Leverage efficiency

Abstract

Peters (2011a) defined an optimal leverage which maximizes the time-average growth rate of an investment held at constant leverage. It was hypothesized that this optimal leverage is attracted to 1, such that, e.g., leveraging an investment in the market portfolio cannot yield long-term outperformance. This places a strong constraint on the stochastic properties of prices of traded assets, which we call “leverage efficiency.” Market conditions that deviate from leverage efficiency are unstable and may create leverage-driven bubbles. Here we expand on the hypothesis and its implications. These include a theory of noise that explains how systemic stability rules out smooth price changes at any pricing frequency; a resolution of the so-called equity premium puzzle; a protocol for central bank interest rate setting to avoid leverage-driven price instabilities; and a method for detecting fraudulent investment schemes by exploiting differences between the stochastic properties of their prices and those of legitimately-traded assets. To submit the hypothesis to a rigorous test we choose price data from different assets: the S&P500 index, Bitcoin, Berkshire Hathaway Inc., and Bernard L. Madoff Investment Securities LLC. Analysis of these data supports the hypothesis.

“Neither a borrower nor a lender be”

Hamlet, Act 1, Scene 3, 75

1 Introduction

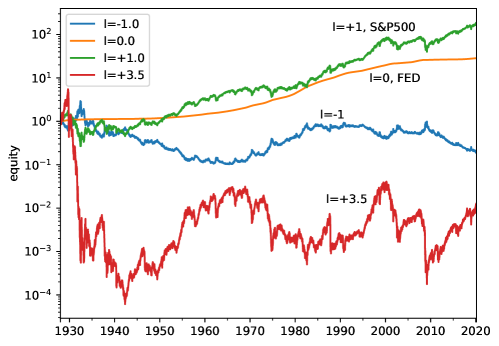

In section 2 we summarize a few key properties of geometric Brownian motion that were pointed out in (Peters, 2011a). We indicate the main elements of the analogy that is often drawn between this model and the dynamics of markets. Section 3 introduces the concept of leverage efficiency, namely the hypothesis that the properties of price fluctuations in real markets are strongly constrained by efficiency arguments so as to make investments of leverage 1 optimal. This hypothesis is motivated by the considerations in section 2 but goes beyond the simple model discussed there. The arguments are robust enough to yield insights into other assets, such as houses, or indeed national economies or the global economy. We summarize example applications of this fundamental constraint on price dynamics in section 4: an explanation of asset price changes in the absence of new information; a resolution of the equity premium puzzle; a protocol for central bank rate setting to avoid leverage bubbles; and the detection of fraudulent investment schemes. Section 5 confronts our theoretical work with data. The arguments leading to the hypothesis are neither specific to the mathematical model nor to any particular asset. Section 6 concludes that optimal leverage is empirically close to 1, as predicted by leverage efficiency, for investments in assets as different as the S&P500 index (SPX, 1927–2020) and Bitcoin (BTC, 2010–2020).

2 Mathematical background

Notation: The present study uses three different levels of realism. To avoid tedious nomenclature and confusion between these, we use three different superscripts:

-

1.

superscript refers to the mathematical model used to motivate and guide our investigations;

-

2.

superscript refers to data analyses performed to test our main hypothesis empirically; and

-

3.

superscript refers to corresponding quantities in the context of real markets and their participants.

Model: The observable is said to undergo geometric Brownian motion if it obeys the Itô stochastic differential equation,

| (1) |

where denotes time, its infinitesimal increment, and the normally distributed Wiener increment, . We call the drift and the volatility.

We pause here to make an important distinction between

averaging over an ensemble and averaging over time. For some special observables,

this distinction is unimportant because they have the following

ergodic property (Peters and Gell-Mann, 2016; Peters, 2019):

Equality of averages

The expectation value of the observable is a constant (independent of time) and the finite-time average of the observable converges to this constant with probability one as the averaging time tends to infinity.

The observable defined by equation (1) does not possess this property. Therefore, we cannot

assume that the expectation value will be informative of what happens to over time. From now on we will refer to the expectation value as the “ensemble average” because it has little to do with the everyday meaning of the word “expect,” whereas it is by definition the average over an ensemble of systems.

Consider the growth rate estimator,

| (2) |

where indexes realizations of the process described by equation (1) and is a time increment. Taking the limit for finite extracts the behavior of the ensemble average, whereas taking the limit for finite extracts the long-time behavior (Peters and Klein, 2013; Peters and Adamou, 2018b). This procedure yields clear interpretations of two well-known characteristics of geometric Brownian motion:

| (3) |

shows that the ensemble-average growth rate is equal to the drift; and

| (4) |

shows that the long-time growth rate, i.e. what an individual will experience eventually, is smaller by a correction term . Equation (4), which shows as equal to the ensemble average of the rate of change , is obtained by applying Itô’s formula to equation (1). Indeed, this rate of change is an ergodic observable for the multiplicative dynamics defined by equation (1), as discussed in (Peters and Gell-Mann, 2016).

Referring to the analogy with stock markets, it was pointed out in (Peters, 2011a) that an individual investor should be more concerned about , the long-time growth rate of a single realization of the process, than about , the growth rate of the average over parallel realizations which are inaccessible to him. For historical reasons, however, is often mistakenly considered in the literature, as noted in (Hughson et al., 2006).

We introduce a leverage parameter to extend the market analogy to leveraged investments. We imagine two assets available to an investor: one riskless, whose price obeys equation (1) with drift and volatility zero; and the other risky, whose price obeys equation (1) with drift

| (5) |

and volatility . The investor has net resources of to allocate between these assets. A leveraged investment in the risky asset is, in effect, a portfolio in which is held in the risky asset and the remainder is held in the riskless asset. Each holding achieves the same fractional change – which we shall call the “return” – as its respective asset, so that the total resources evolve as

| (6) | |||||

| (7) |

The case , in which the investor holds only the riskless asset, results in deterministic exponential growth at a rate equal to the drift . The case , in which the investor places all his resources in the risky asset, is equivalent to equation (1), where .

