Bayesian inference for a class of latent Markov models for categorical longitudinal data

Abstract

We propose a Bayesian inference approach for a class of latent Markov models. These models are widely used for the analysis of longitudinal categorical data, when the interest is in studying the evolution of an individual unobservable characteristic. We consider, in particular, the basic latent Markov, which does not account for individual covariates, and its version that includes such covariates in the measurement model. The proposed inferential approach is based on a system of priors formulated on a transformation of the initial and transition probabilities of the latent Markov chain. This system of priors is equivalent to one based on Dirichlet distributions. In order to draw samples from the joint posterior distribution of the parameters and the number of latent states, we implement a reversible jump algorithm which alternates moves of Metropolis-Hastings type with moves of split/combine and birth/death types. The proposed approach is illustrated through two applications based on longitudinal datasets.

Key words: Bayes factor; Dirichlet distribution; hidden Markov models; reversible jump algorithm.

1 Introduction

The class of latent Markov (LM) models was introduced by Wiggins, (1955, 1973) for the analysis of categorical longitudinal data. These models are specially tailored to study the evolution of an individual characteristic which is not directly observable. The basic LM formulation is similar to that of hidden Markov (HM) models for time series data (MacDonald and Zucchini, , 1997); in fact, a latent Markov chain, typically of first order, is used to represent the evolution of the latent characteristic over time. Moreover, the response variables observed at the different occasions are assumed to be conditionally independent given this chain (assumption of local independence). The basic idea behind this assumption is that the latent process fully explains the observable behavior of a subject. Furthermore, the latent state to which a subject belongs at a certain occasion only depends on the latent state at the previous occasion. An LM model may also be seen as an extension of the latent class (LC) model (Lazarsfeld and Neil, , 1968; Goodman, , 1974), in which the assumption that each subject belongs to the same latent class throughout the survey is suitable relaxed.

Typical applications of LM models are in studies of the human behaviors and conditions in health, education, sociology, and criminology. These models have also been adopted in economics to study the job market or customer’s choice problems. In addition to Wiggins, among the first authors dealing with LM models, it is also worth mentioning Van de Pol and De Leeuw, (1986), Van de Pol and Langeheine, (1990), Collins and Wugalter, (1992), and Langeheine and Van de Pol, (1994). For a complete review of the state of art of the LM models, see Bartolucci et al., (2010).

The basic LM model, relying on a homogenous Markov chain, has several extensions based on parameterizations that allow us to include hypotheses and constraints of interest. Generally speaking, these parameterizations may concern the conditional distribution of the response variables given the latent process (measurement model), and/or the distribution of the latent process (latent model). An example of an LM model based on constraints on the measurement model is given by the LM Rasch model (Bartolucci et al., , 2008), which is a generalization of the model introduced by Rasch, (1961) allowing each subject to evolve in his/her ability level. About the latent model, the most interesting constraints may be expressed on the transition matrix. In particular, transitions between two given states may be excluded, and/or certain elements of the transition matrix may be constrained to be equal (see, among others, Bartolucci, , 2006; Vermunt et al., , 1999). These parametrizations may also be exploited to include individual covariates in the measurement or in the latent model. The case of covariates included in the measurement model was dealt with by Bartolucci and Farcomeni, (2009) among others, whereas the case of covariates included in the latent model, so that they affect the initial and the transition probabilities of the Markov chain, was dealt with by Vermunt et al., (1999) and Bartolucci et al., 2007b . In the present paper, we focus on LM models with constraints and individual covariates included in the measurement model only.

In the frequentist approach, estimation of the parameters of an LM model is typically based on the maximum likelihood approach through the Expectation -Maximization (EM) algorithm (Baum et al., , 1970; Dempster et al., , 1977), whose implementation makes use of suitable recursions. As typically happens for latent variable models, the likelihood function of an LM model may be multimodal, and the search of the global maximum may be cumbersome, also due to the slowness to converge of the EM algorithm. Moreover, this kind of literature has not still provided a commonly accepted criterion for formal assessment of the number of the states of the latent chain, although information criteria are typically used. We refer, in particular, to the Akaike Information Criterion (AIC), see Akaike, (1973), and the Bayesian Information Criterion (BIC), see Schwarz, (1978). On the other hand, in the Bayesian inference approach, parameter estimation does not suffer from the problem of multimodality of the likelihood and model selection is well principled. Obviously, the condition to apply this type of inference is that one is able to draw samples from the joint posterior distribution of the model parameters and the number of latent states.

In this paper, we propose a Bayesian inference approach for the basic LM model and its extended versions based on suitable parametrizations of the conditional response probabilities given the latent states. These parametrizations may be used to formulate hypotheses of interest or include individual covariates. The approach is based on a system of priors that we propose following the approach for HM models of Cappé et al., (2005) and Spezia, (2010). Instead of formulating the prior distributions directly on the initial and transition probabilities of the Markov chain, we formulate these distributions on unnormalized versions of these probabilities. In particular, we assume that each unnormalized initial and transition probability a priori has an independent Gamma distribution with suitable hyperparameters. This system of priors considerably facilitates Bayesian model estimation from the practical point of view, while being equivalent to a system of priors based on Dirichlet distributions on the normalized probabilities.

Under the above system of priors, we estimate the model parameters and select the number of latent states through a reversible jump (RJ) algorithm (Green, , 1995). As is well known, this is a Markov chain Monte Carlo (MCMC) algorithm which represents an extension of the Metropolis-Hastings algorithm (Metropolis et al., , 1953; Hastings, , 1970) that allows us to simulate samples from the posterior distribution when the parameter space has varying dimension. Our implementation of the RJ algorithm follows that proposed by Richardson and Green, (1997) for Bayesian estimation of finite mixture models and that of the RJ algorithm of Robert et al., (2000) for estimation of HM models. In particular, this implementation is based on a series of transdimensional moves (i.e., split/combine and birth/death moves), which allow us to change the number of latent states. These moves are alternated with moves of MH type to draw samples from the posterior distribution of the model parameters, when the same number of latent states is held fixed.

The paper is organized as follows. Section 2 illustrates the basic LM model for univariate and multivariate categorical longitudinal data, whereas its extensions are discussed in Section 3. The proposed system of priors is illustrated in Section 4. In Section 5 we describe the RJ algorithm to draw samples for the posterior distribution of the model parameters and the number of latent states. Finally, two applications are illustrated in Section 6. These applications are based on a dataset about marijuana consumption and a dataset about female labour participation. Finally, in Section 7 we draw main conclusions about the proposed approach.

2 Basic latent Markov model

We introduce the preliminary concepts about the basic LM model for categorical longitudinal data, in which the conditional distribution of each response variable given the corresponding latent variable and the initial and transition probabilities of the latent process are unconstrained.

