Option Pricing from Wavelet-Filtered Financial Series

Abstract

We perform wavelet decomposition of high frequency financial time series into large

and small time scale components. Taking the FTSE100 index as a case study, and working

with the Haar basis, it turns out that the small scale component defined by most

( ) of the wavelet coefficients can be neglected for the purpose of

option premium evaluation. The relevance of the hugely compressed information provided

by low-pass wavelet-filtering is related to the fact that the non-gaussian statistical structure

of the original financial time series is essentially preserved for expiration times which are larger

than just one trading day.

Keywords: Dynamical hedging; Non-gaussian markets; Financial time series analysis.

I Introduction

The problem of option pricing bouch-pott ; mant-stan ; voit has been a main topic of investigation in much of the econophysics literature, challenged by the well-known inadequacy of the standard Black-Scholes model to the real world bouch-pott ; mant-stan ; voit ; matacz ; borland ; lmori . Options are an imperative element in modern markets, since they play a fundamental role, as convincingly shown long ago by Black and Scholes, in reducing portfolio risk. As an alternative to the Black-Scholes model, one of the authors has implemented an option pricing scheme which is based on the evaluation of statistical averages taken over samples generated from the underlying asset log-return time series lmori . This method, which we will refer to as “Empirical Option Pricing” (EOP), has been succesfully validated through a careful study of FTSE100 options.

A deeper understanding of the statistical features of financial time series is in order, since this would eventually allow us to replace real samples by accurate synthetic financial series, improving the statistical ensembles used in EOP. As a closely related issue, our aim in this work is to show that financial series can be hugely compressed (we mean lossy compression, in the information theoretical sense) by wavelet-filtering, without spoiling option premium evaluation by EOP. The low-pass wavelet-filtered signal contains log-return fluctuations defined on time scales larger than a few hours and it is likely to yield, due to its high compression rate, a more suitable ground for modeling and synthetization.

This paper is organized as follows. Secs. II and III provide brief accounts, respectively, of the EOP method and of the low-pass wavelet-filtering procedure that has been applied to our analysis of the FTSE100 index. The wavelet-filtered financial series, which keeps only of the total number of wavelet components of the original signal is noted to encode the essential statistical information needed for a consistent evaluation of FTSE100 option premiums with expiration times larger than a single trading day. In Sec. IV, we summarize our findings and point out directions of further research.

II Empirical Option Pricing (EOP)

We rephrase here, without paying much attention to rigorous considerations, the main points of EOP lmori . Let be an arbitrary financial index modeled as a continuous stochastic process. More precisely, we write down a Langevin evolution equation for , which is a simple generalization of the one underlying the Black-Scholes model hull ; wilm_etal :

| (1) |

Above, and are the time-dependent interest rate and volatility of the index . The stochasticity of the financial time series comes from the gaussian white noise process appearing in Eq. (1), which satisfies to

| (2) |

Observe that both and may be regarded as stochastic process as well, with fluctuations correlated on time scales which are much larger than the correlation time of .

Working within the Itô prescription, Eq. (1) can be readily rewritten as

| (3) |

where

| (4) |

with

| (5) |

Above, is just the spot price of the index. We are interested, now, to evaluate the premium of an european option which is negotiated with strike price and expiration time . Similarly to what is done in the Black-Scholes treatment, where and are constant, the option premium (for, say, call options) can be obtained from the computation of the statistical average

| (6) |

where is replaced by , the risk-free interest rate, in the definition of provided by Eqs. (4) and (5).

For stochastic processes defined in discrete time, with time step , like real financial time series, Eq. (3) can be replaced by the finite difference equation

| (7) |

where

| (8) |

and is an arbitrary element of a discrete gaussian stochastic process, defined by and . From (7), we get, immediately,

| (9) |

and, therefore,

| (10) |

where time instants are given by , with .

Substituting, now, (4) and (5) (with replaced by ) in (6), we get

| (11) | |||||

It is important to note that , which appears in the above expressions is, from Eq. (4), nothing more than an element of the detrended log-return series, i.e.,

| (12) |

where , due to Eq. (3).

We are now ready to summarize EOP in the four following steps:

(i) A large period ( two years) of reasonably statistically stationary high-frequency (minute-by-minute) log-return series of the underlying asset is “purified” by the remotion of outlier events (typically, log-return fluctuations which are larger than 10 standard deviations) and of the mean one-week asset’s interest rate (detrending). The resulting series is a stochastic process ;

(ii) Since the historical volatility is in general different from the volatility of the financial series during the option lifetime , we introduce a correction factor to define the stochastic process , which yields a putative volatility for that period comment . The -factor is the only adjustable parameter in EOP, which accounts for the distinction between the past and the future behaviors of the financial index .

