Distribution of the time at which vicious walkers reach their maximal height

Abstract

We study the extreme statistics of non-intersecting Brownian motions (vicious walkers) over a unit time interval in one dimension. Using path-integral techniques we compute exactly the joint distribution of the maximum and of the time at which this maximum is reached. We focus in particular on non-intersecting Brownian bridges (”watermelons without wall”) and non-intersecting Brownian excursions (”watermelons with a wall”). We discuss in detail the relationships between such vicious walkers models in watermelons configurations and stochastic growth models in curved geometry on the one hand and the directed polymer in a disordered medium (DPRM) with one free end-point on the other hand. We also check our results using numerical simulations of Dyson’s Brownian motion and confront them with numerical simulations of the Polynuclear Growth Model (PNG) and of a model of DPRM on a discrete lattice. Some of the results presented here were announced in a recent letter [J. Rambeau and G. Schehr, Europhys. Lett. 91, 60006 (2010)].

I Introduction and Motivations

Extreme value statistics (EVS) is at the heart of optimization problems and, as such, it plays a crucial role in the theory of complex and disordered systems Bouchaud97 ; LeDoussal03 . For instance, to characterize the thermodynamical properties of a disordered or glassy system at low temperature, one is often interested in computing its ground state, i.e. the configuration with lowest energy. Similarly, the low temperature dynamics of such systems is determined, at large times, by the largest energy barriers of the underlying free energy landscape. Thus the distribution of relaxation times is directly related to the statistics of the largest barriers in the systems. Hence, EVS has been widely studied in various models of statistical physics during the last few years Dean01 ; Carpentier01 ; Gyorgyi03 ; Bertin06 ; Fyodorov08 ; Fyodorov09 . This renewal of interest for EVS is certainly not restricted to physics but extends far beyond to biology Omalley09 , finance Embrecht97 ; Majumdar_Bouchaud08 or environmental sciences Katz02 where extreme events may have drastic consequences.

EVS of a collection of random variables , which are identical and independent, or weakly correlated, is very well understood, thanks to the identification of three different universality classes in the large (thermodynamical) limit Gumbel58 . In that case, the distribution of the maximum (or the minimum ), properly shifted and scaled, converges to either (i) the Gumbel, or (ii) the Fréchet or (iii) the Weibull distribution, depending on the large argument behavior of the parent distribution of the ’s. By contrast, much less is known about the EVS of strongly correlated variables. In this context, recent progress has been done in the study of EVS of one-dimensional stochastic processes which provide instances of sets of strongly correlated variables whose extreme statistics can be studied analytically. These include Brownian motion (BM) and its variants – which can be often mapped onto elastic lines in dimensions – Ray01 ; Majumdar04 ; Majumdar05 ; Schehr06 ; Gyorgyi07 ; Majumdar08 ; Rambeau09 ; Randon09 ; Majumdar10_convex ; Krapivsky10 , continuous time random walks and Bessel processes Schehr10 , or the random acceleration process (RAP) Burkhardt07 ; Majumdar10 . Incidentally, it was shown that extreme value questions for such one-dimensional processes have nice applications in the study of random convex geometry in two dimensions. For instance, the extreme statistics of one-dimensional Brownian motion enters into the study of the convex hull of planar Brownian motion Randon09 ; Majumdar10_convex while extreme statistics of the RAP appears in the Sylvester’s problem where one studies the probability that points randomly ch osen in the unit disc are the vertices of a convex -sided polygon Hilhorst08 . These stochastic processes involve a single degree of freedom, or several non-interacting degrees of freedom as in Ref. Randon09 ; Majumdar10_convex ; Krapivsky10 , where independent Brownian motions are considered. A natural way to include the effects of interactions in a ”minimal”, albeit non trivial, model is to constraint these Brownian motions not to cross: this yields a model of non-intersecting Brownian motions, which we will focus on in this paper.

Here we thus consider non-colliding Brownian motions

| (1) |

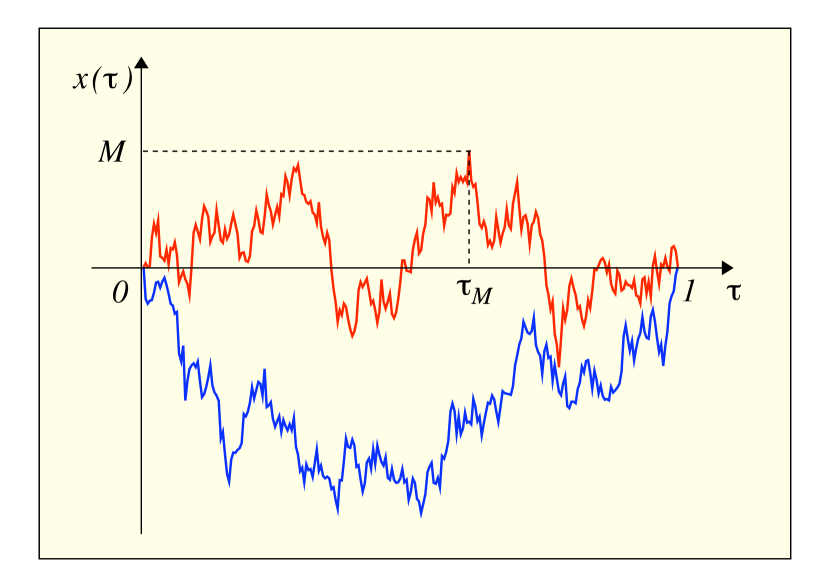

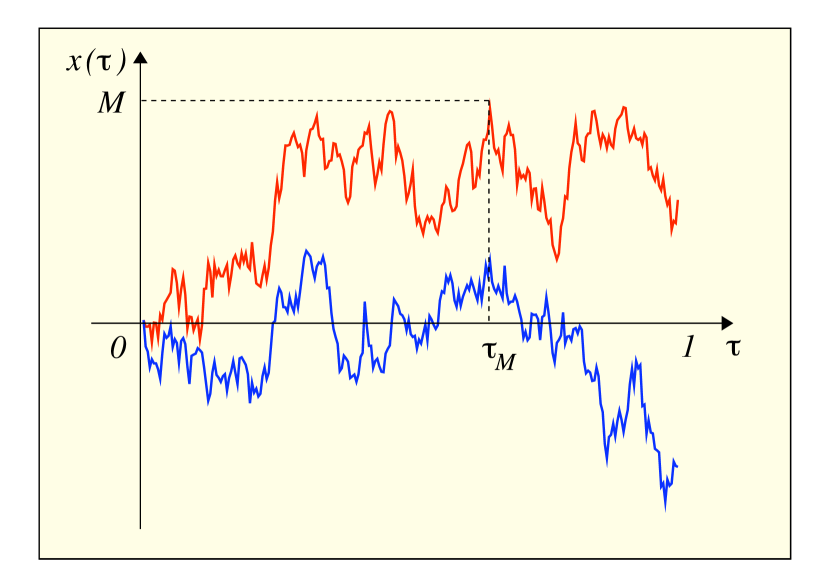

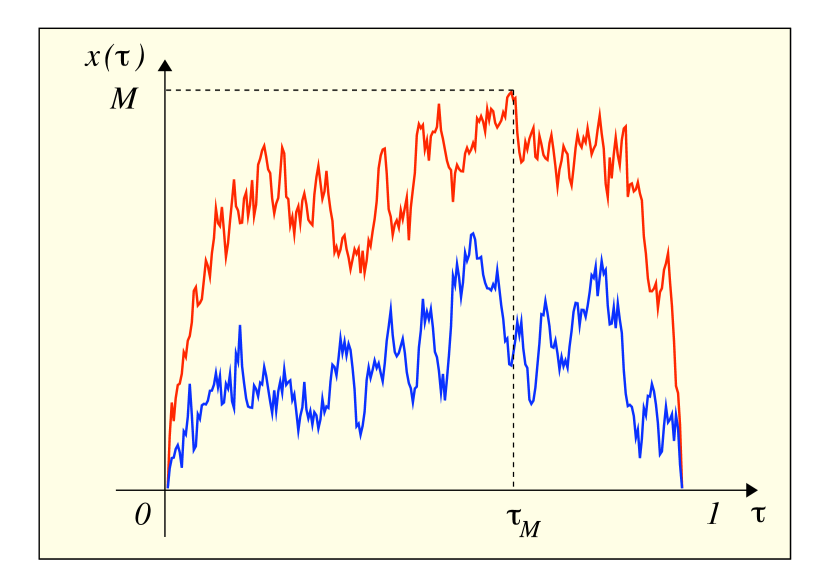

on the unit time interval, . We will consider different types of configurations of such vicious walkers, which are conveniently represented in the plane. In the first case, called ”watermelons”, all the walkers start, at time and end, at time , at the origin (see Fig. 4). They thus correspond to non-intersecting Brownian bridges. In the second case, we will consider such watermelons with the additional constraint that the positions of the walkers have to stay positive (see Fig. 7): we will call these configurations ”watermelons with a wall” and they thus correspond to non-intersecting Brownian excursions. Finally, we will also consider ”stars” configuration, where the endpoints of the Brownian motions in are free. They correspond to non-intersecting free Brownian motions, a realization of which is shown in Fig. 6 for .

Motivated by extreme value questions, we will compute here the joint distribution of the maximal height and the time at which this maximum is reached (see Fig. 4):

| (2) |

The (marginal) distribution of has recently been studied by several authors Feierl07 ; Katori08 ; Schehr08 ; Kobayashi08 ; Feierl09 ; Izumi10 ; Forrester10 , while we have announced exact results for this joint distribution in the two first cases (for bridges and excursions) in a recent Letter Rambeau10 . The goal of this paper is to give a detailed account of the method and the computations leading to these results. On this route we will also provide several new results, including for instance results for the star configuration.

In the physics literature, such non-intersecting Brownian motions were first introduced by de Gennes in the context of fibrous polymers deGennes68 . They were then widely studied after the seminal work of Fisher Fisher84 , who named them ”vicious walkers”, as the process is killed if two paths cross each other. These models have indeed found many applications in statistical physics, ranging from wetting and melting transitions Fisher84 , commensurate-incommensurate transitions Huse84 , networks of polymers Essam95 to persistence properties in nonequilibrium systems Bray04 .

