Bayesian estimation of GARCH model with an adaptive proposal density

Abstract

A Bayesian estimation of a GARCH model is performed for US Dollar/Japanese Yen exchange rate by the Metropolis-Hastings algorithm with a proposal density given by the adaptive construction scheme. In the adaptive construction scheme the proposal density is assumed to take a form of a multivariate Student’s t-distribution and its parameters are evaluated by using the sampled data and updated adaptively during Markov Chain Monte Carlo simulations. We find that the autocorrelation times between the data sampled by the adaptive construction scheme are considerably reduced. We conclude that the adaptive construction scheme works efficiently for the Bayesian inference of the GARCH model.

Keywords:

Markov Chain Monte Carlo, Bayesian inference, GARCH model, Metropolis-Hastings algorithm1 Introduction

In finance volatility of asset returns plays an important role to manage financial risk. To forecast volatility, various empirical models which mimic the properties of the volatility have been proposed. EngleARCH proposed Autoregressive Conditional Heteroskedasticity (ARCH) model where the present volatility is assumed to depend on the squares of past observations. Later BollerslevGARCH advocated Generalized ARCH (GARCH) model which is an extension of the ARCH model and includes additional past volatility terms to the present volatility estimate. It is known that the volatility of the financial assets exhibits clustering in the financial time series. The GARCH model can captures this property. Furthermore the return distribution generated from the GARCH process shows a fat-tailed distribution which is also seen in the real financial markets. There also exists extension of the GARCH model which incorporates the asymmetric property of the volatilityEGARCH ; GJR ; APGARCH ; QGARCH .

A preferred algorithm to infer GARCH model parameters is the Maximum Likelihood (ML) method which estimates the parameters by maximaizing the corresponding likelihood function of the GARCH model. In this algorithm there is a practical difficulty in the maximization procedure when the output results are sensitive to starting values.

By the recent computer development the Bayesian inference by Markov chain Monte Carlo (MCMC) methods, which is an alternative approach to estimate GARCH parameters, has become popular. There exist a variety of methods proposed to implement the MCMC schemeBauwens -HMC . In a recent surveyASAI it is shown that Acceptance-Rejection/Metropolis-Hastings (AR/MH) algorithm works better than other algorithms. In the AR/MH algorithm the proposal density is assumed to be a multivariate Student’s t-distribution and the parameters to specify the distribution are estimated by the ML technique. Recently a new method to estimate those parameters without relying on the ML technique was proposedACS . In the method the parameters are determined by an MCMC simulation. During the MCMC simulation, the parameters are updated adaptively using the data sampled by the MCMC method itself. We call this method ”adaptive construction scheme”. The adaptive construction scheme was tested for artificial GARCH data and it is shown that the adaptive construction scheme can significantly reduce the correlation between sampled dataACS . In this study we apply the adaptive construction scheme to real financial data, US Dollar/Japanese Yen exchange rate and examine the efficiency of the adaptive construction scheme.

2 GARCH Model

The GARCH(p,q) model by BollerslevGARCH is given by

| (1) |

| (2) |

where the GARCH parameters are restricted to , and to ensure a positive volatility, and the stationary condition is also required. is an independent normal error .

In this study we focus on GARCH(1,1) model where the volatility is given by

| (3) |

The likelihood function of the GARCH model is given by

| (4) |

3 Bayesian inference

Using Bayes’ rule the posterior density with observations denoted by is given by

| (5) |

where is the likelihood function. is the prior density which we have to specify depending on . In this study we assume that the prior density is constant.

With we infer as expectation values of . The expectation values are given by

| (6) |

where is the normalization constant. Hereafter we omit since this factor is irrelevant to MCMC estimations.

The MCMC technique gives a method to estimate eq.(6) numerically. The basic procedure of the MCMC method is as follows. First we sample drawn from a probability distribution . Sampling is done by a technique which produces a Markov chain. After sampling some data, we evaluate the expectation value as an average value over the sampled data ,

| (7) |

where is the number of the sampled data. The statistical error for independent data is proportional to . When the sampled data are correlated the statistical error will be proportional to where is the autocorrelation time between the sampled data. The autocorrelation time depends on the MCMC method we employ. Thus it is desirable to take an MCMC method which can generate data with a small .

