Parameter Estimation for Hidden Markov Models with Intractable Likelihoods

Abstract

Approximate Bayesian computation (ABC) is a popular technique for approximating likelihoods and is often used in parameter estimation when the likelihood functions are analytically intractable. Although the use of ABC is widespread in many fields, there has been little investigation of the theoretical properties of the resulting estimators. In this paper we give a theoretical analysis of the asymptotic properties of ABC based maximum likelihood parameter estimation for hidden Markov models. In particular, we derive results analogous to those of consistency and asymptotic normality for standard maximum likelihood estimation. We also discuss how Sequential Monte Carlo methods provide a natural method for implementing likelihood based ABC procedures.

keywords:

[class=AMS]keywords:

math.PR/0000000

, , and

t2T.A. Dean and S.S. Singh’s research is funded by the Engineering and Physical Sciences Research Council (EP/G037590/1) whose support is gratefully acknowledged. This

1 Introduction

††footnotetext: First version: Cambridge University Engineering Department Technical Report 660, 1 October 2010The hidden Markov model (HMM) is an important statistical model in many fields including Bioinformatics (e.g. Durbin et al. (1998)), Econometrics (e.g. Kim, Shephard and Chib (1998)) and Population genetics (e.g. Felsenstein and Churchill (1996)); see also Cappé, Rydén and Moulines (2005) for a recent overview. Often one has a range of HMMs parameterised by a parameter vector taking values in some compact subset of Euclidian space. Given a sequence of observations the objective is to find the parameter vector that corresponds to the particular HMM from which the data were generated.

A common approach to estimating is maximum likelihood estimation (MLE). The parameter estimate, denoted , is obtained via maximizing the log-likelihood of the observations:

where

Unless the model is simple, e.g. linear Gaussian or when is a finite set, one can seldom evaluate the likelihood analytically. There are a variety of techniques, for example sequential Monte Carlo (SMC), for numerically estimating the likelihood. However, in a wide range of applications these methods cannot be used, for example when the conditional density of the observed state of the HMM given the hidden state is intractable, by which we mean that this density cannot be evaluated analytically and has no unbiased Monte Carlo estimator. Despite this, one is often still able to generate samples from the corresponding processes for different values of the parameter (e.g. Jasra et al. (2010)). This has led to the development of methods in which is estimated by taking the value of which maximizes some principled approximation of the likelihood which is itself estimated using Monte Carlo simulation.

One such approach is the convolution particle filter of Campillo and Rossi (2009). Another technique which can be applied to this class of problems is indirect inference; see Gourieroux, Monfort and Renault (1993) and Heggland and Frigessi (2004). However in the context of HMMs, when one does not adopt a linear Gaussian approximation of the filtering density (which can be very inaccurate, as in extended Kalman filter approximations), this method is likely to be very expensive. A third method which has recently received a great deal of attention is approximate Bayesian computation (ABC). A non-exhaustive list of references includes: McKinley, Cook and Deardon (2009); Peters, Wüthrich and Shevchenko (2010); Pritchard et al. (1999); Ratmann et al. (2009); Tavre et al. (1997). See also Sisson and Fan (to be published) for a review on computational methodology.

In the standard ABC approach (omitting for the moment the possible use of summary statistics) one assumes that a data set is given and approximates the likelihood function via probabilities of the form

| (1) |

where denotes the observed state of the HMM, is some suitable metric on the n-fold product space and is a constant which reflects the accuracy of the approximation. In practice these probabilities are themselves estimated using Monte Carlo techniques.

The intuitive justification for the ABC approximation is that for sufficiently small

where denotes the volume of the -ball of radius around the points . Thus the probabilities (1) will provide a good approximation to the likelihood, up to the value of some renormalising factor which is independent of and hence can be ignored. However in general it is not at all clear in what sense an approximation to the likelihood must be ‘good’ in order for the resulting inference procedures to be well behaved. The purpose of this paper is to resolve this issue by directly investigating the effect of the parameter , not on the quality of the approximations (1), but on the behaviour of the resulting ABC based parameter estimators.

We note that in (1) we have implicitly assumed that one is working with the entire data set rather than a summary statistic of it as is usually done in practice, especially when the observations take values in some high dimensional space. For ease of exposition we shall persist with this assumption throughout the rest of the paper, noting where appropriate the conditions under which the results we derive will continue to hold when summary statistics are used (see in particular the remarks at the ends of Sections 3 and 4).

1.1 Contribution and Structure

In this paper we investigate the behaviour of ABC when used to estimate the parameters of HMMs for which the conditional densities of the observations given the hidden state are intractable. We shall use a specialization, first proposed in Jasra et al. (2010), of the standard ABC likelihood approximation (1) for when the observations are generated by a HMM. Specifically we approximate the likelihood of a given sequence of observations from a HMM with the probability

| (2) |

where denotes the ball of radius centered around the point . The benefit of this approach is that it retains the Markovian structure of the model. This facilitates both simpler Markov chain Monte Carlo (MCMC) (e.g. McKinley, Cook and Deardon (2009)) and sequential Monte Carlo (SMC) (e.g. Jasra et al. (2010)) implementation of the ABC approximation. Furthermore our experience suggests that this approximation is competitive, from an accuracy perspective, with a wide range of competing methods; see the two afore mentioned references for a deeper discussion of this point.

One could use the approximate likelihoods (2) to estimate the parameters of a HMM in one of two ways. Firstly one could take a Bayesian approach and use (2) to construct an approximation to the posterior. This is the approach most commonly taken in the literature. Alternatively, as we shall do in this paper, one could take a frequentist approach and estimate the parameters of the HMM with the value of the parameter vector which maximizes the corresponding approximate likelihood (2) of the observations. We shall henceforth term this procedure approximate Bayesian computation maximum likelihood estimation (ABC MLE).

Although the use of ABC has become commonplace there has to date been little investigation of the theoretical properties of its use in parameter estimation in either the Bayesian or frequentist context. In particular the following questions remain to be answered. Is ABC MLE consistent? Do ABC based posterior distributions concentrate around the true value of the parameter vector? Indeed do ABC based estimators converge to anything at all? Although these questions may seem abstract it is well known that even the mighty MLE can fail to converge in practice, see Ferguson (1982). Thus before ABC can be placed on firm mathematical foundations the questions raised above need to be addressed.

The purpose of this paper is to bridge this theoretical gap in the context of maximum likelihood estimation. In particular we develop a theoretical justification of the ABC MLE procedure based on its large sample properties analogous to that provided for MLE by standard results concerning asymptotic consistency and normality. Our approach to this problem is based on the novel observation that ABC MLE can be considered as performing MLE using the likelihoods of a collection of perturbed HMMs. This implies that the ABC MLE should in some sense inherit its behaviour from the standard MLE. Using this observation we first show that unlike the MLE, which is asymptotically consistent, the ABC MLE estimator has an innate asymptotic bias. Secondly we show that this bias can be made arbitrarily small by choosing sufficiently small values of . Together these results show that asymptotically the ABC MLE will converge to the true parameter value with a margin of error which can be made arbitrarily small by taking a suitable choice of . Thus our results allow us to develop a rigorous formulation of the intuitive justification of ABC and in doing so to provide a firm mathematical basis for performing ABC based inference.

We complete the picture by analysing the so called noisy variant (see e.g. Fearnhead and Prangle (2010)) of ABC MLE. We show that unlike the ABC MLE the noisy ABC MLE is always asymptotically consistent. This raises the question: does noisy ABC provide us with a ‘free pass’ when performing parameter estimation? Unfortunately the answer in general is no. We show that under reasonable conditions the Fisher information of the noisy ABC MLE is strictly less than that of the standard MLE. As a result we show that the noisy ABC suffers from a relative loss of information and hence statistical efficiency.

As part of these investigations we establish a novel asymptotic missing information principle for HMMs with observations perturbed by additive uniform noise which may in itself be of independent interest to the reader. Finally we remark that although this study is theoretical it is our belief that the results presented herein will help provide guidance for future methodological developments in the field.

This paper is structured as follows. In Section 2 the notation and assumptions are given. In Section 3 we establish some approximate asymptotic consistency type results for the standard ABC MLE. In Section 4 results concerning the asymptotic consistency and normality of the noisy ABC estimator are presented. An extension of the ABC method using probability kernels is discussed in Section 5 and an overview of the use of SMC methods to provide a practical way of implementing ABC is presented in Section 6. An example is given in Section 7 which provides a qualitative demonstration of the behaviour of the ABC estimator predicted in Sections 3 and 4. The article is summarized in Section 8. Supporting technical lemmas and proofs of some of the theoretical results are housed in the two appendices.

2 Notation and Assumptions

2.1 Notation and Main Assumptions

Throughout this paper we shall use lower case letters to denote dummy variables and upper case letters to denote random variables. Observations of a random variable will be denoted by .

We shall frequently have to refer to various kinds of both finite, infinite and doubly infinite sequences. For brevity the following shorthand notations are used. For any pair of integers , denotes the sequence of random variables ; denotes the sequence ; denotes the sequence and denotes the sequence . Given a sequence of integers and indicies we shall let denote ; denote and denote respectively. Further we shall also use to denote the full sequence . The two notations defined above will be combined in the following manner. Given a doubly infinite sequence of random variables , a doubly infinite sequence of integers and indicies we shall let denote the sequence . The sequences , and are defined analogously. Lastly given a measure on a Polish space we let denote integration w.r.t. the n-fold product measure on the n-fold product space . Moreover, given a function and integers , we shall let denote the partial integrals .

