Measuring Portfolio Diversification

Abstract

In the market place, diversification reduces risk and provides protection against extreme events by ensuring that one is not overly exposed to individual occurrences. We argue that diversification is best measured by characteristics of the combined portfolio of assets and introduce a measure based on the information entropy of the probability distribution for the final portfolio asset value. For Gaussian assets the measure is a logarithmic function of the variance and combining independent Gaussian assets of equal variance adds an amount to the diversification.

The advantages of this measure include that it naturally extends to any type of distribution and that it takes all moments into account. Furthermore, it can be used in cases of undefined weights (zero-cost assets) or moments. We present examples which apply this measure to derivative overlays.

1 Introduction

Combining different assets in a portfolio changes the return and risk111We will leave the precise definition of “risk” here open. characteristics. Diversification strategies allow to fine tune for risk appetite and parameter ranges, which are usually stipulated in investment mandates.

While diversification is an intuitive concept, there is no unique quantitative measure of it. The benefits of portfolio diversification clearly stem from the independence or the offsetting of asset value changes. Hence any good measure should take asset characteristics into account in addition to portfolio exposures to each asset (e.g., asset weights in the portfolio).

Here we want to give a brief review of existing measures before introducing a new measure based on the entropy of the return probability distribution (for the total portfolio). This measure naturally extends to zero-cost assets (for which weights cannot be defined) and we show the diversification benefits of some derivative overlays.

2 Existing Measures

Measures have been suggested (for an overview see for example [5]), which fall broadly into two categories: just weight based and taking return characteristics into account.

- Herfindahl Index

-

A simple and widely used weight-based diversification index given by

(1) where the are the weights for the assets. This measure does not account for inter-dependence between assets and differing risk characteristics.

- Weight Entropy

-

One way to interpret portfolio weights is to see them as the probability of a “randomly”222Here in the sense of equal likelihood. It might indeed be impossible to define randomness consistently. choosen currency unit to be invested in a certain asset. One could then argue that the entropy difference between these probabilities and the uniform distribution is a measure of information content and diversification. The corresponding measure is the weight entropy

(2) This measure also has an intriguing sub-division property, which relates the overall entropy to the entropy of sub-portfolios and the weights of the sub-portfolios.

(3) where are the portfolio weights and are the entropies of the sub-portfolios.

- Portfolio Diversification Index

-

This measure tries to assess how many independent bets there are using the eigenvalues of the covariance matrix of the returns of individual assets making up a combined portfolio (which is usually estimated from historic data). It is given by

(4) where are the ordered and normalized covariance eigenvalues. In its original form it does not deal with the actual weights assigned to the assets. However, they can be incorporated by considering weighted returns, i.e., using the covariance matrix of the fractional contributions of the assets to the total portfolio performance.

An important shortcoming of this measure is its sole reliance on the covariance matrix, which is the second moment of a multi-variate distribution. Only for the special case of (multi-variate) normality does this take all distributional information into account (besides the expected value).

3 Interpretations and Notation

We follow the Bayesian interpretation of probability [2] as a measure of degree of believe, which is always dependent on subjective background information. The probability of proposition to be true, given that is true is denoted by . and can be composed of several propositions. denotes the available (subjective) background information.

Similarly, probability distributions are denoted by , where is a proposition involving a continuous variable .

4 A Measure based on Entropy

Information entropy is known as a measure of dispersion in a distribution. In contrast to the variance, it measures the expected information gained per outcome.333 For a discrete probability distribution the information entropy is invariant under the exchange of any two probability values, i.e., it does not depend on the outcome variable, just on the probabilities of the possible outcomes. We want to argue here that the information entropy of the probability distribution of the final value of the portfolio is a natural measure of diversification. Let us define such a diversification measure as

| (5) |

which is just the negative of the information entropy. Here is the probability distribution for the final value of portfolio . Note that the unit depends on the base of the logarithm used — for the natural logarithm the diversification will be measured in “nats”, which differ by a factor from “bits”.

As the probability distributions are subjective, i.e., dependent on some subjective background information , so will be the diversification measure. This means that our judgment of diversification might change due to new information available.

One pleasing property of this measure is that it does not make any distributional assumptions, but can be applied to any type of distribution. Obviously, it is in itself a challange to find a suitable probability distribution expressing information and beliefs about the portfolio returns.

