118 \copyrightinfo2011

Lubin G. Vulkov

Sensitivity analysis of the early exercise

boundary for American style of Asian options

Abstract.

In this paper we analyze American style of floating strike Asian call options belonging to the class of financial derivatives whose payoff diagram depends not only on the underlying asset price but also on the path average of underlying asset prices over some predetermined time interval. The mathematical model for the option price leads to a free boundary problem for a parabolic partial differential equation. Applying fixed domain transformation and transformation of variables we develop an efficient numerical algorithm based on a solution to a non-local parabolic partial differential equation for the transformed variable representing the synthesized portfolio. For various types of averaging methods we investigate the dependence of the early exercise boundary on model parameters.

Key words and phrases:

Option pricing, American-style Asian options, early exercise boundary, fixed domain transformation2000 Mathematics Subject Classification:

35K15, 35K55, 90A09, 91B281. Introduction

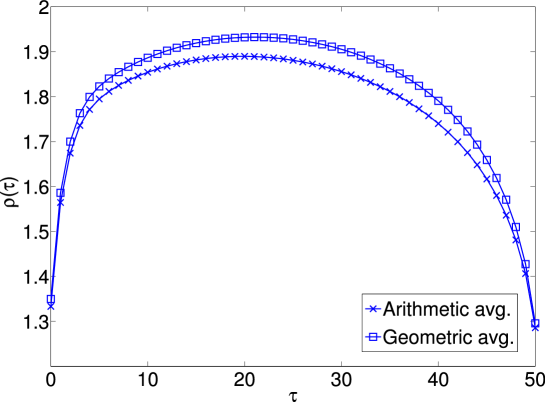

Asian path dependent options belong to the class of financial derivatives whose payoff diagram depends not only on the underlying asset price but also on the path average of underlying asset prices over some predetermined time interval. Such path dependent options can be often found at commodities markets such as oil, grain trade, etc. At expiration, the payoff diagram of such options is less sensitive with respect to sudden changes of the underlying asset value. Therefore a holder of an Asian option can effectively hedge the risk arising from a sudden price jump close to expiry. Typically, the payoff diagram of an Asian path dependent option depends on either arithmetic or geometric average of the spot price of the underlying asset. Such contingent claims can be used as a financial instrument for hedging highly volatile assets or goods. We refer the reader to references [17, 8, 18, 7, 4, 3, 20, 12, 10, 19, 13] discussing qualitative and quantitative aspects of pricing Asian path dependent options.

In this paper, we focus on a special subclass of Asian options. Namely, we will investigate the so-called average strike Asian call options. At the time of expiry , a holder of such an option contract has the right (but not obligation) to purchase the underlying asset for the strike price given as the path average of underlying asset prices. This means that the terminal payoff diagram for such an option has the form: , where is the spot price of the underlying asset, is the path average of the asset prices over the time interval and is the time of maturity.

Concerning the method how the path averaged asset price is calculated at a time , we can distinguish the following methods of averaging of the path :

-

•

arithmetic averaged options, where the average is given by

(1) -

•

weighted arithmetic averaged options, with the average is given by

(2) and is an exponential weight function with the averaging factor ,

-

•

geometric averaged options, where the average is given by

(3)

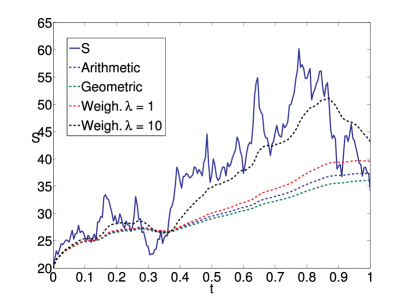

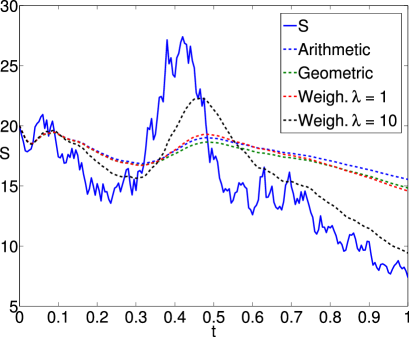

In Figure 1 we plot two different sample paths of the underlying asset price (solid lines) and their arithmetic, geometric and weighted arithmetic path averages. In the case of weighted arithmetic averaging with a weight factor we can observe that the average approaches the sample path when . On the other hand, the weighted arithmetic average approaches the arithmetic average when .