The essence of our approach is to show that in some sense the ABC MLE inherits the properties of the standard MLE. Thus we shall operate under assumptions on the HMMs that are sufficient to ensure asymptotic consistency and normality of the MLE.

It is assumed that the Markov chain is time-homogenous and takes values in a compact Polish space with associated Borel -field . Throughout it will be assumed that we have a collection of HMMs all defined on the same state space and parametrised by some vector taking values in a compact set . Furthermore we shall reserve to denote the ‘true’ value of the parameter vector. For each we let denote the transition kernel of the corresponding Markov chain and for each and we assume that has a density w.r.t. some common finite dominating measure on . The initial distribution of the hidden state will be denoted by .

We also assume that the observations take values in a state space for some . Furthermore, for each we assume that the random variable is conditionally independent of and given and that the conditional laws have densities w.r.t. some common finite dominating measure . We further assume that for every the joint chain is positive Harris recurrent and has a unique invariant distribution . We shall write to denote the laws of the corresponding stationary processes and to denote expectations with respect to the stationary laws .

Given any and let denote the closed ball of radius centered on the point and let denote the uniform distribution on . For any , let denote the indicator function of . Additionally, for any square matrix , we shall let denote the Frobenius norm .

For any two probability measures on a measurable space we let denote the total variation distance between them. For all we let denote the set of real valued measurable functions satisfying .

Finally, we note that the asymptotic results that we prove for the ABC MLE and its noisy variant hold independently of the initial condition of the hidden state process . Thus, in order to keep the presentation as concise as possible we shall suppress the presence of the initial condition of the hidden state except in those instances where it needs to be referred to explicitly.

2.2 Particular Assumptions

In addition to the assumptions above, the following assumptions are made at various points in the article. Assumptions (A1)-(A3) below are sufficient to guarantee asymptotic consistency of the MLE and (A4)-(A5) ensure the existence of an asymptotic Fisher information matrix, denoted . Further, if the asymptotic Fisher information is invertible then under assumptions (A1)-(A5) the MLE will be asymptotically normal, see Douc, Moulines and Ryden (2004) for more details.

-

(A1)

The parameter vector belongs to the interior of and if and only if .

-

(A2)

For all , , the mappings and are continuous w.r.t. .

-

(A3)

There exist constants such that for every , ,

For the remaining assumptions we assume that there exists an open ball centered at such that

-

(A4)

For all , , the mappings and are twice continuously differentiable on .

-

(A5)

There exists a constant such that for every , ,

Remark 1.

In general assumptions (A3) and (A5) hold when the state space is compact and when the conditional laws of the observed state given the hidden state are heavy tailed, see for example Section 7. However we expect that the behaviours predicted by Theorems 1, 2, 3 and 5 will provide a good qualitative guide to the behaviour of ABC MLE in practice even in cases where the underlying HMMs do not satisfy these assumptions.

Assumptions (A1)-(A5) are sufficient to show that in some sense the ABC MLE inherits the its asymptotic properties from the standard MLE. The Lipschitz assumptions below will be used to establish quantitative bounds on the relative performance of the ABC MLE estimator with respect to that of the MLE.

-

(A6)

There exists an such that for all, , ,

-

(A7)

There exists an such that for all, , ,

3 Approximate Bayesian Computation

3.1 Estimation Procedure

Following Jasra et al. (2010) we consider the ABC approximation to the likelihood of a sequence of observations for some fixed given by,

| (3) | ||||

The purpose of this paper is to analyse the asymptotic properties of the ABC parameter estimator for HMMs defined by

Procedure 1 (ABC MLE).

Given and data , estimate with

| (4) |

The key to our analysis is the following observation which is, to our knowledge, original;

| (5) | |||||

where

| (6) |

and where we note that by Lemma 7 the quantity in (6) is well defined a.s..

The crucial point is that the quantity defined in (6) is the density of the measure obtained by convolving the measure corresponding to with where the density is taken w.r.t. the new dominating measure obtained by convolving with . One can then immediately see that the quantities and appearing in (5) are the transition kernels and conditional laws respectively for a perturbed HMM defined such that it is equal in law to the process

| (7) |

where is the original HMM and the are an i.i.d. sequence of distributed random variables. Crucially the constant of proportionality in (5), which by definition is equal to , is by Lemma 7 non-zero a.s. and is independent of the parameter value . Thus it follows that (4) is statistically identical to the estimator

| (8) |

where denotes the likelihood of the observations w.r.t. the law of the perturbed process . The value of expressing the ABC estimator (4) in the mathematically equivalent form (8) is that (8) reveals the underlying mathematical structure of the estimator and furthermore, as we shall see in the next section, expresses it in a form which is particularly tractable to analysis.

3.2 Theoretical Results

It follows from the previous section that performing ABC MLE is equivalent to estimating the parameter by taking a data set generated by one of the original HMMs and finding the value of which maximises the likelihood of that data set under the corresponding perturbed HMM . Thus the ABC MLE estimator will effectively suffer from the problem of model mis-specification. This raises the question of whether the resulting estimator will still be asymptotically consistent. As the following example shows one must expect that, in general, the answer to this question will be no.

Example 1.

For each let be a directly observed sequence of i.i.d. random variables with common law

and let denote the true value of the model parameter. Then for any the ABC MLE will not be asymptotically consistent even though the MLE estimator is asymptotically consistent for any value of . Furthermore for the ABC approximation to the likelihood is maximized at for any sequence of observations.

Although the ABC MLE estimator is no longer asymptotically consistent we show the following below. Almost surely the ABC MLE will converge, with increasing sample size, to a given point in parameter space (more generally the set of accumulation points will belong to a given subset of parameter space). Further, we show that these accumulation points must lie in some neighbourhood of the true parameter value and that the size of this neighbourhood shrinks to zero as goes to zero (Theorem 2). Finally we show that under certain Lipschitz conditions one can obtain a rate for the decrease in the size of these neighbourhoods (Theorem 3). We note that these results are very much misspecified MLE results in the spirit of, for example, White (1982). However because the dominating measures of the original and perturbed HMMs are no longer necessarily mutually absolutely continuous with respect to each other they can no longer be interpreted in terms of minimising Kullback-Leibler distances.

Before we present our results we first discuss some technical issues that arise in their proofs. It is tempting to try and understand the behaviour of the ABC MLE by extending the parameter space to include and then applying standard results from the theory of MLE. Unfortunately the existing theory of MLE requires that the perturbed likelihoods (see (6)) be continuous w.r.t. which is not true for general dominating measures . The essence of our method is show that despite this certain asymptotic quantities associated with the likelihoods of the perturbed processes (7) are still sufficiently continuous as functions of . In order to do this we need to establish that in some probabalistic sense the order of the operations of differentiating and taking asymptotic limits can be interchanged. It it this that constitutes the bulk of Appendix B.

In order to state and prove these results it is convenient to make the following definitions. For any and , let

| (9) |

where denotes the conditional laws of the observations of the perturbed processes (7) given the infinite past and the expectations are taken with respect to the stationary measure of the unperturbed HMM with parameter . Further for we let

| (10) |

Our first result shows that the ABC MLE is asymptotically biased

Theorem 1.

Assume (A2)-(A3). Then for every , is achieved. Further let

be the set of these maximizers, then for any initial distribution we have that almost surely every accumulation point of the sequence of estimators defined in Procedure 1 belongs to .

Proof.

It follows from (A2) and (A3) that for the perturbed HMM defined in (7) the conditional laws are continuous w.r.t. . Further it follows from (A3) and (LABEL:lemFiltStabStandardeq2) that the conditional laws converge uniformly to the conditional laws and are uniformly bounded, both above and away from zero. It then follows that the conditional log-likelihood functions are continuous, uniformly bounded and converge uniformly to and hence that the expected values are also continuous functions of . The first part of the theorem then follows from the compactness of .

The second part of the result now follows from (A2) and (A3) by using the same arguments as used by Douc, Moulines and Ryden (2004) to prove the asymptotic consistency of the MLE. We leave it to the reader to check the details. ∎

Although Theorem 1 shows that the ABC MLE is asymptotically biased, the following result shows that this error can be made arbitrarily small by choosing a sufficiently small .

Theorem 2.

Assume (A1)-(A3). Then

| (11) |

Remark 2.

Theorems 1 and 2 provide a theoretical justification for the ABC MLE procedure analogous to that provided for the standard MLE procedure by the classical notion of asymptotic consistency. In particular they show that an arbitrary degree of accuracy in the parameter estimate can be achieved given sufficient data and a sufficiently small .

In order to prove Theorem 2 we need the following Lemma whose proof is relegated to Appendix B.

Lemma 1.

Assume (A2)-(A3). Then the mapping is continuous in and right continuous in in the sense that for all pairs of sequences and we have that

Proof of Theorem 2.

