Application of Mathematical Optimization Procedures to Intervention Effects in Structural Equation Models

Kentaro Tanaka,

Department of Industrial Engineering and Management,

Graduate School of Decision Science and Technology,

Tokyo Institute of Technology, Japan. tanaka.k.al@m.titech.ac.jp

Atsushi Yagishita,

Specialty Tire Process Engineering Development Department,

Bridgestone Corporation, Japan. and

Masami Miyakawa,

Department of Industrial Engineering and Management,

Graduate School of Decision Science and Technology,

Tokyo Institute of Technology, Japan.

Abstract

For a given statistical model,

it often happens that it is necessary to

intervene the model to reduce the variances of the output variables.

In structural equation models, this can be done by changing the values of

the path coefficients by intervention.

First, we explain that the expectations and variance matrix can be decomposed into several parts in terms of the total effects.

Then, we show that an algorithm to obtain intervention method which minimizes the weighted sum of the variances

can be formulated as a convex quadratic programming.

This formulation allows us to impose boundary conditions for the intervention, so that we can find the practical solutions.

We also treat a problem to adjust the expectations on targets.

Key words: Convex quadratic programming; Structural equation models; Total effects.

1 Introduction

The methods of structural equation models (SEMs) developed

by geneticists (Wright (1923)) and economists (Haavelmo (1943) and Koopmans (1949))

are widely used as analytical tools in a lot of fields including genetics, econometrics, social sciences and statistical quality control.

To meet the demands of the practical researchers,

thousands of studies on parameter estimation and model fitting for structural equation models have been made.

However, structural equation models are more than tools for analysis.

We can use structural equation models as tools to represent the causal relationships between the variables (Pearl (2009)).

If we intervene a part of the causal structure,

then the overall causal structure changes.

By using the structural equation model that represents the correct causal relationships,

we can evaluate the amount of change caused by the intervention.

This means that we can compute the optimal intervention method

to minimize the variance of a variable.

Kuroki and Miyakawa (2003), Kuroda et al. (2006) and Kuroki (2008)

evaluated the intervention effect for the variance of a variable

and give some methods to obtain the optimal intervention that minimizes the variance.

However, it is difficult to use their methods in practice

because they implicitly uses the impractical assumption

that the intervention can be made freely without any constraint

(e.g. we may have a bound for an intervention by changing a parameter of a structural equation because of the cost to change it).

In this paper,

we formulate the problems to obtain the optimal intervention that minimizes the variances

and to adjust the expectations as convex quadratic programmings.

This formulation enables us to easily impose boundary conditions for interventions.

To this purpose, we first introduce some ideas of decomposition of total effects in Section 2.

Note that the term “decomposition of total effects”

means not only decomposition of total effects into direct and indirect effects,

but also decomposition by paths or set of variables.

We also explain that the expectations and variance matrix can be decomposed into several parts in terms of the total effects.

In Section 3,

we show that the problem to obtain the optimal intervention that minimizes the variances can be formulated as a convex quadratic programming.

We also treat a problem to adjust the expectations.

Next, in Section 4,

we show how the proposed algorithms given in Section 3

work by using a toy model.

Finally, we give some discussion in Section5.

2 Decomposition of total effects and Interventions

First, in Section 2.1,

we briefly mention structural equation models and path diagrams, and then introduce some notations.

Next, in Section 2.2,

we introduce matrix representation of total effects and their decomposition.

The idea of decomposition of total effects is very important to consider the optimal intervention

which we will treat in Section 3.

Finally, in Section 2.3,

we explain the interventions to the structural equation models.

2.1 Structural Equation Models

The models that the relations among random variables are described in terms of linear equations are called structural equation models.

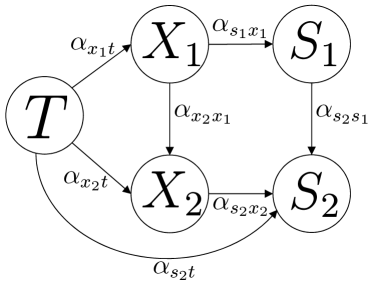

To give some explanations about terms and notations, let us consider an example of structural equation model.

Example 1.

