We introduce and analyze multilevel Monte Carlo algorithms for the

computation of , where

is the solution of a multidimensional Lévy-driven stochastic differential

equation and is a real-valued function on the path space. The

algorithm relies on approximations

obtained by simulating large jumps of the Lévy process individually

and applying a Gaussian approximation

for the small jump part.

Upper bounds are provided for the worst case error over the class of

all measurable real functions

that are Lipschitz continuous with respect to the supremum norm. These

upper bounds are easily tractable

once one knows the behavior of the Lévy measure around zero.

In particular, one can derive upper bounds from the Blumenthal–Getoor

index of the Lévy process.

In the case where the Blumenthal–Getoor index is larger than one, this

approach is superior to

algorithms that do not apply a Gaussian approximation.

If the Lévy process does not incorporate a Wiener process or if the

Blumenthal–Getoor index

is larger than , then the upper bound is of order

when the runtime tends to infinity. Whereas in the case, where

is in and

the Lévy process has a Gaussian component, we obtain bounds of order

.

In particular, the error is at most of order .

60H35,

60H05,

60H10,

60J75,

Multilevel Monte Carlo,

Komlós–Major–Tusnády coupling,

weak approximation,

numerical integration,

Lévy-driven stochastic differential equation,

doi:

10.1214/10-AAP695

keywords:

[class=AMS]

.

keywords:

.

††volume: 21††issue: 1

1 Introduction

Let and denote by the Skorokhod space of

functions mapping to endowed with its

Borel--field.

In this article, we analyze numerical schemes for the evaluation of

where

•

is a solution to a multivariate stochastic

differential equation driven by a multidimensional Lévy process (with

state space ), and

•

is a Borel measurable function that is

Lipschitz continuous with respect to the supremum norm.

This is a classical problem which appears for instance in finance,

where models the risk neutral stock price and denotes the

payoff of a (possibly path dependent) option, and in the past several

concepts have been employed for dealing with it.

A common stochastic approach is to perform a Monte Carlo simulation of

numerical approximations to the solution .

Typically, the Euler or Milstein schemes are used to obtain

approximations. Also higher order schemes can be applied provided that

samples of iterated Itô integrals are supplied and the coefficients

of the equation are sufficiently regular. In general, the problem is

tightly related to weak approximation which is, for instance,

extensively studied in the monograph by Kloeden and Platen KloePla92 for diffusions.

Essentially, one distinguishes between two cases. Either depends

only on the state of at a fixed time or alternatively it depends on

the whole trajectory of . In the former case, extrapolation

techniques can often be applied to increase the order of convergence,

see TalTub90 .

For Lévy-driven stochastic differential equations, the Euler scheme

was analyzed in ProTal97 under the assumption that the

increments of the Lévy process are simulatable. Approximate

simulations of the Lévy increments are considered in JKMP05 .

In this article, we consider functionals that depend on the whole

trajectory. Concerning results for diffusions, we refer the reader to the

monograph KloePla92 . For Lévy-driven stochastic differential

equations, limit theorems in distribution are provided in Jac04

and Rub03 for the discrepancy between the genuine solution and

Euler approximations.

Recently, Giles Gil08 , Gil08b (see also Hei98 )

introduced the so-called multilevel Monte Carlo method to

compute . It is very efficient when is a diffusion. Indeed,

it even can be shown that it is—in some sense—optimal, see CDMR08 . For Lévy-driven stochastic differential equations,

multilevel Monte Carlo algorithms are first introduced and studied

in DerHei10 . Let us explain their findings in terms of the

Blumenthal–Getoor index (BG-index) of the driving Lévy process which

is an index in . It measures the frequency of small jumps,

see (3), where a large index corresponds to a process

which has small jumps at high frequencies. In particular, all Lévy

processes which have a finite number of jumps has BG-index zero.

Whenever the BG-index is smaller or equal to one, the algorithms of

DerHei10 have worst case errors at most of order , when the runtime tends to infinity. Unfortunately, the

efficiency decreases significantly for larger Blumenthal–Getoor indices.