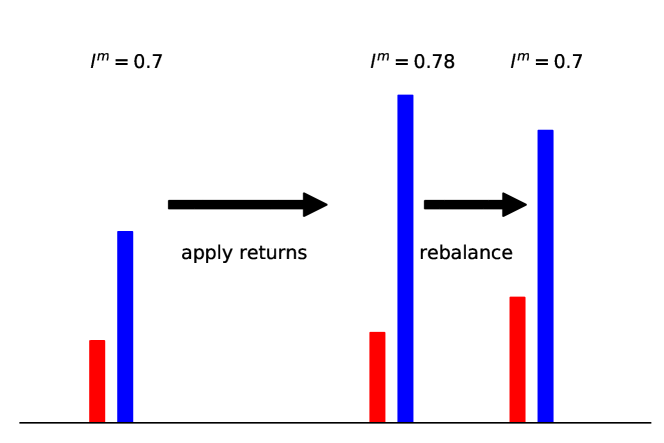

We note that is constant in this setup. The fractional holdings in the two assets do not change over time, even though the values of the holdings do change. Unless or , when only one asset is present, this implies that the portfolio is continuously rebalanced, i.e. resources are moved between the risky and riskless assets to maintain the leverage at . This rebalancing trade is shown schematically in figure 1. In practice, such rebalancing would take place only at finite time intervals and would incur transaction costs. Such effects are included in our empirical work in section 5. Moreover, the leveraged investments imagined in this study should not be confused with “buy-and-hold” portfolios which start with an initial leverage and do not undergo rebalancing. In general, the allocation of such portfolios will change over time.

For the moment, we will think of the risky asset as resembling an investment in the market portfolio and of the riskless asset as resembling a safe government bond or bank deposit. Negative holdings, corresponding to borrowed assets, are possible. Leverage reflects short-selling; reflects part of the investor’s equity being invested in the market and part kept safe accruing interest at rate ; and reflects what is commonly referred to as leveraging, i.e. an investment in the market that exceeds the investor’s equity and includes borrowed funds. The volatility in equation (7) is , proportional to the leverage, and the drift is , reflecting a safe interest rate and the excess drift of the market added in proportion to the leverage. Thus leveraging causes both the excess drift and the fluctuation amplitude to increase linearly.

in equation (7) has the leverage-dependent ensemble-average growth rate,

| (8) |

and the leverage-dependent time-average growth rate,

| (9) |

Crucially equation (9), unlike equation (8), is not monotonic in . Maximizing establishes the existence of an objectively optimal leverage:

| (10) |

Equation (10) implies that, unless , it is possible to choose in equation (7) such that (reflecting a leveraged investment) outgrows in equation (1) (reflecting the market portfolio) in the long run. For example, would imply that, due to the nonlinear effects of multiplicative fluctuations, a rising market could be beaten by keeping a fixed fraction of one’s resources in a savings account.

In reality, the outcome of an investment held for some finite time is given by the growth of the investment averaged over . The growth rate of the ensemble average is a priori irrelevant in practice. Maximizing in equation (8) leads to the recommendation of maximizing (or ). Absent constraints on leverage, this would lead to a negative divergence in , i.e. to ruin, in equation (9). Thus, if (often called the “expected rate of return”) is falsely believed to reflect the quantity an investor should optimize, and if is interpreted as the leverage used in the investment, then the investor would be led to exceed (positively or negatively) the leverage that would truly be most beneficial, with potentially deleterious effects on wealth.

The history of the struggle to make sense of the misleading recommendations derived from equation (8) is the history of decision theory and of probability theory itself, see (Peters, 2011b; Peters and Gell-Mann, 2016; Peters, 2019). Under multiplicative growth, such as in equation (1), the difference between the growth rate of the ensemble average and the long-term growth rate of an individual trajectory is the difference between arithmetic and geometric means. This was identified in the context of a repeated gamble as early as (Whitworth, 1870), while the correction term in its present form, , follows directly from (Itô, 1944). Optimal leverage for equation (7) was computed by (Kelly, 1956) and in the form of equation (10) by (Merton, 1969), although neither pointed to the non-ergodicity of as the origin of their findings. The present study is concerned with the dynamic properties of the optimal leverage observed in time series from real markets.

3 Leverage efficiency

The efficient market hypothesis (Bachelier, 1900; Fama, 1965) claims that the price of an asset traded in an efficient market reflects all the information publicly available about the asset. The corollary is that it is impossible for a market participant, without access to privileged information, consistently to achieve growth at a rate exceeding the long-time growth rate of the market (“to beat the market”) by trading assets. We refer to this concept as price efficiency.

Here we propose a different, fluctuations-based, market efficiency, which we call

Leverage efficiency:

It is impossible for a market participant without privileged information to beat the market

by applying leverage.

Simple strategies such as borrowing money to invest, , or keeping some money in the bank, , should not yield consistent market outperformance, i.e. there should be no leverage arbitrage. This reasoning was used in (Peters, 2011a) to hypothesize that real markets self-organize so that

| (11) |

is an attractive point for their stochastic properties (represented by , , and in the model).

The hypothesis we are about to test is motivated by the model equation (7) and its properties in equation (8), equation (9), and equation (10), in the sense that this model motivates the existence of an optimal leverage. But it is by no means derived from the model, as the hypothesis requires the dynamic adjustment, or self-organization, of the stochastic properties of the system, which, in the model, are represented by fixed parameters. One would have to think of , and as slowly-varying (compared to the fluctuations) functions of time, related to one another as well as to through a dynamic which has , i.e.

| (12) |

as an attractor.

Although inspired by a mathematical model, the hypothesis in equation (11) does not rest on model-specific properties. Crucial for it are the identification of the time-average growth rate and the consequent establishment of an optimal leverage, about which economic arguments may be framed.

