Portfolio Insurance under a risk-measure constraint

Abstract

We study the problem of portfolio insurance from the point of view of a fund manager, who guarantees to the investor that the portfolio value at maturity will be above a fixed threshold. If, at maturity, the portfolio value is below the guaranteed level, a third party will refund the investor up to the guarantee. In exchange for this protection, the third party imposes a limit on the risk exposure of the fund manager, in the form of a convex monetary risk measure. The fund manager therefore tries to maximize the investor’s utility function subject to the risk measure constraint. We give a full solution to this nonconvex optimization problem in the complete market setting and show in particular that the choice of the risk measure is crucial for the optimal portfolio to exist. Explicit results are provided for the entropic risk measure (for which the optimal portfolio always exists) and for the class of spectral risk measures (for which the optimal portfolio may fail to exist in some cases).

Key words: Portfolio insurance, Utility maximization, Convex risk measures, CVaR, entropic risk measure

MSC: 91G10

1 Introduction

We consider the problem of a fund manager who wants to structure a portfolio insurance product where the investors pay the initial value at time and are guaranteed to receive at least the amount at maturity . We assume that if, at time , the value of the fund’s portfolio is smaller than , a third party pays to the investor the shortfall amount . In practice, this guarantee is indeed usually provided by the bank which owns the fund. The final payoff for the investor will be

| (1.1) |

In exchange, the third party imposes a limit on the risk of shortfall , represented by a law-invariant convex risk measure . We assume that the investors’ attitude to gains above the guaranteed level is modeled by a concave utility function .

The fund manager therefore faces the following problem:

| (1.2) | |||

| (1.3) |

The utility function applies only to the random variable as the investor is indifferent to the portfolio’s value below the guarantee .

This is a nonstandard maximization problem, because the objective function is not concave, and it therefore cannot be solved using standard Lagrangian methods. We use a technique similar to the one developed in Jin and Zhou (2008) in the context of behavioral portfolio optimization to decouple the problem (1.2)–(1.3) into two separate convex optimization problems and show that in a complete market case the optimal solution has a simple structure.

An interesting outcome of our study is that the maximization problem (1.2) may not admit an optimal solution for all convex risk measures, which means that not all convex risk measures may be used to limit fund’s exposure in this way. We provide conditions for the existence of the solution and show, for example, that in the Black-Scholes model, the CVaR risk measure does not satisfy these conditions.

Portfolio insurance is a widely popular concept in financial industry, and there exists an extensive literature on this topic. When the guarantee constraint is imposed in an almost sure way, a common strategy is the option based portfolio insurance, which uses put options written on the underlying risky asset as protection. The optimality of OBPI for European and American capital guarantee is studied in El Karoui et al. (2005). The difficulty of finding a sufficiently long-dated option for use in OBPI has lead to the appearance of strategies which involve only the underlying risky asset, of which the most popular is the Constant Proportion Portfolio Insurance (CPPI), (Black and Perold, 1992), where the exposure to the risky asset is proportional to the difference between the value of the fund and the discounted value of the guaranteed payment. If the price path of the underlying risky asset admits jumps, the CPPI strategy no longer ensures that the fund value will be a.s. above the guaranteed level at maturity, unless the portfolio is completely deleveraged (Cont and Tankov, 2009), which usually imposes too strong a restriction on the potential gains.

The current market practice is therefore to require that the portfolio stays above the guaranteed level with a sufficiently high probability, or, for example, that it remains above the guarantee for a certain set of stress scenarios, chosen from historical data coming from highly volatile periods. A more flexible approach, which can take into account not only the probability of loss but also the sizes of potential losses, is to impose a constraint on a risk measure of the shortfall. This has led to the development of literature on portfolio insurance and, more generally, portfolio optimization under probabilistic / risk measure constraints.

Emmer et al. (2001) study one-period portfolio optimization under Capital-at-Risk constraint (the Capital-at-Risk is defined as the difference between the mean value of the portfolio and its VaR). Still in the one-period setting, Rockafellar and Uryasev (2000) provide an algorithm for minimizing the CVaR of a portfolio under a return constraint. Boyle and Tian (2007) discuss continuous-time portfolio optimization under the constraint to outperform a given benchmark with a certain confidence level. Like us, these authors also face some issues related to the non-convexity of the optimization problem, although the non-convexity appears for a different reason (non-convexity of the constraint itself).

