Sparse Single-Index Model

Pierre Alquier111Corresponding author.

LPMA222Research partially supported by the French “Agence Nationale pour la Recherche” under grant ANR-09-BLAN-0128 “PARCIMONIE”.

Université Paris Diderot – Paris VII

Boîte 188, 175 rue du Chevaleret

75013 Paris, France

CREST-LS

3 avenue Pierre Larousse

92240 Malakoff, France

alquier@math.jussieu.fr

Gérard Biau

LSTA & LPMA333Research partially supported by the French “Agence Nationale pour la Recherche” under grant ANR-09-BLAN-0051-02 “CLARA”.

Université Pierre et Marie Curie – Paris VI

Boîte 158, Tour 15-25, 2ème étage

4 place Jussieu, 75252 Paris Cedex 05, France

DMA444Research carried out within the INRIA project “CLASSIC” hosted by Ecole Normale Supérieure and CNRS.

Ecole Normale Supérieure

45 rue d’Ulm

75230 Paris Cedex 05, France

gerard.biau@upmc.fr

Abstract

Let be a random pair taking values in . In the so-called single-index model, one has , where is an unknown univariate measurable function, is an unknown vector in , and denotes a random noise satisfying . The single-index model is known to offer a flexible way to model a variety of high-dimensional real-world phenomena. However, despite its relative simplicity, this dimension reduction scheme is faced with severe complications as soon as the underlying dimension becomes larger than the number of observations (“ larger than ” paradigm). To circumvent this difficulty, we consider the single-index model estimation problem from a sparsity perspective using a PAC-Bayesian approach. On the theoretical side, we offer a sharp oracle inequality, which is more powerful than the best known oracle inequalities for other common procedures of single-index recovery. The proposed method is implemented by means of the reversible jump Markov chain Monte Carlo technique and its performance is compared with that of standard procedures.

Index Terms — Single-index model, sparsity, regression estimation, PAC-Bayesian, oracle inequality, reversible jump Markov chain Monte Carlo method.

2010 Mathematics Subject Classification: 62G08, 62G05, 62G20.

1 Introduction

Let be a collection of independent observations, distributed as a generic independent pair taking values in and satisfying . Throughout, we let be the distribution of , so that the sample is distributed according to . In the regression function estimation problem, the goal is to use the data in order to construct an estimate of the regression function . In the classical parametric linear model, one assumes

where and . Here

is a linear function of the components of . More generally, we may define

| (1.1) |

where is an unknown univariate measurable function. This is the celebrated single-index model, which is recognized as a particularly useful variation of the linear formulation and can easily be interpreted: The model changes only in the direction , and the way it changes in this direction is described by the function . This model has applications to a variety of fields, such as discrete choice analysis in econometrics and dose response models in biometrics, where high-dimensional regression models are often employed. There are too many references to be included here, but the monographs of McCullagh and Nelder [33] and Horowitz [27] together with the references [25, 28, 21, 18, 29] will provide the reader with good introductions to the general subject area.

One of the main advantages of the single-index model is its supposed ability to deal with the problem of high dimension (Bellman [6]). It is known that estimating the regression function is especially difficult whenever the dimension of becomes large. As a matter of fact, the optimal mean square convergence rate for the estimation of a -times differentiable regression function converges to zero dramatically slowly if the dimension is large compared to . This leads to an unsatisfactory accuracy of estimation for moderate sample sizes, and one possibility to circumvent this problem is to impose additional assumptions on the regression function. Thus, in particular, if holds for every , then the underlying structural dimension of the model is 1 (instead of ) and the estimation of can hopefully be performed easier. In this regard, Gaïffas and Lecué show in [22] that the optimal rate of convergence over the single-index model class is (instead of ), thereby answering a conjecture of Stone [40].

Nevertheless, practical estimation of the link function and the index still requires a degree of statistical smoothing. Perhaps the most common approach to reach this goal is to use a nonparametric smoother (for instance, a kernel or a local polynomial method) to construct an approximation of , then substitute into an empirical version of the mean square error , and finally choose to minimize (see e.g. Härdle, Hall and Ichimura [25] and Delecroix, Hristache and Patilea [21] where the procedure is discussed in detail). The rationale behind this type of two-stage approach, which is asymptotic in spirit, is that it produces a -consistent estimate of , thereby devolving the difficulty to the simpler problem of computing a good estimate for the one-dimensional function . However, the relative simplicity of this strategy is accompanied by severe difficulties (overfitting) when the dimension becomes larger than the number of observations . Estimation in this setting (called “ larger than ” paradigm) is generally acknowledged as an important challenge in contemporary statistics, see e.g. the recent monograph of Bühlmann and van de Geer [9]. In fact, this drawback considerably reduces the ability of the single-index model to behave as an effective dimension reduction technique.

On the other hand, there is empirical evidence that many signals in high-dimensional spaces admit a sparse representation. As an example, wavelet coefficients of images often exhibit exponential decay, and a relatively small subset of all wavelet coefficients allow for a good approximation of the original image. Such signals have few nonzero coefficients and can therefore be described as sparse in the signal domain (see for instance [8]). Similarly, recent advances in high-throughput technologies—such as array comparative genomic hybridization—indicate that, despite the huge dimensionality of problems, only a small number of genes may play a role in determining the outcome and be required to create good predictors ([43] for instance). Sparse estimation is playing an increasingly important role in the statistics and machine learning communities, and several methods have recently been developed in both fields, which rely upon the notion of sparsity (e.g. penalty methods like the Lasso and Dantzig selector, see [41, 11, 10, 7] and the references therein).

In the present document, we consider the single-index model (1.1) from a sparsity perspective, i.e., we assume that has only a few coordinates different from . In the dimension reduction scenario we have in mind, the ambient dimension can be very large, much larger than the sample size , but we believe that the representation is sparse, i.e., that very few coordinates of are nonzero. This assumption is helpful at least for two reasons: If is large and the number of nonzero coordinates is small enough, then the model is easier to interpret and its efficient estimation becomes possible. Our setting is close in spirit of the approach of Cohen, Daubechies, DeVore, Kerkyacharian and Picard [16], who study approximation from queries of functions of the form , where is approximately sparse (in the sense that it belongs to a weak- space). However, these authors dot not provide any statistical study of their model. Our modus operandi will rather rely on the so-called PAC-Bayesian approach, originally developed in the classification context by Shawe-Taylor and Williamson [39], McAllester [32] and Catoni [12, 13]. This strategy was further investigated for regression by Audibert [4] and Alquier [1] and, more recently, worked out in the sparsity framework by Dalalyan and Tsybakov [19, 20] and Alquier and Lounici [2]. The main message of [19, 20, 2] is that aggregation with a properly chosen prior is able to deal nicely with the sparsity issue. Contrary to procedures such as the Lasso, the Dantzig selector and other penalized least square methods, which achieve fast rates under rather restrictive assumptions on the Gram matrix associated to the predictors, PAC-Bayesian aggregation requires only minimal assumptions on the model. Besides, it is computationally feasible even for a large and exhibits good statistical performance.