Assume that six random variables , , , and are generated by the following linear structural equations:

where:

•

are the intercepts;

•

are proportionality coefficients called path coefficients;

•

are the

error terms.

We will soon explain the meanings of subscripts such as .

Figure 1: An example of path diagram

In the above equations, we presume that each left-hand side is determined by the right-hand side,

i.e. right-hand sides are causes and left-hand sides are the results.

If we represent a causal effect by an arrow with its path coefficient,

then the relations among the random variables , , , and

can be graphically represented as Figure 1.

This graph is called the path diagram.

The arrow from to means presumed direct causal effect from to .

For this arrow, is said to be parent of .

Conversely, is said to be child of .

These are graph theoretic terms.

Here, has two parents and , and we denote them by as an abbreviation for parents of .

Furthermore, we denote by removing the effect of .

Thus, represents the mean of when the effects of the parents of are removed.

We also use terms ancestor and descendant as graph theoretic terms.

For example, the ancestors of are and ,

and the descendants of are , and .

∎

We now formulate the general structural equation model in a way

so that it is easier to use for the calculations of total effects, means and variances

which we will treat in Section 2.2.

Consider a random vector the elements of which are generated by linear structural equations.

We divide the random vector into three disjoint parts: , and ,

so that the elements of are the ancestors of some elements of

and the elements of are not the ancestors of some elements of nor some elements of themselves.

This decomposition is uniquely determined if once we choose .

Now, a structural equation model can be represented by using vectors and matrices as follows:

(1)

Here, , and are the means of , and , respectively

when the effects of their parents are removed;

, , , are the matrices which consist of the path coefficients;

and , and are the error terms.

We assume that the means of are all zero values

and have the variance matrices , and respectively.

Furthermore, to avoid cycles in the structural equations,

we assume that the elements in diagonal and upper triangular portion of the coefficients matrices , and are all zero values.

This formulation is possible by sorting the variables by their parent-child relations whenever the structural equations do not contain cycles.

For example, the equations in Example 1 can be formulated in the form of (1)

by letting

, and ,

where the matrices of the path coefficients are as follows:

2.2 Total Effects, Means and Variances

For a given structural equation model,

the total effect from a variable to a variable which is one of the descendants of

is defined as the change in that is produced

when is increased by and all error terms are fixed to .

Therefore the total effect from to is equal to

the derivative of with respect to

for the structural equations eliminating all error terms.

The direct effect from to

is defined as the path coefficient from to

and it coincides with the partial derivative of with respect to

for the structural equations eliminating all error terms.

The indirect effect from to

is defined as the total effect minus the direct effect.

For the precise and general definitions of the terms such as direct, indirect and total effects,

see Bollen (1987), Bollen (1989), Sobel (1990) and Pearl (2009).

Let us consider the following example.

Example 2.

In Example 1, the total effect from to is calculated as follows.

We obtain the following equations by eliminating all error terms in structural equations in Example 1.

From the above equations, we obtain the following relation between and

when all error terms are fixed to .

Therefore the total effect from to is equal to

.

The total effect can be decomposed into direct and indirect effects.

First, the direct effect is which is the path coefficient of .

The remainder

is the indirect effect and the terms

,

and

correspond respectively to the effects of the paths

,

and

from the front.

∎

Let us denote the total effect from to by .

Furthermore, let us denote the matrix of the total effects from to by

where and -element of is the total effect from to .

Proposition 1.

(Bollen (1987), Sobel (1990))

Assume that the structural equations for are written in the equation

.

Furthermore, we assume that is invertible

where is the identity matrix.

Then the matrix of the total effect is given by .

Note that always exists in the model of (1).

Intuitively, the elements of represents the direct effects

and the elements of represents the indirect effects through one variable.

In the same way, the elements of can be considered as the indirect effects through variable.

Therefore, the total effect is equal to

and the above proposition holds.

In the next example,

we treat a decomposition of a total effect

and introduce some useful notations for the calculations of means and variances of which we will treat later in this section.

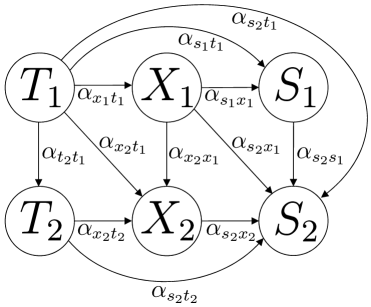

Example 3.