Another stream of literature (Föllmer and Leukert, 1999; Bouchard et al., 2009) considers hedging problems when the hedging constraint is imposed with a certain confidence level rather than almost surely. The viscosity solution approach of Bouchard et al. (2009) was extended in (Bouchard et al., 2010) to stochastic control problems under target constraint (that is, for example, under the constraint to outperform a benchmark with a certain probability) but it does not seem to be possible to treat risk measure constraints in this setting.

He and Zhou (2010) have recently introduced a general methodology for solving law-invariant portfolio optimization problems by reformulating them in terms of the quantile function of the terminal value of the portfolio. While such a reformulation is in principle possible for our problem using the dual representation results for law-invariant convex risk measures (see Föllmer and Schied (2004) and Jouini et al. (2006)), the resulting problem is still non-linear and non-convex so such a transformation does not necessarily simplify the treatment.

Gundel and Weber (2007) solve the problem of maximizing the (robust) utility of a portfolio under a constraint on the expected shortfall, which includes, in particular, all coherent risk measures. The main difference of our paper from that of Gundel and Weber, and the main novelty of our paper is that in our approach, the utility function is only applied to positive gains while the risk measure is only applied to negative shortfall. This brings us much closer to the reality of portfolio insurance and at the same time allows to obtain explicit solutions.

The rest of the paper is organized as follows. In section 2 we introduce the model and optimization problem, and state the main theoretical results, including a decoupling method to solve the problem (1.2) and the conditions under which this problem admits a finite solution. In sections 3 and 4 we investigate the case where one uses, respectively, the entropic risk measure and the spectral risk measures. The proofs of all theoretical results are postponed to section 5.

2 Main results

Let be a filtered probability space. We consider an arbitrage-free complete financial market consisting of risky assets with -adapted price processes and the risk-free asset with price process . We do not specify the dynamics of risky assets and the precise definition of admissible strategies because they are not relevant for what follows. See Karatzas and Shreve (1998) for the standard example of a market which satisfies our assumptions in the Brownian filtration. For an admissible trading strategy , the investor’s portfolio value is

The unique martingale measure will be denoted by , and we define . The market completeness implies that for any -measurable random variable with such that , there exists an admissible trading strategy such that a.s.

Since the interest rate is zero, to avoid direct arbitrage for the investor. Moreover, without loss of generality, we will assume in the rest of the paper.

The attitude of the investor towards gains above is measured, in the spirit of the Von Neumann-Morgenstern expected utility theory, by a twice differentiable, strictly concave and strictly increasing function , satisfying the usual condition . We suppose and we denote and if and otherwise. Moreover, we assume that the following integrability condition holds: for all .

The risks are measured using the convex law-invariant risk measure (see Föllmer and Schied (2004)). The domain of definition of may contain unbounded claims and may be taken equal, for example, to as in Kaina and Rüschendorf (2009) or a more general Orlicz space as in Biagini and Frittelli (2009). To simplify notation later on, we additionally define if and .

Using the market completeness, the optimization problem (1.2)–(1.3) can be reformulated as the problem to find, if it exists, an such that

| (2.1) |

where

| (2.2) |

and . To simplify the notation, let us define

We choose . The problem (2.1) cannot be solved using classical Lagrangian methods because the function is not concave.

Since for all ,

where , only is important for the investor. This remark suggests the following decoupling: let and consider

| (2.3) | |||

| and | |||

| (2.4) | |||

For all we define:

| (2.5) |

and

| (2.6) |

Problem is a minimization of a linear function over a convex set and, as we will see later, Problem can be viewed as a concave maximization problem under a linear constraint. We will start by analysing Problems and and then Theorem 2.1 will clarify the relationship between these problems and (2.1).

Remark 2.1.

Before going on, it is important to investigate the behavior of and on trivial sets. If then and then which means that . Therefore, and .

In the next lemma we will solve explicitly problem .

Lemma 2.1.

Suppose . The unique maximizer of problem is given by

| (2.7) |

where is the unique solution of

| (2.8) |

The value function is strictly increasing and continuous in , and for every there exists such that

| (2.9) |

for all and all .

