Theoretical Sensitivity Analysis for Quantitative Operational Risk Management ***Forthcoming in International Journal of Theoretical and Applied Finance.

This Version: May 24, 2017)

Abstract

We study the asymptotic behavior of the difference between

the values at risk and for

heavy-tailed random variables and with

for application in sensitivity analysis of quantitative operational risk management

within the framework of the advanced measurement approach of Basel II (and III).

Here describes the loss amount of the present risk profile

and describes the loss amount caused by an additional loss factor.

We obtain different types of results

according to the relative magnitudes of the thicknesses of the tails of and .

In particular, if the tail of is sufficiently thinner than that of , then

the difference between prior and posterior risk amounts

is asymptotically equivalent to

the expectation (expected loss) of .

Keywords: Sensitivity Analysis, Quantitative Operational Risk Management,

Regular Variation, Value at Risk

AMS Subject Classification: 60G70, 62G32, 91B30

1 Introduction

Value at risk (VaR) is a standard risk measure and is widely used in quantitative financial risk management. In this paper, we study the asymptotic behavior of VaRs for heavy-tailed random variables (loss variables). We focus on the asymptotic behavior of the difference between two VaRs of

| (1.1) |

with , where and are regularly varying random variables and denotes the confidence level of VaR. For our main result, we show that the behavior of () drastically changes according to the relative magnitudes of the thicknesses of the tails of and . Interestingly, when the tail of is sufficiently thinner than that of , is approximated by the expected loss (EL) of , that is, , .

This study is strongly related to quantitative operational risk management within the framework of the Basel Accords, which is a set of recommendations for regulations in the banking industry. Here, we briefly introduce the financial background.

Basel II (International Convergence of Capital Measurement and Capital Standards: A Revised Framework) was published in 2004, and in it, operational risk was added as a new risk category (see Basel Committee on Banking Supervision (2004) (BCBS) and [McNeil et al.(2005)] for the definition of operational risk). Beginning in 2013, the next accord, Basel III, was scheduled to be introduced in stages. Note that the quantitative method for measuring operational risk was not substantially changed in Basel III at this stage, so here we refer to mainly Basel II.

To measure the capital charge for operational risk, banks may choose among three approaches: the basic indicator approach, the standardized approach, and an advanced measurement approach. While the basic indicator approach and the standardized approach prescribe explicit formulas, the advanced measurement approach does not specify a model to quantify a risk amount (risk capital), and hence banks adopting this approach must construct their own quantitative risk model and verify it periodically ‡‡‡In 2016, BCBS is proposing to remove the advanced measurement approach from the regulatory framework (Pillar I) in the finalization of Basel III (also known as Basel IV). Needless to say, this examination does not mean that advanced methods for risk measurement are unnecessary. It is still important in practice to utilize internal models to improve risk profiles. See [BCBS(2014)], [BCBS(2016)], and [PwC Financial Services(2015)]..

[McNeil et al.(2005)] pointed out that although everyone agrees on the importance of understanding operational risk, controversy remains regarding how far one should (or can) quantify such risks. Because empirical studies have found that the distribution of operational loss has a fat tail (see [Moscadelli(2004)]), we should focus on capturing the tail of the loss distribution.

Basel II does not specify a measure of the risk but states that “a bank must be able to demonstrate that its approach captures potentially severe ‘tail’ loss events. Whatever approach is used, a bank must demonstrate that its operational risk measure meets a soundness standard comparable to that of the internal ratings-based approach for credit risk, (i.e., comparable to a one-year holding period and a percentile confidence interval)” in paragraph 667 of [BCBS(2004)]. A typical risk measure, which we adopt in this paper, is VaR at the confidence level . Meanwhile, estimating the tail of an operational loss distribution is often difficult for a number of reasons, such as insufficient historical data and the various kinds of factors in operational loss. We therefore need sufficient verification of the appropriateness and robustness of the model used in quantitative operational risk management.

One verification approach for a risk model is sensitivity analysis (also called model behavior analysis). The term “sensitivity analysis” can be interpreted in a few different ways. In this paper, we use this term to mean analysis of the relevance of a change in the risk amount with changing input information (e.g., added/deleted loss data or changing model parameters). Using sensitivity analysis is advantageous not only for validating the accuracy of a risk model but also for deciding the most effective policy with regard to the variable factors. This examination of how the variation in the output of a model can be apportioned to different sources of variations in risk will give impetus to business improvements. Moreover, sensitivity analysis is also meaningful for scenario analysis. Basel II requires not only use of historical internal/external data and Business Environment and Internal Control Factors (BEICFs) as input information, but also use of scenario analyses to evaluate low-frequency high-severity loss events that cannot be captured by empirical data. As noted above, to quantify operational risk we need to estimate the tail of the loss distribution, so it is important to recognize the impact of our scenarios on the risk amount.

