Limit theorems for power variations of pure-jump processes with application to activity estimation

Abstract

This paper derives the asymptotic behavior of realized power variation of pure-jump Itô semimartingales as the sampling frequency within a fixed interval increases to infinity. We prove convergence in probability and an associated central limit theorem for the realized power variation as a function of its power. We apply the limit theorems to propose an efficient adaptive estimator for the activity of discretely-sampled Itô semimartingale over a fixed interval.

doi:

10.1214/10-AAP700keywords:

[class=AMS] .keywords:

.and

1 Introduction

Realized power variation of a discretely sampled process can be defined as the sum of the absolute values of the increments of the process raised to a given power. The leading case is when the power is , which corresponds to the realized variance that is widely used in finance. It is well known that under very weak conditions (see, e.g., JS ) the realized variance converges to the quadratic variation of the process as the sampling frequency increases. Powers other than have also been used as a way to measure variation of the process over a given interval in time as well as for estimation in parametric or semiparametric settings. Recently, Ait-Sahalia and Jacod SJ06 have used the realized power variation as a way to test for presence of jumps on a given path and JT07 have used it to test for common arrival of jumps in a multivariate context.

The limiting behavior of the realized power variation has been studied in the continuous semimartingale case in BNS03 and BNGJPS05 . Some of these results are extended by BNSW05 to situations when jumps are present but only when they have no asymptotic effect on the behavior of the realized power variation. A comprehensive study of the limiting behavior of the realized power variation when the observed process is a continuous semimartingale plus possible jumps is contained in J06b . This work includes also cases when jumps affect the limit of the realized power variation.

A common feature of the above cited papers is that the observed process always contains a continuous martingale. At the same time there are different applications, for example, for modeling internet traffic TT07 or volume of trades ACD08 and asset volatility TT08 , where pure-jump semimartingales, that is, semimartingales without a continuous martingale and nontrivial quadratic variation, seem to be more appropriate. Parametric models of pure-jump type for financial prices and/or volatility have been proposed in BNS01 , COGARCH , CGMY03 , among others. The main goal of this paper is to derive the limit behavior of the realized power variation of pure-jump semimartingales.

Some work has already been done in this direction. When the power exceeds the (generalized) Blumenthar–Getoor index of the jump process, it follows from Lepingle and J06b that the (unscaled) realized power variation converges almost surely to the sum of jumps raised to the corresponding power, which in general is not predictable (JS , Definition I.2.1) although the exact rate of this convergence is not known.

The limiting behavior of the realized power variation when the power is less than the Blumenthal–Getoor index is not known in general (apart from the fact that it explodes). Here we concentrate precisely on this case. We make an assumption of locally stable behavior of the Lévy measure of the jump process. That is we assume that the Lévy measure behaves like that of a stable process around zero, while its behavior for the “big” jumps is left unrestricted. This assumption allows us to derive the asymptotic behavior of the realized power variation in this case. Unlike the case when the power exceeds the Blumenthal–Getoor index, here the realized power variation needs to be scaled down by a factor determined by the Blumenthal–Getoor index and its limit is an integral of a predictable process. The latter is a direct measure for the stochastic volatility of the discretely-observed process, which is of key interest for financial applications. Thus the realized power variation for powers less than the Blumenthal–Getoor index contains information for the value of this index as well as the underlying stochastic volatility, and hence the importance of the limit results for this range of powers that are derived here. Finally, in earlier work Woerner03 , Woerner , Woerner07 , some limit theorems for realized power variations for pure-jump processes were studied, but the results apply in somewhat limiting situations regarding time-dependence and presence of a drift term (i.e., an absolutely continuous process), both of which are very important characteristics of financial data.

A distinctive feature of this paper is that the convergence results for the realized power variation are derived on the space of functions of the power equipped with the uniform topology. In contrast, all previous work has characterized the limiting behavior for a fixed power. The uniform convergence is important when one needs to use an infinite number of powers in estimation or the power of the realized power variation needs first to be estimated itself from the data. Such a case is illustrated in an application of the limit theorems derived in the paper.

Our application is for the estimation of the activity level of a discretely observed process. The latter is the smallest power for which the realized power variation does not explode (formally the infimum). In the case of a pure-jump process the activity level is just the Blumenthal–Getoor index of the jumps and when a continuous martingale is present it takes its highest value of . Apart from the importance of the Blumenthal–Getoor index in itself, the activity level provides information on the type of the underlying process (e.g., whether it contains a continuous martingale or not). The latter determines the appropriate scaling factor of the realized power variation in estimating integrated volatility measures.

We use the realized power variation computed over two different frequencies to estimate the activity level. The choice of the power is critical as it affects both efficiency and robustness. We develop an adaptive estimation strategy using our limit results. In a first step we construct an initial consistent estimator of the activity, and then, based on the first step estimator, we choose the optimal power to estimate the activity on the second step.

The paper is organized as follows. Section 2 presents the theoretical setup. Section 3 derives convergence in probability and associated central limit theorems for the appropriately scaled realized power variation. Section 4 applies the limit results of Section 3 to propose an efficient adaptive estimator of the activity of a discretely sampled process. Section 5 contains a short Monte Carlo study of the behavior of the estimator. Proofs are given in Section 6.

2 Theoretical setup

The theoretical setup of the paper is as follows. We will assume that we have discrete observations of some one-dimensional process, which we will always denote with . The process will be defined on some filtered probability space with denoting the filtration. We will restrict attention to the class of Itô semimartingales, that is, semimartingales with absolutely continuous characteristics (see, e.g., JS ).

Throughout we will fix the time interval to be , and we will suppose that we observe the process at the equidistant times , where . The asymptotic results in this paper will be of fill-in type, that is, we will be interested in the case when for a fixed .

The activity of the jumps in is measured by the so-called (generalized) Blumenthal–Getoor index. All of our limiting results for the realized power variation will depend in an essential way on it. The index is defined as

| (1) |

where . The index was originally defined in BG61 only for pure-jump Lévy processes. The definition in (1) extends it to an arbitrary jump semimartingale and was proposed in SJ07 . We recall the following well-known facts: (1) the index takes its values in ; (2) it depends on the particular realization of the process on the given interval; (3) the value of for the index separates finite from infinite variation jump processes.

Finally, we define the main object of our study, the realized power variation. It is constructed from the discrete observations of the process as

| (2) |

where . Our main focus will be the behavior of when is pure-jump semimartingale and we will restrict further attention to the case when the power is below the Blumenthal–Getoor index and the drift term has no asymptotic effect.

3 Limit theorems for power variation

We start with deriving the asymptotic limit of the appropriately scaled realized power variation and then proceed with a central limit theorem associated with it. To ease exposition we first present the results in the Lévy case and then generalize to the case when is a semimartingales with time-varying characteristics. For completeness we state corresponding results in the case when is a continuous martingale (plus jumps) as well.

3.1 Convergence in probability results

The convergence in probability results have been already derived in BNS03 , BNGJPS05 , J06b , Woerner , Woerner03 , TT07 among others with various degrees of generality. We briefly summarize them here as a starting point of our analysis. We first introduce some notation that will be used throughout. We set , where is a random variable with a standard stable distribution with index if [i.e., with characteristic function ], and with standard normal distribution if (i.e., normal with mean 0 and variance 1). Further, , where and are two independent random variables whose distribution is standard stable with index if and is standard normal if . Finally, we denote for and .

Throughout, will denote a continuous truncation function, that is, a continuous function with bounded support such that around the origin, and .