The next example will clarify the role of . Fix such that and suppose . It is then possible to find, for each a random variable such that . Define now

It is clear that for all and , which means that Problem (2.1) does not admit a maximizer. To avoid this problem, we shall use one of the following assumptions on :

| (2.10) | |||

| (2.11) |

Clearly, (2.10) depends on the particular choice of and . In particular, a choice under which for some is not appropriate in this kind of portfolio insurance. As we will see later in the example we will present, for the risk measure in the Black and Scholes model, whereas the same risk measure coupled with a bounded satisfies (2.11).

Assumptions (2.10) and (2.11) can be difficult to check; the following condition, which is simpler, guarantees (2.11) but it is not necessary.

Proposition 2.1.

Condition (2.11) is implied by the condition

| (2.12) |

where is the minimal penalty function of defined by

where is the acceptance set of .

The following result clarifies the relationship between Problem (2.1) and –, giving us a method to solve the former.

Theorem 2.1.

Theorem (2.1) gives us a condition under which the value function of problem (2.1) is finite and a way to compute it:

Algorithm 1 :

-

1.

fix

-

2.

solve and find

-

3.

solve with parameter

-

4.

maximize the value function of , (repeating the steps 1–3), over

The next result establishes a link between the maximizers of problem (2.1) and –.

Theorem 2.2.

Let (2.10) hold.

Remark 2.2.

The main difficulty in applying Theorems 2.1 and 2.2 is how to find a maximizer . Generally, maximization over the sets in is not simple. Our aim here is to show that this latter maximization may be carried out over a subset of , parameterized by a real number. A similar approach was taken in Jin and Zhou (2008).

We already know, from Theorem 2.1, that

In order to focus our attention on the set dependence, we will introduce the following notation:

| (2.17) |

Let us also define and .

Theorem 2.3.

Suppose that the law of has no atom and let . Let such that . Then

| (2.18) |

which means that

| (2.19) |

In order to make the notation simpler, let .

With this result, we can make Algorithm 1 simpler:

Algorithm 2:

-

1.

fix and consider

-

2.

solve with parameter and find

-

3.

solve with parameters

-

4.

find that maximizes

The question of the existence of which maximizes , and the related question of the existence of the optimal pay-off for the fund manager is difficult to answer for general risk measures. A complete answer to this question will be given in section 3 in the case of the entropic risk measure (see Theorem 3.1) and in section 4 for spectral risk measures (Theorem 4.1).

3 Example: entropic risk measure

In this section we show how Theorems 2.2 and 2.3 can be used to solve problem (2.1) when the risk measure in question is the entropic risk measure (ERM) defined by

| (3.1) |

where . Throughout this and the following section, we use the notation of Section 2 and suppose that all the assumptions stated in the beginning of that section stand in force.

As shown in Example 4.33 in Föllmer and Schied (2004) (see also section 5.4 in Biagini and Frittelli (2009) for the case of unbounded claims), the entropic risk measure can be represented as

In particular, .

Theorem 3.1.

Let the risk measure be given by (3.1) and assume that the state price density has no atom and satisfies . Then the optimal payoff for the fund manager is given by

where

-

•

is the unique solution of

-

•

-

•

-

•

is the unique solution of: .