Vicious walkers have also very interesting connections with random matrix theory (RMT), in particular through Dyson’s Brownian motion Dyson62 . For example, for watermelons configurations, it can be shown that the positions of the random walkers at a fixed time , correctly scaled by a dependent factor, are distributed like the eigenvalues of the random Hermitian matrices of the Gaussian Unitary Ensemble of RMT corresponding to Mehta91 . If one denotes by the joint distribution of the positions of the walkers at a given time , in the watermelons configuration, one has indeed (see for instance Ref. Schehr08 for a rather straightforward derivation of this result):

| (3) |

where is a normalization constant and and where we use the notation . This means in particular for the top path that is, at fixed , distributed like the largest eigenvalue of GUE random matrices, which means that in the large limit one has Tracy94-96

| (4) |

where is distributed according to the Tracy-Widom (TW) distribution for , , namely . In the case of watermelons with a wall, the positions of the random walkers are instead related to the eigenvalues of Wishart matrices Schehr08 ; Nadal09 and the fluctuations of the top path are again described by .

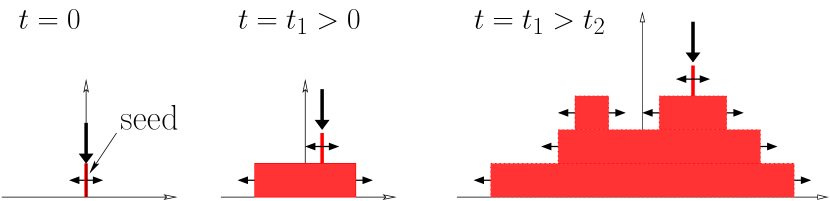

Yet another reason why there is currently a rekindled interest in vicious walkers problems is because of their connection with stochastic growth processes in the Kardar-Parisi-Zhang (KPZ) universality class Kardar86 ; Krug91 in dimensions. This connection is believed to hold for any systems belonging to the KPZ universality class Sasamoto10 , and it can be rigorously shown on one particular model of stochastic growth, the so-called polynuclear growth model (PNG) Franck74 ; Krug89 . It is defined as follows (see Fig. 1). At time a single island starts spreading on a flat substrate at the origin with unit velocity. Seeds of negligible size then nucleate randomly at a constant rate per unit length and unit time and then grow laterally also at unit velocity. When two islands on the same layer meet they coalesce. Meanwhile, nucleations continuously generate additional layers. In the flat geometry nucleations can occur at any point while in the droplet geometry, which we will focus on, nucleations only occur above previously formed layers.

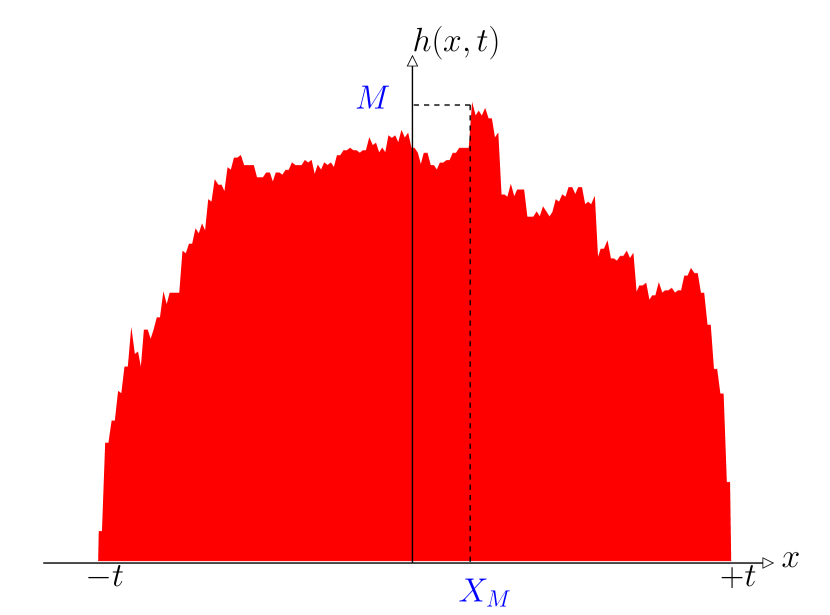

Therefore, for the droplet geometry, denoting by the height of the interface at point and time , one has for . On the other hand, in the long time limit, the profile for becomes droplet-like praeho_thesis , but there remain height fluctuations around this mean value (see Fig. 2 left). The standard way to characterize these fluctuations is to look at the width of the interface with universal exponents and Dhar87 ; Gwa92 , in agreement with the fact that this model belongs to the KPZ universality class. More recently, it was shown for several models belonging to the KPZ universality class Praehofer00 ; Praehofer02 ; Johansson00 ; Gravner01 ; Majumdar_Nechaev04 ; Majumdar06 that, in the growth regime (where is a microscopic time scale) universality extends far beyond the exponents and but also applies to full distribution functions of physical observables. In particular, the scaled cumulative distribution of the height field at a given point coincides with the TW distribution with (respectively ) for the curved geometry (respectively for the flat one), which describes the edge of the spectrum of random matrices in the Gaussian Unitary Ensemble (respectively of the Gaussian Orthogonal Ensemble) Tracy94-96 . Height fluctuations were measured in experiments, both in planar Miettinen05 and more recently in curved geometry in the electroconvection of nematic liquid crystals Takeuchi10 and a good quantitative agreement with TW distributions was found.

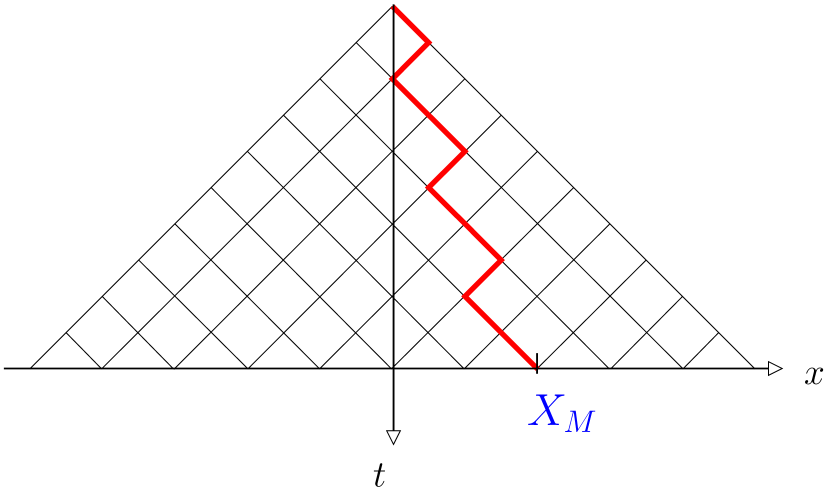

Although the relation with random matrices were initially achieved Praehofer00 through the longest increasing subsequence of random permutations Aldous99 ; Majumdar06 , using in particular the results of the seminal paper by Baik, Deift and Johansson Baik99 , it was then realized that the PNG model in the droplet geometry is actually directly related to the vicious walkers problem in the watermelon configuration Praehofer02 . This was shown through an extension of the PNG model to the so called multi-layer PNG model, where non-intersecting paths naturally appear. Indeed, one can show that the fluctuations of the height field of the PNG model in the droplet geometry are related, in the large time limit to the fluctuations of the top path for the vicious walkers problem in the watermelon geometry in the large limit. This mapping, for reads Praehofer02 ; Ferrari08 :

| (5) |

where is the Airy2 process Praehofer02 which is a stationary, and non-Markovian, process. In particular, , which is consistent with Eq. (4). Hence, from Eq. (I) and map onto and in the growth model while plays essentially the role of (to make the correspondence between and exact one has to consider a watermelon configuration in the interval ). To characterize the fluctuations of the height profile in the droplet geometry beyond the standard roughness it is natural to consider the maximal height and its position Rambeau10 (see Fig. 2). According to KPZ scaling, one expects while . On the other hand from Eq. (I), the joint distribution of and can be written as

| (6) |

where is the joint distribution of the maximum and its position for the process . Finally, the relation (I) also gives us some interesting information for the vicious walkers problem. In the large limit, one has indeed from Eq. (I) that the joint distribution for the watermelons configuration is also given by . One has indeed, for :

| (7) |

and therefore Eq. (6) and Eq. (7) show that one can obtain the distribution of for the growth model from the large limit of the joint distribution , which we compute here for any finite .

It is also well known that stochastic growth models in the KPZ universality class can be mapped onto the model of the directed polymer in a disordered medium (DPRM) Krug91 ; Halpin95 . This is also the case of the PNG model and to make this connection as clear as possible, we consider a discrete version of the PNG model introduced by Johansson Johansson03 . It is a growth model with discrete space and discrete time. The height function is now an integer value while and . The dynamics is defined as follows

| (8) | |||||

where the first term reproduces the lateral expansion of the islands (and also their coalescence when two of them meet) in the continuous PNG model while is a random variable, distributed independently from site to site, which corresponds to the random nucleations (see Fig. 1).

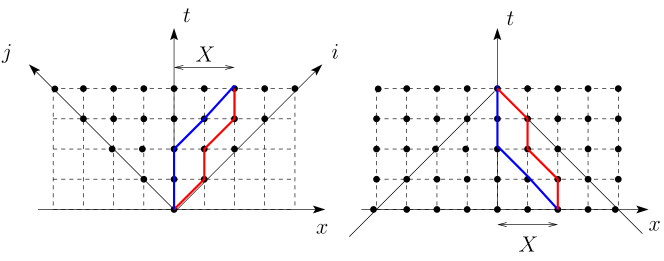

In the droplet geometry, one has if while this constraint is removed in the flat geometry. To understand better the connection between this model (8) and a model of directed polymer, we perform a rotation of the axis (Fig. 3) and define

| (9) |

One can then simply check (for instance by induction on ), that the height field evolving with Eq. (8) in the droplet geometry, is given by

| (10) |

where is the ensemble of directed paths of length , starting in and terminating in (Fig. 3). This formula (10) establishes a direct link between the PNG model and a model of directed polymer. Indeed, the height field corresponds the energy of the optimal polymer (which is here the polymer with the highest energy) with both fixed ends in and and where the random energies, on each site, are given by . The aforementioned result for the distribution of shows that the fluctuations of the energy of the optimal polymer are described in this case by , the Tracy-Widom distribution for . The study of this distribution, for the DPRM in continuum space, has recently been the subject of several works, both in physics dprm_doussal and in mathematics dprm_math .