Leverage efficiency is a tantalizing concept. It posits that the market has a different quality of knowledge than implied by price efficiency. Price efficiency is essentially a static concept, which states that prices coincide with some notion of objective value. Leverage efficiency, on the other hand, constrains dynamics and predicts properties of fluctuations of the prices of traded assets.

Leverage efficiency arises from a dynamical feedback in which prices and their fluctuations respond to changes in optimal leverage, in a manner reminiscent of the basic feedback between prices and supply-demand imbalances familiar in economics. We augment this with criteria for global stability derived from the no leverage arbitrage argument. This mechanism, detailed below, suggests that both and are particularly attractive and that the interval constitutes a stable regime, whereas values outside it are unstable.

-

1.

Leverage feedbacks:

-

(a)

If , investors will eventually borrow money to invest. High demand for risky assets will lead to price increases and low demand for riskless deposits will lead to increased yields on safe bonds, . Both effects reduce . In addition, highly leveraged investments are liable to margin calls and tend to increase volatility. The fall in and the rise in act to decrease .

-

(b)

If , there is no feedback. If we imagine leverage decreasing from scenario (a), asset prices fall and bond yields drop as investors withdraw from the market and move resources to safe deposits. Both effects increase . Optimally leveraged investments require no borrowing, so volatility-increasing margin calls do not occur. Thus the pressures in (a) bearing down on are relaxed. This regime is marginally stable.

-

(c)

If , investors will eventually borrow stock to short-sell. Low demand for risky assets will lead to price decreases and high demand for riskless deposits to a decrease in yields on safe bonds . Both effects make less negative. Highly negatively leveraged investments are liable to margin calls and tend to increase volatility. The increase in and the rise in imply that becomes less negative.

-

(a)

-

2.

Global stability: It is difficult to envisage globally stable economies existing with optimal leverage outside the interval because:

-

(a)

If , everyone should invest in the market more than he owns. This is not possible because the funds to be invested must be provided by someone.

-

(b)

If , everyone should sell more market shares than he owns. This is not possible because the assets to be sold must be provided by someone.

Thus the range is special in not being globally unstable.

-

(a)

We believe the above to be the main drivers behind leverage efficiency. There are additional effects, however, which reinforce it.

-

1.

Economic paralysis: In an economy with there is no incentive to invest in risky assets, which may limit productive economic activity. Policy makers will tend to steer away from such conditions, perceiving as more desirable.

-

2.

Covered short-selling: An investment with is punished by the costs of borrowing stock to short-sell, i.e. covered as opposed to naked short-selling.

-

3.

Asymmetric interest rates: The interest received by a depositor is typically less than the interest paid by a borrower. Therefore, an investment with is punished by low deposit interest rates and an investment with is punished by high borrowing costs. This reinforces as an attractive point.

-

4.

Transaction costs: The costs of buying and selling assets (fees, spreads, and so on) punish any strategy that requires trading. Holding an investment of constant leverage generally requires trading to rebalance the ratio of assets to equity. The two exceptions are investments with and .

3.1 Predictive accuracy

If we use only observed price changes to compute changes in invested wealth, we will tend to overestimate the magnitude of optimal leverage, i.e. . This is because real leveraged investments incur trading and borrowing costs. Therefore, if the leverage efficiency hypothesis holds, we would expect a naïvely determined value of to be a little larger than its predicted value of . It is difficult to estimate the size of this bias, although we will attempt to do so in Sec. 5.

Ignoring these effects for the moment, we can predict how close we expect observed optimal leverage, , to be to its predicted value of 1, when we estimate it from a finite time series. Even assuming that our theory is correct and is attracted to a particular value, we expect random deviations from it to increase as the time series gets shorter. To take an extreme example, with daily data and assuming daily rebalancing, the observed optimal leverage over a window of one day does not exist. Either if the risky return beats the riskless return on that day; or if riskless beats risky. Indeed, the magnitude of the observed optimal leverage will diverge for any window over which the daily risky returns are either all greater than, or all less than, the daily riskless returns. This is unlikely for windows of months or years but using daily data it happens commonly over windows of days or weeks. Even without this divergence, shorter windows are more likely to result in larger positive and negative optimal leverages because relative fluctuations are larger over shorter time scales.

To quantify this idea we solve equation (7) for the time-average growth rate after a finite time . The noise term, which vanishes in the limit , is retained to give

| (13) |

Maximizing this generates a noisy estimate for the optimal leverage over a window of length ,

| (14) |

Thus, in the model, the optimal leverage for a finite time series is normally distributed with mean and standard deviation

| (15) |

We will use this quantity as the standard error for the prediction .

4 Applications of leverage efficiency

4.1 A theory of noise

Leverage efficiency sheds light on the origin and nature of “noise” in financial markets. According to leverage efficiency, prices of risky assets must fluctuate if an excess drift exists, , simply because the market would otherwise become unstable. Furthermore, leverage efficiency tells us, in equation (16) below, the fluctuation amplitude required to avoid instability. But, if price fluctuations are necessary for stability, then the intellectual basis for price efficiency – that changes in price are driven by the arrival of new economic information – cannot be the whole truth. At least some component of observed fluctuations must be driven by the leverage feedbacks described in section 3, which enforce leverage efficiency and which have little to do with information arrival.

Black (1986) differentiated between information-based and other types of price fluctuation, referring to the latter as “noise” and regarding it as a symptom of inaccurate information and market inefficiency. In our model, rearranging equation (12) yields a fluctuation amplitude of

| (16) |

Thus, based purely on leverage efficiency, prices must fluctuate and we can even quantify by how much. An asset whose expectation value grows faster than that of the riskless asset must fluctuate, otherwise systemic stability will be undermined. This is a radical departure from conventional thinking, which has practical consequences. For instance, prices “discovered” at ever higher trading frequencies must necessarily reveal more ups and downs, but this noise is self-generated, imposed by the requirement of leverage stability. Stability as the genesis of volatility constitutes a theory of noise requiring no appeal to the arrival of unspecified information, whether accurate or not.