The paper is organized as follows. In Section 2, we first set out some notation and introduce the single-index estimation procedure. Then we state our main result (Theorem 2.1), which offers a sparsity oracle inequality more powerful than the best known oracle inequalities for other common procedures of single-index recovery. Section 3 is devoted to the practical implementation of the estimate via a reversible jump Markov chain Monte Carlo (MCMC) algorithm, and to numerical experiments on both simulated and real-life data sets. In order to preserve clarity, proofs have been postponed to Section 4 and the description of the MCMC method in its full length is given in the Appendix Section 5.

Note finally that our techniques extend to the case of multiple-index models, of the form

where the underlying structural dimension is supposed to be larger than 1 but substantially smaller than . However, to keep things simple, we let and leave the reader the opportunity to adapt the results to the more general situation .

2 Sparse single-index estimation

We start this section with some notation and basic requirements.

2.1 Notation

Throughout the document, we suppose that the recorded data is generated according to the single-index model (1.1). More precisely, for each ,

where is a univariate measurable function, is a -variate vector, and are independent copies of . We emphasize that it is implicitly assumed that the observations are drawn according to the true model under study. Therefore, this casts our problem in a nonparametric setting rather than in a classical PAC-Bayesian one.

Recall that, in model (1.1), and, consequently, that . However, the distribution of (in particular, the variance) may depend on . We shall not precisely specify this dependence, and will rather require the following condition on the distribution of .

Assumption . There exist two positive constants and such that, for all integers ,

Observe that Assumption holds in particular if , where is a standard Gaussian random variable independent of and is almost surely bounded.

Let denote the -norm of the vector , i.e., . Without loss of generality, it will be assumed throughout the document that the index belongs to , where is the set of all with and , where is the smallest such that .

We will also require that the random variable is almost surely bounded by a constant which, without loss of generality, can be taken equal to 1. Moreover, it will also be assumed that the link function is bounded by some known positive constant . Thus, denoting by the supremum norm of and by the functional supremum norm of over , we set:

Assumption . The condition holds almost surely and there exists a positive constant larger than 1 such that

Remark 2.1

To keep a sufficient degree of clarity, no attempt was made to optimize the constants. In particular, the requirement is purely technical. It can easily be removed by replacing by throughout the document.

In order to approximate the link function , we shall use the vector space spanned by a given countable dictionary of measurable functions . Put differently, the approximation space is the set of (finite) linear combinations of functions of the dictionary. Each of the collection is assumed to be defined on and to take values in . To avoid getting into too much technicalities, we will also assume that each is differentiable and such that, for some positive constant , . This assumption is satisfied by the (non-normalized) trigonometric system

Finally, for any measurable and , we let

and denote by

the empirical counterpart of based on the sample .

2.2 Estimation procedure

We are now in a position to describe our estimation procedure. The method which is presented here is inspired by the approach developed by Catoni in [12, 13]. It strongly relies on the choice of a probability measure on , called the prior, which in our framework should enforce the sparsity properties of the target regression function. With this objective in mind, we first let

i.e., we assume that the distribution over the indexes is independent of the distribution over the link functions. With respect to the parameter , we put

| (2.1) |

where denotes the cardinality of and is the uniform probability measure on the set

We see that may be interpreted as the set of “active” coordinates in the single-index regression of on , and note that the prior on is a convex combination of uniform probability measures on the subsets . The weights of this combination depend only on the size of the active coordinate subset . As such, the value characterizes the sparsity of the model: The smaller , the smaller the number of variables involved in the model. The factor penalizes models of high dimension, in accordance with the sparsity idea.

The choice of the prior on is more involved. To begin with, we define, for any positive integer and all ,

Next, we let be the image of by the map

It is worth pointing out that, roughly, Sobolev spaces are well approximated by as grows (more on this in Subsection 2.3). Finally, we define on the set as the image of the uniform measure on induced by the map , and take

| (2.2) |

Some comments are in order here. First, we note that the prior is defined on endowed with its canonical Borel -field. The choice of instead of in the definition of the prior support is essentially technical. This bound ensures that when the target belongs to , then a small ball around it is contained in . It could be safely replaced by , where is any positive sequence vanishing sufficiently slowly as . Next, the integer should be interpreted as a measure of the “dimension” of the function —the larger , the more complex the function—and the prior adapts again to the sparsity idea by penalizing large-dimensional functions . The coefficients and which appear in (2.1) and (2.2) show that more complex models have a geometrically decreasing influence. Note however that the value 10, which has been chosen because of its good practical results, is somehow arbitrary. It could be, in all generality, replaced by a more general coefficient at the price of a more technical analysis. Finally, we observe that, for each ,

Now, let be a positive real number, called the inverse temperature parameter hereafter. The estimates and of and , respectively, are simply obtained by randomly drawing

where is the so-called Gibbs posterior distribution over , defined by the probability density

[The notation means the density of with respect to .] The estimate has a simple interpretation. Firstly, the level of significance of each pair is assessed via its least square error performance on the data . Secondly, a Gibbs distribution with respect to the prior enforcing those pairs with the most empirical significance is assigned on the space . Finally, the resulting estimate is just a random realization (conditional to the data) of this Gibbs posterior distribution.

2.3 Sparsity oracle inequality

For any and any positive integer , we set

At this stage, it is very important to note that, for each , the infimum is defined on , whereas the prior charges a slightly bigger set, namely .

The main result of the paper is the following theorem. Here and everywhere, the wording “with probability ” means the probability evaluated with respect to the distribution of the data and the conditional probability measure . Recall that is a positive constant such that .

Theorem 2.1

Assume that Assumption and Assumption hold. Set and take

| (2.3) |

Then, for all , with probability at least we have

where is a positive constant, function of , , and only.

