Efficient and fast estimation of the geometric median in Hilbert spaces with an averaged stochastic gradient algorithm.

Abstract

With the progress of measurement apparatus and the development of automatic sensors it is not unusual anymore to get large samples of observations taking values in high dimension spaces such as functional spaces. In such large samples of high dimensional data, outlying curves may not be uncommon and even a few individuals may corrupt simple statistical indicators such as the mean trajectory. We focus here on the estimation of the geometric median which is a direct generalization of the real median in metric spaces and has nice robustness properties. The geometric median being defined as the minimizer of a simple convex functional that is differentiable everywhere when the distribution has no atom, it is possible to estimate it with online gradient algorithms. Such algorithms are very fast and can deal with large samples. Furthermore they also can be simply updated when the data arrive sequentially. We state the almost sure consistency and the rates of convergence of the stochastic gradient estimator as well as the asymptotic normality of its averaged version. We get that the asymptotic distribution of the averaged version of the algorithm is the same as the classic estimators which are based on the minimization of the empirical loss function. The performances of our averaged sequential estimator, both in terms of computation speed and accuracy of the estimations, are evaluated with a small simulation study. Our approach is also illustrated on a sample of more than 5000 individual television audiences measured every second over a period of 24 hours.

Keywords. CLT, functional data, geometric quantiles, high dimension, -median, online algorithms, recursive estimation, Robbins-Monro algorithm, spatial median.

1 Introduction

With the progress of measurement apparatus, the development of automatic sensors and the increasing storage performances of computers it is not unusual anymore to get large samples of functional observations. For example Cardot et al., 2010a analyze a sample of more than 18000 electricity consumption curves measured every half hour over a period of two weeks. Our study is motivated by the estimation of the central point of a sample of vectors of with which correspond to individual television audiences measured every second over a period of 24 hours.

In such large samples of high dimensional data, outlying curves may not be uncommon and a even few individuals may corrupt simple statistical indicators such as the mean trajectory or the principal components (Gervini, (2008)). Detecting these atypical curves automatically is not straightforward in such a high dimensional and large sample context and considering directly robust techniques is an interesting alternative. There are many robust location indicators in the multivariate setting (Small, (1990)) but most of them require high computational efforts to be estimated, even for small sample sizes, when the dimension is relatively large. For example, Fraiman and Muniz, (2001) have extended the notion of trimmed means to a functional context in order to get robust estimators of the mean profile. In order to deal with the dimensionality issue and to reduce the computation time, Cuevas et al., (2007) have proposed random projection techniques in the context of maximal depth estimators and studied their properties via simulation studies. Note that sub-sampling approaches based on survey sampling with unequal probability sampling designs have also been proposed in the literature in order to reduce the computational time (Chaouch and Goga, (2010)).

We focus here on the geometric median, also called -median or spatial median, which is a direct generalization of the real median proposed by Haldane, (1948) and whose properties have been studied in details by Kemperman, (1987). It can be defined even if the random variable does not have a finite first order moment and it has nice robustness properties since its breakdown point is equal to 0.5. As noted in Small, (1990), one drawback of the geometric median is that it is not affine equivariant. Nevertheless, it is invariant to translation and scale changes and thus is well adapted to functional data which are observed with the same units at each instant of time. In a functional context, consistent estimators of the -median have been proposed by Kemperman, (1987), Cadre, (2001) and Gervini, (2008). Iterative estimation algorithms have been developed by Gower, (1974), Vardi and Zhang, (2000) in the multivariate setting and by Gervini, (2008) for functional data. This latter algorithm requires to invert at each step matrices whose dimension is equal to the dimension of the data and thus requires important computational efforts. The algorithm proposed by Vardi and Zhang, (2000) is much faster and only requires operations at each iteration, where is the sample size. Nevertheless, these estimation procedures are not adapted when the data arrive sequentially, they need to store all the data and they cannot be simply updated.

In this paper, we explore another direction. The geometric median being defined as the minimizer of a simple functional that is differentiable everywhere when the distribution has no atom, it is possible to estimate it with online gradient algorithms. Such algorithms are very fast and can be simply updated when the data arrive sequentially. There is a vast literature on stochastic gradient algorithms which mainly focus on finite dimensional situations (see Kushner and Clark, (1978), Ruppert, (1985), Benveniste et al., (1990), Ljung et al., (1992), Duflo, (1997), Kushner and Yin, (2003), Bottou, (2010) in the multivariate case, and Arnaudon et al., (2010) on manifolds). The literature is much less abundant when one has to consider online observations taking values in a functional space (usually an infinite dimensional Banach or Hilbert space) and most works focus on linear algorithms (Walk, (1977), Dippon and Walk, (2006), Smale and Yao, (2006)).

