Network Non-neutrality Debate: An Economic Analysis

Abstract

This paper studies economic utilities and quality of service (QoS) in a two-sided non-neutral market where Internet service providers (ISPs) charge content providers (CPs) for the content delivery. We propose new models that involve a CP, an ISP, end users and advertisers. The CP may have either a subscription revenue model (charging end users) or an advertisement revenue model (charging advertisers). We formulate the interactions between the ISP and the CP as a noncooperative game for the former and an optimization problem for the latter. Our analysis shows that the revenue model of the CP plays a significant role in a non-neutral Internet. With the subscription model, both the ISP and the CP receive better (or worse) utilities as well as QoS in the presence of the side payment at the same time. With the advertisement model, the side payment impedes the CP from investing on its contents.

Index Terms:

Network Non-neutrality, Side Payment, Nash Equilibrium, BargainingI Introduction

Network neutrality, one of the foundations of Internet, is commonly admitted that ISPs must not discriminate traffic in order to favor specific content providers [1]. However, the principle of network neutrality has been challenged recently. The main reason is that new broadband applications cause huge amount of traffic without generating direct revenues for ISPs. Hence, ISPs want to get additional revenues from CPs that are not directly connected to them. For instance, a residential ISP might want to charge Youtube in order to give a premium quality of service to Youtube traffic. This kind of monetary flows, which violate the principle of network neutrality, are called two-sided payment. We use the term side payment to name the money charged by ISPs from CPs exclusively.

On the one hand, the opponents of network neutrality argue that it does not give any incentive for ISPs to invest in the infrastructure. This incentive issue is even more severe in two cases: the one of tier-one ISPs that support a high load, but do not get any revenue from CPs; and the one of 3G wireless networks that need to invest a huge amount of money to purchase spectrum. On the other hand, advocates of network neutrality claim that violating it using side payment will lead to unbalanced revenues among ISPs and CPs, thus a market instability.

Recent work addressed the problem of network neutrality from various perspectives [2, 3, 4, 5, 6, 7, 8, 9]. Among these work, [2, 3, 4] are the closest to our work. Musacchio et al. [2] compare one-sided and two-sided pricing of ISPs. However, they only investigate an example where the joint investments of CPs and ISPs bring revenue from advertisers to CPs. In [3], the authors show how side payment is harmful for all the parties involved such as ISP and CP. Altman et al. in [4] present an interesting bargaining framework to decide how much the ISP should charge the CP. However, their models might give a biased conclusion by overlooking the end users’ sensitivity towards the prices of the CP and the ISP.

In this paper, we unravel the conflicts of the side payment in a more general context. We consider a simplified market composed of one ISP, one CP, some advertisers, and a large number of end users. The ISP charges end-users based on their usage and sets their QoS level according to the price paid. The CP can either have a subscription based or an advertisement based revenue model. For the subscription based revenue model, the CP gets its revenue from the subscription paid by end-users. End-users adapt their demand of content based on the price paid to the ISP and the CP. For the advertisement based revenue model, the CP gets its revenue from advertisers. End users adapt the demand according to the price paid to the ISP and the investment of CP on its contents.

Our work differs from related work [2, 3, 4] by: i) incorporating the QoS provided by the ISP, ii) studying different revenue models of the CP, and iii) introducing the relative price sensitivity of end users in the subscription model. Especially, in the subscription model, the relative price sensitivity decides whether the side payment is beneficial (or harmful) to the ISP and the CP. Our finding contradicts the previous work (e.g. [3]) that argues that the side payment is harmful for all parties involved. In the advertisement model, the ability of CP’s investment to attract the traffic of end users plays a key role. It determines whether the side payment is profitable for the ISP and the CP. Our main contributions are the following.

-

•

We present new features in the mathematical modeling that include the QoS, the relative price sensitivity of end-users, and the CP’s revenues.

-

•

We model the price competition between the ISP and the subscription based CP as a noncooperative game and analyze the properties of the Nash equilibrium. The interaction between the ISP and the advertisement based CP is modeled as an optimization problem. The optimal investment is shown to be a decreasing function of the side payment (from the CP to the ISP).

-

•

We utilize bargaining games to analyze how the side payment is determined.

The rest of this work is organized as follows. In section II, we model the economic behaviors of ISP, CP, advertisers and end users. Section III and IV study the impact of side payment and how the ISP and the CP reach a consensus of side payment. Section V presents numerical study to validate our claims. Section VII concludes this paper.

II Basic Model

In this section, we first introduce the revenue models of the ISP and the CP. Then, we formulate a game problem and an optimization problem for the selfish ISP and the CP. Finally, we describe the bargaining games in a two-sided market.

II-A Revenue Models

We consider a simplified networking market with four economic entities, namely the advertisers, the CP, the ISP and end users. All the end users can access the contents of the CP only through the network infrastructure provided by the ISP. The ISP collects subscription fees from end users. It sets two market parameters where is the non-negative price of per-unit of demand, and is the QoS measure (e.g. delay, loss or rejection probability). End users can decide whether to connect to the ISP or not, or how much traffic they will request, depending on the bandwidth price and the QoS. The CP usually has two revenue models, the user subscription and the advertisement from clicks of users. These two models, though sometimes coexisting with each other, are studied separately in this work for clarity. The CP and the ISP interact with each other in a way that depends on the CP’s revenue models. In the subscription based model, the CP competes with the ISP by charging users a price per-unit of content within a finite time. End users respond to , and by setting their demands elastically. Though has a different unit as , it can be mapped from the price per content into the price per bps (i.e. dividing the price of a content by its size in a finite time). The price not only can stand for a financial disutility, but also can represent the combination of this disutility together with a cost per quality. Thus a higher price may be associated with some better quality (this quality would stand for parameters different than the parameter which we introduce later). Without loss of generality, and can be positive or 0. For the advertisement based model, instead of charging users directly, the CP attracts users’ clicks on online advertisements. The more traffic demands end users generate, the higher the CP’s revenue.