Typically, it is not feasible to simulate the increments of the Lévy

process perfectly, and one needs to work with approximations. This

necessity typically worsens the performance of an algorithm, when the

BG-index is larger than one due to the higher frequency of small jumps.

It represents the main bottleneck in the simulation.

In this article, we consider approximative Lévy increments that

simulate the large jumps and approximate the small ones by a normal

distribution (Gaussian approximation) in the spirit of Asmussen

and Rosiński AsmRos01 (see also CohRos07 ).

Whenever the BG-index is larger than one, this approach is superior to

the approach taken in DerHei10 , which neglects small jumps in

the simulation of Lévy increments.

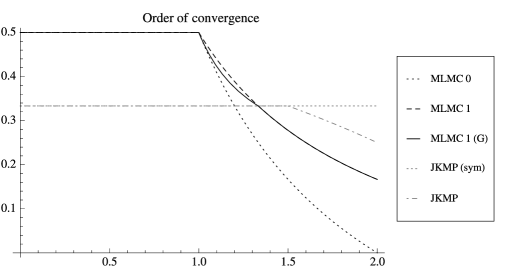

Figure 1: Order of convergence in dependence on the Blumenthal–Getoor index.

To be more precise, we establish a new estimate for the Wasserstein

metric between an approximative solution with Gaussian approximation

and the genuine solution, see Theorem 3.1. It is based on a

consequence of Zaitsev’s generalization Zai98 of the Komlós–Major–Tusnády coupling

KMT75 , KMT76 which might be of its

own interest itself, see Theorem 6.1.

With these new estimates, we analyze a class of multilevel Monte Carlo

algorithms together with a cost function which measures the

computational complexity of the individual algorithms.

We provide upper error bounds for individual algorithms and optimize

the error over the parameters under a given cost constraint. When the

BG-index is larger than one, appropriately adjusted algorithms lead to

significantly smaller worst case errors over the class of

Lipschitz functionals than the ones analyzed so far, see Theorem 1.1, Corollary 1.2 and Figure 1. In particular,

one always obtains numerical schemes with errors at most of order when the runtime of the algorithm tends to infinity.

Notation and universal assumptions

We denote by the Euclidean norm for vectors as well as the

Frobenius norm for matrices and let denote the supremum

norm over the interval . denotes an

-dimensional -integrable Lévy process. By the Lévy–Khintchine formula, it is characterized by a square integrable Lévy-measure [a Borel measure on

with ], a positive semi-definite

matrix ( being a -matrix), and a

drift via

where

Briefly, we call a -Lévy process, and

when , a -Lévy martingale. All Lévy

processes under consideration are assumed to be càdlàg.

As is well known, we can represent as sum of three independent processes

where is a -dimensional Wiener process and

is a -martingale that comprises the compensated

jumps of .

We consider the integral equation

(1)

where is a fixed deterministic initial value.

We impose the standard Lipschitz assumption on the function : for a fixed , and all

, one has

Furthermore, we assume without further mentioning that

We refer to the monographs Ber98 and Sat99 for details

concerning Lévy processes. Moreover, a comprehensive introduction to

the stochastic calculus for discontinuous semimartingales and, in

particular, Lévy processes can be found in Pro05 and Apple04 .

In order to approximate the small jumps of the Lévy process, we need

to impose a uniform ellipticity assumption.

Assumption UE.

There are , and a linear subspace

of such that for all the

Lévy measure is supported on and satisfies

for all with .

Main results

We consider a class of multilevel Monte Carlo algorithms

together with a cost function

that are introduced explicitly in Section 2. For each

algorithm , we denote by a

real-valued random variable representing the random output of the

algorithm when applied to a given measurable function . We work in the real number model of computation, which means that we

assume that arithmetic operations with real numbers and comparisons can

be done in one time unit, see also Nov95 . Our cost function represents the runtime of the algorithm reasonably

well when supposing that

•

one can sample from the distribution and the uniform distribution on in constant time,

•

one can evaluate at any point in constant

time, and

•

can be evaluated for piecewise constant functions in less

than a constant multiple of its breakpoints plus one time units.