In this study, we perform a sensitivity analysis of the operational risk model from a theoretical viewpoint. In particular, we consider mainly the case of adding loss factors. Let be a random variable that represents the loss amount with respect to the present risk profile and let be a random variable of the loss amount caused by an additional loss factor found by a detailed investigation or brought about by expanded business operations. In a practical sensitivity analysis, it is also important to consider the statistical effect (estimation error of parameters, etc.) when validating an actual risk model, but such an effect should be treated separately. We focus on the change from a prior risk amount to a posterior risk amount , where is a risk measure. We use VaR at the confidence level as our risk measure and we study the asymptotic behavior of VaR as .

Our framework is mathematically related to the study of [Böcker & Klüppelberg(2010)]. They regard and as loss amount variables of separate categories (cells) and study the asymptotic behavior of an aggregated loss amount as . In addition, a similar study that adopts a conditional VaR (CVaR; also called an expected shortfall, average VaR, tail VaR, etc.) is found in [Biagini & Ulmer(2008)].

In other related work, [Degen et al.(2010)] study the asymptotic behavior of the “risk concentration”

| (1.2) |

with to investigate the risk diversification benefit when and are identically distributed. Similarly, [Embrechts et al.(2009a)] study (1.2) for multivariate regularly varying random vector to examine asymptotic super-/sub-additivity of VaRs. The properties of (1.2) are also studied in [Embrechts et al.(2009b)], [Embrechts et al.(2013)], and [Embrechts et al.(2015)] with respect to risk aggregation and model robustness.

In contrast, in this work, we aim to estimate the difference in VaRs, such as (1.1), so our results give higher order estimates than the above results. In addition, our result does not require the assumption that and are identically distributed. Moreover, we do not specify a model for and , so our results are applicable to the general case.

Our results also have the following financial implications.

-

(a)

When is a loss amount with high frequency and low severity, the effect of adding is estimated by capturing the EL of ; thus, we should focus on the body of the distribution of rather than the tail,

-

(b)

When is a loss amount with low frequency and high severity, we should take care to capture the tail of .

Similar empirical and statistical arguments are found in [Frachot et al.(2001)], and we provide the theoretical rationale for these arguments.

The rest of this paper is organized as follows. In Section 2, we introduce the framework of our model and some notation. In Section 3, we give rough estimations of the asymptotic behavior of the risk amount . Our main results are in Section 4, and we present finer estimations of the difference between and , that is, . In Section 5, we present some numerical examples of our results. Section 6 concludes the paper. Section A is an appendix. In Section A.1, we give a partial generalization of the results in Section 4 when and are not independent. One of these results is related to the study of risk capital decomposition and we study these relations in Section A.2. All the proofs of our results are given in Section A.3.

2 Notation and Model Settings

We fix the probability space as , and assume that all random variables below are defined on it. For a random variable and , we define the -quantile (VaR) by

| (2.1) |

where is the distribution function of .

We denote by the set of regularly varying functions with index ; that is, if and only if for any . When , a function is called slowly varying. For the details of regular variation and slow variation, see [Bingham et al.(1987)] and [Embrechts et al.(2003)]. For a random variable , we denote when the tail probability function is in . We mainly treat the case of , in which the th moment of is infinite for . Two well-known examples of heavy-tailed distributions that have regularly varying tails are the generalized Pareto distribution (GPD) and the g-h distribution (see [Degen et al.(2006)], [Dutta & Perry(2006)]), which are widely used in quantitative operational risk management. In particular, the GPD plays an important role in extreme value theory, and can approximate the excess distributions over a high threshold of all the commonly used continuous distributions. See [Embrechts et al.(2003)] and [McNeil et al.(2005)] for details.

Let and be non-negative random variables and assume and for some . We call (resp. ) the tail index of (resp. ). A tail index represents the thickness of a tail probability. For example, the relation means that the tail of is fatter than that of .

We regard as the total loss amount of a present risk profile. In the framework of the standard loss distribution approach (LDA, see [Frachot et al.(2001)] for details), is often assumed to follow a compound Poisson distribution. If we consider a multivariate model, is given by , where is the loss amount variable of the th operational risk cell (). We are aware of such formulations, but we do not limit ourselves to such situations in our settings.

The random variable means an additional loss amount. We consider the total loss amount variable as a new risk profile. As mentioned in Section 1, our interest is in how a prior risk amount changes to a posterior amount .

3 Basic Results of Asymptotic Behavior of

First we give a rough estimation of in preparation for introducing our main results in the next section.

Proposition 1.

- (i)

-

If , then ,

- (ii)

-

If , then ,

- (iii)

-

If , then

as , where the notation , denotes and is a random variable whose distribution function is given by .