Similarly, one can also write the height field in the flat geometry (here of course the fluctuations of the height field are invariant by a translation along the axis). One has indeed :

| (11) |

where is the ensemble of directed paths of length , starting in and ending in (see Fig. 3). Given that these two ensembles and are obviously similar (Fig. 3), these two equations (10) and (11) allow to write krug_dprm

| (12) |

For the directed polymer, corresponds to the energy of the optimal polymer, of length and with one free end. From that Eq. (12), one sees that the joint distribution of and in the vicious walkers problem corresponds to the joint distribution of the energy and the transverse coordinate of the free end of the optimal polymer. From the aforementioned results for the distribution of , we also conclude that the cumulative distribution of is given by , the Tracy-Widom distribution for . Although this result was obtained rather indirectly using this relation (12), it was recently shown directly by computing the cumulative distribution of the maximal height of non-intersecting excursions in the limit , in Ref. forrester_npb . We conclude this paragraph about the DPRM by noticing that this model, with one free end, has been widely studi ed in the context of disordered elastic systems toy_model , in particular using the approximation of the so-called ”toy-model” where the Airy2 process in (I) is replaced by a Brownian motion LeDoussal03 ; toy_model . A recent discussion of the toy model and its applications to the DPRM can be found in Ref. vivien . We also mention that physical observables related to have been studied for the DPRM in different geometry, like the winding number of the optimal polymer on a cylinder brunet_cylindre .

The paper is organized as follows. In section II we present in detail the method to compute the joint distribution of and for non-intersecting Brownian motions. We will show results for bridges, excursions and stars. In section III, we will extend this approach for any number of vicious walkers both for bridges and excursions. We will then confront, in section IV, our analytical results to numerical simulations, which were obtained by simulating Dyson’s Brownian motion, before we conclude in section V. Some technical details have been left in the appendices.

II Distribution of the position of the maximum for two vicious Brownian paths

II.1 Introduction

Our purpose is to study simultaneous Brownian motions , subjected to the condition that they do not cross each other. In the literature, such system has been studied first in the continuous case by de Gennes deGennes68 , and in the discrete case by Fisher Fisher84 . He named this kind of system vicious walkers, as the process is killed if two paths cross each others. The name ‘vicious Brownian paths’ will refer in the following to Brownian paths under the condition that they do not cross each other.

In this Section, we focus on the case . The two vicious Brownian paths start at and obey the non-crossing condition for . We examine three different geometries:

-

(i)

periodic boundary conditions where we consider non-intersecting bridges, also called ”watermelons” configurations (see Fig. 4): this will be treated in subsection E,

-

(ii)

free boundary conditions where we consider non-intersecting free Brownian motions, also called ”stars” configurations (see Fig. 6): this will be treated in subsection F,

-

(iii)

periodic boundary conditions, plus a positivity constraint where we consider non-intersecting excursions, also called ”watermelons with a wall” configurations (see Fig. 8): this will be treated in subsection G.

We compute, for each case, the joint distribution of the couple which are respectively the maximum of the uppermost vicious Brownian path, and its position : . Integrating over , we find the probability distribution function (pdf) of the time to reach the maximum .

This computation is based on a path integral approach, using the link between the problem of vicious Brownian paths and the quantum mechanics of fermions. This is described in subsection B. Then we present, in subsection C, the method to compute the joint probability distribution function of the maximum and the time to reach it for vicious Brownian paths, with general boundary conditions. An emphasis is put on the regularization scheme, essential to circumvent the basic problem of Brownian motion which is continuous both in space and time: you cannot force it to be in a point without re-visiting it infinitely many times immediately after. At this stage, general formulae will be obtained, and will be used directly in the paragraphs E, F and G. The extension to a general number of paths will be treated straightforwardly in Section III.

II.2 Path integral approach: treating the vicious Brownian paths as fermions

Let us consider two Brownian motions, obeying the Langevin equations

| (13) |

where ’s are independent and identical Gaussian white noises of zero mean, i.e. and . Taking into account the non-crossing condition, the probability that the two paths end at at time , given that they started at at time is

| (14) |

where the subscript ’’ in the notation means that we treat the case of Brownian paths. The exponential terms are the weight of each Brownian path, and the Heaviside theta function ensures that the paths do not cross. In this Section, bold letters will denote vectors with two components, such as for example the positions at a given time of the two Brownian paths or the starting points . In the previous formula (14), is a normalization constant, such that

| (15) |

Notice that the integration is ordered, and we will write it shortly .

We recognize in formula (14) the path integral representation of the quantum propagator of two identical free particles, subjected not to cross each other. In one dimension, this can be implemented by requiring that the two particles are fermions deGennes68 ; Schehr08 . Therefore the probability reduces to the quantum propagator of two identical fermions in one dimension:

| (16) |

with the total Hamiltonian of the two-particle system , being the identity operator acting in the Hilbert space of the particle. The one-particle Hamiltonians are (for ) in a position representation. The states (and ) are the tensorial product of the one-particle eigenstates of position , where each state obeys the eigenvalue equation , with the position operator acting in the Hilbert space of the particle, and the position of this particle.

In our calculations we deal with more general Hamiltonians, but they will be written in the same way as the sum of individual one-particle Hamiltonians (no interaction between the two particles), and with (identical particles). Thus we will treat systems of two identical indistinguishable particles, so that one can write down a two-particle eigenstate of the total Hamiltonian as an antisymmetric product of the one-particle eigenstates of . Explicitely, if and are two eigenstates of the one-particle Hamiltonian , with energies and , then the eigenstate of the two-particle problem with energy is

| (17) |

Projecting onto the position basis , and using the general notation (lower-case letter for one particle wave function), and (capital letter for the two particle wave function), this is the usual Slater determinant

| (18) |

Hence inserting the closure relation into (16), one obtains the spectral decomposition of the propagator (with )

| (19) |

This result can also be found via the Karlin-McGregor formula karlin_mcgregor . It states that the probability of propagating without crossings is nothing but the determinant formed from one-particle propagators (named ):

| (20) |

The discrete version of this formula (20) is given by the Lindström-Gessel-Viennot (LGV) theorem LGV . The basic idea behind this formula is nothing but the method of images. To recover our quantum mechanical expression obtained by considering fermions (19), one has to express the one-particle propagator as

| (21) |

and use the Cauchy-Binet identity (169).

II.3 Joint probability distribution of position and time

The method to compute the distribution of the maximum and the time at which it is reached can be described as follows. Let us consider the process of such Brownian paths with the non-intersecting condition with and . Keeping the same notations, the starting points are and , or , and the end-points are and , or . First we consider and as fixed. Given a set of points , and an intermediate time , such as , we ask what is the probability that and ? In other terms, we seek the joint probability density of , given that the paths start in at and end in at . The answer to this question is well known from quantum mechanics: cut the process in two time-intervals, one from to , and the second piece from to . Because of the Markov property, these two parts are statistically independent, and one should take the product of propagators to obtain the joint pdf of , given that the initial and final conditions are respectively , and :

| (22) |

where is the normalization constant, obtained by integrating over all possible cuts , and all possible intermediate points

| (23) |

where we remind that the integration over is ordered: . Using the closure relation of the states , one finds that

| (24) |

Because we will not care about the lowest path and its intermediate position in the following, we compute the marginal by integrating over all possible values of , obtaining the joint probability density that the upper path is in at time given that the paths start in at time and end in at time :

| (25) |

From now on we will set, for simplicity, . This can be done without loss of generality because the Brownian scaling implies and . A simple dimensional analysis allows to resinsert the time in our calculations.

II.4 Maximum, and the regularization procedure

The maximum and the time to reach it are defined by

| (26) |

Hence, to compute the joint probability of the couple , we want to impose and , knowing that the upper path does not cross the line . This condition is implemented by inserting the product of Heaviside step functions

| (27) |

in the path integral formula (14). The propagator of two vicious Brownian paths, with the constraint that they do not cross , reads

| (28) |

for all , and . The second Heaviside step function does not change the value of the path integral (it does not select a smaller class of paths) because for all , if and , then automatically. Accordingly to our first analysis, this propagator (28) reduces to the propagator of two identical fermions without interaction between them, but with a hard wall in . Hence the associated Hamiltonian is

| (29a) | |||

| with the one particle Hamiltonian | |||

| (29b) | |||

| for , where is the hard wall potential in : | |||

| (29c) | |||

| This one particle Hamiltonian has eigenfunctions | |||

| (29d) | |||

| with the associated energies | |||

| (29e) | |||

| Hence, with these informations, one is able to compute the propagator using the spectral decomposition, as in Eq. (19): | |||

| (29f) | |||

with the Slater determinant built with the one particle eigenfunctions (29d).

To obtain the joint pdf of and , one would insert this propagator in formulas (22-25), with and . With this procedure one naively finds zero, because we impose the intermediate point to be on the edge of the hard wall potential. This problem originates in the continuous nature of the Brownian motion: once in a point, the Brownian motion explore its vicinity immediatly before and after feller . This implies that we cannot prescribe the upper path to be in without being in for close to . Another problem is that the normalization constant can not be written as a single propagator. Indeed one can not insert the closure relation as we did from Eq. (23) to Eq. (24), because the potential depends actually on the position .

Hence one should prescribe a regularization scheme to avoid this phenomenon. A common way to deal with it is to take , with a small regularization parameter, compute all quantities as functions of , and at the end take the limit . This regularization scheme is similar to that introduced in Ref. Majumdar08 . Following the same ideas, one obtains the joint pdf as

| (30a) | |||

| where is the probability weight of all paths starting in and ending in in the unit time interval and such that , and is the normalization constant. Explicitly, one has | |||

| (30b) | |||

| for all , and where we write a dummy integration over with the delta function forcing to be . The normalization depends on the regularization parameter | |||

| (30c) | |||

In the following paragraphs, all three configurations have their paths beginning at the origin. The problem of the continuous Brownian paths forbids to take directly . Instead of that, we will separate artificially the paths by an amount . Details of this regularization are left in the concerned paragraphs.

II.5 Periodic boundary condition: vicious Brownian bridges

In this case, the two paths start from the origin at and arrive also at the origin at final time : . Without extra condition, this defines two Brownian bridges. Here we compute the joint probability density function for two Brownian bridges, under the condition that they do not cross each other.