As pointed out below, in that case, the average runtime to evaluate

is less than a constant multiple of . We analyze the minimal worst case error

Here and elsewhere, denotes the class of measurable

functions that are Lipschitz continuous with respect

to supremum norm with coefficient one.

In this article, we use asymptotic comparisons. We write for

and or, equivalently , for

Our main findings are summarized in the following theorem.

Theorem 1.1

Assume that Assumption UE

is valid and

let be a decreasing and invertible

function such that for all

and, for a fixed ,

(2)

for all sufficiently small .

[(II)]

(I)

If or

then

(II)

If

then

where .

The class of algorithms together with appropriate parameters

which establish the error estimates above are stated explicitly in

Section 2.

In terms of the Blumenthal–Getoor index

(3)

we get the following corollary.

Corollary 1.2

Assume that Assumption UE

is valid and that the BG-index satisfies .

If or , then

and, if and ,

Visualization of the results and relationship to other work

Figure 1 illustrates our findings and related results. The

-axis and -axis represent the Blumenthal–Getoor index and the

order of convergence, respectively. Note that MLMC 0 stands for the

multilevel Monte Carlo algorithm which does not apply a Gaussian

approximation, see DerHei10 . Both lines marked as MLMC 1

illustrate Corollary 1.2, where the additional (G) refers to

the case where the SDE comprises a Wiener process.

These results are to be compared with the results of Jacod et al. JKMP05 . Here an approximate Euler method is analyzed by means of weak

approximation. In contrast to our investigation, the object of that

article is to compute for a fixed time . Under quite

strong assumptions (for instance, and have to be four times

continuously differentiable and the eights moment of the Lévy process

needs to be finite), they provide error bounds for a numerical scheme

which is based on Monte Carlo simulation of one approximative solution.

In the figure, the two lines quoted as JKMP represent the order of

convergence for general, respectively pseudo symmetrical, Lévy processes.

Additionally to the illustrated schemes, JKMP05 provide an

expansion which admits a Romberg extrapolation under additional assumptions.

We stress the fact that our analysis is applicable to general path

dependent functionals and that our error criterion is the worst case

error over the class of Lipschitz continuous functionals with respect

to supremum norm. In particular, our class contains most of the

continuous payoffs appearing in finance.

We remark that our results provide upper bounds for the inferred error

and so far no lower bounds are known. The worst exponent appearing in

our estimates is which we obtain for Lévy processes with

Blumenthal–Getoor index . Interestingly, this is also the worst

exponent appearing in RubWik03 in the context of strong

approximation of SDEs driven by subordinated Lévy processes.

Agenda

The article is organized as follows. In Section 2, we

introduce a class of multilevel Monte Carlo algorithms together with a

cost function. Here, we also provide the crucial estimate for the mean

squared error which motivates the consideration of the Wasserstein

distance between an approximative and the genuine solution, see (2). Section 3 states the central estimate for the

former Wasserstein distance, see Theorem 3.1. In this

section, we explain the strategy of the proof and the structure of the

remaining article in detail. For the proof, we couple the driving Lévy process with a Lévy process constituted by the large jumps plus a

Gaussian compensation of the small jumps and we write the difference

between the approximative and the genuine solution as a telescoping sum

including further auxiliary processes, see (11) and (12). The individual errors are then controlled in Sections 4 and 5 for the terms which do not depend on the

particular choice of the coupling and in Section 7 for

the error terms that do depend on the particular choice. In between, in

Section 6, we establish the crucial KMT like coupling

result for the Lévy process.

Finally, in Section 8, we combine the approximation

result for the Wasserstein metric (Theorem 3.1) with

estimates for strong approximation of stochastic differential equations

from DerHei10 to prove the main results stated above.

2 Multilevel Monte Carlo

Based on a number of parameters, we define a multilevel Monte Carlo

algorithm : We denote by and natural

numbers and let and denote

decreasing sequences of positive reals.

Formally, the algorithm can be represented as a tuple

constituted by these parameters, and we denote by the set of all

possible choices for .

We continue with defining processes that depend on the latter

parameters. For ease of notation, the parameters are omitted in the

definitions below.