It is also known in the multivariate setting that averaging procedures can lead to efficient estimation procedure under additional assumptions on the noise and when the target is defined as the minimizer of a strictly convex function (Polyak and Juditsky, (1992), Pelletier, (2000)). There is little work on averaging when considering random variables taking values in Hilbert spaces and, as far as we know, they only deal with linear algorithms (Dippon and Walk, (2006)). Nevertheless, it has been noted in an empirical study whose aim was to estimate the geometric median with functional data (Cardot et al., 2010a ) that averaging could improve in an important way the accuracy of the estimators.

The paper is organized as follows. We first fix notations, give some properties of the geometric median and present our stochastic gradient algorithm as well as its averaged version. We also note that our study extends directly to the estimation of geometric quantiles defined by Chaudhuri, (1996). In a third section we state the almost sure consistency and the rates of convergence of the stochastic gradient estimators as well as the asymptotic normality of its averaged version. We get that the asymptotic distribution of the averaged version of the algorithm is the same as the classic estimators. A fourth section is devoted to a small simulation study which aims at comparing the performances of our estimator with the static algorithm developed by Vardi and Zhang, (2000). The comparison is performed according to two points of view, for the same sample size and for the same computation time. We also analyze a real example with a large sample of individual television audiences measured every second over a period of 24 hours. The proofs are gathered in Section 6.

2 The algorithms and some properties of the geometric median

2.1 Definitions and assumptions

Let be a separable Hilbert space such as or , for some closed interval . We denote by its inner product and by the associated norm.

The geometric median of a random variable taking values in is defined by (see Kemperman, (1987)):

| (1) |

Note that this general definition (1) does not assume the existence of the first order moment of We suppose from now on that the following assumptions are fulfilled.

-

A1.

The random variable is not concentrated on a straight line: for all there is such that and

-

A2.

The law of is a mixing of two “nice” distributions : , where

-

–

is not strongly concentrated around single points: if is the ball , and is a random variable with law ,

-

–

is a discrete measure, . We denote by the support of and assume that .

-

–

As shown in Kemperman, (1987), assumption (A1) ensures that the median is uniquely defined. The second assumption could probably be relaxed, but it is general enough for most natural examples. As noted in Chaudhuri, (1992), the conditions on are satisfied when with , whenever has a bounded density on every compact subset of . More precisely, this property is closely related to small ball probabilities since

If for some small and some positive constant it is easy to check that

whenever

When the dimension is not finite and small ball probabilities have been derived for some particular classes of Gaussian processes (see Nazarov, (2009) for a recent reference). In this case, by symmetry of the distribution, the median is equal to the mean, and many processes satisfy, for positive constants which depend on the process under study,

| (2) |

so that for all positive . Similar properties of shifted small balls, for close to can be found in Li and Shao, (2001).

2.2 Some convexity and robustness properties of the median

In this section we derive quantitative convexity bounds which will be useful in the proofs. As a consequence, we are also able to bound for the gross sensitivity error, which is a classical robustness indicator (see Huber and Ronchetti, (2009)).

Recalling the definition of the median (eq. (1)), let us denote by the function we would like to minimize:

| (3) |

This function is convex since it is a convex combination of convex functions. However, convexity is not sufficient to get the convergence of the algorithm. Under assumptions (A1) and (A2) this function can be decomposed in two parts:

where the discrete part has been isolated. The first part is Fréchet differentiable everywhere (Kemperman, (1987)), so is differentiable except on , the support of the discrete part . We denote by its Fréchet derivative,

Remark 1.

It will be useful to define on the set . If , we define by “forgetting” ,

This function is Fréchet differentiable in , and we let

The median is then the unique solution of the nonlinear equation,

| (5) |

To exhibit some useful strong convexity and robustness properties of the median we need to introduce the Hessian of functional , for . It is denoted by maps to and it is easy to check (see Koltchinskii, (1997) for the multivariate case and Gervini, (2008) for the functional one) that

where is the identity operator in and for and belonging to The operator is not compact but it is bounded when

If we define , and the projection onto the orthogonal complement of ,

| (6) |

We can now state a strong convexity property of functional which can be seen as an extension to an infinite dimensional setting of Proposition 4.1 in Koltchinskii, (1997).

Proposition 2.1.

Recall that is the ball of radius in . Under assumptions A1 and A2, there is a strictly positive constant , such that:

In other words, is strictly convex in and it is strongly convex on any bounded set, as shown in the following corollary.

Corollary 2.2.

Assume hypotheses of Proposition 2.1 are fulfilled. For any strictly positive , there is a strictly positive constant such that:

As a particular case of Proposition 2.1, we get that there exist two strictly positive constants such that

| (7) |

As noted in Kemperman, (1987), the geometric median has a 50 % breakdown point. Furthermore, an immediate consequence of (7) is that operator has a bounded inverse. Thus, the gross error sensitivity, which is also a classical indicator of robustness, is bounded for the median in a separable Hilbert space. Indeed, thanks to the expression derived in Gervini, (2008), it is bounded as follows,

2.3 The algorithms

Given , independent copies of , a natural estimator of is the solution of the empirical version of (5),

The solution is defined implicitly and is found by iterative algorithms.