3.1.1 The Lévy case

Theorem 3.1

(a) Suppose is given by

| (3) |

where and are constants, and is a standard Brownian motion; is a homogenous Poisson measure with compensator . Denote with the Blumenthal–Getoor index of the jumps in . Then, if and for a fixed , we have

| (4) |

locally uniformly in .

(b) Suppose is given by

| (5) |

where is some constant; is a Poisson measure with compensator where

| (6) |

with

| (7) |

for some , and ; and . Assume that if . Then for a fixed , we have

| (8) |

locally uniformly in .

Remark 3.1.

The crucial assumption in the pure-jump case is the decomposition of the Lévy measure in (6). This assumption implies that locally the process behaves like the stable, that is, the very small jumps of the process are as if from a stable process. This assumption allows to scale the realized power variation using the Blumenthal–Getoor index . We note that is not necessarily a Lévy measure (since it can be negative) and thus (7) does not allow to represent (in distribution) as a sum of two independent jump processes, the first being the stable and the second with Blumenthal–Getoor index of .

Remark 3.2.

If jumps are of finite variation, in part (b) of the theorem we restrict to be equal to the sum of the jumps on the interval. The reason for this is that if a drift term is present (or equivalently a compensator for the small jumps), then it “dominates” the jumps and determines the behavior of the realized power variation (see, e.g., J06b ).

Remark 3.3.

When in the pure-jump case the limit of the realized power variation is just the some of the th absolute power of the jumps, and this result does not follow from a law of large numbers but rather by proving that an approximation error for this sum vanishes almost surely. Thus the behavior of the realized power variation for and is fundamentally different. The case is the dividing one. In this case the realized power variation (unscaled) converges neither to a constant nor to the sum of the absolute values of the jumps raised to the power (which is infinite). It can be shown that after subtracting the “big” increments, that is, keeping only those for which , for an arbitrary constant , the realized power variation converges to a nonrandom constant.

We note that the behavior of the realized power variation for in the pure-jump case is very different from the case when does not contain jumps. In the latter case for all powers the limit of the realized power variation is determined by law of large numbers, and hence we always need to scale the realized power variation in order to converge to a nondegenerate limit (see, e.g., BNGJPS05 ).

3.1.2 Extension to general semimartingales

Now we extend Theorem 3.1 to the case when and (and the drift terms and ) in (3) and (5) are stochastic. Nothing fundamentally changes, apart from the fact that the limits are now random (depending on the particular realization of the process ). In the case of continuous martingale plus jumps, we can substitute (3) with the following:

where is locally bounded and is a process with càdlàg paths; in addition and for every almost surely; is a homogenous Poisson measure with compensator and is a predictable function satisfying

| the process is locally bounded with | |||

| for some nonrandom function | (10) | ||

| and some constant . |

Additionally we assume that is an Itô semimartingale satisfying equations similar to (3.1.2) and (3.1.2) (with arbitrary driving Brownian motion and Poisson measure (and jump size function) satisfying a condition as (3.1.2) with ) with locally bounded coefficients. We note that the generalized Blumenthal–Getoor index of the jumps of in (3.1.2) is bounded by the nonrandom .

In the pure-jump case more care is needed in introducing time variation. Essentially we should keep the behavior around of the jump compensator intact. Therefore the generalization of (5) that we consider is given by

| (11) |

where and are processes with càdlàg paths; is a jump measure with compensator where is given by (6). We note that under this specification, the generalized Blumenthal–Getoor index of in (11) equals on every path, where is the constant appearing in (7). Further we assume and for every almost surely and impose the following dynamics for the process :

where is a Brownian motion; is a homogenous Poisson measure on with compensator for denoting some -finite measure on , satisfying for any with ; is an -valued predictable function satisfying

| the process is locally bounded with | |||

| for some nonrandom function | (13) | ||

| on , , where is the constant in (7), and for . |

Additionally we assume that and are Itô semimartingales satisfying equations similar to (3.1.2) and (3.1.2) (with arbitrary driving Brownian motion and Poisson measure) with locally bounded coefficients. This specification for is fairly general and it importantly allows for dependence between the driving jump measure in (11) and , which is important for financial applications (see, e.g., the COGARCH model of COGARCH ).

The restrictions on and in (3.1.2) and (3.1.2) are stronger than needed for the convergence in probability results in the next theorem, but they will be used for deriving the central limit results in the next subsection. These assumptions are nevertheless weak and therefore we impose them throughout. For example, the Itô semimartingale restrictions on and and their coefficients, together with conditions (3.1.2) and (3.1.2), will be automatically satisfied if solves

| (14) |

for some twice continuously differentiable function with at most linear growth and being the Lévy process in (3) or (5) (see, e.g., Remark 2.1 in J06b ). The next theorem states the general result on convergence in probability of realized power variation.

Theorem 3.2

Remark 3.4.

As seen from the above theorem, in both cases the (scaled) realized power variation estimates an integrated volatility measure for , which is important for measuring volatility in financial applications. What is different in the two cases is the scaling factor that is used. The latter depends on the activity of that we formally define later in Section 4 and then estimate using the limit theorems of the current section.

3.2 CLT results

Since in our application we make use of the realized power variation over two frequencies, and , we derive a CLT for the vector . In the next and subsequent theorems will stand for convergence stable in law (see, e.g., JS for a definition for filtered probability spaces).

3.2.1 The Lévy case

As for the convergence in probability we start with the Lévy case. The result is given in the following theorem.

Theorem 3.3

(a) Suppose is given by the process in (3) with Blumenthal–Getoor index . Then, for a fixed and any such that , we have

| (17) |

where the convergence takes place in , the space of -valued continuous functions on equipped with the uniform topology; is a continuous centered Gaussian process, independent from the filtration on which is defined, with the following variance–covariance for some :

(b) Suppose is given by the process in (5), and (7) holds with . Then, for a fixed and any such that either (i) when or (ii) , and symmetric and , we have

| (18) | |||

where the convergence takes place in , the space of -valued continuous functions on equipped with the uniform topology; is a continuous centered Gaussian process, independent from the filtration on which is defined, with the following variance–covariance for some :

Remark 3.5.

The result in part (a) for a fixed has been already shown (see, e.g., BNGJPS05 and references therein). In the pure-jump case (5), the result in (3.3) for a fixed has been derived by Woerner03 but only in the case when there is no drift [i.e., only under condition (ii) in part (b) of Theorem 3.3] and a slightly more restrictive condition on the residual measure . The general treatment here is important for financial applications, as the presence of risk premium means theoretically that the dynamics of traded assets should contain a drift term. Allowing for a drift term is also important for applications to processes exhibiting strong mean reversion like asset volatilities and trading volumes (see, e.g., ACD08 ).

Remark 3.6.

Theorem 3.3 shows that the convergence of the scaled and centered power variation is uniform over . This result has not been shown before. The uniformity is important, for example, in adaptive estimation where the power of the realized power variation to be used needs to be estimated from the data. This is illustrated in our application in Section 4.

Remark 3.7.

Comparing Theorem 3.3 with Theorem 4.1 we see that both in parts (a) and (b) we have imposed the stricter restrictions,

[with for part (a)] and . The lower bound for is determined from the presence of a “less active” component in . The restriction comes from the presence of a drift term. We note that it is more restrictive the lower the is. In fact when , the presence of a drift term will slow down the rate of convergence of the scaled power variation, and therefore the limiting result in (3.3) will not hold. In contrast for high values of , is very weak and in the limiting case when [part (a) of the theorem] it is never binding. We can interpret the restrictions and similarly. They come from the presence in of a less active jump component with Blumenthal–Getoor index .

