Efficient Learning of Generalized Linear and Single Index Models with Isotonic Regression

Abstract

Generalized Linear Models (GLMs) and Single Index Models (SIMs) provide powerful generalizations of linear regression, where the target variable is assumed to be a (possibly unknown) 1-dimensional function of a linear predictor. In general, these problems entail non-convex estimation procedures, and, in practice, iterative local search heuristics are often used. Kalai and Sastry (2009) recently provided the first provably efficient method for learning SIMs and GLMs, under the assumptions that the data are in fact generated under a GLM and under certain monotonicity and Lipschitz constraints. However, to obtain provable performance, the method requires a fresh sample every iteration. In this paper, we provide algorithms for learning GLMs and SIMs, which are both computationally and statistically efficient. We also provide an empirical study, demonstrating their feasibility in practice.

1 Introduction

The oft used linear regression paradigm models a target variable as a linear function of a vector-valued input . Namely, for some vector , we assume that . Generalized linear models (GLMs) provide a flexible extension of linear regression, by assuming the existence of a “link” function such that . “links” the conditional expectation of to in a linear manner, i.e. (see [MN89] for a review). This simple assumption immediately leads to many practical models, including logistic regression, the workhorse for binary probabilistic modeling.

Typically, the link function is assumed to be known (often chosen based on problem-specific constraints), and the parameter is estimated using some iterative procedure. Even in the setting where is known, we are not aware of a classical estimation procedure which is computationally efficient, yet achieves a good statistical rate with provable guarantees. The standard procedure is iteratively reweighted least squares, based on Newton-Ralphson (see [MN89]).

In Single Index Models (SIMs), both and are unknown. Here, we face the more challenging (and practically relevant) question of jointly estimating and , where may come from a large non-parametric family such as all monotonic functions. There are two issues here: 1) What statistical rate is achievable for simultaneous estimation of and ? 2) Is there a computationally efficient algorithm for this joint estimation? With regards to the former, under mild Lipschitz-continuity restrictions on , it is possible to characterize the effectiveness of an (appropriately constrained) joint empirical risk minimization procedure. This suggests that, from a purely statistical viewpoint, it may be worthwhile to attempt to jointly optimize and on the empirical data.

However, the issue of computationally efficiently estimating both and (and still achieving a good statistical rate) is more delicate, and is the focus of this work. We note that this is not a trivial problem: in general, the joint estimation problem is highly non-convex, and despite a significant body of literature on the problem, existing methods are usually based on heuristics, which are not guaranteed to converge to a global optimum (see for instance [WHI93, HH94, MHS98, NT04, RWY08]). We note that recently, [SSSS10] presented a kernel-based method which does allow (improper) learning of certain types of GLM’s and SIM’s, even in an agnostic setting where no assumptions are made on the underlying distribution. On the flip side, the formal computational complexity guarantee degrades super-polynomially with the norm of , which [SSSS10] show is provably unavoidable in their setting.

The recently proposed Isotron algorithm [KS09] provides the first provably efficient method for learning GLMs and SIMs, under the common assumption that is monotonic and Lipschitz, and assuming the data corresponds to the model. The algorithm attained both polynomial sample and computational complexity, with a sample size dependence that does not depend explicitly on the dimension. The algorithm is a variant of the “gradient-like” perceptron algorithm, with the added twist that on each update, an isotonic regression procedure is performed on the linear predictions. Recall that isotonic regression is a procedure which finds the best monotonic one dimensional regression function. Here, the well-known Pool Adjacent Violator () algorithm provides a computationally efficient method for this task.

Unfortunately, a cursory inspection of the Isotron algorithm suggests that, while it is computationally efficient, it is very wasteful statistically, as each iteration of the algorithm throws away all previous training data and requests new examples. Our intuition is that the underlying technical reasons for this are due to the fact that the algorithm need not return a function with a bounded Lipschitz constant. Furthermore, empirically, it not clear how deleterious this issue may be.