In order to prove (11), given that by Lemma 1 the mapping is continuous, it is sufficient to show that for any there exists an such that for all . Suppose that this property does not hold. Then, by the compactness of , there must exist and sequences and such that

for all . However it would then follow from the continuity of that which violates (A1). (In Douc, Moulines and Ryden (2004) it is shown that under (A2) and (A3) that (A1) is equivalent to having that for all .) ∎

The next result shows that, under some additional assumptions, we can characterise the rate at which the asymptotic error in the ABC MLE decreases with .

Theorem 3.

Assume (A1)-(A7) and that the asymptotic Fisher information matrix is invertible. Then there exist finite positive constants such that for all

The proof of Theorem 3 relies on the following lemma whose proof is given in Appendix B.

Lemma 2.

Assume (A1)-(A7). Then , and exist for all where is as in (A4) and (A5). Furthermore

| (12) |

for some and .

Proof of Theorem 3.

Since by assumption is invertible and thus positive definite it follows that there exists some such that

| (13) |

By Lemma 2, is twice continuously differentiable on and so there exists a constant such that

| (14) |

By Theorem 2 there exists a constant such that for all ,

| (15) |

Consider any . By Lemma 2 both and exist and clearly they must both be equal to zero and hence by (12)

| (16) |

Further by the fundamental theorem of calculus

| (17) |

By (13), (14) and (15) it now follows that

| (18) |

Remark 3.

In many cases the complete data sequence is too high-dimensional and instead one performs inference using a summary statistic where is some mapping from to a lower dimensional Euclidean space, e.g. see Tavre et al. (1997). In general this mapping will destroy the Markovian structure of the data and the results derived in this section will not be applicable to ABC based parameter inference conducted using the corresponding summary statistic.

However in practice it is often the case that the mapping is of the form for some function that maps from to a space of lower dimension. When this is true it is easy to see that the Markovian structure of the data is preserved. Moreover suppose that assumptions (A1)-(A7) hold for the underlying HMM. If the mapping preserves the identifiability of the system, that is to say if assumption (A1) also holds for the HMMs with observations , then it is trivial to see that assumptions (A2)-(A7) will also be preserved for all reasonable choices of and thus that Theorems 1, 2 and 3 will also hold for ABC MLE performed using the summary statistic.

4 Noisy Approximate Bayesian Computation

4.1 Estimation Procedure

In the previous section we showed that performing ABC MLE is equivalent to estimating the parameter by choosing the value of the maximizer of the likelihoods of the perturbed HMMs defined in (7). Since the likelihoods over which we maximise are misspecified with respect to the law of the process that is generating the data the resulting estimator has an inherent asymptotic bias.

Suppose now that a sequence of observations from the unperturbed HMM corresponding to some is given. The sequence of noisy observations where , has the same law as a sample from the corresponding perturbed HMM defined in (7). As a result estimating by applying the ABC MLE estimator (4) to the noisy observations in place of , is statistically equivalent to estimating by applying standard MLE to the perturbed HMMs (7). Clearly one would expect that the resulting estimator would inherit the properties of MLE, in particular that it would be asymptotically consistent. In light of the discussion and remarks immediately following the definition of Procedure 1 these observations lead one to the following noisy ABC MLE procedure:

Procedure 2 (Noisy ABC MLE).

Given and data estimate with

| (19) |

4.2 Theoretical Results

In this section we investigate mathematically the noisy ABC MLE procedure defined in Section 4.1. In particular we show that under the assumptions made in Section 2.2 that the noisy ABC MLE inherits the properties of asymptotic consistency and normality from the MLE. Further we provide an analysis of the performance of the noisy ABC MLE relative to the standard MLE by comparing their asymptotic variances. It is first shown that the asymptotic Fisher information of the ABC MLE is strictly less than that of the MLE and hence that the asymptotic variance of the ABC MLE estimator is strictly greater. Thus it follows that the noisy ABC MLE procedure comes at the cost of a loss in accuracy relative to that of the standard ABC procedure. Finally we show that this loss in accuracy can be made arbitrarily small by choosing small enough.

The first result establishes that under (A1)-(A3) the noisy ABC MLE inherits the property of asymptotic consistency.

Theorem 4.

Assume (A1)-(A3). Then Procedure 2 is asymptotically consistent.

Proof.

It is sufficient to show that if (A1)-(A3) hold for the original HMM then they also hold for the perturbed HMM. Recall, for the perturbed HMM, the transitions are as for the original HMM and the likelihood is as (6). Thus (A3) for the original model immediately implies (A3) for the perturbed model.

In order to establish that (A2) holds for the perturbed model it is sufficient to observe that continuity of the mapping for any , follows from continuity of the mapping , uniform boundedness of (ie. (A3)) and the dominated convergence theorem.

It remains to show that (A1) is also inherited by the perturbed model. This assumption is equivalent to demanding that for every there exists some such that

| (20) |

where denotes the law of the process . However by applying Lemma 6 it immediately follows that (20) holds if and only if

for all and so (A1) holds for the original HMMs if and only if it also holds for the perturbed HMMs. ∎

Next we consider the question of asymptotic normality. In Douc, Moulines and Ryden (2004) it was shown that under conditions (A1)-(A5) the MLE for HMMs has asymptotic Fisher information matrix where

Further it was shown that if is invertible then the MLE is asymptotically normal with asymptotic variance equal to . It follows from the proof of Theorem 4 that if (A1)-(A3) hold for the original HMM then they also hold for the perturbed HMM. Further if (A4) and (A5) hold for the original HMM then a simple application of the dominated convergence theorem shows that they also hold for the perturbed HMM. Thus, under assumptions (A1)-(A5) the asymptotic Fisher information matrix of the noisy ABC MLE exists and is equal to where

Moreover if is invertible then the noisy ABC MLE estimator will be asymptotically normal with asymptotic variance equal to . Using these results we can analyze the asymptotic performance of the noisy ABC MLE estimator relative to that of the standard MLE estimator by comparing the two Fisher information matrices. Unfortunately one cannot in general make any explicit quantitative comparisons between these two quantities, however the following result establishes some qualitative relations between the two.

Theorem 5.

Assume (A1)-(A5). Then:

-

1.

. Further if is connected and (see Section 2.1) then the inequality is strict.

-

2.

as .

-

3.

as . Hence for epsilon sufficiently small the ABC MLE is asymptotically normal with asymptotic variance equal to .

-

4.

If (A6) and (A7) hold then .

Theorem 5 tells us that asymptotic variance of the noisy ABC MLE estimator is strictly greater than that of the MLE estimator and hence that there is a loss in accuracy relative to the MLE in using noisy ABC MLE. For very large values of the asymptotic variance of the noisy ABC MLE grows without bound and the loss in accuracy becomes almost complete. Thus if one chooses values of which are too large the noisy ABC MLE becomes ineffective. Furthermore we have shown that by taking small enough values of the loss in accuracy can be be made arbitrarily small and hence that we can obtain (ignoring computational issues) a performance of the noisy ABC MLE arbitrarily close to that of the MLE. Finally, the theorem provides a rate of convergence for the Fisher information matricies for when the likelihoods obey certain simple Lipschitz assumptions.

The proof of Theorem 5 is based on the following lemma, see Appendix B for the proof.

Lemma 3.

Assume (A1)-(A5). Then

where for every doubly infinite sequence the random variable is equal to the difference in the Fisher informations of the conditional laws of and given , that is

Remark 5.

The quantity is also equal to the missing information in the conditional law of relative to that in the conditional law of (where both laws are conditioned on ). Here the term missing information is meant in the sense of that proposed for i.i.d. random variables in Orchard and Woodbury (1972). Hence, Lemma 3 can be considered as a conditional asymptotic missing information principle for HMMs with observations perturbed by uniform additive noise.

Theorem 5 is then an immediate corollary of the following lemma which establishes the behaviour of for different values of .

Lemma 4.

Assume (A1)-(A5). Then:

-

1.

is positive semi-definite. Further if is connected and then for any .

-

2.

as .

-

3.

as .

-

4.

Assume that (A6) and (A7) also hold. Then .

The proof of Lemma 4 is again deferred to Appendix B.

Remark 6.

Comments similar to those in Remark 3 concerning summary statistics also hold for the results on the noisy ABC MLE given in this section. In particular we note that given a summary statistic of the form one can derive a result analogous to Theorem 5 in which the Fisher information matrices and are replaced with the Fisher information matrices for the HMMs and where is a perturbed version of defined in an analogous manner to (7).

5 Smoothed ABC

ABC estimators based on Procedures 1 and 2 have an inherent lack of smoothness due to the fact that the estimator effectively gives weight one to points inside the balls and weight zero to those outside them. As seen in the next section, this becomes particularly problematic if one then tries to estimate these probabilities using SMC algorithms as the algorithm can collapse due to the use of indicator functions; see Del Moral, Doucet and Jasra (2008a) for some discussion.

A common way of smoothing ABC, see for example Beaumont, Zhang and Balding (2002), is to approximate the likelihoods of a sequence of observations not with (3) but instead with the smoothed approximations

where is the density w.r.t. Lebesgue measure of some smooth probability distribution . One then estimates the parameters via maximising (LABEL:KernelApproxeq1).