Also, the restriction , which in particular implies that the function is subadditive, is crucial for bounding the effect of the “residual” jump components in .

Remark 3.8.

We can also derive a central limit theorem when (and when there are no “residual” jump components). In this case pure-continuous and pure-jump martingales differ. While in the former case the rate of convergence continuous to be , in the latter the rate slows down. The precise result is the following:

Suppose is symmetric stable plus a drift, that is, the process in (5) with and further when . Set when and when . Then for a fixed we have

| (19) |

where is pure-jump Lévy process with Lévy density and zero drift with respect to the “truncation” function . This is an asymmetric stable process with index .

3.2.2 Extension to general semimartingales

We proceed with the analogue of Theorem 3.3 in the more general setup of Section 3.1.2. We state the case when only, since as seen from Theorem 3.3 and Remark 3.8, the case needs an assumption of zero drift, and this limits its usefulness for financial applications where the drift arises from the presence of risk premium.

Theorem 3.4

(a) Suppose is given by (3.1.2), and (3.1.2) is satisfied with . Then, for a fixed and any such that , we have

| (20) | |||

where the convergence takes place in , the space of -valued continuous functions on equipped with the uniform topology; is a continuous centered Gaussian process, independent from the filtration on which is defined, with the following variance–covariance for some :

(b) Suppose is given by (11)–(3.1.2) with and (7) holds with . Then, for a fixed and any such that , we have

| (21) | |||

where the convergence takes place in —the space of -valued continuous functions on equipped with the uniform topology; is a continuous centered Gaussian process, independent from the filtration on which is defined, with the following variance–covariance for some :

Part (a) of the theorem has been derived in BNGJPS05 , while part (b) is a new result. We note that compared with the Lévy case in part (b) of the theorem we have a slightly stronger restriction for , that is, cannot be arbitrarily small when is close to 2. This is of no practical concern as the very low powers are not very attractive because of the high associated asymptotic variance. This is further discussed in Section 4.

4 Application: Adaptive estimation of activity

We proceed with an application of our limit results. We first define our object of interest, the activity level of the discretely-observed process, and show how the realized power variation can be used for its inference. Following that we develop an adaptive strategy for its estimation.

4.1 Definitions

We define the activity level of an Itô semimartingale as the smallest power for which the realized power variation does not explode, that is,

| (22) |

takes values in and is defined pathwise. It is determined by the most active component in and the order of the different components forming the Itô semimartingale from least to most active is: finite activity jumps, jumps of finite variation, drift (absolutely continuous process), infinite variation jumps, continuous martingale. When the dominating component of is its jump part (and only then), coincides with the generalized Blumenthal–Getoor index. Thus, for in (3.1.2), , and for in (11) and (3.1.2), . We note that determines uniquely the appropriate scale for the realized power variation in the estimation of the integrated volatility measures of the process (see Theorems 3.1 and 3.2).

When the process is observed discretely, is unknown and our goal is to derive an estimator for it. Since the scaling of the realized power variation depends on the activity level, we can identify the latter by taking a ratio of the realized power variation over two scales. Therefore our estimation will be based on the following function of the power:

| (23) |

A two-scale approach for related problems has been previously used also in ZMA05 , SJ07 , TT07 .

4.2 Limit behavior of

For ease of exposition here we restrict attention to the Lévy case. The extension to the general semimartingales in (3.1.2), (11) and (3.1.2) follows from an easy application of Theorem 3.4. In what follows, for any and both in we denote

Corollary 4.1

(a) Suppose is given by (3). Then for a fixed and any we have

| (25) |

where is a centered Gaussian process on with for some and independent from the filtration on which is defined, provided and , where is the Blumenthal–Getoor index of .

As seen from the corollary, will estimate the activity level only for powers that are below the activity level, which of course is unknown. Corollary 4.1 shows further that the power is also crucial for the rate at which the activity level is estimated. The range of values of for which is -consistent for defined in (22) depends on the activity of the most active part of the process, but also on the activity of the less active parts, that is, in part (a) and in part (b). For example, when the observed process is a continuous martingale plus jumps [part (a) of the corollary], then the activity of the jumps needs to be sufficiently low in order to estimate at a rate . Similar observation holds for the pure-jump case as well. The activity of the less active components of is unknown but we want an estimator of that is robust, in the sense that it has rate of convergence for most values of . Based on the corollary, this means that we need to use values of that are “sufficiently” close to half of the activity level .

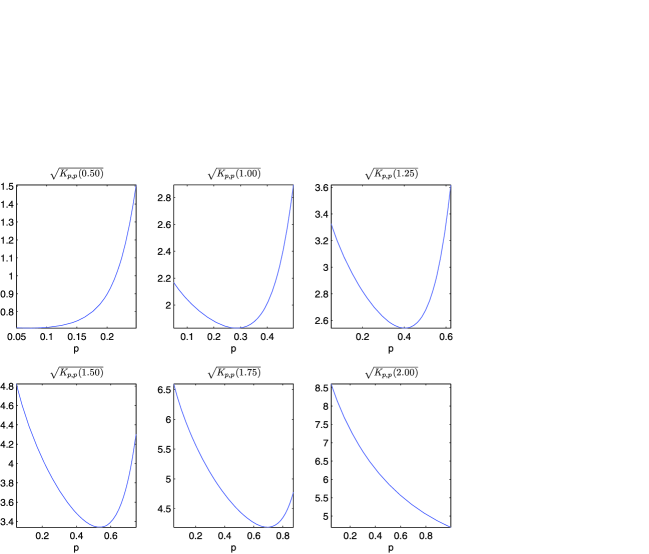

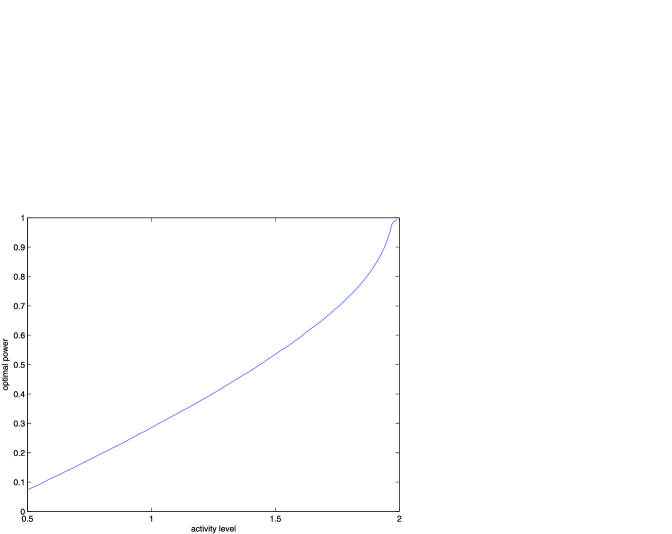

The presence of a less active component in the observed process aside, the power at which is evaluated is also important for the rate of convergence and the asymptotic variance of the estimation of the overall activity index. There is a difference between case (a) and case (b) in this regard. When the activity level of is (and there are no jumps), will be -consistent for any power. In contrast, in the pure-jump case, this will be true only for powers less than . Using powers slows down the rate of convergence from to , as pointed out in Remark 3.8. In Figure 1 we plotted the asymptotic standard deviation of for different values of the activity index . For activity less than the asymptotic variance has a pronounced U-shape pattern, and as a result it is minimized somewhere within the admissible range (for -rate of convergence), but the minimizing power depends on . On the other hand, when , i.e. when continuous martingale is present, the asymptotic variance is minimized for ( is admissible if ), although changes very little around . These observations are further confirmed from Figure 2, which plots the power at which the asymptotic variance is minimized as a function of the activity level.

