Testing affiliation in private-values models of first-price auctions using grid distributions

Abstract

Within the private-values paradigm, we construct a tractable empirical model of equilibrium behavior at first-price auctions when bidders’ valuations are potentially dependent, but not necessarily affiliated. We develop a test of affiliation and apply our framework to data from low-price, sealed-bid auctions held by the Department of Transportation in the State of Michigan to procure road-resurfacing services: we do not reject the hypothesis of affiliation in cost signals.

doi:

10.1214/10-AOAS344keywords:

.and

1 Motivation and introduction

During the past half century, economists have made considerable progress in understanding the theoretical structure of equilibrium strategic behavior under market mechanisms, such as auctions, when the number of potential participants is relatively small; see Krishna (2010) for a comprehensive presentation and evaluation of progress.

One analytic device, commonly used to describe bidder motivation at single-object auctions, is a continuous random variable which represents individual-specific heterogeneity in valuations. The conceptual experiment involves each potential bidder’s receiving a draw from a distribution of valuations. Conditional on his draw, a bidder is then assumed to act purposefully, maximizing either the expected profit or the expected utility of profit from winning the auction. Another frequently-made assumption is that the valuation draws of bidders are independent and that the bidders are ex ante symmetric—their draws being from the same distribution of valuations. This framework is often referred to as the symmetric independent private-values paradigm (symmetric IPVP). Under these assumptions, a researcher can then focus on a representative agent’s decision rule when describing equilibrium behavior.

At many real-world auctions, the latent valuations of potential bidders are probably dependent in some way. In auction theory, it has been assumed that dependence satisfies affiliation, a term coined by Milgrom and Weber (1982). Affiliation is a condition concerning the joint distribution of signals. Often, affiliation is described using the intuition presented by Milgrom and Weber: “roughly, this [affiliation] means that a high value of one bidder’s estimate makes high values of the others’ estimates more likely.” Thus described, affiliation seems like a relatively innocuous condition. In the case of continuous random variables, following the path blazed by Karlin (1968), some refer to affiliation as multivariate total positivity of order two, or for short. Essentially, under affiliation, with continuous random variables, the off-diagonal elements of the Hessian of the logarithm of the joint probability density function of signals are all nonnegative, that is, the joint probability density function is log-supermodular. Under joint normality of signals, affiliation requires that all the pair-wise covariances be weakly positive.

How is affiliation related to other forms of dependence? Consider two continuous random variables and , having joint probability density function as well as conditional probability density functions and and conditional cumulative distribution functions and . Introduce and , functions that are nondecreasing in their arguments. de Castro (2007) has noted that affiliation implies (a) is decreasing in (and in the other case), often referred to as a decreasing inverse hazard rate, which implies (b) is nonincreasing in (and in the other case), also referred to as positive regression dependence, which implies (c) is nonincreasing in (and in the other case), also referred to as left-tail decreasing in (), which implies (d) is positive, which implies that (e) is positive, which implies (f) is positive. The important point to note is that affiliation is a much stronger form of dependence than positive covariance. In addition, de Castro (2007) has demonstrated that, within the set of all signal distributions, the set satisfying affiliation is small, both in the topological sense and in the measure-theoretic sense.

Affiliation delivers several predictions and results: first, under affiliation, the existence and uniqueness of a monotone pure-strategy equilibrium (MPSE) is guaranteed. Also, four commonly-studied auction formats—the oral,ascending-price (often referred to by economists as the English) and the second-price, sealed-bid (often referred to by economists as the Vickrey) as well as two first-price ones—can be ranked in terms of the revenues they can be expected to generate. Specifically, the expected revenues at English auctions are weakly greater than those at Vickrey auctions which are greater than those at first-price auctions—either the sealed-bid or the oral, descending-price (often referred to by economists as the Dutch) formats. Note, however, that when bidders are asymmetric, their valuation draws being from different marginal distributions, these rankings no longer apply. In fact, in general, very little can be said about the revenue-generating properties of the various auction formats and pricing rules under asymmetries.

Empirically investigating equilibrium behavior at auctions when latent valuations are affiliated has challenged researchers for some time. Laffont and Vuong (1996) showed that identification has been impossible to establish in many models when affiliation is present. In fact, Laffont and Vuong demonstrated that any model within the affiliated-values paradigm (AVP) is observationally equivalent to a model within the affiliated private-values paradigm (APVP). For this reason, virtually all empirical workers who have considered some form of dependence have worked within the APVP.

Only a few researchers have dealt explicitly with models within the APVP. In particular, Li, Perrigne and Vuong (2000) have demonstrated nonparametric identification within the conditional IPVP, a special case of the APVP, while Li, Perrigne and Vuong (2002) have demonstrated nonparametric identification within the APVP. One of the problems that Li et al. faced when implementing their approach is that nonparametric kernel-smoothed estimators are often slow to converge. In addition, Li et al. do not impose affiliation in their estimation strategy, so the first-order condition used in their two-step estimation strategy need not constitute an equilibrium. Hubbard, Li and Paarsch (2009) have sought to address some of these technical problems using semiparametric methods which sacrifice the full generality of the nonparametric approach in lieu of additional structure.

To date, except for Brendstrup and Paarsch (2007), no one has attempted to examine, empirically, models in which the private values are potentially dependent, but not necessarily affiliated. Incidentally, using data from sequential English auctions of two different objects, Brendstrup and Paarsch found weak evidence against affiliation in the valuation draws of two objects for the same bidder.

de Castro (2007) has noted that, within the private-values paradigm, affiliation is unnecessary to guarantee the existence and uniqueness of a MPSE. In fact, he has demonstrated existence and uniqueness of a MPSE under a weaker form of dependence, one where the inverse hazard rate is decreasing in the conditioned argument.