(iii) An ensemble of samples, each of length ( minute) is defined from one-hour translations of the initial sequence , , …, . In other words,

| (13) |

where and ;

(iv) Option premiums are computed from (6), (11) and (12), with statistical averages taken over the ensemble , defined in (13). We note, furthermore, that the optimal value for the -factor is found through the least squares method, devised for the comparison between the market and modeled option premiums.

A good agreement has been attained between the market and EOP values in a detailed study of the FTSE100 index options lmori . The comparison data is reported in the MKT and OP columns of Table I.

The performance of EOP would benefit greatly from the use of synthetic financial series which would enlarge the ensemble of samples . Thus, one may wonder, having modeling aims in mind, on what are the relevant statistical facts hidden in the financial time series. The essential question we address is, accordingly, whether the financial series be decomposed into relevant and irrelevant contributions, as far as option pricing is concerned. In the next section, we recall some ideas on wavelet-filtering, which have been crucial in the investigation of this issue.

III Wavelet-Filtering and EOP

Log-return fluctuations are constantly affected by avalanches of market orders which have to do with speculative trends, and are clearly time-localized events. These features render the financial time series suggestively adequate for wavelet analysis.

Since there is no requirement of continuity for the log-return time series, we have chosen, due to easiness of handling, to work with Haar wavelets walker . In the same way as for any other discrete wavelet basis, the Haar wavelets are labelled by two integer indices and and are given by

| (14) |

where

| (15) |

is the function known as “mother wavelet”. Observe that the above basis functions are defined in the domain .

| Strike | 02dec05 () | 06dec05 () | 09dec05 () | ||||||

| Price | MKT | OP | MKT | OP | MKT | OP | |||

| 410.5 | 412.67 | 413.00 | X | X | X | X | X | X | |

| 312 | 312.79 | 313.12 | 324 | 321.87 | 322.25 | 298 | 297.51 | 297.74 | |

| 214.5 | 213.94 | 214.19 | 225.5 | 222.87 | 223.15 | 199 | 197.72 | 197.87 | |

| 122.5 | 121.93 | 122.17 | 131.5 | 129.48 | 129.65 | 103.5 | 102.35 | 102.20 | |

| 50 | 48.61 | 48.55 | 53.5 | 53.52 | 53.41 | 29.5 | 29.72 | 29.15 | |

| 13 | 13.01 | 13.00 | 12.5 | 14.97 | 14.90 | 3.5 | 4.79 | 4.65 | |

| 2.5 | [0.60] | 0.60 | 2 | 1.66 | 1.65 | 0.5 | 0.35 | 0.29 | |

| 0.5 | [0.0] | 0.0 | X | X | X | X | X | X | |

| Strike | 19dec05 () | 03jan06 () | 12jan06 () | ||||||

| Price | MKT | OP | MKT | OP | MKT | OP | |||

| 329.5 | 332.38 | 333.05 | X | X | X | X | X | X | |

| 234.5 | 237.49 | 237.64 | 368.5 | 368.36 | 368.84 | 414 | 414.96 | 415.12 | |

| 148 | 149.46 | 150.09 | 271 | 268.86 | 269.30 | 314 | 315.02 | 315.18 | |

| 76 | 77.75 | 77.97 | 177 | 176.67 | 174.97 | 215 | 215.09 | 215.25 | |

| 28.5 | 30.91 | 31.09 | 93 | 91.20 | 91.40 | 119 | 116.81 | 116.81 | |

| 8 | [5.18] | 5.09 | 34.5 | 34.40 | 34.44 | 40 | 34.72 | 34.38 | |

| 2.5 | [0.60] | 0.54 | 9 | 8.41 | 8.39 | 5.5 | 4.51 | 4.36 | |

| 0.5 | [0.0] | 0.0 | 2 | [0.19] | 0.18 | 0.5 | 0.20 | 0.16 | |

| X | X | X | 0.5 | [0.0] | 0.0 | X | X | X | |

The detrended log-return series of length and zero mean comment2 can always be expanded in wavelet modes as

| (16) |

Low-pass wavelet-filtering can be straightforwardly implemented from the expansion (16) by retaining the modes which have the scale index , where is an arbitrarily fixed threshold. We have taken (following the prescriptions given in step (i) of EOP, as discussed in Sec. II) a financial time series of 241664 minutes (around two years of data) for the the FTSE100 index, ending on 17th november, 2005. The series is partitioned into 59 subseries, each of length 4096 (corresponding to and about two weeks of market activity), which are then wavelet-filtered with threshold parameter (compression rate of ).