Remark 4.1.

We note that in Corollary 4.1 (and in fact throughout the paper) we kept fixed. What happens if goes to infinity? In this case the result in Corollary 4.1 will remain valid without any assumption on the relative speed of and but only in the case when is symmetric stable. In all other cases captured by the specification in (5) we will need to impose a restriction on the relative speed with which increases. This happens because the error in estimating depends on and cannot vanish by just increasing the time span .

4.3 Two-step estimation of activity

We turn now to the explicit construction of an estimator of the activity level guided by the results of Corollary 4.1. Our goal here is to derive a point estimator of the activity level which has good robustness and efficiency properties. As we noted in the previous subsection, the powers used in the construction of an estimator for the activity level are crucial for its consistency, rate of convergence and asymptotic efficiency. Importantly, whether to use a given power in the estimation depends on the value of which is unknown and is itself being estimated.

This suggests implementing an adaptive (two-stage) estimation procedure, where on a first stage we construct an initial consistent estimator of the activity. Any estimator with arbitrary rate of convergence on this first stage can be used; the only requirement is that it is consistent. Then, on a second stage, we can use the first-stage estimator to select the power(s) at which is evaluated. This can be done because the convergence in (25) and (26) is uniform in . We give the generic construction of the two-stage estimator in the Lévy case in the following theorem.

Theorem 4.1

Fix some and suppose is given either by (3) or (5) with activity level defined in (22). Let be an arbitrary consistent estimator of constructed from , that is, we have as . Suppose the functions and are continuously differentiable in in a neighborhood of and we have identically . Set

Finally, denote

| (27) |

where is some weighting function, which is either continuous on or Dirac mass at some point in and such that . Then we have

| (28) |

where is standard normal defined on an extension of the original probability space provided:

-

[(b)]

-

(a)

if is given by (3), then and the Blumenthal–Getoor index of the jumps in , , is such that (which implies ),

- (b)

The two-step estimator can be viewed as a weighted average of over an adaptively selected region of powers. This range is determined on the basis of an initial consistent estimator of the activity. The averaging of the powers on the second stage might be beneficial since the correlation between the centered evaluated over different powers is not perfect. We would expect that the biggest benefit from averaging different powers in the estimation will come from using powers that are sufficiently apart. However, as we saw from Figure 1, significantly different powers would imply that at least one of them is associated with too high asymptotic variance and this could offset the benefit from the averaging. Therefore, in practice on the second stage one can just evaluate at a single power. This case is stated in the next corollary.

Corollary 4.2

Let be an arbitrary consistent estimator of constructed from , that is, we have as . Set

| (29) |

where is some continuous function and further we set . Then we have for a fixed

| (30) |

for being standard normal, provided and for as in Theorem 4.1 we have:

A natural choice for the function , that is, the power that is used on the second stage, will be the one that minimizes the asymptotic variance . This is further discussed in the numerical implementation in the next section. Alternatively, one can sacrifice some of the efficiency in exchange for robustness to a wider range of by picking power closer to . We finish this section with stating the equivalent of Corollary 4.2 in the case when is a semimartingale with time-varying characteristics. The theorem gives also feasible estimates of the asymptotic variance of the two-step estimator.

Theorem 4.2

Suppose and are given by (29) for some fixed .

(a) If is given by (3.1.2) and (3.1.2) is satisfied with , then we have

| (31) |

where is standard normal and is defined on an extension of the original probability space.

Remark 4.2.

Although the choice of the first-step estimator does not affect the first-order asymptotic properties of the two-stage estimator, in practice it can matter a lot. One possible choice for a first-step estimator of the activity is

| (34) |

where and is an arbitrary constant. It is easy to show that under the assumptions of Theorem 3.4, is a consistent estimator for . Another alternative first step estimator is evaluated at some small power. The latter will be a consistent estimator only if we know apriori that the true value of is higher than some positive number.

5 Numerical implementation

In this section we test on simulated data the limit results of Section 3. We do this by investigating the finite sample performance of the activity estimator of Section 4. In our Monte Carlo study we work with the following model for :

| (35) |

where the jumps of are with either of the following two compensators:

| (36) |

The first compensator is that of a tempered stable CGMY02 , Ro04 whose Blumenthal–Getoor index is the parameter and the second compensator is of a compound Poisson (which has of course a Blumenthal–Getoor index of ). Note that for the tempered stable process the value of in (7) is equal to . Therefore, the assumption in Theorems 3.3 and 3.4 will always be satisfied.

| Case | Jump specification | ||

|---|---|---|---|

| A | 0.0 | 1.0 | Tempered stable with , and |

| B | 0.0 | 1.0 | Tempered stable with , and |

| C | 0.8 | 0.0 | None |

| D | 0.8 | 1.0 | Rare-jump with , |

In Table 1 we listed the four different cases we consider in the Monte Carlo. The first two correspond to pure-jump processes with two different values of the level of activity. The last two cases correspond to a setting where a Brownian motion is present and therefore overall activity of is . In Case D the jumps in addition to the Brownian motion have share in the total variation of on a given interval, which is consistent with empirical findings for financial price data.

If we think of a unit of time being a day, then in our Monte Carlo on each “day” we sample times. This corresponds to approximately every minute for hours trading day and every minutes for hours trading day. The activity estimation is performed over days, that is, we set . This corresponds to calendar month of financial data. This Monte Carlo setup is representative of a typical financial application that we have in mind. We do not report results for other choices of and although we experimented with. Quite intuitively, an increase led to a reduction in the variance of the estimators, while an increase in led to the elimination of any existing biases. Finally, we consider number of Monte Carlo replications.

Following our discussion in Section 4.3 we calculate over each simulation the following two-step estimator . In the first stage we evaluate the function at . This yields an initial consistent, albeit far from efficient, estimator for the activity, provided of course the activity is above . Then, given our first step estimator of the activity, we compute the power at which is minimized [recall the definition of in (4.2)]. Our two-stage estimator is simply the value of at this optimal power.

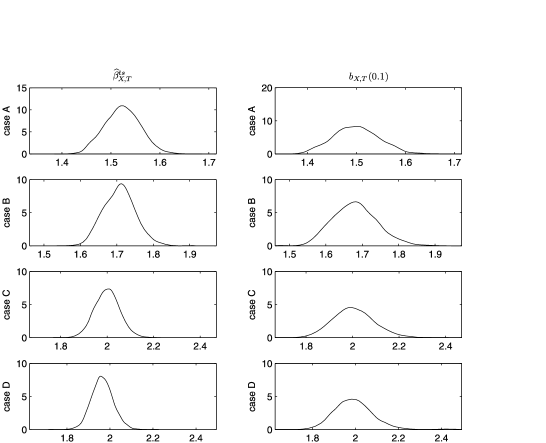

In the Monte Carlo we compare the performance of our estimator with an ad-hoc one where we simply evaluate at the fixed “low” power . In Figure 3 we plot the histograms of the two estimators and . As we can see from this figure, the adaptive estimation of the activity clearly outperforms the ad-hoc one based on a fixed power. In all cases is much more concentrated around the true value. This is further confirmed from Table 2, which reports summary statistics for the two estimators. The interquartile range for the ad-hoc estimator is from to wider than that of the adaptive estimator. A similar conclusion holds also for the mean absolute deviation reported in the last column of the table. Thus, we can conclude that choosing an “optimal” power can lead to nontrivial improvements in the estimation of the activity, which is consistent with our theoretical findings in Section 4.2.