By using exactly the same arguments as in Section 3.1 it is clear that the smoothed ABC MLE estimator resulting from approximating the likelihoods of a sequence of observations with (LABEL:KernelApproxeq1) for some suitable kernel is statistically equivalent to estimator obtained by by approximating the true likelihoods with the likelihoods of the perturbed HMM defined to be

| (22) |

where the are such that . Further, in an analogous manner to Section 4.1 one can define a smoothed noisy ABC MLE by applying the smoothed ABC MLE defined above to noisy data of the form where again .

It is natural to ask whether results analogous to Theorems 1, 2, 3, 4 and 5 hold for the smoothed ABC MLE and the smoothed noisy ABC MLE. By a careful reading of the proofs of these theorems one can see that analogous results hold when the density of satisfies the following conditions:

-

(i)

for all .

-

(ii)

is continuously differentiable.

-

(iii)

for the reference measure and all ,

-

(iv)

.

We observe that these conditions hold for many commonly used smoothing distributions, in particular the Gaussian distribution.

6 Implementing ABC via SMC

SMC algorithms are commonly used to approximate conditional laws of the form (we drop the notation and omit dependence upon here). At each time the conditional law of the hidden state is approximated by a collection of particles, as

| (23) |

The crucial feature of the SMC algorithm with respect to any form of likelihood based parameter inference is that at each step, , is an approximation to the conditional likelihood . Thus when the conditional likelihoods are tractable SMC algorithms can be used to generate approximations to the full likelihoods , e.g. see Andrieu, Doucet and Tadic (2009) for the use of SMC for MLE in this standard setting.

Consider now the ABC MLE and noisy ABC MLE procedures defined in Sections 3 and 4 and recall that we approximate the true likelihoods with the likelihoods of the perturbed HMMs (7). To see how standard SMC methods can be implemented in the context of these estimators consider the extended process defined such that are the hidden state and observation process of the original HMM and for all , where is an i.i.d. sequence of random variables. Clearly the marginal distributions of the observations of the extended process are equal to those of the observations of the perturbed HMMs defined in (7). Thus in order to compute the ABC approximation to the likelihood of a sequence of observations it is sufficient to compute the likelihood of the observations under the extended HMM detailed above. Since the conditional densities of the observed state given the hidden state of the extended HMM are trivial the corresponding likelihoods may be computed using standard SMC. This suggests the following SMC algorithm for evaluating the ABC approximate likelihoods (3), see Jasra et al. (2010)

Algorithm 1.

SMC for Computation of Approximate Bayesian Likelihood .

For do

-

1.

Generate proposal states where each and each .

-

2.

Weight each proposed state with .

-

3.

Renormalise the weights; .

-

4.

Generate the particles by sampling multinomially from the proposals according to the weights .

Finally approximate the likelihood by .

Similarly, given a distribution with smooth density w.r.t. Lebesgue measure, one can define a SMC algorithm for computing the corresponding smoothed ABC approximations to the likelihoods in an analogous manner; the details follow from Algorithm 2.

Note that in general one does not have to resample the particles at every step and more efficient approaches may be possible, see for example Del Moral, Doucet and Jasra (2008b) and the references therein. A detailed analysis of the SMC method, including description of resampling and convergence results can be found in Doucet, De Freitas and Gordon (2001) and Del Moral (2004).

7 Numerical Example

It is common in economics to model the log returns of a sequence of price data using a HMM. Typically one uses the hidden state to model certain underlying economic factors which cannot be directly observed and the observed state to model the log returns of the prices themselves. Furthermore it has become increasingly common to model the distribution of the log returns of asset prices using -stable distributions due to their seemingly good fit to the actual data, see for example Rachev and Mittnik (2000). Unfortunately the likelihoods of -stable distributions are intractable and so using them presents difficulties when trying to infer model parameters from real financial data.

In this section we study the performance of both the standard and noisy ABC MLE procedures when used to estimate the scale parameter of the following toy economic model with intractable likelihoods. The hidden state takes values in the set and the corresponding Markov chain has transition matrix

Conditional on the hidden state the observed state where denotes the -stable distributions with parameters and , see for example Samorodnitsky and Taqqu (1994). Intuitively the hidden state denotes the health of the underlying economy, being good ie. growth and being bad ie. recession. Given the state of the economy the log returns of the relevant asset price are then -stable distributed with a positive or negative drift as appropriate.

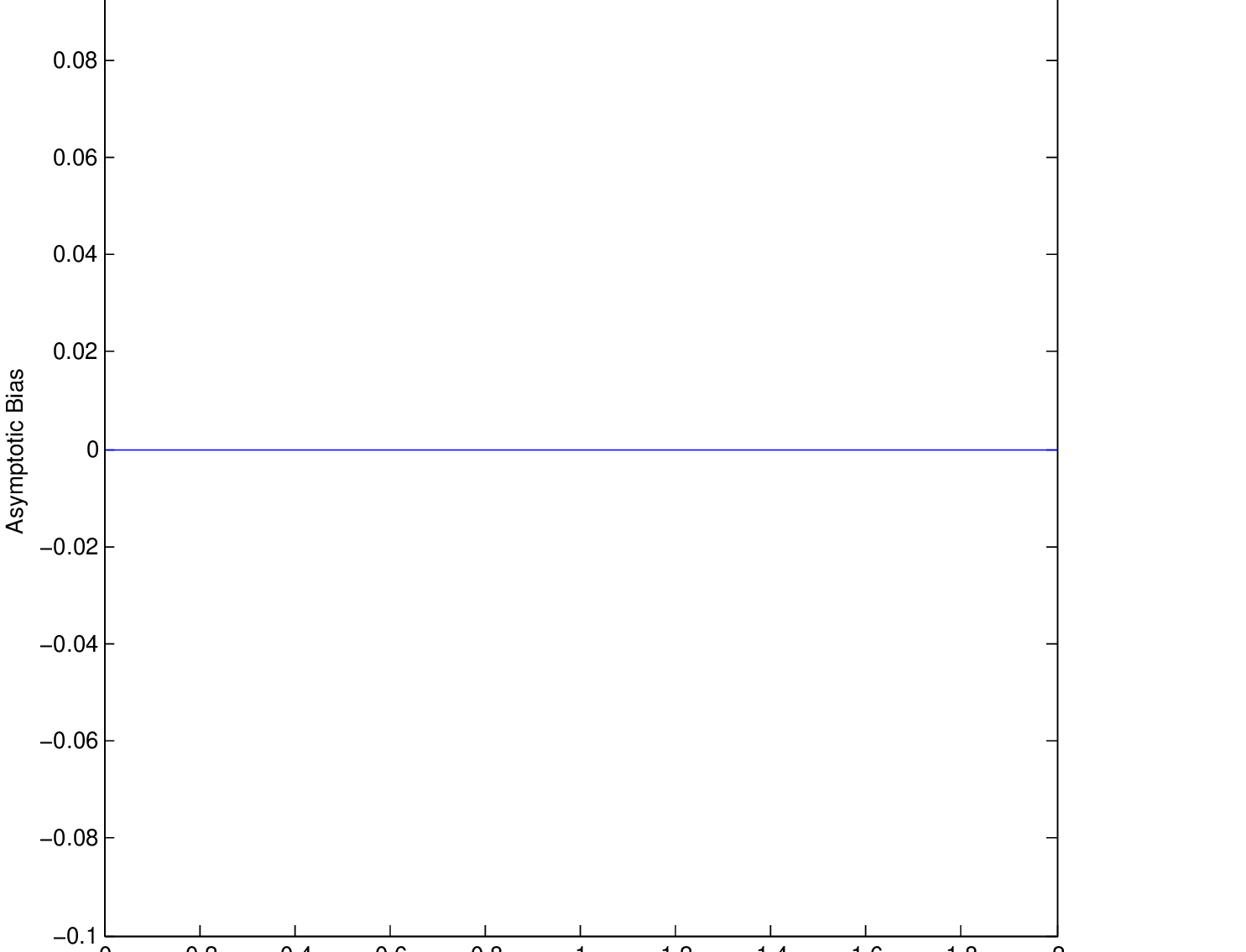

In Figure 1 we plot the asymptotic bias of the ABC MLE when used to estimate the parameters and given that the true model parameters are , and . We note that the ABC MLE seems to induce a bias in the estimates of the scale parameters but not of the location parameters. Intuitively this can be understood as being due to the fact that the observed states of the perturbed HMMs (7) have a greater variance than those of the corresponding original HMMs but the same mean position. Lastly we note that for very small the size of the bias seems to be ie. one order of magnitude less than the upper bound obtained in Theorem 3.