In this paper we are concerned with American style of Asian floating strike options giving its holder the right to exercise it anytime before the obligatory expiration time . Our main purpose is to provide a numerical quantitative analysis of the early exercise boundary position for a floating strike Asian call option by means of a solution to the transformed nonlocal parabolic partial differential equation derived by Bokes and Ševčovič [1, 16] for the case of arithmetic averaging. The main goal of this paper is to analyze the dependence and sensitivity of the early exercise boundary with respect to various model parameters.

The paper is organized as follows. In the next section, we recall the partial differential equation for pricing floating strike Asian options. We also recall the method of dimension reduction of the equation. Next we discuss American style of Asian options and the early exercise boundary. A key tool for derivation of our numerical algorithm is transformation of the reduced equation to a fixed spatial domain. The resulting equation is a nonlocal parabolic PDE with an algebraic constraint between its solution and the free boundary position. In Section 3 we employ the method of finite difference approximation. We discretize our nonlocal equation in space and time. To this end we make use of multiplicative operator splitting method. Results of numerical computations are presented in Section 4. We discuss the impact of the averaging method on the form of the early exercise boundary. We furthermore analyze the dependence of the early exercise boundary with respect to various model parameters. We furthermore make a comparison of its position for different averaging methods.

2. Partial differential equation for pricing average strike Asian options

In this section we recall the parabolic partial differential equation for pricing Asian options. Derivation of the pricing equation is based on standard assumptions made on stochastic behavior of the underlying asset price . Henceforth, we will suppose that follows a geometric Brownian motion, that is,

where is the risk-free interest rate, is the dividend yield on the asset, is the standard Wiener process. Although the aforementioned assumption made on has obvious deficiencies like constancy of the volatility or normality of the distribution of asset returns, we adopt this assumption throughout the paper.

Since the payoff diagram depends on both the spot asset price and the path average at so does the price of an Asian option for . It means is a function depending not only on the underlying asset spot price and time but also on the average of the underlying asset price over the interval , i.e. . In order to derive the pricing equation for an option price one has to calculate its differential over a time interval with an infinitesimal length . The price as well as its path average are stochastic variables and so does the option price . To calculate the differential we have to find a relationship between the differential of the path average and the time . Taking a differential of (1) we obtain the expression:

for the case of arithmetic average . On the other hand, for the case of geometric averaging we obtain from (3):

Similarly, for the exponentially weighted arithmetic average with the weight parameter we obtain

In all averaging methods under consideration, we can conclude the following relation between the differential as a function of the stochastic variable and the differential .

| (4) |

where the function is given by

| (5) |

It means that the differential is a stochastic variable with the leading order term of the order (see Kwok [12], Dai [3], Ševčovič[16]). Applying Itō’s lemma (cf. Kwok [12]) for the function and taking into account (4) we conclude the stochastic differential equation for the option price in the form:

Under the assumption of perfect replicability of the market and nonexistence of arbitrage opportunities (cf. Kwok [12]), it can be shown that the risk neutral price of an Asian call option is a solution to the parabolic partial differential equation

| (6) |

satisfying the payoff diagram corresponding to the averaged strike Asian option, i.e.

where .

It is also well known that the PDE for average strike Asian options allows for a dimension reduction by introducing a new state variable and the function defined as follows:

| (7) |

where . After straightforward computations we obtain a parabolic PDE for the function :

| (8) |

where . A solution satisfies the initial condition:

A solution to the aforementioned equation (8) is defined on the fixed spatial interval . The function given by corresponds to the price of an Asian floating strike path dependent option for the so-called European style of contracts for which the option expires exactly at the time .