=240pt Summary statistics Estimator Median IQR MAD Case A 1.50 1.5237 0.0495 0.0247 1.50 1.4985 0.0632 0.0316 Case B 1.75 1.7075 0.0590 0.0294 1.75 1.6785 0.0814 0.0407 Case C 2.00 2.0001 0.0719 0.0359 2.00 2.0005 0.1176 0.0588 Case D 2.00 1.9632 0.0664 0.0332 2.00 1.9865 0.1164 0.0573 \tabnotetext[]tt1Note: IQR is the inter-quartile range, and MAD is the mean absolute deviation.

We next investigate how well we can apply the feasible CLT for the two-step activity estimator. For each estimated we calculate standard errors using (33). Table 3 provides summary statistics for how well these estimated asymptotic standard errors track the exact finite-sample standard error of the two-step estimator . Since is simulated from a Lévy process, the latter is computed as the standard error of over the Monte Carlo replications.

=245pt Summary statistics for Median IQR MAD Case A 3.3341 3.2774 0.2005 0.1005 Case B 4.0320 3.8366 0.2638 0.1320 Case C 4.9588 4.6678 0.2609 0.0590 Case D 4.6626 4.7929 0.4596 0.2298 \tabnotetext[]tt1Notes: is the exact variance of the two-step estimator, computed from the Monte Carlo replications of the estimator. is the estimated asymptotic standard error using (33). MAD is computed around the exact standard error of the estimator .

6 Proofs

The proof of Theorems 3.1 and 3.2 follows from results in TT07 and therefore is omitted here. For the rest of the results, we first proof the ones for the Lévy case, and then proceed with those involving semimartingales with time-varying characteristics. In what follows we use and as a shorthand for and , respectively. In the proofs will denote a positive constant that does not depend on the sampling frequency and might change from line to line.

6.1 Proof of Theorem 3.3

The proof of the theorem consists of showing (1) finite-dimensional convergence (i.e., identifying the limit) and (2) tightness of the sequence. In the proof we will show part (b) only. Part (a) can be established in exactly the same way. We will assume that in (7) is that of a standard stable process and therefore . The result for an arbitrary then will follow trivially by rescaling (and centering). In what follows will stand for a standard symmetric -stable process, defined on some probability space which is possibly different from the original one.

Step 1 (Finite-dimensional convergence). We start with establishing the final-dimensional convergence. It will follow from Lemma 6.1 below in which we denote with the Hadamard product of two matrixes (i.e., the element-by-element product). The stated lemma is slightly stronger than what we need for two reasons. First, it contains locally uniform convergence in and in the theorem we work with a fixed . Second, in the lemma we will show the finite-dimensional convergence for a process defined in the following way:

| (37) |

where is the Poisson measure of Theorem 3.3; for arbitrary càdlàg processes and with and for some and a Brownian motion , is defined via for and further for . Obviously includes the Lévy case of Theorem 3.3, and the generalization will be needed later for the proof of Theorem 3.4.

Lemma 6.1

Let for some integer , and is vector of ones. Then, if is given by (37) and under the conditions of Theorem 3.3(b) (in particular all elements of are in ), we have the following convergence locally uniformly in t:

| (38) | |||||

and the -valued process is defined on an extension of the original probability space, is continuous, and conditionally on the -field of the original probability space is centered Gaussian with variance–covariance matrix process given by defined via

| (39) |

We start with some notation. We set when and for . We further denote

| (40) |

and

First, we have

using the algebraic inequality for and the fact that for . Therefore we are left with showing (6.1) with and substituted with and , respectively.

For arbitrary power we set

It is convenient also to write further with

for . Using Theorem IX.7.19 in JS it suffices to show the following for all and arbitrary element from the vector :

| (43) |

| (44) | |||

where and ,

| (45) |

| (46) |

for being an arbitrary bounded local martingale defined on the original probability space.

We start with (43). We prove it for the first element of and arbitrary element of the vector , the proof for the second element of is similar. Because of the assumption on the Lévy measure in (6) we can write

for and where

with

where we recall that is a standard stable process which is defined on an extension of the original probability space and is independent of it. We have for , because of our assumption of the symmetry of and for this case. Also, by the assumptions of the theorem, and therefore the integral with respect to in the definition of is well defined. Then, using the algebraic inequality for and arbitrary and , it is easy to show that for we have

where is some constant and

| (48) |

The three processes are well defined because and are defined on an extension of the original probability space and independent from the original filtration. Then, using the fact that is independent from the processes for , for and any positive , the Hölder’s inequality, and the basic one for and arbitrary , we easily have

| (49) |

for any . Taking into account the restriction on and , we have for some . In a similar way we can show for some where

Further, since for , and using the self-similarity property of a strictly stable process, we have . We have similarly , where

because is independent from . Next, to prove (43), we need only show that for some . We show this only for the case , since for it is trivially satisfied. For the proof we make use of the following general inequality for arbitrary real numbers and and :

| (50) | |||

for some and a positive constant . The inequality follows by looking at the difference on the following two sets: and . On the former we apply a second-order Taylor series approximation and further use on this set [therefore (6.1) holds with ]. On the set we use the subadditivity of the function . We can substitute in the above inequality with and with . Then, by first conditioning on the filtration generated by , and then using the fact that has symmetric distribution, we get

| (51) |

Next we have for some (note that we have universal bounds on and )

| (52) |

where is the hitting time of the Brownian motion of the level for for some positive , whose negative powers (of ) are finite. Then for such that (recall the assumption on for ) we have

| (53) | |||

with some and a positive constant . This follows from the self-similarity of the strictly stable process, the fact that since (see, e.g., SATO ) and the preceding inequality (52). Similarly, for some using the Chebyshev’s inequality we have

with some . Combining (49)–(6.1) and using that stable distribution has a density with respect to Lebesgue measure (see, e.g., Remark 14.18 in SATO ) we prove for some and thus (43) follows. Similarly we have for some where

Before proceeding with (6.1) we derive a result that we make use of later for the proof of Theorem 3.4. First, for two random variables and and some we have

| (55) |

Then we can apply this inequality twice, use the fact that for any , the fact that ; the fact that the stable distribution has finite moments for powers that are negative but higher than ; the bound in (52) and finally the Chebyshev’s inequality to get

for any , and and where is some positive constant that does not depend on . Similarly for two random variables and and and we can derive

for any and where the constant depends on only. Using this inequality then it is easy to derive the following bound:

| (57) | |||

for any and where the constant does not depend on .

We continue with (6.1). First using Lemma 1(b) in TT07 , since for each element of the vector we have , we have [recall the notation in (40) and (6.1)]

where and for the first limit while for the last two . Next, by Riemann integrability, we have

| (58) |

Therefore, to show (39) we need only to prove that for arbitrary

| (59) |

for some . But this follows by using the Burkholder–Davis–Gundy inequality (if ) and the elementary one for arbitrary reals and some , together with the definition of the process .

Turning to (45), we show it only for the first component of , the proof for the second one being exactly the same. Using again Lemma 1(b) in TT07 we have

| (60) | |||

for and . Then (45) follows by combining this result with (58)–(59). We are left with proving (46). It suffices to show

| (61) | |||

First, if is a discontinuous martingale, then using (43)–(45), we have that is C-tight, that is, it is tight and any limit is continuous. At the same time trivially converges to a discontinuous limit. Therefore the pair is tight (see JS , Theorem VI3.33(b)). But then the left-hand side of (6.1) converges to the predictable version of the quadratic covariation of the limits of and (use Theorem VI.6.29 of JS for this), which is zero since continuous and discontinuous martingales are orthogonal (see JS , Proposition I.4.15).