Remark 2.2

Interestingly enough, analysis of the estimate is still possible when Assumption is not satisfied. Indeed, even if Bernstein’s inequality (see Lemma 4.1) is not valid, a recent paper by Seldin, Cesa-Bianchi, Laviolette, Auer, Shawe-Taylor and Peters [38] provides us with a nice alternative inequality assuming less restrictive assumptions. However, we would then suffer a loss in the upper bound of Theorem 2.1. It is also interesting to note that recent results by Audibert and Catoni [5] allow the study of PAC-Bayesian estimates without Assumption N. However, the results of these authors are valid for linear models only, and it is therefore not clear to what extent their technique can be transposed to our setting.

Theorem 2.1 can be given a simple interpretation. Indeed, we see that if there is a “small” and a “small” such that is close to , then is also close to up to terms of order . However, if no such or exists, then one of the terms and starts to dominate, thereby deteriorating the general quality of the bound. A good approximation with a “small” is typically possible when is sparse or, at least, when it can be approximated by a sparse parameter. On the other hand, a good approximation with a “small” is possible if has a sufficient degree of regularity.

To illustrate the latter remark, assume for instance that is the (non-normalized) trigonometric system and suppose that the target belongs to the Sobolev ellipsoid, defined by

for some unknown regularity parameter (see, e.g., Tsybakov [42]). Observe that, in this context, the approximation sets take the form

It is important to note that the regularity parameter is assumed to be unknown, and this casts our results in the so-called adaptive setting. The following additional assumption will be needed:

Assumption . The random variable has a probability density on , bounded from above by a positive constant .

Last, we let be the set such that and set .

Corollary 2.1

Assume that Assumption , Assumption and Assumption hold. Suppose also that belongs to the Sobolev ellipsoid , where the real number is an (unknown) regularity parameter. Set and take as in (2.3). Then, for all , with probability at least we have

| (2.4) |

where is a positive constant, function of , , , and only.

As far as we are aware, all existing methods achieving rates of convergence similar to the ones provided by Corollary 2.1 are valid in an asymptotic setting only ( fixed and ). The strength of Corollary 2.1 is to provide a finite sample bound and to show that our estimate still behaves well in a nonasymptotic situation if the intrinsic dimension (i.e., the sparsity) is small with respect to . To understand this remark, just assume that is a function of such that as . Whereas a classical asymptotic approach cannot say anything clever about this situation, our bounds still provide some information, provided the model is sparse enough (i.e., is sufficiently small with respect to ).

We see that, asymptotically ( fixed and ), the leading term on the right-hand side of inequality (2.4) is . This is the minimax rate of convergence over a Sobolev class, up to a factor. However, when is “small” and is not sparse (i.e., is not “small”), the term starts to emerge and cannot be neglected. Put differently, in large dimension, the estimation of itself is a problem—this phenomenon is not taken into account by asymptotic studies.

It is worth mentioning that the approach developed in the present article does not offer any guarantee on the point of view of variable (feature) selection. To reach this objective, an interesting route to follow is the sufficient dimension reduction (SDR) method proposed by Chen, Zou and Cook [15], which can be applied to the single-index model to estimate consistently the parameter and perform variable selection in a sparsity framework. Note however that such results require strong assumptions on the distribution of the data.

3 Implementation and numerical results

A series of experiments was conducted, both on simulated and real-life data sets, in order to assess the practical capabilities of the proposed method and compare its performance with that of standard procedures. Prior to analysis, we first need to discuss its concrete implementation, which has been carried out via a Markov Chain Monte Carlo (MCMC) method.

3.1 Implementation via reversible jump MCMC

The use of MCMC methods has become a popular way to compute Bayesian estimates. For an introduction to the domain, one should refer to the comprehensive monograph of Marin and Robert [30] and the references therein. Importantly, in this computational framework, an adaptation of the well-known Hastings-Metropolis algorithm to the case where the posterior distribution gives mass to several models of different dimensions was proposed by Green [23] under the name Reversible Jump MCMC (RJMCMC) method. In the PAC-Bayesian setting, MCMC procedures were first considered by Catoni [12], whereas Dalalyan and Tsybakov [19, 20] and Alquier and Lounici [2] explore their practical implementation in the sparse context using Langevin Monte Carlo and RJMCMC, respectively. Regarding the single-index model, MCMC algorithms were used to compute Bayesian estimates by Antoniadis, Grégoire and McKeague [3] and, more recently, by Wang [44], who develop a fully Bayesian method to analyse the single-index model. Our implementation technique is close in spirit to the one of Wang [44].

As a starting point for the approximate computation of our estimate, we used the RJMCMC method of Green [23], which is in fact an adaptation of the Hastings-Metropolis algorithm to the case where the objective posterior probability distribution (here, ) assigns mass to several different models. The idea is to start from an initial given pair and then, at each step, to iteratively compute from via the following chain of rules:

-

•

Sample a random pair according to some proposal conditional density with respect to the prior ;

-

•

Take

where

This protocol ensures that the sequence is a Markov chain with invariant probability distribution (see e.g. Marin and Robert [30]). A usual choice is to take , so that the Markov chain is homogeneous. However, in our context, it is more convenient to let if is odd and if is even. Roughly, the effect of is to modify the index while will essentially act on the link function . While the ideas underlying the proposal densities and are quite simple, a precise description in its full length turns out to be more technical. Thus, in order to preserve the readability of the paper, the explicit construction of and has been postponed to the Appendix Section 5.

From a theoretical point of view, it is clear that the implementation of our method requires knowledge of the constant (the upper bound on ). A too small will result in a smaller model, which is unable to perform a good approximation. On the other hand, a larger induces a poor bound in Theorem 2.1. In practice, however, the influence of turns out to be secondary compared to the impact of the parameter . Indeed, it was found empirically that a very large choice of (e.g., ) does not deteriorate the overall quality of the results, as soon as is appropriately chosen. This is the approach that was followed in the experimental testing process.

Besides, the time for the Markov chains to converge depends strongly on the ambient dimension and the starting point of the simulations. When the dimension is small (typically, ), the chains converge fast and any value may be chosen as a starting point. In this case, we let the MCMC run steps and obtained satisfying results. On the other hand, when the dimension is larger (typically, ), the convergence is very slow, in the sense that takes a very long time to stabilize. However, using as a starting point for the chains the preliminary estimate (see below) significantly reduces the number of steps needed to reach convergence—we let the chains run steps in this context. Nevertheless, as a general rule, we encourage the users to inspect the convergence of the chains by checking if is stabilized, and to run several chains starting from different points to avoid their attraction into local minima.