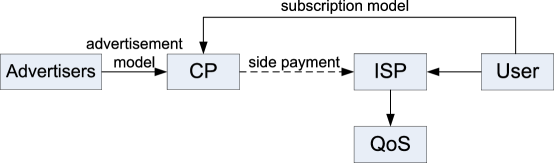

To better understand network neutrality and non-neutrality, we describe the monetary flows among different components. The arrows in Figure 1 represent the recipients of money. A “neutral network” does not allow an ISP to charge a CP for which it is not a direct provider for sending information to this ISP’s users. On the contrary, monetary flow from a CP to an ISP appears when “network neutrality” is violated. The ISP may charge the CP an additional amount of money that we denote by where is the price of per-unit of demand. We denote by the tax rate of this transferred revenue imposed by the regulator or the government to the ISP.

We present market demand functions for the subscription and the advertisement based revenue models.

II-A1 Subscription model

Let us define the average demand of all users by that has

| (1) |

where , , and are all positive constants. The parameter reflects the total potential demand of users. The parameters and denote the responsiveness of demand to the price and the QoS level of the ISP. The physical meaning of (1) can be interpreted in this way. When the prices of the ISP and the CP increase (resp. decrease), the demand decreases (resp. increases). If the QoS of the ISP is improved, the demand from users increases correspondingly. The parameter represents the relative sensitivity of to . We deliberately set different sensitivities of end users to the prices of the ISP and the CP because and refers to different type of disutilities. If , the prices of the ISP and the CP are regarded as having the same effect on . When , users are more sensitive to the change of than . The positive prices and can not be arbitrarily high. They must guarantee a nonnegative demand .

We denote to be the pricing strategy of the CP that has . The utility (or revenue equivalently) of the CP is expressed as

| (2) |

Note that the variable is interchangeable with all the time. Next, we present the utility of the ISP with QoS consideration. We assume that the pricing strategy of the ISP is defined by . To sustain a certain QoS level of users, the ISP has to pay the costs for operating the backbone, the last-mile access, and the upgrade of the network, etc. Let be the amount of bandwidth consumed by users that depends on the demand and the QoS level . We assume that is a positive, convex and strictly increasing function in the 2-tuple . This is reasonable because a larger demand or higher QoS usually requires a larger bandwidth of the ISP. We now present a natural QoS metric as the expected delay 111The QoS metric can be the functions of packet loss rate or expected delay etc.. The expected delay is computed by the Kleinrock function that corresponds to the delay of M/M/1 queue with FIFO discipline or M/G/1 queue under processor sharing [10]. Similar to [10], instead of using the actual delay, we consider the reciprocal of its square root, . Thus, the cost can be expressed as , where the price of per-unit of bandwidth invested by the ISP. Therefore, the cost of the ISP is denoted by . The utility of the ISP is defined as the difference between revenue and cost:

| (3) |

II-A2 Advertisement model

Nowadays, a small proportion of CPs like Rapidshare and IPTV providers get their income from end users. Most of other CPs provide contents for free, but collect revenues from advertisers. The demand from users is transformed into attentions such as clicks or browsing of online advertisements. To attract more eyeballs, a CP needs to invest money on its contents, incurring a cost . The investment improves the potential aggregate demand in return. Let be a concave and strictly increasing function of cost . With abuse of notations we denote the strategy of the CP by . Hence, the demand to the CP and the ISP is written as

| (4) |

The utility of the ISP is the same as that in (3). Next, we describe the economic interaction between advertisers and the CP. There are advertisers interested in the CP, each of which has a fixed budget in a given time interval (e.g., daily, weekly or monthly). An advertiser also has a valuation to declare its maximum willingness to pay for each attention. The valuation is a random variable in the range . Suppose that is characterized by probability density function (PDF) and cumulative distribution function (CDF) . We assume that the valuations of all advertisers are independent and identically distributed (i.i.d). Let be the price of per attention charged by the CP. We denote by the demand of attentions from advertisers to the CP. Therefore, can be expressed as [11]

| (5) |

When the CP increases , the advertisers will reduce their purchase of attentions. It is also easy to see that the revenue of advertising, , decreases with regard to either. However, the attentions that the CP can provide is upper bounded by the demand of users through the ISP. Then, we can rewrite as that in [11] by

| (6) |

Correspondingly, subtracting investment from revenue, we obtain the utility of the CP by

| (7) |

Lemma 1

The optimal demand is a strictly decreasing function of if the pdf is nonzero in .

Proof: According to (7), there has where is an arbitrarily small positive constant. This is because for . Hence, is a strictly decreasing function of .

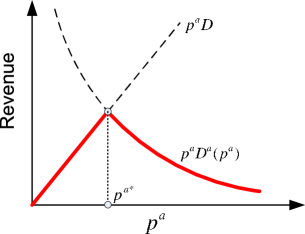

To illustrate how the optimal is found, we follow [11] by drawing figure 2. The X-coordinate denotes the price and the Y-coordinate denotes the CP’s revenue. The curve in red represents the revenue of the CP coming from advertisers. The optimal price is obtained at . Here, we denote a function such that . According to the demand curve of attentions, is a decreasing function of . The utility of the CP is a function of the demand and the cost , i.e. .