We propose now an alternative and simple estimation algorithm which can be seen as a stochastic gradient algorithm (Ruppert, (1985); Duflo, (1997)) and is defined as follows

| (8) |

with a starting point that can be random and bounded, e.g. for some positive constant fixed in advance, or deterministic. If , we set and so the algorithm does not move. The sequence of descent steps controls the convergence of the algorithm. The direction is an “estimate” of the gradient of at since the conditional expectation given the sequence of -algebra satisfies

| (9) |

Note that our particular choice of subgradient ensures that this equality always holds.

Defining now by the sequence of “errors” in these estimates,

| (10) |

algorithm (8) can also be seen as a non linear Robbins-Monro algorithm,

| (11) |

Thanks to (9) and (10), the sequence is a sequence of martingale differences. Let us note that the bracket of the associated martingale satisfies,

| (12) |

Our second algorithm consists in averaging all the estimated past values,

with so that

Remark 2.

An extension of the notion of quantiles in Euclidean and Hilbert spaces has been proposed by Chaudhuri, (1996). In such spaces, quantiles are associated to a direction and a magnitude specified by a vector such that . The geometric quantile of say corresponding to direction and magnitude is defined, uniquely under previous assumptions, by

If one recovers the geometric median. When is close to one, is a (directed) extreme quantile. In any case, is characterized by:

so that it can be naturally estimated with the following stochastic algorithm

as well as with its averaged version.

3 Convergence results

3.1 Almost sure convergence of the stochastic gradient algorithm

We first state the almost sure consistency of our sequence of estimators under classical and general assumptions on the descent steps

Theorem 3.1.

If (A1) and (A2) hold, and if satisfies the usual conditions:

then

3.2 Rates of convergence and asymptotic normality

We present now the rates of convergence of the stochastic gradient algorithm as well as the asymptotic distribution of its averaged version. The proofs are given in Section 6. More specific sequences are considered and we suppose from now on that , where is a positive constant and . We need one additional assumption to get these rates of convergence:

-

A3.

There is a positive constant such that

(13)

This assumption is not restrictive when the dimension is strictly larger than two as discussed in Section 2.1.

The following proposition states that, on events of arbitrarily high probability, the functional estimator attains the classical rates of convergence in quadratic mean (see (Duflo,, 1997, theorem 2.2.12) for the multivariate case) up to a logarithmic factor.

Proposition 3.2.

Assume (A1), (A2) and (A3). Then, there exist an increasing sequence of events , and constants , such that , and

Remark 3.

An immediate consequence of Proposition 3.2 is that

Assumption (A3) is needed to bound the difference between and its quadratic approximation, in a neighborhood of as stated in the following Lemma.

Lemma 3.3.

Assume (A3) is in force. Then,

Finally, Theorem 3.4 stated below probably gives the most important result of this work. It is shown that the averaged estimator and the classic static estimator have the same asymptotic distribution. Consequently, for large sample sizes, it is possible to get, very quickly, estimators which are as efficient, at first order, as the slower static one Note that the asymptotic distribution of has been derived in the multivariate case by Haberman, (1989), Theorem 6.1. For variables taking values in a Hilbert space, such asymptotic distribution has only been proved for a particular case, when the support of is a finite dimensional space (Theorem 6 in Gervini, (2008)).

Theorem 3.4.

Assume (A1), (A2) and (A3). Then,

with,

Note that with (7), operator is well defined, it is bounded and positive.

4 Illustrations on simulated and real data

4.1 A simulation study

A simple simulation study is performed to check the good behavior of the averaged stochastic estimator and to make a comparison with the static estimator developed by Vardi and Zhang, (2000). Two points of view are considered. The first classic one consists in evaluating the performances of these two different approaches for different sample sizes. The second one, which is the point of view that should be adopted when computation time matters, consists in comparing the accuracy of both approaches when the allocated computation time is fixed in advance.

We use ![]() (R Development Core Team, (2010)) and the function spatial.median from the library ICSNP to estimate the median with the algorithm developed by Vardi and Zhang, (2000).

(R Development Core Team, (2010)) and the function spatial.median from the library ICSNP to estimate the median with the algorithm developed by Vardi and Zhang, (2000).

For simplicity, we consider random variables taking values in and make simulations of Gaussian random vectors with median and covariance matrix:

In order to compare the accuracy of the different algorithms, we compute the following estimation error,

| (14) |

where is an estimator of

Our averaged estimator depends on the tuning parameters and which control the descent steps It is well known that for the particular case , the choice of parameter is crucial for the convergence and depends on the second derivative of in which is unknown in practice. As usually done for such procedures, we fix and focus on the choice of We also run in parallel the algorithm for 10 initial points chosen randomly in the sample and then select the best estimate which corresponds to the minimum value of

which is the empirical version of (3).