Second if is a continuous martingale orthogonal to the Brownian motion used in defining , we can proceed similarly to BNGJPS05 and argue as follows. If we set for , then is a martingale. It remains also martingale, conditionally on , for the filtration generated by the Poisson measure and the Brownian motion since is uniquely determined by these processes. Therefore, by a martingale representation theorem (see JS , Theorem III.4.34)

when for an appropriate predictable function and process . Therefore is a sum of pure-discontinuous martingale, which hence is orthogonal to (see JS , Definition I.4.11), and a continuous martingale which is also orthogonal to because of our assumption on . This implies that for a continuous martingale orthogonal to the Brownian motion we have

and this shows (6.1) in this case.

The only case that remains to be covered is when . For this case we can use the bounds derived above for , and and from here (6.1) follows easily in this case.

Step 2 (Tightness). We are left with establishing tightness, which follows from the next lemma.

Lemma 6.2

We will prove only that the sequence

is tight in the space of -valued functions on and the arguments generalize to the tightness of . For arbitrary we can write

where

and for , with

where is defined in (6.1) in the proof of Lemma 6.1 and is a residual term whose moments involve the processes , and of (48). It can be shown using the continuity of the power function and the restriction on that

| (62) |

For we can first apply the inequality for , and then use the continuity of the power function for positive powers to show that

| (63) |

For we easily have for

| (64) |

and Theorem 12.3 in Billingsley implies tightness. Turning to , it is identically for due to our assumptions. So we look at the case . We can decompose as with

where and

For we can write

For the first expectation on the left-hand side of (6.1) we have, similarly to (64),

| (66) |

For the second expectation on the right-hand side of (6.1), we apply the following inequality, similarly to (6.1). For every and and we have

for some .

Substituting in the above inequality with and with and using the fact that is odd in , we get

for some . For we have for sufficiently small

Then using the definition of the set and the calculation in (6.1) we can conclude

| (67) |

Combining the above results we get the tightness of on the space of continuous functions of in the interval .

6.2 Proof of Remark 3.8

In what follows we denote

It is no restriction, of course, to assume that the constant in (7) corresponds to that of a standard stable, and we proceed in the proofs with that assumption. In view of Theorem XVII.2.2 in Feller71 we need to prove the following:

| (68) | |||||

| (69) | |||||

where is an arbitrary positive constant.

We recall that is symmetric stable process plus a drift, that is, , where denotes symmetric stable process with Lévy density equal to in (7) and when and when . Using the self-similarity of the symmetric stable we have .

First we state several basic facts about the stable distribution that we make use of in the proof. We recall that for the tail of the symmetric stable we have (see, e.g., Zolotarev86 ) as where for two functions and , means . Therefore the tail probability of the stable distribution varies regularly at infinity, and we can use this fact and Theorems 8.1.2 and 8.1.4 in Teugels87 to write for

| (72) |

as . We continue with the proof of (68)–(6.2). We start with showing (68). First we have

We note that the second term on the right-hand side of (6.2) is identically zero, while the convergence of the first term can be split into two cases. First, when the result follows from the bound for the term in (6.1) and (6.1) in the proof of Theorem 3.3, provided . When the convergence follows from a trivial application of the Taylor expansion.

Second using the rate of decay of the tail probability of the stable distribution we have

Third using a Taylor expansion around and the fact that we evaluate on a set growing to infinity at the rate , we have

Thus to prove (68) we need to show

But this follows from (6.2) with

and hence we are done. We turn now to (69). It is easy to show that

Therefore, (69) will follow if we can show

| (74) | |||

To show (6.2) we can apply (72) with

Finally, (6.2) follows trivially from the expression for the tail probability of a stable stated earlier.

6.3 Proof of Corollary 4.1

Again, as in the proof of Theorem 3.3 we will show only part (b), the proof of part (a) being identical. Since the process has no fixed time of discontinuity, the result of Lemma 6.1 implies that the convergence in (6.1) holds for an arbitrary fixed . Then, there is a set on which for and from Theorem 3.2 (under the conditions of this theorem) . On is a continuous transformation of and , and thus Lemma 6.1 implies the finite-dimensional convergence of the sequences on the left-hand sides of (25) and (26). Similarly, since tightness is preserved under continuous transformations, using Lemma 6.2 we have that the left-hand sides of (25) and (26) are tight. Hence the result of Theorem 4.1 follows.

6.4 Proof of Theorem 4.1

We first show the result for the case when is continuous on . Set

Since is continuous in a neighborhood of and as well as when is given by (3), then there are such that for all and . Similarly if is given by (5), then , and due to the assumptions of the theorem, there exist such that for and when and and when .

Denote with the subset of for which and are continuously differentiable. From the assumptions of Theorem 4.1 the set contains a neighborhood of . Then, using a Taylor expansion on the set where is the set defined in the proof of Corollary 4.1 above, we can write

where is between and and

The last term on the right-hand side of (6.4) is asymptotically negligible because is consistent for . We now show that the second term in (6.4) is asymptotically negligible. First note that since we also have . Then to establish the asymptotic negligibility it suffices to show that

| (76) |

where and . For any we have

The first probability in the second line of (76) is converging to as , while the second one converges to zero as . This is because when , and where are some constants that satisfy the conditions of Theorem 3.3, and as a consequence of this theorem converges uniformly in for .

We are left with the first term in (6.4). Using the uniform convergence result of Theorem 3.3, the fact that the integration over a bounded interval is continuous for the uniform metric on the space of continuous functions (in fact for this even finite dimensional convergence suffices) we have

where

and and are the first and second elements, respectively, of the limiting Gaussian process of part (a) and (b) of Theorem 3.3. The proof of Theorem 4.1 for the case of continuous then easily follows. The proof in the case of being Dirac mass at some point follows from the proof of Corollary 4.2 given below.

6.5 Proof of Corollary 4.2

Denote with the set of values of for which for some satisfying the conditions of Theorem 3.3 in the different cases for . Finally, set . We know that this set contains neighborhood of because of the continuity of and the fact that . Then we can write

where is between and and

The result of Corollary 4.2 then will follow if we can show that is bounded in probability on the set . But this holds true because we can prove exactly as in Theorem 3.3 that

converges uniformly in (under the same conditions for the power as in that theorem).

6.6 Proof of Theorem 3.4

We do not show here part (a). The finite-dimensional convergence for this case (without jumps in ) has been already shown in BNGJPS05 (extending their result to the case with jumps satisfying the conditions of Theorem 3.4, part(a) follows trivially using the subadditivity of for ). The tightness can be shown in exactly the same way as part (b) (i.e., in the decomposition in equation (8.2); in BNGJPS05 we can apply the same techniques as in the proof of our Lemma 6.2).

Proof of part(b) We will establish only the finite-dimensional convergence, the proof the tightness is done exactly as in Lemma 6.2. Also we will prove the finite-dimensional convergence for a fixed and the second element of the vector on the left-hand side in (3.4). The generalization will follow immediately.

As in the previous proofs we assume that in (7) corresponds to that of a standard stable. Upon using a localization argument as in J06b we can and will assume the following stronger assumption on the various processes in (11) and (3.1.2):

We have and for some positive constant which bounds also the coefficients in the Itô semimartingale representations of the processes and ; .