Because affiliation is unnecessary to guarantee existence and uniqueness of bidding strategies in models of first-price auctions with private values, expected revenue predictions based on empirical models in which affiliation is imposed are potentially biased. Knowing whether valuations are affiliated is central to ranking auction formats in terms of the expected revenues generated. In the absence of affiliation, the expected-revenue rankings delivered by the linkage principle of Milgrom and Weber (1982) need not hold: the expected-revenue rankings across auctions formats remain an empirical question. Thus, investigating the empirical validity of affiliation appears both an important and a useful exercise.

In next section of this paper we present a brief description of affiliation and its soldier—total positivity of order two (). Subsequently, following the theoretical work of de Castro (2007, 2008), who introduced the notion of the grid distribution, in Section 3 we construct a tractable empirical model of equilibrium behavior at first-price auctions when the private valuations of bidders are potentially dependent, but not necessarily affiliated.111The grid distributions discussed and used in this paper can also be modeled as contingency tables, which have been used extensively in applications in the social sciences; see Douglas et al. (1990) for the connections between contingency tables and positive dependence properties, including affiliation (), which is the focus of this paper. In Section 4 we develop a test of affiliation, which is based on grid distributions, rather than kernel-smoothing methods, thus avoiding the drawback encountered by Li, Perrigne and Vuong (2000, 2002), while in Section 5 we apply our methods in an empirical investigation of low-price, sealed-bid, procurement-contract auctions held by the Department of Transportation in the State of Michigan, and do not reject the null hypothesis of affiliation.

This information is potentially useful to a policy maker. The apparent high degree of estimated affiliation also explains why low levels of observed competition are often sufficient to maintain relatively low profit margins: strong affiliation is akin to fierce competition. Under strong affiliation, a potential winner knows that his nearest competitor probably has a valuation (cost) close to his, and this disciplines his bidding behavior: he becomes more aggressive than under independence. We summarize and conclude in Section 6, the final section of the paper. The results of a small-scale Monte Carlo to investigate the numerical as well as small-sample properties of our proposed test are reported in the supplemental document—de Castro and Paarsch (2010).

2 Affiliation and

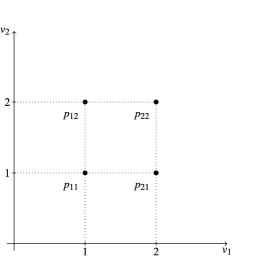

As mentioned above, affiliation is often described using an example with two random variables that can take on either a low or a high value. The two random variables are affiliated if high (low) values of each are more likely to occur than high and low or low and high values. A commonly-used graph of the four possible outcomes in a two-bidder auction game with two values is depicted in Figure 1. The and points are more likely than the or points. Letting denote the probability of , affiliation in this example then reduces to —viz.,

Put another way, means that the determinant of the matrix

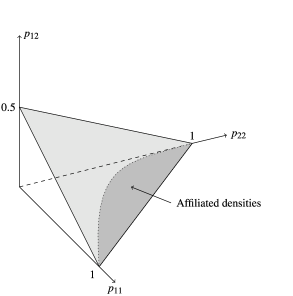

must be weakly positive. Independence in valuations obviously satisfies the lower bound on this determinental inequality. Note, too, that affiliation restricts distributions to a part of the simplex depicted in Figure 2. In that figure, it is the region of the simplex that appears below a semi-circle rising from the line where equals one. In order to draw this figure, we needed to impose symmetry, so and are equal; thus, the intercept for is one half. Conditions that are weaker than affiliation, but that also guarantee existence and uniqueness of equilibrium, are depicted in Figure 2, too. In fact, in this simple example, the entire simplex satisfies these weaker conditions. In richer examples, however, it is a subset of the simplex, but one that contains the set of affiliated distributions. Thus, the assumption of affiliation could be important in determining the revenues a seller can expect from a particular auction format.

Slavković and Fienberg (2009) have discussed geometric representations of distributions, like some of those considered here. Their representations are based on tetrahedrons, while ours reduce to triangles because of symmetry.

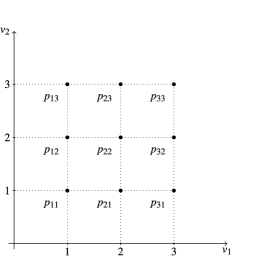

Another important point to note is that affiliation is a global restriction. To see the importance of this fact, introduce the valuation for each bidder; five additional points then appear, as is depicted in Figure 3. Affiliation requires that the probabilities at all collections of four points satisfy ; that is, the following additional six inequalities must hold:

Of course, symmetry would imply that equal for all and , so the joint mass function for two bidders and three valuations under symmetric affiliation can be written as the following matrix:

where the determinants of all submatrices must be positive. Note, too, that all the points must also live on the simplex, so

How many inequalities are relevant? Let us represent the above matrix in the following tableau:

|

where the row and column numbers will be used later to define inequalities. There are or nine possible combinations of four cells—that is, nine inequalities. However, by symmetry, three are simply duplicates of others. The following tableau represents all of the inequalities:

|

|

where means form a matrix with elements from rows and and columns and of the first tableau. Observe that when the three inequalities highlighted in bold are satisfied, all others will be also satisfied. In fact, the inequality derives from and . Finally, inequality derives from the other two, previously established—viz., and . All other inequalities can be obtained from the adjacent ones in this fashion.

Adding values to the type spaces of bidders expands the number of determinental restrictions required to satisfy , thus restricting the space of distributions that can be entertained. Likewise, adding bidders to the game, particularly if the bidders are assumed symmetric, also restricts the space of distributions that can be entertained. For example, suppose a third bidder is added, one who is symmetric to the previous two. The probability mass function for triplets of values , where and , can be represented as an array whose slices can then be represented by the following three matrices for bidders and , indexed by the values of bidder :

In general, if the number of bidders is and the number of values is , then, without symmetry or affiliation, probability arrays have unique elements. Also, de Castro (2008) has shown that symmetry reduces this to elements, while affiliation restricts where these probabilities can live on the simplex via the determinental inequalities required by . It is well known that a function is (affiliated), if and only if, it is in all relevant collections of four points. As an aside, in this three-by-three example, only nine constraints are relevant—viz.,

If these hold, then the remainder are satisfied, too. Knowing the maximum number of binding constraints is relevant later in the paper when we discuss our test statistic.