3.2 Simulation study

In this subsection, we illustrate the finite sample performance of the presented estimation method on three synthetic data sets and compare its predictive capabilities with those of three standard statistical procedures. In all our experiments, we took as dictionary the (non-normalized) trigonometric system and denote accordingly the resulting regression function estimate defined in Section 2 by . In accordance with the order of magnitude indicated by the theoretical results, we set . This choice can undoubtedly be improved a bit but, as the numerical results show, it seems sufficient for our procedure to be fairly competitive.

The tested competing methods are the Lasso (Tibshirani [41]), the standard regression kernel estimate (Nadaraya [34, 35] and Watson [45], see also Tsybakov [42]), and the estimation strategy discussed in Härdle, Hall and Ichimura [25]. While the procedure of Härdle, Hall and Ichimura is specifically tailored for single-index models, the Lasso is designed to deal with the estimation of sparse linear models. On the other hand, the nonparametric kernel method is one of the best options when no obvious assumption (such as the single-index one) can be made on the shape of the targeted regression function.

We briefly recall that, for a linear model of the form , the Lasso estimate takes the form , where

and is a regularization parameter. Theoretical results (see e.g. Bunea, Tsybakov and Wegkamp [10]) indicate that should be of the order . Throughout, is assumed to be known, and we let , since this choice is known to give good practical results. The Nadaraya-Watson kernel estimate will be denoted by . It is defined by

for some nonnegative kernel on and . In the experiments, we let be the Gaussian kernel and chose the smoothing parameter via a classical leave-one-out procedure on the grid , see, e.g., Györfi, Kohler, Krzyżak and Walk [24] (notation stands for the floor function). Finally, the estimation procedure advocated in Härdle, Hall and Ichimura [25] takes the form

for some kernel on , with and

All calculations were performed with the Gaussian kernel. We used the grid for the optimization with respect to , whereas the best search for was implemented via a pathwise coordinate optimization.

The various methods were tested for the general regression model

for three different choices of (single-index or not) and two values of , namely and . In each of these models, the observations take values in , with and , and have independent components uniformly distributed on . The noise variables are independently distributed according to a Gaussian , with . It is worth pointing out that for and , and are of the same order, which means that the setting is nonasymptotic. It is essentially in this case that the use of estimates tailored to sparsity, which reduce the variance, is expected to improve the performance over generalist methods. On the other hand, the situation and is less difficult and mimics the asymptotic setting.

The three examined functions , for , were the following ones:

-

[Model 1] A linear model .

-

[Model 2] A single-index function .

-

[Model 3] A purely nonparametric model ,

where, in the first and second model, . Thus, in [Model 1] and [Model 2], even if the ambient dimension is large, the intrinsic dimension of the model is in fact equal to 2.

For each experiment, a learning set of size was generated to compute the estimates and their performance, in terms of mean square prevision error, was evaluated on a separate test set of the same size. The results are shown in Table 1 ( and Table 2 (. As each experiment was repeated times, these tables report the median, the mean and the standard deviation (s.d.) of the prevision error of each procedure.

| median | 0.061 | 0.063 | 0.046 | 0.293 | |

|---|---|---|---|---|---|

| mean | 0.061 | 0.063 | 0.047 | 0.290 | |

| s.d. | 0.016 | 0.014 | 0.011 | 0.063 | |

| median | 0.050 | 0.067 | 0.307 | 0.198 | |

| mean | 0.069 | 0.080 | 0.338 | 0.208 | |

| s.d. | 0.081 | 0.057 | 0.082 | 0.072 | |

| median | 0.375 | 0.405 | 0.830 | 0.354 | |

| mean | 0.402 | 0.407 | 0.890 | 0.336 | |

| s.d. | 0.166 | 0.110 | 0.176 | 0.006 |

| median | 0.053 | 0.051 | 0.042 | 0.227 | |

|---|---|---|---|---|---|

| mean | 0.056 | 0.050 | 0.043 | 0.237 | |

| s.d. | 0.011 | 0.006 | 0.004 | 0.044 | |

| median | 0.047 | 0.052 | 0.332 | 0.209 | |

| mean | 0.049 | 0.053 | 0.337 | 0.218 | |

| s.d. | 0.009 | 0.012 | 0.063 | 0.045 | |

| median | 0.305 | 0.343 | 0.793 | 0.333 | |

| mean | 0.321 | 0.338 | 0.833 | 0.324 | |

| s.d. | 0.092 | 0.042 | 0.145 | 0.041 |

| median | 0.057 | 1.156 | 0.060 | 0.507 | |

|---|---|---|---|---|---|

| mean | 0.095 | 1.124 | 0.066 | 0.533 | |

| s.d. | 0.143 | 0.241 | 0.026 | 0.081 | |

| median | 0.050 | 0.502 | 0.795 | 0.308 | |

| mean | 0.051 | 0.539 | 0.776 | 0.326 | |

| s.d. | 0.011 | 0.200 | 0.208 | 0.109 | |

| median | 0.358 | 0.788 | 1.910 | 0.374 | |

| mean | 0.504 | 0.771 | 1.931 | 0.391 | |

| s.d. | 0.320 | 0.168 | 0.468 | 0.101 |

| median | 0.053 | 0.092 | 0.050 | 0.519 | |

|---|---|---|---|---|---|

| mean | 0.054 | 0.100 | 0.050 | 0.508 | |

| s.d. | 0.007 | 0.026 | 0.006 | 0.026 | |

| median | 0.047 | 0.242 | 0.503 | 0.329 | |

| mean | 0.070 | 0.267 | 0.502 | 0.339 | |

| s.d. | 0.099 | 0.111 | 0.106 | 0.073 | |

| median | 0.361 | 0.736 | 1.968 | 0.418 | |

| mean | 0.557 | 0.765 | 2.045 | 0.406 | |

| s.d. | 0.519 | 0.226 | 0.546 | 0.076 |

Some comments are in order. First, we note without surprise that:

-

1.

The Lasso performs well in the linear setting [Model 1].

-

2.

The single-index methods and are the best ones when the targeted regression function really involves a single-index model [Model 2].

-

3.

The kernel method gives good results in the purely nonparametric setting [Model 3].

Interestingly, provides slightly better results than the single-index-tailored estimate , especially for . This observation can be easily explained by the fact that does not integrate any sparsity information regarding the parameter , whereas tries to focus on the dimension of the active coordinates, which is equal to 2 in this simulation. As a general finding, we retain that is the most robust of all the tested procedures.