-

•

attains the supremum of

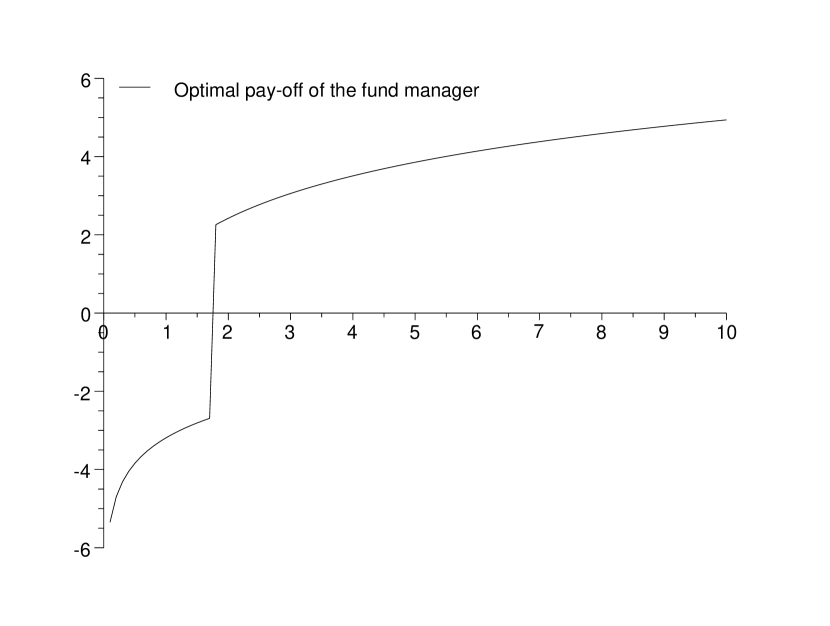

Numerical example

We will apply Theorem 3.1 in a simple case. Let the market be composed of one risky asset, , which follows the Black and Scholes dynamics:

Suppose . The unique equivalent martingale measure is given by , where .

We will use the exponential utility function . For this example we take , , , , , , , , and .

The optimal pay-off is a spread of two options on the log contract : one option is sold to match the desired risk tolerance and the second one is bought to obtain the gain profile desired by the investor.

| (3.2) |

where the numerical values of the constants are

The optimal pay-off of the fund manager as function of is shown in Figure 1. Figure 3 shows the gain for the investor compared to the situation where no risk is allowed. The (opposite of) extra capital made available due to the risk tolerance is given by and the probability of no loss is . Finally, the optimal value function for is . Figure 2 shows the value function as function of .

4 Example: and spectral risk measures

The is a coherent risk measure defined by

| (4.1) |

where is a generalized inverse distribution function of . Since the generalized inverse distribution function has at most a countable number of discontinuities, this definition does not depend on the particular choice of this function (right-continuous or left-continuous). In this section we shall always use the definition

| (4.2) |

with the convention .

The is the building block for a wide class of coherent risk measures called spectral risk measures. Given a probability measure on , the spectral risk measure is defined by

| (4.3) |

where

| (4.4) |

The function is right-continuous, nonincreasing and by Fubini’s Theorem, . The case corresponds to . The function completely characterizes the spectral risk measure .

In this section, we solve the portfolio optimization problem when the risk constraint is given by a spectral risk measure. We first need to compute the mappings and .

Lemma 4.1.

For with , let be the conditional distribution of on and define . if and only if

| (4.5) |

In this case

| (4.6) | |||||

| (4.7) |

Corollary 4.1.

The function is given by

Assume that the limit

| (4.8) |

exists. Then

The following theorem, which is the main result of this section, characterizes the solution of the problem (2.1) when the risk constraint is given by a spectral risk measure via a one-dimensional optimization problem.

Theorem 4.1.

Assume that there exists with such that with

where is the solution of

Then the solution to the problem (2.1) is given by

Remark 4.1.

If is attained only by and

(the latter condition holds, in particular, if ), then but this infimum is not achieved: the extra gain from allowing a risk tolerance is bounded, but the optimal claim does not exist. Intuitively, claims which are “almost optimal” will lead to a very large loss occurring with a very small probability.

If

then : the extra gain from allowing a risk tolerance is unbounded.

The special case:

In this case, and , and the limit appearing in Condition (4.5) in Lemma 4.1 becomes

Corollary 4.1, Lemma 2.1 and Theorems 2.3 and 4.1 enable us to give the solution of Problem (2.1):

- •

-

•

If then there exists with .

The maximum in (4.9) is always attained for some because the value function is continuous and is compact. If then Theorem 4.1 applies and then we have a optimal solution for Problem (2.1). If the maximum is attained at , then, as in Remark 4.1, the optimal claim does not exist.

5 Proofs

5.1 Proof of Lemma 2.1

Introduce the new probability space and let denote the expectation under the conditional probability . The maximizer of , if it exists, is given by

where is the maximizer of the following problem on the new probability space:

This is a classical problem of maximizing a concave function under a linear constraint which can be solved by Lagrangian methods (see e.g., Karatzas and Shreve (1998)). First, is continuously differentiable, and since the mapping is convex and finite for all , it is differentiable, and using Fatou’s lemma we get that for all . Therefore, the solution to the above optimization problem is

where is the unique solution of .

To show that is strictly increasing, let . Then the random variable

belongs to , which proves that .