This work seeks to address these issues both theoretically and practically. We present two algorithms, the GLM-tron algorithm for learning GLMs with a known monotonic and Lipschitz , and the L-Isotron algorithm for the more general problem of learning SIMs, with an unknown monotonic and Lipschitz . Both algorithms are practical, parameter-free and are provably efficient, both statistically and computationally. Moreover, they are both easily kernelizable. In addition, we investigate both algorithms empirically, and show they are both feasible approaches. Furthermore, our results show that the original Isotron algorithm (ran on the same data each time) is perhaps also effective in several cases, even though the algorithm does not have a Lipschitz constraint.

More generally, it is interesting to note how the statistical assumption that the data are in fact generated by some GLM leads to an efficient estimation procedure, despite it being a non-convex problem. Without making any assumptions, i.e. in the agnostic setting, this problem is at least hard as learning parities with noise.

2 Setting

We assume the data are sampled i.i.d. from a distribution supported on , where is the unit ball in -dimensional Euclidean space. Our algorithms and analysis also apply to the case where is the unit ball in some high (or infinite)-dimensional kernel feature space. We assume there is a fixed vector , such that , and a non-decreasing -Lipschitz function , such that for all . Note that plays the same role here as in generalized linear models, and we use this notation for convenience. Also, the restriction that is 1-Lipschitz is without loss of generality, since the norm of is arbitrary (an equivalent restriction is that and that is -Lipschitz for an arbitrary ).

Our focus is on approximating the regression function well, as measured by the squared loss. For a real valued function , define

measures the error of , and measures the excess error of compared to the Bayes-optimal predictor . Our goal is to find such that (equivalently, ) is as small as possible.

In addition, we define the empirical counterpart , based on a sample , to be

Note that is the standard fixed design error (as this error conditions on the observed ’s).

Our algorithms work by iteratively constructing hypotheses of the form , where is a non-decreasing, -Lipschitz function, and is a linear predictor. The algorithmic analysis provides conditions under which is small, and using statistical arguments, one can guarantee that would be small as well.

To simplify the presentation of our results, we use the standard notation, which always hides only universal constants.

3 The GLM-tron Algorithm

We begin with the simpler case, where the transfer function is assumed to be known (e.g. a sigmoid), and the problem is estimating properly. We present a simple, parameter-free, perceptron-like algorithm, GLM-tron, which efficiently finds a close-to-optimal predictor. We note that the algorithm works for arbitrary non-decreasing, Lipschitz functions , and thus covers most generalized linear models. The pseudo-code appears as Algorithm 1.

To analyze the performance of the algorithm, we show that if we run the algorithm for sufficiently many iterations, one of the predictors obtained must be nearly-optimal, compared to the Bayes-optimal predictor.

Theorem 1.

Suppose are drawn independently from a distribution supported on , such that , where , and is a known non-decreasing -Lipschitz function. Then for any , the following holds with probability at least : there exists some iteration of GLM-tron such that the hypothesis satisfies

In particular, the theorem implies that some has . Since equals up to a constant, we can easily find an appropriate by using a hold-out set to estimate , and picking the one with the lowest value.

The proof is along similar lines (but somewhat simpler) than the proof of our subsequent Thm. 2. The rough idea of the proof is showing that at each iteration, if is not small, then the squared distance is substantially smaller than . Since this is bounded below by , and , there is an iteration (arrived at within reasonable time) such that the hypothesis at that iteration is highly accurate. The proof is provided in Appendix A.1.

4 The L-Isotron Algorithm

We now present L-Isotron, in Algorithm 2, which is applicable to the harder setting where the transfer function is unknown, except for it being non-decreasing and -Lipschitz. This corresponds to the semi-parametric setting of single index models.

The algorithm that we present is again simple and parameter-free. The main difference compared to GLM-tron algorithm is that now the transfer function must also be learned, and the algorithm keeps track of a transfer function which changes from iteration to iteration. The algorithm is also rather similar to the Isotron algorithm [KS09], with the main difference being that instead of applying the procedure to fit an arbitrary monotonic function at each iteration, we use a different procedure, , which fits a Lipschitz monotonic function. This difference is the key which allows us to make the algorithm practical while maintaining non-trivial guarantees (getting similar guarantees for the Isotron required a fresh training sample at each iteration).