As discussed before, there is again a regularization scheme to adopt in both starting and ending points. We separate by an amount the two paths at the starting and ending points, taking . At the end of the computation, we shall take the limit . Then the joint probability density function for two vicious Brownian bridges is

| (31a) | |||

| where is defined in Eq. (30a). The numerator of Eq. (30a), the probability weight, reads | |||

| (31b) | |||

| and the denominator of Eq. (30a), i.e. the normalization, is given by | |||

| (31c) | |||

| where the subscript refers to ‘Bridges’, and with the relation deduced from Eq. (30a) | |||

| (31d) | |||

We obtain this limit by expanding the numerator and the denominator in power series of and , keeping only the dominant term in each case.

To compute the probability weight , we start with Eq. (30b), in which we put :

| (32) |

Using the spectral decomposition (29f), one has

| (33) |

The integral over is easy due to the delta function. By antisymmetry of Slater determinants in the exchange of and , the product is symmetric in the exchange of and . Then one can replace by twice the product of its diagonal terms which is

| (34) |

The same operations applies to .

| (35) |

Permuting the order of integrations, one can compute the integration with respect to as

| (36) |

due to the orthonormalization of the eigenfunctions . Performing the integration over leads to, at lowest order in ,

| (37) |

The next step is to expand in powers of inside the Slater determinants: the first column does not depend on , and in the second column, we expand at order , each of the two elements, sweeping the constant term by linear combination with the first column. This yields

| (40) | ||||

| (43) | ||||

| (44) |

where we use the scaled variables and the determinant

| (45) |

Performing the same expansion in powers of in , with , one can identify the dominant term as a factor of the product of powers , so that

| (46) |

Inserting the expansion (44) in (37), and identifying the the leading term, one obtains

| (47) |

It can be written in the more compact form

| (48) |

with the help of the function

| (49) |

which can also be written as a determinant:

| (50) |

and are the first and second Hermite polynomials. This expression is obtained by factorizing all the -dependence in the last line of the determinant, and performing the integration directly in this last line. The Hermite polynomials then appear naturally, see Appendix E. Then one proceeds to the expansion of the determinants with respect to their last lines, which permits the integration over (four terms, because there are two determinants ), and one obtains a simple, though long, expression (apart from the exponentials, only algebraic terms appear).

The limit in Eq. (31d) exists provided the normalization constant admits the following expansion

| (51) |

where is a number (independent of and ). It can be computed using the normalization of the joint pdf

| (52) |

One finds . The joint pdf reads

| (53) |

where for compactness we use the Hermite polynomial .

A direct integration over gives the probability distribution function of , the time at which the maximum is reached, regardless to the value of the maximum:

| (54) |

The fact that enters in this expression only through the product reflects the symmetry of the distribution around , which of course is expected for periodic boundary conditions. To center the distribution, over an unit length interval, one can use , and the distribution of is then

| (55) |

Two asymptotic analysis can be made:

-

•

for (or equivalently ), one has

-

•

and for in the vicinity of , better written in terms of the behaviour in of the centered distribution

(56)

Furthermore, an integration of with respect to gives the pdf of the maximum (the derivative of the cumulative distribution). Using the change of variables , the integral gives

which coincides with the result computed in Ref. Schehr08 , .

II.6 Free boundary conditions: stars configuration

In this subsection, we consider two vicious Brownian paths starting from the origin with free end-points: this is the star configuration (a subscript ’’ will be used). The starting points are the same as before , but the endpoints are free, so that for fixed, we sum over all endpoints such that . Hence one has

| (57) |

where the probability weight is given by

| (58) | ||||

where the integrations satisfy and respectively. The normalization is such that

| (59) |

As in the previous subsection, we will use only the leading order term of the expansion of and in powers of and . The computation of the probability weight can be done along the same lines as before (33-37), keeping in mind that only the final points change. At lowest order in , one has

| (60) |

where we have integrated over first, and then over , with the delta function coming from the closure relation of eigenfunctions. For the eigenfunctions evaluated in the final points one obtains

| (61) |

in terms of the previous , and with the variables (for ). Using the expansion in written in Eq. (44), one finds the leading order to be ) so that the expansion is

| (62) |

with

| (63) |

where is given in Eq. (45). As before, the integration over the moments and , corresponding to the top walker, can be factorized in the determinants. From the part , one recognizes , and for the part , we introduce

| (64) |

With the help of the two functions and , one obtains

| (65) |

and can be written as determinants, as in Eq. (50), and

| (66) |

where we used the relation in Eq. (239), and where stands for (for compactness). The fact that we do not have the periodic boundary conditions introduces an asymmetry, thus the two determinants and do not have the same form.

As before we also expand the normalization in powers of and , the leading term being

with a number, independent of and which can be computed by the normalization condition:

| (67) |

One finds , and the joint probability distribution function, for two stars configuration is

| (68) |

Integrating over one obtains the marginal, i.e. the pdf of the time to reach the maximum

| (69) |

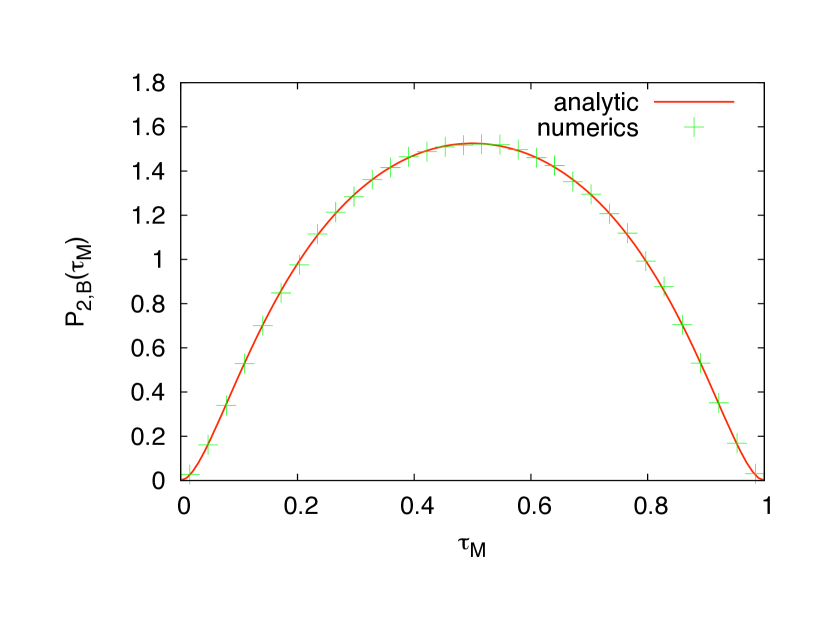

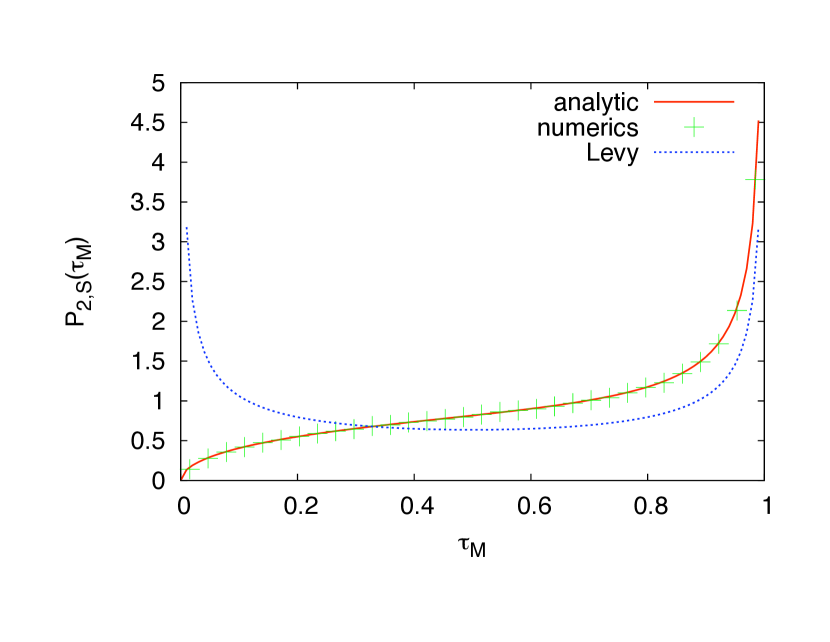

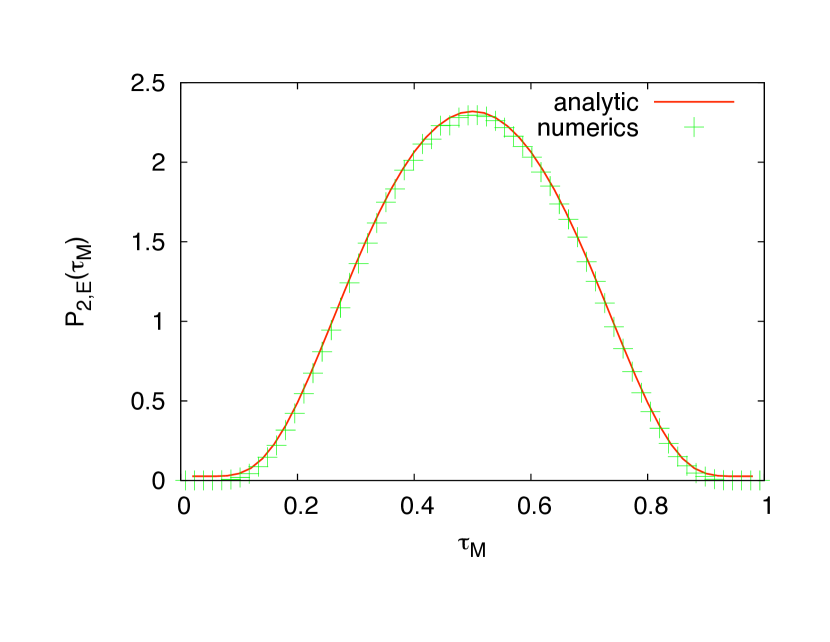

which is plotted with a comparison with numerical simulation in Fig. 7.

One easily obtains the asymptotic behavior of the distribution of the time :

-

•

for , one has

-

•

for the probability distribution diverges as

which can be compared to the divergence of the distribution of the time for one Brownian motion (the Lévy arcsine law, plotted in Fig. 7) . The fact that we have another uncrossing Brownian path below preserves the exponent of the divergence, but changes slightly the prefactor.