4.1.1 Fixed sample sizes

We perform 1000 simulations for different sample sizes, and Table 1 presents basic statistics for the estimation errors (first quartile , median and third quartile ), according to criterion (14), for the algorithm by Vardi and Zhang, (2000) and our averaged procedure considering different values for

| n=250 | n=500 | n=2000 | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Estimator | [Q1 | median | Q3] | [Q1 | median | Q3] | [Q1 | median | Q3] |

| 0.45 | 0.60 | 0.80 | 0.38 | 0.53 | 0.69 | 0.25 | 0.35 | 0.47 | |

| 0.21 | 0.29 | 0.40 | 0.15 | 0.21 | 0.29 | 0.06 | 0.09 | 0.12 | |

| 0.15 | 0.22 | 0.31 | 0.11 | 0.16 | 0.21 | 0.05 | 0.08 | 0.10 | |

| 0.15 | 0.21 | 0.30 | 0.09 | 0.15 | 0.20 | 0.05 | 0.07 | 0.10 | |

| 0.13 | 0.19 | 0.25 | 0.09 | 0.13 | 0.18 | 0.04 | 0.06 | 0.09 | |

| 0.13 | 0.18 | 0.25 | 0.09 | 0.13 | 0.18 | 0.04 | 0.06 | 0.09 | |

| 0.12 | 0.18 | 0.25 | 0.09 | 0.13 | 0.18 | 0.04 | 0.06 | 0.08 | |

| 0.13 | 0.19 | 0.26 | 0.09 | 0.13 | 0.18 | 0.04 | 0.06 | 0.09 | |

| 0.13 | 0.19 | 0.26 | 0.09 | 0.13 | 0.18 | 0.04 | 0.06 | 0.09 | |

| 0.14 | 0.20 | 0.27 | 0.09 | 0.14 | 0.19 | 0.05 | 0.07 | 0.09 | |

| Vardi & Zhang | 0.12 | 0.18 | 0.25 | 0.09 | 0.12 | 0.17 | 0.04 | 0.06 | 0.08 |

At first, we can note that even for moderate sample sizes the averaged procedure performs well in comparison with the Vardi and Zhang estimator which only gives slightly better estimations. We can also remark that the averaged stochastic estimator is not much sensitive to the tuning parameter which can take values in the interval without modifying the performances of the estimator. As a matter of fact, we noted on simulations that interesting values for are around or above which is about 2.7 for this particular simulation study.

4.1.2 Fixed computation time

Even if both algorithms require computation times which are (for observations in dimension ), the averaged stochastic gradient approach is much faster (on the same computer, with procedures coded in the same ![]() language).

For example, in previous simulations, if the sample size is the

averaged estimator is about 30 times faster. When the dimension gets larger the difference is even more impressive,

as we will see in the next section.

language).

For example, in previous simulations, if the sample size is the

averaged estimator is about 30 times faster. When the dimension gets larger the difference is even more impressive,

as we will see in the next section.

Let us suppose the allocated time for computation is limited and fixed in advance, say 1 second, and compare the sample sizes that can be handled by the different algorithms. The static estimator by Vardi and Zhang, (2000) can deal with observations, whereas our recursive algorithm, coded in the ![]() language, can take into account observations so that it will gives much better estimates of the median, as seen in Table 1. Finally, if the algorithm is coded in C and called from

language, can take into account observations so that it will gives much better estimates of the median, as seen in Table 1. Finally, if the algorithm is coded in C and called from ![]() , then it is at least 20 times faster than its

, then it is at least 20 times faster than its ![]() analogue, so that it can deal with at least observations, during the same second.

analogue, so that it can deal with at least observations, during the same second.

4.2 Estimation of the median television audience profile

The analysis of audience profiles for different channels, or different days of the year, is an essential tool to understand the consumers’ habits as regards television. The French company Médiamétrie provides official television audience rates in France. Médiamétrie works with a panel of about 9000 individuals and the television sets of these individuals are equipped with sensors that measure the audience of the different channels at a second scale.

A sample of around 7000 people is drawn every day in this panel and the television consumption of the people belonging to this sample is recorded every second. The data are then sent sequentially to Médiamétrie during the night. Survey sampling techniques with unequal probability sampling designs are used by Médiamétrie to select the sample and thus the i.i.d assumption is clearly not satisfied. Nevertheless, our aim is just to give an illustration of the ability of our averaged stochastic algorithm to deal with a large sample of very high dimensional data. Moreover, Médiamétrie has noted in these samples the presence of some atypical behaviors so that robust techniques may be helpful.