II-B Problem Formulation

Two economic entities, the ISP and the CP, want to maximize their utilities. With the subscription model, the strategy profile of the ISP is to set the 2-tuple and that of the CP is to set . This is actually a game problem in which the ISP and the CP compete by setting their prices. The ISP’s QoS is tunable. Thus, we call this game “QoS Agile Price competition”. With the advertisement model, the strategy of the ISP is still the price paid by end users, while that of the CP is to determine the investment level . The ISP and the CP maximize their own utilities selfishly, but do not compete with each other. We name this maximization as “Strategic Pricing and Investment”.

Definition 1

QoS Agile Price Competition In the subscription model, the CP charges users based on their traffic demands. If the Nash equilibrium exists, it can be expressed as

| (8) | |||||

| (9) |

Definition 2

Strategic Pricing and Investment In the advertisement model, the ISP sets and the CP sets to optimize their individual utilities. If there exists an equilibrium , it can be solved by

| (10) | |||||

| (11) |

II-C Bargaining Game

The side payment serves as a fixed parameter in the above two problems. A subsequent and important problem is how large the side payment should be. When the ISP decides the side payment unilaterally, it might set a very high in order to obtain the best utility. However, this leads to a paradox when the ISP sets and at the meantime. With the subscription based model, if the ISP plays a strategy and the CP plays , the noncooperative game leads to a zero demand and hence a zero income. This can be easily verified by taking the derivative of over (also see [3]). In other words, the ISP cannot set and simultaneously in the price competition. Similarly, with the advertisement based model, the ISP meets with the same paradox. There are two possible ways, the Stackelberg game and the bargaining game, to address this problem. Their basic principle is to let the ISP to choose and asynchronously. In this work, we consider the bargaining game in a market where the ISP and the CP usually have certain marketing powers. Our analysis in this work is close to the one presented in [4], but comes up with quite different observations.

We here analyze the bargaining games of the side payments that are played at different time sequences. The first one, namely pre-bargaining, models the situation that the bargaining takes place before the problems (G1) or (G2). The second one, defined as post-bargaining, models the occurrence of bargaining after the problems (G1) or (G2). Let be the bargaining power of the ISP over the CP. They negotiate the transfer price determined by . Since the utilities can only be positive, the optimal maximizes a virtual utility

| (12) |

We use (12) to find as a function of the strategies of the ISP and the CP.

III Price Competition of the Subscription Model

In this section, we first investigate how the relative price sensitivity influences the price competition between the ISP and the CP. We then study the choice of side payment under the framework of bargaining games.

III-A Properties of Price Competition

This subsection investigates the impact of side payment on Nash Equilibrium of the noncooperative game G1. Before eliciting the main result, we show some basic properties of the subscription based revenue model.

Lemma 2

The utility of the CP, , in (2) is a finite, strictly concave function with regard to (w.r.t.) .

Proof: Taking the derivative of over , we obtain . The demand is less than so that , are finite. Hence, is finite and strictly concave w.r.t. .

Similarly, we draw the following conclusion.

Lemma 3

The utility of the ISP, , in (3) is a finite, strictly concave function w.r.t. the 2-tuple if the market parameters satisfy .

Proof: We compute the Hessian matrix of by

| (17) |

When is negative definite, there must have and , that is, . If the Hessian matrix if negative definite, is strictly concave with regard to the 2-tuple .

For the QoS Agile Price Competition, we summarize our main results as below.

Lemma 4

When the ISP and the CP set their strategies selfishly,

-

•

the Nash equilibrium is unique;

-

•

the QoS level at the NE is influenced by the side payment in the ways:

-

–

improved QoS with ;

-

–

degraded QoS with ;

-

–

unaffected QoS with

if satisfy and .

-

–

Proof: Because and are concave functions, the best responses of the ISP and the CP can be found either inside the feasible region or at the boundary. In the beginning, we assume that the NE is not at the boundary. Then, the derivatives , and are zero at the NE ,

| (18) | |||||

| (19) | |||||

| (20) |

The best response functions of the ISP and the CP are written as

| (21) | |||||

| (22) |

The above equations yield

| (23) | |||||

| (24) | |||||

| (25) | |||||

| (26) |

From (23), we can see that the QoS is better (resp. worse) if (resp. ). The QoS is unchanged with side payment when equals to 1.

Next, we consider the case that the NE is at the boundary. The NE contains three variables so that there are many possibilities of hitting the boundary. We will not enumerate all of them because the methods of analysis are almost the same. Here, we study two examples when either in (23) or in (25) are outside of .

Obviously, cannot be less than 0. This is because the demand at the NE is non-zero. If in (23) is larger than , is positive at when and are zero (i.e. and are at the equilibrium). Thus, G1 is equivalent to the game with a fixed QoS provision. The NE prices are characterized by

given and are positive.

If in (25) is negative, is negative at when and are zero The best strategy of the ISP is to set and . The demand function turns into . Thus, the best strategy of the CP is

| (27) |

Submitting (27) to (21), we validate that the best response of the ISP is .

By enumerating all the boundary conditions, we can always find that the NE is unique. When the NE is not at the boundary, the QoS is better with side payment from the CP to the ISP if , and vice versa.