We can make the following decomposition:

| (77) | |||||

| (78) | |||||

where for and

We start with . We can apply directly Lemma 6.1 to show that converges stably to the limit on the right-hand side of (3.4) (recall our stronger assumption on the process stated at the beginning of the proof). We continue with the term which we now show is asymptotically negligible. First we denote the set

Then, using the exponential inequality for continuous martingales with bounded variation [see, e.g., RY ] it is easy to derive

Using a second-order Taylor expansion and the fact that is bounded from below on the set , we get

where we also made use of the following inequality:

Finally, a first-order Taylor expansion together with the fact that is bounded from below on the set gives

Combining the above two inequalities we get

This implies the asymptotic negligibility of . We continue with . We can use the standard inequality for as well as Hölder’s inequality to get

Similar inequalities as for on the set give

These two inequalities establish the asymptotic negligibility of . We continue with . First, for some denote the set . Then we can decompose into

where is a number between and and . Note that for sufficiently small is well defined because of the boundedness from below of .

Using the Burkholder–Davis–Gundy inequality, Hölder’s inequality, the assumption of Itô semimartingale for the process (due to which the leading term in is ) and the integrability condition for the dominating function of the jumps in , , in (3.1.2), we have for

| (79) |

for some constant that does not depend on . We will show that the three terms , and are asymptotically negligible. For and we make use of the fact that a sufficient condition for asymptotic negligibility of , where is -measurable, is (see Theorem VIII.2.27 of JS (or the first part of Lemma 4.1 in J07 )). Note that for we use the fact that is bounded by a constant on the set . For we can first make use of Doob’s inequality to show that for some constant that depends on . Then, since for some and constant , using Hölder’s inequality we have that is also asymptotically negligible. This proves the asymptotic negligibility of the term .

We are left with proving asymptotic negligibility of . We start with some preliminary results that we will make use of. We have for

| (80) |

where we made use of Hölder’s inequality and the fact that is an Itô semimartingale with bounded coefficients and therefore for . Similarly for and arbitrary

| (81) | |||

where we made use of Hölder’s inequality, the Burkholder–Davis–Gundy inequality (recall ) and (79).

Further, for some deterministic sequence denote

Then we can apply the result in (6.1) to get for any

| (82) |

Similarly using the same arguments as above and (6.1), we get for , some , and any

| (83) | |||

Finally, using (80) and (6.6), we get for any

| (84) |

We are now ready to prove the asymptotic negligibility of . We can make the following decomposition using a Taylor expansion on the set :

where is between and and recall . Then using the definition of the set we have . Therefore, using the definition of the function , it clearly suffices to show

for some . Setting for some , we can use the Hölder inequality to bound

Then using the bounds in (80), (6.6) and (6.6) we get

for some . Similarly for we can use Hölder’s inequality to get

Then using the bounds in (80), (6.6), (82) and (84) we get

for some . Finally, we can make use of the restrictions on and to pick for which (6.6) and (6.6) will be fulfilled.

6.7 Proof of Theorem 4.2

The proof follows directly from the fact that under the conditions of the theorem: (1) the functions and are continuous both in and ; (2) is consistent for ; (3) converges uniformly in (after scaling appropriately).

Acknowledgments

We would like to thank Per Mykland, Neil Shephard and particularly Jean Jacod for many helpful comments and suggestions. We also thank an anonymous referee for careful reading and constructive comments on the paper.

References

- (1) {barticle}[mr] \bauthor\bsnmAït-Sahalia, \bfnmYacine\binitsY. and \bauthor\bsnmJacod, \bfnmJean\binitsJ. (\byear2009). \btitleEstimating the degree of activity of jumps in high frequency data. \bjournalAnn. Statist. \bvolume37 \bpages2202–2244. \biddoi=10.1214/08-AOS640, mr=2543690 \endbibitem

- (2) {barticle}[mr] \bauthor\bsnmAït-Sahalia, \bfnmYacine\binitsY. and \bauthor\bsnmJacod, \bfnmJean\binitsJ. (\byear2009). \btitleTesting for jumps in a discretely observed process. \bjournalAnn. Statist. \bvolume37 \bpages184–222. \biddoi=10.1214/07-AOS568, mr=2488349 \endbibitem

- (3) {barticle}[mr] \bauthor\bsnmAndrews, \bfnmBeth\binitsB., \bauthor\bsnmCalder, \bfnmMatthew\binitsM. and \bauthor\bsnmDavis, \bfnmRichard A.\binitsR. A. (\byear2009). \btitleMaximum likelihood estimation for -stable autoregressive processes. \bjournalAnn. Statist. \bvolume37 \bpages1946–1982. \biddoi=10.1214/08-AOS632, mr=2533476 \endbibitem

- (4) {bincollection}[vtex] \bauthor\bsnmBarndorff-Nielsen, \bfnmOle E.\binitsO. E., \bauthor\bsnmGraversen, \bfnmSvend Erik\binitsS. E., \bauthor\bsnmJacod, \bfnmJean\binitsJ., \bauthor\bsnmPodolskij, \bfnmMark\binitsM. and \bauthor\bsnmShephard, \bfnmNeil\binitsN. (\byear2005). \btitleA central limit theorem for realised power and bipower variations of continuous semimartingales. In \bbooktitleFrom Stochastic Calculus to Mathematical Finance (Y. Kabanov and R. Lipster, eds.) \bpages33–68. \bpublisherSpringer, \baddressBerlin. \biddoi=10.1007/978-3-540-30788-4_3, mr=2233534 \endbibitem

- (5) {barticle}[vtex] \bauthor\bsnmBarndorff-Nielsen, \bfnmOle E.\binitsO. E. and \bauthor\bsnmShephard, \bfnmNeil\binitsN. (\byear2001). \btitleNon-Gaussian Ornstein–Uhlenbeck-based models and some of their uses in financial economics. \bjournalJ. R. Stat. Soc. Ser. B Stat. Methodol. \bvolume63 \bpages167–241. \biddoi=10.1111/1467-9868.00282, mr=1841412 \endbibitem

- (6) {barticle}[mr] \bauthor\bsnmBarndorff-Nielsen, \bfnmOle E.\binitsO. E. and \bauthor\bsnmShephard, \bfnmNeil\binitsN. (\byear2003). \btitleRealized power variation and stochastic volatility models. \bjournalBernoulli \bvolume9 \bpages243–265. \biddoi=10.3150/bj/1068128977, mr=1997029 \endbibitem

- (7) {barticle}[mr] \bauthor\bsnmBarndorff-Nielsen, \bfnmOle E.\binitsO. E., \bauthor\bsnmShephard, \bfnmNeil\binitsN. and \bauthor\bsnmWinkel, \bfnmMatthias\binitsM. (\byear2006). \btitleLimit theorems for multipower variation in the presence of jumps. \bjournalStochastic Process. Appl. \bvolume116 \bpages796–806. \biddoi=10.1016/j.spa.2006.01.007, mr=2218336 \endbibitem

- (8) {bbook}[mr] \bauthor\bsnmBillingsley, \bfnmPatrick\binitsP. (\byear1968). \btitleConvergence of Probability Measures. \bpublisherWiley, \baddressNew York. \bidmr=0233396 \endbibitem

- (9) {bbook}[mr] \bauthor\bsnmBingham, \bfnmN. H.\binitsN. H., \bauthor\bsnmGoldie, \bfnmC. M.\binitsC. M. and \bauthor\bsnmTeugels, \bfnmJ. L.\binitsJ. L. (\byear1987). \btitleRegular Variation. \bseriesEncyclopedia of Mathematics and Its Applications \bvolume27. \bpublisherCambridge Univ. Press, \baddressCambridge. \bidmr=898871 \endbibitem