Assume that six random variables , , , , and are generated by the following linear structural equations:

The path diagram of the above linear structural equations is given in Figure 2.

Figure 2: An example of path diagram with six variables

The above equations can be formulated in the form of (1)

by letting

, and ,

where the matrices of the path coefficients are as follows:

In this model,

the total effect from to is calculated as follows:

Furthermore, the total effect from to is decomposed into the following eight paths:

(2)

In the above paths, only the first path represents

the direct effect with the value of

and the other paths represent indirect effects with the values of

, , , , , and ,

respectively.

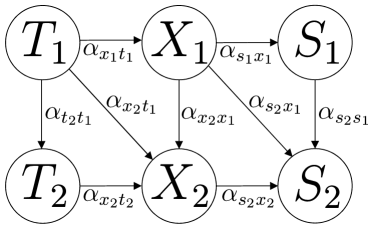

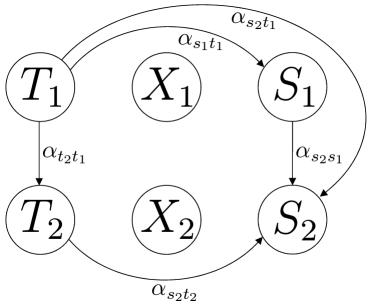

Figure 3: A path diagram when the direct paths from to are removed.Figure 4: A path diagram when the paths through are removed.

Now,

we decompose the total effect from to into the following two parts.

1.

Let us denote by

the total effect from to through .

Because the last five paths in (2)

go through and ,

we obtain

This is equal to the total effect from to in the model of Figure 3.

2.

Let us denote by

the total effect from to when the effect of are removed.

From the above decomposition, the first three paths in (2)

do not go through and .

Therefore, we obtain

This is equal to the total effect from to in the model of Figure 4.

Next, let us consider the following two matrices

where and are the identity matrices.

Then we obtain

and

Note that the -elements of and ,

which corresponds to ),

are equivalent to and .

This equivalence can be justified as Theorem 1.

∎

As in Example 3, we define the following two matrices for the model of (1):

(3)

(4)

where and are the identity matrices.

The next lemma can be shown by direct calculation.

Lemma 1.

Let be a square matrix which can be represented as follows:

where are square matrices.

If are non-singular matrices,

then the following equation holds for the inverse matrix of .

∎

In the next theorem, we obtain the matrix representations of total effects

from to , from to and from to ,

and justify the decomposition of the total effect which is treated in Example 3.

Theorem 1.

(5)

(6)

(7)

(8)

where for is the submatrix of

corresponding to the rows of and the columns of .

By using the definitions of and in (3) and (4),

and the identity for non-singular matrix , we obtain

Therefore, we obtain

the matrix representations (5), (6) and (7),

and the decomposition .

∎

Note that

(9)

are also obtained from the proof of Theorem 1,

and they are also obtained from Proposition 1.

Furthermore, note that, for example, the matrix of total effects needs both

the premultiplication of and the postmultiplication of .

This is a thing that is different from the result of Proposition 1.

Next, we calculate the means of , and .

From structural equation model (1),

we obtain the following equations:

By multiplying both sides of the above three equations

by inverse of and respectively,

we obtain the following equations:

(10)

(11)

By taking the means of both sides of (10), (11) and (LABEL:eq:transformed_sem_des),

we can compute the means of , and , and obtain the following proposition.

Proposition 2.

(13)

(14)

(15)

Proof: By taking the means of both sides of (10)

and using (9),

we obtain (13) as follows:

Next, by substituting (10) into (11) and taking the means,

we obtain (14) as follows:

where we are using (5) and (9) in the third equality.

Finally, by substituting (10) and (11) into (LABEL:eq:transformed_sem_des) and taking the means,

we obtain (15) as follows:

where we are using

(3), (4), (6) and (9)

in the second equality

and using (8)

in the third equality.

∎

The above proposition says that the means can be decomposed by means of the total effects.

Almost the same things can be said about the variance matrix of , and .