We choose a square matrix such that .

Moreover, for , we let denote the -Lévy martingale

which comprises the compensated jumps of that are larger than

, that is

Here and elsewhere, we denote .

We let be an independent Wiener process (independent

of and ), and consider, for , the

processes as driving processes. Let denote

the solution to

where is given via and the set is

constituted by the random times that

are inductively defined via and

Clearly, is constant on each interval

and one has

(4)

Note that we can write

The multilevel Monte Carlo algorithm—identified with —estimates each expectation

(resp., ) individually by sampling

independently (resp., ) versions of [] and taking the

average. The output of the algorithm is then the sum of the individual

estimates. We denote by a random variable that models

the random output of the algorithm when applied to .

The mean squared error of an algorithm

The Monte Carlo algorithm introduced above induces the mean squared error

when applied to .

For two -valued random elements and , we

denote by the Wasserstein

metric of second-order with respect to supremum norm, that is

(5)

where the infimum is taken over all probability measures on

having first marginal and second

marginal . Clearly, the Wasserstein distance depends

only on the distributions of and .

Now, we get for , that

We set

and remark that estimate (2) remains valid for the worst

case error .

The main task of this article is to provide good estimates for the

Wasserstein metric . The remaining terms on

the right-hand side of (2) are controlled with estimates

from DerHei10 .

The cost function

In order to simulate one pair , we

need to simulate all displacements of of size larger or

equal to on the time interval . Moreover, we need the

increments of the Wiener process on the time skeleton . Then we can construct our

approximation via (4). In the real number model of

computation (under the assumptions described in the Introduction), this

can be performed with runtime less than a multiple of the number of

entries in , see DerHei10 for a

detailed description of an implementation of a similar scheme. Since

we define, for ,

Then supposing that and for , yields that

(7)

Algorithms achieving the error rates of Theorem 1.1

Let us now quote the choice of parameters which establish the error

rates of Theorem 1.1.

In general, one chooses and for

. Moreover, in case (I), for sufficiently large ,

one picks

(8)

where and are appropriate constants that do not depend on

.

In case (II), one chooses

(9)

where again and are appropriate constants. We refer the

reader to the proof of Theorem 1.1 for the error estimates of

this choice.

3 Weak approximation

In this section, we provide the central estimate for the Wasserstein

metric appearing in (2).

For ease of notation, we denote by and two positive

parameters which correspond to and above.

We denote by a square matrix with . Moreover,

we let denote the process constituted by the compensated jumps of

of size larger than , and let be a

-dimensional Wiener process that is independent of and .

Then we consider the solution of the

integral equation

where is given as and , where is, in

analogy to above, the set of random times

defined inductively via and

The process is closely related to from

Section 2 and choosing and ,

implies that and are

identically distributed.

We need to introduce two further crucial quantities: for , let

and .

Theorem 3.1

Suppose that Assumption UE

is valid. There exists a finite constant that depends only on

, and such that for , , and with , one has

and, if , one has

Corollary 3.2

Under Assumption UE,

there exists a constant such that for

all and with , one has

and, in the case where ,

{pf}

Choose and observe that since . Using that , it is straight forward to verify the estimate

with Theorem 3.1.

3.1 Strategy of the proof of Theorem 3.1 and main

notation

We represent as

where is the process which comprises the

compensated jumps of of size smaller than .

Based on an additional parameter , we couple

with . The introduction of the explicit coupling is

deferred to Section 7. Let us roughly explain the idea

behind the parameter .

In classical Euler schemes, the coefficients of the SDE are updated in

either a deterministic or a random number of steps of a given (typical)

length. Our approximation updates the coefficients at steps of order

as the classical Euler method. However, in our case the Lévy

process that comprises the small jumps is ignored for most of the time

steps. It is only considered on steps of order of size .

On the one hand, a large reduces the accuracy of the

approximation. On the other hand, the part of the small jumps has to be

approximated by a Wiener process and the error inferred from the

coupling decreases in . This explains the increasing and

decreasing terms in Theorem 3.1. Balancing and

then leads to Corollary 3.2.

