Stochastic Optimal Multi-Modes Switching with a

Viscosity Solution Approach ††thanks: The research

leading to these results has received funding from the European

Community’s FP 7 Programme under contract agreement

PITN-GA-2008-213841, Marie Curie ITN ”Controlled Systems”.

Abstract

We consider the problem of optimal multi-modes switching in finite horizon, when the state of the system, including the switching cost functions are arbitrary (). We show existence of the optimal strategy, and give when the optimal strategy is finite via a verification theorem. Finally, when the state of the system is a markov process, we show that the vector of value functions of the optimal problem is the unique viscosity solution to the system of variational partial differential inequalities with inter-connected obstacles.

. Real options, Backward stochastic differential equations, Snell envelope, Stopping times, Switching, Viscosity solution of PDEs, Variational inequalities

AMS Classification subjects. 60G40, 62P20, 91B99, 91B28, 35B37, 49L25

1 Introduction

We consider a power plant which produces electricity and which has several modes of production, e.g., the lower, the middle and the intensive modes. The price of electricity in the market fluctuates in reaction to many factors such as demand level, weather conditions, unexpected outages etc. Moreover, electricity is non-storable once produced, it should be almost immediately consumed. Therefore, as a consequence, the station produces electricity in its instantaneous most profitable mode known that when the plant is in mode , the yield per unit time is given by means of and, on the other hand, switching the plant from the mode to the mode is not free and generates expenditures given by and possibly by other factors in the energy market.

The switching from one regime to another one is realized sequentially at random times which are part of the decisions. So the manager of the power plant faces two main issues:

when should she decide to switch the production from its current mode to another one?

to which mode the production has to be switched when the decision of switching is made?

The manager faces the issue of finding the optimal strategy of management of the plant. This is related with the price of the power plant in the energy market.

Optimal switching problems for stochastic systems were studied by several authors (see e.g. [2, 3, 5, 10, 11, 12, 14, 15, 16, 20, 28, 31] and the references therein). The motivations are mainly related to decision making in the economic sphere. In order to tackle those problems, authors use mainly two approaches. Either a probabilistic one [11, 12, 20] or an approach which uses partial differential inequalities (PDIs for short) [2, 5, 14, 16, 31, 28].

In the finite horizon framework Djehiche et al. [12] have studied the multi-modes switching problem in using probabilistic tools. They have proved existence of a solution and found an optimal strategy when the switching costs from state to state is strictly non–negative (). The partial differential equation approach of this work has been carried out by El Asri and Hamadène [16]. We showed that when the price process is solution of a Markovian stochastic differential equation, then this problem is associated to a system of variational inequalities with interconnected obstacles for which we provided a solution in viscosity sense. This solution is bind to the value function of the problem. Moreover the solution of the system is unique.

Using purely probabilistic tools such as the system of backward stochastic differential equations with oblique reflections (RBSDEs for short), Hamadène and Zhang [21] have considered this optimal switching problem when the switching costs from state to state is non–negative . But in general case the optimal strategy may not exist.

The purpose of this work is to fill in this gap by providing a solution to the optimal multiple switching problem using probabilistic tools and partial differential equation approach.

We prove existence and provide a characterization of an optimal strategy of this problem when the payoff rates and the switching costs are adapted only to the filtration generated by a Brownian motion. Later on, in the case when is a solution of a SDE, we show that the value function of the problem is associated an uplet of deterministic functions which is the unique solution of the following system of PDIs:

| (1.1) |

where an operator associated with a diffusion process and . It turns out that this system is the deterministic version of the Verification Theorem of the optimal multi-modes switching problem in infinite horizon.

This paper is organized as follows: In Section 2, we formulate the problem and give the related definitions. In Section 3, we shall introduce the optimal switching problem under consideration and give its probabilistic Verification Theorem. It is expressed by means of a Snell envelope. Then we introduce the approximating scheme which enables us to construct a solution for the Verification Theorem. Moreover we give some properties of that solution, especially the dynamic programming principle. Section 4 is devoted to the connection between the optimal switching problem, the Verification Theorem and the associated system of PDIs. This connection is made through BSDEs with one reflecting obstacle in the Markovian case. Further we provide some estimate for the optimal strategy of the switching problem which, in combination with the dynamic programming principle, plays a crucial role in the proof of existence of a solution for (1.1). In Section 5, we show that the solution of PDIs is unique in the class of continuous functions which satisfy a polynomial growth condition. In section 6 some numerical examples are given. We close this paper an appendix in which some technical results are proved.