The procedure takes as input a set of points in , and fits a non-decreasing, -Lipschitz function , which minimizes . This problem has been studied in the literature, and we followed the method of [YW09] in our empirical studies. The running time of the method proposed in [YW09] is . While this can be slow for large-scale datasets, we remind the reader that this is a one-dimensional fitting problem, and thus a highly accurate fit can be achieved by randomly subsampling the data (the details of this argument, while straightforward, are beyond the scope of the paper).

We now turn to the formal analysis of the algorithm. The formal guarantees parallel those of the previous subsection. However, the rates achieved are somewhat worse, due to the additional difficulty of simultaneously estimating both and . It is plausible that these rates are sharp for information-theoretic reasons, based on the 1-dimensional lower bounds in [Zha02a] (although the assumptions are slightly different, and thus they do not directly apply to our setting).

Theorem 2.

Suppose are drawn independently from a distribution supported on , such that , where , and is an unknown non-decreasing -Lipschitz function. Then the following two bounds hold:

-

1.

(Dimension-dependent) With probability at least , there exists some iteration of L-Isotron such that

-

2.

(Dimension-independent) With probability at least , there exists some iteration of L-Isotron such that

As in the case of Thm. 1, one can easily find which satisfies the theorem’s conditions, by running the L-Isotron algorithm for sufficiently many iterations, and choosing the hypothesis which minimizes based on a hold-out set.

5 Proofs

5.1 Proof of Thm. 2

First we need a property of the algorithm that is used to find the best one-dimensional non-decreasing -Lipschitz function. Formally, this problem can be defined as follows: Given as input the goal is to find such that

| (1) |

is minimal, under the constraint that for some non-decreasing -Lipschitz function . After finding such values, obtains an entire function by interpolating linearly between the points. Assuming that are in sorted order, this can be formulated as a quadratic problem with the following constraints:

| (2) | |||||

| (3) |

Lemma 1.

Let be input to where are increasing and . Let be the output of . Let be any function such that , for , then

Proof.

We first note that , since otherwise we could have found other values for which make (1) even smaller. So for notational convenience, let , and we may assume w.l.o.g. that . Define . Then we have

| (4) |

Suppose that . Intuitively, this means that if we could have decreased all values by an infinitesimal constant, then the objective function (1) would have been reduced, contradicting the optimality of the values. This means that the constraint must be tight, so we have (this argument is informal, but can be easily formalized using KKT conditions). Similarly, when , then the constraint must be tight, hence . So in either case, each summand in (4) must be non-negative, leading to the required result. ∎

We also use another result, for which we require a bit of additional notation. At each iteration of the L-Isotron algorithm, we run the procedure based on the training sample and the current direction , and get a non-decreasing Lipschitz function . Define

Recall that are such that , and the input to the L-Isotron algorithm is . Define

to be the expected value of each . Clearly, we do not have access to . However, consider a hypothetical call to with inputs , and suppose returns the function . In that case, define

for all . Our proof uses the following proposition, which relates the values (the values we can actually compute) and (the values we could compute if we had the conditional means of each ). The proof of Proposition 1 is somewhat lengthy and requires additional technical machinery, and is therefore relegated to Appendix B.

Proposition 1.

With probability at least over the sample , it holds for any that is at most the minimum of

and

The third auxiliary result we’ll need is the following, which is well-known (see for example [STC04], Section 4.1).

Lemma 2.

Suppose are i.i.d. -mean random variables in a Hilbert space, such that . Then with probability at least ,

With these auxiliary results in hand, we can now turn to prove Thm. 2 itself. The heart of the proof is the following lemma, which shows that the squared distance between and the true direction decreases at each iteration at a rate which depends on the error of the hypothesis :

Lemma 3.

Suppose that and and . Then

Proof.

We have

| Since , substituting this above and rearranging the terms we get, | ||||

| (5) | ||||

Consider the first term above,

| (6) | |||

| (7) | |||

| (8) |

The term (6) is at least , the term (8) is at least (since ). We thus consider the remaining term (7). Letting be the true transfer function, suppose for a minute it is strictly increasing, so its inverse is well defined. Then we have

The second term in the expression above is positive by Lemma 1. As to the first term, it is equal to , which by the Lipschitz property of is at least . Plugging this in the above, we get

| (9) |

This inequality was obtained under the assumption that is strictly increasing, but it is not hard to verify that the same would hold even if is only non-decreasing.