3.3 Real data

The real-life data sets used in this second series of experiments are from two different sources. The first one, called AIR-QUALITY data (, ), has been first used by Chambers, Cleveland, Kleiner and Tukey [14] and has been later considered as a benchmark in the study and comparison of single-index models (see, for example, Antoniadis, Grégoire and McKeague [3] and Wang [44], among others). This data set originated from an environmental study relating ozone concentration measures at meteorological variables, namely wind speed, temperature and radiation. The data is available as a package in the software [37], which we employed in all the numerical experiments. The programs are available upon request from the authors.

The second category of data arises from the UC Irvine Machine Learning Repository http://archive.ics.uci.edu/ml, where the following packages have been downloaded from:

-

•

AUTO-MPG (Quinlan [36], , ).

-

•

CONCRETE (Yeh [46], , ).

-

•

HOUSING (Harrison and Rubinfeld [26], , ).

-

•

SLUMP-1, SLUMP-2 and SLUMP-3, which correspond to the concrete slump test data introduced by Yeh [47] (, ). Since there are 3 different output variables in the original data set, we created a single experiment for each of these variables (1 refers to the output “slump”, 2 to the output “flow” and 3 to the output “28-day Compressive Strength”).

-

•

WINE-RED and WINE-WHITE (Cortez, Cerdeira, Almeida, Matos and Reis [17], , , ).

We refer to the above-mentioned references for a precise description of the meaning of the variables involved in these data sets. For homogeneity reasons, all data were normalized to force the input variables to lie in —in accordance with the setting of our method—and to ensure that all output variables have standard deviation . In two data sets (AIR-QUALITY and AUTO-MPG) there were some missing values and the corresponding observations were simply removed.

For each method and each of the nine data sets, we randomly split the observations in a learning and a test set of equal sizes, computed the estimate on the learning set, evaluated the prediction error on the test set, and repeated this protocol 20 times. The results are summarized in Table 3.

| Data set | |||||

|---|---|---|---|---|---|

| AIR QUALITY | median | 0.117 | 0.099 | 0.107 | 0.129 |

| mean | 0.128 | 0.096 | 0.113 | 0.130 | |

| s.d. | 0.044 | 0.029 | 0.029 | 0.035 | |

| AUTO-MPG | median | 0.044 | 0.049 | 0.070 | 0.068 |

| mean | 0.051 | 0.050 | 0.072 | 0.069 | |

| s.d. | 0.017 | 0.006 | 0.011 | 0.009 | |

| CONCRETE | median | 0.089 | 0.087 | 0.106 | 0.094 |

| mean | 0.091 | 0.087 | 0.107 | 0.094 | |

| s.d. | 0.008 | 0.003 | 0.005 | 0.004 | |

| HOUSING | median | 0.074 | 0.059 | 0.086 | 0.086 |

| mean | 0.076 | 0.061 | 0.085 | 0.088 | |

| s.d. | 0.015 | 0.013 | 0.012 | 0.016 | |

| SLUMP-1 | median | 0.289 | 0.171 | 0.201 | 0.208 |

| mean | 0.244 | 0.187 | 0.213 | 0.226 | |

| s.d. | 0.062 | 0.050 | 0.049 | 0.047 | |

| SLUMP-2 | median | 0.219 | 0.196 | 0.172 | 0.215 |

| mean | 0.216 | 0.194 | 0.171 | 0.213 | |

| s.d. | 0.053 | 0.025 | 0.019 | 0.022 | |

| SLUMP-3 | median | 0.065 | 0.070 | 0.053 | 0.116 |

| mean | 0.073 | 0.079 | 0.052 | 0.126 | |

| s.d. | 0.033 | 0.027 | 0.010 | 0.026 | |

| WINE-RED | median | 0.173 | 0.171 | 0.183 | 0.171 |

| mean | 0.174 | 0.170 | 0.174 | 0.183 | |

| s.d. | 0.009 | 0.008 | 0.007 | 0.010 | |

| WINE-WHITE | median | 0.191 | 0.187 | 0.185 | 0.184 |

| mean | 0.202 | 0.188 | 0.186 | 0.185 | |

| s.d. | 0.045 | 0.003 | 0.004 | 0.004 |

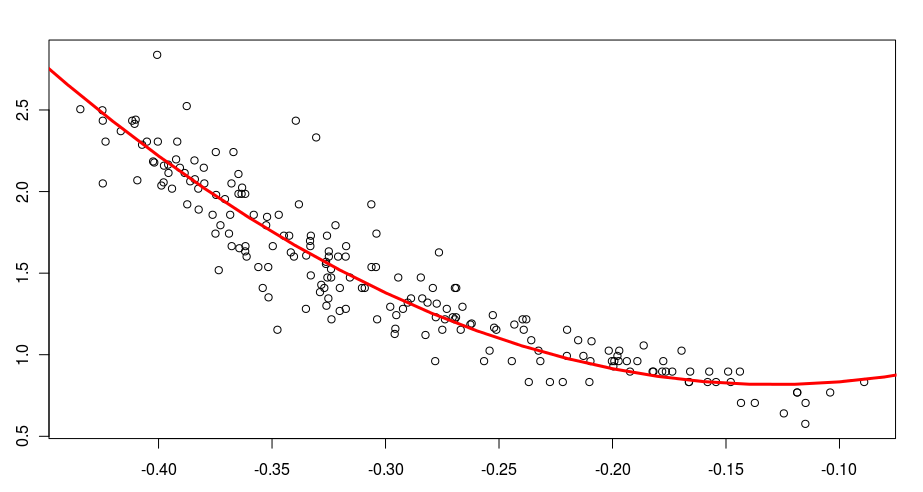

We see that all the tested methods provide reasonable results on most data sets. The Lasso is very competitive, especially in the nonasymptotic framework. The estimation procedure offers outcomes which are similar to the ones of , with a slight advantage for the latter method however. Altogether, and provide the best performance in terms of prediction error in 6 out of 9 experiments. Besides, when it is not the best, the method is close to the best one, as for example in SLUMP-3 and WINE-RED. As an illustrative example, the plot of the resulting fit of our procedure to the data set AUTO-MPG is shown in Figure 1.