2 Assumptions and formulation of the problem

Throughout this paper (resp. ) is a fixed real (resp.

integers) positive numbers.

Let

and be two continuous functions for which there exists a constant such that for any and

| (2.1) |

for , and are continuous functions and of polynomial growth, there exist some positive constants and such that for each :

| (2.2) |

for any , are satisfying

| (2.3) |

which means that it is less expensive to switch directly in one step from regime to than in two steps via an intermediate regime .

Moreover we assume that there exists a constant such that for any ,

| (2.4) |

This condition means that switching back and forth is not free.

We now consider the following system of variational inequalities with inter-connected obstacles:

| (2.5) |

where is given by:

| (2.6) |

hereafter the superscript stands for the transpose, is the trace operator and finally is the inner product of .

The main objective of this paper is to focus on the uniqueness of the solution in viscosity sense of (2.5) whose definition is:

Definition 2.1

Let be a -uplet of continuous functions defined on , -valued and such that for any and . The -uplet is called:

-

a viscosity supersolution (resp. subsolution) of the system (2.5) if for each fixed , for any and any function such that and is a local maximum of (resp. minimum), we have:

(2.7) -

a viscosity solution if it is both a viscosity supersolution and subsolution.

There is an equivalent formulation of this definition (see e.g. [6]) which we give because it will be useful later. So firstly we define the notions of superjet and subjet of a continuous function .

Definition 2.2

Let , an element of and finally the set of symmetric matrices. We denote by (resp. ), the superjets (resp. the subjets) of at , the set of triples such that:

Note that if has a local maximum (resp. minimum) at , then we obviously have:

We now give an equivalent definition of a viscosity solution of the parabolic system with inter-connected obstacles (2.5).

Definition 2.3

Let be a -uplet of continuous functions defined on , -valued and such that for any . The -uplet is called a viscosity supersolution (resp. subsolution) of (2.5) if for any , and (resp. ),

It is called a viscosity solution it is both a viscosity subsolution and supersolution.

As pointed out previously we will show that system (2.5) has a unique solution in viscosity sense. This system is the deterministic version of the optimal -states switching problem will describe briefly in the next section.

3 The optimal -states switching problem

3.1 Setting of the problem

Let be a fixed probability space on which

is defined a standard -dimensional Brownian motion

whose natural filtration is

. Let

be

the completed filtration of with the -null sets of .

Let:

- be the -algebra on of -progressively measurable sets;

- be the set of -measurable and -valued processes such that and be the set of -measurable, continuous processes such that ;

- for any stopping time , denotes the set of all stopping times such that .

Let be the set of all possible activity modes of the production of a power plant. A management strategy of the plant consists, on the one hand, of the choice of a sequence of nondecreasing stopping times (i.e. and ) where the manager decides to switch the activity from its current mode to another one. On the other hand, it consists of the choice of the mode , which is an -measurable random variable taking values in , to which the production is switched at from its current mode. Therefore the admissible management strategies of the plant are the pairs and the set of these strategies is denoted by .

Let be an -measurable, -valued continuous stochastic process which stands for the market price of factors which determine the market price of the commodity. Assuming that the production activity is in mode 1 at the initial time , let denote the indicator of the production activity’s mode at time :

| (3.1) |

Then for any , the state of the whole economic system related to the project at time is represented by the vector:

| (3.2) |

Finally, let be the instantaneous profit when the system is in state , and for , let denote the switching cost of the production at time from current mode to another mode . Then if the plant is run under the strategy the expected total profit is given by:

Therefore the problem we are interested in is to find an optimal strategy a strategy such that for any .

Note that in order that the quantity makes sense, we assume throughout this paper that, for any the processes and belong to and respectively. There is one to one correspondence between the pairs and the pairs . Therefore throughout this paper one refers indifferently to or .

