) are not applicable. To the best of our knowledge, necessary and sufficient conditions for invertibility of such nonlinear models are not known.

We will consider a simple lower bound for the Lyapunov exponent which will be useful for the construction of a criteria for invertibility. From now on, we will write instead of for brevity.

Definition 2.4

Assume that the equation (5) has a unique stationary solution . Assume also that for any fixed the function is continuously differentiable. Denote

We will refer to as stability coefficient and call a heteroscedastic model locally invertible if and locally non-invertible otherwise.

A similar definition for non-linear ARMA models was considered in Chan and Tong (2009).

Unlike top Lyapunov exponent, may be written down explicitly using the chain differentiation rule. Denote

then

therefore

If the process is ergodic and

due to Birkhoff-Khinchin ergodic theorem

| (11) |

Also note that since

it must also be that

The quantity has an intuitive interpretation. It indicates whether the behaviour of is convergent or explosive in the neighborhood of the true volatility value (this will be formalized in Theorems 3.1 - 3.4). For the invertibility of (5), three cases are possible:

1. If , is stable and invertibility takes place (see Straumann and Mikosch (2006), Theorem 2.8).

2. If , Theorem 2.8 of Straumann and Mikosch (2006) is not valid anymore. The behaviour of is ”stable” in the neighborhood of the true volatility value .

3. If , the behaviour of is explosive in the neighborhood of the true volatility value .

Definition 2.5

It is interesting that the unstable assumption of case 3 is (under mild technical conditions) sufficient for the proper non-invertibility for EGARCH and VGARCH models. On the other hand, in case 2 if we only assume that , both models are invertible. These are the main results of this paper, to be considered in the following section. In addition, we show that in both cases for any starting point the sample distribution of

converges to the stationary one. Together with proper non-invertibility it implies that the approximation is inconsistent if .

3 Main Results

Before we formulate the main results, let’s introduce the conditions to be used. First one is a regularity condition.

Condition 3.1

The distribution of is absolutely continuous with respect to Lebesgue measure on with continuous density , , and

Condition 3.1 may probably be somewhat relaxed, although a condition similar to is essential in establishing the -irreducibility of relevant Markov chains, see Proofs section.

We will formulate the assumption on using the equation (11). Denote and stability coefficients for EGARCH and VGARCH respectively. Note that for EGARCH due to (8)

and by definition of the stationary solution

For VGARCH due to (9)

and

3.1 Invertibility criteria

Now we will formulate the main results:

Theorem 3.1 (Proper non-invertibility for EGARCH)

Theorem 3.2 (Proper non-invertibility for VGARCH)

Besides the proper non-invertibility, another important question is the joint behaviour of the true volatility and its approximation . As it turns out, the sample distribution converges to the stationary one:

Theorem 3.3 (LLN for in EGARCH)

i) If , the process , the stationary solution of (10) with , is ergodic and for any and starting point

where is the indicator function.

ii) If , for any starting point and

Theorem 3.4 (LLN for in VGARCH)

i) If , the process , the stationary solution of (10) with , is ergodic and for any and starting point