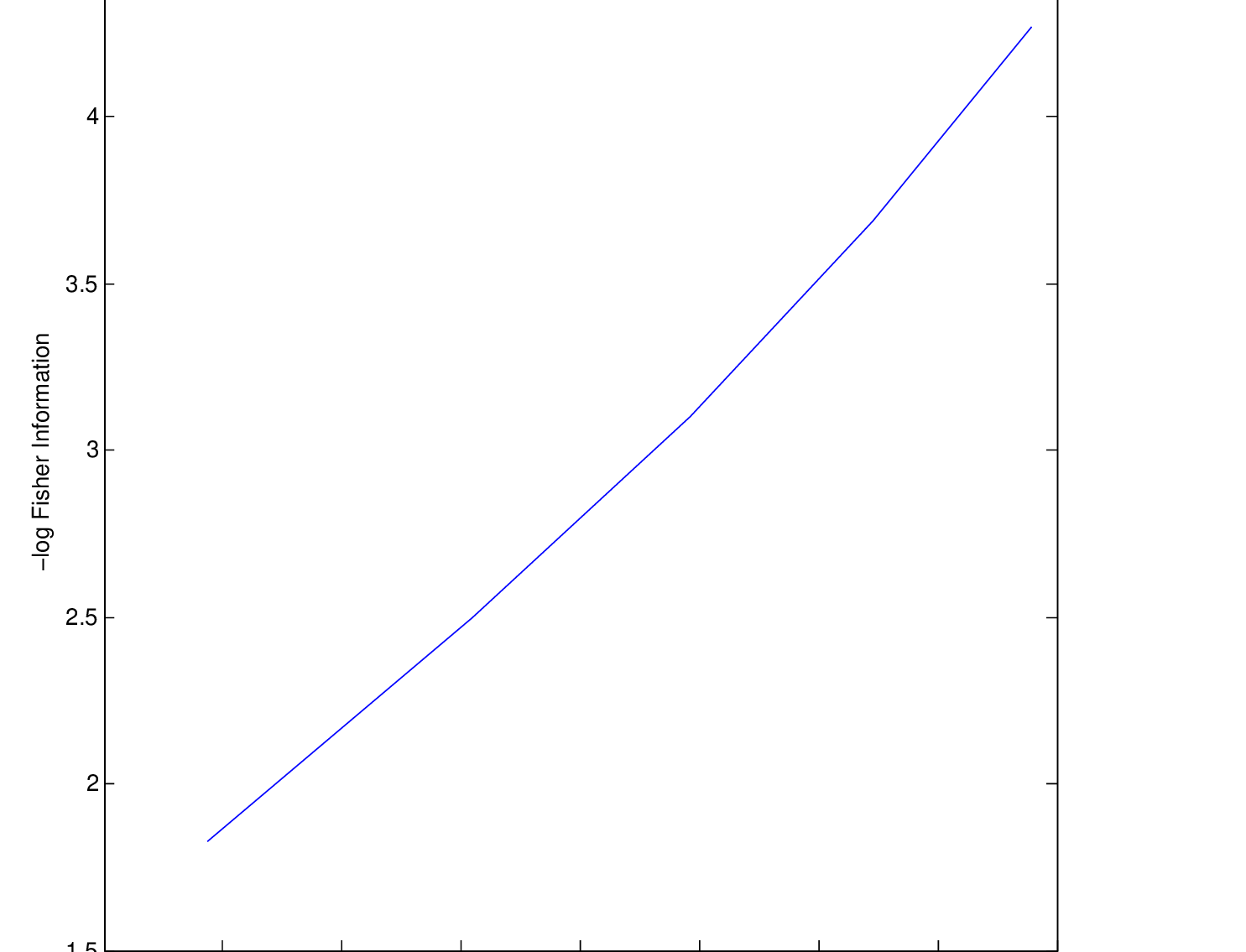

Finally we investigate the behaviour of the noisy ABC MLE. In the first graph in Figure 2 we plot the Fisher information matrix as a function of . The data suggests that for small the loss of information is . In the second graph we plot the log of the inverse of the Fisher information as a function of log . In this case the resulting data suggests that the Fisher information in the noisy ABC MLE decays as the inverse of the fourth power of for sufficiently large values of .

This second plot indicates that the Fisher information in the noisy ABC MLE decays as the fourth power of , at least for large values of . This suggests that in order for ABC MLE to provide accurate parameter estimates one must use relatively small values of . However this conflicts with the need to keep reasonably large in order to achieve computational stability. we note that even in this simple 1-D linear model we had to use large numbers of particles in our SMC algorithms to obtain accurate estimates of the ABC likelihoods for small values of . In higher dimensions this problem will be even worse as the volumes of the balls around the observations will decay even more quickly with than in the one dimensional case. This suggests that in order for ABC to become a truly practical statistical method one needs to find algorithms that can generate samples from arbitrarily small neighborhoods of a point in an efficient manner. One way in which this may be done is to marry ABC with techniques from the rapidly growing field of rare event simulation (see Rubino and Tuffin (2009) for a recent overview of this area).

8 Summary

In this article we have investigated the behaviour of the ABC and noisy ABC MLEs when used for estimating the parameters of HMMs. We have shown that mathematically these estimators should both be understood as being MLEs implemented using the likelihoods of a collection of perturbed HMMs. Using this insight we have shown that the standard ABC MLE has an innate asymptotic bias which can be made arbitrarily small by choosing a sufficiently small value of the parameter . Further we have shown that the noisy ABC MLE provides an asymptotically consistent estimator which is also, under certain conditions analogous to those for the MLE, asymptotically normal. Moreover this noisy version of the estimator has a loss of information relative to the MLE which manifests itself via an increase in the variance of the parameter estimates. Finally we have shown that under very mild conditions these results can be extended to smoothed versions of the standard and noisy ABC MLEs.

These theoretical results help to solidify and extend existing intuition associated to the approximations that have been considered. Further they suggest some possible avenues for future investigation. Firstly one would expect that the theoretical results in this paper will hold under much weaker assumptions than those presented here. The question of finding the necessary mathematical tools to relax these assumptions remains an interesting and important open problem. Secondly, the numerical results suggest that in order to provide an efficient and accurate method of parameter estimation ABC MLE will in practice need to be combined with computational techniques that allow one to generate samples effectively from sets with very small probabilities. The question of finding a generally applicable method of doing this is the topic of our current research.

Appendix A: Auxiliary Results

Here we present some supporting technical lemmas. The first result is a standard result from real analysis which we state without proof.

Lemma 5.

Suppose that there exists a function and sequence of continuously differentiable functions , , such that are bounded uniformly in and , uniformly in and the sequence is Cauchy uniformly in z. Then is itself uniformly bounded and continuously differentiable and uniformly in .

The second lemma is concerned with the identifiability of probability distributions under additive noise.

Lemma 6.

Let distributions and on for some be given and suppose that the characteristic function of is equal to zero on a set of Lebesgue measure zero. Then

Proof.

For any distribution we shall let denote the corresponding characteristic function. It is well known that for any pair of random variables and , and that if and only if for all . Thus we have that

∎

The following three Lemmas are well known results concerned with the connectedness of the support of a measure. We state them without proof.

Lemma 7.

Let a probability distribution on for some be given. Then for all the set

is measurable and

Lemma 8.

If the support of is connected then so is the support of the n-fold product measure for any .

Lemma 9.

Suppose that the support of a probability measure on is connected (see Section 2.1), then so is the support of the probability measure for any .

The next lemma shows that adding noise to an observation will, in general, result in a loss of information. The lemma after shows that for very large amounts of noise the loss in information will be almost complete.

Lemma 10.

Suppose that there exists a collection of distributions on some parameterised by and with densities with respect to some common finite dominating measure , and that the densities are differentiable w.r.t. . For all and let . Then for any and

| (24) |

where denotes the density of the distribution with respect to the finite dominating measure . Furthermore, if the supports of the distributions are all connected then we have equality in (24) if and only if both quantities are equal to the zero matrix.

Proof.

Let be given and let be a random variable distributed according to . Observe that given the quantity is equal to the density of the random variable (with respect to the appropriate dominating measure) where is an independent random variable and . By a straightforward application of the Fisher identity and the fact that one has that a.s. where denotes the joint density of the random variables from which it follows that for any , . Furthermore given we have that

| (25) |

Applying Jensen’s inequality to (25) yields

for all from which (24) immediately follows.

We now prove the second assertion. Since the mapping is strictly convex it further follows from Jensen’s inequality that for any ,

if and only if and hence is measurable. Thus equality holds in (24) if and only if is measurable for all which holds if and only if is measurable. Hence in order to prove the final part of the result it is sufficient to show that is measurable if and only if it is equal to zero a.s. Assume that is measurable. Then a.s.. Using the fact that one then has that

| (26) |

for a.s. all such that .

Suppose now that is not a.s. constant. Then there must exist and such that . It then follows from Lemma 7 that there must exist points and such that for all

| (27) |

Since the support of is connected there exists a continuous curve contained in the support of such that and . By the continuity of one can find a finite sequence of open balls of radius less than or equal to such that , , and such that for every , . Consider any two neighbouring balls and . From the above we have that is a.s. constant on and and that there exists some ball contained in with non zero mass and thus that is a.s. constant on . Hence it follows that is a.s. constant which contradicts the assumption that is not a.s. constant. Thus it follows that if is measurable that must be a.s. equal to some constant . Further, since it then follows that . Conversely if a.s. then clearly it is measurable. ∎

Lemma 11.

Suppose that there exists a collection of distributions on some parameterised by the parameter vector . Assume that for every the corresponding distribution has a density with respect to some common finite dominating measure , that the densities are continuously differentiable w.r.t. and that the corresponding score functions are uniformly bounded above in norm by some some . For all and let . Then for any and any sequence of positive real numbers such that

for all where denotes the density of the distribution with respect to the finite dominating measure .