Lemma 4 means that that the QoS provision of the ISP is influenced by the side payment. We interpret the results by considering and separately. When users are indifferent to the price set by the ISP and that by the CP (i.e., ), a positive tax rate leads to the degradation of in the presence of side payment. Next, we let be 0 and investigate the impact of . If users are more sensitive to the price of the ISP (i.e. ), the side payment is an incentive of the ISP to improve its QoS. Otherwise, charging side payment leads to an even poorer QoS of the ISP. According to (23)(26), if users are more sensitive to the CP’s price, a good strategy of the ISP is to share its revenue with the CP so that the latter sets a lower subscription fee.

III-B Bargaining of Side Payment

To highlight the bargaining of side payment, we make the following two simplifications: i) the tax ratio is 0, and ii) can be positive, zero or negative. We let because it turns out to have the similar effect as . The above analysis has shown that a negative might benefit both the ISP and the CP in some situations. Hence, we relax the feasible region of in the bargaining game.

Pre-bargaining: In the pre-bargaining, is chosen based on the NE of the ISP and the CP. The equations (23) (25) yield the expression of

| (28) |

The utility is increasing or decreasing in depending on the sign of . If , a positive improves not only the QoS level of the ISP, but also the utilities of the ISP and the CP. As increases, decreases and increases consequently until hits 0. Hence, in the pre-bargaining, . The prices and are computed by

| (29) | |||||

| (30) |

On the contrary, when , a negative benefits both of them. Then, is a negative value such that is 0. When , the QoS and the utilities are unaffected by any . Also, the selection of is uninfluenced by the bargaining power .

Post-bargaining: For the post-bargaining, the ISP and the CP compete for the subscription of users first, knowing that they will bargain over afterwards [4]. In brief, we find as a function of , and first. Then, the ISP and the CP compete with each other by setting the prices. To solve the maximization in (12), we let be 0 and obtain

| (31) |

Submitting (31) to , we rewrite the ISP’s utility by

| (32) |

The utility of the CP is proportional to that of the ISP, i.e. . After knowing , we compute the derivatives , and by

| (33) | |||||

| (34) | |||||

| (35) |

The best responses of and will not happen at the same time unless or . The condition does not hold because it leads to a zero demand and zero utilities. When is not 1, only one of (33) and (35) is 0. Here, we consider the case . The utility reaches its maximum upon , while is still strictly increasing w.r.t. . Thus, the ISP increases until the demand is 0, which contradicts the condition of a nonzero . If , is negative and is 0. Then, the CP decreases until 0 and the ISP sets to achieve its best utility accordingly. By letting (35) be 0, we can find at the Nash equilibrium

The price of side payment, , is thus computed by

| (36) |

When , and can be arbitrary values in their feasible region that satisfy . Similar result has been shown in [4]. The analysis of is omitted here since it can be conducted in the same way.

IV Price, QoS and Investment settings of the Advertisement Model

This subsection analyzes how the side payment influences the optimal strategies of the ISP and the CP with the advertisement model. The bargaining games are adopted to determine the amount of side payment. Compared with subscription based model, the advertisement based model exhibits quite different behaviors.

IV-A Properties of Advertisement Mode

In general, the subscription model is limited to file storage CDNs, newspaper corporations, or some big content owners such as movie producers. Most of content providers are not able to provide enough unique contents so that they do not charge users, but make money from online advertisements. In this subsection, we present the general properties of the advertisement model and a couple of case studies.

Lemma 5

For any feasible investment of the CP, there exists a best strategy of the ISP, . When increases, the price and the QoS (i.e. and ) become larger.

Proof: According to lemma 3, is a strictly concave function of 2-tuple in the feasible region. When is determined, the best response is derived accordingly.

The two-tuple at the NE is solved by

| (37) | |||||

| (38) |

if . Since is an increasing function, we can easily find that and increase w.r.t. .

In G2, the CP and the ISP do not compete with each other. On one hand, the ISP sets the two-tuple with the observation of . On the other hand, the CP adjusts based on . The investment of the CP brings more demand of end users, which increases the revenues of not only the ISP, but also the CP. Hence, different from G1, the problem G2 is not a game. Instead of studying the Nash equilibrium, we look into the best responses of the ISP and the CP in G2.

Theorem 1

There exists a unique best response, namely , with the advertisement model if the revenue of the CP, , is a concave function w.r.t. .

Proof: In the proof, we will show that the best response equations of the ISP and the CP have only one solution.

First, we assume that is not obtained at the boundary (i.e. , and ). To get the best response functions of the ISP, we derive over and ,

| (39) | |||||

| (40) |

Submitting (40) and (4) to (39), we obtain

| (41) |

The best response functions of the ISP give rise to the demand function

| (42) |

The derivative of over is expressed as

| (43) |

Letting , we obtain the following equation

| (44) |

Given that is a strictly concave function of , is decreasing in terms of . The revenue of the CP, , is increasing and concave so that the expression is a non-decreasing function of . In the demand function (44), the left side is a decreasing function of , while the right side is non-decreasing w.r.t. . This indicates that is a non-increasing of . However, the demand of the ISP in (42) is an increasing function of . Thus, the intersection of (42) and (44) is the unique fixed point.

If (42) and (44) do not have an intersection in the range , the best response might be at the boundary. We consider the cases when each variable in the set is negative according to the fixed point equation composed of (42) and (44). If , and , the demand at the equilibrium is negative, which is not true. Hence, we only need to consider two cases of the fixed point equation from (42) and (44). i) and ii) . If the intersection of (42) and (44) has and , the demand of the end users is and is chosen to be 0. Submitting the above expression of to (44), we obtain a new fixed point equation w.r.t.

| (45) |

Because the left side is a decreasing function of and the right side is an increasing function of , the solution in the range is unique if it exists. For the case that the intersection of (42) and (44) has and , the CP sets to be 0. Then, the aggregate total demand is actually . The equations (42) and (39) yield

| (46) |

Note in the case ii), if derived from the fixed point equation (45) is less than 0, the CP will set the to be 0. Similarly, in case iii), if in (46) is less than 0, the ISP’s best strategy is to let .