Next, from

(10), (11), (2.2)

and the assumption ,

we obtain (17) as follows:

where we are using (5), (9) and in the third equality.

Finally, from the assumption ,

we have

(21)

Now, from (10) and (11), can be calculated as follows:

Therefore, by substituting (2.2), (2.2) and (2.2) into (21),

we obtain (18) as follows:

where we are using (3), (4), (5), (6), (9),

, and

in the second equality,

and (8) in the third equality.

∎

In the following, we only consider the case where the assumption of Proposition 3 holds, i.e.

.

2.3 Interventions to Structural Equation Models

An intervention to a structural equation model means changing structure of the structural equation model.

Throughout this paper,

we consider only intervention to the structures between and in the model of (1),

(for more general case of intervention, see Pearl (2009)).

In this case, only the elements of are directly affected by the intervention and are called treatment variables.

Of course, the elements of are also affected indirectly by the intervention.

The elements of are called covariates and the elements of are called output variables.

The effects caused by the intervention are called intervention effects.

For example, the changes on the means of the output variables after the intervention are intervention effects.

Assume that , and in (1)

are changed into , and , respectively, by the intervention,

where is the column vector of error terms that their means are all zero values and the variance matrix is .

Furthermore, we assume that the assumption of Proposition 3 again holds after the intervention, i.e.

.

Then the structural equation for is changed from

to

(23)

Let us define the following matrices.

(24)

(25)

The elements of are the total effects from to after the intervention of (23).

Note that does not change after the intervention of (23).

Let us denote by and the means and the variances of

after the intervention of (23).

Then the following corollary holds immediately from Proposition 2 and 3.

Corollary 1.

After the intervention of (23),

the mean vector of is given by

Furthermore, assume that ,

then the variance matrix of after the intervention of (23) is given by

(26)

In the following sections,

we treat only the intervention by which the error terms of do not change i.e. .

3 Application of Mathematical Optimization Procedures to Intervention Effects

In Section 3.1,

we first consider intervention to the path coefficients

to reduce the variances of the output variables.

Next, in Section 3.2,

we treat intervention to the means to adjust the mean values of output variables.

3.1 Application of Mathematical Optimization Procedures to Intervention Effects for Variances

For a given structural equation model,

it often happens that it is necessary to intervene the model to reduce the variances of the output variables.

In structural equation models, this can be done by changing the values of

the path coefficients by intervention.

In this section, we show that an algorithm to obtain the intervention method which minimizes

the weighted sum of the variances can be formulated as a convex quadratic programming.

This formulation allows us to impose the boundary conditions

for the intervention, so that we can find the practical solutions.

Let us denote by

elements of interest in

, by the dimension of ,

and by the -th element of .

The variance of , which we denote by , is the diagonal element of in relation to .

Then the minimization of the weighted sum of the variances of , under constraint

that the elements of have upper and lower bounds

can be formulated as follows:

(27)

(28)

where

are the weights,

and and are the matrices,

the elements of which are the lower and upper bounds for .

We assume that these values are determined appropriately in advance.

Now we formulate the above problem as a convex quadratic programming.

At first, we neglect the terms

and

in the variance matrix of (26),

because they are not changed by changing .

Let us define the following functions:

(29)

where and are the row vectors

of and in relation to .

Then the minimization of the objective function in (27) is equivalent to

Remember that the definition of is

in (24).

By using operator, Kronecker product and (36) (see Appendix A.1),

the column vector in (29) can be formulated as follows:

(30)

where is the row vector of in relation to ,

and is the row vector of in relation to

(see (6) of Theorem 1).

Let us define the following matrices and column vectors:

By using these definitions and (30),

the column vector in (29) can be

represented as follows:

(31)

Hence, we obtain

and

Note that the third term in the right-hand side of the above equation is constant with respect to

and negligible in the minimization problem of (27).

Therefore, the minimization problem of (27)

under the constraint of (28)

can be represented as the following convex quadratic programming:

where

and .

The Karush-Kuhn-Tucker (KKT) conditions of the problem of (LABEL:eq:QP_programming_for_variances)

are given as follows:

where the elements of and are Lagrange multipliers (for more detail see Rockafellar (1996)).