3.2 The Verification Theorem

To tackle the problem described above Djehiche et al. [12] have introduced a Verification Theorem which is expressed by means of Snell envelope of processes. The Snell envelope of a stochastic process of (with a possible positive jump at ) is the lowest supermartingale of such that for any , . It has the following expression:

The Verification Theorem for the -states optimal switching problem is the following:

Theorem 3.1

Assume that there exist processes of such that:

| (3.3) |

Then:

-

(i)

-

(ii)

Define the sequence of -stopping times as follows :

where:

-

-

for any and

-

for any on the set

with and .

Then the strategy satisfiesand it is optimal.

-

(iii)

If

or is constant, then the optimal strategy is finite.

-

The proof is divided in four steps

Step 1.

(i) It consists in showing that for any

, as defined by (3.3), is the expected total

profit or the value function of the optimal problem, given that the

system is in mode at time . More precisely,

where is the set of strategies such that , -a.s. if at time the system is in the mode .

Let us admit for a moment the following Lemma whose proof is given in the appendix.

Lemma 3.1

For every .

| (3.4) |

From properties of the Snell envelope and at time the system is in mode , we have:

Now, from Lemma 3.1 and the definition of we have:

It implies that

since . Therefore

| (3.5) |

since between and (resp. and ) the production is in regime (resp. regime ) and then (resp. ) which implies that

Repeating this reasoning as many times as necessary we obtain that for any

Then, the strategy satisfies

If not which contradicts the assumption

. Therefore, taking the limit as

we obtain .

Step 2. (ii) We show that the strategy

it is optimal i.e. for any .

The definition of the Snell

envelope yields

But, once more using a similar characterization as (3.4), we get

Therefore,

Repeat this argument times to obtain

Finally, taking the limit as yields

Hence, the strategy is optimal.

Step. 3 (iii) Next, we show that the strategy is finite if

Indeed, let . If , then from (3.5) we have for any ,

since . Then the right-hand side

converge

to as . But this is contradictory because belong to , and . Henceforth the

strategy is finite.

Step 4. (iii) To complete the proof it remains to show that

the strategy is finite when

is constant. Indeed let . If , then from (3.5)

we have for any ,

We show by induction on that for all ,

| (3.6) |

Indeed, the above assertion is obviously true for . Suppose now it holds true at step . Then, at step , we have

It follow that

Then the right-hand side converge to as . This contradicts the fact that belong to and . Henceforth the strategy is finite:

3.3 Existence of processes ,

The issue of existence of the processes which satisfy (3.3) is also addressed in [12]. Also for let us define the processes recursively as follows: for we set,

| (3.7) |

and for ,

| (3.8) |

Then the sequence of processes have the following properties:

Proposition 3.1

([12], Pro. 3 and Th. 2)

-

for any and , the processes are well defined, continuous and belong to , and verify

(3.9) -

there exist processes of such that for any :

-

, and

-

,

(3.11) where . This characterization means that if at time the production activity is in its regime then the optimal expected profit is .

-

the processes verify the dynamical programming principle of the -states optimal switching problem, , ,

(3.12)

-

Note that except , the proofs of the other points are given in [12]. The proof of can be easily deduced using relation (3.10). From (3.10) for any , and we have:

| (3.13) |

Next using the optimal strategy we obtain the equality instead of inequality in (3.13). Therefore the relation (3.12) holds true.

Remark 3.1

Note that the characterization (3.11) implies that the processes of which satisfy the Verification Theorem are unique.

4 Existence of a solution for the system of variational inequalities

4.1 Connection with BSDEs with one reflecting barrier

Let and let be the solution of the following standard SDE:

| (4.1) |

where the functions and are the ones of (2.1). These properties of and imply in particular that the process solution of the standard SDE (4.1) exists and is unique, for any and .

The operator that is appearing in (2.6) is the infinitesimal generator associated with . In the following result we collect some properties of .

Proposition 4.1

([26]) The process satisfies the following estimates:

-

For any , there exists a constant such that

(4.2) -

There exists a constant such that for any and ,

(4.3)

We consider a BSDE with one reflecting barrier introduced in [18]. This notion will allow us to make the connection between the variational inequalities (2.5) and the -states optimal switching problem described in the previous section.