2.1 Formulation of univariate responses

In the univariate case, let , denote a sequence of categorical response variables with levels or categories, coded from 0 to , independently observed over subjects, that correspond to repeated measurements on the same subject at different occasions.

The main assumption underlying the basic LM model is that of local independence, i.e. for every subject the response variables are conditionally independent given a latent process . This latent process is assumed to follow a first-order Markov chain with state space . Then, for all , the latent variable is conditionally independent of given .

Parameters of the model are the conditional response probabilities , the initial probabilities , and the transition probabilities . Note that the latent process is time homogeneous, so that the transition probabilities do not depend on , moreover the initial probabilities are completely unconstrained. Furthermore, all these probabilities do not depend on since, in its basic version, the model does not account for individual covariates.

The assumptions above imply that the distribution of may be expressed as

where . Moreover, the conditional distribution of given may be expressed as

and, consequently, for the manifest distribution of we have

| (1) | |||||

where . In order to efficiently compute we can use a forward recursion (Baum et al., , 1970), for obtaining for . The recursion is as follows: given , , the t- iteration consists of computing

starting with . We then have,

The above recursion may be efficiently implemented using the matrix notation, and let where is a column vector of ones of suitable dimension and is a column vector with elements . The recursion is then expressed as:

| (2) |

with denoting the initial probability vector, denoting the conditional probability vector and denoting the transition probability matrix.

Finally, for an observed sample of subjects, let denote the observed response vector provided by subject , the model likelihood may be formulated as , where is the vector of all model parameters arranged in a suitable way.

2.2 Multivariate version

In the multivariate case, we observe a vector of response variables, denoted by , for every subject and occasion , with and . Each response variable has categories, , coded from 0 to . Moreover, all responses provided by subject are collected in the vector . The assumption of local independence is usually formulated by also requiring that the elements of each vector are conditional independent given .

The model assumptions imply that

| (3) |

where is made of the subvectors and

with , , , . The manifest probability has the same expression as in (1), with computed as in (3), and it may be computed by exploiting the recursion rule, along similar line as in (2). The likelihood has the same expression as in the univariate categorical data.

3 Constrained and extended versions of the basic model

In the basic LM model outlined in the previous section, all the probabilities are completely unconstrained. There are two generalizations which may be of interest and commonly arise in applications. First, we may put restrictions on the parameter space, in order to give a more parsimonious and easily interpretable model. Secondly, we may have observed covariates together with the outcomes. Both generalizations may concern either the distribution of the response variables (i.e., the measurement model) or the distribution of the latent process (i.e., the latent model). For a more detailed description see Bartolucci et al., (2010).

3.1 Constrained versions

We discuss here only the constraints on the measurement model in order to parameterize the conditional response probabilities. In the univariate case a sensible constraint may be

| (4) |

This constraint corresponds to the hypothesis that the distribution of the response variables only depends on the corresponding latent variable and there is no dependence of this distribution on time.

Other interesting constraints may be expressed by

| (5) |

where , with being a suitable link function, being a design matrix and being a vector of parameters.

In the case of binary response variables, we can parameterize the conditional probabilities through the logit link function . With response variables having more than two categories, a natural choice is that of multinomial logit link function, so that . However when the response variables have an ordinal nature, global or continuation type logits are more suitable; see Bartolucci, (2006). For instance, in the case of binary variables, by assuming that

we can formulate a LM version of the Rasch model (Rasch, , 1961), which finds a natural application in psychological and educational assessment. In this case, the parameters are interpreted as ability levels.

3.2 Extended versions based on the inclusion of individual covariates

As discussed above, the covariates can be included both in the measurement model and in the latent model. In the former case, the conditional distribution of the response variables given the latent states may be parameterized by generalized logits. This parametrization recalls that used in (5), for the univariate case, and in (7), for the multivariate case, to formulate the constraints on the measurement models. Note that, using this formulation, the assumption of local independence is relaxed by allowing association between the response variables observed at the same occasion even conditional on the latent state.

About the model interpretation, when the covariates are included in the measurement model, the latent process is seen as a way to account for the unobserved heterogeneity between subjects. The advantage with respect to a standard random effect or latent class model with covariates is that we admit that the effect of unobservable covariates could be non constant over time, but it could have its own dynamics.

When the covariates influence initial and transition probabilities of the latent process, we suppose that the response variables measure and depend on the latent variable (e.g. the quality of life), which may evolves over time. In such a case, the main research interest is in modeling the effect of covariates on this latent variable distribution (Bartolucci et al., , 2009).

In this paper, we deal with a model very similar to that proposed by Bartolucci and Farcomeni, (2009), that is a multivariate extension of the basic LM model in which the conditional distribution of the response variables depends on the individual covariates. This extension is illustrated in the following.

Let , denote the vector of individual covariates for subject at occasion . Following the formulation of Bartolucci and Farcomeni, (2009), we parameterize the conditional distribution of the response variables given the latent process by a multivariate marginal link function (Bartolucci et al., 2007a, ). In particular, let denote the column vector having elements for all the possible configurations of the responses. This probability vector is parameterized by marginal logits and marginal log-odds ratios which are collected in the vector that may be simply expressed as

| (8) |

where and are appropriate matrices whose construction is described in Bartolucci et al., 2007a ; see also Colombi and Forcina, (2001). Logits and log-odds ratios may be of local, global, or continuation type; the choice is driven by the nature of the response variables, essentially ordinal or non-ordinal.

To relate the above marginal effects to the covariates, we assume that

| (9) |

where is the subvector of containing the logits and is the subvector containing the log-odds ratios. Moreover, is a suitable design matrix defined on the basis of , whereas and are vectors of parameters. Note that , , may be seen as support points, corresponding to each latent states, for individual random effects which are time-varying.

As discussed above, the resulting model allows for unobserved heterogeneity beyond individual covariates; moreover, the effect of the first is admitted to be time-varying. This extension is of interest when we want to investigate on the direct effect of the covariates on the response variables.

4 Bayesian setting

The basic LM model and its extended versions are considered here in the Bayesian setting; at this aim, we introduce the system of priors elicited for the dimension and the unknown model parameters.

4.1 Basic latent Markov model

In specifying the prior distributions for the initial and transition probabilities we follow the approach of Cappé et al., (2005) and Spezia, (2010), who exploit a transformation (based on unnormalized probabilities) which facilitates the estimation. In particular, we let where , are assumed a-priori independent, with distribution for ; similarly, where , are assumed a-priori independent, with distribution for . The are not identified, but this transformation facilitates the MCMC moves, since it relaxes the constraints on the initial and transition probabilities (see also Cappé et al., , 2003). Typically, the hyperparameters are chosen as , , and , , where is the indicator function. With the latter choice, as usual in LM models, the probability of persistence is greater than the probability of transition. This system of priors results equivalent to a system based on Dirichlet distributions. In the following, we denote by and the vector and the matrix with elements and , respectively.