Assume that the constraints in (LABEL:eq:QP_programming_for_variances) satisfy Slater’s constraint qualification,

i.e. holds.

Then is optimal

if and only if there exist and

which satisfy the above Karush-Kuhn-Tucker conditions for .

Notice that even if holds for some ’s,

the constraints in (LABEL:eq:QP_programming_for_variances) satisfy Slater’s constraint qualification

by considering the inequality constraints as equality constraints.

Example 4.

Let us consider a case where ,

,

is regular,

and constraint is not imposed on , i.e.

Then the Karush-Kuhn-Tucker conditions in this case are given as follows:

Remember that the first term in the last equation means the total effect

from to through after intervention

and the second term means the total effect

from to which does not go through .

Therefore, if the total effect from to through after intervention

offsets the total effect from to which does not go through ,

then the Karush-Kuhn-Tucker conditions hold and the variance of is minimized.

∎

3.2 Application of Mathematical Optimization Procedures to Intervention Effects for Means

We consider the intervention to the means .

From proposition 2, we obtain the mean of as follows:

where is the row vector of in relation to .

Suppose that we want to adjust the mean of to a standard by intervention which changes .

Then the minimization of weighted squared sum of the deviations ,

under constraint that the elements of have upper and lower bounds

can be formulated as follows:

(33)

(34)

where

are the weights,

and and are the matrices,

the elements of which are the lower and upper bounds for .

We assume that these values are determined appropriately in advance.

Note that the third term of the last equation does not depend on and

only the first and second terms are needed for the minimization in (33).

Therefore, the minimization problem of (33)

under the constraint of (34)

can be represented as the following convex quadratic programming:

4 Numerical Experiment

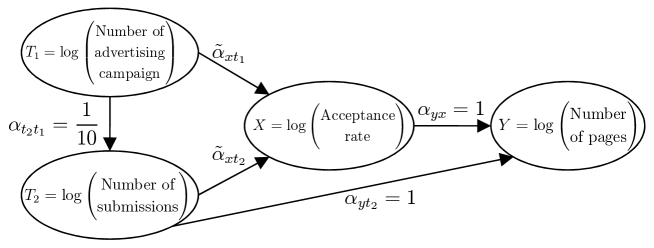

Figure 5: The path diagram of the structural equation model of (35).

To illustrate how the two algorithms

in Section 3

work, we consider the following toy model.

The model used in this numerical experiment is just a toy.

It may contain some inappropriate formulations and should not be taken seriously.

Suppose that an editor of a journal

which is published once a year

wanted to stabilize the number of pages of the journal.

The editor observed the following four variables:

•

- the random variable of the logarithm of the number of advertising campaign for the journal;

•

- the random variable of the logarithm of the number of submissions to the journal;

•

- the random variable of the logarithm of the acceptance rate of the journal;

•

- the random variable of the logarithm of the number of pages of the journal.

The editor can control the borderline whether or not to accept a manuscript graded by some referees.

However, the acceptance rate is random variable

because the grades of the manuscripts submitted to the journal are determined by the reviewers.

Furthermore, the advertising campaign is not the editor’s job and the editor can not control.

To these variables, the editor constructed a simplified structural equation model which is represented as the path diagram in Figure 5 and the following equations:

(35)

where

•

,

•

,

•

,

•

, , and ,

•

and .

The last equation in (35)

means that the number of pages of the journal is

approximately equal to

Average number of pages for each manuscript Number of submissions Acceptance rate.

At this time,

the path coefficients from to were

and so the editor considered to intervene these two coefficients and

to minimize the variance of the number of the pages.

From Section 3.1,

the problem of minimization of the variance can be represented as the following quadratic programming:

where the constraints for and were determined

by the editor’s inspiration to avoid too strong dependency between and .

By computing the above quadratic programming,

the editor obtained the optimal solution

and the variance of reduced to from .

However, the editor noticed that the expectation of the number of pages of the journal

under the optimal solution is

and thought that it might be too small.

Next,

the editor designated the appropriate amount for the expectation of the number of pages of the journal as

and considered to achieve it by intervention to .

From Section 3,

this problem can be formulated as the following quadratic programming:

where the constraint for prevents the acceptance rate from exceeding .

By computing the above quadratic programming,

the editor obtained the optimal solution .