Notice finally the mean value is given by and that the sign of the derivative of changes in .

II.7 Periodic boundary condition and positivity constraint: excursions configuration

Now we come to the computation of the joint probability distribution of the maximum and its position for the configuration of vicious Brownian paths subjected to stay in the half line , in addition to the periodic condition: the two paths start in and end in at . This corresponds to two Brownian excursions, with the non-crossing condition (we will use the subscript ’’).

The positivity constraint is easily implemented in the path integral formulation by adding another hard wall in . The potential associated to each of the two fermions then reads

| (70a) | |||

| The eigenfunctions of the one-particle Hamiltonian | |||

| (70b) | |||

| are given by | |||

| (70c) | |||

| with the associated eigenvalues | |||

| (70d) | |||

| This allows to express the corresponding propagator, for any point , and time , as: | |||

| (70e) | |||

where is a couple of two positive integers, and in which we use the Slater determinant .

Here the regularization is necesary for the boundary values of both fermions, because the lowest path cannot start and end exactly in . Therefore we put and , where the notation differs slightly from the previous one . For this geometry, one uses Eqs. (30a-30c) to obtain the probability weight

| (71a) | ||||

| where the ordered integral covers the domain . The normalization function is | ||||

| (71b) | ||||

| so that | ||||

| (71c) | ||||

Inserting the spectral decomposition of the propagator (70e) in Eq. (71a), one has

| (72) |

We follow the same procedure as before in Eqs. (33-37): using the symmetry in the exchange of indices ( and ) we express the two Slater determinants as the product of their diagonal components

| (73) |

An expansion at lowest order in of this expression, making use of

| (74) |

together with the closure relation of the eigenfunctions

| (75) |

yields

| (76) |

The expansion to the lowest order in of the eigenfunctions reads

| (77) |

where is the Van der Monde determinant

Hence to lowest order, one has

| (78) | |||

To ensure the joint pdf to exist, the normalization must have the same dominant term

Combining these expansions in Eq. (II.7) and in Eq. (II.7) one obtains from Eq. (71c):

| (79) |

where the computation of normalization has been left in Appendix C.

This formula is well suited for an integration over to deduce the marginal law of :

| (80) |

which is plotted in Fig. 9.

Following the methods introduced in Majumdar08 , one is able to compute the asymptotic behavior of when . Starting from the expression of the joint distribution of in Eq. (79), one writes the integral over to get the marginal distribution as

and perform a change of variable

| (81) |

One obtains

| (82) |

When , the argument of the first exponential becomes at leading order, and the dominant term in the sums over and is given by and because of the factor , which enforces . Hence to leading order, one has

| (83) |

By differenciating times the Jacobi identity

| (84) |

with respect to , one has at leading order when

| (85) |

With , one obtains at leading order

| (86) |

which can be approximated by a saddle point method. At leading order when , one obtains

| (87) |

By symmetry one obtains the same behavior when by replacing by in the above formula.

As in the previous paragraphs, it is possible to have a compact formula for the joint pdf, anticipating the general computation for vicious Brownian paths. Let us introduce , the analogue of (49) in this discrete case:

| (88) |

with a generic index standing for () or (). Factorizing the sum over in the last line of the Vandermonde determinant, and using sums defined by

| (89) |

one is able to write

| (90) |

Hence the joint pdf can be expressed in a factorized way, reminiscent of the formula for the watermelons case (48)

| (91) |

In the following we will extend these formula, for bridges and excursions, to particles, for generic .

III Distribution of the position of the maximum for vicious Brownian paths

In this section, we extend the previous method to any number of vicious Brownian paths, ordered as for (again we take a unit time interval, without loss of generality). We want to compute the joint pdf of , respectively the maximum and the time to reach it for different configurations, with

| (92) |

In the same way as in the previous section, the non-colliding condition translates into treating indistinguishable fermions. They do not interact between each other but are all subjected to the same potential (which is one or two hard wall(s) potential in our computations). The Hamiltonian of the system is

| (93) |

with identical one particle Hamiltonians , for . If is the eigenfunction of associated to the energy , one can write the eigenfunction of the -particles problem as a Slater determinant

| (94) |

with and where we used the bold type for vectors: . Hence the propagator reads as in formula (19), but with determinants of matrices. The method to compute the joint probability density function is exaclty the same as before, replacing -vectors by -vectors in formulas (30).

III.1 vicious Brownian bridges

We first consider the watermelon configuration, i.e. the case of on-intersecting Brownian bridges (see definition in subsection II.5). The periodic boundary conditions impose the starting and ending points to be at the origin. As discussed before, this needs a regularization scheme, and we take . The joint pdf is

| (95) |

where is the probability weight of all paths starting and ending in with , given by

| (96) |

is the propagator of indistinguishable fermions, each of them having the one-particle Hamiltonian (29b), with eigenfunctions and eigenvalues given by Eqs (29d, 29e).

The starting point of our computation is given by Eq. (33) with the upper point is now . All the manipulations done before for 2 paths extend to paths. A subtelty is the fact that the ordered integral over the domain is proportional to the same unordered integral over the domain for , because of the symmetry of the integrand. This is shown in Appendix A. With the same argument of symmetry between the exchange of any , and the same for one could use only the diagonal terms for the two Slater determinants expressed in . After permuting the -integrals with the -integrals, this operation gives closure relations, i.e. a product of Dirac delta functions , and the product . The expansion of the Slater determinants evaluated at the initial and final points involves now the function

| (97) |

with the rescaled variables . After the aforementioned manipulations, one finds at lowest order

| (98) |

together with

| (99) |

Therefore one obtains from Eqs (98) and (99) together with Eq. (95):

| (100) |

where

| (101) |

depends on variables . In Eq. (100) the amplitude , whose computation is left in Appendix C, is given by

| (102) |

Moreover the function defined by Eq. (101) can be written as a determinant: is a determinant, and the integration over can be absorbed in its last line. The elements of this last line are indexed by the column index :

| (103) |

with the help of the family of functions

| (104) |

where is the Hermite polynomial of degree (see formula 238). Then is the determinant of a matrix, whose elements indexed by are given by

| (105) |

The next step is to expand the determinant in minors with respect to its last line:

| (106) |

where denotes the determinant of the minor of the matrix , obtained by removing its line and its column. These minors only involves the and , not . Expanding the product of the two functions entering into the expression (100) yields

| (107) |

The dependence on the variables ’s appears only in the last line of that expression (107), and the Cauchy-Binet formula (169) allows to compute the integration with respect to of the product of determinants of minors:

| (108) | |||

where are respectively the line and column indices of the matrix of which we take the determinant, and is the matrix with elements

| (109) |

This matrix enters into the expression of the cumulative distribution of the maximal height of watermelons Feierl09 :

| (110) |

Putting together (107) and (108) in formula (100), and dividing by given in Eq. (99), one finds the joint pdf of and

| (111a) | |||

| or equivalently | |||

| (111b) | |||

with the normalization constant .

It is also interesting to characterize the small behavior of the distribution of . To study it, it is useful to start from Eq. (100) which, after integration over yields

| (112) |

with . To study the behavior of when , we perform the changes of variables , for so that when , one has to leading order

Besides, one has, also to leading order

| (114) | |||||

and similarly

| (115) | |||||

with some regular function . However, being anti-symmetric under the permutation of the variables ’s it is easy to see that this leading order term (114, 115) vanishes after the integration over in Eq. (III.1). In fact if one writes the low expansion of the product as

| (116) |

where ’s are functions of one can show that the first non-vanishing term, after integration over these variables, corresponds to with for , for and more generally for generic . Therefore one has, to leading order

| (117) |

although the explicit calculation of the amplitude is a very hard task.

III.2 vicious Brownian excursions

We now consider watermelons with a wall, i.e. excursions under the non-crossing condition (see the definition in paragraph II.7). Again the starting and ending points are at the origin, but with this configuration we must use , which is slightly different from the cases of bridges, because now, all paths must be positive. The joint pdf of and is

| (118) |

where the probability weight of all paths starting and ending in , verifying for all the non-crossing condition , and for which , reads

| (119) |

Here the integration is over the ordered domain . The boundary conditions of the excursions configuration enforce the use of the propagator associated to fermions confined in the segment (70e): the Hamiltonian is of the form (93), with the one particle Hamiltonian (70b).

One can follow the first steps of the paragraph II.7, replacing now -vectors by -vectors. As in the bridge case, the ordered integration can be set unordered (i.e. integrating over for all ), with a numerical prefactor (see appendix A). The spectral decomposition is done with sums over indices and , as in formula (72). Using the symmetry of the integrand under the exchanges of any couple and (for ) one can write the Slater determinants of the intermediate point (at ) under their diagonal form, with a numerical prefactor, irrelevant in the computation. Hence one has the formula

| (120) |

where is given in Eq. (70c). The expansion to lowest order in gives closure relations (the last line of the preceding expression)

| (121) |

and we use formula (74) to get

| (122) |

where . One can then use the expansion to lowest order in

| (123) |

where is the Vandermonde determinant. In this formula the first line contains only numerical constants, irrelevant for the computation (they will be absorbed in the normalization constant), only the second line is relevant, containing the dependence in and in the indices of the sums , and the lowest order in . Hence one has to lowest order

| (124) |

as well as, for the normalization,

| (125) |

with a number. Taking the double limit one obtains the joint probability

| (126) |

where the numerical constant is given by (see appendix C.2)

| (127) |

Following the notations introduced in the case, we define [writing for compactness the -uplet ]

| (132) |

where we used the property of the Vandermonde determinant to factorize the sum with respect to in the last line of the determinant, which plays the role of associated to , or the role of with , resulting in elements like , for

| (133) |

With this notation, we obtain the compact formula

| (134) |

which is the “discrete” analogue of formula (100) obtained in the case of bridges.

The ultimate step is to expand each determinant with respect to their last line. Then, using the discrete Cauchy-Binet identity with respect to the sums over , one has

| (135) |

with the normalization

| (136) |

and where appear the minors of the matrix whose elements are, for

| (137) |

This matrix enters into the expression of the cumulative probability of the maximum Katori08 :

| (138) |

Defining the vector with elements, for ,

| (139) |

one is able to express the result as the determinant

| (140a) | |||

| or as the matrix product | |||

| (140b) | |||

The behavior of the marginal distribution when can be obtained as explained in paragraph II.7 for vicious excursions. The leading behavior, when , is given by

| (141) |

However the algebraic correction to this leading behavior is hard to evaluate.