We need some auxiliary processes.

Analogously to and , we let denote the set of

random times defined inductively by and

so that the mesh-size of is less than or equal to .

Moreover, we set .

Let us now introduce the first auxiliary processes.

We set and we consider the solution to the integral equation

(10)

and the process given by

It coincides with for all times in and satisfies

Next, we replace the term by the Gaussian term in the

above integral equations and obtain analogs of and which

are denoted by and . To be more precise,

is the solution to the stochastic

integral equation

and is given via

We now focus on the discrepancy of and . By

the triangle inequality, one has

(11)

Moreover, the second term on the right satisfies

(12)

In order to prove Theorem 3.1, we control the error terms

individually. The first term on the right-hand side of (11) is considered in Proposition 4.1. The third and

fourth term are treated in Propositions 5.1 and 5.2, respectively.

The terms on the right-hand side of (12) are investigated

in Propositions 7.1 and 7.2, respectively.

Note that only the latter two expressions depend on the particular

choice of the coupling of and . Once the

above-mentioned propositions are proved, the statement of Theorem 3.1 follows immediately by combining these estimates and

identifying the dominant terms.

4 Approximation of by

Proposition 4.1

There exists a constant

depending on only such that, for , and with , one has

if , and

(13)

for general .

{pf}

For , we consider , ,

and . The

main task of the proof is to establish an estimate of the form

for appropriate values . Since is finite

(see, for instance, DerHei10 ), then Gronwall’s inequality

implies as upper bound:

We proceed in two steps.

1st step.

Note that

so that

(14)

For , we conclude with the Cauchy–Schwarz inequality that

the second term on the right-hand side is bounded by

.

Certainly, is a (local) martingale with respect to the

canonical filtration, and we apply the Doob inequality together with

Lemma .1 to deduce that

Here and elsewhere, for a multivariate local -martingale

, we denote and denotes the

predictable compensator of the classical bracket process of the th

coordinate of .

Note that and . Consequently,

for a constant that depends only on .

Since and , we get

(15)

for an appropriate constant .

2nd step. In the second step we provide appropriate estimates

for and . The processes

and are independent of the random time . Moreover,

has no jumps in , and we obtain

Similarly, we estimate .

Given , is distributed as the unconditioned Lévy process on the time interval . Moreover, we have on

. Consequently,

and analogously as we obtained (16) we get now that

for a constant . Next, note that, by the

Cauchy–Schwarz inequality, so that we arrive at

Combining this estimate with (15) and (16),

we obtain

In the case where , the statement of the proposition follows

immediately via Gronwall’s inequality.

For general , we obtain the result by recalling that

.

with the convention that the supremum of the empty set is zero. Then

By Proposition 5.1 and Lemma .2, is bounded by a constant that

depends only on .

Consider . By Lévy’s modulus of continuity,

is finite almost surely, so that Fernique’s theorem implies that is finite too.

Consequently,

(17)

The result follows immediately by using that and ruling out the asymptotically negligible terms.

6 Gaussian approximation via Komlós, Major and Tusnády

In this section, we prove

the following theorem.

Theorem 6.1

Let and be a

-dimensional -Lévy martingale whose Lévy measure is supported on . Moreover, we suppose that

for , one has

for any with , and set .

There exist constants depending only on such that the

following statement is true.

For every , one can couple the process

with a Wiener process such that

where is a square matrix with

and .

The proof of the theorem is based on Zaitsev’s generalization Zai98 of the Komlós–Major–Tusnády coupling. In this context, a

key quantity is the Zaitsev parameter: Let be a

-dimensional random variable with finite exponential moments in a

neighborhood of zero and set

for all with integrable expectation.

Then the parameter is defined as

In the latter set, we implicitly only consider ’s for which

is finite on a neighborhood of . Moreover, denotes the covariance matrix of .

{pf*}

Proof of Theorem 6.11st step: First, consider a -dimensional infinitely

divisible random variable with

where the Lévy measure is supported on the ball for

a fixed .