Consider now the random -vector which equals , having joint density (mass) function with realization equal to . Affiliation can be formally defined as follows: for all and , the random variables are said to be affiliated if

where

denotes the component-wise maxima of and , sometimes referred to as the join, while

denotes the component-wise minima, sometimes referred to as the meet.

3 Theoretical model

We develop our theoretical model within the private-values paradigm, assuming away any interdependencies. We consider a set of bidders . Now, bidder is assumed to draw , his private valuation of the object for sale, from the closed interval . We note that, without loss of generality, one can reparametrize the valuations from to . Below, we do this. We collect the valuations in the vector which equals and denote this vector without the th element by . Here, we have used the now-standard convention that upper-case letters denote random variables, while lower-case ones denote their corresponding realizations. Note, too, that lives in .

We assume that the values are distributed according to the probability density function which is symmetric; that is, for the permutation we have equals . Letting denote the marginal probability density function of , we note that it equals . [Below, we constrain ourselves to the case where is the same for all , but this is unnecessary and done only because, when we come to apply the method, we do have not enough information to estimate the case with varying ’s.] Our main interest is the case when is not the product of its marginals—the case where the types are dependent. We denote the conditional density of given by

Finally, we denote the largest order statistic of given by and its probability density and cumulative distribution functions by and , respectively.

We assume that bidders are risk neutral and abstract from a reserve price. Given his value , bidder tenders a bid . If his tender is the highest, then bidder wins the object and pays what he bid. A pure strategy is a function which specifies the bid for each value . The interim pay-off of bidder , who bid when his opponents follow , is

We focus on symmetric, increasing pure-strategy equilibria (PSE) which are defined by such that

As mentioned above, in most theoretical models of auctions that admit dependence in valuation draws, researchers have assumed that satisfies affiliation. We do not restrict ourselves to ’s that satisfy affiliation. We assume only that belongs to a set of distributions which guarantees the existence and uniqueness of a MPSE. This set was fully characterized by de Castro (2008) in the particular case of grid distributions, which are considered in our Assumption 4.1, below.

Let denote the set of continuous density functions and let denote the set of affiliated probability functions. For convenience and consistency with the notation used in later sections, we include in the set of all affiliated probability functions, not just the continuous ones. Endow with the topology of the uniform convergence—that is, the topology defined by the norm of the supremum

Let be the set of probability functions and assume there is a measure over it.

We now introduce a transformation which is the workhorse of our method. To define , let denote the function that associates to the ceiling —viz., the smallest integer at least as large as . Thus, for each , we have . Similarly, let denote the “square” (hypercube) where collects . From this, we define as the transformation that associates to each the probability density function given by

Observe that is constant over each square , for all combinations of . The term above derives from the fact that each square has volume . Note that for all probability density functions , equals one for all , that is, is the uniform distribution on .

We now need to introduce a compact notation to represent arrays of dimension . We denote by the set of arrays and by an array in that set. When there are but two bidders, an array is obviously just a matrix. In the application of this model to field data, which we describe in Section 5, is three. The th element of an array is denoted , or for short, where denotes the vector . Now, if . Thus, for , we define the finite-dimensional subspace as

Observe that is a finite-dimensional set. In fact, when is two, a probability density function can be described by a matrix as follows:

| (1) |

for The definition of at the zero measure set of points is arbitrary.

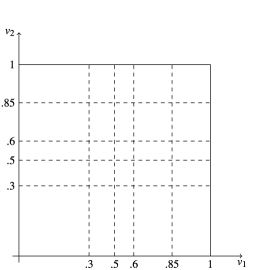

Note, too, that the width of the cells can be allowed to vary. For example, one might be wide, while the next one can be wide, the third wide, the next , and the last . In fact, the transformation can be defined in terms of rectangles, instead of squares as above. To illustrate this, consider again the symmetric case and introduce Figure 4. Let be an arbitrary partitioning of the interval .222We implicitly assume here that the that form become dense in as increases. Now, define by if and only if . Define as the rectangle (box) where collects lies. Thus, . Now, define

The following theorem was proven by de Castro (2008):

Theorem 3.1

Let be a symmetric and continuous probability density function. is affiliated if and only if for all , is also affiliated.

In our notation,

or

Why is this important? Well, in many applications, the set of hypercubes defined by a large will have many empty cells, which causes problems in both estimation and inference. Thus, one may want to subdivide the space of valuations irregularly, but symmetrically, as illustrated in Figure 4 when is two.

4 Test of affiliation

The key result from de Castro (2007) that allows us to develop our test of symmetric affiliation is the following: if the true probability density function exhibits affiliation, then , a discretized version of it, will too. (See Theorem 3.1, above.) To the extent that the grid distribution can be consistently estimated from sample data, one can then test whether the estimated grid distribution exhibits affiliation. Of course, sampling error will exist, but presumably one can evaluate its relative importance using first-order asymptotic methods.

Consider a sequence of auctions indexed at which bidders participated by submitting the bids . We note that affiliation is preserved under a monotonic transformation, so examining a discretization of , the true probability density function of bids under the hypothesis of expected-profit maximizing equilibrium behavior, is the same as examining . Of course, neither nor is known. One can, however, construct an estimate of on the interval by first transforming the observed bids according to

where is the smallest observed bid and is the largest observed bid, and then by breaking up this hypercube into cells and counting the number of times that a particular -tuple falls in that cell.333We know that the support of is strictly positive at , the true upper bound of support of bids, and we assume that is strictly positive at , so is strictly positive at , the true lower bound of support of bids. Consequently, the sample estimators of the lower and upper bounds of support of converge at rate , which is faster than the rate of convergence of sample averages—rate . Hence, when using sample averages in our estimation, we can ignore this first-stage, pre-estimation error—at least under first-order asymptotic analysis. Now, the random vector , which represents the number of outcomes that fall in each of the cells and equals the vector , follows a multinomial distribution having the joint probability mass function

where equals , with , while collects and lives on the simplex—viz., the set

with being an vector of ones. Note, too, that equals , the number of observations.