2.1. American-style of Asian call options

In this paper we are concerned with American style of Asian options (cf. [7, 3, 12]). In contrast to European style of options, American style options can be exercised at any time until the obligatory maturity time . The holder of such an option has the right to exercise it or to keep it depending on the spot price of the underlying at time and its history prior the time . The boundary between “continuation” and “stopping” regions plays an important role in pricing American-style of options. It can be described by the function , where is the so-called early exercise boundary (cf. [8, 5, 6, 9, 2, 12, 11, 14, 15]). According to Kwok [12], the set

is the exercise region. For the case of a call option, there exists a early exercise boundary function such that

It means that , where is the path average of underlying asset prices . We can search the early exercise boundary function in a separated form

For more details we refer the reader to Dai and Kwok [3] or Bokes and Ševčovič [1, 16]. The corresponding spatial domain for the reduced function satisfying (8) is therefore given by

where . From the continuity of at we conclude that

| (9) |

It follows from the payoff diagram that

| (10) |

for and . In terms of the new state variable , we conclude the following boundary conditions for the function :

| (11) |

for . The initial condition for is

| (12) |

Equation (8) and boundary conditions (11) represent a free boundary problem, because the spatial domain depends on the unknown free boundary function which is a part of a solution of the problem.

2.2. Fixed domain transformation

Following ideas of transformation methodology developed by Ševčovič in [16] (see also [1]) we introduce a new state variable and the transformed function defined as:

| (13) |

After straightforward calculations we obtain that is a solution to the following linear parabolic equation

| (14) |

where

For details of derivation of (14) we refer the reader to [1, 16]. The initial condition for the solution is:

| (15) |

The limiting value of the early exercise boundary at expiry (i.e. ) for the continuous arithmetic average type of an Asian option has been derived by Dai and Kwok [3]. For the geometric average it has been discovered by Wu in [18] (see also Detemple [4, p. 69]). For arithmetic weighted averaged floating strike call option it has been derived by Bokes and Ševčovič in [1]. The value is given by:

| (16) |

In the case of geometric averaging, the auxiliary number entering the expression of is a unique solution to the transcendental equation:

| (17) |

Next we recall the boundary conditions for a solution . Taking into account equations (11) we end up with the Dirichlet boundary conditions:

| (18) |

Since and we obtain at . In the limit , assuming the continuity of up to the boundary , we obtain

Passing to the limit in equation (8) we obtain the following algebraic constraint between and the solution :

Therefore we obtain the following algebraic constraint equation between the free boundary position and the partial derivative :

| (19) |

Notice, that this expression contains term and therefore this is not suitable for numerical scheme, because the whole solution is sensitive of this term. Bokes and Ševčovič [1] suggested an equivalent form of (19). They integrated equation (14) with respect to . Taking into account boundary conditions for and and using equality (19) they derived an ODE replacing the algebraic constraint between the free boundary position and of the solution . It has the form:

Remark 1.

Denote by . Then provided that . Since the function is increasing we have and consequently . Similarly, for any we have . In summary, we derived the following inequalities for the initial values of the early exercise boundary

| (21) |

Clearly, in the case .

Remark 2.

The solution can be easily calculated from the solution and the free boundary position . With regard to (13) we obtain:

Taking into account the boundary condition at and integrating the above equation from to , we obtain

Then the option price can be calculated from equality .

3. Numerical algorithm

In this section, we make use of the numerical algorithm proposed by Bokes and Ševčovič in [1, 16] for calculating of the early exercise boundary position . We notice that the original algorithm was derived for arithmetic averaged floating strike Asian call option. In this paper, we generalize it for the case of geometric and exponentially weighted averaged floating strike options.

The algorithm is based on a finite difference discretization in space and time variables. We restrict the spatial domain to a finite interval , where is sufficiently large. For practical purposes, it is sufficient to take . Let is a time discretization step and is a spatial discretization step. We denote by time discretization of and , where . By we denote full space-time approximation of the value . Then the Euler backward in time finite difference approximation of (14) reads as follows:

where and . We prescribe Dirichlet boundary conditions at and for the function . As for the initial condition, we use the vector where . Following [1], we make use of the operator splitting method to the above problem by introducing an auxiliary intermediate step that splits the problem into two parts:

-

•

Convective part

(22) -

•

Diffusive part

A solution to equation (22) can be approximated by the explicit solution to the transport equation

for and satisfying the initial condition and the boundary condition . After some computations (for further details see e.g. Bokes and Ševčovič [1]) we end up with the following solution:

| (24) |

In order to derive full space–time discretization scheme we make use of the central finite difference approximation of equation (• ‣ 3). We obtain

Hence the vector is a solution of a tridiagonal system of linear equations

| (25) |

for , where

Boundary conditions for are given by: , for . The initial condition for is given by equations (15) and (16). In order to determine the free boundary position we take equation (2.2) into account. Applying the forward finite difference approximation we obtain

As for the approximation of the integral , we use the trapezoid quadrature method. If we rewrite equations into the operator form then we obtain the following system of nonlinear algebraic equation for the unknown vector and the free boundary position at the time :

| (27) |

where is a solution of the transport equation given by (24), is a tridiagonal matrix given by (25) and is right side of equation (3). System of equations (27) can be effectively solved by means of successive iterations procedure. For , we set and . Then -th approximation of and is a solution of following system:

| (28) | |||||

| (29) | |||||

| (30) |

We repeat the above iteration procedure for until the prescribed tolerance is achieved (see Table 2).