Let , and be continuous, of polynomial growth and such that . Moreover we assume that for any , the mapping is uniformly Lipschitz. Then we have the following result related to BSDEs with one reflecting barrier:

Theorem 4.1

([18], Th. 5.2 and 8.5) For any , there exits a unique triple of processes such that:

| (4.4) |

Moreover, the following characterization of as a Snell envelope holds true:

| (4.5) |

There exists a deterministic continuous function with polynomial growth such that:

and the function is the unique viscosity solution in the class of continuous function with polynomial growth of the following PDE with obstacle:

4.2 Existence of a solution for the system of variational inequalities

Let be the processes which satisfy the Verification Theorem 3.1 in the case when the process . Therefore using the characterization (4.5), there exist processes

and , , such that the triples ( are unique solutions of the following reflected BSDEs: for any we have

| (4.6) |

Moreover we have the following representation of .

Proposition 4.2

There are deterministic functions such that:

and the functions , are lower semi-continuous and of polynomial growth.

:

For let be the processes constructed in (3.7)-(3.8). Therefore using an induction argument and Theorem 4.1 there exist deterministic continuous with polynomial growth functions () such that for any , , . Inequality (3.9) yields

since is deterministic. Therefore combining the polynomial growth of and estimate (4.2) for we obtain:

for some constants and independent of . In order to complete the proof it is enough to set since as .

We are now going to focus on the continuity of the functions . But first let us deal with some properties of the optimal strategy which exist thanks to Theorem 3.1.

Proposition 4.3

Let be an optimal strategy finite, then there exist two positive constant and which do not depend on and such that:

-

if , then

(4.7) -

If is constant, then

(4.8)

(i) We will show by contradiction, suppose

Recall the characterization of (3.11) that reads as:

If is the optimal strategy then

Taking into account that for any and for any , we obtain:

As is arbitrary then putting to obtain:

which is a contradiction.

(ii) If is the optimal strategy and

is constant then we have:

From (3.6) we have:

Then,

Remark 4.1

Next,for , let be the processes defined as follows:

| (4.9) |

The existence of , is obtained in the same way as the one of . By uniqueness we obtain for any , for any we have , and .

We are now ready to give the continuity of the value functions, when the strategy optimal is finite.

Theorem 4.2

The functions are continuous and solution in viscosity sense of the system of variational inequalities with inter-connected obstacles (2.5).

The continuity of the value functions follows from the dynamic programming principle and is proved in [16].

5 Uniqueness of the solution of the system

In this section we address the main question of this paper, that is uniqueness of the viscosity solution of the system (2.5).

Theorem 5.1

The solution in viscosity sense of the system of variational inequalities with inter-connected obstacles (2.5) is unique in the space of continuous functions on which satisfy a polynomial growth condition, i.e. in the space

The proof is divided in four steps. We will show by contradiction that if and are a subsolution and a supersolution respectively for (2.5) then for any , . Therefore if we have two solutions of (2.5) then they are obviously equal. Actually for some suppose there exists such that:

| (5.1) |

Step 1. Let us take and small enough, so that the following holds:

| (5.2) |

Here is the growth exponent of the functions which w.l.o.g we assume integer and . Then, for a small , let us define:

| (5.3) |

where, and . By the growth assumption on and , there exists a , such that:

On the other hand, from , we have

and consequently is

bounded, and

as , , and . Since and are uniformly continuous on , then as

Step 2. We now show that If then,

and,

since and . Then thanks to (5.1) we have,

which yields a contradiction and we have .

Step 3. We now claim that:

| (5.5) |

Indeed if

then there exists such that:

Now, we then see that

| (5.6) |

let such that and set such that

Then we have

where

From (5.6) we have

It follows that:

Now taking into account of (5.3) to obtain:

But this contradicts the definition of , since and

are uniformly continuous on and the claim (5.5) holds.

Step 4. To complete the proof

it remains to show contradiction. Let us denote

| (5.7) |

Then we have:

| (5.8) |

Taking into account (5.5) then applying the result by Crandall et al. (Theorem 8.3, [6]) to the function

at the point , for any , we can find and , such that:

| (5.9) |

By (5.5), and the definition of viscosity solution, we get:

which implies that:

But from (5.8) there exist two constants , and such that:

As

then

It follows that:

where , and which hereafter may change from line to line. Choosing now , yields the relation

Now, from (2.1), (5.9) and (5) we get:

Next,

and finally,

So that by plugging into (5) and note that we obtain:

By sending , , and taking into account of the continuity of and , we obtain which is a contradiction. The proof of Theorem 5.1 is now complete.