ii) If , for any starting point and

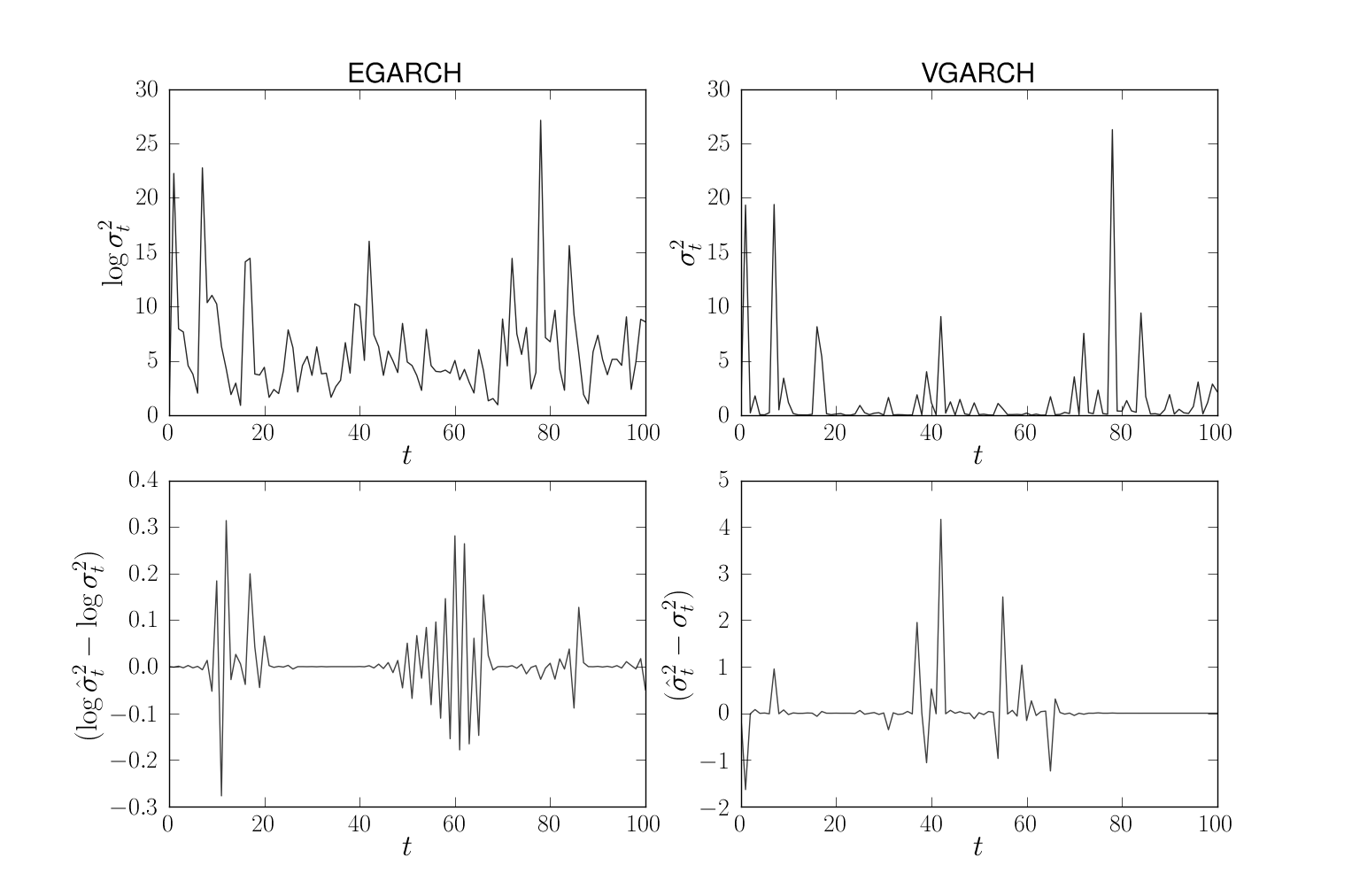

Theorems 3.1 - 3.4 indicate that for some parameter vectors finite sample volatility approximations do not converge to the actual volatility as the sample size increases. In particular, the standard recursive volatility estimator is inconsistent (this is easily checked by setting

The general heteroscedastic model (5) considered in this paper can be re-written as a particular case of NLARMA model (see Chan and Tong (2009), Equation (3)). The issue of invertibility then also becomes a special case of invertibility of NLARMA. However, the latter paper discusses only local invertibility for such models. Therefore, our results complement Chan and Tong (2009) since we establish that local invertibility is (except the case ) equivalent to invertibility for particular cases of NLARMA. It would be very interesting to investigate global invertibility of heteroscedastic models such as EGARCH and VGARCH. It easy to see that a stationary invertible model is necessary globally invertible. Indeed, denote for any ,

so that . Then due to invertibility

as and for some sub-sequence

as . The reverse relation seems more complicated and is left for future research.

Another problem (which also will not be considered here) is the behaviour of tests and estimates unver non-invertibility. Commonly, consistency and asymptotic normalilty are established under invertibility assumption. However, it was shown in Zaffaroni (2008) that the Whittle estimator (which is not residual-based) remains asymptotically normal under non-invertibility too. It will be interesting to see what happens to common estimators such as QMLE.