Input model parameters: Input numerical parameters: Initialization: for to : for to : Solve: for if () break endif end end

4. Numerical results

The aim of this section is to present various computational examples of calculation of the early exercise boundary position for varying model parameters and averaging methods. In all examples discussed in this section we use the following numerical parameters: , , , , . In graphical plots we display the position of the early exercise only.

4.1. Free boundary for floating strike call options

4.1.1. Arithmetic averaged floating strike call options

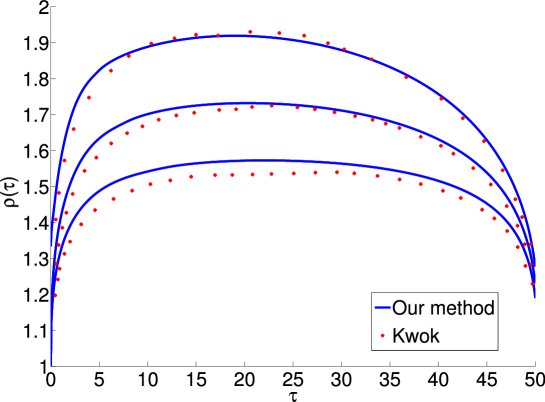

In Figure 3 we compare the free boundary position for various interest rates . Other model parameters are: . We also compare the free boundary position computed by the algorithm described in Section 3 (blue line) and computational results obtained by Dai and Kwok in [3] (red dots).

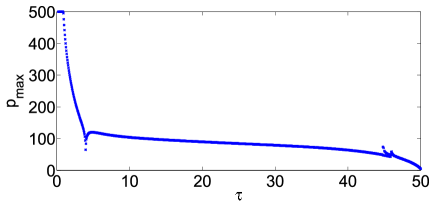

In Figure 4 we show the number of maximal inner iteration steps needed for achievement of the desired tolerance . We can observe that the algorithm requires considerably more inner iteration steps for small times for which the time derivative of is large. As for the model parameters we chose: .

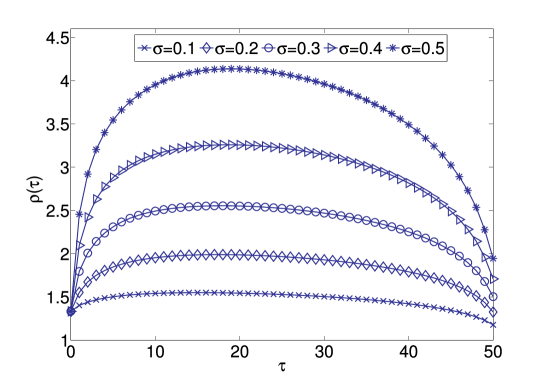

In Figure 5 we plot for different values of the volatility parameter . Other parameters are: . It is worthwile noting that, for , the underlying stochastic process for becomes deterministic. The option price at the time can be therefore calculated as: . Its arithmetic average is given by . In the case of we have for all . Therefore the corresponding option price is equal to zero because it is not worth to exercise it for any . In the case , both . Hence . Finally, in the case we obtain , for all . Since we are dealing with American style of options we exercise the option at the time . Denote by . Then . Now it is easy to verify that

Hence is an increasing function. As both and we conclude that .

In the case of an arithmetic averaged Asian call option we obtain from (19) the following explicit expression for the free boundary position:

| (31) |

4.1.2. Geometric averaged floating strike call option

In Figure 6 we compare the free boundary position computed for the case of arithmetic and geometric averaging. Model parameters were chosen as: . Notice that for all .