These results are easily obtained and not novel. In particular, this proposition is strongly related to the results in [Böcker & Klüppelberg(2010)] (in the framework of LDA).

In contrast with Theorem 3.12 in [Böcker & Klüppelberg(2010)], which implies an estimate for as “an aggregation of and ”, we review the implications of Proposition 1 from the viewpoint of sensitivity analysis. Proposition 1 implies that when is close to one, the posterior risk amount is determined nearly entirely by either of the risk amounts or showing a fatter tail. On the other hand, when the thicknesses of the tails are the same (i.e., ,) the posterior risk amount is given by the VaR of the random variable and is influenced by both and even if is close to one.

Remark 1.

The random variable is a variable determined by a fair coin toss (heads: ; tails: ). That is, is defined as , where is a random variable with the Bernoulli distribution (i.e., ) which is independent of and . Then it holds that . Therefore, defined in Proposition 1 is actually a distribution function.

Remark 2.

Note that we can generalize the results of Proposition 1 to the case where and are not independent. For instance, we can easily show that assertions (i) and (iii) always hold in general. One of the sufficient conditions for assertion (ii) is a “negligible joint tail condition”; that is,

- [A1]

-

as

(see [Jang & Jho(2007)] for details). Related results are also obtained in [Albrecher et al.(2006)] and [Geluk & Tang(2009)].

4 Main Results

In this section, we present a finer representation of the difference between and than Proposition 1. We set the following conditions.

- [A2]

-

There is some such that has a positive, non-increasing density function on ; that is, .

- [A3]

-

The function converges to some real number as .

- [A4]

-

The same assertion as [A2] holds when is replaced with .

Note that condition [A2] (resp. [A4]) and the monotone density theorem (Theorem 1.7.2 in [Bingham et al.(1987)]) imply (resp. ).

Remark 3.

The condition [A3] seems a little strict: it implies that and (a constant multiple of) are asymptotically equivalent, where and are slowly varying functions. However, since the Pickands–Balkema–de Haan theorem (see [Balkema & de Haan(1974)] and [Pickands(1975)]) implies that and are approximated by the GPD, the asymptotic equivalence of and approximately holds (note that [A3] is guaranteed when and follow the GPD: see Section 5). Note that when , condition [A3] is called a “tail-equivalence” (see [Embrechts et al.(2003)] for instance).

Our main result is the following.

Theorem 1.

Define by (1.1) and similarly with switching the roles of and . Then the following assertions hold as . If , then under . If , then under and . If , then under . If , then under and . If , then under and .

The assertions of Theorem 1 are divided into five cases according to relative magnitudes of and . In particular, when , we get different results depending on whether or not is greater than . Assertion (i) implies that if the tail probability of is sufficiently lower than that of , then the effect of a supplement of is limited to the EL of . In fact, we also get a result similar to assertion (i), introduced in Section A.2, when the impact of is absolutely small. These results indicate that if an additional loss amount is not so large, we may not need to be concerned about the effect of a tail event raised by .

Assertion (ii) implies that when , the difference in risk amount cannot be approximated by the EL even if , and we need information on the tail (rather than the body) of the distribution of . For instance, let us consider the case where describes scenario data such that and is large enough (or, equivalently, is small enough) that and . Then, we can formally interpret assertion (ii) as

| (4.1) | |||||

Strictly speaking, if we also assume that exists and is finite ( is given in Remark 3), we have , . Applying Lemma 2 (with ), we get for small , hence (4.1) is verified. Thus, it is sufficient to provide the amount on the right-hand side of (4.1) for an additional risk capital. So, in this case, the information on the pair and detailed information on the tail of enable conservative estimation of the difference.

When the tail of has the same thickness as the tail of , we have assertion (iii). In this case, we see that by a supplement of , the risk amount is multiplied by . The slower the decay speed of , which means the fatter the tail amount variable becomes with an additional loss, the larger the multiplier . Moreover, if is small, we have the approximation

| (4.2) |

Here, is the Landau symbol (little o): . The relation (4.2) has the same form as assertion (ii), and in this case we have a similar implication as (4.1) by letting and .

Assertions (iv)–(v) are merely restated consequences of assertions (i)–(ii). In these cases, is too small compared with and , so we need to compare with . In estimating the posterior risk amount, , the effect of the tail index of is significant.

By Theorem 1, we see that the smaller the tail index , the more precise is the information needed about the tail of .

Remark 4.

It should be noted that assertion (iii) of Theorem 1 is not novel. For instance, a more general result than (iii) is introduced in [Barbe et al.(2006)] (without strict arguments: [Barbe et al.(2006)] have not provided a complete proof, so we give lemmas that immediately show Theorem 1(iii) in Section A.3). Moreover, assertions (iv)–(v) are mathematically the same as (i)–(ii) (thus, the mathematical contribution of our results is centered on the first two assertions). Nevertheless, we have stated assertions (iii)–(v) in Theorem 1 for demonstrating how the asymptotic behavior of the difference in VaR changes by shifting the value of (or ) as mentioned above.