We also consider the same reparametrization for the conditional response probabilities, through the vectors with elements , as . We assume an independent Gamma prior distribution for , choosing for , , .

Finally, for the parameter we define a discrete Uniform prior distribution between 1 and , where is the maximum number of states we admit a priori. Usually is greater than the most complex model that could be visited by the algorithm; we choose .

The above setting can be easily extended to the case of multivariate categorical data.

4.2 Constrained and extended versions

In the constrained versions expressed by (5) and (7), once defined a system of priors for the initial and transition probabilities and for the number of latent states , as in Section 4.1, it only remains to choose a prior distribution for the generic vector of parameters . It is natural to assume , where and are respectively a vector of zeros and an identity matrix of suitable dimension. The choice of depends on the constraints adopted and on the context of application. Typically, .

About the model based on assumption (9), which allows for the inclusion of individual covariates, we assume that the vectors are a-priori independent with distribution . Similarly, we assume that and . Also in this case we assume . Again, concerning the initial and transition probabilities and the number of latent states, are still valid the prior assumptions defined in Section 4.1.

5 Reversible jump algorithm

In this paper, we propose a framework for Bayesian inference on LM models, implementing a RJ algorithm which draws samples from the posterior distribution of the parameters and simultaneously from that of the number of latent states. The proposed framework has many points in common with those developed for HM models (Robert et al., , 2000; Spezia, , 2010) about the specification of the priors and/or the structure of the estimation algorithm.

In particular, the proposed algorithm is based on two different types of move. The moves of the first type are aimed at updating the parameters of the current model given the number of states; those of the second type also allow us to update the number of states. In more detail, the algorithm performs the following steps:

- Step 1:

-

Metropolis-Hastings (MH) move in order to draw, given the current , the parameters from their posterior distributions.

- Step 2:

-

split/combine move (each proposed with probability 0.5). The split proposal consists of choosing a state at random and splitting it into two new ones. The corresponding parameters are split using auxiliary variables. In the combine move a pair of states is picked at random and merged into a new one, so as to recover the values of the auxiliary variables of the split move.

- Step 3:

-

birth/death move (each proposed with probability 0.5). The birth move is accomplished by generating a new state and drawing the new parameters from their respective priors. In the death move a state is selected at random and then deleted along with the corresponding parameters.

This structure closely recalls the one of the RJ algorithm for mixture models proposed by Richardson and Green, (1997), although the birth and death moves are not limited to the empty components (see Spezia, , 2010; Cappé et al., , 2005, Ch. 13). Moreover, in the first type of move, the simulation from the posterior density is accomplished through the MH step instead of implementing a Gibbs sampler. Furthermore, our implementation does not simulate the latent process since it directly exploits the manifest (or marginal) distribution, which is computed by a suitable recursion (Baum et al., , 1970). We decide to simulate from the posterior distribution of the parameters using random walk MH moves without completion because the resulting algorithm is easier to implement within the RJ framework. Moreover, as pointed out in Celeux et al., (2000), the Gibbs sampler is not always appropriate for sampling from a multimodal distribution, because it is not always able to explore the posterior surface and to escape local mode (see also Jasra et al., , 2005). Finally, instead of passing through each step deterministically, we choose to randomly select, at each iteration, among split/combine and birth/death step with probability equal to 0.5. The MH step is always performed.

A well-known problem occurring in Bayesian mixture modeling, is the label switching problem that can be seen as the non-identifiability of the component due to the invariance of the posterior distribution to the permutations in the parameters labeling. Several solutions have been proposed in the literature; in particular, we cite: artificial identifiability constraints (Diebolt and Robert, , 1994; Richardson and Green, , 1997) and the related random permutation sampling (Frühwirth-Schnatter, , 2001), the relabeling algorithm (Celeux, , 1998; Stephens, , 2000) and the label invariant loss function methods (Celeux et al., , 2000; Hurn et al., , 2003). For a general review see Jasra et al., (2005) and Spezia, (2009). Since this issue is of great complexity, we decide to use relabeling techniques retrospectively, by post-processing the RJ output as in Marin et al., (2005). In particular, the label switching is managed by sorting the MCMC sample of the draw obtained at the end of the iterations on the basis of the permutation of the states which minimizes the distance from the posterior mode. More details are given in Section 5.1.

5.1 The algorithm

We now describe in more detail the three steps of the RJ algorithm which allow for the estimates of the model parameters and the unknown number of states . Concerning the constrained and the extended versions, we only illustrate these steps for the multivariate LM model with covariates formulated on the basis of assumption (9); the steps for LM versions based on different assumptions may be easily derived.

Step 1- Metropolis Hastings move

In the first step of the algorithm, with fixed , the model parameters are drawn from their posterior distribution on the basis of separate multiplicative random proposals. About the unnormalized initial, transition and conditional probabilities, we consider a logarithmic transformation of the positive quantities , and , in order to mapped them onto the real line. The proposed moves are:

-

1.

with for .

-

2.

with for .

-

3.

-

(a)

For the basic LM model,

-

-

with for .

-

-

-

(b)

For the extended model with covariates,

-

-

with for .

-

-

with for .

-

-

with , for .

-

-

-

(a)

Note that , and are the dimension of the vectors , and , i.e. respectively, the number of marginal logits, the number of parameters, and the number of log-odds ratios. The acceptance probabilities of the proposed values, for both versions, include the Jacobian that arises because we work with a log-scale transformation. This is given by , and , respectively.

Step 2 - split/combine move

Suppose that the current state of the chain is ; in this step we choose between split and combine move with probability 0.5. Obviously, when , we always propose a split move, while when we propose a combine move.

In the split move a state is randomly selected and split it into two new ones, and . The corresponding parameters are split as follows:

-

1.

Split as

-

2.

Split column of as

-

3.

Split row of as

-

4.

Split as

with and .

-

5.

-

(a)

For the basic LM model, split as

with for .

-

(b)

For the extended model with covariates, perturbate as

-

(a)

It is worth noting that the densities of the proposals are identical, as and have the same distribution and likewise for and and and respectively (here subscripts on these variables are omitted), so the symmetry constraints are satisfied.

In the reverse combine move two distinct states, and , are picked at random and merged into a single state , so as to preserve reversibility:

-

1.

.

-

2.

for .

-

3.

for .

-

4.

.