Proof.

Let be given and let be a random variable distributed according to . As in the proof of Lemma 10 we observe that given the quantity is equal to the density of the random variable (again with respect to the appropriate dominating measure) where is an independent random variable with . Standard computations show that for any

where the last equality follows from the dominated convergence theorem by (A2), (A3), (A4) and (A5). Since it follows that for all . Hence the proof will follow once we establish that for any

| (28) |

Note that given any there exist and such that , and thus that for any we have that . Clearly if then and so the result follows. ∎

The following result establishes a stability-like property of the filter as the amount of noise in certain components of the observations becomes infinite. Before we state the result we recall the extended HMM defined in Section 6. Given a HMM and a perturbed version (see (7)) we define the extended HMM to be the joint process . In other words given a HMM and some the extended HMM is the process

| (29) |

where is such that for each , .

Lemma 12.

Let be a HMM which satisfies (A3) and let be the corresponding extended HMM defined in (29). Then for any , sequences , , any , and

| (30) | ||||

Proof.

Clearly we can assume that . Let , then using assumption (A3) and the well known identity

where is as in (6) it follows that in order to show (30) it is sufficient to show that for any and

| (32) |

In order to prove (32) it is sufficient, by assumption (A3), to show that for any

| (33) |

By assumption (A3) we have that for any there exists some such that for all

It then follows that given the above there exists some such that for all such that . Thus in order to prove (33) it is sufficient to show that for any , . However for any we have that

from which the result follows. ∎

The next five results are restatements of certain well-known stability properties of the filter.

Lemma 13.

Let be a HMM which satisfies (A3) and let the process be the corresponding extended HMM defined as in (29). Then for all , and such that , , all and all sequences

and

where .

Proof.

Corollary 1.

Let be a HMM which satisfies (A3) and let the process be the corresponding extended HMM defined as in (29). Then for all and infinite sequences and the conditional probability laws and exist and are well defined. Further for any

| (36) |

| (37) |

as .

Corollary 2.

Let be a HMM which satisfies (A3) and let be the corresponding extended HMM defined as in (29). Then for all , and such that , all and all sequences

| (38) |

where the constants are as in (A3) and the central quantity in (38) denotes the density of the corresponding conditional probability with respect to the dominating measure .

Proof.

To simplify the exposition we shall only give a proof of (38) for conditional probabilities of the form , the proof in the general case following in an identical manner.

Corollary 3.

Proof.

Let

It follows from (LABEL:lemFiltStabStandardeq2) that

The proof is completed by noting that the difference of the two expectations in (40) can be expressed as

∎

Remark 7.

Corollary 4.

Proof.

It is clear that and . By conditioning on and , the difference of the two expectations in the left hand-side of (41) can be expressed as

The result now follows by bounding the difference of the two conditional expectations in the integrand using (LABEL:extralabelforv510revisiontom3). ∎

Remark 8.

The next result establishes certain properties of the gradient of the filter conditioned on the infinite past, see Le Gland and Mevel (2000) or Tadić and Doucet (2005) for further information concerning the gradient of the filter.

Lemma 14.

Let be a parameterised collection of HMMs which satisfy (A3)-(A5) and let be the corresponding extended HMMs defined as in (29). Then for all where is as in assumptions (A4) and (A5) and every sequence of observations there exists an valued function in such that such that for all ,

| (42) | ||||

where is as in Lemma 13, is a global constant independent of and and denotes the gradient of the density of the conditional law w.r.t. .

Furthermore there exists such that for all , and

| (43) |

almost surely. Finally we have that for any

| (44) | ||||

where (44) defines a continuous function of on .

Proof.

We begin by proving (42) and (43). First note that since it is sufficient to prove the results component wise with respect to the vectors and we can assume that . For any suitable , , and

| (46) | ||||

| (49) |

By (A3), (A5), (41) and Remark 8 we have that for all , , , and such that that

| (50) | ||||

and

| (51) | ||||

where is as in Lemma 13, is as in Corollary 4 and are as in assumption (A3) and (A5). Further by (A3), (A5) and (40) it follows that for all , , and that

| (52) | ||||

It thus follows from (LABEL:lemGradFiltStabeq5)-(52) that for all that for all

| (53) | ||||

Further the first part of (43) follows from (LABEL:lemGradFiltStabeq5)-(49), (A3) and (A5), the uniform boundedness of the densities of conditional probability densities (Corollary 2) and Remark 7. Let be the constant bounding the first part of (43) and for any , and observations let

The functions are densities with respect to of a collection of (random) finite positive measures, each with total mass equal to and for which (53) clearly still holds. Since the space of positive finite measures equipped with the total variation norm is a Banach space (see e.g. Parthasarathy and Steerneman (1985)) it follows from (53) that given a doubly infinite sequence of observations there exists some positive finite measure such that for any

| (55) | ||||

It follows by definition that and thus from (55) that and that its density is bounded above by . Equation (42) and the second part of equation (43) now follow by letting . We shall prove (44) by, for any , applying Lemma 5 to the sequence of functions

| (56) |

for and arbitrary. Clearly the sequence of functions in (56) are continuously differentiable by and . In order to be able to apply Lemma 5 we further need to establish that the functions in (56) and their derivatives are uniformly bounded. This follows from (38) and (43), that

uniformly which follows from (36) and finally that the sequence of derivatives of the functions in (56) is uniformly Cauchy which follows from (42). ∎

Corollary 5.

Proof.

The first part of the corollary can be proved in exactly the same way as Lemma 14.

To prove the second part of the corollary it is sufficient to show that

| (58) |

for some and all , , , and . Inequality (58) can be established by decomposing the two gradients that appear on its left hand side in an analogous manner to (LABEL:lemGradFiltStabeq5)-(49). The bound on the right hand side then follows by bounding the terms in this decomposition individually using (50)-(52) and the fact that

| (59) |

for all , , , and which follows immediately from (LABEL:extralabelforv510revisiontom3). ∎

Appendix B: Proofs of Lemmas 1, 2, 3 and 4

Proof of Lemma 1.

We begin by observing that a straightforward consequence of assumption (A3) is that for all , and sequences

| (60) |

Further by Lemma 13 it follows that the finite history conditional likelihoods converge to the infinite history conditional likelihoods as uniformly in , , the sequence of observations and initial distribution . Thus by (60) it follows that in order to show continuity w.r.t. the first term and right continuity w.r.t. the second term of the mapping it is sufficient to show that these properties hold for the mapping

| (61) |

for all . For the rest of the proof we shall assume an arbitrary fixed and initial distribution are given. Observe that by (A2), (A3) Lemma 7 and the dominated convergence theorem the mapping is continuous w.r.t. its first term and right continuous w.r.t. its second term for all and . Thus by a second application of (A2), (A3) and the dominated convergence theorem one immediately obtains these properties of the mapping for any and sequence . A final application of (A2), (A3) and the dominated convergence theorem along with the inequality (60) yield that the mapping given in (61) is also respectively continuous and right continuous. In order to prove continuity w.r.t. the first term and right continuity w.r.t. the second term of (61) on we shall show for any sequences and , that

| (62) |

as . First note that

Thus in order to prove (62) it is sufficient to show that

| (63) |

and

| (64) |

as . We will now conclude the proof of the theorem by proving (63) and observing that the proof of (64) follows in a completely identical manner. The differences in the values of the likelihoods in (63) evaluated at different parameter values and can be bounded by

where is as in (A3) and (LABEL:thmprobconvpfeq7) follows from (A3), the definition of and the telescopic identity

which holds for any collection of reals . Clearly assumptions (A2) and (A3) and the dominated convergence theorem imply that the quantity in (LABEL:thmprobconvpfeq6) converges to zero as converges to . Furthermore the definition of and convergence of to imply that for any the limit supremum of (LABEL:thmprobconvpfeq7) as is bounded above by

where for all and

It then follows from (A3), (Proof of Lemma 1.), the dominated convergence theorem and the Lebesgue differentiation theorem (see Wheeden and Zygmund (1977), Chapter 10) that

| (68) | ||||

for any . Next we observe that by (A2) we have that for all and and hence that by applying (A3) and the dominated convergence theorem to (68) we have that

Thus it follows from (60), (LABEL:thmprobconvpfeq6), (LABEL:thmprobconvpfeq7) and (Proof of Lemma 1.) that for almost all sequences of observations that

| (70) |

Since

we have that (63) now follows from (60), (70), the Lebesgue differentiation theorem, (A3) and the dominated convergence theorem. ∎

Proof of Lemma 2.

We start by showing that is continuously differentiable. First observe that by (A3), (A4), (A5), (36), (38), (42), (43), (44) and the dominated convergence theorem we have that for arbitrary

| (71) |

uniformly in and and that the quantities in (71) are uniformly bounded. It follows from (71) that

and hence from (71) and Lemma 5 that exists, is continuous and is equal to . Since defined in (6) satisfies all the conditions laid out in (A3)-(A5), the same conclusion applies to . To prove the corresponding results for observe that by the Fisher information identity

Existence and continuity of then follows from (71) and Lemma 5 applied to the functions . Furthermore the fact that now follows from Douc, Moulines and Ryden (2004). We begin the proof of (12) by observing that from (71) and the identity we have that

and similarly, for any that

Thus it is sufficient to show that there exists some positive constant such that for any sequence , initial distribution and ,

| (72) |

For all , sequences and drawn from the original and perturbed processes respectively and

| (73) | ||||

In particular (73) holds true when and so (72) follows from (A3), (A5), (A6), (A7) and (43). ∎

Proof of Lemma 3.