5 Numerical Examples

In this section we numerically verify our main results for typical examples in the standard LDA framework. Let and be given by the compound Poisson variables , , where are independent random variables and the elements of , are each independent and identically distributed. The variables and mean the frequency of loss events, and the variables and indicate the severity of each loss event. We assume that and for some , where denotes the Poisson distribution with intensity . To be strict, we use the GPD, whose distribution function is given by .

Throughout this section, we assume that follows with and set . We also assume that follows and . We set the values of parameters and in each case appropriately. We note that and , where and . Moreover, condition [A3] is satisfied with

| (5.1) |

Indeed, we observe that

| (5.2) |

and Theorem 1.3.9 in [Embrechts et al.(2003)] tells us that and with .

To calculate VaR in the framework of LDA, several numerical methods are known. Monte Carlo, Panjer recursion, and inverse Fourier (or Laplace) transform approaches are widely used (see [Frachot et al.(2001)]). The direct numerical integration of [Luo & Shevchenko(2009)] is an adaptive method for calculating VaR precisely when is close to one, and a similar direct integration method has been proposed by [Kato(2012)]. These approaches are classified as inverse Fourier transform approaches. The precision of these numerical methods was compared in [Shevchenko(2010)]. We need to have quite accurate calculations, so we use direct numerical integration to calculate and .

Unless otherwise noted, we set . Then, the value of the prior risk amount is .

5.1 The case of

First we consider the case of Theorem 1(i). We set . The result is given in Table 1, where

| (5.3) |

and . Here, is simply denoted as .

Although the absolute value of the error becomes slightly larger when is near one, the difference in VaR is accurately approximated by .

5.2 The case of

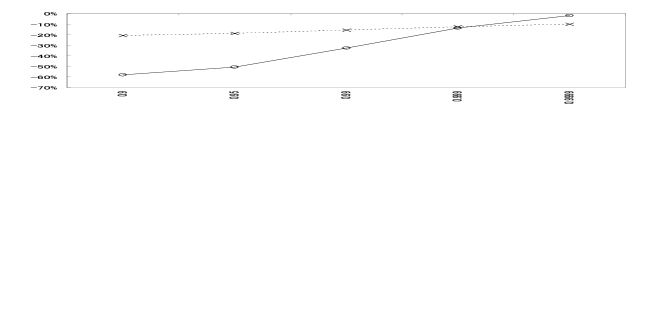

This case corresponds to Theorem 1(ii). As in Section 5.1, we also set . The result is given as Table 2, where and the error is the same as (5.3). We see that the accuracy becomes lower when is close to one or zero. Even in these cases, as Fig. 1 shows for the cases of and , we observe that the error approaches 0 when letting .

| Approx | Error | |||

|---|---|---|---|---|

| 0.1 | 9.500 | 1,111,092 | 1,111,111 | 1.68E-05 |

| 0.2 | 4.500 | 1,249,995 | 1,250,000 | 4.26E-06 |

| 0.3 | 2.833 | 1,428,553 | 1,428,571 | 1.26E-05 |

| 0.4 | 2.000 | 1,666,647 | 1,666,667 | 1.21E-05 |

| 0.5 | 1.500 | 2,000,141 | 2,000,000 | -7.05E-05 |

| Approx | Error | |||

|---|---|---|---|---|

| 0.8 | 0.750 | 3.64E+06 | 3.14E+06 | -1.36E-01 |

| 1.0 | 0.500 | 2.02E+08 | 2.00E+08 | -8.38E-03 |

| 1.2 | 0.333 | 3.31E+09 | 3.30E+09 | -1.73E-03 |

| 1.5 | 0.167 | 5.69E+10 | 5.63E+10 | -9.98E-03 |

| 1.8 | 0.056 | 4.36E+11 | 3.81E+11 | -1.26E-01 |

5.3 The case of

In this section, we set . We apply Theorem 1(iii). We compare the values of and in Table 3, where the error is the same as (5.3). We see that they are very close.

| Approx | Error | ||

|---|---|---|---|

| 100 | 1.05E+11 | 1.05E+11 | -2.05E-07 |

| 1,000 | 3.67E+11 | 3.67E+11 | -1.85E-07 |

| 10,000 | 1.50E+12 | 1.50E+12 | -1.43E-07 |

| 100,000 | 8.17E+12 | 8.17E+12 | -8.51E-08 |

| 1,000,000 | 6.01E+13 | 6.01E+13 | -3.46E-08 |

5.4 The case of

Finally, we treat the case of Theorem 1(iv). We set . Here is too small compared with , so we compare the values of and

| (5.4) |

The results are shown in Table 4. We see that the error () tends to become smaller when is large.