4.2 Equity premium puzzle

The term “equity premium” describes a form of compensation investors demand for holding a risky asset. One way of quantifying this idea is as follows. Imagine you hold a riskless asset with a given time-average growth rate, equal to its drift, which you may swap for a risky asset with a given volatility and a larger drift. How much greater must the risky asset’s time-average growth rate be to entice you to swap?

The literature on this question is large and often takes a psychological and individual-specific perspective. For instance, a more “risk averse” individual will demand a higher equity premium to hold the risky asset. Models of human behaviour enter both into the definition of the equity premium – which, as noted by Fernández (2009), lacks consensus – and into its analysis. Much of the literature draws the conclusion that observed equity premia are inconsistent with dominant behavioural models, typically being larger than those models predict. This is known as the “equity premium puzzle” (Mehra and Prescott, 1985). LeRoy (2016) summarizes the current state of the debate as follows: “Most analysts believe that no single convincing explanation has been provided for the volatility of equity prices. The conclusion that appears to follow from the equity premium and price volatility puzzles is that, for whatever reason, prices of financial assets do not behave as the theory of consumption-based asset pricing predicts.”111The “price volatility puzzle” is that prices are apparently more volatile than dominant models predict.

The framework we have developed here takes a psychologically naïve perspective. We define the equity premium, , without reference to human behaviour or consumption models. It is the difference between the time-average growth rates of the risky asset () and the riskless asset (), which in our model is

| (17) | |||||

| (18) |

We ask what value we expect the equity premium to take in a real market. Leverage efficiency dictates how large volatility must be for the market to avoid a leverage instability (and, therefore, to survive so that we can ask the question). Substituting equation (12) in equation (18) reveals that, under leverage efficiency, the real equity premium is attracted to

| (19) |

or, equivalently, to

| (20) |

Our data analysis in section 5 confirms this prediction.

Under realistic assumptions about actual trading costs, observed optimal leverage is very close to one, meaning that volatility has just the right magnitude to prevent leverage-driven bubbles without making investments in the risky assets unattractive. If trading costs are ignored, is greater than one, meaning volatility is a little lower than naïvely predicted. We regard the consistency of the observed equity premium with the leverage efficiency hypothesis as the long-sought resolution of the equity premium and price volatility puzzles.

4.3 Central bank rate setting

Our observations are also relevant to a central bank setting its lending rate. The rate setter would view the total drift of an appropriate asset or index as given, and the risk-free drift as the central bank’s rate. If the aim is to achieve full investment in productive activity without fuelling an asset bubble, then this rate should be set so that . Since and , this is achieved by setting

| (21) |

Using and for the S&P500 index in section 5.3, the optimal interest rate comes out as 3.8% p.a. for the period analyzed (1927–2020). This is similar to typical real interest rates over this period, suggesting that rate-setting may have been informed, at least in part, by the considerations we outlined above. The task of the central banker can be seen as the task of estimating and in the relevant way. This will involve choices about data and timescales which are far from trivial. For instance, in our data analyses at any given time there is an estimate for and one for for each possible length of lookback window. Operational matters aside, stability with respect to leverage is an important consideration for any central bank. Leverage efficiency provides a simple quantitative basis for a rate setting protocol and may frame qualitative discussions about interest rates in a useful way.

4.4 Fraud detection

The arguments advanced in support of the leverage efficiency hypothesis in section 3 do not relate to specific pairs of riskless and risky assets. Rather, they are general arguments about assets traded in markets, and we expect the predictions of leverage efficiency to hold generally for such assets, absent special conditions. Specifically, we expect observed optimal leverage, , over finite time, , to be consistent with the predictions of its value and uncertainty in equation (11) and equation (15), i.e.

| (22) |

where this range corresponds to one standard deviation in each direction in the model.

Observed optimal leverages inconsistent with this prediction suggest two possibilities: either the prediction is wrong generally; or there are special circumstances associated with the assets under study which make it wrong specifically. We offer evidence in section 5 to refute the first possibility, so we turn our attention to the second. In what circumstances would we expect to observe anomalously high or low optimal leverages? Perhaps when we pick an asset with atypically good or bad performance over the time period studied (which, indeed, we do deliberately using Berkshire Hathaway in section 5). Or perhaps when we study an asset class for which economic policies, such as lower or higher taxes, exist to promote or discourage investment.

Another circumstance, our focus here, is a fraudulent asset whose reported prices are not the result of the trading feedbacks described in section 3. We do not expect our predictions to hold for fabricated asset prices (unless the fabricator is aware of this work). This suggests that we might use observed deviations from leverage efficiency, i.e. inconsistencies with equation (22), as a method for detecting fraudulent investments. We test this proposal in section 5 on the infamous Madoff Ponzi scheme.

5 Tests of leverage efficiency in historical data

We test the leverage efficiency hypothesis by computing the growth rates of constant-leverage investments in the S&P500 index, Bitcoin, Berkshire Hathaway (class A shares), and Madoff’s Ponzi scheme. We assume that cash attracts interest at the Federal Reserve overnight rate.

5.1 Data sets and codes

The data used in this study are publicly available.

-

•

S&P500 (SPX): from https://finance.yahoo.com/

-

•

Bitcoin (BTC): from http://www.coindesk.com/price/

-

•

Berkshire Hathaway (BRK): from https://finance.yahoo.com/

-

•

Madoff (MAD): from http://law.du.edu/, digitized at http://lml.org.uk/madoff/

-

•

Short-term federal rates (FED): spliced from and https://fred.stlouisfed.org

-

•

S&P500 Total Return (SP500TR): from https://finance.yahoo.com

-

•

10-year US Treasury bond rates (DGS10): from https://fred.stlouisfed.org

All of these data sets have their problems. Nonetheless they give an impression of how closely leverage efficiency manifests itself in real markets.