We focus our study on the estimation of the television audience profile during the 6th september 2010. After removing from the sample people that did not watch television at all on that day, we finally get a sample of size For each element of the sample, we have a vector where is the number of seconds within a day, and zero values correspond to seconds during the day where is not watching television.

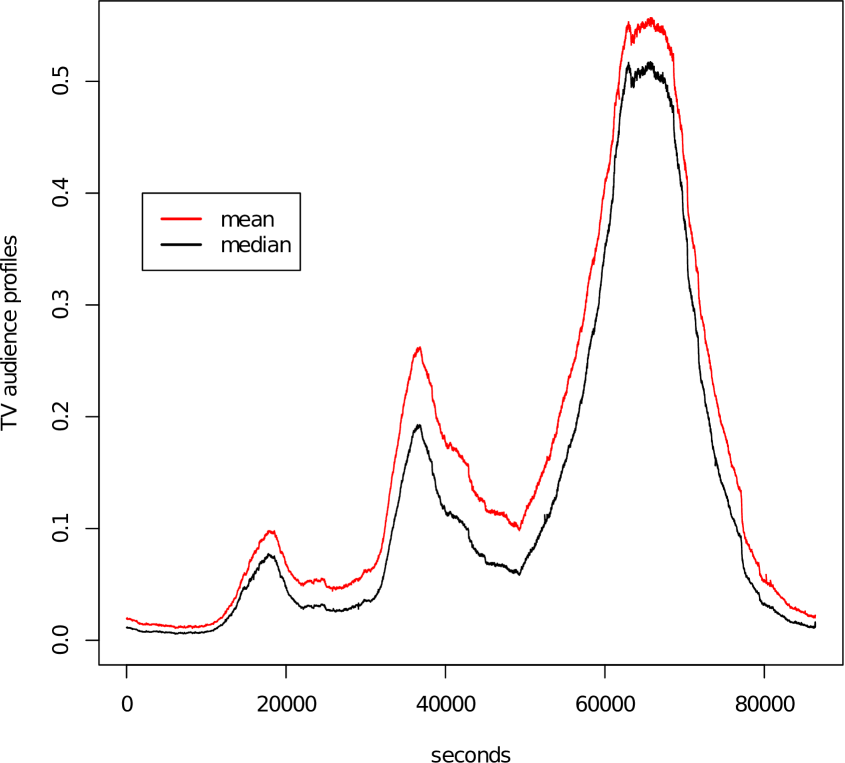

A classical audience indicator is given by the mean profile, drawn in Figure 1, which is simply the proportion of people watching television at every second over the considered period of time. We compare this classical indicator with the geometric median, whose estimation is drawn in black in Figure 1. We can first note that both estimators have the same shape along time, showing three peaks of audience during the day with higher audience rates between 8 and 10 PM. Estimated values are smaller for the geometric median which is less sensitive to small perturbations and outliers. This also indicates that the distribution of the individual audience curves is not symmetric around the mean profile.

From a computational point of view, even if the database is huge, it takes less than one minute for our algorithm to converge whereas we were not able to perform the estimation with the static estimator developed by Vardi and Zhang, (2000) because of memory contraints. The value of the tuning parameter was chosen to be it leads to a value of about 92 for the empirical loss criterion.

5 Concluding remarks

The experimental results confirm that averaged recursive estimators of the geometric median relying on stochastic gradient approaches are of particular interest when one has to deal with large samples of data and potential outliers. Furthermore, when the allocated computation time is limited and fixed in advance and the data arrive online these techniques can deal, in a recursive way, with larger sample sizes and finally provide estimations that are much more accurate than static estimation procedures. We have also noted in the simulation experiment that they are not very sensitive to the value of the tuning parameter

One could imagine many directions for future research that certainly deserve further attention. Taking advantage of the rapidity of our estimation procedure, one could use resampling techniques, similar to the bootstrap, in order to approximate the asymptotic distribution of the estimator given in Theorem 3.4 and then build pointwise confidence intervals. Proving rigorously the validity of such techniques is far beyond the scope of this paper.

Our procedure can also be extended readily for online clustering, adapting the well known MacQueen algorithm (MacQueen, (1967)) to the context. Even if the criterion to be optimized is not convex anymore, it can be proved that stochastic gradient approaches converge almost surely to the set of stationary points (Cardot et al., 2010b ) and thus are interesting candidates for online clustering.

Another direction of interest is online estimation of the conditional geometric median when real covariates are available. For instance, the age or the size of the city where individual live are known by Médiamétrie and it can be possible to take such information into account in order to get varying time regression models that can also be estimated in a very fast way thanks to sequential approaches.

6 Proofs

6.1 Convexity — Proofs of Proposition 2.1 and Corollary 2.2

We first show that is a subgradient of . For points , this is clear since is Fréchet differentiable.

Pick a point in and recall that . We have,

so that is a subgradient of

For the lower bound, thanks to (6), we only need to prove:

| (15) |

where is the projection on the orthogonal of . This quantity is small when is in .