The bound on in Thm. 2 now follows from Lemma 3. Using the notation from Lemma 3, can be set to the bound in Lemma 2, since are i.i.d. -mean random variables with norm bounded by . Also, can be set to any of the bounds in Proposition 1. is clearly the dominant term. Thus, we get that Lemma 3 holds, so either , or . If the latter is the case, we are done. If not, since , and , there can be at most iterations before . Plugging in the values for results in the bound on .

Finally, to get a bound on , we utilize the following uniform convergence lemma:

Lemma 4.

Suppose that for some non-decreasing -Lipschitz and such that . Then with probability at least over a sample , the following holds simultaneously for any function such that and a non-decreasing and -Lipschitz function :

The proof of the lemma uses a covering number argument, and is shown as part of the more general Lemma 7 in the supplementary material. This lemma applies in particular to . Combining this with the bound on , and using a union bound, we get the result on as well.

6 Experiments

In this section, we present an empirical study of the GLM-tron and the L-Isotron algorithms. The first experiment we performed is a synthetic one, and is meant to highlight the difference between L-Isotron and the Isotron algorithm of [KS09]. In particular, we show that attempting to fit the transfer function without any Lipschitz constraints may cause Isotron to overfit, complementing our theoretical findings. The second set of experiments is a comparison between GLM-tron, L-Isotron and several competing approaches. The goal of these experiments is to show that our algorithms perform well on real-world data, even when the distributional assumption required for their theoretical guarantees does not precisely hold.

6.1 L-Isotron vs Isotron

As discussed earlier, our L-Isotron algorithm (Algorithm 2) is similar to the Isotron algorithm of [KS09], with two main differences: First, we apply at each iteration to find the best Lipschitz monotonic function to the data, while they apply the (Pool Adjacent Violator) procedure to fit a monotonic (generally non-Lipschitz) function. The second difference is the theoretical guarantees, which in the case of Isotron required working with a fresh training sample at each iteration.

While the first difference is inherent, the second difference is just an outcome of the analysis. In particular, one might still try and apply the Isotron algorithm, using the same training sample at each iteration. While we do not have theoretical guarantees for this algorithm, it is computationally efficient, and one might wonder how well it performs in practice. As we see later on, it actually performs quite well on the datasets we examined. However, in this subsection we provide a simple example, which shows that sometimes, the repeated fitting of a non-Lipschitz function, as done in the Isotron algorithm, can cause overfit and thus hurt performance, compared to fitting a Lipschitz function as done in the L-Isotron algorithm.

We constructed a synthetic dataset as follows: In a high dimensional space , we let be the true direction. The transfer function is . Each data point is constructed as follows: the first coordinate is chosen uniformly from the set , and out of the remaining coordinates, one is chosen uniformly at random and is set to . All other coordinates are set to . The values are chosen at random from , so that . We used a sample of size to evaluate the performance of the algorithms.

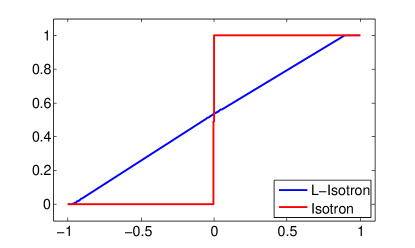

In the synthetic example we construct, the first attribute is the only relevant attribute. However, because of the random noise in the values, Isotron tends to overfit using the irrelevant attributes. At data points where the true mean value equals , Isotron (which uses ) tries to fit the value or , whichever is observed. On the other hand, L-Isotron (which uses ) predicts this correctly as close to , because of the Lipschitz constraint. Figure 1 shows the link functions predicted by L-Isotron and Isotron on this dataset. Repeating the experiment times, the error of L-Isotron, normalized by the variance of the values, was , while the normalized error for the Isotron algorithm was . In addition, we observed that L-Isotron performed better rather consistently across the folds - the difference between the normalized error of Isotron and L-Isotron was .