4 Metropolis-Hastings algorithm

The Metropolis-Hastings (MH) algorithmMH is an MCMC simulation method which generates draws from any probability density. The MH algorithm is an extension of the original Metropolis algorithmMETRO . Let us consider a probability distribution from which we would like to sample data x. The MH algorithm consists of the following steps.

(1) First we set an initial value and .

(2) Then we generate a new value from a certain probability distribution which we call proposal density.

(3) We accept the candidate with a probability of where

| (8) |

When is rejected we keep , i.e. .

(4) Go back to (2) with an increment of .

For a symmetric proposal density , eq.(8) reduces to the Metropolis accept probability:

| (9) |

5 Adaptive construction scheme

Since the proposal density is dependent of the previous value , usually the sampled data are correlated. One may use an independent proposal density which does not depend on the previous value. Although in this case we can generate independent candidates , it is important to choose the one close enough to the posterior density, in order to make the acceptance high enough.

The posterior density of GARCH parameters often resembles to a Gaussian-like shape. Thus one may choose a density similar to a Gaussian distribution as the proposal density. Following WATANABE ; ASAI , in order to cover the tails of the posterior density we use a (p-dimensional) multivariate Student’s t-distribution given by

| (10) |

where and are column vectors,

| (11) |

and . is the covariance matrix defined as

| (12) |

For later use we also define a matrix as

| (13) |

is a parameter to tune the shape of Student’s t-distribution. When the Student’s t-distribution goes to a Gaussian distribution. In this study we take .

There are three parameters to be inferred for the GARCH(1,1) model. Therefore in this case and , and is a matrix. The values of and are not known a priori. We determine these unknown parameters and through MCMC simulations. First we make a short run by the Metropolis algorithm and accumulate some data. Then we estimate and . Note that there is no need to estimate and accurately. Second we perform an MH simulation with the proposal density of eq.(10) with the estimated and . After accumulating more data, we recalculate and , and update and of eq.(10). By doing this, we adaptively change the shape of eq.(10) to fit the posterior density more accurately. We call eq.(10) with the estimated and ”adaptive proposal density”.

The random number generation for the multivariate Student’s t-distribution can be done easily as follows. First we decompose the symmetric covariance matrix by the Cholesky decomposition as . Then substituting this result to eq.(10) we obtain

| (14) |

where . The random numbers are given by , where follows and is taken from the chi-square distribution degrees of freedom . Finally we obtain the random number by .

6 Empirical analysis

We make an empirical analysis based on daily data of the exchange rates for US Dollar and Japanese Yen. The sampling period of the exchange rates is 4 January 1999 to 29 December 2006, which gives 2006 observations. The exchange rates are transformed to where stands for the average value of .

Our implementation of the adaptive construction scheme is as follows. First we make a short run by the Metropolis algorithm. We discard the first 3000 data as burn-in process. Then we accumulate 1000 data to estimate and . The estimated and are substituted to of eq.(10). The shape parameter is set to 10. We re-start a run by the MH algorithm with the proposal density . Every 1000 update we re-calculate and using all accumulated data and update for the next run. We accumulate 100000 data for analysis.

| Adaptive construction | 0.03151 | 0.9403 | 0.01104 |

|---|---|---|---|

| standard deviation | 0.0078 | 0.017 | 0.0047 |

| statistical error | 0.00004 | 0.0001 | 0.00003 |

| Metropolis | 0.0318 | 0.9391 | 0.0114 |

| standard deviation | 0.0079 | 0.018 | 0.005 |

| statistical error | 0.0005 | 0.0014 | 0.0004 |

We also make a Metropolis simulation and accumulate 100000 data for analysis. The Metropolis algorithm in this study is implemented as follows. We draw a new by adding a small random value to the present value :

| (15) |

where . is a uniform random number in and is a constant to tune the Metropolis acceptance. We choose so that the acceptance becomes greater than .