Then

and

We choose with , and observe that for

any with and ,

Hence,

2nd step: In the next step, we apply Zaitsev’s coupling to

piecewise constant interpolations of . Fix and

consider given via

Moreover, we consider a -dimensional Wiener process and its piecewise constant interpolation given

by .

Since is self-adjoint, we find a representation with diagonal and orthogonal. Hence, for

we get

. We denote by the leading and by

the minimal eigenvalue of (or ). Then

is again infinitely divisible and the corresponding Lévy

measure is supported on . By part one, we

conclude that

Now the discontinuities of are i.i.d. with

unit covariance and Zaitsev parameter less than or equal to . By Zai98 , Theorem 1.3,

one can couple the processes and on an appropriate

probability space such that

where are constants only depending on the

dimension .

The smallest eigenvalue of is and, by assumption, . Since

, we get

3rd step:

The general result follows by approximation. First, note that converges as to so that by dominated convergence

Analogously, .

Next, we choose with and we fix such that

We apply the coupling introduced in step 2 and estimate

Straightforwardly, one obtains the assertion of the theorem for

and .

We are now in the position to couple the processes and

introduced in Section 3.1. We adopt again the notation of

Section 3.1.

To introduce the coupling, we need to assume that Assumption UE

is valid, and that , and

are such that .

Recall that is independent of and .

In particular, it is independent of the times in , and given

and we couple the Wiener process with on each interval

according to the coupling provided by Theorem 6.1.

More explicitly, the coupling is established in such a way that, given

, each pair of processes and

is independent of , and the other pairings, and satisfies

(19)

for positive constants and depending only on , see

Theorem 6.1. In particular, by Corollary 6.2,

one has

(20)

for a constant .

Proposition 7.1

Under Assumption UE, there exists a constant depending only

on , and such that for any ,

and with , one has

{pf}

For ease of notation, we write

By construction, and are martingales with respect to

the filtration induced by the processes , ,

and .

Let , ,

and . The proof is similar to

the proof of Proposition 4.1.

Each bracket in the latter formula can be

chosen with respect to a (possibly different) filtration such that the

integrand is predictable and the integrator is a local -martingale.

As noticed before, with respect to the canonical filtration

one has . Moreover, we have with

respect to the enlarged filtration ,

where .

Note that two discontinuities of are at least

units apart and the integrands of the last two integrals in

(7) are constant on so that altogether

Combining the latter two estimates with (7) and applying

Gronwall’s inequality yields the statement of the proposition.

Proposition 7.2

There exists a constant

depending only on and such that

{pf}

Note that

Similar as in the proof of Proposition 5.2, we apply

Lemma .4 to deduce that

(23)

Next, we estimate . Recall that conditional on ,

each pairing of and

is coupled according to

Theorem 6.1, and individual pairs are independent of each other.

Let us first assume that the times in are deterministic with

mesh smaller or equal to . We denote by the number of

entries of which fall into , and we denote,

for , . By (7) and the Markov inequality, one has, for ,

Let now , and . Then for

so that

Note that the upper bound depends only on the number of entries in

, and, since is uniformly

bounded by , we thus get in the general random

setting that

Together with Lemma .2, this gives the appropriate upper

bound for the first summand in (7).

We consider a multilevel Monte Carlo algorithm

partially specified by and for

. The maximal index and the number of

iterations are fixed explicitly below in

such a way that and .

Recall that

see (2). We control the Wasserstein metric via

Corollary 3.2. Moreover, we deduce from DerHei10 , Theorem 2, that there exists a constant that depends only

on and such that, for ,

and

Consequently, one has

(24)

in the general case, and

in the case where .

Note that . With Lemma .3, we conclude that so that . Hence, we can bound from above by a multiple of in (24) and (8).

By Lemma .3, we have as

. Moreover, in the case with general and

, we have . Hence, in case (I), there exists a constant such that

(26)

Conversely, in case (II), i.e. , the term

is negligible in (24),

and we get

(27)

for an appropriate constant .

Now, we specify in dependence on a positive

parameter with . We set

for and conclude that, by (32),

For a positive parameter , we choose as the

maximal integer with . Here, we

suppose that is sufficiently large to ensure the existence of

such a and the property .