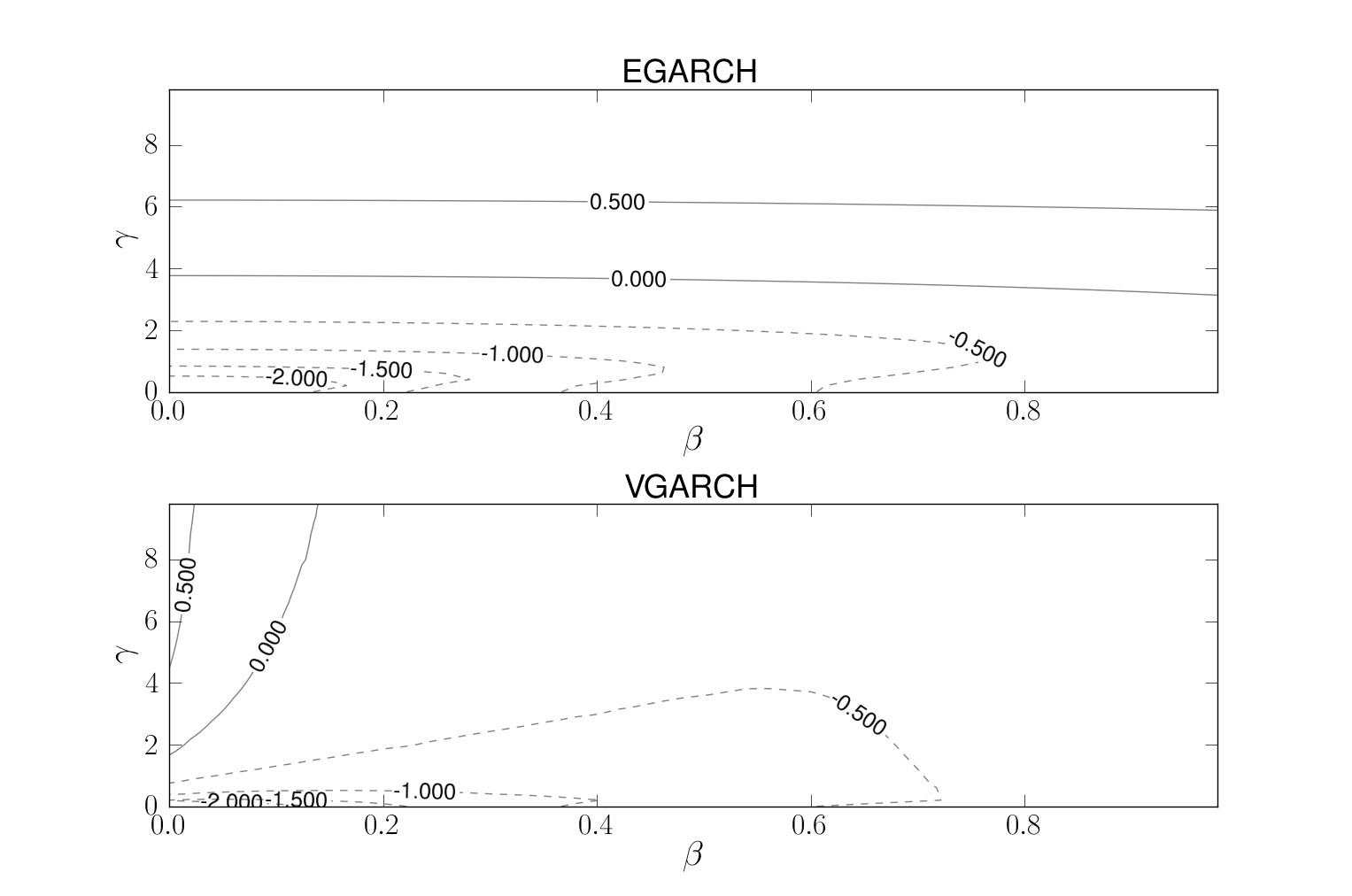

Finally, it is possible in principle that the conditions ensuring the existence of the stationary solution and the lack of stability are mutually exclusive and therefore the Theorems 3.1 - 3.4 are vacuous. However, it is easy to check the opposite (see also the Figures 3.1 and 3.2).

For EGARCH, we’ll show that for any distribution of satisfying Condition 3.1 there exists , such that the Condition 2.2 is satisfied and . Indeed, the Condition 2.2 is satisfied if and . Condition 3.1 ensures that the latter holds. It therefore suffices to choose arbitrary , , and large enough .

For VGARCH we’ll only check a more relaxed statement. Assume in addition to Condition 3.1 that there exists , such that

As a particular example of a distribution with such property, it suffices to choose a unimodal non-symmetric distribution with a maximum not at . For example, an appropriately scaled mixture of and , where both and had exponential distributions but with different parameters, is one such distribution.

Put and select arbitrary , and . Then

Due to dominated convergence theorem, when ,

For arbitrary and and small enough, .