As a by-product we have the following corollary:

Corollary 5.1

Let be a viscosity solution of (2.5) which satisfies a polynomial growth condition then for and ,

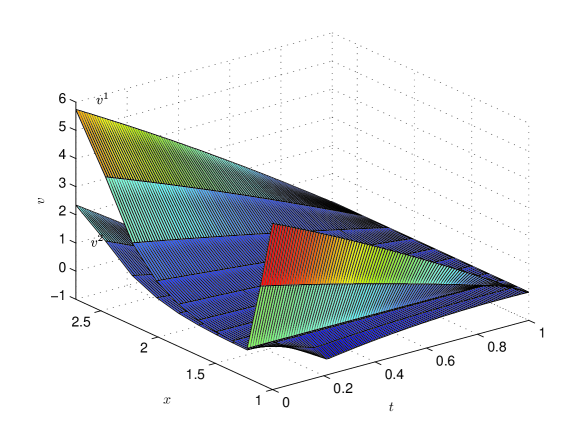

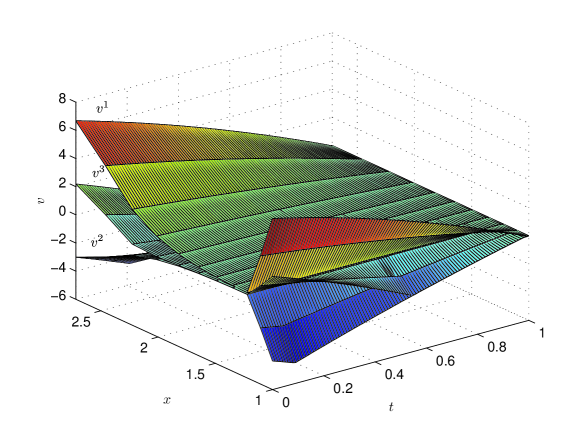

6 Numerical results

We consider now some numerical examples of the optimal switching problem (2.5).

Example 6.1

In this example we consider an optimal switching problem with two

modes, where

, , , , , ,

Example 6.2

We now consider the case of 3 modes where , , , , , , , , , , and finally .

7 Appendix

of Lemma 3.1. From (3.3) we have for any and

| (7.1) |

This also means that the process is a supermartingale which dominates

This implies that the process is a supermartingale which dominates

Since is finite, the process is also a supermartingale which dominates

Thus, the process is a supermartingale which is greater than

To complete the proof it remains to show that it is the smallest one

which has this property and use the characterization of the Snell

envelope see e.g. [4, 17, 19].

Indeed, let

be a supermartingale of class such

that, for any ,

It follows that for every ,

But, the process is a supermartingale and for every ,

It follows that, for every ,

Summing over , we get, for every ,

Hence, the process is the Snell envelope of

which completes the proof of the Lemma.

References

- [1] B. Bouchard, A stochastic target formulation for optimal switching problems in finite horizon, Stochastics, 81 (2009), pp. 171–197.

- [2] K. A. Brekke and B. Øksendal, Optimal switching in an economic activity under uncertainty. SIAM J. Control Optim, (32) (1994), pp. 1021–1036.

- [3] M. J. Brennan and E. S. Schwartz, Evaluating natural resource investments, J. Business 58 (1985), pp. 135–137.

- [4] J. Cvitanic and I. Karatzas, Backward SDEs with reflection and Dynkin games, Annals of Probability 24 (4) (1996), pp. 2024–2056.

- [5] R. Carmona and M. Ludkovski, Pricing asset scheduling flexibility using optimal switching, Appl. Math. Finance, 15 (2008), pp. 405–447.

- [6] M. Crandall, H. Ishii, H and P.L. Lions, User’s guide to viscosity solutions of second order partial differential equations, Bull. Amer. Math. Soc, 27 (1992), 1–67.

- [7] C. Dellacherie and P. A. Meyer, Probabilités et Potentiel, V-VIII, Hermann, Paris, 1980.