This completes the proof.

Lemma 6

The side payment from the CP to the ISP leads to a decreased investment on the contents when the best strategy has and .

Proof: Given that has and , the best strategy is not at the boundary. Let and be two prices of side payment that have . We will prove by contradiction. Assume that when . From (42) we obtain . In the ride side of (44), is decreasing with regard to so that there has . Hence, we obtain . Given is a decreasing function of , there has , which contradicts to the assumption . Therefore, the optimal investment of CP is an decreasing function of the price of side payment.

IV-B Case Study

In this subsection, we aim to find the best strategies of the ISP and the CP when the valuation of advertisers follows a uniform distribution or a normal distribution.

Recall that the potential aggregate demand of users, , is strictly increasing and concave w.r.t . When the CP invests money on contents, becomes larger, while its growth rate shrinks. Here, we assume a log function of ,

| (47) |

where the constant denotes the ability that the CP’s investment brings the demand. The nonnegative constant denotes the potential aggregate demand of end users when is zero (the CP only provides free or basic contents). The utility of the ISP remains unchanged.

Uniform Distribution: Suppose follows a uniform distribution in the range . Then, the CDF is expressed as . The optimal price is obtained when in the range (see subsection II-A2). Alternatively, there has

| (48) |

The above expressions yield the utility of the CP by

| (49) |

Deriving over , we obtain

| (50) |

We let (50) be 0 and get

| (51) |

The rule of the ISP to decide is the same as that in the subscription model, except that the aggregate demand is not a constant, but a function of ,

| (52) |

Note that (51) is strictly decreasing and (52) is strictly increasing. They constitute a fixed-point equation for the 2-tuple . When approaches infinity, (51) is negative while (52) is positive. When is zero, if (51) is larger than (52), there exists a unique fixed-point solution. In this fixed point, the ISP and the CP cannot benefit from changing their strategy unilaterally. We can solve and numerically using a binary search. If (51) is smaller than (52) when is 0, the best strategy of the CP is exactly . The physical interpretation is that the increased revenue from advertisers cannot compensate the investment on the contents. Once and are derived, we can solve and subsequently. In this fixed-point equation, greatly influences the optimal investment . When grows, (51) and (52) decrease at the mean time. The crossing point of two curves, (51) and (52), may shift toward the direction of smaller . Intuitively, the contents of the CP become less when the ISP charges a positive .

Next, we analyze the best strategies of the ISP and the CP when they are at the boundary. Note that we compute and numerically through (51) and (52). They might be negative, thus violating their feasible ranges. If the computed , the derivative cannot be 0 with . When the ISP set its price to be 0, the demand function is rewritten as

| (53) |

Submitting (53) to (51), we obtain a new fixed point equation in term of . The best investment of the CP is obtained by solving this fixed point equation. Similarly, we consider the case that computed from (51) and (52) is less than 0. Due to the constraint , the best strategy of the CP is to set . When is 0, the demand to the ISP is expressed as

| (54) |

By letting and be 0, the best strategy of the ISP is represented as the following

| (55) | |||||

| (56) |

Normal Distribution: Suppose that obeys a normal distribution with the mean and the deviation . The valuation ranges from to (i.e. and ) 222Truncated normal distribution is usually adopted in econometrics. In order to keep mathematical simplicity, we consider a normal distribution.. The probability distribution function is expressed as

| (57) |

The CDF of is computed by . Since the optimal price (or alternatively) is obtained at , we obtain as an implicit function of , (denoted by )

| (58) |

For simplicity, we rewrite as the following

| (59) |

Let be a set of best strategies of the ISP and the CP (computed from their best response functions). To prove the uniqueness of , we show that is a concave function w.r.t. .

Lemma 7

The revenue of the CP, , is a concave function of when the valuation follows a normal distribution with the mean and the variance .

Proof: Denote a function to be the revenue of the CP. To prove the concavity of , we need to show . We derive over and obtain

We next compute the derivative ,

| (60) | |||||

Because is an implicit function of in (58), is positive. Otherwise, the demand from the ISP is negative, which is not feasible. Let us denote functions and by

and

respectively. Here, we will show that and are positive for . The derivative of over is expressed as

for any . Hence, is strictly decreasing for . When goes to infinity, approaches 0, i.e. . Because is a strictly decreasing function, we can infer for any positive . According to the expression of , it is easy to observe for any that has . Thus, is positive for any positive . We derive over subsequently,

From the above expression, we can see that is increasing for and decreasing for . Note that there have and . We can see that is positive in the range . Because and are positive for , so that is a concave function of .

The concavity of implies the uniqueness of the best strategies of the ISP and the CP. We then show how to find numerically. The analysis of the normal distribution is carried out based on the assumption that is not at the boundary first. Then, is the solution of equations , and . According to (58), the inverse function does not have a close form expression. Hence, the derivative contains the variables and ,

| (61) | |||||

By letting be 0, we obtain

| (62) |

The best response of the ISP with the normal distribution is the same as that with the uniform distribution. We submit the demand function in (58) to (52) and obtain

| (63) | |||||

The equations (62) and (63) form a fixed point equation of and .