Recall that (by (A1)), is not supported on a line. Consider the set of subspaces satisfying: . Suppose that this set is non-empty, and let be a maximal element in it (this exists by Zorn’s lemma). The orthogonal of has at least dimension (otherwise, we get a contradiction to A1). Let be two orthogonal vectors in . Let . The map

is continuous on a compact set. Its minimum cannot be zero (since this would contradict the maximality of ). Therefore there exists a such that, for all unit in the plane spanned by , .

The orthogonal of (an hyperplane) and the (2-dimensional) plane spanned by and necessarily intersect: there exists a unit vector such that . Therefore, for all , . In particular, .

Suppose first that is a.s. bounded by . Then

It is easily seen that the last term is bounded below by and (15) holds with

To get rid of the boundedness assumption on , we can just choose large enough so that is strictly positive for .

6.2 Proof of Theorem 3.1.

The proof of Theorem 3.1 follows a classical strategy and consists of two steps.

Lemma 6.1.

Under the hypotheses of Theorem 3.1, there is a random variable such that, and

Proof of Lemma 6.1.

Let us consider Recall that (cf. (11)). Therefore

If we condition with respect to , the last term disappears since is a martingale difference sequence and it comes:

| (16) |

where we used the definition of and (12) for the last term. Since is convex, using Corollary 2.2, we get:

Therefore, for all , From the Robbins Siegmund theorem (see for instance (Duflo,, 1997, page 18)), we deduce that converges almost surely to . Moreover, we note that is bounded in

| (17) |

whenever which is satisfied for example if with ∎

We can now give the proof the theorem.

Proof of Theorem 3.1.

Lemma 6.1 shows that the sequence converges almost surely. Let us check now that its limit is zero. Let us take expectations in equation (16):

The sequence has positive terms, and is bounded above by , therefore it converges. This implies in particular that

| (18) |

This convergence cannot happen unless converges to . Indeed, for each let us introduce the set

For we have with Corollary 2.2,

which contradicts (18) unless . Since converges a.s. to a finite limit, and , the only possible limit is zero:

6.3 Proof of Lemma 3.3 and Proposition 3.2

Proof of Lemma 3.3.

Consider, for , the function defined for We have and It is also clear that the first order derivative of function satisfies Consequently, a Taylor expansion with integral remainder of about gives us

By Lemma 5.7 in Chaudhuri, (1992), there is a constant such that for all

where is the usual norm for bounded linear operators. Since one gets

and this concludes the proof. ∎

Proof of Proposition 3.2.

The proof is composed of 5 steps.

Step 1 — a spectral decomposition.

Recall that is:

| (19) |

Since is bounded and symmetric, it is self-adjoint. Moreover, the operator defined by (19) is trace class: it is self-adjoint, non negative, and if is an orthonormal basis,

Therefore is compact, and there is an increasing sequence of eigenvalues with possible repetitions, and an orthonormal basis of eigenvectors in such that:

Moreover, thanks to (7), the smallest eigenvalue of is strictly positive. For simplicity of notation, we rewrite this decomposition as follows,

where is the multiset that can account for eigenspaces of dimension larger than

In the following, we will need the operators:

Since is bounded, these operators are well defined. Introducing the sequence of real functions, for

we see that and are well defined on provided which we can assume without loss of generality. Elementary analysis shows that there exist constants , such that:

| (20) | ||||

where we recall that , and . Then each operator can be also expressed as follows:

their inverses are bounded operators, and satisfy:

Step 2 — Decomposition of the algorithm.

Let us rewrite the algorithm in the following way

where is the difference between the gradient of and the gradient of its quadratic approximation. Therefore:

| (21) |

Rewriting as , we get by induction,

| (22) |

where

The first two terms of (22) are what we would get if was exactly quadratic: a deterministic gradient part going to , and a noise part; is the error term. We will look at each of these terms in turn.

Step 3 — The deterministic term.

We want to bound . The asymptotic behaviour of in eq. (20) implies that

where is the smallest eigenvalue of . Therefore

| (23) |

Step 4 — The martingale.

The fact that the are operators (instead of real numbers) makes matters more complicated. To deal with this problem, we use the spectral decomposition of the sequence of self-adjoint operators

More precisely, we decompose . For each , is a martingale, and

since when Summing now over , we get:

However, for any , and any ,

This uniformity in allows us to reconstruct , which is bounded by , thanks to (12). We obtain:

Now we use the bounds (20) on :

| (24) |

The exponential terms are very small when is much smaller than , therefore we isolate the last terms. To do that, we choose such that,

| (25) |

with to be chosen later. The first part of the sum (24) (for ) gives us:

| (26) |

This can be made smaller than any prescribed inverse power of , if we choose large enough. In the second part of the sum (24), for , we bound the exponential by and by :

The number of terms is equivalent to , and . Therefore, the whole second term is equivalent to where depends on and For large enough, this dominates the first term (26). Finally we get:

| (27) |

Step 5 — the error term and the conclusion.