Throughout this proof we shall assume that the density of any finite collection of random variables from and is computed assuming that the initial condition of the hidden state process has the stationarity distribution . We begin by observing that from Douc, Moulines and Ryden (2004) we have that

| (74) |

By the Fisher identity we have that for any and subsequences and that

| (75) |

Further by construction of the perturbed process one can easily show that given any and any subset that

| (76) |

Using (75) and (76) it follows that for any

and hence that

| (77) | ||||

Using (77) and (74) and stationarity we have that

where the last equality follows from assumptions (A3) and (A5) and equations (LABEL:lemFiltStabStandardeq2), (43) and (53). In addition, using (42) and the dominated convergence theorem, we conclude from (LABEL:lemasymmissinfeq2) that

| (79) | ||||

where for any sequence

| (80) | ||||

and

| (81) | ||||

Further by using assumptions (A3), (A5) and (LABEL:lemFiltStabStandardeq2), (42), (43) and (44) we have that the conditional likelihood functions and as well as their derivatives are bounded uniformly in and and that the derivatives are uniformly Cauchy in whilst the conditional likelihoods themselves converge uniformly to the quantities and . Hence we can apply Lemma 5 to obtain

| (82) |

It now follows from (79) and (82) that

Finally by applying the Fisher inequality (75) and (76) to the conditional laws and we get that

The result now follows from (Proof of Lemma 3.) and (Proof of Lemma 3.). ∎

Remark 9.

Assume (A1)-(A5). Then in exactly the same way as one proves Lemma 3 one may prove that

where for any pair of sequences and and any integer

| (85) | ||||

Proof of Lemma 4.

We begin by establishing part 1. From (24) and (Proof of Lemma 3.) we have for any and that from which the first assertion of part 1 immediately follows. In order to prove the second assertion of part 1 we note that it is sufficient to prove that under the assumption of connectivity we must have that implies . Since we have by Remark 9 that for all this will follow once we show that for all implies .

Observe that by Lemmas 8 and 9 and the assumption that is connected it follows that is connected for all and and thus from (A3) and (6) that the conditional laws and are also connected for all and sequences and . It then follows from (24) and (85) that for all that implies that

for all , a.s. and hence by Lemma 10 that

a.s. and thus by Fisher’s identity applied to the conditional probabilities that

| (86) |

a.s. also. Finally observe that one can derive expressions for the gradients of the conditional densities and analogous to (80) and (82). It then follows from these and (A3), (A5), (LABEL:extralabelforv510revisiontom3), (36), (37) and (57) that

| (87) |

a.s.. It now follows from (86) and (87) that if for all then a.s. and hence that .

Next we establish part 2. Recall that given a positive semi-definite matrix and a sequence of valued positive semi-definite matrices that if and only if for all . Thus in order to prove part 2 it is sufficient to show that for every sequence and every that . By definition and stationarity

and

| (89) |

Further by assumptions (A3) and (A5) and (43) we have that there exists some such that

| (90) |

a.s. for all and sequences . The proof of the second part of the result will follow from (Proof of Lemma 4.), (89) and (90) once we show that for any

| (91) |

as in probability. The first part of (91) is a straightforward consequence of applying Lemma 11 to the conditional laws . To establish the second part of (91) observe that from (LABEL:lemFiltStabStandardeq2), (42), (44), (82) and (80) we have that there exists some such that for all

| (92) |

for all , and . It then follows from (A3), (A5) and (43), the representation of the score functions given in (73), the representation of integrals w.r.t. the filter gradients given in (LABEL:lemGradFiltStabeq5)-(49) and Lemma 12 that

| (93) |

in probability as . One can then conclude that the second part of (91) holds via (92) and (93). In order to complete the proof of the lemma recall the two random variables and defined in (80) and (81). It follows from (A3), (A5) and the Lebesgue differentiation theorem that a.s. as . Since it follows from the proof of (82) that there exists some such that for all the functions and are bounded above by for all we have that part 3 follows from (Proof of Lemma 3.) and a simple application of the dominated convergence theorem. Finally, part 4 is a trivial consequence of (79), (80) and (81) and assumptions (A3), (A6) and (A7). ∎

References

- Andrieu, Doucet and Tadic (2009) {btechreport}[author] \bauthor\bsnmAndrieu, \bfnmC.\binitsC., \bauthor\bsnmDoucet, \bfnmA.\binitsA. and \bauthor\bsnmTadic, \bfnmV.\binitsV. (\byear2009). \btitleOn-line Parameter Estimation in General State Space Models Using Pseudo Likelihood \btypeTechnical report, \binstitutionDepartment of Statistics, University of Bristol. \endbibitem

- Beaumont, Zhang and Balding (2002) {barticle}[author] \bauthor\bsnmBeaumont, \bfnmM.\binitsM., \bauthor\bsnmZhang, \bfnmW.\binitsW. and \bauthor\bsnmBalding, \bfnmD.\binitsD. (\byear2002). \btitleApproximate Bayesian Computation in Population Genetics. \bjournalGenetics \bvolume162 \bpages2025–2035. \endbibitem

- Campillo and Rossi (2009) {barticle}[author] \bauthor\bsnmCampillo, \bfnmF.\binitsF. and \bauthor\bsnmRossi, \bfnmV.\binitsV. (\byear2009). \btitleConvolution Particle Filter for Parameter Estimation in General State-Space Models. \bjournalIEEE Trans. Aero. Elec. Sys. \bvolume45 \bpages1073–1072. \endbibitem

- Cappé, Rydén and Moulines (2005) {bbook}[author] \bauthor\bsnmCappé, \bfnmO.\binitsO., \bauthor\bsnmRydén, \bfnmT.\binitsT. and \bauthor\bsnmMoulines, \bfnmE.\binitsE. (\byear2005). \btitleInference in Hidden Markov Models. \bpublisherSpringer-Verlag: New York. \endbibitem

- Del Moral (2004) {bbook}[author] \bauthor\bsnmDel Moral, \bfnmP.\binitsP. (\byear2004). \btitleFeynman-Kac Formulae: Genealogical and Interacting Particle Systems with Applications. \bpublisherSpringer-Verlag: New York. \endbibitem

- Del Moral, Doucet and Jasra (2008a) {btechreport}[author] \bauthor\bsnmDel Moral, \bfnmP.\binitsP., \bauthor\bsnmDoucet, \bfnmA.\binitsA. and \bauthor\bsnmJasra, \bfnmA.\binitsA. (\byear2008a). \btitleAn Adaptive Sequential Monte Carlo Method for Approximate Bayesian Computation \btypeTechnical report, \binstitutionUniversity of Bristish Columbia. \endbibitem

- Del Moral, Doucet and Jasra (2008b) {btechreport}[author] \bauthor\bsnmDel Moral, \bfnmP.\binitsP., \bauthor\bsnmDoucet, \bfnmA.\binitsA. and \bauthor\bsnmJasra, \bfnmA.\binitsA. (\byear2008b). \btitleOn Adaptive Resampling Strategies for Sequential Monte Carlo Methods \btypeTechnical report, \binstitutionHAL-INRIA RR-6700. \endbibitem

- Douc, Moulines and Ryden (2004) {barticle}[author] \bauthor\bsnmDouc, \bfnmR.\binitsR., \bauthor\bsnmMoulines, \bfnmE.\binitsE. and \bauthor\bsnmRyden, \bfnmT.\binitsT. (\byear2004). \btitleAsymptotic Properties of the Maximum Likelihood Estimator in Autoregressive Models with Markov Regime. \bjournalAnn. Statist. \bvolume32 \bpages2254–2304. \endbibitem

- Doucet, De Freitas and Gordon (2001) {bbook}[author] \bauthor\bsnmDoucet, \bfnmA.\binitsA., \bauthor\bsnmDe Freitas, \bfnmJ. F. G.\binitsJ. F. G. and \bauthor\bsnmGordon, \bfnmN. J.\binitsN. J. (\byear2001). \btitleSequential Monte Carlo Methods in Practice. \bpublisherSpringer-Verlag: New York. \endbibitem

- Durbin et al. (1998) {bbook}[author] \bauthor\bsnmDurbin, \bfnmR.\binitsR., \bauthor\bsnmEddy, \bfnmS.\binitsS., \bauthor\bsnmKrogh, \bfnmA.\binitsA. and \bauthor\bsnmMitchison, \bfnmG.\binitsG. (\byear1998). \btitleBiological Sequence Analysis: Probabilistic Models of Proteins and Nucleic Acids. \bpublisherCUP: Cambridge. \endbibitem

- Fearnhead and Prangle (2010) {btechreport}[author] \bauthor\bsnmFearnhead, \bfnmP.\binitsP. and \bauthor\bsnmPrangle, \bfnmD.\binitsD. (\byear2010). \btitleSemi-automatic approximate Bayesian Computation. \btypeTechnical report, \binstitutionUniversity of Lancaster. \endbibitem