The proof of Lemma 7 shows that an increasing function of in (62). While in (63) is a decreasing function of . Therefore, the solution of this fixed point is unique if it is not at the boundary.

Next, we investigate the cases where the best strategies are at the boundary. With the advertisement model, the boundary cases include i) , ii) , and iii) . If the fixed point solution computed from (62) and (63) has , then the derivative is not zero at . The demand function is then expressed as

| (64) |

Here, (62) and (64) consist of a new fixed point equation. The optimal strategies of the ISP and the CP is the solution of this fixed point equation. If the fixed point solution computed from (62) and (63) has , then the derivative is not zero . The best response of the ISP is obtained at . We can use (55) and (56) to compute .

IV-C Bargaining of Side Payment

In the bargaining game of advertisement model, can also be negative. We assume that the valuation follows a uniform distribution, and makes the same simplifications as those in subsection III-B.

Pre-bargaining: The pre-bargaining method determines by maximizing the virtual utility ,

where the superscript ∗ denotes the value of a variable at the equilibrium. In the beginning, we assume that does not cause , or outside of their feasible ranges. Submitting (49) to (IV-C), we obtain

| (65) | |||||

Recall that in the pre-bargaining of the subscription model, is independent of the bargaining power . When the ISP charges the CP for per-unit of demand, either or is zero, depending on . Different from that of the subscription model, the optimal side payment relies on the bargaining parameter .

If causes or , we need to replace the and by the corresponding expressions in which the best strategies of the ISP and the CP are at the boundary (see subsection II-A2). Using the same method, we can find the optimal side payment.

Post-bargaining:

In the post-bargaining of advertisement model, the bargaining of happens after the ISP and the CP select their best policies. They negotiate to maximize the virtual utility ,

| (66) |

Deriving over and letting the derivative be 0, we obtain

| (67) |

Submitting (67) to , we have

| (68) |

and . After is determined, the ISP and the CP maximize their individual utilities. Here, our study is limited to the cast that the best strategy satisfies , and . We solve by letting the derivatives be 0 because it is not at the boundary. Here, is expressed as

| (69) |

The derivatives and are

| (70) | |||||

| (71) |

The equations (69) and (70) give rise to

| (72) |

The equations (70), (71) together with the demand function (4) yield

| (73) |

The best investment is the solution of the fixed point equation composed of (72) and (73) if . From (72) and (73), is strictly increasing w.r.t. if and are positive. But increases linearly in (72) and logarithmically in (73). In order to prove the uniqueness of the best strategy, we need to show that computed by (73) is larger than that computed by (72). When is 0, the demand is . We then replace by in (73). If there has , the demand computed by (73) is larger than that computed by (72). Given the above inequality, the best strategy is unique. Otherwise, there might have two fixed point solutions, in which one of them bring more utilities to the ISP and the CP than the other.

V Evaluation

We present some numerical results to reveal how the QoS, prices of the ISP and the CP, as well as their utilities evolve when the price of side payment changes. The impact of bargaining power on the choice of side payment is also illustrated.

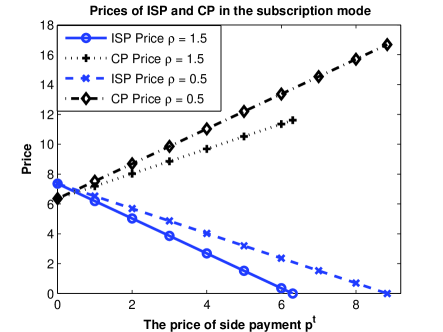

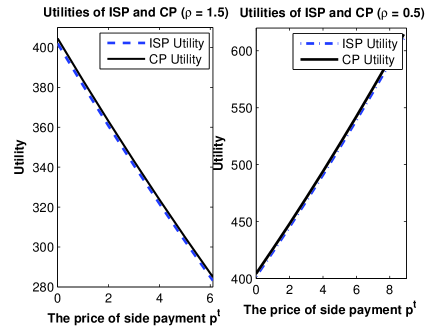

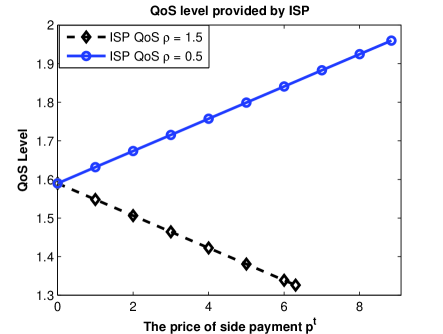

Subscription Model: We consider a networking market where the demand function is given by . The operational cost of per-unit of bandwidth is set to . Two situations, and , are evaluated. The tax rate is set to 0 for simplicity. As is analyzed, the side payment benefits the ISP and the CP depending on whether is greater than 1 or not. Figure 3(a) shows that increases and decreases when becomes larger. In figure 3(b), has different impacts on utilities of the ISP and the CP. When , end users are more sensitive to the change of than . A positive leads to the increase of , causing a tremendous decrease of demand. Hence, both the ISP and the CP lose revenues w.r.t. a positive . Figure 3(c) further shows that a positive yields a better QoS if and a worse QoS if .