The S&P500 is an index of five hundred large companies, listed publicly in the United States. We use it as a proxy for a generic diversified investment in US stocks, but we note some caveats. Firstly, the index does not account for dividends paid to stockholders. This means it will tend to underestimate the performance of a real investment. Secondly, the index suffers from survivorship bias, representing a portfolio of the largest and most successful companies in the US, in which less successful companies are routinely replaced. This acts in the opposite direction to the first caveat. The available time series is sufficiently long (92 years) to leave reasonably small uncertainties in the prediction of optimal leverage, in which the standard error is 0.6.

The large volatility of BTC permits an even more precise prediction of optimal leverage, with a standard error of 0.3, despite the shortness of this time series (10 years). There is no consensus over what asset class BTC is, so it is remarkable that it behaves so similarly to more familiar assets.

Berkshire Hathaway, BRK, is a large conglomerate, well known for its sustained rapid growth over the last half century. We include it as an example of a successful and, we assume, legitimate business. As a cherry-picked investment, we anticipate that its optimal leverage will exceed 1, although by how much is an important question for our theory.

MAD – Bernie Madoff’s Ponzi scheme – is very interesting. Here is a fictitious asset, whose returns were concocted to defraud investors. We find its behavior measurably different from properly traded assets, supporting our proposal in section 4.4 that fraudulent investments may be detected by their deviations from the predictions of leverage efficiency.

The FED data are overnight interest rates paid between banks. It is unclear how well an investment in cash or bonds (or whatever one considers a “riskless” asset) is reflected by these rates. For instance, due to falling interest rates, a longer-term government bond would have appreciated considerably in recent decades. To the extent that short-term inter-bank rates are typically lower than real deposit and borrowing rates, we expect the FED data to underestimate the performance of riskless assets and, therefore, to overestimate the optimal allocation to risky assets.

The S&P500 total return includes dividends. Its time series is shorter, but we include it for completeness and to establish bounds on the effects of dividends.

The 10 year bond yields, DGS10, help us estimate a range of plausible optimal leverage values that might result from using different bond portfolios. Price changes of bonds are not taken into account in any of the analyses we present.

We suspect that, on balance, the competing biases in the data will tend to produce overestimates of real optimal leverage, . We encourage readers to repeat the analyses for different assets and data sets, and to vary parameters and assumptions used in the data analysis. To facilitate this, we provide open-source Python code and data at https://github.com/LMLhub/leverage_efficiency_codes.

5.2 Data analysis

The performance of an investment of constant leverage over a given time window is computed as follows. We start with equity of $1, consisting of $ in the risky asset and cash deposits of $. Each day the values of these holdings are updated according to historical riskless and risky returns. The portfolio is then rebalanced, i.e. the holdings in the risky asset are adjusted so that their ratio to the total equity remains . On non-trading days the return of the market is zero, whereas deposits continue to earn interest payments, which leads to an unrealistic but negligible rebalancing on those days. The investment proceeds in this fashion until the final day of the window, when the final equity is recorded, figure 2.

If at any time the total equity falls to or below zero, we fix it there for all future times: the computation is considered bankrupt for the corresponding leverage, i.e. we do not allow recovery from negative equity. The optimal leverage, , is the leverage for which the final equity is maximized.

Total return from constant-leverage investments in: a) SPX held from 1927-12-31 until 2020-03-01 (92 years); and b) BTC, held from 2010-07-19 and ending 2020-03-01 (10 years). Data analyses 1 (blue), 2 (orange), 3 (green). For descriptions of the computations, see section 5.2. Red vertical dotted lines indicate the prediction and thin vertical pink dotted lines indicate two standard errors away from the prediction, see equation (15). The uncertainties in the prediction are larger for SPX because, while the time series is longer, the volatility is much lower than for BTC. Bitcoin’s volatility and drift are so high that SPX data going back more than 300 years would be required to achieve similar statistical accuracy.

Figure 3 shows the final equity (which has the same magnitude as the fractional change from start to finish) as a function of leverage for a hypothetical investment over the largest available window. The three curves in the figures correspond to the following three sets of assumptions about interest rates and transaction costs, mentioned as additional effects in section 3:

-

•

Data analysis 1 (the “simple” case, blue line in figure 3) is the least realistic analysis, in which the effective federal funds rate is applied to all cash, whether deposited or borrowed. No costs are incurred for short-selling (), akin to naked short-selling, i.e. market returns apply to negative stock holdings exactly as they apply to positive holdings. Transaction costs are neglected. This results in a smooth curve.

-

•

Data analysis 2 (orange line) is like the first case, but it includes friction. Whenever the portfolio is rebalanced a fraction of the value of the assets traded is lost to friction: 0.5% for SPX, BRK, MAD; and 3% for BTC. This resembles transaction costs and introduces kinks (i.e. discontinuities in the first derivative of the curve) at and .

-

•

Data analysis 3 (the “complex” case, green line) is like the second case, but 5% p.a. risk premia are paid for borrowing cash to leverage up as well as for borrowing stock to go short. The kinks become more pronounced.

Time-average growth rates as a function of leverage closely follow a parabola in backtests. a) SPX, b) BTC for the same time intervals as in figure 3. Dashed red curves are parabolic fits on the central 80% of the data. Deviations from the parabolic shape can be seen at the extremes, where the Gaussian model is deficient. Vertical dashed black lines indicate the empirical maximum; vertical dashed pink lines indicate the prediction for its position (optimal leverage 1) and two standard deviations out on either side.

As discussed in section 3, covered short-selling, asymmetric interest rates, and transaction costs tend to penalize investments with leverages other than 0 or 1. This is reflected in the empirical results by the kinks described above and visible in figure 3. For many time windows the discontinuity in the derivative of the return-leverage curve at or is accompanied by a change in sign of the derivative, making the point a global maximum and fixing there. The picture that emerges is this: based on price data only, but pretending that there are no costs to trading and borrowing, optimal leverage is greater than one. For BTC, it is almost two standard errors greater, which we consider significant. However, once our approximations of trading costs are included, real optimal leverage is seen to be very close or even equal to one.