- Felsenstein and Churchill (1996) {barticle}[author] \bauthor\bsnmFelsenstein, \bfnmJ.\binitsJ. and \bauthor\bsnmChurchill, \bfnmG. A.\binitsG. A. (\byear1996). \btitleA Hidden Markov Model Approach to Variation Among Sites in Rate of Evolution. \bjournalMol. Biol. Evol. \bvolume13 \bpages93–104. \endbibitem

- Ferguson (1982) {barticle}[author] \bauthor\bsnmFerguson, \bfnmT. S.\binitsT. S. (\byear1982). \btitleAn Inconsistent Maximum Likelihood Estimate. \bjournalJ. Amer. Statist. Assoc. \bvolume77 \bpages831–834. \endbibitem

- Gourieroux, Monfort and Renault (1993) {barticle}[author] \bauthor\bsnmGourieroux, \bfnmC.\binitsC., \bauthor\bsnmMonfort, \bfnmA.\binitsA. and \bauthor\bsnmRenault, \bfnmE. S.\binitsE. S. (\byear1993). \btitleIndirect Inference. \bjournalJ. Appl. Econometrics \bvolume8 \bpages85–118. \endbibitem

- Heggland and Frigessi (2004) {barticle}[author] \bauthor\bsnmHeggland, \bfnmK.\binitsK. and \bauthor\bsnmFrigessi, \bfnmA.\binitsA. (\byear2004). \btitleEstimating functions in indirect inference. \bjournalJ. Roy. Statist. Soc. Ser. B \bvolume66 \bpages447–462. \endbibitem

- Jasra et al. (2010) {barticle}[author] \bauthor\bsnmJasra, \bfnmA.\binitsA., \bauthor\bsnmSingh, \bfnmS. S.\binitsS. S., \bauthor\bsnmMartin, \bfnmJ. S.\binitsJ. S. and \bauthor\bsnmMcCoy, \bfnmE.\binitsE. (\byear2010). \btitleFiltering via Approximate Bayesian Computation. \bjournalStat. Comput,. \endbibitem

- Kim, Shephard and Chib (1998) {barticle}[author] \bauthor\bsnmKim, \bfnmS.\binitsS., \bauthor\bsnmShephard, \bfnmN.\binitsN. and \bauthor\bsnmChib, \bfnmS.\binitsS. (\byear1998). \btitleStochastic Volatility: Likelihood Inference and Comparison with ARCH Models. \bjournalRev. Econom. Stud. \bvolume65 \bpages361–393. \endbibitem

- Le Gland and Mevel (2000) {barticle}[author] \bauthor\bsnmLe Gland, \bfnmF.\binitsF. and \bauthor\bsnmMevel, \bfnmL.\binitsL. (\byear2000). \btitleExponential Forgetting and Geometric Ergodicity in Hidden Markov Models. \bjournalMath. Control Signals Systems \bvolume13 \bpages63–93. \endbibitem

- McKinley, Cook and Deardon (2009) {barticle}[author] \bauthor\bsnmMcKinley, \bfnmJ.\binitsJ., \bauthor\bsnmCook, \bfnmC.\binitsC. and \bauthor\bsnmDeardon, \bfnmR.\binitsR. (\byear2009). \btitleInference for Epidemic Models Without Likelihooods. \bjournalIntl. J. Biostat. \bvolume5. \endbibitem

- Orchard and Woodbury (1972) {binproceedings}[author] \bauthor\bsnmOrchard, \bfnmT.\binitsT. and \bauthor\bsnmWoodbury, \bfnmM. A.\binitsM. A. (\byear1972). \btitleA Missing Information Principle: Theory and Applications. In \bbooktitleProc. Sixth Berkeley Symp. Math. Stat. Prob. \bpages697–715. \endbibitem

- Parthasarathy and Steerneman (1985) {barticle}[author] \bauthor\bsnmParthasarathy, \bfnmK. R.\binitsK. R. and \bauthor\bsnmSteerneman, \bfnmT.\binitsT. (\byear1985). \btitleA Tool in Establishing Total Variation Convergence. \bjournalTrans. Amer. Math. Soc. \bvolume95 \bpages626–630. \endbibitem

- Peters, Wüthrich and Shevchenko (2010) {barticle}[author] \bauthor\bsnmPeters, \bfnmG.\binitsG., \bauthor\bsnmWüthrich, \bfnmM. W.\binitsM. W. and \bauthor\bsnmShevchenko, \bfnmP.\binitsP. (\byear2010). \btitleChain Ladder Method: Bayesian Bootstrap Versus Classical Bootstrap. \bjournalInsurance Math. Econom. \bvolume47 \bpages36–51. \endbibitem

- Pritchard et al. (1999) {barticle}[author] \bauthor\bsnmPritchard, \bfnmJ. K.\binitsJ. K., \bauthor\bsnmSeielstad, \bfnmM. T.\binitsM. T., \bauthor\bsnmPerez-Lezaun, \bfnmA.\binitsA. and \bauthor\bsnmFeldman, \bfnmP.\binitsP. (\byear1999). \btitlePopulation Growth of Human Y Chromosome Microsatellites. \bjournalMol. Biol. Evol. \bvolume16 \bpages1791–1798. \endbibitem

- Rachev and Mittnik (2000) {bbook}[author] \bauthor\bsnmRachev, \bfnmS. T.\binitsS. T. and \bauthor\bsnmMittnik, \bfnmS.\binitsS. (\byear2000). \btitleStable Paretian Models in Finance. \bpublisherWiley. \endbibitem

- Ratmann et al. (2009) {barticle}[author] \bauthor\bsnmRatmann, \bfnmO.\binitsO., \bauthor\bsnmAndrieu, \bfnmC.\binitsC., \bauthor\bsnmWiuf, \bfnmC.\binitsC. and \bauthor\bsnmRichardson, \bfnmS.\binitsS. (\byear2009). \btitleModel Criticism Based on Likelihood-Free Inference, with an Application to Protein Network Evolution. \bjournalProc. Natl. Acad. Sci. USA \bvolume106 \bpages10576–10581. \endbibitem

- Rubino and Tuffin (2009) {bbook}[author] \bauthor\bsnmRubino, \bfnmG.\binitsG. and \bauthor\bsnmTuffin, \bfnmB.\binitsB. (\byear2009). \btitleRare Event Simulation using Monte Carlo Methods. \bpublisherWiley. \endbibitem

- Samorodnitsky and Taqqu (1994) {bbook}[author] \bauthor\bsnmSamorodnitsky, \bfnmG.\binitsG. and \bauthor\bsnmTaqqu, \bfnmM. S.\binitsM. S. (\byear1994). \btitleStable Non-Gaussian Random Processes. \bpublisherChapman & Hall, New York. \endbibitem

- Sisson and Fan (to be published) {bincollection}[author] \bauthor\bsnmSisson, \bfnmS.\binitsS. and \bauthor\bsnmFan, \bfnmY.\binitsY. (\byearto be published). \btitleLikelihood-Free Markov Chain Monte Carlo. In \bbooktitleBrooks, S. P., Gelman, A., Jones, G. and Meng X.L. (Eds); Handbook of Markov Chain Monte Carlo \bpublisherChapman & Hall: London. \endbibitem

- Tadić and Doucet (2005) {barticle}[author] \bauthor\bsnmTadić, \bfnmV.\binitsV. and \bauthor\bsnmDoucet, \bfnmA.\binitsA. (\byear2005). \btitleExponential Forgetting and Geometric Ergodicity for Optimal Filtering in General State Space Models. \bjournalStochastic Process. Appl. \bvolume115 \bpages1408–1436. \endbibitem

- Tavre et al. (1997) {barticle}[author] \bauthor\bsnmTavre, \bfnmS.\binitsS., \bauthor\bsnmBalding, \bfnmD. J.\binitsD. J., \bauthor\bsnmGriffiths, \bfnmR. C.\binitsR. C. and \bauthor\bsnmDonnelly, \bfnmP.\binitsP. (\byear1997). \btitleInferring Coalescence Times From DNA Sequence Data. \bjournalGenetics \bvolume145 \bpages505–518. \endbibitem

- Wheeden and Zygmund (1977) {bbook}[author] \bauthor\bsnmWheeden, \bfnmR. L.\binitsR. L. and \bauthor\bsnmZygmund, \bfnmA.\binitsA. (\byear1977). \btitleMeasure and Integral; An Introduction to Real Analysis. \bpublisherMarcel Dekker, New York. \endbibitem

- White (1982) {barticle}[author] \bauthor\bsnmWhite, \bfnmH.\binitsH. (\byear1982). \btitleMaximum Likelihood Estimation of Misspecified Models. \bjournalEconometrica \bvolume50 \bpages1–25. \endbibitem

- Wilkinson (2008) {barticle}[author] \bauthor\bsnmWilkinson, \bfnmR. D.\binitsR. D. (\byear2008). \btitleApproximate Bayesian Computation (ABC) Gives Exact Results Under Model Error. \bjournalBiometrika \bvolume20 \bpages1–13. \endbibitem