- (10) {barticle}[mr] \bauthor\bsnmBlumenthal, \bfnmR. M.\binitsR. M. and \bauthor\bsnmGetoor, \bfnmR. K.\binitsR. K. (\byear1961). \btitleSample functions of stochastic processes with stationary independent increments. \bjournalJ. Math. Mech. \bvolume10 \bpages493–516. \bidmr=0123362 \endbibitem

- (11) {barticle}[vtex] \bauthor\bsnmCarr, \bfnmP.\binitsP., \bauthor\bsnmGeman, \bfnmH.\binitsH., \bauthor\bsnmMadan, \bfnmD.\binitsD. and \bauthor\bsnmYor, \bfnmM.\binitsM. (\byear2002). \btitleThe fine structure of asset returns: An empirical investigation. \bjournalJ. Business \bvolume75 \bpages305–332. \endbibitem

- (12) {barticle}[mr] \bauthor\bsnmCarr, \bfnmPeter\binitsP., \bauthor\bsnmGeman, \bfnmHélyette\binitsH., \bauthor\bsnmMadan, \bfnmDilip B.\binitsD. B. and \bauthor\bsnmYor, \bfnmMarc\binitsM. (\byear2003). \btitleStochastic volatility for Lévy processes. \bjournalMath. Finance \bvolume13 \bpages345–382. \biddoi=10.1111/1467-9965.00020, mr=1995283 \endbibitem

- (13) {bbook}[vtex] \bauthor\bsnmFeller, \bfnmWilliam\binitsW. (\byear1971). \btitleAn Introduction to Probability Theory and Its Applications. Vol. II, 2nd ed. \bpublisherWiley, \baddressNew York. \bidmr=0270403 \endbibitem

- (14) {barticle}[vtex] \bauthor\bsnmJacod, \bfnmJ.\binitsJ. (\byear2007). \btitleStatistics and high-frequency data. In \bjournalSemstat Course in La Manga, La Manga, Spain. \endbibitem

- (15) {barticle}[mr] \bauthor\bsnmJacod, \bfnmJean\binitsJ. (\byear2008). \btitleAsymptotic properties of realized power variations and related functionals of semimartingales. \bjournalStochastic Process. Appl. \bvolume118 \bpages517–559. \biddoi=10.1016/j.spa.2007.05.005, mr=2394762 \endbibitem

- (16) {bbook}[mr] \bauthor\bsnmJacod, \bfnmJean\binitsJ. and \bauthor\bsnmShiryaev, \bfnmAlbert N.\binitsA. N. (\byear2003). \btitleLimit Theorems for Stochastic Processes, \bedition2nd ed. \bseriesGrundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences] \bvolume288. \bpublisherSpringer, \baddressBerlin. \bidmr=1943877 \endbibitem

- (17) {barticle}[mr] \bauthor\bsnmJacod, \bfnmJean\binitsJ. and \bauthor\bsnmTodorov, \bfnmViktor\binitsV. (\byear2009). \btitleTesting for common arrivals of jumps for discretely observed multidimensional processes. \bjournalAnn. Statist. \bvolume37 \bpages1792–1838. \biddoi=10.1214/08-AOS624, mr=2533472 \endbibitem

- (18) {barticle}[mr] \bauthor\bsnmKlüppelberg, \bfnmClaudia\binitsC., \bauthor\bsnmLindner, \bfnmAlexander\binitsA. and \bauthor\bsnmMaller, \bfnmRoss\binitsR. (\byear2004). \btitleA continuous-time GARCH process driven by a Lévy process: Stationarity and second-order behaviour. \bjournalJ. Appl. Probab. \bvolume41 \bpages601–622. \bidmr=2074811 \endbibitem

- (19) {barticle}[mr] \bauthor\bsnmLépingle, \bfnmD.\binitsD. (\byear1976). \btitleLa variation d’ordre des semi-martingales. \bjournalZ. Wahrsch. Verw. Gebiete \bvolume36 \bpages295–316. \bidmr=0420837 \endbibitem

- (20) {bbook}[mr] \bauthor\bsnmRevuz, \bfnmDaniel\binitsD. and \bauthor\bsnmYor, \bfnmMarc\binitsM. (\byear1999). \btitleContinuous Martingales and Brownian Motion, \bedition3rd ed. \bseriesGrundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences] \bvolume293. \bpublisherSpringer, \baddressBerlin. \bidmr=1725357 \endbibitem

- (21) {barticle}[mr] \bauthor\bsnmRosiński, \bfnmJan\binitsJ. (\byear2007). \btitleTempering stable processes. \bjournalStochastic Process. Appl. \bvolume117 \bpages677–707. \biddoi=10.1016/j.spa.2006.10.003, mr=2327834 \endbibitem

- (22) {bbook}[vtex] \bauthor\bsnmSato, \bfnmK.\binitsK. (\byear1999). \btitleLévy Processes and Infinitely Divisible Distributions. \bpublisherCambridge Univ. Press. \endbibitem

- (23) {bmisc}[vtex] \bauthor\bsnmTodorov, \bfnmV.\binitsV. and \bauthor\bsnmTauchen, \bfnmG.\binitsV. (\byear2010). \btitleVolatility jumps. J. Bus. Econom. Statist. To appear. \endbibitem

- (24) {barticle}[mr] \bauthor\bsnmTodorov, \bfnmViktor\binitsV. and \bauthor\bsnmTauchen, \bfnmGeorge\binitsG. (\byear2010). \btitleActivity signature functions for high-frequency data analysis. \bjournalJ. Econometrics \bvolume154 \bpages125–138. \biddoi=10.1016/j.jeconom.2009.06.009, mr=2558956 \endbibitem

- (25) {bmisc}[vtex] \bauthor\bsnmWoerner, \bfnmJ.\binitsJ. (\byear2003). \btitlePurely Discontinuous Lévy Processes and power variation: Inference for the integrated volatility and the scale paramter. Working paper, Univ. Oxford. \endbibitem

- (26) {barticle}[mr] \bauthor\bsnmWoerner, \bfnmJeannette H. C.\binitsJ. H. C. (\byear2003). \btitleVariational sums and power variation: A unifying approach to model selection and estimation in semimartingale models. \bjournalStatist. Decisions \bvolume21 \bpages47–68. \biddoi=10.1524/stnd.21.1.47.20316, mr=1985651 \endbibitem

- (27) {barticle}[mr] \bauthor\bsnmWoerner, \bfnmJeannette H. C.\binitsJ. H. C. (\byear2007). \btitleInference in Lévy-type stochastic volatility models. \bjournalAdv. in Appl. Probab. \bvolume39 \bpages531–549. \biddoi=10.1239/aap/1183667622, mr=2343676 \endbibitem

- (28) {barticle}[mr] \bauthor\bsnmZhang, \bfnmLan\binitsL., \bauthor\bsnmMykland, \bfnmPer A.\binitsP. A. and \bauthor\bsnmAït-Sahalia, \bfnmYacine\binitsY. (\byear2005). \btitleA tale of two time scales: Determining integrated volatility with noisy high-frequency data. \bjournalJ. Amer. Statist. Assoc. \bvolume100 \bpages1394–1411. \biddoi=10.1198/016214505000000169, mr=2236450 \endbibitem

- (29) {bbook}[vtex] \bauthor\bsnmZolotarev, \bfnmV. M.\binitsV. M. (\byear1986). \btitleOne-dimensional Stable Distributions. \bseriesTranslations of Mathematical Monographs \bvolume65. \bpublisherAmer. Math. Soc., \baddressProvidence, RI. \bidmr=854867 \endbibitem