Clearly, all data sets under study have a dimension which is small compared to . To correct this situation, we ran the same series of experiments by adding some additional irrelevant dimensions to the data. Specifically, the observations were embedded into a space of dimension by letting the new fake coordinates follow independent uniform random variables. The results are shown in Table 4. In this nonasymptotic framework, the method —which is not designed for sparsity—collapses, whereas takes a clear advantage over its competitors. In fact, it provides the best results in 3 out of 9 experiments (AUTO-MPG, CONCRETE and HOUSING). Besides, when it is not the best, the method is very close to the best one, as for example in SLUMP-3 and WINE-RED.

| Augmented data set | |||||

|---|---|---|---|---|---|

| AIR QUALITY | median | 0.172 | 0.272 | 0.164 | 0.281 |

| mean | 0.244 | 0.291 | 0.163 | 0.291 | |

| s.d. | 0.163 | 0.116 | 0.038 | 0.046 | |

| AUTO-MPG | median | 0.043 | 0.062 | 0.085 | 0.202 |

| mean | 0.044 | 0.072 | 0.086 | 0.203 | |

| s.d. | 0.009 | 0.018 | 0.008 | 0.014 | |

| CONCRETE | median | 0.087 | 0.093 | 0.113 | 0.245 |

| mean | 0.087 | 0.094 | 0.112 | 0.094 | |

| s.d. | 0.007 | 0.008 | 0.005 | 0.009 | |

| HOUSING | median | 0.071 | 0.199 | 0.092 | 0.226 |

| mean | 0.075 | 0.181 | 0.095 | 0.227 | |

| s.d. | 0.023 | 0.084 | 0.013 | 0.018 | |

| SLUMP-1 | median | 0.270 | 0.426 | 0.276 | 0.271 |

| mean | 0.290 | 0.409 | 0.274 | 0.262 | |

| s.d. | 0.101 | 0.079 | 0.055 | 0.042 | |

| SLUMP-2 | median | 0.276 | 0.332 | 0.195 | 0.253 |

| mean | 0.285 | 0.349 | 0.198 | 0.254 | |

| s.d. | 0.075 | 0.063 | 0.043 | 0.034 | |

| SLUMP-3 | median | 0.079 | 0.371 | 0.061 | 0.372 |

| mean | 0.082 | 0.361 | 0.058 | 0.279 | |

| s.d. | 0.025 | 0.079 | 0.013 | 0.031 | |

| WINE-RED | median | 0.178 | 0.222 | 0.172 | 0.245 |

| mean | 0.176 | 0.226 | 0.174 | 0.246 | |

| s.d. | 0.085 | 0.033 | 0.006 | 0.029 | |

| WINE-WHITE | median | 0.199 | 0.239 | 0.187 | 0.252 |

| mean | 0.204 | 0.256 | 0.188 | 0.260 | |

| s.d. | 0.091 | 0.041 | 0.005 | 0.019 |

Thus, as a general conclusion to this experimental section, we may say that our PAC-Bayesian oriented procedure has an excellent predictive ability, even in nonasymptotic/high-dimensional situations. It is fast, robust, and exhibits performance at the level of the gold standard Lasso.

4 Proofs

4.1 Preliminary results

Throughout this section, we let be the prior probability measure on equipped with its canonical Borel -field. Recall that and that, for each , we have .

Besides, since almost surely, we note once and for all that for all ,

(Pythagora’s theorem). We start with four technical lemmas. Lemma 4.1 is a version of Bernstein’s inequality, whose proof can be found in Massart [31, Chapter 2, inequality (2.21)]. Lemma 4.2 is a classical result, whose proof can be found, for example, in Catoni [13, page 4]. For a random variable , the notation means the positive part of .

Lemma 4.1

Let be independent real-valued random variables. Assume that there exist two positive constants and such that, for all integers ,

Then, for any ,

Given a measurable space and two probability measures and on , we denote by the Kullback-Leibler divergence of with respect to , defined by

(Notation means “ is absolutely continuous with respect to ”.)

Lemma 4.2

Let be a measurable space. For any probability measure on and any measurable function such that , we have

| (4.1) |

where the supremum is taken over all probability measures on and, by convention, . Moreover, as soon as is bounded from above on the support of , the supremum with respect to on the right-hand side of (4.1) is reached for the Gibbs distribution given by

Lemma 4.3

Assume that Assumption N holds. Set and take

Then, for all and any data-dependent probability measure absolutely continuous with respect to we have, with probability at least ,

where the pair is distributed according to .

Proof of Lemma 4.3. Fix and . The proof starts with an application of Lemma 4.1 to the random variables

Note that these random variables are independent, identically distributed, and that

Thus, by Assumption N,

where we set

More generally, for all integers ,

In the last inequality, we used the fact that together with

Therefore, by Assumption N,

with .

Thus, for any inverse temperature parameter , taking , we may write by Lemma 4.1

Therefore, using the definition of , we obtain

Next, we use a standard PAC-Bayesian approach (Catoni [12, 13], Audibert [4] and Alquier [1]). Let us remind the reader that is a prior probability measure on the set . We have

and consequently, using Fubini’s theorem,

Therefore, for any data-dependent posterior probability measure absolutely continuous with respect to , adopting the convention ,

Recalling that stands for the distribution of the sample , the latter inequality can be more conveniently written as

Thus, using the elementary inequality we obtain, with probability at most ,

where the probability is evaluated with respect to the distribution of the data and the conditional probability measure . Put differently, letting

we have, with probability at least ,

This concludes the proof of Lemma 4.3.

Lemma 4.4

Under the conditions of Lemma 4.3 we have, with probability at least ,

Proof of Lemma 4.4. The beginning of the proof is similar to the one of Lemma 4.3. More precisely, we apply Lemma 4.1 with and obtain, for any inverse temperature parameter ,

Thus, using the definition of ,

Integrating with respect to leads to

whence, by Fubini’s theorem,

Thus, for any data-dependent posterior probability measure absolutely continuous with respect to ,

Therefore, by Jensen’s inequality,

Consequently, by the elementary inequality , we obtain, with probability at most ,

Equivalently, with probability at least ,

4.2 Proof of Theorem 2.1

The proof starts with an application of Lemma 4.3 with (the Gibbs distribution) as posterior distribution. More precisely, we know that, with probability larger than ,

where the probability is evaluated with respect to the distribution of the data and the conditional probability measure . Observe that

Consequently, with probability at least ,

Next, using Lemma 4.2 we deduce that, with probability at least ,

where the infimum is taken over all probability measures on . In particular, letting be the set of all probability measures on , we have, with probability at least ,

Next, observe that, for ,

| (4.2) |

Therefore, with probability at least ,

| (4.5) | |||

| (4.6) |

By Lemma 4.4 and inequality (4.2), for any data-dependent distribution , with probability at least ,

| (4.7) |

Thus, combining inequalities (4.6) and (4.7), we may write, with probability at least ,

| (4.10) | |||

| (4.11) |

For any subset of , any positive integer and any , let the probability measure be defined by

with

and

where, for , we put

With this notation, inequality (4.11) leads to

| (4.14) | |||

| (4.15) |

To finish the proof, we have to control the different terms in (4.15). Note first that

and, consequently,

| (4.16) |

Next,

By technical Lemma 4.5, we know that

Similarly, by technical Lemma 4.6,

Putting all the pieces together, we are led to

| (4.17) |

Finally, it remains to control the term

To this aim, we write

Computation of C

By Fubini’s theorem,

By the triangle inequality, for and , it holds

Since , we have , so that as soon as . This shows that the set

is contained in the support of . In particular, this implies that is centered at and, consequently,

This proves that .