5.3 The entire time series

The return-leverage curves in figure 3 for an investment window spanning the entire time series shows optimal leverages of (SPX) and (BTC) for the simple case (data analysis 1) and (SPX) and (BTC) for the complex case (data analysis 3). For comparison, predicted ranges for were computed from equation (15) using the value of obtained by fitting equation (9) to return-leverage curves. These predictions were (SPX) and (BTC). The significance of these numbers will become clearer in section 5.4.

The time-average growth rate in equation (9), specific to the model in equation (7), is parabolic in . We show in figure 4 the time-average growth rate for the simple case, which is the logarithm of the total return divided by the window length. Given the known deficiencies of the geometric Brownian motion model, the parabolic fit (red dashed line) is remarkably good within the range of the model’s validity. It is simultaneously remarkably bad outside this range: daily rebalanced investments with leverage or (SPX) and or (BTC) would have gone bankrupt (producing a negative divergence in the logarithmic return) due to extreme events. For highly-leveraged investors, the non-Gaussian tails of the return distribution, which determine their ruin probability, are far more important than any other property.

The parameters of the fitted parabola are a fit of the model equation (9). We take them as meaningful definitions of the empirical riskless drift , excess drift , and volatility . We display them in table 1 for all the assets studied, together with the observed riskless growth rate , observed equity premium , and predicted equity premium from equation (20).

| (%p.a.) | (%p.a.) | (%) | (%p.a.) | (%p.a.) | (%p.a.) | ||

| 1927-12-31–2020-03-01 | |||||||

| SPX vs. FED | 1.1 (0.6) | 3.5 | 3.8 | 19 | 3.6 | 2.0 | 1.9 |

| 2010-07-19–2020-03-01 | |||||||

| BTC vs. FED | 1.5 (0.3) | 1.2 | 180 | 110 | 0.66 | 120 | 89 |

| 1980-03-18–2020-03-01 | |||||||

| BRK vs. FED | 3.0 (0.7) | 4.3 | 16 | 23 | 4.5 | 13 | 7.9 |

| 1990-12-01–2005-05-01 | |||||||

| MAD vs. FED | 100 (9) | -12 | 9.2 | 3.0 | 4.0 | 7.5 | 4.6 |

| 1962-01-02–2020-05-07 | |||||||

| SPX vs. DGS10 | 0.6 (1.0) | 6.0 | 1.8 | 17 | 6.0 | 0.4 | 0.9 |

| 1988-01-05–2020-03-01 | |||||||

| SP500TR vs. FED | 2.7 (1.0) | 3.0 | 8.3 | 18 | 3.2 | 6.4 | 4.1 |

Lower part: to gauge the effect of considering dividends and using overnight rates, we tried out SPX leveraged vs. ten-year rates, giving a low optimal leverage of 0.6; and SP500TR vs. overnight rates, giving a high optimal leverage of 2.7.

From a least-squares fit we obtain p.a., p.a., and as the parameter estimates for SPX. For BTC the numbers are more interesting because they are outside the range of most people’s intuition. Here we find p.a. (interest rates were generally lower over the BTC period than the SPX period), p.a., and . In both cases we performed a one-parameter fit on the central 80% of the data in figure 4, after fixing the coordinates of the maximum.

The meanings of these numbers warrant some remarks. For SPX the riskless drift is practically identical to the realised time-average growth rate of a cash deposit. For BTC the estimate is a little off because the parabolic fit is not perfect and the scales of the process are so different that the riskless drift is irrelevant. To be explicit, the excess drift does not correspond to the excess growth rate of stock over cash, which we identify as the equity premium. Instead, due to the wealth-depleting effect of the volatility – manifested in the model as in equation (9) – a real investment in the S&P500 outgrew federal deposits at only p.a., which is less than the excess drift of p.a.. For BTC the effect is vastly more pronounced: a real investment in BTC outgrew federal deposits by p.a..

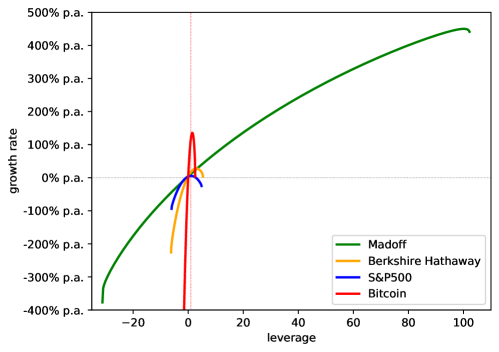

We also include in table 1 statistical properties for two other assets, BRK and MAD, whose reported performance was notably impressive over the periods studied. BRK is an asset whose prices are the result of normal trading activity, while we know, thanks to Markopolos (2005), that MAD prices were fabricated to defraud investors. The observed optimal leverage of BRK is just under three standard errors greater than its predicted value of 1. This deviation from leverage efficiency, while significant, does not falsify our theory. We have deliberately chosen an asset with atypically rapid growth – its performance is the stuff of investment legend – to test the limits of our prediction.

By contrast, the observed optimal leverage of MAD is fully eleven standard errors greater than the prediction. This is a consequence of the extremely low volatility, , reported by the fraudsters. These dramatic deviations from the prediction of leverage efficiency and from the volatility levels of other investment assets would, to a regulator aware of leverage efficiency, have indicated a need for further investigation. The difference between asset prices arising from trade and from fraud is further illustrated in figure 5: the growth rate-leverage curve for MAD is “off the chart” that would have been appropriate for SPX, BTC, and BRK.

5.4 Shorter time scales

So far we have used the predicted variance of observed optimal leverage, equation (15), as a standard error. But we can go further by treating it as a testable prediction in itself.

Likening to the observed optimal leverage over a window of size , we investigate how well equation (15) predicts the fluctuations in . We compile histograms of by moving windows of size across the record and compare the standard deviation of found in these histograms to the standard deviation of .

Figure 6 shows, on double-logarithmic scales, the standard deviation of against the window length for the simple case. Good agreement is found with the model-specific prediction in equation (15). We note that, for shorter time scales, the standard deviation is slightly higher than predicted, which may have to do with data discreteness and the divergence of optimal leverage for short windows with few rebalancing trades. For long windows the statistics are poor, primarily because we consider only non-overlapping windows. There are no free parameters in equation (15). The correct -scaling is observed, and even the prefactor is approximately right ( is the estimate from Sec. 5.3).