For , the unconstrained maximum-likelihood estimates of the ’s are the ’s. To test for affiliation, maximize the following logarithm of the likelihood function (minus a constant):

subject to {longlist}

the vector lies in the simplex ;

all of the determinental inequalities required for hold. Then compare this value of with the unconstrained one.

While the determinental constraints required for are convex sets of the parameters when the submatrices are symmetric, they are not for general submatrices. However, by taking logarithms of both sides of any general determinental inequality

one can convert this into a linear inequality, which does give rise to convex constraint sets, albeit in variables that are logarithms of the original variables. To wit,

defines a convex set (in the transformed variables ). Of course, the adding-up constraint for the simplex must be finessed—for example, by considering the following:

which gives rise to a convex set. Thus, the problem is almost a linear programme.

For known and fixed , the specific steps involved in implementing the test in this problem are the following. First, form the grid distribution of the joint density as the unknown array . Letting denote the array of counts for the grid distribution, the logarithm of the likelihood function for this multinomial process is

| (2) |

Now, the following inequalities must be met:

| (3) |

while symmetry requires the following linear restrictions:

| (4) |

where is any permutation, and affiliation requires the following determinental inequalities:

| (5) |

hold. A test of affiliation, within a symmetric environment, involves comparing the maximum of equation (2), subject to the constraints in (3) and (4), with the maximum of equation (2), subject to the constraints in (3), (4) and (5).

Our test of symmetric affiliation is based on the difference between the maximum of the logarithm of the likelihood function and the maximum of the logarithm of the likelihood function under symmetric affiliation . Obviously, the sampling theory associated with the difference in these two values of the objective function is not straightforward because not all of the inequality constraints required by may hold and, from sample to sample, the ones that do hold can change, but we shall suggest several strategies to deal with this, below.

Experience gleaned from other models with a related structure—for example, Wolak (1987, 1989a, 1989b, 1991) as well as Bartolucci and Forcina (2000), who investigated in binary models—suggests that the likelihood ratio (LR) statistic

| (6) |

is not distributed according to a standard random variable.

Introducing as a short-hand notation, for the -vector created from the array , our constrained-optimization problem can be summarized in a notation similar to that of Wolak (1989b) as

where is the function representing all relevant constraints where and is the total number of variables under the alternative hypothesis. (Here, for notational parsimony, we have ignored the adding-up condition, which is implicit.)

Consider , a neighborhood of the true value . Denote by the matrix of partial derivatives whose -element is . Now, let us define the set . Denote by Fisher’s information matrix which is defined by

evaluated at . Finally, denote by

the variance–covariance matrix of and by , the probability that constraints bind, that constraints are strictly satisfied, that is, they are nonbinding. We have the following:

Theorem 4.1

Consider the local hypothesis testing problem

The asymptotic distribution of the likelihood-ratio statistic satisfies the following property:

where is the asymptotic value of the test statistic, while is an independent random variable having degrees of freedom.

It is sufficient and straightforward to verify that the assumptions of Theorem 4.2 in Wolak (1989a) are satisfied. Because this statistic depends on the unknown population grid distribution , the statistic is not pivotal. Kodde and Palm (1986) have provided lower and upper bounds for this test statistic for tests of various sizes and different numbers of maximal constraints.

According to Wolak (1989a), the best way to evaluate the weights is using Monte Carlo simulation. Wolak also offered lower and upper bounds for the probabilities above [see his equations (19) and (20), page 215]; these bounds are based on Kodde and Palm (1986). An alternative strategy would be to adapt the bootstrap methods of Bugni (2008) to get the appropriate p-values of the test statistic. Yet a third strategy would be to adapt the subsampling methods described in Politis, Romano and Wolf (1999) as was done by Romano and Shaikh (2008).

4.1 Some comparisons with other nonparametric methods

It should be noted, too, that our proposed estimation strategy involves nothing more than estimating a histogram using a special class of grids. Scott [(1992), page xi] has argued that the classical histogram “remains the most widely applied and most intuitive nonparametric estimator.” In other words, the procedure proposed here is not based on any unfamiliar concepts. Of course, there are more statistically efficient methods, but they also have limitations, as Scott (1992) has discussed. Also, although the rate of convergence of histogram estimation is slow, it is still reasonable; see Scott [(1992), Theorem 3.5, page 82].

Note, too, the similarities between grid-distribution and kernel-smoothed estimators. Kernel-smoothed density estimators are well-behaved and have good rates of convergence when the probability density functions to be estimated are continuously differentiable .444Methods exist that require fewer smoothness conditions—for example, the function need just be continuous ; others require additional smoothness, or higher. This does not change our claims. The set is dense in the set of all probability density functions. Similarly, grid distribution estimators are well-behaved for probability density functions in , which is also a dense set in the set of all probability density functions.555Recall that is the set of grid distributions where the interval is subdivided into intervals, that is, While probability density functions form a familiar and well-known class probability density functions, the probability density functions in are also familiar because they are just (a special class of) simple functions, which are fundamental, such as in the definition of the Lebesgue integral. When estimating grid distributions, one has to choose or, equivalently, the size of the bin , which is nothing more than the bandwidth of the grid-distribution estimator. Similarly, kernel-smoothing requires a choice of bandwidth parameter, too. In sum, nonparametric estimation using either grid distributions or smoothed kernels is very similar.

4.2 Consistency and power of the proposed test

Of course, one concern is that appears fixed in our analysis, but is increasing, so our test is potentially inconsistent. We imagine a sequence of with values increasing as increases, but not as fast as . Below, we discuss in detail what we have in mind. Another worry is that the test statistic will be ill-behaved if tends to infinity. Thus, an upper bound must exist. This discussion leads us to introduce the following assumption concerning which allows us to side-step these technical problems:

Assumption 4.1

The true data-generating process is a grid distribution, that is, there exists such that .