To illustrate the main results, we show the figures demonstrating the behaviour of instability coefficient and sample paths of models (6) and (7).

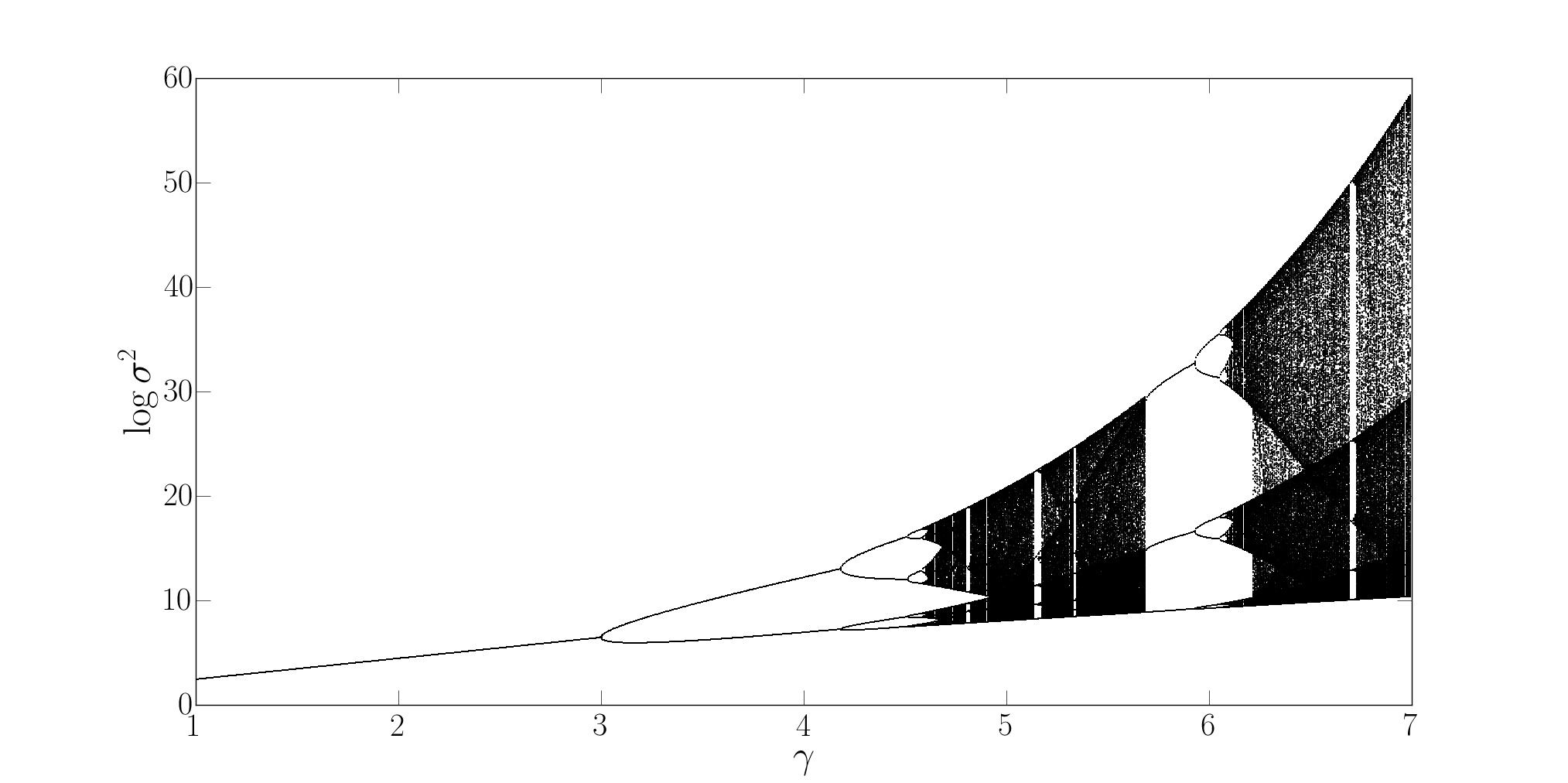

3.2 Deterministic Chaos in EGARCH

We’ll discuss a simple case of deterministic EGARCH model, which sheds light onto the origin of non-invertibility in this particular model and also on the intuitive sense of local invertibility. Assume that the Condition 2.2 is satisfied and

| (12) |

then

| (13) |

We don’t pursue the task of the formal proof, but numerical simulations show that the dynamical system given by of (13) is chaotic in the sense of Devaney once is large enough. More precisely, when increases, the system experiences period-doubling bifurcations and eventually becomes chaotic.