The standard deviation of in the simple case (symbols) as a function of window length can be predicted based on the specific model equation (15) (straight lines), using the parameters found in section 5.3. Only non-overlapping windows were used.

In figure 7 the diminishing fluctuations in are illustrated as follows: for every day the optimal leverage is computed for the longest available window (always starting on the earliest available date) for the simple and complex cases. As time passes, the optimal leverage approaches , especially for the complex case, and – as predicted – much faster for BTC.

Also shown are the one- and two-standard deviation envelopes about , based on the estimates in section 5.3 for: a) S&P500 data beginning in 1927; and b) BTC data beginning in 2010.

Figure 7 illustrates the convergence of over time, but provides no information regarding the typicality of the time series. Further insight into the dynamics of can be gained by examining time series for fixed window lengths. Figure 8 shows for the simple case for windows ranging from one to twenty years as a function of the end date of the window. From the strong fluctuations over short time scales emerges attractive behavior consistent with the leverage efficiency hypothesis. For the complex case (not shown) the effects of the stickiness of the points and are visible, and lend additional support to the hypothesis as it applies to real markets.

a) SPX b) BTC. Observed optimal leverage, , fluctuates strongly on short time scales but appears to converge to on long time scales, which constitutes the central result of the study. The convergence for BTC is much faster (note the horizontal date scales).

6 Discussion

Nothing in nature, not even Brown’s pollen (Mazo, 2002), truly follows Brownian motion, whether geometric or not. Nor is anything in nature knowably faithfully described by any mathematical expression (Rényi, 1967). However, just as the movements of Brown’s pollen, in the appropriate regime, have some properties in common with Wiener noise, so the movements of share prices have some properties in common with geometric Brownian motion. Specifically, the daily excess returns for the markets investigated – like the fractional changes in geometric Brownian motion – are sometimes positive and sometimes negative. For any time window that includes both positive and negative daily excess returns, regardless of their distribution, a well-defined optimal constant leverage exists in our computations, section 5.2. We have investigated empirically the properties of such optimal leverages.

Stability arguments, which do not depend on the specific distribution of returns and go beyond the model of geometric Brownian motion, led us to the quantitative prediction that, on sufficiently long time scales, real optimal leverage is attracted to .

We used specific properties of geometric Brownian motion to predict the fluctuations in , providing a scale on which to judge our observations, which is supported by figure 6. While some parameter choices must be made, especially when attempting a degree of realism, we consider our empirical findings a significant corroboration of our hypothesis. The points and are special due to the kinks in figure 3. The economic paralysis argument suggests that is a stronger attractor than , and our observations support this argument. One interpretation is that interest rates have been set at a level that strongly encourages investment in risky assets, so that, even in the presence of trading costs and possibly other constraints, investment is directed into business ventures rather than savings accounts.

Leverage efficiency also suggests a fundamental explanation for the existence of volatility in markets and, specifically, for its observed levels. Price fluctuations are necessary to avoid leverage instability and their observed amplitude is consistent with predictions that assume leverage efficiency. The corollary is that mainstream theories in which price fluctuations are caused by the public disclosure of information or by market dysfunction are, at best, incomplete. Trading at arbitrarily high frequencies will reveal structure, but this structure will be largely self-referential, without economic meaning beyond imposing market stability at ever shorter time scales.

The existence of optimal leverage is important conceptually, and its observed value and associated stability arguments are of practical significance. While these arguments do not preclude special conditions under which it is optimal to invest more than one’s equity or to short-sell an asset, they give a fundamental scale to leverage in general. In other words, if it appears that optimal leverage is outside the band , then a special reason – such as insider knowledge, a tax incentive, or a fraud – for this violation of leverage efficiency must exist. Artificially maintaining such conditions will lead to instabilities. Consider housing: many societies consider it desirable for an individual to be able to purchase a home whose price exceeds his equity without having to take reckless risks. Without carefully designed restrictions on speculative home purchases, policies which aim to achieve the corresponding market conditions, i.e. , will defeat their purpose and create investment bubbles followed by crashes or other unintended consequences.

Leverage efficiency is “accountable” in the sense of Popper (1982, Chap. I.2), who demanded that a “theory will have to account for the imprecision of the prediction”.222Popper does not refer to stochastic theories in this discussion. To apply his arguments to our case, specifically equation (15), we replace “precision in the initial conditions” in his Chap. I.3 by “window length”. Both concepts quantify the information available about the system. Leverage efficiency predicts its own imprecision, equation (15), and the degree of its validity can be meaningfully and objectively tested. This is particularly important given the complexity of the systems involved.

We emphasize that our work is in no way meant to advocate or evaluate constant-leverage or any other investment strategies. Leverage efficiency is a fundamental organizing principle for the stochastic properties of markets. The data analysis in this study is an empirical test of this fundamental principle.

Our results are relevant to the equity premium, or price volatility, puzzle (Mehra and Prescott, 1985). The values of volatility we observe in the most realistic analysis (the complex case) are as predicted by excess return, equation (16). In a simplistic analysis which ignores trading and other costs, we find volatility is less than one would expect, not more as consumption-based asset pricing models tend to suggest. We consider the puzzle essentially solved by our analysis.

Arguing in the context of the model, a strong link between interest rates and leverage is equation (10): reducing the risk-free interest rate (something we liken to the rate at which governments lend) increases optimal leverage because, assuming that overall drift does not change, it implicitly increases and creates an incentive to invest rather than save. This tends to lead to an eventual increase in real leverage. Conversely, increasing the risk-free interest rate reduces optimal leverage. We remark that effecting a change in real leverage, for instance in an attempt to avoid asset bubbles, through a change in is only one option available to policymakers. In some situations, the more direct approach of prohibiting leverages outside a range might be more appropriate.