As the discussion above made clear, this assumption is similar to the assumptions of smoothness concerning which kernel-smoothing methods require. In addition to this analogy, we offer two additional justifications for Assumption 4.1.

First, the set of grid distributions is dense in the set of all distributions: even if the data-generating process (DGP) were not a grid distribution, there is a grid distribution that is arbitrarily close to it. To wit, no finite amount of data could reject Assumption 4.1. In this sense, Assumption 4.1 is almost “no assumption.”

Second, the DGP in question is a distribution of values, which are discrete (up to, say, dollars or cents or Yen or Won or whatever units one wants). When one assumes a smooth probability density function, one is making an approximation, for computational convenience: such an approximation does not seem, to us at least, any more appealing than the one we make. On the contrary, it seems more natural to us to assume simple probability density functions rather than any smoothness conditions. In general, smoothness is just a tool used to lighten the burden in the technical analysis of a particular problem. In our case, by assuming that the distribution is simple (i.e., a grid distribution), we can stay closer to reality.

Under Assumption 4.1, our test is consistent, for Assumption 4.1 implies that a exists such that . Therefore, the number of inequalities required for affiliation remains fixed. We are then in the standard framework considered by Wolak, which has a fixed set of inequalities. Thus, consistency follows directly from Wolak’s research. A technically sophisticated reader may feel that our consistency result is trivial, once Assumption 4.1 is made. The point of this paper (and this subsection, in particular) is not to provide a technical proof of consistency, but rather to remove any doubts concerning the consistency of our test under a reasonable assumption.

For any specific implementation, is assumed fixed in the approximation. In the asymptotics, we imagine increasing as increases, until some upper bound is reached. In any application, however, if is quite large, not what we encounter in our application, then one can vary , which will potentially yield different estimates.

The power of the proposed test clearly depends on the choice of . Were chosen to be one (i.e., a uniform distribution on the -dimensional hypercube), then affiliation would never be rejected. On the other hand, given a finite sample of observations, a large will result in many cells having no elements. While the choice of is obviously important and certainly warrants additional theoretical investigation, perhaps along the lines of research in time-series analysis by Guay, Guerre and Lazarova (2008) concerning optimal adaptive detection of correlation functions, it is beyond the scope of this paper. In fact, in most applications to auctions, where samples are often quite small, will be dictated by practical considerations—viz., the relative size of .

4.3 Bounding the number of inequalities

For our test statistic to be well-behaved, it is important to know that an upper bounds exists on the number of inequalities. For arbitrary and , assuming a symmetric distribution, we can construct a bound on how many inequalities there are. Because we focus on symmetric distributions,

where is a permutation of . Thus, we need only consider sorted indices, indices for which . Consider , a sorted index having different numbers; let denote the number of repetitions of the different numbers in . Obviously, . Using this notation, the number of permutations of is then . For instance, the index has or different permutations.

Given the above, we can now focus our attention to sorted indices only. Consider the lexicographic order of them. In this way, we can attribute an unambiguous natural number to each sorted index of length . For example, consider , in which case corresponds to 1; , to 2; , to 3; to 5; , to 7; and to 11. It is important to develop an algorithm to convert a sorted index into a corresponding number, which we describe now.

First, let us define as the number of all indices that areweakly below (in the lexicographic order) to the index , that is, the index that has in all positions and has length . It is easy to seethat , because there is just one index weakly below , itself. Also, , because , and are the sorted indices weakly below . Similarly, , because , , , are the sorted indices weakly below . From this argument, it is not difficult to see that . Observe, too, that , because there are only the indexes , , , weakly below . de Castro (2008) has proven the following:

Lemma 4.1

.

Thus, if we fix the number of bidders and the number of intervals , then there are different indices. Affiliation will be satisfied if the corresponding inequality is satisfied for any pair of indices . Since there are or pair of such indices, it is sufficient to test inequalities. Note, however, that this is an upper bound because some inequalities are implied by others. The above discussion also provides some guidance concerning how to choose the inequalities; however, in an effort to conserve space, we leave the discussion of what the minimal set of sufficient inequalities is to another paper.

4.4 Two related papers

Like us, Li and Zhang (2008) have examined some important economic implications of affiliation. Instead of considering bids, however, Li and Zhang examined the entry behavior of potential bidders whose signals may be affiliated. Theirs is a parametric analysis and they implemented their test using simulation methods, examining timber sales organized by the Department of Forestry in the State of Oregon. Li and Zhang found only a small degree of affiliation, perhaps because the zero/one entry decision is not as informative as bid data.

Jun, Pinkse and Wan (2009) have developed a consistent nonparametric test designed for continuous data. By avoiding discretization, Jun et al. presumably have more information than we do. On the other hand, having rejected affiliation with their test, it is unclear what to do within their framework because an alternative hypothesis is unspecified. In contrast, our approach augments the theoretical work of de Castro (2008) where the alternative hypothesis is clearly outlined.

4.5 Policy uses for grid distributions

de Castro (2008) has developed a complete theoretical treatment of grid distributions, even in the absence of affiliation.666de Castro’s method is too long to be described in detail here; his paper is more than seventy pages long. In a nutshell, the method is as follows: first, it is shown that the usual proof of uniqueness of monotonic pure-strategy equilibrium can be adapted to grid distribution. Thus, if there is a monotonic pure-strategy equilibrium, then it is unique and characterized by the solution to a differential equation. Also, since we consider the symmetric case, an explicit solution is available. In the case of grid distributions, this solution is proven to be a rational function (a quotient of polynomials). It is then shown that in each square defining a grid distribution, it is sufficient to verify the equilibrium inequality (optimality of following the bidding function) only with respect to a finite number of pairs (types, bids). This step is necessary because, in principle, one needs to check an infinite number of pairs (types, bids). The final number of points to be tested is small (less than six) for each square. Finally, it is proven that the candidate is an equilibrium if and only if the test is satisfied. de Castro has also provided expressions for revenues when is a grid distribution. His idea is as follows: first, assume that for some ; that is, the DGP is a grid distribution—Assumption 4.1 holds. Standard estimation methods (histograms) can be used to calculate that best approximate .