As discussed in Devaney (1989), the period-doubling behaviour is typical for maps . For example, the famous logistic map exhibits the same type of bifurcations. It is also quite interesting that under (12) the local non-invertibility of EGARCH is equivalent to instability of which is the only fixed point of . If this point was stable in the sense of , there would be at least an interval of stable behaviour. In the general ”stochastic” case, discussed in the previous subsection, the stability is equivalent to invertibility with the exception of the case .

4 Proofs

4.1 Markov chain foundations

In this section, we’ll present the proofs of Theorems 3.1 - 3.4. The main technical tool used is the general result stating the existence of a stationary distribution in Markov chains (Theorem 10.0.1 of Meyn and Tweedie (2009)), we’ll re-state it for convenience. We also re-use some notation and definitions from the book.

Assume that is a Markov chain with a polish space as state space, transition probabilitites , is a measure on . Also fix - a distribution on . Denote

Denote the maximal irreducibility measure (see (Meyn and Tweedie, 2009, Proposition 4.2.2)),

Theorem 4.1 (Theorem 10.0.1 of Meyn and Tweedie (2009))

If the chain is recurrent then it admits a unique (up to constant multiples) invariant measure . This invariant measure is finite (rather than merely -finite, and therefore the chain is positive), if there exists a petite set such that

| (14) |

4.2 Proofs of Theorems 3.1 and 3.2

The proofs of these two theorems will follow exactly the same recipe. In Step 1, we establish the following drift criteria from Meyn and Tweedie (2009) for a certain set :

Definition 4.1 (Strict drift towards C)

For some set , some constants and and an extended real-valued function

| (15) |

where

In Step 2 we’ll check that the chosen is petite.

In Step 3 we check the condition (14) and -irreducibility of , using the strict drift condition.

Finally, we establish that the appropriate Markov chain is indeed recurrent using the following slightly modified version of Theorem 8.4.3 from Meyn and Tweedie (2009):

Theorem 4.2

Assume that is -irreducible and there exist a petite set and a function which is unbounded off petite sets (in the sense that is petite for all n), such that has a strict drift towards . Then for all and is recurrent.

The recurrence of and Theorem 4.1 imply the existence of the stationary distribution , and finally the equation (14) ensures is finite.

Throughout the proofs we will denote () a function of which converges to (is bounded) as and model parameters and the distribution of are fixed.

Proof of Theorem 3.1.

First of all, note that the equation (8) together with (6) are equivalent to

| (16) |

where we define

It is more convenient to instead consider the chain defined by

| (17) |

where for brevity we put

denote for

and recursively define

so that

It is easy to see that for any and under Condition 3.1 . Indeed, due to Condition 3.1 for any and

For an arbitrary we get the result by induction and Fubini theorem. From now on we will consider the modification of the chain on the space

(which exists as we’ve just shown).

Step 1. Put for some

We’ll first show that for some and all

| (18) |

if and are large enough. Indeed,

| (19) |

Note that the conditions and ensure that . For and , by the definition of and Lemma 4.1 (a)

| (20) |

For , once again using definition of and Lemma 4.1 (b), we get

| (21) |

For , using Taylor’s expansion we find that for any

| (22) |

Using condition and the dominated convergence theorem, we infer that for some and large enough the right-hand side of (22) is no more than

The case is similar.

Step 2. We’ll show now that for some , the sets are -petite for the chain , and

where is the Lebesgue measure on . It will also ensure that is unbounded off petite sets, since it easy to see that sets of form are subsets of for large enough , .

The only non-trivial part is checking that once is large enough the equation

| (23) |

on and has a solution for any and . The part of (23) is equivalent to

which is satisfied if and only if

where we put

Then for , the part of (23) is satisfied and for large enough we have

| (24) |

where we used the definition of . On the other hand, if , and is large enough

| (25) |

From (24) and (25) and continuity of we conclude that for some and (23) is satisfied. Lemma 4.2 implies that is petite. The fact that is petite is proved by using Lemma 4.3 with

The technical details are omitted as they are similar to the above case. The set is petite as a union of and .

In order to ensure the strict drift condition (15), it only remains to show that

For part of ,

For part, it is achieved in a similar fashion to the proofs of (19) - (21). Thus, the correctness of (15) is established. Theorem 4.2 implies that the chain on the space is indeed recurrent.