Table 4 also indicates that the supplement of has quite a large effect on the risk amount when the distribution of has a fat tail. For example, when , the value of is more than times and is heavily influenced by the tail of . We see that a small change of may cause a huge impact on the risk model.

In our examples, we do not treat the case of Theorem 1(v), but a similar implication is obtained in that case, too.

| Approx | Error | |||

|---|---|---|---|---|

| 2.5 | 2.12E+12 | 1.52E+12 | -2.82E-01 | 4.00E+11 |

| 3.0 | 4.64E+13 | 4.56E+13 | -1.61E-02 | 3.34E+13 |

| 3.5 | 2.99E+15 | 2.99E+15 | -3.04E-04 | 2.86E+15 |

| 4.0 | 2.52E+17 | 2.52E+17 | -5.38E-06 | 2.50E+17 |

| 4.5 | 2.23E+19 | 2.23E+19 | -2.09E-07 | 2.22E+19 |

6 Concluding Remarks

In this paper, we have introduced a theoretical framework of sensitivity analysis for quantitative operational risk management. Concretely speaking, we have investigated the impact on the risk amount (here, VaR) arising from adding the loss amount variable to the present loss amount variable when the tail probabilities of and are regularly varying ( for some ). The result depends on the relative magnitudes of and . One implication is that we must pay more attention to the form of the tail of when its tail is fatter. Nonetheless, as long as , the difference between the prior VaR and the posterior VaR is approximated by the EL of . As mentioned in the end of Section 1, similar phenomena were empirically found in [Frachot et al.(2001)]. As far as we know, this paper is the first to provide a theoretical rationale for these while paying attention to the difference between the tail indices of loss distributions.

We have mainly treated the case where and are independent, except for a few cases discussed in Section A.1. In related studies of the case where and are dependent, [Böcker & Klüppelberg(2010)] invoke a Lévy copula to describe the dependency and give an asymptotic estimate of Fréchet bounds of total VaR. In [Embrechts et al.(2009a)], the sub- and super-additivity of quantile-based risk measures is discussed when and are correlated (see also Remark 6). However, the focus of these studies is concentrated on the case of . Directions of our future work are to deepen our study and extend it to more general cases when and have a dependency structure (including the case of ).

Another interesting topic is to study a similar asymptotic property of CVaRs,

| (6.1) |

Since CVaR is coherent and continuously differentiable (in the sense of [Tasche(2008)]), the following inequality holds in general (assuming )

| (6.2) |

(see Proposition 17.2 in [Tasche(2008)]§§§The author thanks one of the anonymous referees for highlighting this point.). Another remaining task is to investigate the property of more precisely when is close to one.

A Appendix

A.1 Consideration of dependency structure

In Sections 3–5, we have mainly assumed that and are independent, since they were caused by different loss factors. However, huge losses often happen due to multiple simultaneous loss events. Thus, it is important to allocate risk capital considering a dependency structure between loss factors. Basel II states that “scenario analysis should be used to assess the impact of deviations from the correlation assumptions embedded in the bank’s operational risk measurement framework, in particular, to evaluate potential losses arising from multiple simultaneous operational risk loss events” in paragraph 675 of [BCBS(2004)].

In this section, we consider the case where and are not necessarily independent, and present generalizations of Theorem 1. Recall that and are random variables for some . We focus on the case of . Let (resp. ) be a regular conditional probability distribution with respect to (resp., ) given (resp., ); that is, and . Here, is the Borel field of . We define the function by . We see that the function satisfies

| (A.1) |

for each .

We prepare the following conditions.

- [A5]

-

There is some such that has a positive, non-increasing, continuous density function on for -a.a. .

- [A6]

-

It holds that

(A.2) for any compact set and

(A.3) for some constants and , where is the -norm under the measure .

Let be the expectation under the probability measure . Under condition [A5], we see that for each

| (A.4) |

We do not distinguish the left- and right-hand sides of (A.4). In particular, the left-hand side of (A.3) is regarded as .

Remark 5.

-

(i)

Note that condition [A5] includes condition [A2]. Under [A5]–[A6], we have and then the negligible joint tail condition [A1] is also satisfied (therefore, the dependency of and considered in this section is not so strong).

-

(ii)

Conditions [A5] and [A6] seem to be a little strong, but we have an example. Let be a non-negative random variable that is independent of and let be a positive measurable function. We define

(A.5) If we assume that for some and that has a positive, non-increasing, continuous density function , then we have and

(A.6) Since has an upper bound, we see that satisfies (A.2) by using Theorem 1.5.2 of [Bingham et al.(1987)]. Moreover, it follows that for

(A.7) and the right-hand side of (A.7) converges to as . Thus (A.3) is also satisfied.