| dataset | L-Iso | GLM-t | Iso | Lin-R | Log-R | SIM |

|---|---|---|---|---|---|---|

| communities | 0.34 0.04 | 0.34 0.03 | 0.35 0.04 | 0.35 0.04 | 0.34 0.03 | 0.36 0.05 |

| concrete | 0.35 0.06 | 0.40 0.07 | 0.36 0.06 | 0.39 0.08 | 0.39 0.08 | 0.35 0.06 |

| housing | 0.27 0.12 | 0.28 0.11 | 0.27 0.12 | 0.28 0.12 | 0.27 0.11 | 0.26 0.09 |

| parkinsons | 0.89 0.04 | 0.92 0.04 | 0.89 0.04 | 0.90 0.04 | 0.90 0.04 | 0.92 0.03 |

| winequality | 0.78 0.07 | 0.81 0.07 | 0.78 0.07 | 0.73 0.08 | 0.73 0.08 | 0.79 0.07 |

| dataset | GLM-t | Iso | Lin-R | Log-R | SIM |

|---|---|---|---|---|---|

| communities | 0.01 0.01 | 0.01 0.02 | 0.02 0.02 | 0.01 0.02 | 0.02 0.03 |

| concrete | 0.04 0.03 | 0.00 0.01 | 0.04 0.03 | 0.04 0.03 | 0.00 0.02 |

| housing | 0.02 0.05 | 0.00 0.07 | 0.02 0.05 | 0.01 0.05 | -0.01 0.06 |

| parkinsons | 0.03 0.02 | 0.00 0.01 | 0.02 0.01 | 0.02 0.01 | 0.04 0.04 |

| winequality | 0.03 0.02 | 0.00 0.01 | -0.05 0.03 | -0.05 0.03 | 0.01 0.01 |

6.2 Real World Datasets

We now turn to describe the results of experiments performed on several UCI datasets. We chose the following 5 datasets: communities, concrete, housing, parkinsons, and wine-quality.

On each dataset, we compared the performance of L-Isotron (L-Iso) and GLM-tron (GLM-t) with Isotron and several other algorithms. These include standard logistic regression (Log-R), linear regression (Lin-R) and a simple heuristic algorithm (SIM) for single index models, along the lines of standard iterative maximum-likelihood procedures for these types of problems (e.g., [Cos83]). The algorithm works by iteratively fixing the direction and finding the best transfer function , and then fixing and optimizing via gradient descent. For each of the algorithms we performed 10-fold cross validation, using fold each time as the test set, and we report averaged results across the folds.

Table 1 shows the mean squared error of all the algorithms across ten folds normalized by the variance in the values. Table 2 shows the difference between squared errors between the algorithms across the folds. The results indicate that the performance of L-Isotron and GLM-tron (and even Isotron) is comparable to other regression techniques and in many cases also slightly better. This suggests that these algorithms should work well in practice, while enjoying non-trivial theoretical guarantees.

It is also illustrative to see how the transfer functions found by the two algorithms, L-Isotron and Isotron, compare to each other. In Figure 2, we plot the transfer function for concrete and communities. The plots illustrate the fact that Isotron repeatedly fits a non-Lipschitz function resulting in a piecewise constant function, which is less intuitive than the smoother, Lipschitz transfer function found by the L-Isotron algorithm.

References

- [BM02] P. Bartlett and S. Mendelson. Rademacher and gaussian complexities: Risk bounds and structural results. Journal of Machine Learning Research, 3:463–482, 2002.

- [Cos83] S. Cosslett. Distribution-free maximum-likelihood estimator of the binary choice model. Econometrica, 51(3), May 1983.

- [HH94] J. Horowitz and W. Härdle. Direct semiparametric estimation of single-index models with discrete covariates, 1994.

- [KS09] A. T. Kalai and R. Sastry. The isotron algorithm: High-dimensional isotonic regression. In COLT ’09, 2009.

- [Men02] S. Mendelson. Improving the sample complexity using global data. IEEE Transactions on Information Theory, 48(7):1977–1991, 2002.

- [MHS98] A. Juditsky M. Hristache and V. Spokoiny. Direct estimation of the index coefficients in a single-index model. Technical Report 3433, INRIA, May 1998.