IV Numerical simulations

In this section we present the results of our numerical simulations of the distribution both for the cases of bridges and excursions. To generate numerically such watermelons configurations we exploit the connection between these vicious walkers problems and Dyson’s Brownian motion, which we first recall.

IV.1 Relationship with Dyson’s Brownian motion

To make the connection between the vicious walkers problem and Dyson’s Brownian motion, we consider the propagator of the vicious walkers

| (142) |

which is the probability that the process reaches the configuration at time given that at time : this is thus a conditional probability. This propagator satisfies the Fokker-Planck equation:

| (143) |

together with the initial condition

| (144) |

and the non-crossing condition, which is specific to this problem,

| (145) |

On the other hand, let us focus on Dyson’s Brownian motion. For this purpose we consider random matrices whose elements are time dependent and are themselves Brownian motions. For instance, for random matrices from GUE, i.e. with , we consider random Hermitian matrices , of size , which elements are given by

| (146) |

where and are independent Brownian motions (with a diffusion constant ). We denote the eigenvalues of (146) [or more generally of a matrix belonging to a ensemble with which is constructed as in Eq. (146) with the appropriate symmetry]. One can then show that the ’s obey the following equations of motion (which define Dyson’s Brownian motion) Mehta91 ; Dyson62

| (147) |

where ’s are independent Gaussian white noises, . Let be the propagateur of this Dyson’s Brownian motion (147). It satisfies the Fokker-Planck equation

| (148) |

Of course, one has also here if , for any time and from Eq. (IV.1) one actually obtains

| (149) |

This Fokker-Planck equation can be transformed into a Schrödinger equation by applying the standard transformation risken_book :

| (150) | |||||

where is such that

| (151) |

On the other hand, given Eqs (149) and (150) one has

| (152) |

From Eqs (IV.1) and (150), one obtains that satisfies the following Schrödinger equation

| (153) |

Hence for a generic value of , (153) is the Schrödinger equation associated to a Calogero-Sutherland Hamiltonian (on an infinite line) calogero ; sutherland . However for the special value , the strength of the interaction vanishes exactly and in that case the equation satisfied by (149, 151, 153) is identical to the one satisfied by the propagator in the vicious walkers problem (143, 144, 145) : in that case Eq. (153) corresponds to the Schrödinger equation for free fermions. In other words, for the special value there exists a simple relation between vicious walkers and Dyson Brownian motion which can be simply written as

| (154) |

In particular, for watermelons without wall on the unit time interval, for which the initial and final positions coincide, this relation (154) tells us that this process is identical to Dyson’s Brownian motion where the elements of the matrices are themselves Brownian bridges i.e. , in Eq. (146) such that and . This then allows to generate easily watermelons because one can generate a Brownian bridge on the interval from a standard Brownian motion via the relation .

For non-intersecting excursions, one can show that the dynamics corresponds to Dyson’s Brownian motion associated to random symplectic and Hermitian matrices, as explained in Ref. Katori08 .

IV.2 Numerical results

To sample non-intersecting Brownian bridges we use the aforementioned equivalence to Dyson’s Brownian motion. We consider the discrete-time version of the matrix in Eq. (146), at step :

| (155) |

where are independent discrete-time Brownian bridges. They are constructed from ordinary discrete-time and continuous space random walks where each jump is drawn from a Gaussian distribution. The aforementioned relation, to construct Brownian bridges, reads in discrete time .

Diagonalizing the matrix at each step gives the ordered ensemble of distinct eigenvalues , which is equivalent to a sample of non-intersecting Brownian bridges, see Eq. 154. For each sample, we keep in memory the maximal value of , and the step time at which . The plots shown here are obtained by making the histogram of the rescaled time (with a bin of size to smoothen the curve), with steps averaged over samples, for . For Brownian excursions, one has to use another symmetry for the matrix, which is explained in Ref. Katori08 .

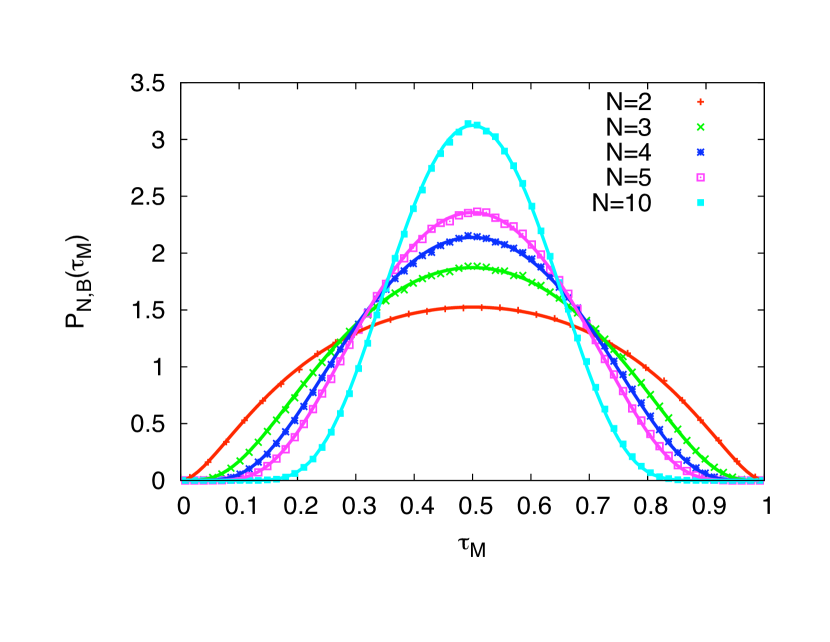

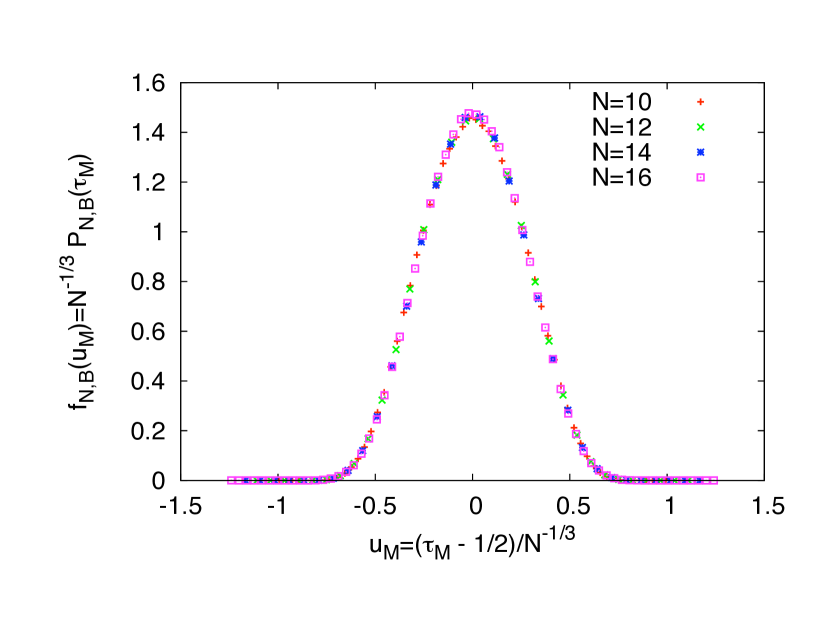

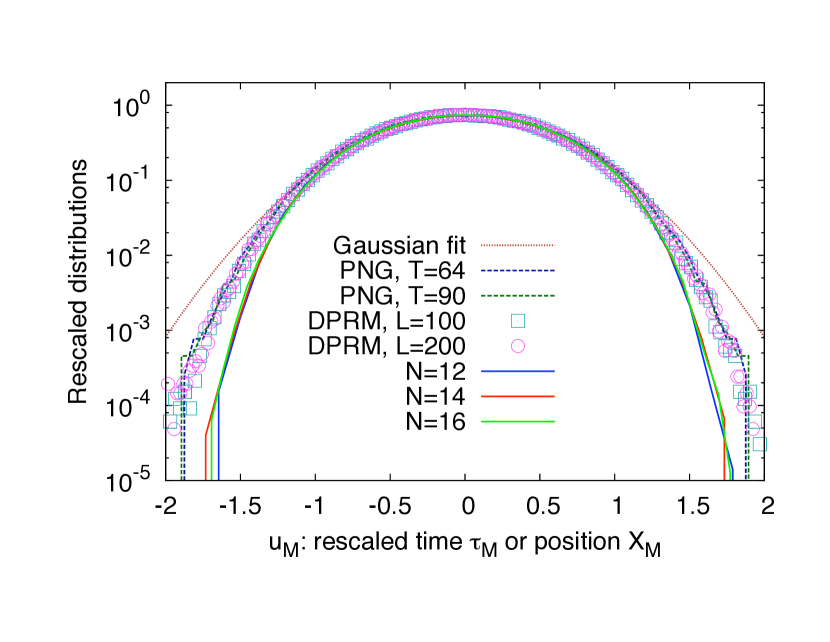

First we present the comparison between our exact result for Brownian bridges and numerical simulations, for . The agreement between our numerical results and our exact analytical formula is perfect, see Fig. 10. Then, anticipating on the applocation of our results to growing interfaces, we show a plot of the rescaled distribution as a function of the rescaled time . Despite the fact that this scaling requires in principle that , one sees that the rescaled distributions for moderate values of fall on a single master curve, see Fig. 11. However, given the relatively narrow range of explored in these simulations, one can not be sure that the asymptotic, large , behavior is reached.

To compare our analytical results for -watermelons to growing interfaces models and the DPRM, we have simulated both the PNG model and a discrete model of DPRM on a lattice. To sample the PNG model, we have applied the rules that were discussed before (see Fig. 1) where the time interval is discretized. In particular we use a discretization of the nucleation process: at each time step, a nucleation occurs at site such that with a small probability , whose value is chosen such that one recovers a uniform density of nucleation events in the continuum limit. The interface evolves during a time . We compute the distribution of the position of the maximal height of the droplet (see Fig. 2 left), averaged over samples. In Fig. 12 we have plotted the distribution of the rescaled position for and (both of them being statistically independent): the collapse of these data on a single master curve is consistent with the expected KPZ scaling in .