Step 3. Let’s check now that (14) takes place with , and and large enough. Put

and note that due to (18) and law of iterated expectations

We’ll now prove that for some , the chain is -irreducible with

Indeed, for any and

hence for any and

For any due to (14)

and hence there exists , . Therefore for any ,

Now all the conditions of Theorem 4.1 are verified. Hence, we have established that the system (17) has an invariant probability measure. Define a new (extended) probability space as a cartesian product

where is a uniform measure concentrated on . There exists a measurable function , such that the distribution of

is the invariant probability measure of (17). Put

Then is a strictly stationary solution of (17). It only remains to note that due to the definition of

is the stationary solution of (10) with and

Proof of Theorem 3.2.

Let’s rewrite the VGARCH evolution equations (7) and (9) in the explicit form:

| (26) |

where we define

We will consider a Markov chain . Define

If , then

| (27) |

because the second degree polynomial with respect to inside the probability in (27) has at most roots and the distribution of is continuous due to Condition 3.1. Similarly, for any and due to induction and Fubini theorem

Hence we the chain has a modification defined on , which we will consider from now on.

We also recursively define

so that

Step 1. Fix positive real and . Their values will be chosen later, for now we’ll just say that we select them in the following order: is small enough, then large enough, then large enough, large enough, and finally - large enough. Define

In order to check the strict drift condition, we’ll demostrate that for some and all

| (28) |

if and are chosen appropriately. First note that

| (29) |

Second, we’ll show that for any

| (30) |

where depends only on model parameters. For any

| (31) |

where

Condition implies that , thus . Note also that both and are uniformly bounded. Due to Lemma 4.1 (c) and (31), (30) is fulfilled. Applying it together with (29) iteratively, we obtain

| (32) |

where (not importantly),

| (33) |

For , , using (30) and (29) we infer

for any and ,

| (34) |

If , , we similarly have

once

| (35) |

The case is less straightforward. First, fix any and assume (any function which grows quicker than linearly but slower than exponentially will work). The case of such that

is considered similarly, we have

if

| (36) |

Consider now the case (and by definition of ). We will choose large enough, depending on . Note that

| (37) |

Let’s estimate the right-hand side of (37) from above. Note that

thus due to Lemma 4.1 (c), the family of conditional distributions

is uniformly integrable. For a fixed , due to the fact that the function is continuous

as uniformly in . Therefore, due to dominated convergence theorem for and appropriately quickly,

Finally, for large enough and appropriately chosen , for any the right-hand side of (37) is no greater than

and for all

if only

| (38) |

To sum up, we have shown that for (28) to be true the constants defining the function may be chosen in the following order:

1) .

2) is large enough so that (38) holds.

3) is large enough and - large enough depending on , so that (36) holds and the rhs of (37) is no greater than for .

Thus, (28) is established.

Step 2. Similarly to the proof of Step 2 of the Theorem 3.1, we will show now that the sets are -petite for the chain , and

with some , , where is Lebesgue measure on . It will also ensure that is unbounded off petite sets, since it easy to see that sets of form are subsets of for large enough , .

For that, we will use Lemma 4.2 with

To ensure the Lemma’s conditions, we will show that once is large enough the equation

| (39) |

on and has a solution for and any , such that . Indeed, there exists a continuous function , defined for large and any , such that

| (40) |

Note that on is uniformly separated from both and . Assume that ; the case is similar. When , and for some

On the other hand, when , for some

and

Since is a continuous function, for large enough there’s a solution to (39), such that . Due to Lemma 4.2, for some and any

To ensure the strict drift condition (15), it only remains to show that

It easily follows from (29) and (32). Thus, the correctness of (15) is established. Theorem 4.2 implies that is indeed recurrent.

4.3 Proof of the case i) of Theorems 3.3 and 3.4

The proofs for these laws of large numbers will also require some general Markov chain technique. Essentially, they are corollaries of theorems 3.1 and 3.2 and of corresponding Markov chains being positive Harris recurrent.

Definition 4.2

The set is called Harris recurrent if for all

The Markov chain is called Harris recurrent if any set in is Harris recurrent.