At this stage, we cannot find financial applications of (A.5). One of our aims for the future is to give a more natural example satisfying [A5]–[A6], or to weaken the assumptions more than [A5]–[A6].

Now we present the following theorem.

Theorem 2.

- (i)

-

Assume and . If , then

(A.8) - (ii)

-

Assume , and . Then the same assertions as Theorem 1 hold.

Relation (A.8) gives an implication similar to (5.12) in [Tasche(2000)]. The right-hand side of (A.8) has the same form as the so-called component VaR:

| (A.9) |

under some suitable mathematical assumptions. In Section A.2 we study the details. We can replace the right-hand side of (A.8) with (A.9) by a few modifications of our assumptions:

- [A5’]

-

The same condition as [A5] holds by replacing with .

- [A6’]

Indeed, our proof also works upon replacing with .

Remark 6.

In this section, we treat only the case where the dependency of and is not very strong (see Remark 5(i)). Needless to say, it is meaningful to study a more highly correlated case. In such a case, the dependence structure between and is more effective for the asymptotic behavior of . Therefore, it is not so easy to introduce a result like Theorem 1 without deeply investigating the dependency of and .

When , the asymptotic behavior of as is studied in several papers within the framework of multivariate extreme value theory, including the case where and are highly correlated. For instance, the arguments in Section 6 in Embrechts et al. (2009) show that when and are identically distributed (and thus ) and the dependence of and is described by the Fréchet copula (say, ), the asymptotic sub- and super-additivity of VaR for and is determined by the tail dependence coefficients of .

A.2 Effect of a supplement of a small loss amount

In this section, we treat modified versions of Theorems 1(i) and 2(i). We do not assume that the random variables are regularly varying, but that the additional loss amount variable is very small. Let be non-negative random variables and let . We define a random variable by . We regard (resp. ) as the prior (resp. posterior) loss amount variable and consider the limit of the difference between the prior and posterior VaR when taking . Instead of making assumptions of regular variation, we adopt “Assumption ” in [Tasche(2000)]. Then Lemma 5.3 and Remark 5.4 in [Tasche(2000)] imply

By (A.2), we have

| (A.11) |

where we simply put . In particular, if and are independent, then

| (A.12) |

Thus, the effect of a supplement of the additional loss amount variable is approximated by its component VaR or EL. So, assertions similar to Theorems 1(i) and 2(i) also hold in this case.

The concept of the component VaR is related to the theory of risk capital decomposition (or risk capital allocation). Let us consider the case where and are loss amount variables and the total loss amount variable is given by with a portfolio . We try to calculate the risk contributions for the total risk capital , where is a risk measure.

One idea is to apply Euler’s relation

| (A.13) |

when is linear homogeneous and is differentiable with respect to and . In particular we have

| (A.14) |

and the second term in the right-hand side of (A.14) is regarded as the risk contribution of . As in early studies considering the case of , the same decomposition as (A.14) is obtained in [Garman(1997)] and [Hallerbach(2003)] and the risk contribution of is called the component VaR. The consistency of the decomposition of (A.14) has been studied from several points of view ([Denault(2001)], [Kalkbrener(2005)], [Tasche(2000)], and so on). In particular, Theorem 4.4 in [Tasche(2000)] implies that the decomposition of (A.14) is “suitable for performance measurement” (Definition 4.2 of [Tasche(2000)]). Although many studies assume that is a coherent risk measure, the result of [Tasche(2000)] also applies to the case of .

Another approach toward calculating the risk contribution of is to estimate the difference between the risk amounts , which is called the marginal risk capital—see [Merton & Perold(1993)]. (When , it is called a marginal VaR.) This is intuitively understandable, however the aggregation of marginal risk capitals is not equal to the total risk amount .

A.3 Proofs

In this section we present the proofs of our results. First, we list the auxiliary lemmas used to show our main results.

Lemma 1.

Let be nonnegative random variables satisfying and for . Assume the negligible joint tail condition [A1] (replacing and with and ). Then as . Moreover .

Proof.

When , we see that

| (A.15) |

Similarly, for each ,

| (A.16) |

Since is arbitrary, the left-hand side of (A.16) is bounded from above by 1. Therefore, we observe , and so the assertions are true.

The above arguments also work well in the case of by switching the roles of and . When , the assertions are given by Lemma 4 in [Jang & Jho(2007)]. ∎

Remark 7.

In the above lemma, condition [A1] is required only when . The assertions always hold in general when .

The following Lemma 2 is strongly related to Theorem 2.4 in [Böcker & Klüppelberg(2005)] and Theorem 2.14 in [Böcker & Klüppelberg(2010)] when .

Lemma 2.

Let , be random variables with . We assume that , for some . Then , .

Proof.