One consequence of the above is that the measure is not just a function of a finite number of moments/cumulants, like the variance. Instead depends on all moments and remains defined even if moments become undefined (like for power-law distributions). For example, for the Cauchy distribution

| (6) |

all moments are undefined, but our diversification measure remains well-defined and takes the value

| (7) |

For the simple case of normally distributed final portfolio values with variance one finds

| (8) |

where stands for the set of propositions that the final portfolio value will be .

The more peaked the probability distribution, the larger the value for the diversification measure. In the extreme limiting case of a delta function the measure approaches infinity. Hence one could argue that cash, which generally has the least uncertainty about its future value in currency terms, has the highest diversification of all investable assets.

5 Motivation

Let us consider the case of two independent assets and , whose future value is normally distributed with equal variance and expected value. Our diversification measure for each asset takes the value

| (9) |

Let us now form a combined portfolio by investing the fraction and of the total portfolio value in asset and , respectively. The final value of portfolio is then given by

| (10) |

As and are normal, is normal with variance

| (11) |

and the diversification measure for takes the form

| (12) |

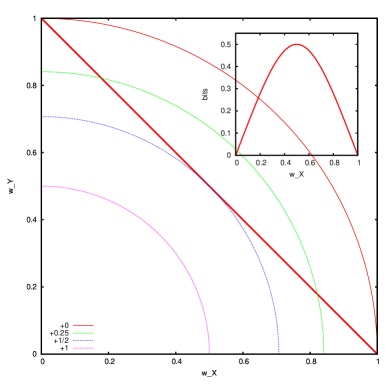

Hence diversification depends logarithmically on the distance to the origin in weight space. This is illustrated in Figure 1.

This is a sensible behaviour for a diversification measure: for equal variances it is maximized for equal weights (in which case it increases by half a bit) and the increase due to diversification is independent of asset variances. Furthermore, it is additive - if the total diversification is bits, then we can think of it as being the equally weighted mixture of

| (13) |

independent assets (of equal variancence) each with diversification .

This result can easily be generalized to the case of differing variance and for and , respectively. Using one finds the result

| (14) | |||||

Here the first term is the (equally weighted) average diversification and the second term is the diversification benefit dependent on the weights and variances.

6 Transformation Properties

Let the value of portfolio be a strong monotonic increasing function of the value of portfolio , the “underlying”. The portfolio value probability distributions are related by

| (15) |

Substituting this into the definition for the diversification measure one finds

| (16) |

where

| (17) |

is the “future delta” (the delta at the time for which the diversification measure is evaluated).

One special case of this is constant gearing

| (18) |

where and the diversification benefit is

| (19) |

This illustrates that gearing (), which steepens the dependence of the final portfolio value on the final asset value, decreases diversification.

The results above can be generallized to strongly monotonic decreasing relationships. If there is no strong monotonic relationship then the domain can be broken into distinct segments, which are either strong monotonic or constant.

7 Examples

For the examples below we assume that asset returns are log-normal with constant (log-return) variance and expected growth factor equal to the risk free rate growth . Hence the Black-Scholes formulas can be used for the option pricing.

7.1 Long dated put

We consider here the diversification over a one year horizon. We augment the asset with a bought put option with expiry in two years and strike price . Let be the remaining life time of the option at the time for which we consider the diversification measure. The change of the combined portfolio value with the underlying asset is then the sum of future “deltas”

| (20) |

where is the (continuous) dividend yield and

| (21) |

Let us assume here that there is no dividend yield on the asset, i.e., . The diversification benefit is then

| (22) |

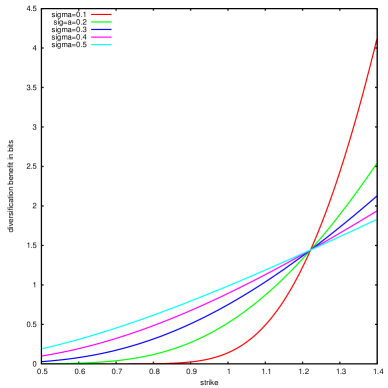

We evaluate this for different strike prices . Figure 2 shows the resulting diversification benefits for different standard deviations (for the annual log returns).