We will proof the case i) of both theorems simultaneously. Consider the chain defined either by (16) or (26). For such a chain, positivity was proven in theorems 3.1 and 3.2. Aperiodicity follows from the fact that

and petiteness of , . In the Step 3 of theorems 3.1 and 3.2 we showed that for , large enough and any , where is either or . By (Meyn and Tweedie, 2009, Proposition 9.1.1), this implies Harris recurrence. By (Meyn and Tweedie, 2009, Theorem 13.0.1), for any

| (41) |

as . By (Meyn and Tweedie, 2009, Theorem 17.0.1), positive Harris recurrence also implies LLN of the form

| (42) |

for any , , where is a stationary version of . It remains to check that the statement we need is a combination of (41) and (42). Indeed, denote

By (42) and Fubini theorem applied to and

which implies ergodicity for the process . By (41) and Borel-Cantelli lemma, for any

Therefore, for any

and for any random variable which is measurable with respect to

Setting , where is any starting point for , concludes the proof.

4.4 Proof of Theorem 3.3 ii)

We will use notation from the proof of case i). It suffices to check that for the chain , defined in (17) and any and

We will use Theorem 8.4.3 from Meyn and Tweedie (2009) in order to establish transience of the chain . Denote

For brevity, denote

Let us now check that for some and any , such that ,

| (43) |

Indeed, for and any due to Fatou’s lemma

Therefore, (43) holds true for all small as needed.

As was shown during the proof of Step 2 of Theorem 3.1, the set is petite for any , . During Step 3 of the same Theorem, it was established that the chain is -irreducible. The exact same proof of irreducibility works in the case too, except for the equality which is not true anymore. Instead, we’ll verify directly that for large enough and and any there exists , such that . It suffices to check that for any and large enough there exist , such that

Indeed, for any there exist , such that

Then for any

and

It remains to choose any . Hence, the chain is -irreducible. It’s easy to check now that and are both in .

4.5 Proof of Theorem 3.4 ii)

We need to check that for the chain , defined in (26) and any and

Fix , and denote

with as defined during the Step 1 of the proof of Theorem 3.2. Let us now check that for some , , and any , such that ,

| (44) |

It’s easy to see that for and

| (46) |

Put

we will select in what follows. For such that we have

where

Let’s estimate and separately. First, using (46), (45) and the inequality

| (47) |

which is valid for any , we get

| (48) |

According to (31) and Lemma 4.1 (c), the nominator (48) is uniformly integrable for , and its denominator tends to infinity for a fixed as

Due to dominated convergence theorem,

as .

For we will consider 2 cases.

1) . Similarly to the estimation of the right-hand side of (37), when is large enough, is small enough, for any such that

we have

Therefore, for any such ,

we have

| (49) |

XXX Add the proof of -irreducibility.

4.6 Auxilliary results

Lemma 4.1

Assume is a random variable with a distribution absolutely continuous with respect to Lebesgue measure with density , such that

Then

| (a) |

| (b) |

and for any and

| (c) |

Proof.

(a) If the left-hand side is . If , due to Condition 3.1 for any

where for all . Noting that is uniformly bounded on , is integrable over the same interval and that

concludes the proof (using a slightly modified dominated convergence theorem). The case is similar.

(b) For and

Since may be arbitrarily small, the proof for is thus complete. The case is similar.

(c) For any the polynom has 2 roots, denote them and . Then

and it’s easy to check that

It suffices to show that

Since

it is enough to check that

Indeed, for due to Condition 3.1

where, once again, . The case is similar, and is obvious.

Lemma 4.2

Let be an arbitrary set and be a continuously differentiable function for any . Assume also that for any the equation

has a solution

which is uniformly bounded for , .

Also assume to be i.i.d. random variables with and absolutely continuous distribution whose density is uniformly separated from on

Put . Then for some and any ,

where is standard Lebesgue measure on .

Proof. Denote a -ball in with a center in and radius , then for small enough and any ,

| (51) |

The inequality (51) implies that for some and any parallelepiped

The application of monotone class theorem concludes the proof.

The following is a direct corollary of Lemma 4.2:

Lemma 4.3

In the conditions of Lemma 4.2, assume that

where is an arbitrary set and is a measurable space and for any

is measurable. Also assume that for some random element in , independent with ,

for any . Then for some and any ,

5 Acknowledgements

The author is grateful for the support of AHL Research during work on this paper. I would also like to thank Dr. Jeremy Large, Professor Neil Shephard, Dr. Kevin Sheppard (all of Oxford-Man Institute of Quantitative Finance), Professor Anders Rahbek (Copenhagen) and Professors Michael Boldin, Yuri Tyurin and Valeri Tutubalin (all of Moscow State University) for helpful discussions.