Control of A

Clearly,

Control of B

We have

Control of E

Write

Control of D

Finally,

The inequality

leads to

Consequently,

and therefore

Thus, taking and putting all the pieces together, we obtain

where is a positive constant, function of , and . Combining this inequality with (4.15)-(4.17) yields, with probability larger than ,

Choosing finally

we obtain that there exists a positive constant , function of , , and such that, with probability at least ,

This concludes the proof of Theorem 2.1.

4.3 Proof of Corollary 2.1

We already know, by Theorem 2.1, that with probability at least ,

By definition, for all ,

In particular, if is such that , then

| (4.20) | ||||

| (4.21) |

Observe that, for any ,

Since , we may write

and apply (4.20) with

In order to do so, we just need to check that , that is

But, by the Cauchy-Schwarz inequality,

Thus,

Next, with this choice of ,

for some positive constant depending only on and (see for instance Tsybakov [42]). Therefore, inequality (4.20) leads to

| (4.22) |

Letting be the ceiling function and choosing in (4.22) concludes the proof.

4.4 Some technical lemmas

Lemma 4.5

For any subset of , any positive integer and any , let the probability measure be defined by

Then

Proof. For simplicity, we assume that . Up to a permutation of the coordinates, the proof remains valid for any subset of . Still for simplicity, we let denote . By a symmetry argument, it can be assumed that has nonnegative coordinates—this just means that is arbitrarily fixed in one of the faces of . We denote by this face and note that

Finally, without loss of generality, we suppose that the largest coordinate in is , and let be the uniform probability measure on , defined by

Set , and let

Note that . Therefore, for each , all the coordinates of are nonnegative. Obviously , so that, for all , . Denoting by the convex hull of the set , we also have . Next, observe that , which implies .

Clearly,

Thus,

Observe that is homothetic to , by a factor of . This means that

Consequently, we obtain

Lemma 4.6

For any subset of , any positive integer and any , let the probability measure be defined by

where, for , we put

Then

Proof. Observe that

Now,

where It easily follows, using the fact that the support of is included in the set , that

Note that

where the second equality is true since is (the image of) the uniform probability measure on . This implies

By the triangle inequality,

Since , we have , so that

as soon as . We conclude that

5 Annex: Description of the MCMC algorithm

This annex is intended to make thoroughly clear the specification of the proposal conditional densities and introduced in Section 3.

5.1 Notation

To provide explicit formulas for the conditional densities and we first set

where it is recalled that denotes the (non-normalized) trigonometric system. We let (respectively, ) be the set of nonzero coordinates of the vector (respectively, ), and denote finally by (respectively, ) the vector of dimension (respectively, ) which contains the nonzero coordinates of (respectively, ). Recall that all densities are defined with respect to the prior , which is made explicit in Subsection 2.2.

For a generic , given and , we let the density with respect to be defined by

where the are the empirical least square coefficients given by

In the experiments, we fixed . Note that simulating with respect to is an easy task, since one just needs to compute a least square estimate and then draw from a truncated Gaussian distribution.

5.2 Description of

We take

Roughly, the idea is that tries to remove one component in , keeps the same number of components, whereas adds one component. The density takes the form

The density is the density of when and

where and the are independent random variables uniformly distributed in . Throughout, the value of was fixed at . It is noteworthy that when we change the parameter from to , then we also change the function from to . Thus, with this procedure, the link function is more “adapted” to and the subsequent move is more likely to be accepted in the Hastings-Metropolis algorithm.

In the case where we are to remove one component, is given by

where is just obtained from by setting the -th component to 0 and by renormalizing the parameter in order to have . We set

The idea is that smaller components are more likely to be removed than larger ones. Finally, the density takes the form

We set

where denotes the -th component of . In words, the idea is that a new nonzero coordinate in is more likely to be interesting in the model if the corresponding feature is correlated with the current residual.

5.3 Description of

In the same spirit, we let the conditional density be defined by

We choose

and

With this choice, , which means that the proposal density tries to add one coefficient in the expansion of , while leaving unchanged. Finally

and the proposal tries to remove one coefficient in .

Acknowledgments.

The authors thank three referees for valuable comments and insightful suggestions, which lead to a substantial improvement of the paper. They also thank John O’Quigley for his careful reading of the article.

References

- [1] P. Alquier. PAC-Bayesian bounds for randomized empirical risk minimizers. Mathematical Methods of Statistics, 17:279–304, 2008.

- [2] P. Alquier and K. Lounici. PAC-Bayesian bounds for sparse regression estimation with exponential weights. Electronic Journal of Statistics, 5:127–145, 2011.

- [3] A. Antoniadis, G. Grégoire, and I.W. McKeague. Bayesian estimation in single-index models. Statistica Sinica, 14:1147–1164, 2004.

- [4] J.-Y. Audibert. Aggregated estimators and empirical complexity for least square regression. Annales de l’Institut Henri Poincaré: Probability and Statistics, 40:685–736, 2004.

- [5] J.-Y. Audibert and O. Catoni. Robust linear least squares regression. The Annals of Statistics, in press, 2011.

- [6] R.E. Bellman. Adaptive Control Processes: A Guided Tour. Princeton University Press, 1961.

- [7] P.J. Bickel, Y. Ritov, and A.B. Tsybakov. Simultaneous analysis of Lasso and Dantzig selector. The Annals of Statistics, 37:1705–1732, 2009.

- [8] A.M. Bruckstein, D.L. Donoho, and M. Elad. From sparse solutions of systems of equations to sparse modeling of signals and images. SIAM Review, 51:34–81, 2009.