For a given fixed variance, if the strike price of the put option is low, then the final asset value distribution is hardly affected and the diversification effect diminishes. As the strike price increases more “negative” outcomes (asset value below strike price) are eliminated as the put-payoff compensates for the loss. This is equivalent to a narrowing of the probability distribution and an increase of the diversification measure. We note that the diversification benefit gained with increasing strike price is far more substantial for less volatile assets.

Note that the option considered here still has one year left to expiry at the time for which we consider the diversification measure. The above still holds, with the trend becoming more extreme as there is less time to expiry remaining.

7.2 Put-Spread

The put spread, being the combination of a bought upper put and a sold lower put, is now considered. The totla portfolio future delta is now

| (23) |

where is the strike of the upper put and is the strike of the lower put.

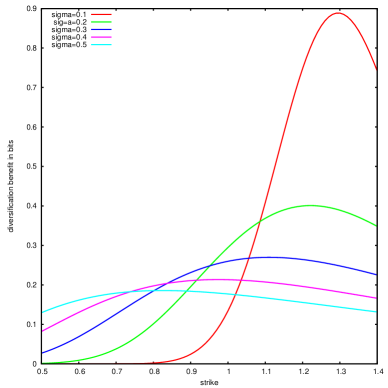

Figure 3 shows the resulting diversification benefits for the put spread as a function of the (upper) strike price given different standard deviations (for the annual log returns). The shape of the curve results from the competition between the increase in the diversification benefit from increasing the strike price of the upper put as illustrated in Figure 2, and the loss of diversification from the lower sold put. Note though that these effects are not additive as follows from (16) and the non-linearity of the logarithm.

7.3 Collar

The collar is a popular strategy because the downside protection is (partially or fully) financed by selling upside participation (in form of a sold call). As the collar is the combination of a bought put with a sold call we have (including the underlying)

| (24) |

where is the strike of the put, and the strike of the call.

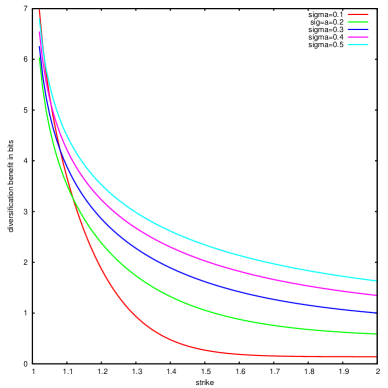

Figure 4 shows the net diversification benefit achieved from a collar in terms of the strike of the upper sold call option. The strike of the bought put was fixed at 100% and curves for different volatilities (of the annualized log-return distribution) are shown.

As the call strike price approaches the put strike price at 100% all uncertainty is removed (it becomes a synthetic sold future paired with the underlying asset) and the diversification benefit increases to infinity. The amount of diversification is notably higher in the case of more volatile assets.

8 Conclusion

In this paper we advocate that a measure of portfolio diversification should be a functional of the (subjective) probability distribution for the final portfolio value. In this way it automatically incorporates asset exposures and asset characteristics.

We propose the negative information entropy of the probability distribution of the final portfolio value as a suitable diversification measure, which takes all moments into account.

This measure can be applied to all types of distributions and does not require that asset returns or weights are defined. This means that this measure can deal with holdings which can have positive and negative values, like derivative structures, in a portfolio.

For the simplistic case of independent, normally distributed asset returns, we have demonstrated that the negative information entropy is a logarithmic function of the portfolio variance. Combining Gaussian assets of equal variance adds an amount to the diversification measure which only depends on the asset weights.

For derivative overlays our result (16) links the future delta to the diversification benefit.

For the more realistic example of log-normal final asset value probability distributions we have given some simple examples illustrating how derivative-overlays lead to a diversification benefit, as measured by our index.

As protective derivative overlays narrow the probability distribution of the final portfolio value, they increase the diversification as measured by our measure.

We find that for a long-dated put option, the diversification rises rapidly with increasing strike price for less volatile underlying stocks. For the case of a put spread, this index can be used to select the strike prices that maximizes the net diversification benefit for a given level of volatility. For the case of a collar, the portfolio diversification benefit achieved increases dramatically as the sold call strike approaches the bought put strike.

Appendix A Understanding Information Entropy

Let us assume that (discrete) events occur with likelihood in a repeated experiment. On observing the outcome the information gained in bits is .

One way to look at this is as follows: if our state of knowledge is that we judge an object to be equally likely in one of positions then we gain bits when we find out where it actually is.