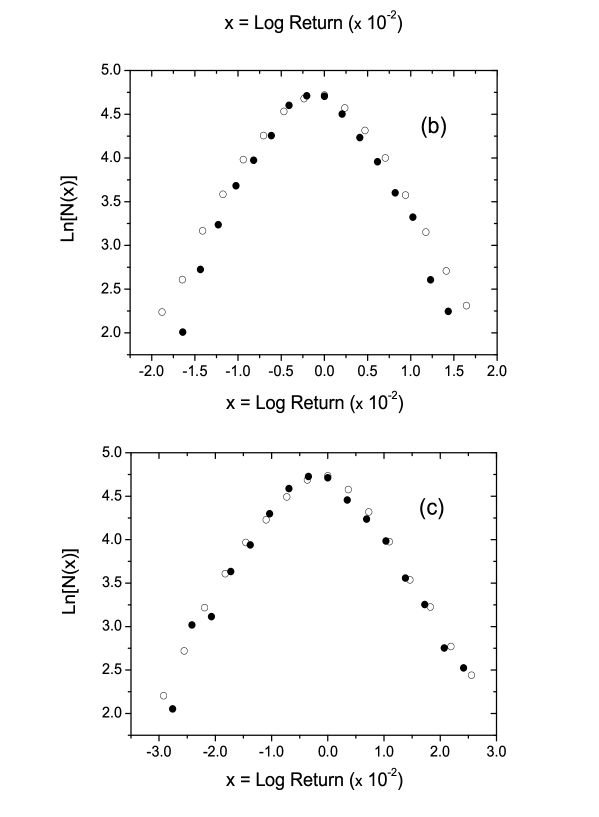

Since wavelets with have zero mean, we expect that the histograms of log-returns will not be much affected for time horizons minutes. This is actually verified in Fig. 1. Therefore, on the grounds of Eq. (11), it is clear that option prices can be alternatively estimated through the use of the low-pass wavelet filtered series within EOP for time horizons which are larger than one trading day ( minutes).

In Table I, we report the computed premiums for call options based on the FTSE100 index with expiration times ranging from a few days to one month, in december 2005 and january 2006. The agreement between the original and the wavelet-filtered option premium evaluations is significative. It is important to recall, as already indicated in Ref. lmori , that the Black-Scholes framework is unable to yield good estimates of the market option premiums listed in Table I.

IV Conclusions

We have found, taking the FTSE100 index as a case study, that its high frequency (minute-by-minute) time series can be highly compressed for the purpose of option pricing. The original and the low-pass wavelet-filtered series have remarkably similar performances within EOP, even for a compression rate of , which means that only 967 out of the original 241664 wavelet components have been selected throught the wavelet-filtering procedure. The retained wavelet coefficients have scale index smaller than the fixed threshold and are associated to log-return fluctuations defined on time scales larger than a few hours. It turns out, thus, that one is entitled to use the filtered time series to precify FTSE100 options with expiration times which are larger than just one trading day, where log-returns are still clearly non-gaussian random variables. A promising approach to option pricing, deserved for further investigation, is to address the problem of series synthetization from the analysis of the statistical properties of the compressed wavelet-filtered financial indices directly in wavelet space, in a spirit similar to what is done in the context of artificial multrifractal series arneodo_etal2 . It is likely that EOP would, then, be considerably improved from the use of much larger synthetic statistical ensembles.

Acknowledgements.

This work has been partially supported by CNPq and FAPERJ. The authors would also like to thank an anonimous referee for a number of insightful comments, which have been of fundamental importance in shaping the final form of this work.References

- (1) J.P. Bouchaud and M. Potters, Theory of Financial Risks - From Statistical Physics to Risk Management, Cambridge University Press, Cambridge (2000).

- (2) R. Mantegna and H.E. Stanley, An Introduction to Econophysics, Cambridge University Press, Cambridge (2000).

- (3) J. Voit, The Statistical Mechanics of Financial Markets, Springer-Verlag (2003).

- (4) A. Matacz, Int. J. Theor. Appl. Finance 3, 143 (2000).

- (5) L. Borland, Phys. Rev. Lett. 89, 098701 (2002); Quant. Fin. 2, 415 (2002).

- (6) L. Moriconi, Physica A 380, 343 (2007).

- (7) J. Hull, Options, Futures and Other Security Derivatives, Prentice Hall, New Jersey (1993).

- (8) P. Wilmott, S. Howison, and J. Dewinne, The Mathematics of Financial Derivatives, Cambridge University Press, Cambridge (1995).

- (9) Whenever volatilities are given in percentual amounts, throughout the paper, we mean the “annualized volatilities”, defined by , where is the standard deviation of the minute-by-minute log-return financial series (we assume 252 trading days per year, and 8.5 market hours per day).

- (10) J.S. Walker, A Primer on Wavelets and Their Scientific Applications, Chapman Hall/CRC (1999).

- (11) Our real detrended samples have some residual mean values, which are, in practice, neglegible for all purposes in EOP (see the second column in table III). In the general case, an additional wavelet basis function , for , is included in the expansion (16).

- (12) A. Arnéodo, E. Bacry, and J.-F. Muzy, J. Math. Phys. 39, 4163 (1998).