For , we put and . Note that (resp. ) is a left-continuous version of the generalized inverse function of (resp. ) defined in [Böcker & Klüppelberg(2005)]. By Proposition 2.13 in [Böcker & Klüppelberg(2005)], we have and .

By Theorem 1.5.12 in [Bingham et al.(1987)], we get and as . Thus

| (A.17) |

Then we have and as , which imply our assertions. ∎

The following lemma is easily obtained from Theorem A3.3 in [Embrechts et al.(2003)].

Lemma 3.

Let be a regularly varying function and let be such that and as . Then .

We are now ready to prove the main results.

Proof of Theorem 2. Define

| (A.18) |

Since , the relation (A.3) implies that is uniformly integrable with respect to . Thus, is continuous in . Moreover, since it follows that

| (A.19) | |||||

for each , we see that by virtue of (A.2).

We prove the following proposition.

Proposition 2.

.

Proof.

By the assumptions and [A5], we have

| (A.20) |

for , where

| (A.21) | |||||

| (A.22) | |||||

| (A.23) |

Since , and , we have

| (A.24) |

To estimate the term , we define a random variable by and a function by

| (A.25) |

Then assumption [A6] implies

| (A.26) | |||||

Moreover we can rewrite as

| (A.27) |

where . Then Taylor’s theorem implies

| (A.28) | |||||

where . Thus

| (A.29) |

Now we complete the proof of Theorem 2(i). Let us put and . Obviously and we may assume ( is given in [A5]). Since , we have

| (A.30) |

where . Proposition 2 implies that the left-hand side of (A.30) is asymptotically equivalent to . Moreover, using Proposition 1(i) and Lemma 3, we have as . On the other hand,

| (A.31) |

and so the right-hand side of (A.31) converges to one as by using Proposition 1(i) and Lemma 3 again. Thus, the right-hand side of (A.30) is asymptotically equivalent to . Then we obtain the assertion.

Proof of Theorem 2. When , the assertion is obtained from Remark 5(i) and Lemmas 1–2, so we consider only the case of . The assertion is obtained by a proof similar to that of Theorem 2(i) by using the following proposition instead of Proposition 2.

Proposition 3.

It holds that

| (A.32) |

Proof.

Take any . The same calculation as in the proof of Proposition 2 gives us

| (A.33) |

where is the same as on replacing with (.) By assumption [A3] and the monotone density theorem, we see that

| (A.34) |

By a calculation similar to the one in the proof of Proposition 2, we get

| (A.35) |

for some positive constant . Assumption [A6] implies that the right-hand side of (A.35) converges to zero as for each . Indeed, if then this is obvious. If , we have

| (A.36) | |||||

Thus we get

| (A.37) |

By assumption [A6], we have

| (A.38) |

where . Then it holds that

| (A.39) |

by virtue of the monotone density theorem and assumption [A3].

Acknowledgments

The author would like to thank the anonymous referees for their valuable comments and suggestions, which have improved the quality of the paper.

References

- Albrecher et al.(2006) H. Albrecher, S. Asmussen & D. Kortschak (2006) Tail asymptotics for the sum of two heavy-tailed dependent risks, Extremes 9 (2), 107–130.

- Balkema & de Haan(1974) A. Balkema & L. de Haan (1974) Residual life time at great age, Annals of Probability 2, 792–804.

- Barbe et al.(2006) P. Barbe, A.-L. Fougeres & C. Genest (2006) On the tail behavior of sums of dependent risks, Astin Bulletin 36 (2), 361–373.

- BCBS(2004) Basel Committee on Banking Supervision (2004) International Convergence of Capital Measurement and Capital Standards: A Revised Framework, Bank of International Settlements, Available from http://www.bis.org/

- BCBS(2014) Basel Committee on Banking Supervision (2014) Standardised Measurement Approach for Operational Risk, Bank of International Settlements, Available from http://www.bis.org/

- BCBS(2016) Basel Committee on Banking Supervision (2016) Operational risk - Revisions to the Simpler Approaches, Bank of International Settlements, Available from http://www.bis.org/

- Biagini & Ulmer(2008) F. Biagini & S. Ulmer (2008) Asymptotics for operational risk quantified with expected shortfall, Astin Bulletin 39, 735–752.

- Bingham et al.(1987) N. H. Bingham, C. M. Goldie & J. L. Teugels (1987) Regular Variation, Cambridge: Cambridge University Press.

- Böcker & Klüppelberg(2005) C. Böcker & C. Klüppelberg (2005) Operational VaR: a closed-form approximation, Risk 18 (12), 90–93.

- Böcker & Klüppelberg(2010) C. Böcker & C. Klüppelberg (2010) Multivariate models for operational risk, Quantitative Finance 10 (8), 855–869.