The continuity of follows from inequality

| (5.1) |

and the continuity of , which is straightforward since the function is strictly decreasing and continuous. The upper bound on is also a consequence of (5.1), after taking expectations.

5.2 Proof of Proposition 2.1

By definition of ,

from which the result follows.

5.3 Proof of Theorem 2.1

Let us first prove (2.13). We start with the inequality “”.

Let such that . Define and .

One has then

The first inequality holds because and is the sup over . The second inequality follows from the fact that is nondecreasing in provided we can prove that . Let , then and then

which means

i.e.

Let us now focus on the inequality “”. Let be such that

By the assumption of the theorem, for all . Fix . Our aim is to find, for every , such that

| (5.2) |

Since is arbitrary it will then follow that . If , by Lemma 2.1 there exists an explicit maximizer of Problem , denoted by , and is continuous in . Therefore, we can find with sufficiently close to so that . Then satisfies (5.2). If then, as we saw in Remark 2.1, taking and satisfies .

5.4 Proof of Theorem 2.2

Let be an optimal solution for (2.1), and . It is clear that . It is also clear that , since otherwise and one can increase the utility and reduce the risk by increasing . Theorem 2.1 and the fact that is increasing in (Lemma 2.1) then give:

which means that achieves the supremum in (2.13). Moreover, since is strictly increasing in , we get a contradiction unless , which means that achieves the minimum in .

5.5 Proof of Theorem 2.3

We will use the methods developed in Jin and Zhou (2008) (see the proof of Theorem ). There are however some important differences in our proof which arise in particular due to the presence of risk measures in our context.

The theorem will be proved in two steps: in Step 1 we will prove that for every , there exists such that so that , and in Step 2 we will find, for every , an such that . We can then conclude that

Treating separately the trivial cases as described in Remark 2.1, we can assume , and set . Let us fix so that

This is possible since has no atom. Consider the following sets:

| (5.3) | |||||

| (5.4) |

from which it follows . If then , so we can suppose .

Step 1. Let . Our aim is to construct with and . This will imply that . Introduce the following notation:

-

1.

-

2.

-

3.

, that is, , because has no atom.

-

4.

, that is, the law of on is the same as the law of on .

Let

Observe that since on , and on , we have that . Now define

By definition, on and on . In addition, since , we easily get that for every .

Let and be the distribution functions of, respectively, and , and and their generalized inverses (defined in (4.2)). From the above inequality, they satisfy for all . Let be a random variable with uniform distribution on . Since is law invariant, we obtain that and therefore . On the other hand, (this is due to our choice of the constant ). Since the choice of was arbitrary, this means that .

Step 2. Let be feasible for with parameter , and define

-

1.

-

2.

-

3.

-

4.

, that is, the law of on is the same as the law of on .

Let

Note that now, . We define a new random variable by

| (5.5) |

We have and it is easy to see that . Moreover, since , a simple computation shows that

By definition,

| (5.6) | |||

but since is positive,

which enables us to conclude that .

5.6 Proof of Theorem 3.1

Proof.

Fix and consider the problem:

where

Working on the new space , we can transform this minimization into

where

Using Lagrangian methods we can find the unique optimal solution:

where is the unique solution of:

and so

A simple calculation then gives:

If now we set , by Lemma 2.1 , Problem with parameters can be solved and its unique solution is

where, by (2.8),

Using Theorem 2.3, the optimal is the maximizer of the function

∎

5.7 Proof of Lemma 4.1

Proof.

In order to compute we reformulate Problem in terms of the conditional distribution function of on . Introduce a new probability via . Let be the distribution function of under this probability and its generalized inverse. Using this new probability we can rewrite the ingredients of our problem as

and

and then using (4.3) we obtain

To express , we use the following well known result:

Lemma 5.1.

Let and be distribution functions on . Then

Using this lemma, Problem can be expressed as

| (5.7) | |||

| (5.8) |

where the is taken over all generalized inverse distribution functions of non-positive random variables. Such a function can always be written as

| (5.9) |

where is a positive measure on . Using Fubini’s theorem, we can rewrite problem (5.7)–(5.8) in terms of this measure:

The solution of this problem can easily be shown to be a point mass: where and can be found from

| (5.10) | |||

| (5.11) |

The constraint (5.11) gives us

and using definition (4.7) we get

The function is differentiable on and may only have a singularity at ; using l’Hôpital’s rule, we get

So if and only if is bounded on , which is true if and only if . ∎

5.8 Proof of Corollary 4.1

Proof.