The author also thanks anonymous referees for their suggestions which helped to improve the presentation.

References

- Andersen et al. (2009) Andersen, T.G., Davis, R.A., Kreiss, J.-P. and Mikosch, T., (2009), Handbook of financial time series. Springer.

- Boldin (2000) Boldin, M.V., (2000), On empirical processes in heteroscedastic time series and their use for hypothesis testing and estimation. Mathematical Methods of Statistics 9, 65-89.

- Boldin (2002) Boldin, M.V., (2002), On sequential residual empirical processes in heteroscedastic time series. Mathematical Methods of Statistics 11, 453-464.

- Baillie et al. (1996) Baillie, R. T., Bollerslev, T. and Mikkelsen, H. O., (1996), Fractionally integrated generalized autoregressive conditional heteroscedasticity. Journal of Econometrics 74, 3-30.

- Bollerslev (1986) Bollerslev, T., (1986), Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics 31, 307-327.

- Bougerol and Picard (1992a) Bougerol, P. and N. Picard, N., (1992a), Strict stationarity of Generalized autoregressive processes. The Annals of Probability 20, 1714-1730.

- Bougerol and Picard (1992b) Bougerol P. and Picard, N., (1992b), Stationarity of GARCH processes and of some nonnegative time series. Journal of Econometrics 52, 115-127.

- Brockwell and Davis (1991) Brockwell, P. and Davis, R., (1991), Time series: theory and methods. 2nd ed. Springer, New York.

- Chan and Tong (2009) Chan, K.-S. and Tong, H., (2010), Note on the invertibility of nonlinear ARMA Model. Journal of Statistical Planning and Inference 140, 3709-3714.

- Devaney (1989) Devaney, R., (1989), An introduction to chaotic dynamical systems. 2nd ed., Addison-Wesley Publishing Company, Advanced Book Program, Redwood City, CA.

- Engle (1982) Engle, R.F., (1982), Autoregressive conditional heteroskedasticity with estimates of the variance of U.K. inflation. Econometrica 50, 987-1008.

- Engle and Ng (1993) Engle, R.F. and Ng, V., (1993), Measuring and testing impact of news on volatility. Journal of Finance 48, 1749-1778.

- Francq and Zakoian (2010) Francq, C. and Zakoian, J.-M., (2010), GARCH models: structure, statistical inference and financial applications. Wiley-Blackwell.

- Giraitis and Robinson (2000) Giraitis, L. and Robinson, P.M., (2000), Whittle estimation of ARCH models. Econometric Theory 17, 608-631.

- Granger and Andersen (1978) Granger, C. W. J. and Andersen, A., (1978), On the invertibility of time series models. Stochastic Processes and Applications 8, 87-92.

- Horvath and Teyssiere (2001) Horvath, L. and Teyssiere, G., (2001), Empirical process of the squared residuals of an arch sequence. The Annals of Statistics 29, 445-469.

- Lee and Hansen (1994) Lee, S.W. and Hansen, B., (1994), Asymptotic Theory for the GARCH(, ) quasimaximum likelihood estimator. Econometric Theory 10, 29-53.

- Ling and Tong (2005) Ling, S. and Tong, H., (2005), Testing for a linear MA model against threshold MA models. The Annals of Statistics 33, 2529-2552.

- Ling et al. (2007) Ling, S., Tong, H. and Li, D., (2007), Ergodicity and invertibility of threshold moving-average models. Bernoulli 13, 161-168.

- Meyn and Tweedie (2009) Meyn, S. and Tweedie, R.L., (2009), Markov chains and stochastic stability. 2nd ed., Cambridge University Press, Cambridge.

- Nelson (1991) Nelson, D. B., (1991), Conditional heteroskedasticity in asset returns: a new approach. Econometrica 59, 347-370.

- Sorokin (2004) Sorokin, A. A., (2004), On the minimum distance estimates in ARCH model. Mathematical Methods of Statistics 13, 329-355.

- Straumann and Mikosch (2006) Straumann, D. and Mikosch, T., (2006), Quasi-maximum-likelihood estimation in conditionally heteroscedastic time series: a stochastic recurrence equations approach. The Annals of Statistics 34, 2449-2495.

- Tong (1990) Tong, H., (1990), Non-linear time series: a dynamical system approach. Oxford University Press, Oxford.

- Zaffaroni (2008) Zaffaroni, P., (2009), Whittle estimation of EGARCH and other exponential volatility models. Journal of Econometrics 151, 190-200.