The error term is , where . With Lemma 3.3, we get that

| (28) |

Since converges a.s. to , we deduce two things about : it is almost surely bounded, and (28) becomes a.s. eventually true. To use these facts we introduce the following sequence of events:

for a value of to be chosen later, and defined by (25). This sequence is increasing and ; from now on we work on .

Once more, since is very small when is much smaller than , only the last terms in the sum defining matter. This is why we re-use the definition of and cut the sum in two parts. For , and ,

where we used the crude bound in the first part, and for the second part, and the definition of .

As before, it is easy to see that the first term is bounded by any prescribed inverse power of , say . For the second term, we already know that is bounded. Therefore, on and for

| (29) |

Let us choose such that . Then

Defining , this reads:

| (30) |

Let us prove by induction that, for some large enough, and for ,

Suppose that for all , and let us prove that . Using (30), we know that:

If the max on the right hand side is , we get:

which is the desired result since . If this is not the case, then the is . However, so for larger than some , . Hence

This concludes the induction step and the proof of Proposition 3.2. ∎

6.4 Proof of Theorem 3.4

We use the same decomposition as in Pelletier, (2000). It consists in linearizing the target function around the true value Recall the following decomposition of the error (21),

where is a martingale difference sequence and are error terms, . Defining now,

and rearranging the previous expression, we obtain:

Summing these equalities, it comes,

Applying Abel’s transform, and dividing by yields:

To prove that last term is a martingale for which the CLT holds,

we need to check that the assumptions of Theorem 5.1 in (Jakubowski,, 1988) are fulfilled. We first have that the martingale difference sequence is a.s. bounded, Let us define

which can also be decomposed as follows

Since we have by a direct computation,

Using now, for the inequality where is the usual the norm for linear operators, we directly get, with Theorem 3.1,

With similar arguments, it is easy to show that

so that when tends to infinity. Then condition 5.2 in (Jakubowski,, 1988) is satisfied and is a consequence of a direct application of Chow’s Lemma, see for instance (Duflo,, 1997, page 22).

Now, it remains to prove that

| (31) |

Let us denote by , and the three terms.

Let us turn to the second term . Since we have, for two positive constants ,

which goes to zero since . Therefore .

Finally, for the last term , since there exists a positive constant such that , we have:

Since the right hand side term converges to zero (as can be seen e.g. by Kronecker’s lemma, using the fact that ), , therefore (31) holds, and Theorem 3.4 is finally proved.

Acknowledgements. We would like to thank the referees for their helpful and valuable suggestions. We also thank the company Médiamétrie for allowing us to illustrate our methodologies with their data.

References

- Arnaudon et al., (2010) Arnaudon, M., Dombry, C., Phan, A., and Yang, L. (2010). Stochastic algorithms for computing means of probability measures. Preprint, http://hal.archives-ouvertes.fr/hal-00540623/PDF/algo_means4.pdf.

- Benveniste et al., (1990) Benveniste, A., Métivier, M., and Priouret, P. (1990). Adaptive Algorithms and Stochastic Approximations, volume 22 of Applications of Mathematics. Springer-Verlag, New York.

- Bottou, (2010) Bottou, L. (2010). Large-scale machine learning with stochastic gradient descent. In Lechevallier, Y. and Saporta, G., editors, Compstat 2010, pages 177–186. Physica Verlag, Springer.

- Cadre, (2001) Cadre, B. (2001). Convergent estimators for the -median of a Banach valued random variable. Statistics, 35(4):509–521.

- (5) Cardot, H., Cénac, P., and Chaouch, M. (2010a). Stochastic approximation to the multivariate and the functional median. In Lechevallier, Y. and Saporta, G., editors, Compstat 2010, pages 421–428. Physica Verlag, Springer.

- (6) Cardot, H., Cénac, P., and Monnez, J.-M. (2010b). Fast clustering of large datasets with sequential -medians : a stochastic gradient approach. Technical report, Institut de Mathématiques de Bourgogne.

- Chaouch and Goga, (2010) Chaouch, M. and Goga, C. (2010). Design-based estimation for geometric quantiles with application to outliers detection. Computational Statistics and Data Analysis, 54:2214–2229.

- Chaudhuri, (1992) Chaudhuri, P. (1992). Multivariate location estimation using extension of -estimates through -statistics type approach. Ann. Statist., 20:897–916.

- Chaudhuri, (1996) Chaudhuri, P. (1996). On a geometric notion of quantiles for multivariate data. J. Amer. Statist. Assoc., 91(434):862–872.

- Cuevas et al., (2007) Cuevas, A., Febrero, M., and Fraiman, R. (2007). Robust estimation and classification for functional data via projection-based depth notions. Computational Statistics, 22:481–496.