-

5.

-

(a)

For the basic LM model for .

-

(b)

For the extended model with covariates for .

-

(a)

Note that the split/combine move does not influence the parameters and as they are not affected by the number of states.

The split move is accepted with probability whereas the combine move is accepted with probability . In the basic LM model, can be computed as

When we deal with the model assumption (9), the above formula becomes

In both the equation, represents the likelihood computed via the forward algorithm, while is the prior distribution of all model parameters. Moreover, and are respectively the probabilities to split a specific component out of available ones, and to combine one of possible pairs of components. We also note that cancels out and that the Uniform variables involved have densities equal to unity. The factorials and the coefficient 2 arise from combinatorial reasoning related to label switching. is the Jacobian of the transformation from to , which is the product of five determinants , , , and or .

Step 3 - birth/death move

This step is performed with probability 0.5, along similar lines as split/combine move.

The birth move is accomplished by generating a new state, denoted by , drawing the new parameters from their respective priors. The remaining parameters are simply copied to the proposed new state . In the death move a state is selected at random and then deleted along with the corresponding parameters.

The acceptance probability of the birth move is , where may be expressed by the following formulas

that can be applied to the basic LM model and to the model with covariates, respectively.

The death move is accepted with probability . Since the proposal densities are equal to the priors of the corresponding parameters, and because the components in remain the same in , many terms cancel out in the expression above. Note that .

Post-processing method

At the end of the iterations of the algorithm, we select the model with the highest posterior probability of the number of state , i.e. the model that has been visited most often by the RJ algorithm, after discarding the burn-in period. After that we collect the MCMC sample of the draws obtained when the best model was visited. Then it is possible to compute the ergodic averages of those parameters, as and , that are not affected by the number of states. Concerning the remaining model parameter estimates, and in order to tackle the label switching problem, we need to apply the post-processing method, as in Marin et al., (2005). In particular, for a sample drawn from the posterior distribution of the parameters of a model with latent states, the post-processing method is based on the following steps:

-

1.

compute the posterior mode as:

-

2.

Let denote the vector with elements permuted according to certain permutation of the latent states and let denote the space of all possible permutations.

-

3.

For , substitute with the corresponding permutation which minimizes the distance from , i.e.,

6 Empirical illustrations

To illustrate the Bayesian inference for the class of LM models proposed in this paper, we describe the analysis of two real datasets. The first one concerns the use of marijuana among young people and it is analyzed using the basic LM model and a model with constraints on the conditional response probabilities. The second one is a dataset extracted from the database derived from the Panel Study of Income Dynamics, and is about fertility and female participation to the labor market. In this case, to fit the data, we use the more complex LM model based on assumption (9), which allows for the presence of covariates.

6.1 Marijuana consumption dataset

The marijuana consumption dataset has been taken from five annual waves (1976-1980) of the National Youth Survey (Elliott et al., , 1989) and is based on respondents who were aged 13 years in 1976. The use of marijuana is measured through ordinal variables, one for each annual wave, with levels coded as 0 for never in the past year, 1 for no more than once a month in the past year and 2 for more than once a month in the past year. We want to explore whether there is an increase of marijuana use with age.

As illustrated by Vermunt and Hagenaars, (2004), a variety of models may be used for the analysis of this dataset but a LM approach is desirable for its flexibility and easy interpretation (see Bartolucci, , 2006).

In our implementation, we used the system of priors outlined in Section 4.1 with , , and , for the unnormalized initial and transition probabilities and for the conditional response probabilities, respectively; was set equal to 10. Moreover, in the MH step, the parameters were updated for fixed through an increment random walk proposal on each , , and , with , and . The sampler parameters were tuned so as to achieve acceptance rates in the range for all values . In the split move we used and as parameters of the Gamma distributions. We also decided to simplify the model using constraint (4), in which the conditional probabilities were assumed to be time homogeneous, i.e. and analogously, . Finally, the algorithm ran for iterations with a burn-in of iterations. The starting values were randomly chosen. The acceptance rates are illustrated in Table 1. Concerning the transdimensional moves, we note that the acceptance rates are a bit lower than desired, but if we consider that split/combine or birth/death moves only involve a change of model dimension, and all the other parameters are updated in each sweep, they are not too low (see Robert et al., , 2000, for comparable results).

| Performed | Accepted | % Accepted | |

|---|---|---|---|

| MH with fixed k | 1,000,000 | ||

| Initial probabilities | 209,312 | 20.93 | |

| Transition probabilities | 127,815 | 12.78 | |

| Conditional probabilities | 133,458 | 13.35 | |

| Birth | 250,268 | 2,129 | 0.85 |

| Death | 250,229 | 2,117 | 0.85 |

| Split | 250,107 | 770 | 0.31 |

| Combine | 249,396 | 788 | 0.32 |

The estimated posterior probabilities are 0.689, 0.277, 0.031, 0.002 for and below 0.001 for smaller and larger values of . Hence, the most probable model is that with three latent state, the same as selected by Bartolucci, (2006) using BIC.

In order to face the label switching problem, at the end of all iterations, we post-processed the output as illustrated in Section 5.1. Moreover, to have a clearer interpretation of the results, the MCMC draws were sorted on the basis of the conditional probabilities of the last category of the response variables. Doing this, the last class of the LM model may be interpreted as that of subjects with high tendency to use marijuana. Once the output was post-processed, we estimated the parameters of the model by the ergodic averages, taken over the final 800,000 iterations; the resulting parameter estimates are reported in Table 2. We can see that these results are very similar to that obtained by Bartolucci, (2006) with the EM algorithm.

| 1 | 0.868 | 1 | 0.847 | 0.128 | 0.025 |

|---|---|---|---|---|---|

| 2 | 0.080 | 2 | 0.073 | 0.693 | 0.233 |

| 3 | 0.052 | 3 | 0.016 | 0.065 | 0.919 |

We also tried to put constraints on the distribution of the response variables, so as to give a proper interpretation of the model. We assumed a parametrization for the conditional local logits of any response variable given the latent state:

| (14) |

where may be interpreted as the tendency to use marijuana for a subject in the state and , for , are the cutpoints common to all the response variables. Note that we assumed again the constraint (4), i.e. the distribution of the response variables does not depend on time. The parametrization used here requires the choice of the prior distributions on and , that we assumed to be and , respectively. We considered two choices of the prior parameters, i.e. , for all and , in order to see how the posterior distribution of the number of states changes with different values of the hyperparameters. The sensitivity to prior specification and therefore the choice of the hyperparameters is in fact one of the difficulties in Bayesian modeling, especially when there is little information to be used. We computed the posterior distribution of also considering two different values of the parameters for the transition probabilities, i.e. §§§indicated in Table 3 as and . The prior parameters for the initial probabilities were left unchanged, i.e. for .