In order to make the dependence on explicit, we introduce the notation

where

Noting that and making a change of variable,

The function can then be rewritten as

∎

5.9 Proof of Theorem 4.1

Proof.

From Theorem 2.3 we need to maximize the function over . Assume that achieves its maximum at the point such that with and let . Then, is constant on the interval , which means that ,

and therefore . This argument shows that the solution of the optimization problem appearing in the right-hand side of (2.19) does not change if we replace the expression for given by Corollary 4.1 by

Applying Lemma 2.1 we then find

where

If there exists a with which maximizes the value function then the optimal contingent claim is given by

where

is the optimal solution of Problem corresponding to , which can be deduced from the proof of Lemma 4.1. ∎

Acknowledgement

This research is part of the Chair Financial Risks of the Risk Foundation sponsored by Société Générale, the Chair Derivatives of the Future sponsored by the Fédération Bancaire Française, and the Chair Finance and Sustainable Development sponsored by EDF and Calyon.

References

- Biagini and Frittelli (2009) Biagini, S. and M. Frittelli (2009). On the extension of the Namioka-Klee theorem and on the Fatou property for risk measures. In Optimality and Risk — Modern Trends in Mathematical Finance, pp. 1–28. Springer.

- Black and Perold (1992) Black, F. and A. Perold (1992). Theory of constant proportion portfolio insurance. Journal of Economic Dynamics and Control 16(3-4), 403–426.

- Bouchard et al. (2010) Bouchard, B., R. Elie, and C. Imbert (2010). Optimal control under stochastic target constraints. SIAM Journal on Control and Optimization 48(5), 3501–3531.

- Bouchard et al. (2009) Bouchard, B., R. Elie, and N. Touzi (2009). Stochastic target problems with controlled loss. SIAM Journal on Control and Optimization 48, 3123–3150.

- Boyle and Tian (2007) Boyle, P. and W. Tian (2007). Portfolio management with constraints. Mathematical Finance 17(3), 319–343.

- Cont and Tankov (2009) Cont, R. and P. Tankov (2009). Constant proportion portfolio insurance in the presence of jumps in asset prices. Mathematical Finance 19(3), 379–401.

- El Karoui et al. (2005) El Karoui, N., M. Jeanblanc, and V. Lacoste (2005). Optimal portfolio management with American capital guarantee. Journal of Economic Dynamics and Control 29(3), 449–468.

- Emmer et al. (2001) Emmer, S., C. Klüppelberg, and R. Korn (2001). Optimal portfolios with bounded capital at risk. Mathematical Finance 11(4), 365–384.

- Föllmer and Leukert (1999) Föllmer, H. and P. Leukert (1999). Quantile hedging. Finance and Stochastics 3(3), 251–273.

- Föllmer and Schied (2004) Föllmer, H. and A. Schied (2004). Stochastic finance. An introduction in discrete time. de Gruyter Studies in Mathematics.

- Gundel and Weber (2007) Gundel, A. and S. Weber (2007). Robust utility maximization with limited downside risk in incomplete markets. Stochastic Processes and Their Applications 117(11), 1663–1688.

- He and Zhou (2010) He, X. D. and X. Y. Zhou (2010). Portfolio choice via quantiles. preprint.

- Jin and Zhou (2008) Jin, H. and Y. Zhou (2008). Behavioral portfolio selection in continuous time. Mathematical Finance 18(3), 385–426.

- Jouini et al. (2006) Jouini, E., W. Schachermayer, and N. Touzi (2006). Law invariant risk measures have the Fatou property. Advances in mathematical economics 9, 49–71.

- Kaina and Rüschendorf (2009) Kaina, M. and L. Rüschendorf (2009). On convex risk measures on -spaces. Mathematical Methods of Operations Research 69(3), 475–495.

- Karatzas and Shreve (1998) Karatzas, I. and S. Shreve (1998). Methods of mathematical finance. Springer Verlag.

- Rockafellar and Uryasev (2000) Rockafellar, R. and S. Uryasev (2000). Optimization of conditional value-at-risk. Journal of risk 2, 21–42.