- [MN89] P. McCullagh and J. A. Nelder. Generalized Linear Models (2nd ed.). Chapman and Hall, 1989.

- [NT04] P. Naik and C. Tsai. Isotonic single-index model for high-dimensional database marketing. Computational Statistics and Data Analysis, 47:775–790, 2004.

- [Pis99] G. Pisier. The Volume of Convex Bodies and Banach Space Geometry. Cambridge University Press, 1999.

- [RWY08] P. Ravikumar, M. Wainwright, and B. Yu. Single index convex experts: Efficient estimation via adapted bregman losses. Snowbird Workshop, 2008.

- [SSSS10] S. Shalev-Shwartz, O. Shamir, and K. Sridharan. Learning kernel-based halfspaces with the zero-one loss. In COLT, 2010.

- [SST10] N. Srebro, K. Sridharan, and A. Tewari. Smoothness, low-noise and fast rates. In NIPS, 2010. (full version on arXiv).

- [STC04] J. Shawe-Taylor and N. Christianini. Kernel Methods for Pattern Analysis. Cambridge University Press, 2004.

- [WHI93] P. Hall W. Härdle and H. Ichimura. Optimal smoothing in single-index models. Annals of Statistics, 21(1):157–178, 1993.

- [YW09] L. Yeganova and W. J. Wilbur. Isotonic regression under lipschitz constraint. Journal of Optimization Theory and Applications, 141(2):429–443, 2009.

- [Zha02a] C. H. Zhang. Risk bounds for isotonic regression. Annals of Statistics, 30(2):528–555, 2002.

- [Zha02b] T. Zhang. Covering number bounds for certain regularized function classes. Journal of Machine Learning Research, 2:527–550, 2002.

Appendix A Appendix

A.1 Proof of Thm. 1

The reader is referred to GLM-tron (Alg. 1) for notation used in this section.

The main lemma shows that as long as the error of the current hypothesis is large the distance of our predicted direction vector from the ideal direction decreases.

Lemma 5.

At iteration in GLM-tron, suppose , then if , then

Proof.

We have

| (12) |

Consider the first term above,

Using the fact that is non-decreasing and -Lipschitz (for the first term) and and , we can lower bound this by

| (13) |

For the second term in (12), we have

| (14) |

Using the fact that , and using Jensen’s inequality to show that

, and assuming , we get

| (15) |

Combining (13) and (15) in (12), we get

∎

The bound on for some now follows from Lemma 5. Let . Notice that for all are i.i.d. -mean random variables with norm bounded by , so using Lemma 2, . Now using Lemma 5, at each iteration of algorithm GLM-tron, either , or . If the latter is the case, we are done. If not, since , and , there can be at most iterations before . Overall, there is some such that

In addition, we can reduce this to a high-probability bound on using Lemma 4, which is applicable since . Using a union bound, we get a bound which holds simultaneously for and .

Appendix B Proof of Proposition 1

To prove the proposition, we actually prove a more general result. Define the function class

and

where is possibly infinite (for instance, if we are using kernels).

It is easy to see that the proposition follows from the following uniform convergence guarantee:

Theorem 3.

With probability at least , for any fixed , if we let

and define

then

To prove the theorem, we use the concept of (-norm) covering numbers. Given a function class on some domain and some , we define to be the smallest size of a covering set , such that for any , there exists some for which . In addition, we use a more refined notion of an -norm covering number, which deals with an empirical sample of size . Formally, define to be the smallest integer , such that for any , one can construct a covering set of size at most , such that for any , there exists some such that .

Lemma 6.

Assuming , we have the following covering number bounds:

-

1.

.

-

2.

.

-

3.

.

-

4.

Proof.

We start with the first bound. Discretize to a

two-dimensional grid

. It is easily verified that for any function , we can define a piecewise linear function , which passes through points in the grid, and in between the points, is either constant or linear with slope 1, and . Moreover, all such functions are parameterized by their value at , and whether they are sloping up or constant at any grid interval afterwards. Thus, their number can be coarsely upper bounded as .

The second bound in the lemma is a well known fact - see for instance pg. 63 in [Pis99]).