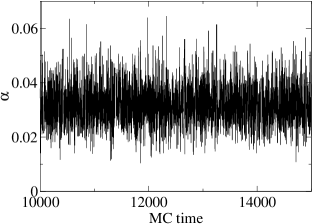

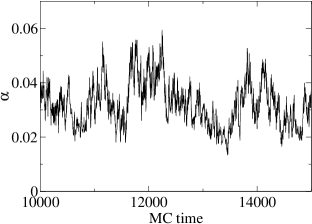

Fig. 1 compares the Monte Carlo time history of sampled by the adaptive construction scheme with that by the Metropolis algorithm. It is clearly seen that the data produced by the Metropolis algorithm are very correlated. On the other hand the sampled data by the adaptive construction scheme seem to be well de-correlated. For other parameters and we also see the similar behavior.

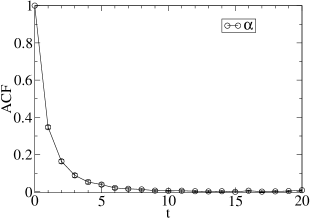

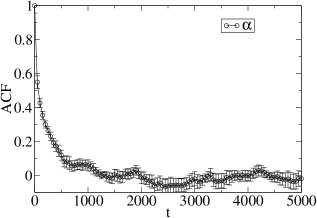

In order to see correlations between sampled data, we measure the autocorrelation function (ACF) defined as

| (16) |

where and are the average value and the variance of certain successive data respectively.

Fig. 2 shows the ACF for the adaptive construction scheme and the Metropolis algorithm. The ACF of the the adaptive construction scheme decreases quickly as Monte Carlo time increases. On the other hand the ACF of the Metropolis algorithm decreases very slowly which indicates that the correlation between the sampled data is very large.

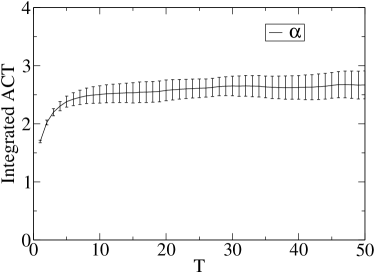

We estimate the autocorrelation time by the integrated autocorrelation time . To calculate we define as

| (17) |

is given by . In practice, however, it is impossible to sum up to . Since typically increases with and reaches a plateau we estimate at this plateau. Fig. 3 illustrates of sampled by the adaptive construction scheme. increases with and reaches a plateau around .

Results of are summarized in Table 1. The values of from the Metropolis simulations are very large, typically several hundreds. On the other hand from the adaptive construction scheme are very small, 111 is called an inefficiency factor.. This results in a factor of 10 reduction in terms of the statistical error. This reduction property is confirmed by the statistical errors of the sampled data (See Table 1). Thus it is concluded that the adaptive construction scheme is effectively working for reducing the correlations between the sampled data.

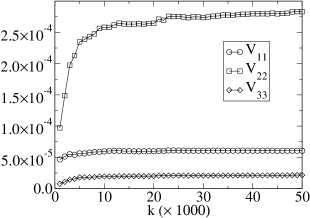

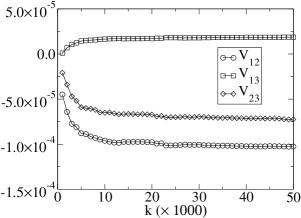

Fig. 4 shows the convergence property of the matrix . The matrix elements are defined by with . For instance . All elements of converge quickly to certain values as the simulations are proceeded.

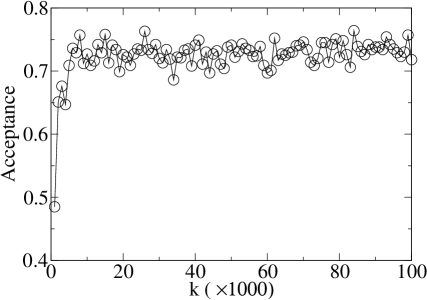

Fig. 5 shows the acceptance at the MH algorithm with the adaptive proposal density of eq.(10). Each acceptance is calculated every 1000 updates and the calculation of the acceptance is based on the latest 1000 data. At the first stage of the simulation the acceptance is low. This is because at this stage and are not calculated accurately yet. However the acceptances increase quickly as the simulations are proceeded and reaches a plateau where the acceptance is more than 70%.