Then

. Since , we conclude that

It remains to consider case (II). Here, (27) and (8) yield

Next, let such that . Again we let be a positive parameter which is assumed to be

sufficiently large so that we can pick as the maximal natural

number larger than and satisfying . Then,

by (31),

We fix or in the case where , and note that, by definition of ,

is finite. We consider . For , one has

where .

Hence, we find a decreasing and invertible function that dominates and satisfies for . Then for , one has

for and we are in the

position to apply Theorem 1.1: In the first case, we get

In the second case, we assume that and obtain

so that

These estimates yield immediately the statement of the corollary.

Appendix

Lemma .1

Let be a previsible process with state space , let be a square integrable -valued Lévy

martingale and denote by the process given via

where denotes the predictable compensator

of the classical bracket process for the th coordinate of . One

has, for any stopping time with finite expectation , that is a uniformly square integrable martingale

which satisfies

The statement of the lemma follows from the Itô isometry for Lévy

driven stochastic differential equations. See, for instance, DerHei10 , Lemma 3, for a proof.

Lemma .2

The processes and introduced in Section 3.1 satisfy

where is a constant that depends only on .

{pf}

The result is proven via a standard Gronwall inequality type argument

that is similar to the proofs of the above propositions. It is

therefore omitted.

Lemma .3

Let , and

be an invertible and decreasing function such that, for ,

Then

(31)

for all .

Moreover, there exists a finite constant depending only on

such that for all with one has

for all sufficiently large . This implies that there exists a

finite constant depending only on such that for all

with one has

For general, one has

Moreover,

\upqed

Lemma .4

Let and denote a filtration.

Moreover, let, for , and denote nonnegative

random variables such that

is -measurable, and is -measurable

and independent of . Then one has

(2){barticle}[author]

\bauthor\bsnmAsmussen, \bfnmS.\binitsS. and \bauthor\bsnmRosiński, \bfnmJ.\binitsJ.

(\byear2001).

\btitleApproximations of small jumps of Lévy Processes with a

view towards

simulation.

\bjournalJ. Appl. Probab.

\bvolume38

\bpages482–493.

\bidmr=1834755

\endbibitem

(4){barticle}[author]

\bauthor\bsnmCohen, \bfnmS.\binitsS. and \bauthor\bsnmRosiński, \bfnmJ.\binitsJ.

(\byear2007).

\btitleGaussian approximation of multivariate Lévy processes with

applications to simulation of tempered stable processes.

\bjournalBernoulli

\bvolume13

\bpages195–210.

\bidmr=2307403

\endbibitem

(5){barticle}[author]

\bauthor\bsnmCreutzig, \bfnmJ.\binitsJ.,

\bauthor\bsnmDereich, \bfnmS.\binitsS.,

\bauthor\bsnmMüller-Gronbach, \bfnmT.\binitsT. and \bauthor\bsnmRitter, \bfnmK.\binitsK.

(\byear2009).

\btitleInfinite-dimensional quadrature and approximation of distributions.

\bjournalFound. Comput. Math.

\bvolume9

\bpages391–429.

\bidmr=2519865

\endbibitem

(6){bunpublished}[author]

\bauthor\bsnmDereich, \bfnmS.\binitsS. and \bauthor\bsnmHeidenreich, \bfnmF.\binitsF.

(\byear2009).

\btitleA multilevel Monte Carlo algorithm for Lévy driven stochastic

differential equations.

\bnotePreprint.

\endbibitem

(7){bincollection}[author]

\bauthor\bsnmGiles, \bfnmM. B.\binitsM. B.

(\byear2008).

\btitleImproved multilevel Monte Carlo convergence using the Milstein

scheme.

In \bbooktitleMonte Carlo and Quasi-Monte Carlo Methods 2006\bpages343–358.

\bpublisherSpringer, \baddressBerlin.

\bidmr=2479233

\endbibitem

(8){barticle}[author]

\bauthor\bsnmGiles, \bfnmM. B.\binitsM. B.

(\byear2008).