The third bound in the lemma follows from combining the first two bounds, and using the Lipschitz property of (we simply combine the two covers at an scale, which leads to a cover at scale for ).

To get the fourth bound, we note that by corollary 3 in [Zha02b]. . Note that unlike the second bound in the lemma, this bound is dimension-free, but has worse dependence on and . Also, we have by definition of covering numbers and the first bound in the lemma. Combining these two bounds, and using the Lipschitz property of , we get

Upper bounding by , the the fourth bound in the lemma follows. ∎

Lemma 7.

With probability at least over a sample the following bounds hold simultaneously for any ,

Proof.

Lemma 6 tells us that . It is easy to verify that the same covering number bound holds for the function classes and , by definition of the covering number and since the loss function is -Lipschitz. In a similar manner, one can show that the covering number of the function class is at most .

Now, one just need to use results from the literature which provides uniform convergence bounds given a covering number on the function class. In particular, combining a uniform convergence bound in terms of the Rademacher complexity of the function class (e.g. Theorem 8 in [BM02]), and a bound on the Rademacher complexity in terms of the covering number, using an entropy integral (e.g., Lemma A.3 in [SST10]), gives the desired result. ∎

Lemma 8.

With probability at least over a sample , the following holds simultaneously for any : if we let

denote the empirical risk minimizer with that fixed , then

Proof.

For generic losses and function classes, standard bounds on the the excess error typically scale as . However, we can utilize the fact that we are dealing with the squared loss to get better rates. In particular, using Theorem 4.2 in [Men02], as well as the bound on from Lemma 6, we get that for any fixed , with probability at least ,

To get a statement which holds simultaneously for any , we apply a union bound over a covering set of . In particular, by Lemma 6, we know that we can cover by a set of size at most , such that any element in is at most -far (in an -norm sense) from some . So applying a union bound over , we get that with probability at least , it holds simultaneously for any that

| (16) |

Now, for any , if we let denote the closest element in , then and are -close uniformly for any and any . From this, it is easy to see that we can extend (16) to hold for any , with an additional element in the right hand side. In other words, with probability at least , it holds simultaneously for any that

Picking (say) provides the required result. ∎

Lemma 9.

Let be a convex class of functions, and let . Suppose that . Then for any , it holds that

Proof.

It is easily verified that

| (17) |

This implies that .

Consider the Hilbert space of square-integrable functions, with respect to the measure induced by the distribution on (i.e., the inner product is defined as ). Note that is a member of that space. Viewing as a function , what we need to show is that

By expanding, it can be verified that this is equivalent to showing

To prove this, we start by noticing that according to (17), minimizes over . Therefore, for any and any ,

| (18) |

as by convexity of . However, the right hand side of (18) equals

so to ensure (18) is positive for any , we must have . This gives us the required result, and establishes the first inequality in the lemma statement. The second inequality is just by convexity of the squared function. ∎

Proof of Thm. 3.

We bound in two different ways, one which is dimension-dependent and one which is dimension independent.

We begin with the dimension-dependent bound. For any fixed , let be . We have from Lemma 8 that with probability at least , simultaneously for all ,

and by Lemma 9, this implies

| (19) |

Now, we note that since , then as well. Again applying Lemma 8 and Lemma 9 in a similar manner, but now with respect to , we get that with probability at least , simultaneously for all ,

| (20) |

Combining (19) and (20), with a union bound, we have

Finally, we invoke the last inequality in Lemma 7, using a union bound, to get

We now turn to the dimension-independent bound. In this case, the covering number bounds are different, and we do not know how to prove an analogue to Lemma 8 (with rate faster than ). This leads to a somewhat worse bound in terms of the dependence on .

As before, for any fixed , we let be . Lemma 7 tells us that the empirical risk is concentrated around its expectation uniformly for any . In particular,

as well as

but since was chosen to be the empirical risk minimizer, it follows that

so by Lemma 9,

| (21) |

Now, it is not hard to see that if , then as well. Again invoking Lemma 7, and making similar arguments, it follows that

| (22) |

Combining (21) and (22), we get

We now invoke Lemma 7 to get

| (23) |

∎