Under de Castro’s method, one can then test whether has a symmetric MPSE. The method developed by de Castro is exact: to wit, modulo sampling error, has a symmetric MPSE if and only if the method detects it. Errors can occur only in simple numerical operations such as sums, divisions and square roots. It turns out that determining the existence of a symmetric MPSE is nontrivial when affiliation is absent.

If has a symmetric MPSE, then it can be used to calculate expected revenues under the first- and second-price auctions, denoted and , respectively. In this way, one can determine which auction format yields a higher expected revenue for and, also, the magnitude of the revenue difference , to decide whether it is significant.777As explained above, de Castro has shown that if a monotone, pure-strategy equilibrium exists in a first-price auction, then it is unique. Moreover, we can obtain the underlying distribution of values from the distribution of bids, as is typically done in the econometrics of auctions. Although second-price auctions may have multiple equilibria, in general, in the literature, researchers typically consider only the truthful bidding equilibrium. The truth-telling equilibrium does not depend on the assumption of affiliation: it is an equilibrium for any distribution. Thus, if we have the distribution of values, we also have the distribution of bids for this equilibrium.

The procedure can then be repeated using , which is obtained under the constraint that the distribution satisfies affiliation. We know that, under affiliation, a symmetric MPSE exists and that , but the method also allows one to decide whether the magnitudes of the differences and are economically important. It is quite possible that the expected-revenue difference between first- and second-price auctions is nonzero, but small in economic terms, and the method allows one to examine sampling variability by repeating the above procedures using resampled draws from or . Thus, if the estimated difference is economically large relative to the sampling error, then this is important information for a policy maker to know.

Thus, the grid distributions proposed in this paper have many advantages because a theory exists that can be used for policy analysis. Such theories have not yet been developed for other methods; if affiliation is rejected under these methods, then what to do?

5 Empirical application

Above, in Section 3, in the tradition of the theoretical literature concerning auctions, we developed our model of bidding in terms of valuations for an object to be sold at auction under the first-price, sealed-bid format. Sealed-bid tenders are often used in procurement—that is, low-price, sealed-bid auctions at which a buyer (often a government agency) seeks to find the lowest-cost producer of some good or service. In this section we report results from an empirical investigation of procurement tenders for road resurfacing by a government agency. Although it is well known that results from auctions can be translated to procurement, and vice versa, sometimes this translation is tedious. We direct the interested reader to the work of de Castro and de Frutos (2010) who have developed a procedure to translate results from auctions to procurement.

We have applied our empirical framework to data from low-price, sealed-bid, procurement auctions held by the Department of Transportation (DOT) in the State of Michigan. At these auctions, qualified firms are invited to bid on jobs that involve resurfacing roads in Michigan. We have chosen this type of auction because the task at hand is quite well understood. In addition, there are reasons to believe that firm-specific characteristics make the private-cost paradigm a reasonable assumption; for example, the reservation wages of owners/managers, who typically are paid the residual, can vary considerably across firms. On the other hand, other features suggest that the cost signals of individual bidders could be dependent, perhaps even affiliated; for example, these firms hire other factor services in the same market and, thus, face the same costs for inputs such as energy as well as paving inputs. For example, suppose paving at auction has the following Leontief production function for bidder :

where denotes the managerial labor, while and denote other factor inputs which are priced competitively at and , respectively, at auction . Assume that , bidder ’s marginal value of time, is an independent, private-cost draw from a common distribution. In addition, assume that the other factor prices and are draws from another joint distribution, and that they are independent of . The marginal cost per mile at auction can be then written as

which is a special case of an affiliated private-cost (APC) model, known as a conditional private-cost model. The costs in this model are affiliated only when the distribution of is log-concave, which is discussed extensively in de Castro (2007). Li, Perrigne and Vuong (2000) have studied this model extensively. In short, the affiliated private-cost paradigm (APCP) seems a reasonable null hypothesis.

We did not investigate issues relating to asymmetries across bidders because we do not know bidder identities, data necessary to implement such a specification. Because no reserve price exists at these auctions, we treat the number of participants as if it were the number of potential bidders and focus on auctions at which three bidders participated. Thus, we are ignoring the potential importance of participation costs which others, including Li (2005), have investigated elsewhere.

The data for this part of the paper were provided by the Michigan DOT and were organized and used by Hubbard, Li and Paarsch (2009); a complete description of these data is provided in that paper. In Table 1 we present the summary descriptive statistics concerning our sample of observations— auctions that involved three bidders each. We chose auctions with just three bidders not only to illustrate the general nature of the method (if we can do three, then we can do ), but also to reduce the data requirements. When we subdivide the unit hypercube into cells, the average number of bids in a cell is proportional to . When is very large, the sample size must be on the order of in order to expect at least one observation in each cell. This example also illustrates the potential limitations of our approach; viz., even in relatively large samples, some of the cells will not be populated, so will need to be kept small. However, one can circumvent this problem by varying the width of the subdivisions as we do below. Of course, one must then adjust the conditions which define the determinental inequalities. We describe this below, too.

| Variable | Mean | St. Dev. | Median | Minimum | Maximum |

|---|---|---|---|---|---|

| Engineer’s estimate | 475,544.54 | 491,006.52 | 307,331.26 | 54,574.41 | 3,694,272.59 |

| Winning bid | 466,468.63 | 507,025.81 | 286,102.57 | 41,760.32 | 3,882,524.81 |

| All tendered bids | 507,332.42 | 564,842.58 | 317,814.77 | 41,760.32 | 5,693,872.81 |

Our bid variable is the price per mile. Notice that both the winning bids as well as all tendered bids vary considerably, from a low of $41,760.32 per mile to a high of $5,693,872.81 per mile. What explains this variation? Well, presumably heterogeneity in the tasks that need to be performed. One way to control for this heterogeneity would be to retrieve each and every contract and then to construct covariates from those contracts. Unfortunately, the State of Michigan cannot provide us with this information, at least not any time soon.