7 Summary

We proposed the adaptive construction scheme to construct a proposal density for the MH algorithm of the GARCH(1,1) model. The construction of the proposal density is performed using the data generated by MCMC methods. During the MCMC simulations the proposal density is updated adaptively. In this study we applied the adaptive construction scheme for the Bayesian inference of the GARCH(1,1) model by using US Dollar/Japanese Yen exchange rate. The numerical results show that the adaptive construction scheme significantly reduces the correlations between the sampled data. The autocorrelation time of the adaptive construction method is calculated to be , which is comparable to that of the AR/MH methodASAI . It is concluded that the adaptive construction scheme is an efficient method for the Bayesian inference of the GARCH(1,1) model. The adaptive construction scheme is not limited to the GARCH(1,1) model and can be applied for other GARCH-type models.

Acknowledgments

The numerical calculations were carried out on Altix at the Institute of Statistical Mathematics and on SX8 at the Yukawa Institute for Theoretical Physics in Kyoto University.

References

- (1) Engle, R. F.: Autoregressive Conditional Heteroskedasticity with Estimates of the Variance of the United Kingdom inflation. Econometrica 50, 987–1007 (1982)

- (2) Bollerslev, T.: Generalized Autoregressive Conditional Heteroskedasticity. Journal of Econometrics 31, 307–327 (1986)

- (3) Nelson, D. B.: Conditional Heteroskedasticity in Asset Returns: A New Approach. Econometrica 59, 347–370 (1991)

- (4) Glston, L. R., Jaganathan, R. Runkle, D.E.: On the Relation Between the Expected Value and the Volatility of the Nominal Excess on Stocks. Journal of Finance 48, 1779–1801 (1993)

- (5) Ding, Z., Granger, C.W.J., Engle, R.F.: A long memory property of stock market returns and a new model. Journal of Empirical Finance 1, 83–106 (1993)

- (6) Sentana, E.: Quadratic ARCH Models. Review of Economic Studies 62, 639–661 (1995)

- (7) Bauwens, L., Lubrano, M.: Bayesian inference on GARCH models using the Gibbs sampler. Econometrics Journal 1, c23-c46 (1998)

- (8) Kim. S., Shephard, N., Chib, S.: Stochastic volatility: Likelihood inference and comparison with ARCH models. Review of Economic Studies 65, 361–393 (1998)

- (9) Nakatsuma, T.: Bayesian analysis of ARMA-GARCH models: Markov chain sampling approach. Journal of Econometrics 95, 57–69 (2000)

- (10) Mitsui, H., Watanabe, T.: Bayesian analysis of GARCH option pricing models. J. Japan Statist. Soc. (Japanese Issue) 33, 307–324 (2003)

- (11) Asai, M.: Comparison of MCMC Methods for Estimating GARCH Models. J. Japan Statist. Soc. 36, 199–212 (2006)

-

(12)

Takaishi, T.: Bayesian Estimation of GARCH model by Hybrid Monte Carlo.

Proceedings of the 9th Joint Conference on Information Sciences 2006, CIEF-214

arXiv:physics/0702240v1 (2007) doi:10.2991/jcis.2006.159 - (13) Takaishi, T.: An adaptive Markov Chain Monte Carlo method for GARCH model. arXiv:0901.0992v1 (2009)

- (14) Hastings, W.K.: Monte Carlo Sampling Methods Using Markov Chains and Their Applications. Biometrika 57, 97–109 (1970)

- (15) Metropolis, N., Rosenbluth, A.W., Rosenbluth, M.N., Teller, A.H., Teller, E.: Equations of State Calculations by Fast Computing Machines. J. of Chem. Phys. 21, 1087–1091 (1953)