4.1.3. Weighted arithmetic averaged floating strike call option

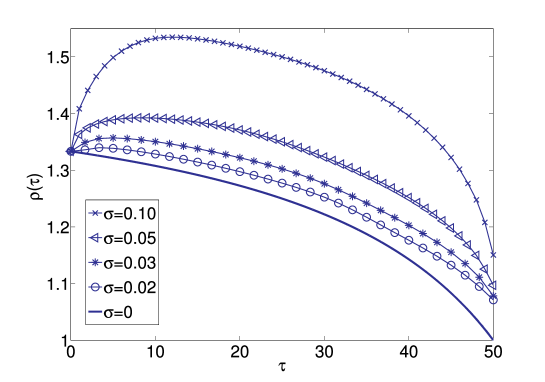

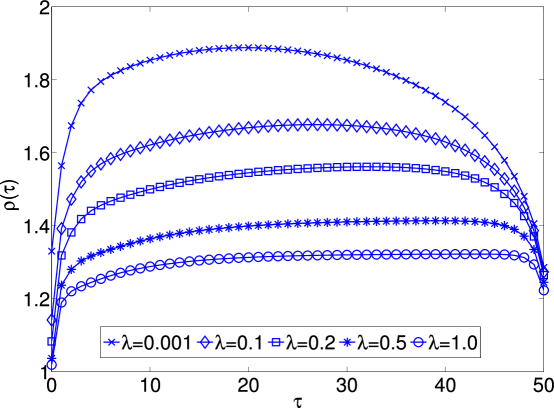

In Figure 7 we plot the free boundary position for various weight parameters .

It is easy to verify that . As a consequence we deduce that the option price is equal to zero. This is also reason for the limit . In what follows, we will estimate rate of convergence of using the so-called experimental order of convergence. Assuming that

as , we can approximate the order parameter as follows:

| (32) |

where . The results shown in Table 1 indicate . It means that it might be reasonable to conjecture that

| 0.2 | 0.561828 | – |

| 0.5 | 0.413783 | 0.333 |

| 1.0 | 0.320136 | 0.370 |

| 2.0 | 0.247010 | 0.374 |

| 3.0 | 0.212705 | 0.368 |

| 4.0 | 0.191862 | 0.358 |

| 5.0 | 0.177658 | 0.344 |

| 10.0 | 0.147227 | 0.271 |

| 20.0 | 0.113350 | 0.377 |

4.2. Comparison of the early exercise boundary position for various averaging methods.

In Remark 1 we pointed out that if and in the case , where are the free boundary position for arithmetic, geometric and weighted arithmetic averaged Asian call options, respectively (see (21)). This relation has been rigorously derived for only. However, it follows from results depicted in Figures 6 and 7 that it might be plausible to state the following conjecture on the comparison of early exercise boundaries for various averaging methods:

Conjecture 1

Let be the free boundary positions for arithmetic, geometric and exponentially weighted arithmetic averaged Asian call options. Then for any it holds:

4.3. Initial early exercise boundary position

In this section, we investigate the initial early exercise boundary position at . It corresponds to the value at .

Let us denote by the free boundary position as a function of and remaining model parameters, i.e. . Using obvious scaling properties of the governing equation (14) and the algebraic constraint (19) we can conclude that for arithmetic, geometric or weighted arithmetic average the following scaling property holds true:

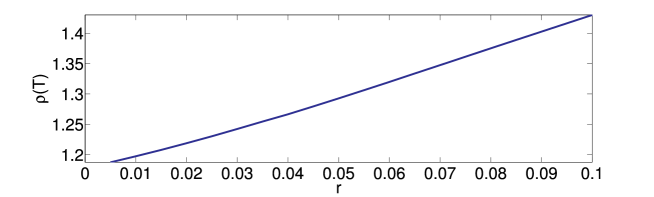

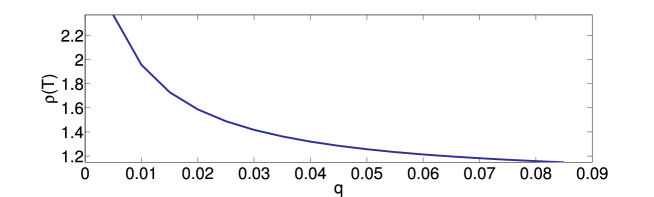

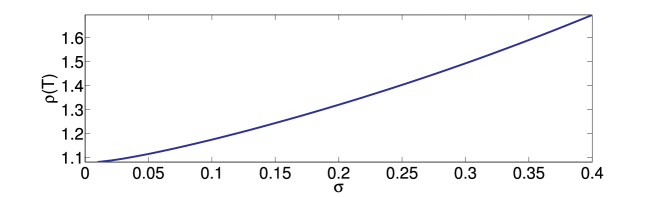

With regard to the previous argument, it is therefore sufficient to study dependence of on for arbitrary but fixed value of the parameter . In Figure 8 (top) we plot dependence of on for . In Figure 8 (middle) we plot dependence of on for . Finally, in Figure 8 (bottom) we plot dependence of on for . In all case we chose .