The prediction of a range for the optimal leverage of a finite-time investment, equation (22), allows the detection of specific investments whose observed optimal leverages lie outside it. If the prediction is believed generally, then special circumstances must apply to such investments. One such circumstance is fraud: prices which do not arise from the trading feedbacks that give rise to leverage efficiency, for example because they are made up, will not have statistical properties consistent with leverage efficiency. We propose that such inconsistencies be used to detect fraudulent investment schemes and show in section 5 that the infamous Ponzi scheme of Bernard Madoff and associates might have been detected sooner, and without great difficulty, using this idea.

We do not consider our arguments specific to traditional financial markets, as demonstrated by their surprising applicability to BTC. They are relevant also to other regularly traded assets and commodities, related even to such basic needs as food and shelter. They are relevant to macroeconomic decisions. Indeed, the same type of dynamics – multiplicative growth with fluctuations – is at work in many other systems. Equation (1) has been used to describe the growth of populations in ecology (Lewontin and Cohen, 1969), the early spread of a disease in epidemiology (Daley and Gani, 1999), and as the basis for the evolution of cooperation (Peters and Adamou, 2018a).

We have argued that is a natural attractor for an economic or market system, with the end points of the interval being sticky. We note that a sticky may correspond to a depression, in which there is no incentive to invest and to take risks. The aim of economic policy may be viewed as creating conditions where for the entire economy is close to one.

Acknowledgements

We thank Zonlab ltd. for support, G. D. Nystrom for bringing the equity premium puzzle to our attention, I. Lehti for pointing us to the S&P500 total return data set, A. Messinger for suggesting we study Berkshire Hathaway returns, and C. Connaughton for invaluable help in preparing the codes for publication.

References

- Bachelier [1900] L. J. B. A. Bachelier. Le jeu, la chance, et le hasard. Paris: Gauthier-Villars, 1900.

- Black [1986] F. Black. Noise. The Journal of Finance, 41(3):528–543, 1986. ISSN 1540-6261. doi:10.1111/j.1540-6261.1986.tb04513.x.

- Daley and Gani [1999] D. J. Daley and J. M. Gani. Epidemic modeling: An introduction. Cambridge University Press, 1999.

- Fama [1965] E. Fama. The behavior of stock-market prices. J. Business, 38(1):34–105, Jan. 1965. doi:10.1086/294743.

- Fernández [2009] P. Fernández. The equity premium in 150 textbooks. Working paper, IESE Business School, University of Navarra, 2009. URL http://www.iese.edu/research/pdfs/DI-0829-E.pdf.

- Hughson et al. [2006] E. Hughson, M. Stutzer, and C. Yung. The misuse of expected returns. Financial Analysts Journal, 62(6):88–96, 2006. doi:10.2469/faj.v62.n6.4356.

- Itô [1944] K. Itô. Stochastic integral. Proc. Imperial Acad. Tokyo, 20:519–524, 1944.

- Kelly [1956] J. L. Kelly, Jr. A new interpretation of information rate. Bell Sys. Tech. J., 35(4):917–926, July 1956. doi:10.1109/TIT.1956.1056803.

- LeRoy [2016] S. F. LeRoy. excess volatility tests. In S. N. Durlauf and L. E. Blume, editors, The New Palgrave Dictionary of Economics, pages 78–80. Springer, 2016.

- Lewontin and Cohen [1969] R. C. Lewontin and D. Cohen. On population growth in a randomly varying environment. Proc. Nat. Ac. Sci., 62(4):1056–1060, 1969. doi:10.1073/pnas.62.4.1056.

- Markopolos [2005] H. M. Markopolos. The world’s largest hedge fund is a fraud. Filed with the Securities and Exchange Commission, Nov. 2005.

- Mazo [2002] R. M. Mazo. Brownian Motion. Oxford University Press, 2002.

- Mehra and Prescott [1985] R. Mehra and E. C. Prescott. The equity premium puzzle. J. Monetary Econ., 15:145–161, 1985.

- Merton [1969] R. C. Merton. Lifetime portfolio selection under uncertainty: the continuous-time case. Rev. Econ. Stat., 51:247–257, 1969.

- Peters [2011a] O. Peters. Optimal leverage from non-ergodicity. Quantitative Finance, 11(11):1593–1602, Nov. 2011a. doi:10.1080/14697688.2010.513338.

- Peters [2011b] O. Peters. The time resolution of the St Petersburg paradox. Philosophical Transactions of the Royal Society A, 369(1956):4913–4931, Dec. 2011b. doi:10.1098/rsta.2011.0065.

- Peters [2019] O. Peters. The ergodicity problem in economics. Nature Physics, 15:1216–1221, 2019. doi:10.1038/s41567-019-0732-0.

- Peters and Adamou [2018a] O. Peters and A. Adamou. An evolutionary advantage of cooperation. arXiv:1506.03414, May 2018a. URL http://arxiv.org/abs/1506.03414.

- Peters and Adamou [2018b] O. Peters and A. Adamou. The sum of log-normal variates in geometric brownian motion. arXiv:1802.02939, 2018b. URL https://arxiv.org/abs/1802.02939.

- Peters and Gell-Mann [2016] O. Peters and M. Gell-Mann. Evaluating gambles using dynamics. Chaos, 26:23103, 2016. doi:10.1063/1.4940236.

- Peters and Klein [2013] O. Peters and W. Klein. Ergodicity breaking in geometric Brownian motion. Physical Review Letters, 110(10):100603, Mar. 2013. doi:10.1103/PhysRevLett.110.100603.

- Popper [1982] K. Popper. The open universe: An argument for Indeterminism. Routledge, 1982.

- Rényi [1967] A. Rényi. A Socratic dialogue on mathematics. In R. Hersh, editor, 18 unconventional dialogues on the nature of mathematics, chapter 1. Springer (2006), 1967.

- Whitworth [1870] W. A. Whitworth. Choice and chance. Deighton Bell, 2 edition, 1870.