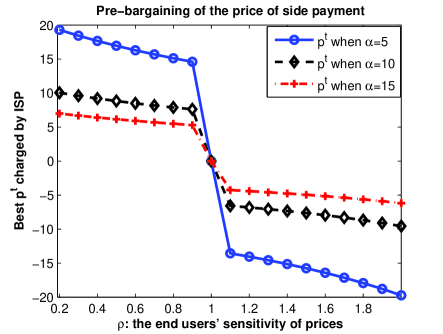

Next, the ISP and the CP bargain with each other to determine . We relax the choice of so that it can be negative. In the pre-bargaining game, is independent of the bargaining power . The optimal is obtained when decreases to 0, its lower bound. We evaluate by changing and in figure 3(d). When increases from 0.2 to 2, decreases until it becomes negative. A negative means that the ISP needs to transfer revenue to the CP instead. When , can be an arbitrary value as long as and are nonnegative. Figure 3(d) also shows that a larger results in a smaller absolute value of .

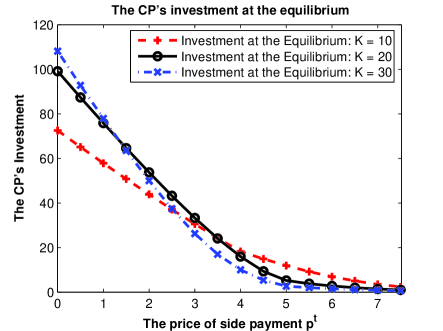

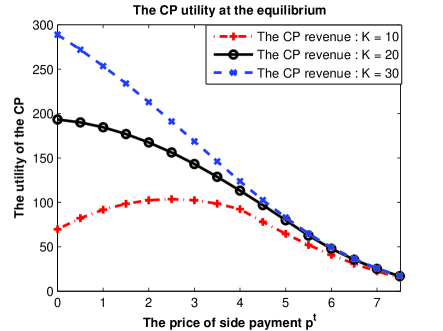

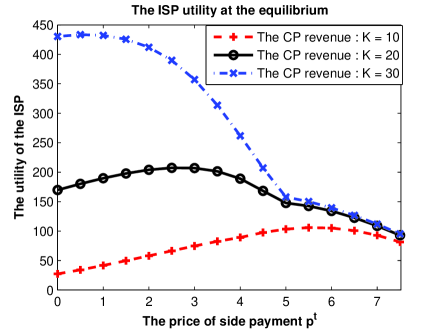

Advertisement Model: In the advertisement model, we consider the demand function . The coefficient reflects the efficiency of the CP’s investment to attract end users. The valuation of each click/browsing follows uniform distribution in the range [0, 10]. The total budget of advertisers is set to 1000. We conduct two sets of experiments. The first one is to evaluate the impact of side payment on the best strategies of the ISP and the CP. The second one is to find the optimal in the pre-bargaining game. In figure 4(a), the CP’s investment is a decreasing function of . When is large enough, reduces to 0. Figure 4(b) illustrates the utility of the CP when when and change. The CP’s utility increases first and then decreases with when increases. For the cases and , the increase of usually leads to the decrease of revenues. In figure 4(c), the utility of the ISP with and increases first and then decreases when grows. These curves present important insights on the interaction between the CP and the ISP. If the contents invested by the CP can bring a large demand, the side payment is not good for both the ISP and the CP. On the contrary, when the efficiency is small, the CP can obtain more utility by paying money to the ISP.

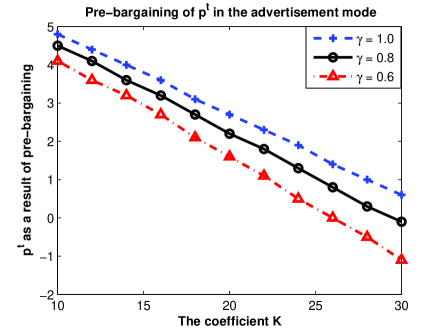

Figure 4(d) shows the relationship among , and in the pre-bargaining game. Different from the subscription model, depends on the bargaining power . One can observe that is a decreasing function of , and is negative when is large. This is to say, the ISP needs to pay money to the CP so that the CP can invest more on its contents. We also find that the optimal is a decreasing function of . This is because the ISP is less powerful in negotiating with the CP when decreases.

VI Related Work

There is one particular economic issue that is at the heart of the conflict over network neutrality. Hahn and Wallsten [1] write that net neutrality “usually means that broadband service providers charge consumers only once for Internet access, do not favor one content provider over another, and do not charge content providers for sending information over broadband lines to end users.”

This motivates us to study [3] the implications of being non-neutral and of charging the content providers. Using non-cooperative game theoretic tools, we showed that if one ISP has the power to impose payments on CPs, not only the end users suffer, but also the ISP’s performance degrades. More precisely, we show that the only possible equilibrium (characterized by prices) induces zero demand from the users. This phenomenon does not occur if the price that the CP is requested to pay to the ISP is fixed by some regulators. In [4] we focus on mechanisms based on the Nash bargaining (also known as proportional fairness [12]) paradigm (which is known in the network engineering context as the proportional fair assignment). It is the unique way of transferring utilities that satisfies a well known set of four axioms [13] related to fairness. We use a weighted version of this concept that takes into account the fact that one player may have more weights than the other one in deciding the amount of side payment. It is introduced in the context of network neutrality by [6]. She analyzes the investment of a CP to duopoly ISPs for better quality of service. The bargaining powers of the CP and the ISPs have been shown to be a knob of investment policies. In [14], we explore the effects of content-specific (i.e. not application neutral) pricing, including multiple CPs providing different types of content. Also, we consider competition among multiple providers of the same type and includes different models with consumer stickiness (or loyalty).