\btitleMultilevel Monte Carlo path simulation.

\bjournalOper. Res.

\bvolume56

\bpages607–617.

\bidmr=2436856

\endbibitem

(9){barticle}[author]

\bauthor\bsnmHeinrich, \bfnmS.\binitsS.

(\byear1998).

\btitleMonte Carlo complexity of global solution of integral equations.

\bjournalJ. Complexity

\bvolume14

\bpages151–175.

\bidmr=1629093

\endbibitem

(12){bbook}[author]

\bauthor\bsnmKloeden, \bfnmP. E.\binitsP. E. and \bauthor\bsnmPlaten, \bfnmE.\binitsE.

(\byear1992).

\btitleNumerical Solution of Stochastic Differential Equations.

\bseriesApplications of Mathematics (New York)

\bvolume23.

\bpublisherSpringer, \baddressBerlin.

\bidmr=1214374

\endbibitem

(13){barticle}[author]

\bauthor\bsnmKomlós, \bfnmJ.\binitsJ.,

\bauthor\bsnmMajor, \bfnmP.\binitsP. and \bauthor\bsnmTusnády, \bfnmG.\binitsG.

(\byear1975).

\btitleAn approximation of partial sums of independent RV’s

and the

sample DF. I.

\bjournalZ. Wahrsch. Verw. Gebiete

\bvolume32

\bpages111–131.

\bidmr=0375412

\endbibitem

(14){barticle}[author]

\bauthor\bsnmKomlós, \bfnmJ.\binitsJ.,

\bauthor\bsnmMajor, \bfnmP.\binitsP. and \bauthor\bsnmTusnády, \bfnmG.\binitsG.

(\byear1976).

\btitleAn approximation of partial sums of independent RV’s, and

the sample

DF. II.

\bjournalZ. Wahrsch. Verw. Gebiete

\bvolume34

\bpages33–58.

\bidmr=0402883

\endbibitem

(15){barticle}[author]

\bauthor\bsnmNovak, \bfnmE.\binitsE.

(\byear1995).

\btitleThe real number model in numerical analysis.

\bjournalJ. Complexity

\bvolume11

\bpages57–73.

\bidmr=1319050

\endbibitem

(16){bbook}[author]

\bauthor\bsnmProtter, \bfnmP.\binitsP.

(\byear2005).

\btitleStochastic Integration and Differential Equations,

2nd ed.

\bseriesStochastic Modelling and Applied Probability

\bvolume21.

\bpublisherSpringer, \baddressBerlin.

\bidmr=2273672

\endbibitem

(18){barticle}[author]

\bauthor\bsnmRubenthaler, \bfnmS.\binitsS.

(\byear2003).

\btitleNumerical simulation of the solution of a stochastic differential

equation driven by a Lévy process.

\bjournalStochastic Process. Appl.

\bvolume103

\bpages311–349.

\bidmr=1950769

\endbibitem

(19){barticle}[author]

\bauthor\bsnmRubenthaler, \bfnmS.\binitsS. and \bauthor\bsnmWiktorsson, \bfnmM.\binitsM.

(\byear2003).

\btitleImproved convergence rate for the simulation of stochastic differential

equations driven by subordinated Lévy processes.

\bjournalStochastic Process. Appl.

\bvolume108

\bpages1–26.

\bidmr=2008599

\endbibitem

(21){barticle}[author]

\bauthor\bsnmTalay, \bfnmD.\binitsD. and \bauthor\bsnmTubaro, \bfnmL.\binitsL.

(\byear1990).

\btitleExpansion of the global error for numerical schemes solving stochastic

differential equations.

\bjournalStochastic Anal. Appl.

\bvolume8

\bpages483–509.

\bidmr=1091544

\endbibitem

(22){barticle}[author]

\bauthor\bsnmZaitsev, \bfnmA. Yu.\binitsA. Y.

(\byear1998).

\btitleMultidimensional version of the results of Komlós, Major and

Tusnády for vectors with finite exponential moments.

\bjournalESAIM Probab. Statist.

\bvolume2

\bpages41–108.

\bidmr=1616527

\endbibitem