Then, the expectation of the number of the pages under the optimal solutions

and

is the .

As a result, the editor succeeded in minimizing the variance of the number of pages of the journal

and adjusting the expectation to the appropriate amount.

What should the editor do, if the editor wants to change the expectation of the number of pages

with the minimized variance?

In this case, all the editor has to do is to re-intervene to .

The interventions to the path coefficients and are not needed

because the intervention to changes the expectation without changing the minimized variance,

(though, if the constraint for is too strong,

then the interventions to and might be needed to adjust the expectation).

This is the reason why we separate the problem into two algorithms

as in Section 3.

Furthermore, note that this two-step procedure has been used in the area of statistical quality control.

Taguchi (1987)

recommended the two-step optimization to solve the design optimization problem,

in which we first maximize the S/N ratio and adjust the expectation on target in the next step.

5 Conclusion

We have introduced matrix representation of total effects and some ideas of their decomposition.

Then, we have shown

that problems

to obtain the optimal intervention that minimizes the variances

and to adjust the expectations

can be formulated as convex quadratic programmings.

In Theorem 3,

we assume that .

However, this assumption does not hold if there are latent variables

that affect both and , or both and , or both and .

In future work,

we intend to extend our results to the case where the assumption of Theorem 3 does not hold.

Throughout this paper,

we treat only the case that

the structural equation model which represents the true relationships between real objects is given in advance.

Is the method introduced in this paper not useful if we do not have the true model?

We think the answer is yes.

If the given model is not true, then the intervention effect computed by using the method in this paper

and the intervention effect observed in real mostly have different values.

Therefore, the intervention and the computation of the intervention effect based on the given model

can be used for verification whether the model is true or not.

We also intend to consider this subject in future work.

Appendix A Appendix

A.1 Kronecker product and Vec Operator

Let be an matrix and

be a matrix.

The matrix

is called the Kronecker product of and .

The operator for a matrix

is defined as follows.

Let be an matrix.

The following relation holds.

(36)

References

(1)

Bollen (1987)

[1] Bollen, K. A. (1987). “Total, Direct, and Indirect

effects in Structural Equation Models”, Sociological Methodology, 17, 37–69.

Bollen (1989)

[2] Bollen, K. A. (1989). Structural Equations with

Latent Variables, New York: Wiley.

Haavelmo (1943)

[3] Haavelmo, T. (1943). “The Statistical Implications of

a System of Simultaneous Equations”, Econometrica, 11, 1–12.

Koopmans (1949)

[4] Koopmans, T. C. (1949). “Identification Problems in

Economic Model Construction”, Econometrica, 17, 125–144.

Kuroda et al. (2006)

[5] Kuroda, K., Miyakawa, M. & Tanaka, K. (2006).

“Formulation of Intervention to Arrows in Causal Diagram and Its

Applications (in Japanese)”, Japanese J. Appl. Statist., 35,

79–91.

Kuroki (2008)

[6] Kuroki, M. (2008). “The Evaluation of Causal Effects

on the Variance and its Application to Process Analysis (in Japanese)”, J. Japanese Soc. Quality Control, 38, 87–98.

Kuroki and Miyakawa (2003)

[7] Kuroki, M. & Miyakawa, M. (2003). “Covariate

selection for estimating the causal effect of control plans by using causal

diagrams”, J. Royal Stat. Soc. Series B, 65, 209–222.

Pearl (2009)

[8] Pearl, J. (2009). Causality: Models, Reasoning

and Inference, New York: Cambridge University Press, 2nd edition.

Rockafellar (1996)

[9] Rockafellar, R. T. (1996). Convex Analysis, New

Jersey: Princeton University Press.

Sobel (1990)

[10] Sobel, M. E. (1990). “Effect Analysis and Causation

in Linear Structural Equation Models”, Psychometrika, 55,

495–515.

Taguchi (1987)

[11] Taguchi, G. (1987). The System of Experimental

Design: Engineering Methods to Optimize Quality and Minimize Costs, USA:

Quality Resources.

Wright (1923)

[12] Wright, S. (1923). “The Theory of Path

Coefficients: A Reply to Niles’s Criticism”, Genetics, 8,

239–255.