In the MH step, the elements of both the parameters and , were updated through a normal random walk proposal, ; moreover in the split move the parameter was split into and , where , with , whereas in the reverse combine move the selected two parameters were combined into . The parameters setting for the unnormalized initial and transition probabilities was the same as in the basic LM model. The results were based on 1,000,000 iterations of the algorithm after a burn-in of 200,000 sweeps.

Table 3 shows the results of the sensitivity analysis to prior specification. We can see that almost all the values of the hyperparameters lead to choose again a model with three latent states, even if the posterior probabilities of are quite different. The first column of the table shows our choice in this application, that it seems to be the more adequate given the prior information we have.

| k | ||||

|---|---|---|---|---|

| 0.000 | 0.000 | 0.000 | 0.000 | |

| 3 | 0.474 | 0.341 | 0.932 | 0.915 |

| 4 | 0.365 | 0.361 | 0.067 | 0.082 |

| 5 | 0.122 | 0.189 | 0.001 | 0.003 |

| 6 | 0.031 | 0.075 | 0.000 | 0.000 |

| 7 | 0.007 | 0.025 | 0.000 | 0.000 |

| 0.001 | 0.010 | 0.000 | 0.000 |

The acceptance rates for the random walk MH move and for the dimension changing moves are illustrated in Table 4. We can see that these rates, for split/combine and birth/death moves, are higher than those achieved in fitting the basic LM model.

| Performed | Accepted | % Accepted | |

|---|---|---|---|

| MH with fixed k | 1,000,000 | ||

| Initial probabilities | 195,551 | 19.56 | |

| Transition probabilities | 129,441 | 12.94 | |

| 176,501 | 17.65 | ||

| 185,274 | 18.53 | ||

| Birth | 250,348 | 5,543 | 2.21 |

| Death | 249,399 | 5,481 | 2.20 |

| Split | 250,199 | 1,611 | 0.64 |

| Combine | 250,054 | 1,677 | 0.67 |

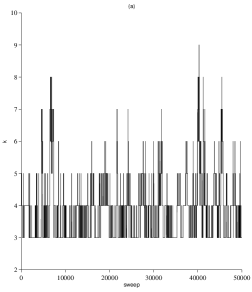

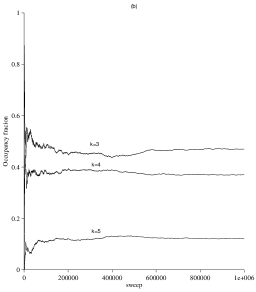

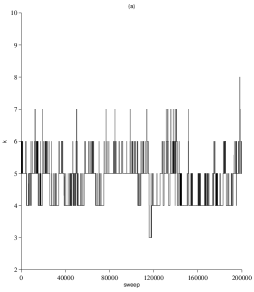

Figure 1 shows the mixing and the stationarity of the algorithm with the plot of the first 50,000 values of after the burn-in, and the plot of the cumulative occupancy fractions for different values of against the number of sweeps. From Figure 1(b) we can see that the burn-in is adequate to achieve stability in the occupancy fractions.

Tables 5 and 6 show the parameter estimates, computed after post-processing the MCMC output. Even in this case, the latent states may be ordered, representing subjects with “no tendency to use marijuana”, “incidental users of marijuana” and “high tendency to use marijuana”.

| 1 | -5.321 | 1 | 0.775 | |||

| 2 | -0.176 | 2 | -1.977 | |||

| 3 | 4.173 |

| 1 | 0.897 | 1 | 0.838 | 0.148 | 0.015 |

|---|---|---|---|---|---|

| 2 | 0.077 | 2 | 0.056 | 0.717 | 0.227 |

| 3 | 0.026 | 3 | 0.027 | 0.058 | 0.915 |

From the results, we can see that most subjects starts with a low tendency to drug consumption but from the estimated marginal probabilities of the latent classes emerge that the tendency to use marijuana increases with age, since the probability of the third class increases across time. From the estimated transition matrix we can see that a large percentage of subjects remains in the same latent class, but around 23% of incidental users switches to the class of high frequency users.

6.2 Analysis of the Panel Study of Income Dynamics dataset

The second dataset analyzed in this paper is very similar to that used by Hyslop, (1999) and by Bartolucci and Farcomeni, (2009). The dataset was extracted from the database derived from the Panel Study of Income Dynamics, which is primarily sponsored by the National Science Foundation, the National Institute of Aging, and the National Institute of Child Health and Human Development and is conducted by the University of Michigan. The database is freely accessible from the website http://psidonline.isr.umich.edu, to which we refer for details.

Our dataset concerns women who were followed from 1987 to 1993. There are two binary response variables: fertility (indicating whether a woman had given birth to a child in a certain year) and employment (indicating whether she was employed). The covariates are race (dummy variable equal to 1 for a black woman), age (in 1986), education (year of schooling), child 1-2 (number of children in the family aged between 1 and 2 years, referred to the previous year), child 3-5, child 6-13, child 14- and income of the husband (in dollars, referred to the previous year).

In analyzing the dataset, the most interesting question concerns the direct effect of the covariates on the response variables. The approach considered here, allows us to separate these effects from the effect of the unobserved heterogeneity by modeling the latter by a latent process. In this way, we admit that the unobserved heterogeneity effect on the response variable is time-varying.

On these data, we fitted a model formulated on the basis of assumption (9) with , where denoting an identity matrix of dimension and the vector includes the covariates indicated previously further to a dummy variable for each year. In particular, the logits may be parameterized as follows:

whereas, for the log-odds ratio we have

We implemented the proposed RJ algorithm with the following parameters setting and initialization. We used the prior distribution defined in Section 4.1 and 4.2 with , and , with . The parameters used for the proposal distributions in the MH move were , , , and . These values allowed us to obtain acceptance rates in the range 0.15-0.30. In the split/combine move we used for the Normal proposal and for the Gamma distributions. The Markov chain was initialized from the maximum likelihood estimation obtained through the EM algorithm, with . Moreover, we ran the RJ algorithm for 1,000,000 iterations discarding the first 200,000 as burn-in.