As events occur with probability the average information gain (in bits) is

| (25) |

which is called the information entropy.

The information entropy has some interesting properties:

-

•

if for one .

-

•

takes a maximum value of if the possible outcomes are equally likely.

-

•

if outcome is really a combination of different outcomes then

(26) where is the entropy based on (the probability that one of the events occures) and is the entropy for outcomes , given that (one of them) occured.

Maximum entropy methods generally maximize the information entropy subject to constraints on the probabilities, such as specified moments.

Appendix B Log-normal assets

The log-normal distribution with expected value is given by the probability distribution

| (27) |

where is the variance of the distribution of . This yields for the diversification measure

| (28) |

It is interesting to note that in contrast to the gaussian case (which depends solely on the variance), the measure here also depends on the expected value.

Appendix C Effects of Skewness and Kurtosis

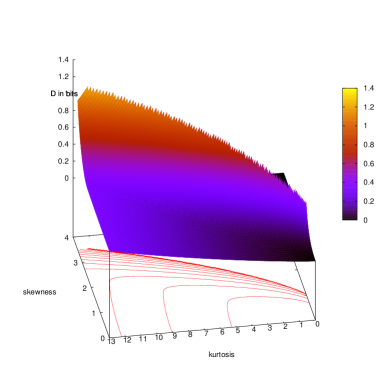

As the normal distribution is a maximum entropy distribution, any other distribution with equal variance must have more diversification according to our measure. Figure 5 shows the increase in diversification for maximum entropy distributions of given skewness and kurtosis for a fixed variance of .

Appendix D Comments on Weight Entropy and Herfindahl Index

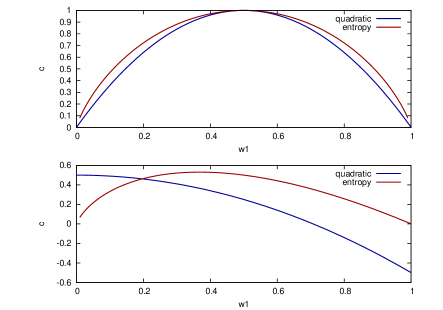

The Weight Entropy and Herfindahl index are both diversification measures solely based on portfolio weights. We want to investigate the difference between these measures for the two and three asset case.

For a portfolio with two assets, the Weight Entropy (entropy) and Herfindahl Index (quadratic) measures are shown below in figure 6. Both are maximal for . If the contribution to the overall measure from one asset only is considered, we see (in the lower panel) that large weights effectively give a negative contribution for the quadratic measure, while there are no negative contributions to the entropy measure.

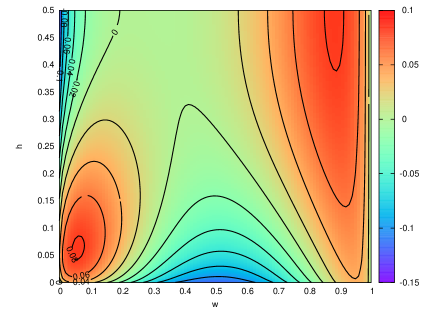

Figure 7 shows the differences for the three asset case. There are large areas where the quadratic measure (Herfindahl Index) understates diversification by up to of the maximum value compared to the entropy measure. On the other hand, around and (and equivalently for and ) the quadratic measure overstates diversification relative to the entropy measure.

Both measures can be extended to the correlated gaussian case by considering the exposure to the “eigen-vector portfolios” of the correlation matrix instead of the actual asset weights. This, however, still does not account for varying risk profiles of the assets (or eigen-vector portfolios).

References

- [1]

- [2] Jaynes E T, Bretthorst L G (2003), Probability Theory: The Logic of Science, Cambridge University Press,Cambridge

-

[3]

Kirchner U (2010), ‘A Subjective and Probabilistic Approach to Derivatives’, arXiv 1001.1616[q-fin.PR]

(Online at http://arxiv.org/abs/1001.1616) -

[4]

Kirchner U (2009), ‘Market Implied Probability Distributions and Bayesian Skew Estimation’, arXiv 0911.0805[q-fin.PR]

(Online at http://arxiv.org/abs/0911.0805) - [5] Woerheide W, Persson D (1993), ‘An Index of Portfolio Diversification’, Financial Services Review 2(2), 73-85