On the other hand, we have simulated a directed polymer model in dimensions as depicted in Fig. 3 (left), where on each site, there is a random energy variable, with Gaussian fluctuations. We find the optimal path of length , which is the polymer with minimal energy, with one free end-point. And we compute the distribution of the position of this end-point, averaged over samples. In Fig. 12 we have plotted the distribution of the rescaled position for and (both of them being statistically independent): the collapse of these data, for different , on a single master curve is consistent with the expected KPZ scaling in , while the value of was adjusted such that these data coincide with the ones for the PNG.

For comparison we have plotted on this same graph, on Fig. 12, the data for the rescaled time of the maximum for non-intersecting Brownian bridges, i.e. the same data as in Fig. 11 (except ), without any additional fitting parameter.

One sees that the finite results describe quite accurately the center of the distribution, whereas there is a systematic deviation in the tails of the distribution (as expected since is relatively small). Both data, for watermelons on the one hand and for the PNG on the other hand, suffer respectively from finite and finite effects. Our data for the PNG seem to indicate that when increases, the probability weight is slightly displaced from the tails to the center of the (rescaled) distribution: this suggests that the limiting distribution is not Gaussian (the best Gaussian fit is plotted with a dotted line in Fig. 12). This convergence to the asymptotic distribution is however quite slow.

V Conclusion

In conclusion, we have presented a detailed derivation of the analytic computation of the distribution of the time at which the maximal height of vicious walkers is reached. Our analytic approach is based on a path integral approach for free fermions, which incorporates in a rather physical way the non-colliding condition. We have considered three different types of vicious walkers configurations: non-intersecting free Brownian motions, ”stars” configuration, for , non-intersecting Brownian bridges, ”watermelons” configurations, for any number of vicious walkers and finally non-intersecting Brownian excursions, ”watermelons with a wall” also for any . We have also checked our results using numerical simulations of Dyson’s Brownian, which uses the deep connection between vicious walkers and Random Matrix Theory, which we have reminded in detail.

Thanks to the connection between vicious walkers and the Airy process (7), our results yields, in the large limit, results for the distribution of , the position of the maximal height of a curved growing interface in the KPZ universality class (Fig. 2 left) or the transverse coordinate of the end-point of the optimal directed polymer (Fig. 2 right). We have shown that our analytical results for finite , correctly rescaled, are in good agreement with our numerical data for the PNG model and DPRM on the square lattice. Performing the large asymptotic analysis of our formula (100, 134) remains a formidable challenge, which will hopefully motivate further study of this problem.

Acknowledgements.

We thank the Centro Atomico in Bariloche for hospitality where part of this article was written.Appendix A Integration over ordered variables

In the main text, we have to sum over realizations with the constraint . Here we study how integrals may be simplified by the symmetry of the integrand.

A.1 , two variables

Consider a box in one dimension, and a function of two variables . In the main text, we want to compute ordered integrals like

| (156) |

This is usually easier to compute the integral over the whole domain, that is to say

| (157) |

Here we make a link between those two quantities, when is symmetric in the exchange of and . Let us start from equation (157) with a symmetric function

| (158) |

From the second to the third line we use triangular integration in the second term. From the third line to the forth, we relabelled the variables in the second term. In this operation if was antisymmetric, we would have a minus sign, and hence a cancellation of the two terms. The conclusion for two variables is that if is antisymmetric, the integration over the whole domain is zero, but if is symmetric in the exchange of the two variables, we have the useful formula

| (159) |

A.2 variables

The previous result can be extended for variables, and the result is, for symmetric in the exchange of any of two of its arguments

| (160) |

with and an integration on the domain in the left-hand side (lhs), and an integration over the whole domain for in the right-hand side (rhs).

The proof is done by applying iteratively the formula (159) first to the couples changing the upper limit of integrations from to . This operation results gives a factor for each couple so that:

| (161) |

Then one repeats this procedure for the couples to , which gives a factor , and continues until step with the couples to to have

| (162) |

Doing so until one obtains the result (160).

Appendix B Cauchy-Binet identity

B.1 Continuous version

In the main text, we are confronted with integrals of two determinants that takes the form:

| (163) |

where , , are functions of one variable, and each variable has the same domain of integration (in the main text we usually integrate over the momenta from to ). We have

| (164) |

is the symmetric group, is the signature of the permutation . Now we make the change of variables . That is and the Jacobian is unity. So we have

| (165) |

is a group, so it exists so that , and . Moreover . Getting back to the variables we have

| (166) |

In the last line, the term in bracket is simply the determinant . The permutation does not appear anymore, so we have . Hence

| (167) |

At this stage, the basic result is that we have expressed the first determinant only as a product of the diagonal terms. This is used in the main text.

To go further we use the fact that the determinant of one matrice is the same as the determinant of its transpose:

| (168) |

From the second to the third line, we factorized the integrals, and we wrote for each . We recognize the determinant of the matrix whose elements indexed by are given by an integral of the product , yielding the so-called Cauchy-Binet identity:

| (169) |

Moreover, one can easily deduce from Eq. (169) the following relation, valid for any integrable function :

| (170) |

This relation is used in the main text.

B.2 Discrete version

Here we consider the following multiple sum:

| (171) |

Changing the indices of the sums , or , one gets

| (172) |

where we re-arranged the columns in the remaining determinant in the ‘natural’ order, thus factorizing the signature of the permutation . Hence there is a sum over the permutations of , giving the cardinal . We obtain as in the continuous case that the first determinant is written as the product of its diagonal terms with a factor :

| (173) |

Factorizing the sums, one gets

| (174) |

In the same way as in the continuous case, if one considers

| (175) |

one finally obtains

| (176) |

Appendix C Normalization constant

In this section, we compute the normalization constant of the joint distributions and for non-interesecting bridges and excursions respectively.

C.1 Non-intersecting Brownian bridges

To compute the amplitude in Eq. (102) we use the fact that the integration of in Eq. (100), i.e. must yield back the pdf of which was computed in Ref. Schehr08 . Indeed in Ref. Schehr08 it was shown that

| (177) | |||||

| (178) |

where the amplitude can be computed using a Selberg integral Schehr08

| (179) |

The pdf of the maximum, is thus given by

| (180) | |||

| (181) |

where, in the last two lines, we have expanded both determinants in minors with respect to the last column (we recall that denotes the minor of the matrix , obtained by removing its line and its column). Note that these minors do not depend on . This suggests to consider, in the last two lines of Eq. (180), only the integral over the variable where we perform an integration by part. This yields:

| (182) |

Inserting this result of the integration by part (C.1) in Eq. (180) and using the following identity (which we have explicitly checked for but can only conjecture for any integer ):

| (183) |

one obtains finally

On the other hand, from the definition of given in Eq. (100) one has

| (185) |

with

| (186) |

To compute this integral over (185) we compute instead

| (187) |

and clearly

| (188) |

The structure of in Eq. (C.1) suggests to compute its Laplace transform with respect to

| (189) | |||||

where we have regularized the integrals over and with the help of this exponential term . The next step is to expand the determinants in Eq. (189) with respect to their last column. This yields

| (190) |

where

| (191) |

This integral (191) can be easily evaluated using residues, this yields

| (192) |

Using this result (192) in the expression above (C.1), one obtains

| (193) |

Using the results identity shown above (191, 192) we can write as

| (194) | |||||

Under this form (194) it is easy to invert the Laplace transform to obtain and finally one obtains

| (195) |

Finally, using the identity (185) together with the explicit expressions (C.1, 195) one obtains

| (196) |

as given in the text in Eq. (102).

C.2 Non-intersecting Brownian excursions

In this subsection we compute the constant of the formula (134) with the same method. Let us recall the joint distribution of and for the vicious excursions

| (197) |

and where

| (198) |

with the same notation as in the main text and . The normalization of this joint pdf is

| (199) |

As in the case of bridges we can use the result of Ref. Schehr08 of the cumulative distribution of the maximum of vicious excursions

| (200) |

where is the square of the Vandermonde determinant

| (201) |

and is a normalization constant obtained by imposing :

| (202) |

The derivative of the cumulative gives the pdf of the maximum

| (203) |

The term in the parenthesis of the second line comes from the derivative of the exponential, giving a factor that can be simplified by the symmetry in the exchange of and .

Now we have to compute the marginal by integrating the joint pdf given by Eq (197) over

| (204) |

to identify our constant . As in the Bridges case, we compute instead the function of

| (205) |

and at the end we will recover

| (206) |

The formula for is best treated with a Laplace transform, because the convolution in the second line of Eq. (205) becomes a simple product. Taking the Laplace transform with respect to , one has

| (207) |

the Laplace transform of being

| (208) |

This has been introduced to regularize the integrand so that one can permute the integral from the Laplace transform and the infinite sum over . Writting the Vandermonde determinant as

| (209) |

one can use the identity, shown below in Eq. (218), with with to get

| (210) |

Under this form, we are ready to take the inverse Laplace transform of using the Bromwich integral:

| (211) |

where is such that the vertical line keeps all the poles of the integrand to its left. The poles in the complex plane are located in , for on the negative real axis, so that is well-suited. We close the contour with a semi-circle to the left. By the Jordan lemma, the integral on the semi-circle when is zero. The residue theorem then gives

| (212) |

Taking and re-labelling , one obtains

| (213) |

In order to compare this formula with Eq. (203), we need to simplify the last term in the brackets. To this end, we introduce the function :

| (214) |

which is totally symmetric under the exchange of any couple of its arguments. One has

| (215) |

where we change the role of and in the last line. Equating the last line with the first, one obtains

| (216) |

Inserting this identity in formula (213), the comparison with Eq. (203) is straightforward, and one obtains

| (217) |

as given in the text in Eq. (127)

Appendix D Identity

We want to show the identity

| (218) |

This will be shown by induction on : we thus first analyse the case of this identity

| (219) |

for any real (indeed this has a limit for and one can extend the result for ). The first step is to separate the series in the lhs into two parts

| (220) |

The first series is geometric and one has

| (221) |

In the second, one can permute the limit with the sum because of the normal convergence

| (222) |

To compute the rhs, we consider the function on the complex plane

| (223) |

This function has simple poles in with and in . One can verify that with

| (224) |

Then using the Jordan lemma, one has that the contour integral of along the infinite circle centered in is zero. Using the residue theorem, one finds

| (225) |

or

| (226) |

Inserting Eq. (226) in Eq. (222) and Eq. (221) in Eq. (220), one has

| (227) |

which is the announced result for .