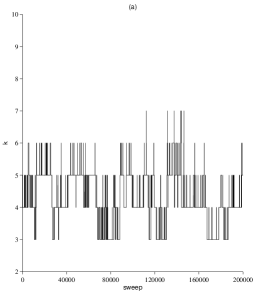

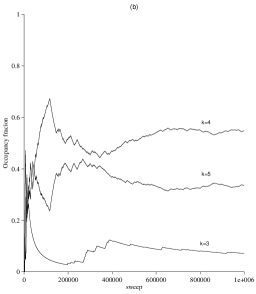

After the burn-in, the algorithm visited five states with posterior probabilities illustrated in Table 7. Table 8 also shows the acceptance rates for the different moves, whereas in Figure 2 and Figure 3 are illustrated the trace of in the first 200,000 iterations, after the burn-in, and the ergodic averages of the model probabilities, for both the choices of the prior parameters, . We can see that the algorithm leads to choose a model with a number of state between 4 and 5. The acceptance rates, especially for the split/combine move, are again a bit low, but this can be due to the complexity of the model.

| k | ||

|---|---|---|

| 0.081 | 0.006 | |

| 4 | 0.554 | 0.298 |

| 5 | 0.320 | 0.580 |

| 6 | 0.044 | 0.107 |

| 0.003 | 0.009 |

| % Accepted | % Accepted | |

| MH with fixed k | ||

| Initial probabilities | 19.21 | 18.64 |

| Transition probabilities | 18.18 | 16.17 |

| 16.13 | 17.71 | |

| 25.34 | 29.37 | |

| Birth | 0.32 | 0.35 |

| Death | 0.33 | 0.36 |

| Split | 0.12 | 0.11 |

| Combine | 0.12 | 0.10 |

In Table 9 we show the estimates of the parameters, collected in vectors and , affecting the marginal logits of fertility and employment and the log-odds ratio between these variables, for and and for and . These estimates are straightforward to compute, through the ergodic averages of the draws obtained when the best model was visited. In Table 10 are also illustrated the same estimates computed by the ergodic means over all the draws (after discarding the burn-in) without limiting these averages to the draws obtained when the selected model was visited. This can be done since the parameters and do no depend by the number of states. In both the tables, we also show the 90%, 95% and 99% posterior credible intervals not containing zero. Note that some covariates have been standardized, before starting the estimation algorithm, for computing purposes.

| Effect | |||||

| Logit fertility | intercept | next table | next table | ||

| race | -0.082 | -0.082 | |||

| age† | 1.434 | * | 1.680 | * | |

| -2.473 | *** | -2.736 | *** | ||

| education† | 0.369 | *** | 0.363 | *** | |

| child 1-2 | -0.019 | -0.010 | |||

| child 3-5 | -0.375 | *** | -0.381 | *** | |

| child 6-13 | -0.673 | *** | -0.683 | *** | |

| child 14- | -0.454 | * | -0.467 | * | |

| income† | 0.051 | 0.057 | |||

| Logit employment | intercept | next table | next table | ||

| race | 0.089 | 0.205 | |||

| age† | -0.780 | -2.016 | |||

| 0.367 | 1.433 | ||||

| education† | 1.093 | *** | 1.510 | *** | |

| child 1-2 | -0.916 | *** | -1.147 | *** | |

| child 3-5 | -0.706 | ** | -0.894 | ** | |

| child 6-13 | -0.259 | -0.377 | |||

| child 14- | 0.363 | 0.354 | |||

| income† | -0.537 | *** | -0.696 | *** | |

| Log-odds ratio | intercept | -1.165 | -2.622 | * | |

| † In standardized form | |||||

| posterior HPD not containing zero | |||||

| posterior HPD not containing zero | |||||

| posterior HPD not containing zero | |||||

| Effect | ||||||

| Logit fertility | intercept | next table | next table | |||

| race | -0.085 | -0.080 | ||||

| age† | 1.339 | 1.725 | ||||

| -2.367 | ** | -2.793 | ** | |||

| education† | 0.364 | *** | 0.367 | *** | ||

| child 1-2 | -0.021 | -0.013 | ||||

| child 3-5 | -0.378 | *** | -0.373 | *** | ||

| child 6-13 | -0.679 | *** | -0.680 | *** | ||

| child 14- | -0.471 | * | -0.449 | |||

| income† | 0.053 | 0.051 | ||||

| Logit employment | intercept | next table | next table | |||

| race | 0.079 | 0,127 | ||||

| age† | -0.849 | -1,182 | ||||

| 0.468 | 0,645 | |||||

| education† | 1.145 | *** | 1,395 | *** | ||

| child 1-2 | -0.870 | ** | -1,151 | *** | ||

| child 3-5 | -0.704 | ** | -0,897 | ** | ||

| child 6-13 | -0.255 | -0,384 | ||||

| child 14- | 0.352 | 0,382 | ||||

| income† | -0.543 | *** | -0,669 | *** | ||

| Log-odds ratio | intercept | -1.594 | * | -2,118 | ||

| † In standardized form | ||||||

| posterior HPD not containing zero | ||||||

| posterior HPD not containing zero | ||||||

| posterior HPD not containing zero | ||||||

On the basis of the estimates of the parameters for the covariates, we can see that the results are very similar both if we take the means of the draws limited to the model of interest or if we take the overall means. Moreover these estimates are not influenced by the prior specification we used. In particular, age seems to have an effect on fertility but not on employment. At this regards we can consider that the women in the sample were aged between 18 and 47, which is a limited range of years if we want to effectively study the effect of aging on the probability of having a job. We also note that the education has a significant effect on both fertility and employment, whereas income of the husband affects only the logit of employment. Moreover, the number of children aged between 1 and 5 years has an effect on the employment while the number of children aged between 3 and 13 years affects the fertility. The log-odds ratio between the two response variables is negative and is significant based on the 90% posterior interval. This result can be interpreted as a negative association between the two response variables, referred to the same year.

In order to estimate the value of the remaining parameters, and in order to face the label switching problem we applied the post-processing algorithm of Marin et al., (2005); moreover, we sorted the output of the algorithm on the basis of the drawn support points . Once the post-processing algorithm has been performed we could compute the estimates of those parameters that are affected by the number of state on the basis of the ergodic averages, after discarding the draws obtained during the burn-in period.