- Degen et al.(2006) M. Degen, P. Embrechts & D. D. Lambrigger (2006) The quantitative modeling of operational risk: between g-and-h and EVT, Astin Bulletin 372, 265–291.

- Degen et al.(2010) M. Degen, D. D. Lambrigger & J. Segers (2010) Risk concentration and diversification: second-order properties, Insurance: Mathematics and Economics 46 (3), 541–546.

- Denault(2001) M. Denault (2001) Coherent allocation of risk capital, Journal of Risk 4 (1), 1–34.

- Dutta & Perry(2006) K. Dutta & J. Perry (2006) A tale of tails: an empirical analysis of loss distribution models for estimating operational risk capital, Working papers of the Federal Reserve Bank of Boston, Available from http://www.bos.frb.org/ No. 06-13, 2006.

- Embrechts et al.(2003) P. Embrechts, C. Klüppelberg & T. Mikosch (2003) Modelling Extremal Events. Berlin: Springer.

- Embrechts et al.(2009a) P. Embrechts, D. Lambrigger & M. Wüthrich (2009a) Multivariate extremes and the aggregation of dependent risks: examples and counter-examples, Extremes 12 (2), 107–127.

- Embrechts et al.(2009b) P. Embrechts, P. Nešlehová & M. Wüthrich (2009b) Additivity properties for value-at-risk under Archimedean dependence and heavy-tailedness, Insurance: Mathematics and Economics 44, 164–169.

- Embrechts et al.(2013) P. Embrechts, G. Puccetti & L. Rüschendorf (2013) Model uncertainty and VaR aggregation, Journal of Banking and Finance 37 (8), 2750–2764.

- Embrechts et al.(2015) P. Embrechts, P. Wang & B. Wang (2015) Aggregation-robustness and model uncertainty of regulatory risk measures, Finance and Stochastics 19 (4), 763–790.

- Frachot et al.(2001) A. Frachot, P. Georges & T. Roncalli (2001) Loss distribution approach for operational risk, Working Paper, Crédit Lyonnais, Groupe de Recherche Opérationelle, Available from http://gro.creditlyonnais.fr/

- Garman(1997) M. Garman (1997) Taking VaR to pieces, Risk 10 (10), 70–71.

- Geluk & Tang(2009) J. Geluk & Q. Tang (2009) Asymptotic tail probabilities of sums of dependent subexponential random variables, Journal of Theoretical Probability 22 (4), 871–882.

- Hallerbach(2003) W. Hallerbach (2003) Decomposing portfolio value-at-risk: a general analysis, Journal of Risk 5 (2), 1–18.

- Jang & Jho(2007) J. Jang & J. H. Jho (2007) Asymptotic super(sub)additivity of value-at-risk of regularly varying dependent variables, Preprint, MacQuarie University, Sydney.

- Kalkbrener(2005) M. Kalkbrener (2005) An axiomatic approach to capital allocation, Mathematical Finance 15 (3), 425–437.

- Kato(2012) T. Kato (2012) Quantitative operational risk management: properties of operational value at risk (OpVaR), RIMS Kokyuroku 1818, 91–112.

- Luo & Shevchenko(2009) X. Luo & P. V. Shevchenko (2009) Computing tails of compound distributions using direct numerical integration, The Journal of Computational Finance 13 (2), 73–111.

- McNeil et al.(2005) A. J. McNeil, R. Frey & P. Embrechts (2005) Quantitative Risk Management Concepts, Techniques and Tools, Princeton, New Jersey: Princeton University Press.

- Merton & Perold(1993) R. C. Merton & A. F. Perold (1993) Theory of risk capital in financial firms, Journal of Applied Corporate Finance 5 (1), 16–32.

- Moscadelli(2004) M. Moscadelli (2004) The modelling of operational risk: experience with the analysis of the data collected by the Basel Committee, Technical report of Banking Supervision Department, Banca d’Italia, 517, Available from http://www.bancaditalia.it/

- Pickands(1975) J. Pickands (1975) Statistical inference using extreme order statistics, Annals of Statistics 3, 119–131.

- PwC Financial Services(2015) PwC Financial Services (2015), Operational risk: the end of internal modelling?, RiskMinds 2015 Point of View, Available from http://www.pwc.com/

- Shevchenko(2010) P. V. Shevchenko (2010) Calculation of aggregate loss distributions, The Journal of Operational Risk 5 (2), 3–40.

- Tasche(2000) D. Tasche (2000) Risk contributions and performance measurement, Working Paper, Center for Mathematical Sciences, Munich University of Technology, Available from http://www-m4.ma.tum.de/

- Tasche(2008) D. Tasche (2008) Capital allocation to business units and sub-portfolios: the Euler principle. In: Pillar II in the New Basel Accord: The Challenge of Economic Capital, 423–453. London: Risk Books.