Let us prove the general result by induction. Consider the quantity

| (228) |

With the lemma (which we show below)

| (229) |

and the induction hypothesis at rank (218) that we use in the second term of Eq. (228), we have proved the formula at rank which ends the induction proof of the identity (218).

In order to prove the lemma (229), we put with the real , and we shall take the limit . Denoting for

| (230) |

one sees that

| (231) |

Using the fact that is a simple geometric series, we apply this relation to compute :

| (232) |

The domain of definition of is the positive real axis, and in this domain, coincides with the function defined over all the real line

| (233) |

One sees easily that is an odd function , which implies that , which shows the lemma for . To go further, the Taylor series of must have only odd powers of . Because they coincide on , this is true for :

| (234) |

Indeed this odd power series expansion extends to all (with other coefficients) thanks to the relation (231) because we differentiate twice to obtain from

| (235) |

and this prove that

| (236) |

which, regarding the definition (230), ends the proof of the lemma (229).

Appendix E Some useful formulae for Hermite polynomials

For our purpose, the following integral representation of the Hermite polynomial is useful

| (237) |

The formula used in the text is explicitely

| (238) |

For the stars configurations we use the identity

| (239) |

(in particular with and ).

References

- (1) J.-P. Bouchaud, M. Mézard, J. Phys. A 30, 7997 (1997).

- (2) P. Le Doussal, C. Monthus, Physica A 317, 140 (2003)

- (3) D. S. Dean, S. N. Majumdar, Phys. Rev. E 64, 046121 (2001).

- (4) D. Carpentier, P. Le Doussal, Phys. Rev. E 63, 026110 (2001); Erratum-ibid. 73, 019910 (2006).

- (5) G. Györgyi, P. C. W. Holdsworth, B. Portelli, Z. Racz, Phys. Rev. E 68, 056116 (2003).

- (6) E. Bertin, M. Clusel, J. Phys. A 39, 7607 (2006).

- (7) Y. V. Fyodorov, J.-P. Bouchaud 2008 J. Phys. A: Math. Theor. 41 372001.

- (8) Y. V. Fyodorov, P. Le Doussal, A. Rosso, J. Stat. Mech. P10005 (2009).

- (9) L. O’Malley, G. Korniss, T. Caraco, Bull. Math. Bio. 71, 1160 (2009).

- (10) P. Embrecht, C. Klüppelberg, T. Mikosh, Modelling, Extremal Events for Insurance and Finance (Springer), Berlin (1997).

- (11) S. N. Majumdar, J.-P. Bouchaud, Quantitative Finance 8, 753 (2008).

- (12) R. W. Katz, M. P. Parlange, P. Naveau, Adv. Water Resour. 25, 1287 (2002).

- (13) E. J. Gumbel, Statistics of Extremes (Dover), 1958.

- (14) S. Raychaudhuri, M. Cranston, C. Pryzybla, Y. Shapir, Phys. Rev. Lett. 87, 136101 (2001).

- (15) S. N. Majumdar, A. Comtet, Phys. Rev. Lett. 92, 225501 (2004).

- (16) S. N. Majumdar, A. Comtet, J. Stat. Phys. 119, 777 (2005).

- (17) G. Schehr, S. N. Majumdar, Phys. Rev. E 73, 056103 (2006).

- (18) G. Györgyi, N. R. Moloney, K. Ozogany, Z. Racz , Phys. Rev. E 75, 021123 (2007).

- (19) S. N. Majumdar, J. Randon-Furling, M. J. Kearney, M. Yor, J. Phys. A Math. Theor. 41, 365005 (2008).

- (20) P. L. Krapivsky, S. N. Majumdar, A. Rosso, J. Phys. A: Math. Theor. 43, 315001 (2010).

- (21) J. Rambeau, G. Schehr, J. Stat. Mech., P09004 (2009).

- (22) J. Randon-Furling, S. N. Majumdar, A. Comtet, Phys. Rev. Lett. 103, 140602 (2009).

- (23) S. N. Majumdar, A. Comtet, J. Randon-Furling, J. Stat. Phys. 138, 955 (2010).

- (24) G. Schehr, P. Le Doussal, J. Stat. Mech. P01009 (2010).

- (25) T. W. Burkhardt, G. Györgyi, N. R. Moloney, Z. Racz , Phys. Rev. E 76, 041119 (2007).

- (26) S. N. Majumdar, A. Rosso, A. Zoia, J. Phys. A: Math. Theor. 43, 115001 (2010).

- (27) H. J. . Hilhorst, P. Calka, G. Schehr, J. Stat. Mech. P10010 (2008).

- (28) T. Feierl, Proc. of the AofA2007, DMTCS Proc. (2007).

- (29) M. Katori, M. Izumi, N. Kobayashi, J. Stat. Phys. 131, 1067 (2008).

- (30) G. Schehr, S.N. Majumdar, A. Comtet, J. Randon-Furling, Phys. Rev. Lett. 101, 150601 (2008).

- (31) N. Kobayashi, M. Izumi, M. Katori, Phys. Rev. E 78 051102 (2008).

- (32) T. Feierl, Proc. of IOWA 2009, Lecture Notes in Computer Science, vol. 5874 (2009).

- (33) M. Izumi, M. Katori, preprint arXiv:1006.5779.

- (34) P. J. Forrester, S. N. Majumdar, G. Schehr, preprint arXiv:1009.2362, submitted to Nucl. Phys. B.

- (35) J. Rambeau, G. Schehr, Europhys. Lett. 91, 60006 (2010).

- (36) P.G. de Gennes, J. Chem. Phys. 48, 2257 (1968).

- (37) M. E. Fisher, J. Stat. Phys. 34, 667 (1984).

- (38) D. A. Huse, M. E. Fisher, Phys. Rev. B 29, 239 (1984).

- (39) J. W. Essam, A. J. Guttmann, Phys. Rev. E 52, 5849 (1995).

- (40) A. J. Bray, K. Winkler, J. Phys. A 37, 5493 (2004).

- (41) F. J . Dyson, J. Math. Phys. 3, 1191 (1962); ibid. 1198.

- (42) M. L. Mehta, Random matrices, Academic Press, New York, (1991).

- (43) C. A. Tracy, H. Widom, Comm. Math. Phys. 159, 151 (1994); ibid. 177, 727 (1996).

- (44) C. Nadal, S. N. Majumdar, Phys. Rev. E 79, 061117 (2009).

- (45) M. Kardar, G. Parisi, Y.-C. Zhang, Phys. Rev. Lett. 56, 889 (1986).

- (46) J. Krug, H. Spohn, in Solids far from equilibrium (ed. by C. Godrèche), Cambridge Univ. Press, New York (1991).

- (47) T. Halpin-Healy, Y. C. Zhang, Phys. Rep. 254, 215 (1995).

- (48) T. Sasamoto, H. Spohn, Phys. Rev. Lett. 104, 230603 (2010).

- (49) F. C. Franck, J. Cryst. Growth 22, 233 (1974)

- (50) J. Krug, H. Spohn, Europhys. Lett. 8, 219 (1989).

- (51) M. Prähofer, Ph. D thesis, Ludwig-Maximilians-Universität, München, 2003.

- (52) D. Dhar, Phase Transitions 9, 51 (1987)

- (53) L.-H. Gwa, H. Spohn, Phys. Rev. Lett. 68, 725 (1992)

- (54) M. Prähofer, H. Spohn, Phys. Rev. Lett. 84, 4882 (2000)

- (55) M. Prähofer, H. Spohn, J. Stat. Phys., 108, 1071 (2002)

- (56) K. Johansson, Comm. Math. Phys. 209, 437 (2000).

- (57) J. Gravner, C. A. Tracy and H. Widom, J. Stat. Phys. 102, 1085 (2001)

- (58) S. N. Majumdar, S. Nechaev, Phys. Rev. E 69, 011103 (2004)

- (59) S. N. Majumdar, Les Houches Lecture Notes on ”Complex Systems”, 2006 ed. by J.P. Bouchaud, M. Mézard and J. Dalibard

- (60) J. Baik, P. Deift, K. Johansson, J. Amer. Math. Soc. 12, 1189 (1999)

- (61) D. Aldous, P. Diaconis, Bull. Amer. Math. Soc. 36, 413 (1999)

- (62) L. Miettinen, M. Myllys, J. Merikoski, J. Timonen, Eur. Phys. J. B 46, 55 (2005).

- (63) K. A. Takeuchi, M. Sano, Phys. Rev. Lett. 104, 230601 (2010).

- (64) P. Ferrari, Lecture Notes of Beg-Rohu Summer School, available at http://ipht.cea.fr/Meetings/BegRohu2008/.

- (65) K. Johansson, Comm. Math. Phys. 242, 277 (2003).

- (66) E. Brunet, B. Derrida, Phys. Rev. E 61, 6789 (2000); Physica A 279, 395 (2000); P. Calabrese, P. Le Doussal, A. Rosso, Europhys. Lett. 90, 20002 (2010); V. Dotsenko, Europhys. Lett. 90, 20003 (2010).

- (67) G. Amir, I. Corwin, J. Quastel, arXiv:1003.0443, to appear in Comm. on Pure and Appl. Math.

- (68) J. Krug, P. Meakin, T. Halpin-Healy, Phys. Rev. A 45, 638 (1992).

- (69) P. J. Forrester, S. N. Majumdar, G. Schehr, Nucl. Phys. B 844, 500 (2011).

- (70) M. Mézard, J. Phys. 51, 1831 (1990); G. Parisi, J. Phys. 51, 1595 (1990).

- (71) E. Agoritsas, V. Lecomte, T. Giamarchi, Phys. Rev. B 82, 184207 (2010).

- (72) E. Brunet, Phys. Rev. E 68, 041101 (2003).

- (73) S. Karlin, J. McGregor, Pacific J. Math. 9, 1141 (1959).

- (74) B. Lindström, Bull. London Math. Soc., 5, 85 (1973); I. Gessel, G. Viennot, Adv. Math. 58, 300 (1985).

- (75) W. Feller, An introduction to Probability Theory and its applications, (Wiley, New York, 1971), Vol. 1 & 2.

- (76) H. Risken, The Fokker-Plank Equation, Springer (1984).

- (77) F. Calogero, J. Math. Phys. 10, 2197 (1969).

- (78) B. Sutherland, J. Math. Phys. 12, 246 (1971).