In Table 11 and 12 we show the results of this estimation procedure, through the estimates of the support points (one for the marginal logit of fertility and the other for that of employment) corresponding to each latent state, and the estimated initial probabilities and transition probability matrix, for both the hyperparameters chosen in the prior specification. Though the number of states selected is different, both the specifications lead to the same conclusions. In particular, the latent process can be interpreted as an error component which follows a process that may be seen as a discrete version of an . The support points are in increasing order on the basis of the marginal logit of employment; the latent states may therefore be interpreted as different levels to give birth to a child or to get a job position. For example, the first latent state corresponds to subjects with the highest propensity to fertility and the lowest propensity to employment. Moreover, it is interesting to observe that the transition matrix has an almost symmetric structure, with a large percentage of subjects that remains in the same latent state.

| Support points | |||||||

|---|---|---|---|---|---|---|---|

| Latent state | Fertility | Empl. | Initial prob. | Transition probabilities | |||

| 1 | -1.796 | -4.937 | 0.092 | 0.734 | 0.065 | 0.055 | 0.146 |

| 2 | -1.936 | -3.718 | 0.102 | 0.072 | 0.643 | 0.067 | 0.219 |

| 3 | -2.648 | -0.002 | 0.228 | 0.071 | 0.072 | 0.754 | 0.103 |

| 4 | -2.609 | 5.980 | 0.578 | 0.021 | 0.027 | 0.009 | 0.944 |

| Latent | Support points | Initial | ||||||

|---|---|---|---|---|---|---|---|---|

| state | Fertility | Empl. | prob. | Transition probabilities | ||||

| 1 | -1.902 | -5.461 | 0.084 | 0.553 | 0.063 | 0.090 | 0.060 | 0.234 |

| 2 | -1.965 | -5.117 | 0.103 | 0.043 | 0.754 | 0.050 | 0.052 | 0.101 |

| 3 | -3.180 | 0.174 | 0.194 | 0.048 | 0.052 | 0.684 | 0.163 | 0.053 |

| 4 | -2.117 | 3.542 | 0.090 | 0.187 | 0.081 | 0.059 | 0.555 | 0.117 |

| 5 | -2.634 | 7.786 | 0.530 | 0.022 | 0.014 | 0.005 | 0.021 | 0.939 |

7 Conclusion

In this paper, we proposed a framework for Bayesian inference on a class of LM models for categorical longitudinal data. We considered in particular the basic LM version, in which the latent Markov chain is of first-order and time homogeneous, and some extended versions which include constraints and individual covariates in the measurement model, which corresponds to the conditional distribution of the response variables given the latent states.

The proposed inferential approach is based on a system of priors whose specification follows that adopted by Cappé et al., (2005) and Spezia, (2010) for HM models. In particular, this system of priors is formulated on a transformation of the initial and transition probabilities which is equivalent to a system based on Dirichlet distributions.

With the aim of estimating the model parameters and the number of latent states, we implemented an RJ algorithm that allows us to simultaneously draw samples from the posterior distribution of the parameters and the number of states. The choice of the system of priors leads to an algorithm easier to implement; in particular, the computation of the Jacobian of the transformation from the current value of the parameters to the new value is easier with respect to a system of priors based on Dirchlet distributions. The structure of the proposed RJ algorithm has many points in common with the RJ algorithms for mixture models of Richardson and Green, (1997) and for HM models of Robert et al., (2000). In particular, our algorithm is based on moves of MH type, which update the parameters of the current model given the number of states, and moves of split/combine and birth/death type, aimed at also updating the number of states.

The proposed approach can be extended in several ways and even applied to different LM formulations. We are referring, in particular, to the development of a similar Bayesian framework for the extended versions of the LM model in which individual covariates are included in the latent model. These covariates are then assumed to affect the initial and transition probabilities of the latent Markov chain. This extension would require a different formulation of the priors, based, for instance, on Normal distributions assumed on suitable transformations of these initial and transition probabilities. Natural transformations are based on multinomial logits.

Moreover, it is possible to extend the proposed framework in order to deal with missing responses, that we can assume to be missing at random in the sense of Rubin, (1976). Thus, the missing data mechanism is ignorable for posterior inference. It is possible to make the proposed RJ algorithm able to handle data with missing responses of this type. The missing data can be estimated along with the parameters of the LM model, through the steps of the algorithm.

Other interesting extensions concern the implementation of an algorithm for path prediction, i.e. to predict the sequence of latent states of a subject on the basis of the observed data, and the Bayesian model averaging, in order to estimate parameters with invariable dimension with respect to the number of states (e.g., parameters for the covariates) and for prediction of the responses.

Finally, an aspect that has to be remarked and that requires additional future work, concerns the sensibility of the inferential results on the prior specification. A first analysis has already been done in the two illustrative examples, showing that differences in the prior specification may lead to differences in the estimation of the number of latent states. However, further research is necessary in order to have a more conclusive answer about this issue.

References

- Akaike, (1973) Akaike, H. (1973). Information theory and an extension of the Maximum Likelihood principle. In Petrov, B. and Csaki, F., editors, Second International Symposium on Information Theory, pages 267 –281, Budapest. Akademiai Kiado.

- Bartolucci, (2006) Bartolucci, F. (2006). Likelihood inference for a class of latent Markov models under linear hypotheses on the transition probabilities. Journal of the Royal Statistical Society, Series B, 68:155–178.

- (3) Bartolucci, F., Colombi, R., and A., F. (2007a). An extended class of marginal link functions for modelling contingency tables by equality and inequality constraints. Statistica Sinica, 17:692–711.

- Bartolucci and Farcomeni, (2009) Bartolucci, F. and Farcomeni, A. (2009). A multivariate extension of the dynamic logit model for longitudinal data based on a latent Markov heterogeneity structure. Journal of the American Statistical Association, 104:816–831.

- Bartolucci et al., (2010) Bartolucci, F., Farcomeni, A., and Pennoni, F. (2010). An overview of latent Markov models for longitudinal categorical data. arXiv:1003.2804.

- Bartolucci et al., (2009) Bartolucci, F., Lupparelli, M., and Montanari, G. (2009). Latent Markov model for longitudinal binary data: an application to the performance evaluation of nursing homes. Annals of Applied Statistics, 3:611:636.

- (7) Bartolucci, F., Pennoni, F., and Francis, B. (2007b). A latent Markov model for detecting patterns of criminal activity. Journal Of The Royal Statistical Society, Series A, 170:115–132.

- Bartolucci et al., (2008) Bartolucci, F., Pennoni, F., and Lupparelli, M. (2008). Likelihood inference for the latent Markov Rasch model. In Huber, C., Limnios, N., Mesbah, M., and Nikulin, M., editors, Mathematical Methods for Survival Analysis, Reliability and Quality of Life, pages 239–254. Wiley.

- Baum et al., (1970) Baum, L. E., Petrie, T., Soules, G., and Weiss, N. (1970). A maximization technique occurring in the statistical analysis of probabilistic functions of Markov chains. The Annals of Mathematical Statistics, 41:164–171.

- Cappé et al., (2005) Cappé, O., Moulines, E., and Rydén, T. (2005). Inference in Hidden Markov Models. Springer-Verlag New York, Inc., Secaucus, NJ, USA.

- Cappé et al., (2003) Cappé, O., Robert, C., and Rydén, T. (2003). Reversible jump, birth-and-death and more general continuous time Markov chain Monte Carlo samplers. Journal Of The Royal Statistical Society, Series B, 65:679–700.