- Dippon and Walk, (2006) Dippon, J. and Walk, H. (2006). The averaged Robbins-Monro method for linear problems in a Banach space. J. Theoret. Probab., 19(1):166–189.

- Duflo, (1997) Duflo, M. (1997). Random iterative models, volume 34 of Applications of Mathematics (New York). Springer-Verlag, Berlin. Translated from the 1990 French original by Stephen S. Wilson and revised by the author.

- Fraiman and Muniz, (2001) Fraiman, R. and Muniz, G. (2001). Trimmed means for functional data. TEST, 10:419–440.

- Gervini, (2008) Gervini, D. (2008). Robust functional estimation using the median and spherical principal components. Biometrika, 95(3):587–600.

- Gower, (1974) Gower, J. C. (1974). Algorithm as 78: The mediancentre. Journal of the Royal Statistical Society. Series C (Applied Statistics), 23(3):466–470.

- Haberman, (1989) Haberman, J. (1989). Concavity and estimation. Ann. Statist., 17:1631–1661.

- Haldane, (1948) Haldane, J. B. S. (1948). Note on the median of a multivariate distribution. Biometrika, 35(3-4):414–417.

- Huber and Ronchetti, (2009) Huber, P. and Ronchetti, E. (2009). Robust Statistics. John Wiley and Sons, second edition.

- Jakubowski, (1988) Jakubowski, A. (1988). Tightness criteria for random measures with application to the principle of conditioning in Hilbert spaces. Probab. Math. Statist., 9(1):95–114.

- Kemperman, (1987) Kemperman, J. H. B. (1987). The median of a finite measure on a Banach space. In Statistical data analysis based on the -norm and related methods (Neuchâtel, 1987), pages 217–230. North-Holland, Amsterdam.

- Koltchinskii, (1997) Koltchinskii, V. I. (1997). -estimation, convexity and quantiles. Ann. Statist., 25(2):435–477.

- Kushner and Clark, (1978) Kushner, H. J. and Clark, D. S. (1978). Stochastic Approximation Methods for Constrained and Unconstrained Systems. Springer-Verlag, Berlin.

- Kushner and Yin, (2003) Kushner, H. J. and Yin, G. G. (2003). Stochastic approximation and recursive algorithms and applications, volume 35 of Applications of Mathematics (New York). Springer-Verlag, New York, second edition. Stochastic Modelling and Applied Probability.

- Li and Shao, (2001) Li, W. and Shao, Q.-M. (2001). Gaussian processes: Inequalities, small ball probabilities and applications. In Rao, C. and Shanbhag, D., editors, Stochastic Processes: Theory and Methods. Handbook of Statistics, volume 19, pages 533–598. Elsevier, New York.

- Ljung et al., (1992) Ljung, L., Pflug, G., and Walk, H. (1992). Stochastic Approximation and Optimization of Random Systems. Birkhäuser, Boston.

- MacQueen, (1967) MacQueen, J. (1967). Some methods for classification and analysis of multivariate observations. In Proc. Fifth Berkeley Sympos. Math. Statist. and Probability (Berkeley, Calif., 1965/66), pages Vol. I: Statistics, pp. 281–297. Univ. California Press, Berkeley, Calif.

- Nazarov, (2009) Nazarov, A. (2009). Exact -small ball asymptotics of gaussian processes and the spectrum of boundary-value problems. J. Theoret. Probab., 22:640–665.

- Pelletier, (2000) Pelletier, M. (2000). Asymptotic almost sure efficiency of averaged stochastic algorithms. SIAM J. Control Optim., 39(1):49–72 (electronic).

- Polyak and Juditsky, (1992) Polyak, B. and Juditsky, A. (1992). Acceleration of stochastic approximation. SIAM J. Control and Optimization, 30:838–855.

- R Development Core Team, (2010) R Development Core Team (2010). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria. ISBN 3-900051-07-0.

- Ruppert, (1985) Ruppert, D. (1985). A Newton-Raphson version of the multivariate Robbins-Monro procedure. Ann. Statist., 13(1):236–245.

- Smale and Yao, (2006) Smale, S. and Yao, Y. (2006). Online learning algorithms. Found. Comput. Math., 6(2):145–170.

- Small, (1990) Small, C. G. (1990). A survey of multidimensional medians. International Statistical Review / Revue Internationale de Statistique, 58(3):263–277.

- Vardi and Zhang, (2000) Vardi, Y. and Zhang, C.-H. (2000). The multivariate -median and associated data depth. Proc. Natl. Acad. Sci. USA, 97(4):1423–1426 (electronic).

- Walk, (1977) Walk, H. (1977). An invariance principle for the Robbins-Monro process in a Hilbert space. Z. Wahrscheinlichkeitstheorie und Verw. Gebiete, 39(2):135–150.