Some other recent work includes [15, 5, 7, 2, 17, 16]. Authors in [15] employ the theory of product-line restriction and find that network neutrality potentially harms the welfare of small CPs. Economides et. al. in [5], on the contrary, find that regulated network neutrality has a better welfare than the two-sided pricing (i.e. pricing both CPs and end users). This contradictory conclusion is drawn on the assumption that CPs’ contents are homogeneous. In [7], the authors study the effects of service discrimination on investment incentives for the ISPs and the CPs, and their implications for social welfare. They show that net neutrality might not necessarily prohibit the investment of the ISPs, and the discriminatory regime may weaken the investment incentive of the CPs. [2] compares one-sided and two-sided pricing of the ISPs in a network where the joint investments of the CPs and the ISPs bring revenue from advertisers to the CPs. Other references that explored the fact that the consumer pays two entities for one good (for accessing contents through the Internet) are [17, 16]. They study the impact of this competition on the users as well as on the level of investment in the infrastructure.

The side payment from the CP to the ISP is expected to be financed by the income from the users and publicity. Cooperative games is a well established scientific area that provides us with tools for designing such mechanisms which, moreover, possess some fairness properties. In [8, 9] the Shapley value (which is known to have some fairness properties [18]) has been used for deciding how revenues from users should be split between the service and the content providers.

VII Conclusion and Future Work

In this paper, we have studied the two-sided ISP pricing in a non-neutral market composed of one ISP, one CP, a number of advisers and end users. We first answer under what situations the side payment charged by the ISP is beneficial for the ISP (or the CP). Then, we study how the price of side payment is determined. Different from existing work, our models take account of three important features, the relative price sensitivity, the revenue models, and the QoS provided by the ISP. These new features give rise to quite different results, enabling us to understand the two-sided pricing comprehensively. With the subscription model, the relative price sensitivity determines whether the ISP should charge the side payment from the CP or not. With the advertisement model, the charge of side payment depends on the ability of the CP’s investment to attract the demand. Our work also has a couple of potential limitations. For instance, the usage based pricing is usually adopted by wireless ISPs, but not the wireline ISPs that use the xDSL technology. Sometimes, the CPs might obtain revenue from both end users and the advertisers, which is not considered here. Our future work would address these limitations.

References

- [1] R. Hahn and S. Wallsten, “The economics of net neutrality,” The Berkeley Economic Press Economists’ Voice, Vol.3, No.6, 2006, pp:1-7.

- [2] J. Musacchio, G. Schwartz and J. Walrand, “A two-sided market analysis of provider investment incentives with an application to the net-neutrality issue”, Review of Network Economics, 8(1), 2009.

- [3] E. Altman, P. Bernhard, S. Caron, G. Kesidis, J. Rojas-Mora and S.L. Wong. ”A Study of Non-Neutral Networks with Usage-based Prices”, 3rd ETM Workshop of ITC conference, 2010.

- [4] E. Altman, M.K. Hanawal and R. Sundaresan, ”Nonneutral network and the role of bargaining power in side payments”, NetCoop, Ghent, Belgium, Nov. 2010.

- [5] N. Economides and J. Tag, “Net neutrality on the internet: A two-sided market analysis”, working paper. Available at http://ideas.repec.org/p/net/wpaper/0714.html

- [6] V. Claudia Saavedra “Bargaining power and the net neutrality debate”, working paper, 2010. Available at http://sites.google.com/site/claudiasaavedra/

- [7] J.P. Choi and B.C. Kim, “Net Neutrality and Investment Incentives”, working paper, 2008 http://ideas.repec.org/p/ces/ceswps/_2390.html

- [8] T.B. Ma, D.M. Chiu, J.C.S. Lui et.al, “On Cooperative Settlement Between Content, Transit and Eyeball Internet Service Providers”, to appear in IEEE/ACM Trans. on Networking.

- [9] T.B. Ma, D.M. Chiu, J.C.S. Lui et.al, “Internet Economics: The use of Shapley value for ISP settlement”, IEEE/ACM Trans. on Networking, Vol.18, No.3, 2010.

- [10] R. El-Azouzi, E. Altman and L. Wynter, “Telecommunications Network Equilibrium with Price and Quality-of-Service Characteristics”, in Proc. of ITC, 2003.

- [11] J. Liu, D.M. Chiu, “Mathematical Modeling of Competition in Sponsored Search Market”, in ACM Workshop on NetEcon’10, Vancouver, 2010.

- [12] F.P. Kelly, A. Maulloo and D. Tan, “Rate control in communication networks: shadow prices, proportional fairness and stability,” J. Oper. Res. Society, Vol. 49, pp: 237-252, 1998.

- [13] J.F. Nash Jr, “The bargaining problem,” Econometrica, Vol 18, pp: 155-162, 1950.

- [14] S. Caron, G. Kesidis and E. Altman, “Application neutrality and a paradox of side payments”, The 3rd Workshop on Re-Architecting the Internet (ReArch 2010), Philadelphia, collocated with ACM CoNEXT.

- [15] B.E. Hermalin and M.L. Katz, “The economics of product-line restrictions with applications to the network neutrality debate”. Information Economics and Policy Vol.19, pp. 215-248, 2007.

- [16] H.K. Cheng, S. Bandyopadyay and H. Guo, ”The debate on Net Neutrality: A policy Perspective”, Information Systems Research, March, 2010.

- [17] P. Njoroge, A. Ozdagler, N. Stier-Moses, G. Weintraub, “Investment in two-sided markets and the net-neutrality debate,” Decision, Risk, and Operations Working Papers Series, DRO-2010-05, Columbia Business School, July 2010.

- [18] E. Winter, “The Shapley value,” Chapter 53 in The Handbook of Game Theory, Vol. 3. R.J.Aumann and S.Hart, North-Holland, 2002.