- Celeux, (1998) Celeux, G. (1998). Bayesian inference for mixtures: The label-switching problem. In Payne, R. and Green, P., editors, COMPSTAT 98-Proc. in Computational Statistics, pages 227–232. Physica, Heidelberg.

- Celeux et al., (2000) Celeux, G., Hurn, M., and Robert, C. P. (2000). Computational and inferential difficulties with mixture posterior distributions. Journal of the American Statistical Association, 95:957–970.

- Collins and Wugalter, (1992) Collins, L. and Wugalter, S. (1992). Latent class models for stage-sequential dynamic latent variables. Multivariate Behavioral Research, 27:131–157.

- Colombi and Forcina, (2001) Colombi, R. and Forcina, A. (2001). Marginal regression models for the analysis of positive association of ordinal response variables. Biometrika, 88:1007–1019.

- Dempster et al., (1977) Dempster, A. P., Laird, N. M., and Rubin, D. B. (1977). Maximum Likelihood from incomplete data via the EM algorithm. Journal of the Royal Statistical Society, Series B, 39:1–38.

- Diebolt and Robert, (1994) Diebolt, J. and Robert, C. (1994). Estimation of finite mixture distributions through Bayesian sampling. Journal of the Royal Statistical Society, Series B, 56:363–375.

- Elliott et al., (1989) Elliott, D. S., Huizinga, D., and Menard, S. W. (1989). Multiple Problem Youth: Delinquency, Substance Use, and Mental Health Problems. Springer-Verlag New York, Inc.

- Frühwirth-Schnatter, (2001) Frühwirth-Schnatter, S. (2001). Markov chain Monte Carlo estimation of classical and dynamic switching and mixture models. Journal of the American Statistical Association, 96:194– 209.

- Goodman, (1974) Goodman, L. (1974). Exploratory latent structure analysis using both identifiable and unidentifiable models. Biometrika, 61:215–231.

- Green, (1995) Green, P. J. (1995). Reversible jump Markov chain Monte Carlo computation and Bayesian model determination. Biometrika, 82:711–732.

- Hastings, (1970) Hastings, W. K. (1970). Monte Carlo sampling methods using Markov chains and their applications. Journal of Chemical Physics, 21:1087–1091.

- Hurn et al., (2003) Hurn, M., Justel, A., and Robert, C. P. (2003). Estimating mixtures of regressions. Journal of Computational and Graphical Statistics, 12:55–79.

- Hyslop, (1999) Hyslop, D. R. (1999). State dependence, serial correlation and heterogeneity in intertemporal labor force participation of married women. Econometrica, 67:1255–1294.

- Jasra et al., (2005) Jasra, A., Holmes, C. C., and Stephens, D. A. (2005). MCMC and the label switching problem in Bayesian mixture models. Statistical Science, 20:50–67.

- Langeheine and Van de Pol, (1994) Langeheine, R. and Van de Pol, F. (1994). Discrete time mixed Markov latent class models. In Dale, A. and R.B., D., editors, Analyzing social and political change. A casebook of methods, pages 171–197. London: Sage.

- Lazarsfeld and Neil, (1968) Lazarsfeld, P. F. and Neil, H. W. (1968). Latent Structure Analysis. Houghton Mifflin, Boston.

- MacDonald and Zucchini, (1997) MacDonald, I. L. and Zucchini, W. (1997). Hidden Markov and other Models for Discrete-Valued Time Series. Chapman and Hall, London.

- Marin et al., (2005) Marin, J. M., Mengersen, K. L., and Robert, C. P. (2005). Bayesian modelling and inference on mixture of distributions. In Dey, D. and Rao, C., editors, Handbooks of Statistics, volume 25, pages 459–507, Amsterdam. Elsevier Science.

- Metropolis et al., (1953) Metropolis, N., Rosenbluth, A. W., Rosenbluth, M. N., Teller, A. H., and Teller, E. (1953). Equation of state calculations by fast computing machine. Journal of Chemical Physics, 21:1087–1091.

- Rasch, (1961) Rasch, G. (1961). On general laws and the meaning of measurement in psychology. Proceedings of the 4th Berkeley Symposium on Mathematical Statistics and Probability 4, 321–333.

- Richardson and Green, (1997) Richardson, S. and Green, P. (1997). On Bayesian analysis of mixture with an unknown number of components. Journal fo the Royal Statistical Society, Series B, 59:731–792.

- Robert et al., (2000) Robert, C., Ryden, and T. Titterington, D. (2000). Bayesian inference in hidden Markov models through the reversible jump Markov chain Monte Carlo method. Journal of the Royal Statistical Society, Series B, 62:57–75.

- Rubin, (1976) Rubin, D. B. (1976). Inference and missing data. Biometrika, 63:581–592.

- Schwarz, (1978) Schwarz, G. (1978). Estimating the dimension of a model. The Annals of Statistics, 6:461–464.

- Spezia, (2009) Spezia, L. (2009). Reversible jump and the label switching problem in hidden Markov models. Journal of Statistical Planning and Inference, 139:2305–2315.

- Spezia, (2010) Spezia, L. (2010). Bayesian analysis of multivariate gaussian hidden Markov models with an unknown number of regimes. Journal of Time Series Analysis, 31:1–11.

- Stephens, (2000) Stephens, M. (2000). Dealing with label switching in mixture models. Journal Of The Royal Statistical Society, Series B, 62:795–809.

- Van de Pol and De Leeuw, (1986) Van de Pol, F. and De Leeuw, J. (1986). A latent Markov model to correct for measurement error. Sociological Methods & Research, 15:118–141.

- Van de Pol and Langeheine, (1990) Van de Pol, F. and Langeheine, R. (1990). Mixed Markov latent class models. Sociological Methodology, 20:213–247.

- Vermunt and Hagenaars, (2004) Vermunt, J. and Hagenaars, J. (2004). Ordinal longitudinal data analysis. In Hauspie, R., Cameron, N., and Molinari, L., editors, Methods in Human Growth Research, pages 374–393. Cambridge University Press., Cambridge.

- Vermunt et al., (1999) Vermunt, J., Langeheine, R., and Böckenholt, U. (1999). Discrete-time discrete-state latent Markov models with time-constant and time-varying covariates. Journal of Educational and Behavioral Statistics, 24:179–207.

- Wiggins, (1955) Wiggins, L. (1955). Mathematical models for the Analysis of Multi-wave Panels. PhD thesis, Columbia University, Ann Arbor.

- Wiggins, (1973) Wiggins, L. (1973). Panel analysis. Latent probability models for attitude and behavior processes. Elsevier, New York, US.