How can we deal with this heterogeneity? Well, in our case, we have an engineer’s estimate of the price per mile to complete the project.888Of course, besides , it is possible that other covariates, which are common knowledge to all the bidders, exist. If these other common-knowledge covariates exist, then we could wrongly conclude that the signals have a strong form of correlation when, in fact, the correctly-specified model of signals (conditioned on the common-knowledge information) would have only small correlation. Unfortunately, we do not have access to any additional information. Were such information available, then we would condition on it as well. We assume that , the cost to bidder at auction , can be factored as follows:

| (7) |

where is a known function. One example of this is

Another is

Under equation (7), the equilibrium bid at auction for bidder takes the following form:

so

Of course, we do not know , but we can estimate either parametrically, under an appropriate assumption, or nonparametrically, using the following empirical specification:

where denotes and denotes .

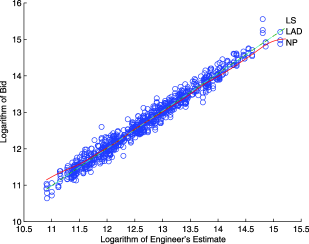

Empirical results from this exercise are presented in Figure 5. In this figure are presented results for the nonparametric regression (NP), the least-squares regression (LS) and the least-absolute-deviations (LAD) regression. To get some notion of the relative fit, note that the for the LS regression is around . The LS estimates of the constant and slope coefficients are and , respectively, while LAD estimates of the constant and slope coefficients are and , respectively.

Subsequently, we took the normalized fitted residuals, which (for the LS case) are depicted in Figure 6, and applied the methods described in Section 4 above for a of two. Our test results are as follows: the maximum of the logarithm of the likelihood function (minus a constant) without symmetry was , while the maximum of the logarithm of the likelihood function under symmetry was , and under symmetric affiliation it was also —a total difference of .999The results for the LAD residuals were identical: the probability array obtained by discretizing the LAD residuals was exactly the same as in the LS case because none of the fitted residuals was classified differently. This is not, perhaps, surprising given the similar fits of the two empirical specifications. At size , twice the above difference is above the lower bound provided by Kodde and Palm (1986), but below the upper bound, so the test is inconclusive.

Because a of two is unusually small, we introduced a symmetric, but nonequispaced, grid distribution—like the one depicted in Figure 4, but with intervals , and . The inequalities can be derived in the usual way, but the adding-up inequality must be rewritten, in this case as

Again, we applied our methods. Our test results are as follows: the maximum of the logarithm of the likelihood function (minus a constant) under symmetry was , while the maximum under symmetric affiliation was —a difference of .101010Again, the results for the LAD residuals were virtually identical: the probability array obtained by discretizing the LAD residuals was almost the same as in the LS case. At size , twice the above difference is below the lower bound provided by Kodde and Palm, so we do not reject the hypothesis of symmetric affiliation. To put these results into some context, the center of the simplex had a logarithm of the likelihood function of ; using the marginal distribution of low, medium and high costs and imposing independence yielded a logarithm of the likelihood function of .

6 Summary and conclusions

We have constructed a tractable empirical model of equilibrium behavior at first-price auctions when bidders’ private valuations are dependent, but not necessarily affiliated. Subsequently, we developed a test of affiliation and then investigated its small-sample properties. We applied our framework to data from low-price, sealed-bid auctions used by the Michigan DOT to procure road-resurfacing: we do not reject the hypothesis of affiliation in cost signals.

This information is potentially useful to a policy maker. The apparent high degree of estimated affiliation also explains why low levels of observed competition are often sufficient to maintain relatively low profit margins: strong affiliation is akin to fierce competition. Under strong affiliation, a potential winner knows that his nearest competitor probably has a valuation (cost) close to his, and this disciplines his bidding behavior: he becomes more aggressive than under independence.

Our research has other policy implications, too. As mentioned above, it is well known that, under affiliation, the English auction format, on average, generates more revenue for the seller than the first-price, sealed-bid format. In procurement, under affiliation, an English or a Vickrey auction would get the job done more cheaply than the low-price, sealed-bid format. Were the English or Vickrey formats being used and affiliation not rejected, then the procurement agency would be justified in its choice of mechanism. What remains a bit of a puzzle is why the low-price, sealed-bid format is used in the presence of such strong affiliation. Perhaps, other features, such as the ability of the low-price, sealed-bid auction format to thwart collusion are important, too. Alternatively, perhaps other moments of the bid distribution, such as the variance, are important to the procurement agency.

On the other hand, had affiliation been rejected, then the procedures described in Section 4 could be used to determine which auction format would get the job done most cheaply, on average. Again, it is possible that the English or Vickrey formats would still be preferred. In any case, the methods described in Section 4 permit a better understanding of the bidding differences, which can aid in choosing the best auction format.

Acknowledgments

Previous versions of this paper circulated underde Castro and Paarsch (2007) and de Castro and Paarsch (2008). For their comments on that research, we thank Kurt Anstreicher, Samuel Burer, Victor Chernozhukov, Srihari Govindan, Emmanuel Guerre, Han Hong, Joel L. Horowitz, Ali Hortaçsu, Kenneth L. Judd, Roger Koenker, David Prentice, Joseph P. Romano, Che-Lin Su, Elie Tamer and Michael Wolf. Timothy P. Hubbard deserves special recognition and thanks for his advice and help with AMPL as well as his comments and insights on the earlier research. We are also grateful to Stephen E. Fienberg, Vijay Krishna, Charles F. Manski, E. Glen Weyl and Frank A. Wolak as well as two anonymous referees who provided helpful comments and useful suggestions on the penultimate draft of this paper.

Monte Carlo Study \slink[doi]10.1214/00-AOAS344SUPP \slink[url]http://lib.stat.cmu.edu/aoas/344/supplement.pdf \sdatatype.pdf \sdescriptionIn this supplement, we discribe a small-scale Monte Carlo study used to investigate the numerical as well as small-sample properties of our testing strategy.