- [9] P. Bühlmann and S. van de Geer. Statistics for High-Dimensional Data. Springer, New York, 2011.

- [10] F. Bunea, A. Tsybakov, and M. Wegkamp. Sparsity oracle inequalities for the Lasso. Electronic Journal of Statistics, 1:169–194, 2007.

- [11] E.J. Candès and T. Tao. The Dantzig selector: Statistical estimation when is much larger than . The Annals of Statistics, 35:2313–2351, 2005.

- [12] O. Catoni. Statistical Learning Theory and Stochastic Optimization. Springer, 2004.

- [13] O. Catoni. PAC-Bayesian Supervised Classification: The Thermodynamics of Statistical Learning, volume 56 of Lecture Notes-Monograph Series. IMS, 2007.

- [14] J.M. Chambers, W.S. Cleveland, B. Kleiner, and P.A. Tukey. Graphical Methods for Data Analysis. Wadsworth & Brooks, Belmont, 1983.

- [15] X. Chen, C. Zou, and R.D. Cook. Coordinate-independent sparse sufficient dimension reduction and variable selection. The Annals of Statistics, 38:3696–3723, 2010.

- [16] A. Cohen, I. Daubechies, R. DeVore, G. Kerkyacharian, and D. Picard. Capturing ridge functions in high dimension from point queries. Constructive Approximation, in press, 2011.

- [17] P. Cortez, A. Cerdeira, F. Almeida, T. Matos, and J. Reis. Modeling wine preferences by data mining from physicochemical properties. Decision Support Systems, 47:547–553, 2009.

- [18] A.S. Dalalyan, A. Juditsky, and V. Spokoiny. A new algorithm for estimating the effective dimension-reduction subspace. Journal of Machine Learning Research, 9:1647–1678, 2008.

- [19] A.S. Dalalyan and A.B. Tsybakov. Aggregation by exponential weighting, sharp PAC-Bayesian bounds and sparsity. Machine Learning, 72:39–61, 2008.

- [20] A.S. Dalalyan and A.B. Tsybakov. Sparse regression learning by aggregation and Langevin Monte-Carlo. Journal of Computer and System Sciences, in press, 2011.

- [21] M. Delecroix, M. Hristache, and V. Patilea. On semiparametric -estimation in single-index regression. Journal of Statistical Planning and Inference, 136:730–769, 2006.

- [22] S. Gaïffas and G. Lecué. Optimal rates and adaptation in the single-index model using aggregation. Electronic Journal of Statistics, 1:538–573, 2007.

- [23] P.J. Green. Reversible jump Markov chain Monte Carlo computation and Bayesian model determination. Biometrika, 82:711–732, 1995.

- [24] L. Györfi, M. Kohler, A. Krzyżak, and H. Walk. A Distribution-Free Theory of Nonparametric Regression. Springer, New York, 2002.

- [25] W. Härdle, P. Hall, and H. Ichimura. Optimal smoothing in single-index models. The Annals of Statistics, 21:157–178, 1993.

- [26] D. Jr. Harrison and D.L. Rubinfeld. Hedonic housing prices and the demand for clean air. Journal of Environmental Economics and Management, 5:81–102, 1978.

- [27] J.L. Horowitz. Semiparametric Methods in Econometrics. Springer, 1998.

- [28] H. Ichimura. Semiparametric least squares (SLS) and weighted SLS estimation of single-index models. Journal of Econometrics, 58:71–120, 1993.

- [29] O. Lopez. Single-index regression models with right-censored responses. Journal of Statistical Planning and Inference, 139:1082–1097, 2009.

- [30] J.-M. Marin and C. Robert. Bayesian Core: A Practical Approach to Computational Bayesian Analysis. Springer, New York, 2007.

- [31] P. Massart. Concentration Inequalities and Model Selection. Springer, Berlin, 2007.

- [32] D.A. McAllester. Some PAC-Bayesian theorems. In Proceedings of the Eleventh Annual Conference on Computational Learning Theory, pages 230–234, New York, 1998. ACM.

- [33] P. McCullagh and J.A. Nelder. Generalized Linear Models. Chapman and Hall, 1983.

- [34] E.A. Nadaraya. On estimating regression. Theory of Probability and its Applications, 9:141–142, 1964.

- [35] E.A. Nadaraya. Remarks on nonparametric estimates for density functions and regression curves. Theory of Probability and its Applications, 15:134–137, 1970.

- [36] J.R. Quinlan. Combining instance-based and model-based learning. In Proceedings of the Tenth International Conference on Machine Learning, pages 236–243, Amherst, 1993. Morgan Kaufmann.

- [37] R Development Core Team. R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, 2008.

- [38] Y. Seldin, N. Cesa-Bianchi, F. Laviolette, P. Auer, J. Shawe-Taylor, and J. Peters. PAC-Bayesian analysis of the exploration-exploitation trade-off. arXiv:1105.4585, 2011.

- [39] J. Shawe-Taylor and R. Williamson. A PAC analysis of a Bayes estimator. In Proceedings of the Tenth Annual Conference on Computational Learning Theory, pages 2–9, New York, 1997. ACM.

- [40] C.J. Stone. Optimal global rates of convergence for nonparametric regression. The Annals of Statistics, 10:1040–1053, 1982.

- [41] R. Tibshirani. Regression shrinkage and selection via the Lasso. Journal of the Royal Statistical Society, Series B, 58:267–288, 1996.

- [42] A.B. Tsybakov. Introduction to Nonparametric Estimation. Springer, 2009.

- [43] L.J. van’t Veer, H. Dai, M.J. van de Vijver, Y.D. He, A.A.M. Hart, M. Mao, H.L. Peterse, K. van der Kooy, M.J. Marton, A.T. Witteveen, G.J. Schreiber, R.M. Kerkhoven, C. Roberts, P.S. Linsley, R. Bernards, and S.H. Friend. Gene expression profiling predicts clinical outcome of breast cancer. Nature, 415:530–536, 2002.

- [44] H.B. Wang. Bayesian estimation and variable selection for single index models. Computational Statistics and Data Analysis, 53:2617–2627, 2009.

- [45] G.S. Watson. Smooth regression analysis. Sankhyā Series A, 26:359–372, 1964.

- [46] I.-C. Yeh. Modeling of strength of high-performance concrete using artificial neural networks. Cement and Concrete Research, 28:1797–1808, 1998.

- [47] I.-C. Yeh. Modeling slump flow of concrete using second-order regressions and artificial neural networks. Cement and Concrete Composites, 29:474–480, 2007.