We furthermore proposed and consequently estimated the analytical formula for dependence of on . With respect to the scaling property we can fix . Among various nonlinear estimators for the value on the best estimation results we achieved with the function

with with where as an error indicator we chose the least square minimizer:

where and parameter samples were generated from random vectors. We denoted by the numerically computed free boundary position at computed for the model parameters and time horizon .

Acknowledgments

The research was supported by ERDF-017/2009/4.1/OPVaV-CESIUK project and bilateral Slovak–Bulgarian project APVV SK-BG-0034-08.

References

- [1] T. Bokes and D. Ševčovič, Early Exercise Boundary for American Type of Floating Strike Asian Option and Its Numerical Approximation, Applied Mathematical Finance, 2011.

- [2] J. Chadam, Free Boundary Problems in Mathematical Finance, in Progress in industrial mathematics at ECMI 2006, vol. 12 of Math. Ind., p. 655–665, Springer, Berlin, 2008.

- [3] M. Dai and Y. K. Kwok, Characterization of Optimal Stopping Regions of American Asian and Lookback Options, Math. Finance 16 (1) (2006) 63–82.

- [4] J. Detemple, American-Style Derivatives: Valuation and Computation, Chapman and Hall/CRC, 2006.

- [5] R. Geske and H. E. Johnson, The American Put Option Valued Analytically, J. Finance, 39 (1984) 1511–1524.

- [6] R. Geske and R. Roll, On Valuing American Call Options with the Black–Scholes European Formula, J. Finance, 89 (1984) 443–455.

- [7] A. T. Hansen and P. L. Jørgensen, Analytical Valuation of American-style Asian Options, Management Science, 46 (2000) 1116–1136.

- [8] J. C. Hull, Options, Futures and Other Derivative Securities, Prentice Hall, third ed., 1997.

- [9] I. Karatzas, On the Pricing American Options, Appl. Math. Optim., 17 (1988) 37–60.

- [10] B. C. Kim and S. Y. Oh, Pricing of American-style Fixed Strike Asian Options with Continuous Arithmetic Average, 2004.

- [11] R. A. Kuske and J. B. Keller, Optimal Exercise Boundary for an American Put Option, Applied Mathematical Finance, 5 (1998) 107–116.

- [12] Y. K. Kwok, Mathematical Models of Financial Derivatives, Springer Finance, Springer, Berlin, second ed., 2008.

- [13] V. Linetsky, Spectral Expansions for Asian (Average Price) Options, Operations Research, 52 (2004) 856–867.

- [14] R. Mallier, Evaluating Approximations for the American Put Option, Journal of Applied Mathematics, 2 (2002) 71–92.

- [15] A. Pascucci, Free Boundary and Optimal Stopping Problems for American Asian Options, Finance Stoch, 12 (2008) 21–41.

- [16] D. Ševčovič, Transformation Methods for Evaluating Approximations to the Optimal Exercise Boundary for Linear and Nonlinear Black–Scholes Equations, In: M. Ehrhardt (ed.), Nonlinear Models in Mathematical Finance: New Research Trends in Option Pricing, p. 153-198, Nova Science Publishers, Inc., Hauppauge, 2008.

- [17] P. Wilmott, S. Howison, and J. Dewynne, The mathematics of financial derivatives, Cambridge University Press, Cambridge, 1995. A student introduction.

- [18] L. Wu, Y. K. Kwok and H. Yu, Asian Options with the American Early Exercise Feature, International Journal of Theoretical and Applied Finance, 2 (1999) 101–111.

- [19] R. Wu and M. C. Fu, Optimal Exercise Policies and Simulation-based Valuation for American-Asian Options, Operations Research, 51 (2003) 52–66.

- [20] U. Wystup, FX Options and Structured Products, www.mathfinance.com, 2006.