References

- Bartolucci and Forcina (2000) Bartolucci, F. and Forcina, A. (2000). A likelihood ratio test for within binary variables. Ann. Statist. 28 1206–1218. \MR1811325

- Brendstrup and Paarsch (2007) Brendstrup, B. O. and Paarsch, H. J. (2007). Semiparametric estimation of multi-object, sequential, English auctions. J. Econom. 141 84–108. \MR2411738

- Bugni (2008) Bugni, F. (2008). Bootstrap inference in partially identified models. Typescript, Dept. Economics, Northwestern Univ.

- de Castro (2007) de Castro, L. I. (2007). Affiliation, equilibrium existence, and the revenue ranking of auctions. Typescript, Dept. Economics, Carlos III Univ.

- de Castro (2008) de Castro, L. I. (2008). Grid distributions to study single object auctions. Typescript, Dept. Economics, Univ. Illinois Urbana-Champaign.

- de Castro and de Frutos (2010) de Castro, L. I. and de Frutos, M.-A. (2010). How to translate results from auctions to procurements. Econom. Lett. 106 115–118. \MR2650000

- de Castro and Paarsch (2007) de Castro, L. I. and Paarsch, H. J. (2007). Testing for affiliation and monotone pure-strategy equilibrium in models of first-price auctions with private values. Typescript, Dept. Economics, Univ. Iowa.

- de Castro and Paarsch (2008) de Castro, L. I. and Paarsch, H. J. (2008). Using grid distributions to test for affiliation in models of first-price auctions with private values. Typescript, Dept. Economics, Univ. Iowa.

- de Castro and Paarsch (2010) de Castro, L. I. and Paarsch, H. J. (2010). Supplement to “Testing affiliation in private-values models of first-price auctions using grid distributions.” DOI: 10.1214/10-AOAS344SUPP.

- Douglas et al. (1990) Douglas, R., Fienberg, S. E., Lee, M. L. T., Sampson, A. R. and Whitaker, L. R. (1990). Positive dependence concepts for ordinal contingency tables. In Topics in Statistical Dependence (H. W. Block, A. R. Sampson and T. H. Savits, eds.). IMS, Hayward, CA. \MR1193977

- Guay, Guerre and Lazarova (2008) Guay, A., Guerre, E. and Lazarova, S. (2008). Optimal adaptive detection of small correlation functions. Typescript, Dept. Economics, Queen Mary Univ. London.

- Hubbard, Li and Paarsch (2009) Hubbard, T. P., Li, T. and Paarsch, H. J. (2009). Semiparametric estimation in models of first-price, sealed-bid auctions with affiliation. Typescript, Dept. Economics, Univ. Melbourne.

- Jun, Pinkse and Wan (2009) Jun, S. J., Pinkse, J. and Wan, Y. (2009). A consistent nonparametric test of affiliation in auction models. Typescript, Dept. Economics, Pennsylvania State Univ.

- Karlin (1968) Karlin, S. (1968). Total Positivity 1. Stanford Univ. Press, Stanford, CA. \MR0230102

- Kodde and Palm (1986) Kodde, D. A. and Palm, F. C. (1986). Wald criteria for jointly testing equality and inequality restrictions. Econometrica 54 1243–1248. \MR0859464

- Krishna (2010) Krishna, V. (2010). Auction Theory, 2nd ed. Academic Press, San Diego, CA.

- Laffont and Vuong (1996) Laffont, J.-J. and Vuong, Q. H. (1996). Structural analysis of auction data. Amer. Econom. Rev. 86 414–420.

- Li (2005) Li, T. (2005). Econometrics of first-price auctions with binding reservation prices. J. Econom. 126 173–200. \MR2118282

- Li, Perrigne and Vuong (2000) Li, T., Perrigne, I. M. and Vuong, Q. H. (2000). Conditionally independent private information in OCS wildcat auctions. J. Econom. 98 129–161. \MR1790650

- Li, Perrigne and Vuong (2002) Li, T., Perrigne, I. M. and Vuong, Q. H. (2002). Structural estimation of the affiliated private value model. RAND J. Econom. 33 171–193.

- Li and Zhang (2008) Li, T. and Zhang, B. (2008). Testing for affiliation in first-price auctions using entry behavior. Typescript, Dept. Economics, Vanderbilt Univ.

- Milgrom and Weber (1982) Milgrom, P. R. and Weber, R. J. (1982). A theory of auctions and competitive bidding. Econometrica 50 1089–1122.

- Politis, Romano and Wolf (1999) Politis, D. N., Romano, J. P. and Wolf, M. (1999). Subsampling. Springer, Berlin. \MR1707286

- Romano and Shaikh (2008) Romano, J. P. and Shaikh, A. M. (2008). Inference for identifiable parameters in partially identified econometric models. J. Statist. Plann. Inference 138 2786–2807. \MR2422399

- Scott (1992) Scott, D. W. (1992). Multivariate Density Estimation: Theory, Practice, and Visualization. Wiley, New York. \MR1191168

- Slavković and Fienberg (2009) Slavković, A. B. and Fienberg, S. E. (2009). Algebraic geometry of contingency tables. In Algebraic and Geometric Methods in Statistics (P. Gibilisco, E. Riccomagno, M.-P. Rogantin and H. P. Wynn, eds.). Cambridge Univ. Press, New York.

- Wolak (1987) Wolak, F. A. (1987). An exact test for multiple inequality and equality constraints in the linear regression model. J. Amer. Statist. Assoc. 82 782–793. \MR0909983

- Wolak (1989a) Wolak, F. A. (1989a). Local and global testing of linear and nonlinear inequality constraints in nonlinear econometric models. Econometric Theory 5 1–35. \MR0990785

- Wolak (1989b) Wolak, F. A. (1989b). Testing inequality constraints in linear econometric models. J. Econom. 41 205–235. \MR1007731

- Wolak (1991) Wolak, F. A. (1991). The local nature of hypothesis tests involving inequality constraints in nonlinear models. Econometrica 59 981–995. \MR1113543