- [8] S. J. Deng and Z. Xia, Pricing and Hedging Electric Supply Contracts: A Case with Tolling Agreements, preprint, Georgia Institute of Technology, Atlanta, 2005.

- [9] A. Dixit, Entry and exit decisions under uncertainty, J. Political Economy, 97 (1989), pp. 620–638.

- [10] A. Dixit and R. S. Pindyck, Investment Under Uncertainty, Princeton University Press, Princeton, NJ, 1994.

- [11] B. Djehiche and S. Hamadène, On a finite horizon starting and stopping problem with risk of abandonment, Int. J. Theor. Appl. Finance, 12 (2009), pp. 523–543.

- [12] B. Djehiche, S. Hamadène, A. Popier, A finite horizon optimal multiple switching problem, SIAM J. Control Optim. 48 (4) (2009) 2751–2770.

- [13] K. Duckworth and M. Zervos, A problem of stochastic impulse control with discretionary stopping, in Proceedings of the 39th IEEE Conference on Decision and Control, IEEE Control Systems Society, Piscataway, NJ, 2000, pp. 222–227.

- [14] K. Duckworth and M. Zervos, A model for investment decisions with switching costs, Ann. Appl. Probab, 11 (2001), pp. 239–260.

- [15] B. El Asri, Optimal Multi-Modes Switching Problem in Infinite Horizon, Stochastics and Dynamics, 10 (2) (2010), pp. 231–261.

- [16] B. El Asri and S. Hamadène, The finite horizon optimal multi-modes switching problem: The viscosity solution approach, Appl. Math. Optim, 60 (2009), pp. 213–235.

- [17] N. El Karoui, Les aspects probabilistes du contrôle stochastique, in Ecole d’été de Probabilités de Saint-Flour, Lecture Notes in Math. 876, Springer-Verlag, New York, 1980.

- [18] N. El Karoui, C. Kapoudjian, E. Pardoux, S. Peng, and M. C. Quenez, Reflected solutions of backward SDEs and related obstacle problems for PDEs, Ann. Probab., 25 (1997), pp. 702–737.

- [19] S. Hamadène, Reflected BSDEs with discontinuous barriers, Stoch. Stoch. Rep., 74 (2002), pp. 571–596.

- [20] S. Hamadène and M. Jeanblanc, On the starting and stopping problem: Application in reversible investments, Math. Oper. Res., 32 (2007), pp. 182–192.

- [21] S. Hamadène and J. Zhang, Switching problem and related system of reflected backward SDEs, Stochastic Processes and their Applications, 120 (2010) 403–426

- [22] Y. Hu and S. Tang, Multi-dimensional BSDE with oblique reflection and optimal switching, Probab. Theory Related Fields (2009) doi:10.1007/s00440-009-0202-1.

- [23] V. Ly Vath and H. Pham, Explicit solution to an optimal switching problem in the two-regime case, SIAM J. Control Optim., 46 (2007), pp. 395–426.

- [24] T. S. Knudsen, B. Meister, and M. Zervos, Valuation of investments in real assets with implications for the stock prices, SIAM J. Control Optim., 36 (1998), pp. 2082–2102.

- [25] A. Porchet, N. Touzi, and X. Warin, Valuation of power plants by utility indifference and numerical computation, Math. Methods Oper. Res., 70 (2009), pp. 47–75.

- [26] D. Revuz and M. Yor, Continuous Martingales and Brownian Motion, Springer-Verlag, Berlin, 1991.

- [27] H. Shirakawa, Evaluation of investment opportunity under entry and exit decisions. Srikaisekikenkysho Kkyroku (987) (1997), pp. 107–124.

- [28] S. Tang and J. Yong, Finite horizon stochastic optimal switching and impulse controls with a viscosity solution approach, Stoch. Stoch. Rep., 45 (1993), pp. 145–176.

- [29] L. Trigeorgis, Real options and interactions with financial flexibility, Financial Management, 22 (1993), pp. 202–224.

- [30] L. Trigeorgis, Real Options: Managerial Flexibility and Strategy in Resource Allocation, MIT Press, Cambridge, MA, 1996.

- [31] M. Zervos, A problem of sequential entry and exit decisions combined with discretionary stopping, SIAM J. Control Optim., 42 (2003), pp. 397–421.